Recording Business Transaction: Analysis of Income Statements and Financial Position

VerifiedAdded on 2022/12/27

|16

|2803

|24

AI Summary

This document discusses the process of recording business transactions, including writing double entry records in T-accounts and determining opening balances. It also covers the preparation of trial balance, analysis of income statements, and evaluation of financial position. Additionally, it explains the concept of drawings in small businesses and provides calculations for financial ratios. The document is relevant for students studying accounting or finance.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Recording business

transaction

transaction

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

a. Writing down double entry record transaction in T- accounts.................................................3

b. Determining the accounts and bring down an opening balance account.................................5

c. Prepare Trial balance as at 31st October 2020.........................................................................8

d. Analysing Income statements for the period ended 31st October 2020..................................9

e. Evaluating statements of financial position as at 31st October 2020.....................................10

f. Letter to Linda explaining what drawings are concerning small business and answering her

query about holiday....................................................................................................................11

PART B..........................................................................................................................................11

Calculation of ratio....................................................................................................................11

Linda' s competitors ratio average were as follows: Analysing performance to each of the

ratios calculated with the comparison of her competitors.........................................................12

CONCLUSION..............................................................................................................................13

REFERENCES................................................................................................................................1

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

a. Writing down double entry record transaction in T- accounts.................................................3

b. Determining the accounts and bring down an opening balance account.................................5

c. Prepare Trial balance as at 31st October 2020.........................................................................8

d. Analysing Income statements for the period ended 31st October 2020..................................9

e. Evaluating statements of financial position as at 31st October 2020.....................................10

f. Letter to Linda explaining what drawings are concerning small business and answering her

query about holiday....................................................................................................................11

PART B..........................................................................................................................................11

Calculation of ratio....................................................................................................................11

Linda' s competitors ratio average were as follows: Analysing performance to each of the

ratios calculated with the comparison of her competitors.........................................................12

CONCLUSION..............................................................................................................................13

REFERENCES................................................................................................................................1

INTRODUCTION

Recording business transaction refers to the part of process that is part of accounting

process using accounting books and other transaction books and need to be recorded timely and

accurately (Chow and Schoenbaum, 2020). All the transaction were need in monetary terms and

based on double entry accounting system in which every transaction is recorded twice manner of

ledger. All the accounts are very different from each other and has different nature and

accordingly treated to record in journal and ledger entry. There is always been a perfect match

between two sides. In this report based on different business transaction and has to be identified

and will be need to evaluate systematically. All transaction are recorded in accounting books as

per the rules and along with prepare financial statements to determine position of performance.

Apart from proper calculation of financial ratios and their efficiency in monetary terms is being

compare of industry ratio.

PART A

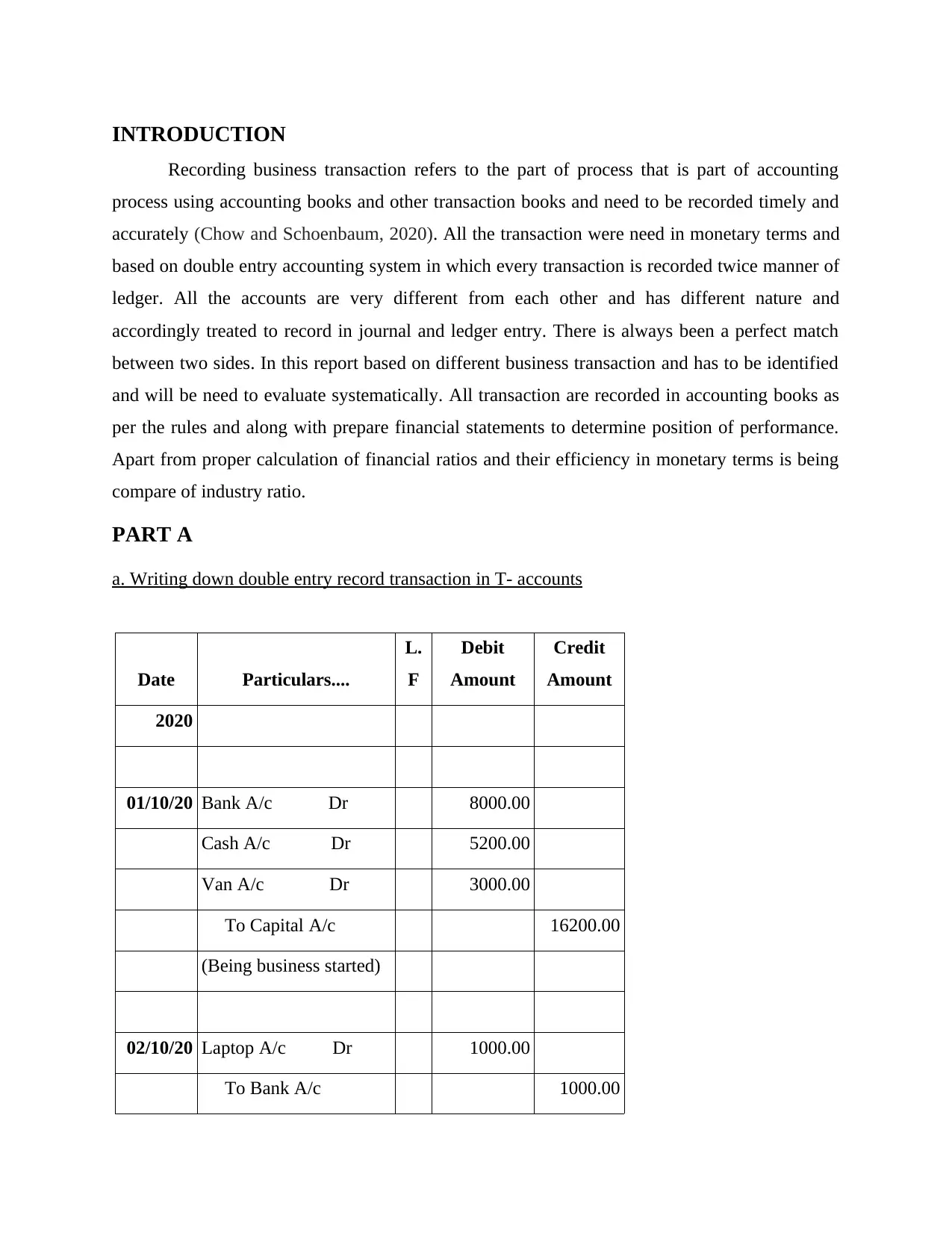

a. Writing down double entry record transaction in T- accounts

Date Particulars....

L.

F

Debit

Amount

Credit

Amount

2020

01/10/20 Bank A/c Dr 8000.00

Cash A/c Dr 5200.00

Van A/c Dr 3000.00

To Capital A/c 16200.00

(Being business started)

02/10/20 Laptop A/c Dr 1000.00

To Bank A/c 1000.00

Recording business transaction refers to the part of process that is part of accounting

process using accounting books and other transaction books and need to be recorded timely and

accurately (Chow and Schoenbaum, 2020). All the transaction were need in monetary terms and

based on double entry accounting system in which every transaction is recorded twice manner of

ledger. All the accounts are very different from each other and has different nature and

accordingly treated to record in journal and ledger entry. There is always been a perfect match

between two sides. In this report based on different business transaction and has to be identified

and will be need to evaluate systematically. All transaction are recorded in accounting books as

per the rules and along with prepare financial statements to determine position of performance.

Apart from proper calculation of financial ratios and their efficiency in monetary terms is being

compare of industry ratio.

PART A

a. Writing down double entry record transaction in T- accounts

Date Particulars....

L.

F

Debit

Amount

Credit

Amount

2020

01/10/20 Bank A/c Dr 8000.00

Cash A/c Dr 5200.00

Van A/c Dr 3000.00

To Capital A/c 16200.00

(Being business started)

02/10/20 Laptop A/c Dr 1000.00

To Bank A/c 1000.00

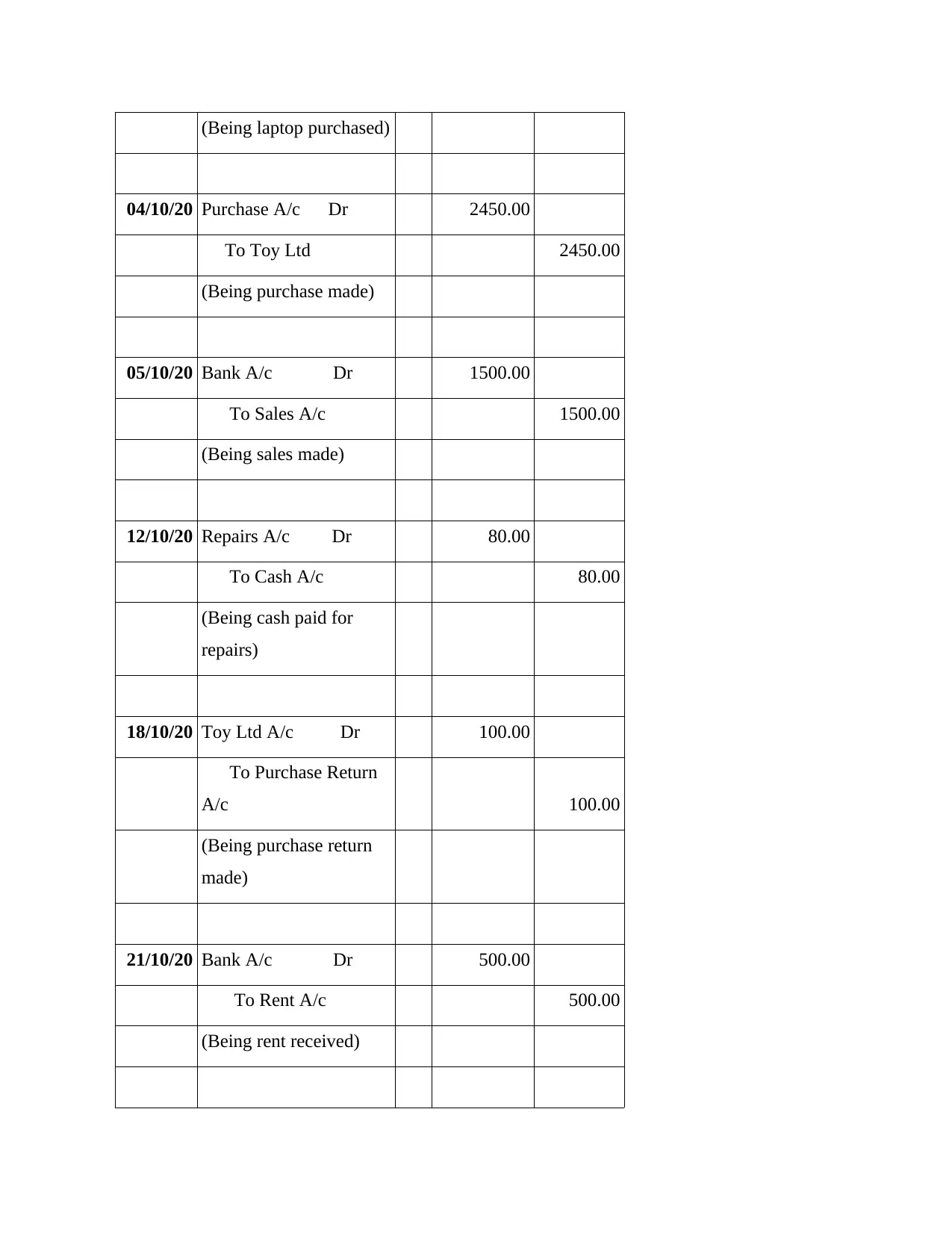

(Being laptop purchased)

04/10/20 Purchase A/c Dr 2450.00

To Toy Ltd 2450.00

(Being purchase made)

05/10/20 Bank A/c Dr 1500.00

To Sales A/c 1500.00

(Being sales made)

12/10/20 Repairs A/c Dr 80.00

To Cash A/c 80.00

(Being cash paid for

repairs)

18/10/20 Toy Ltd A/c Dr 100.00

To Purchase Return

A/c 100.00

(Being purchase return

made)

21/10/20 Bank A/c Dr 500.00

To Rent A/c 500.00

(Being rent received)

04/10/20 Purchase A/c Dr 2450.00

To Toy Ltd 2450.00

(Being purchase made)

05/10/20 Bank A/c Dr 1500.00

To Sales A/c 1500.00

(Being sales made)

12/10/20 Repairs A/c Dr 80.00

To Cash A/c 80.00

(Being cash paid for

repairs)

18/10/20 Toy Ltd A/c Dr 100.00

To Purchase Return

A/c 100.00

(Being purchase return

made)

21/10/20 Bank A/c Dr 500.00

To Rent A/c 500.00

(Being rent received)

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

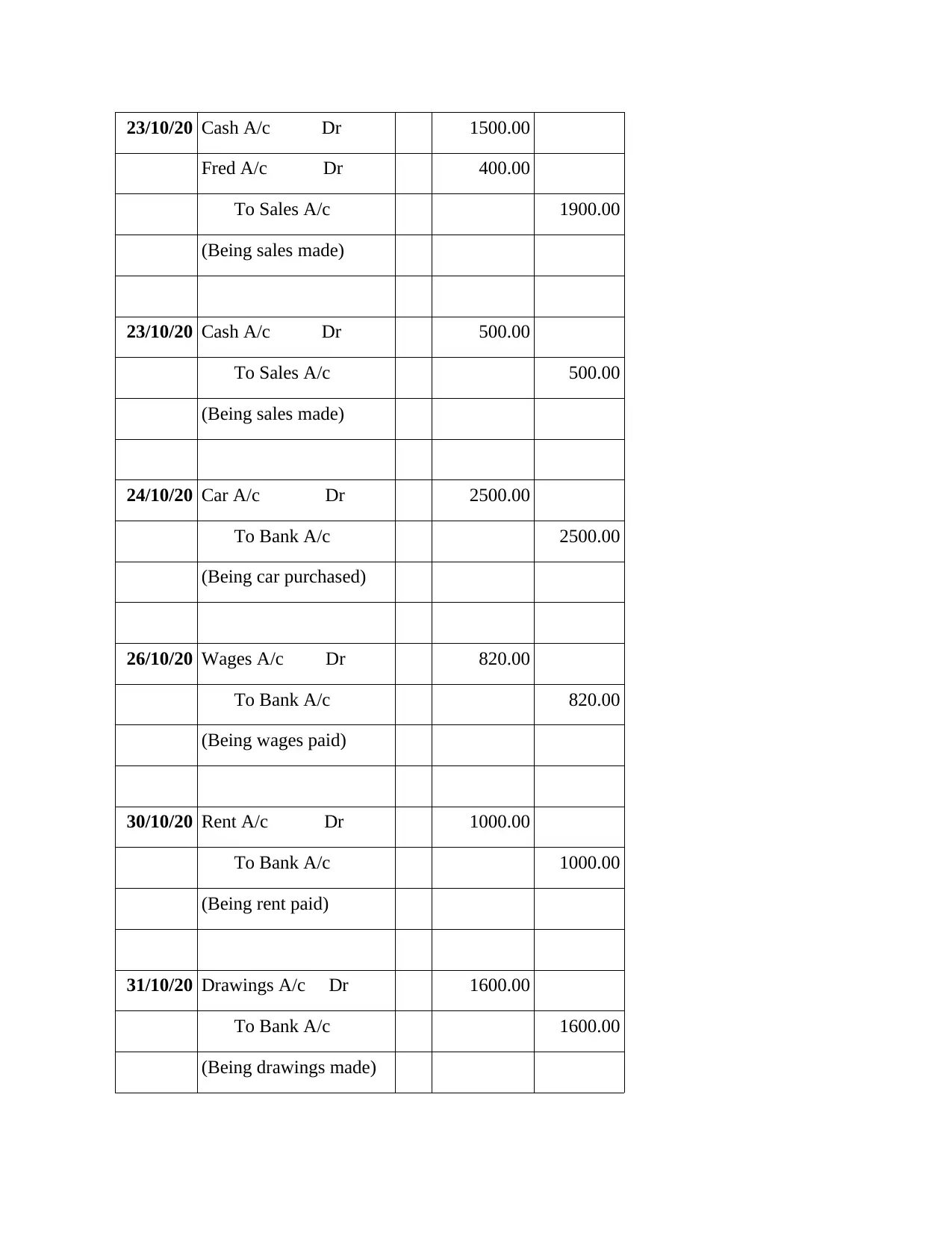

23/10/20 Cash A/c Dr 1500.00

Fred A/c Dr 400.00

To Sales A/c 1900.00

(Being sales made)

23/10/20 Cash A/c Dr 500.00

To Sales A/c 500.00

(Being sales made)

24/10/20 Car A/c Dr 2500.00

To Bank A/c 2500.00

(Being car purchased)

26/10/20 Wages A/c Dr 820.00

To Bank A/c 820.00

(Being wages paid)

30/10/20 Rent A/c Dr 1000.00

To Bank A/c 1000.00

(Being rent paid)

31/10/20 Drawings A/c Dr 1600.00

To Bank A/c 1600.00

(Being drawings made)

Fred A/c Dr 400.00

To Sales A/c 1900.00

(Being sales made)

23/10/20 Cash A/c Dr 500.00

To Sales A/c 500.00

(Being sales made)

24/10/20 Car A/c Dr 2500.00

To Bank A/c 2500.00

(Being car purchased)

26/10/20 Wages A/c Dr 820.00

To Bank A/c 820.00

(Being wages paid)

30/10/20 Rent A/c Dr 1000.00

To Bank A/c 1000.00

(Being rent paid)

31/10/20 Drawings A/c Dr 1600.00

To Bank A/c 1600.00

(Being drawings made)

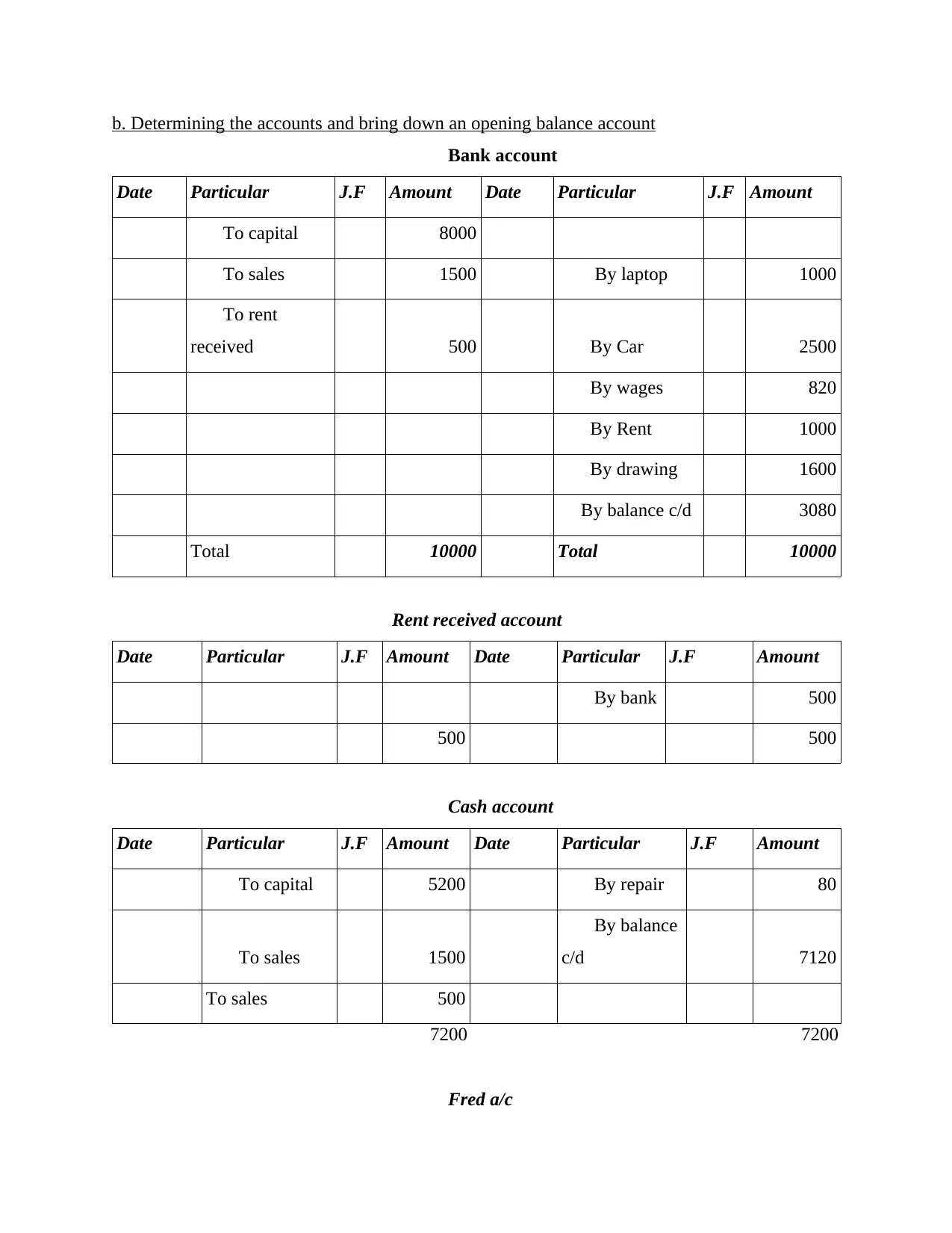

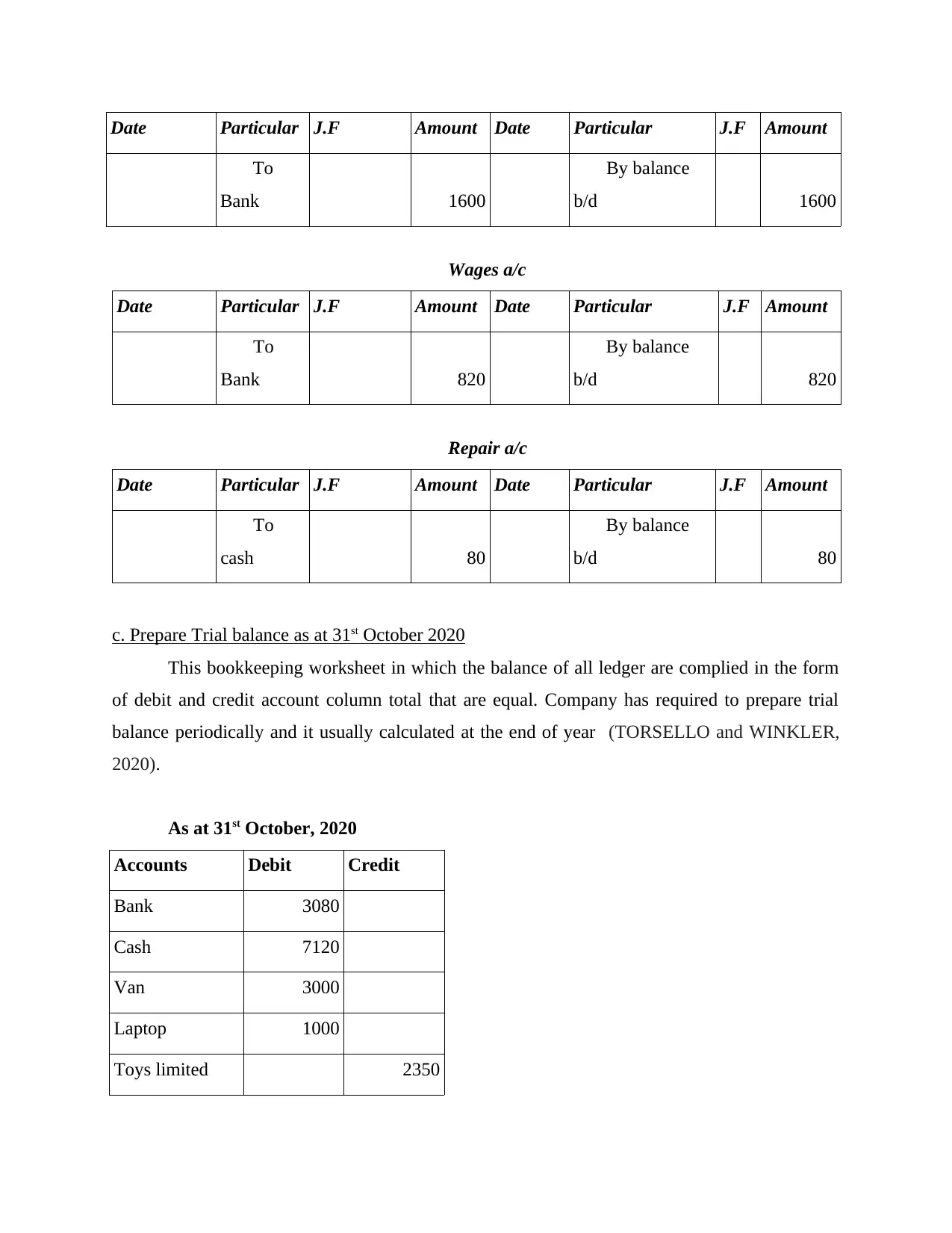

b. Determining the accounts and bring down an opening balance account

Bank account

Date Particular J.F Amount Date Particular J.F Amount

…...To capital 8000

…...To sales 1500 …....By laptop 1000

…...To rent

received 500 …...By Car 2500

…...By wages 820

…...By Rent 1000

…...By drawing 1600

….By balance c/d 3080

Total 10000 Total 10000

Rent received account

Date Particular J.F Amount Date Particular J.F Amount

…...By bank 500

500 500

Cash account

Date Particular J.F Amount Date Particular J.F Amount

…...To capital 5200 …...By repair 80

…...To sales 1500

…...By balance

c/d 7120

To sales 500

7200 7200

Fred a/c

Bank account

Date Particular J.F Amount Date Particular J.F Amount

…...To capital 8000

…...To sales 1500 …....By laptop 1000

…...To rent

received 500 …...By Car 2500

…...By wages 820

…...By Rent 1000

…...By drawing 1600

….By balance c/d 3080

Total 10000 Total 10000

Rent received account

Date Particular J.F Amount Date Particular J.F Amount

…...By bank 500

500 500

Cash account

Date Particular J.F Amount Date Particular J.F Amount

…...To capital 5200 …...By repair 80

…...To sales 1500

…...By balance

c/d 7120

To sales 500

7200 7200

Fred a/c

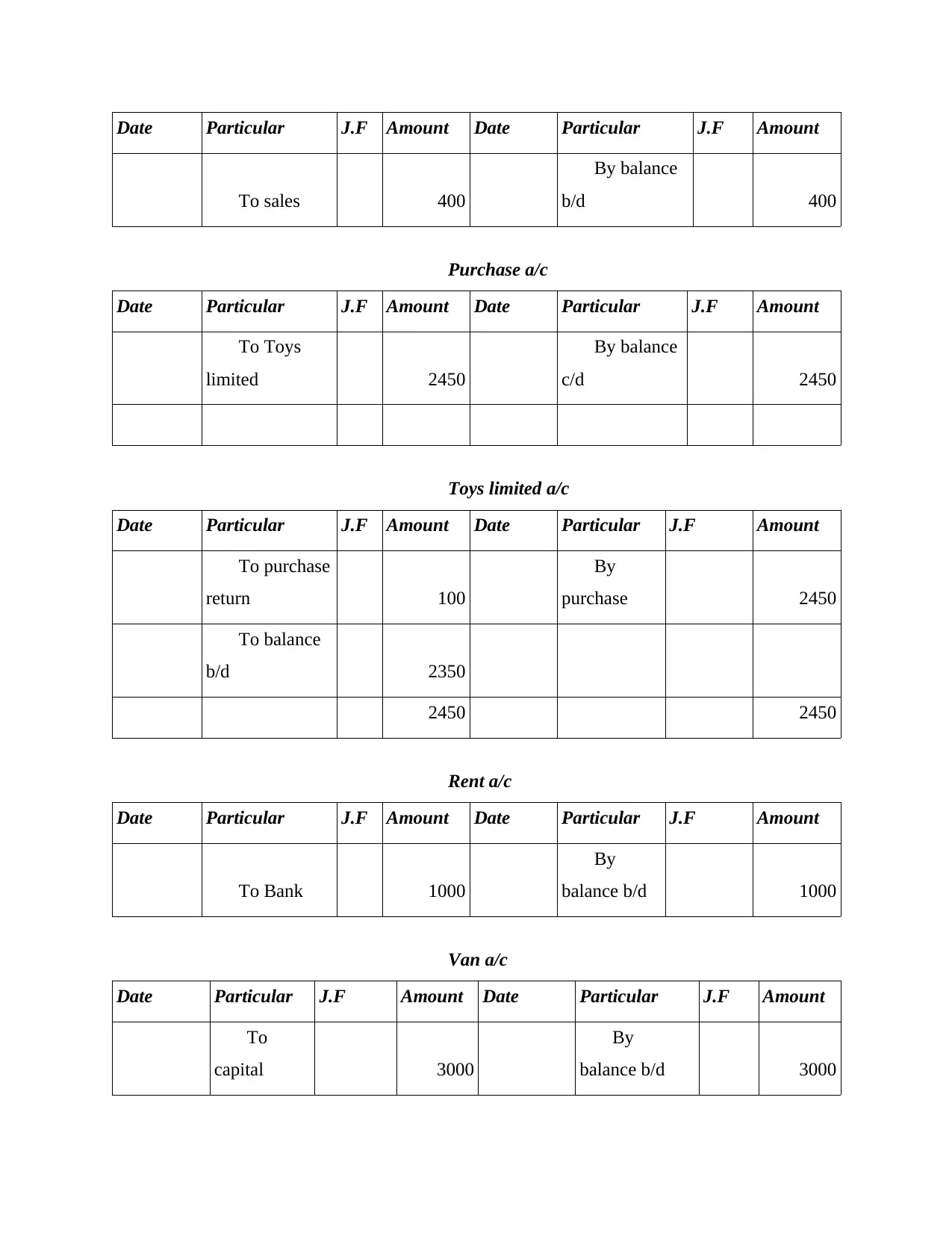

Date Particular J.F Amount Date Particular J.F Amount

…...To sales 400

…...By balance

b/d 400

Purchase a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To Toys

limited 2450

…...By balance

c/d 2450

Toys limited a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To purchase

return 100

…...By

purchase 2450

…...To balance

b/d 2350

2450 2450

Rent a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To Bank 1000

…...By

balance b/d 1000

Van a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To

capital 3000

…...By

balance b/d 3000

…...To sales 400

…...By balance

b/d 400

Purchase a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To Toys

limited 2450

…...By balance

c/d 2450

Toys limited a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To purchase

return 100

…...By

purchase 2450

…...To balance

b/d 2350

2450 2450

Rent a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To Bank 1000

…...By

balance b/d 1000

Van a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To

capital 3000

…...By

balance b/d 3000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

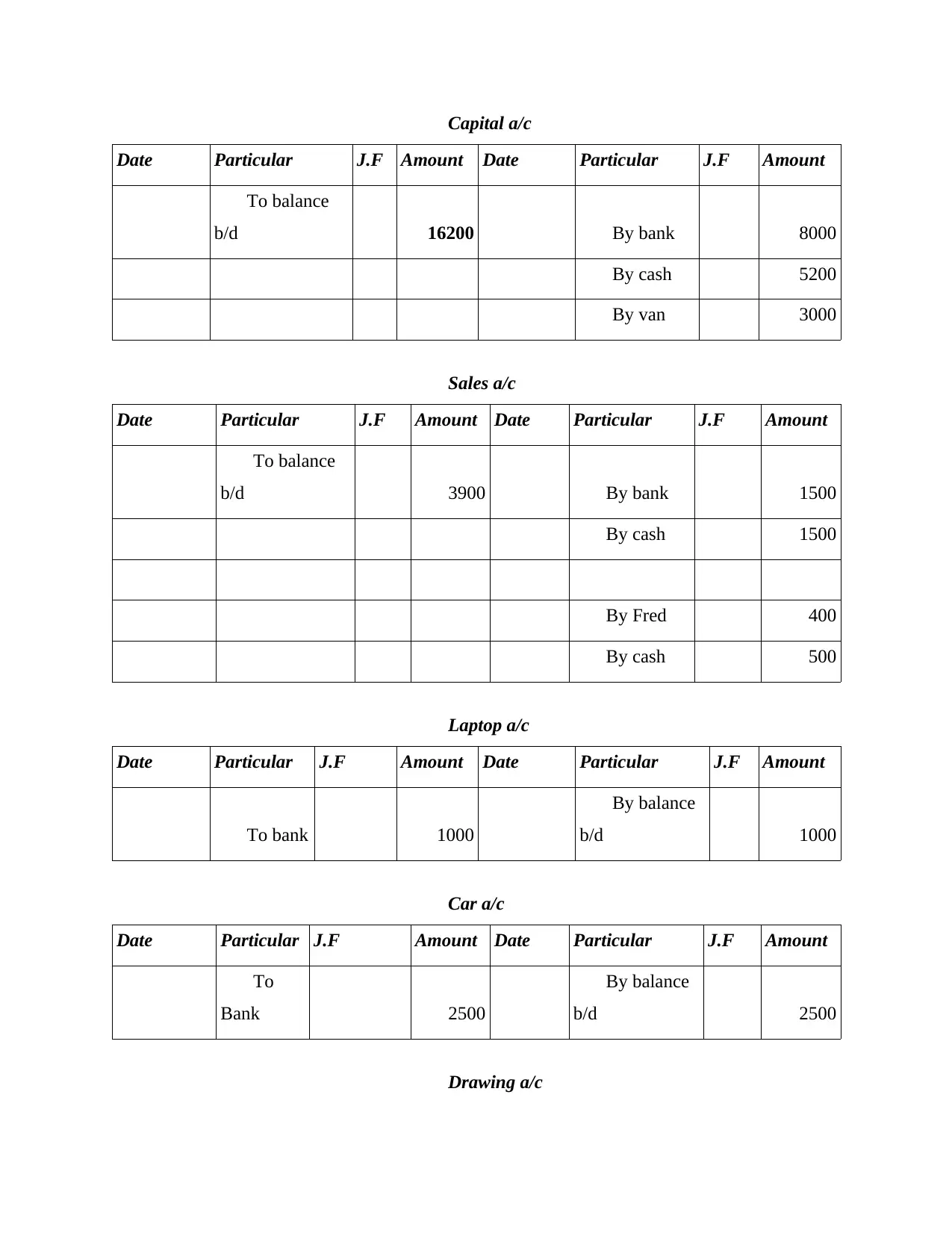

Capital a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To balance

b/d 16200 …...By bank 8000

…...By cash 5200

…...By van 3000

Sales a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To balance

b/d 3900 …...By bank 1500

…...By cash 1500

…...By Fred 400

…...By cash 500

Laptop a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To bank 1000

…...By balance

b/d 1000

Car a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To

Bank 2500

…...By balance

b/d 2500

Drawing a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To balance

b/d 16200 …...By bank 8000

…...By cash 5200

…...By van 3000

Sales a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To balance

b/d 3900 …...By bank 1500

…...By cash 1500

…...By Fred 400

…...By cash 500

Laptop a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To bank 1000

…...By balance

b/d 1000

Car a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To

Bank 2500

…...By balance

b/d 2500

Drawing a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To

Bank 1600

…...By balance

b/d 1600

Wages a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To

Bank 820

…...By balance

b/d 820

Repair a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To

cash 80

…...By balance

b/d 80

c. Prepare Trial balance as at 31st October 2020

This bookkeeping worksheet in which the balance of all ledger are complied in the form

of debit and credit account column total that are equal. Company has required to prepare trial

balance periodically and it usually calculated at the end of year (TORSELLO and WINKLER,

2020).

As at 31st October, 2020

Accounts Debit Credit

Bank 3080

Cash 7120

Van 3000

Laptop 1000

Toys limited 2350

…...To

Bank 1600

…...By balance

b/d 1600

Wages a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To

Bank 820

…...By balance

b/d 820

Repair a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To

cash 80

…...By balance

b/d 80

c. Prepare Trial balance as at 31st October 2020

This bookkeeping worksheet in which the balance of all ledger are complied in the form

of debit and credit account column total that are equal. Company has required to prepare trial

balance periodically and it usually calculated at the end of year (TORSELLO and WINKLER,

2020).

As at 31st October, 2020

Accounts Debit Credit

Bank 3080

Cash 7120

Van 3000

Laptop 1000

Toys limited 2350

Purchase 2450

Purchase return 100

Sales 3900

Rent received 500

Rent paid 1000

Wages 820

Drawing 1600

Capital 16200

Repairing

account 80

Fred account 400

Car account 2500

Total 22550 22550

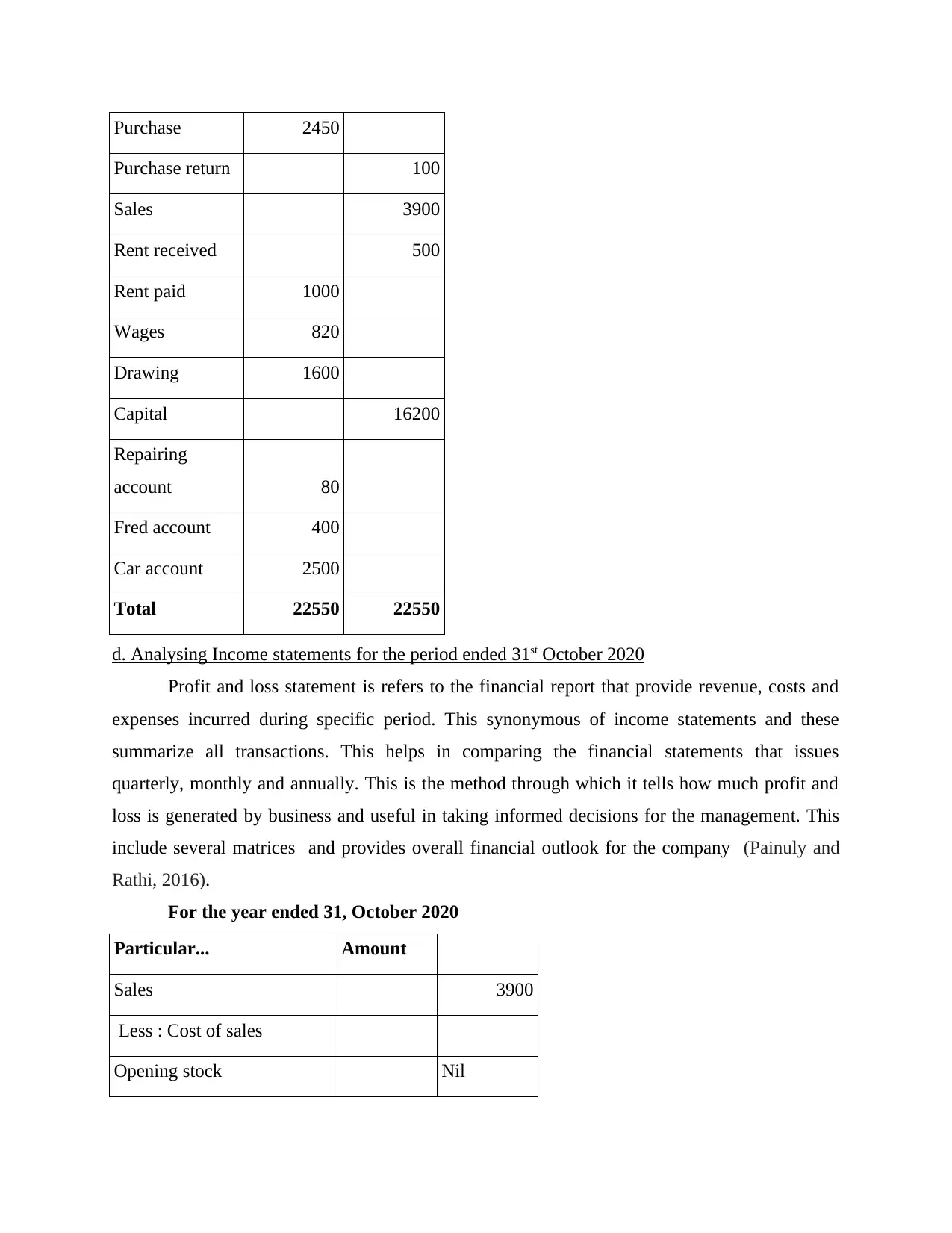

d. Analysing Income statements for the period ended 31st October 2020

Profit and loss statement is refers to the financial report that provide revenue, costs and

expenses incurred during specific period. This synonymous of income statements and these

summarize all transactions. This helps in comparing the financial statements that issues

quarterly, monthly and annually. This is the method through which it tells how much profit and

loss is generated by business and useful in taking informed decisions for the management. This

include several matrices and provides overall financial outlook for the company (Painuly and

Rathi, 2016).

For the year ended 31, October 2020

Particular... Amount

Sales 3900

Less : Cost of sales

Opening stock Nil

Purchase return 100

Sales 3900

Rent received 500

Rent paid 1000

Wages 820

Drawing 1600

Capital 16200

Repairing

account 80

Fred account 400

Car account 2500

Total 22550 22550

d. Analysing Income statements for the period ended 31st October 2020

Profit and loss statement is refers to the financial report that provide revenue, costs and

expenses incurred during specific period. This synonymous of income statements and these

summarize all transactions. This helps in comparing the financial statements that issues

quarterly, monthly and annually. This is the method through which it tells how much profit and

loss is generated by business and useful in taking informed decisions for the management. This

include several matrices and provides overall financial outlook for the company (Painuly and

Rathi, 2016).

For the year ended 31, October 2020

Particular... Amount

Sales 3900

Less : Cost of sales

Opening stock Nil

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Purchase 2450

Less: Purchase return 100

Less: Closing stock 250

Gross revenue 1800

Less: Operating expenses

Expenses on repairing 80

Wages 820

Rent paid 1000 1900

Add: Operating income

Rent received 500

Net profit 400

e. Evaluating statements of financial position as at 31st October 2020

This is very important part of business which is utilised by business to present financial

capabilities in financial year. Balance year supports business analyst and stakeholders to

determine overall financial position of organisation and ability to pay the operation activities and

functions (Ekici and Ekici, 2019). It involves details of past years in order to compare with other

company and this data supports the company to improve their performance by reviewing the

financial statements and make it easy for the firm to enhance their financial performance. Their

need of balancing the all transactions from asset and liabilities side is essential to prepare the

further process in accounting.

As at December, 31, October 2020

Particulars... Amount Total

Fixed assets

.Car 2500

Van 3000

.Laptop 1000 6500

Less: Purchase return 100

Less: Closing stock 250

Gross revenue 1800

Less: Operating expenses

Expenses on repairing 80

Wages 820

Rent paid 1000 1900

Add: Operating income

Rent received 500

Net profit 400

e. Evaluating statements of financial position as at 31st October 2020

This is very important part of business which is utilised by business to present financial

capabilities in financial year. Balance year supports business analyst and stakeholders to

determine overall financial position of organisation and ability to pay the operation activities and

functions (Ekici and Ekici, 2019). It involves details of past years in order to compare with other

company and this data supports the company to improve their performance by reviewing the

financial statements and make it easy for the firm to enhance their financial performance. Their

need of balancing the all transactions from asset and liabilities side is essential to prepare the

further process in accounting.

As at December, 31, October 2020

Particulars... Amount Total

Fixed assets

.Car 2500

Van 3000

.Laptop 1000 6500

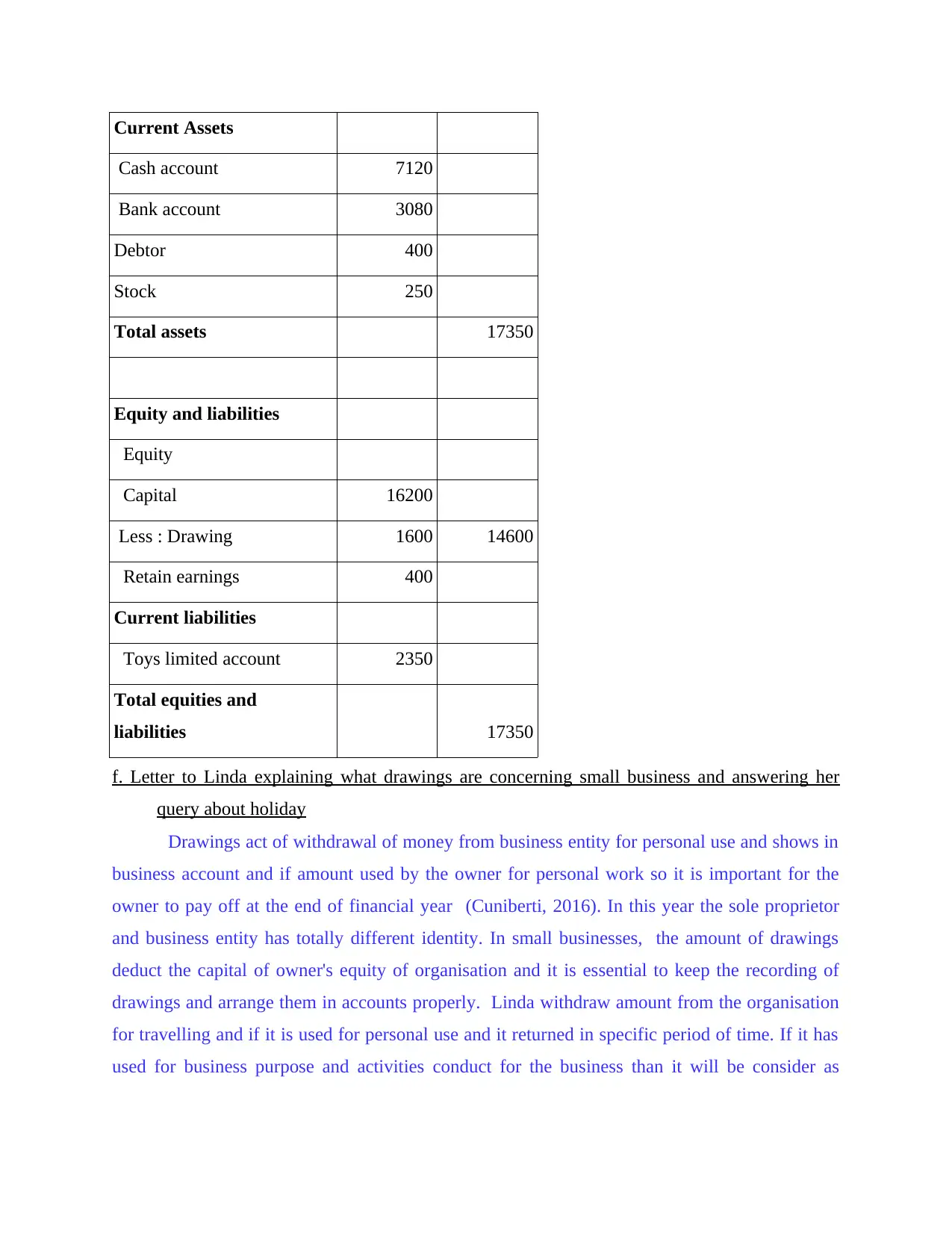

Current Assets

.Cash account 7120

.Bank account 3080

Debtor 400

Stock 250

Total assets 17350

Equity and liabilities

..Equity

..Capital 16200

.Less : Drawing 1600 14600

..Retain earnings 400

Current liabilities

..Toys limited account 2350

Total equities and

liabilities 17350

f. Letter to Linda explaining what drawings are concerning small business and answering her

query about holiday

Drawings act of withdrawal of money from business entity for personal use and shows in

business account and if amount used by the owner for personal work so it is important for the

owner to pay off at the end of financial year (Cuniberti, 2016). In this year the sole proprietor

and business entity has totally different identity. In small businesses, the amount of drawings

deduct the capital of owner's equity of organisation and it is essential to keep the recording of

drawings and arrange them in accounts properly. Linda withdraw amount from the organisation

for travelling and if it is used for personal use and it returned in specific period of time. If it has

used for business purpose and activities conduct for the business than it will be consider as

.Cash account 7120

.Bank account 3080

Debtor 400

Stock 250

Total assets 17350

Equity and liabilities

..Equity

..Capital 16200

.Less : Drawing 1600 14600

..Retain earnings 400

Current liabilities

..Toys limited account 2350

Total equities and

liabilities 17350

f. Letter to Linda explaining what drawings are concerning small business and answering her

query about holiday

Drawings act of withdrawal of money from business entity for personal use and shows in

business account and if amount used by the owner for personal work so it is important for the

owner to pay off at the end of financial year (Cuniberti, 2016). In this year the sole proprietor

and business entity has totally different identity. In small businesses, the amount of drawings

deduct the capital of owner's equity of organisation and it is essential to keep the recording of

drawings and arrange them in accounts properly. Linda withdraw amount from the organisation

for travelling and if it is used for personal use and it returned in specific period of time. If it has

used for business purpose and activities conduct for the business than it will be consider as

travelling expenditure in the income statements at side of debit side. If drawings were made than

it will impact on debit and credit side and accordingly treated in books.

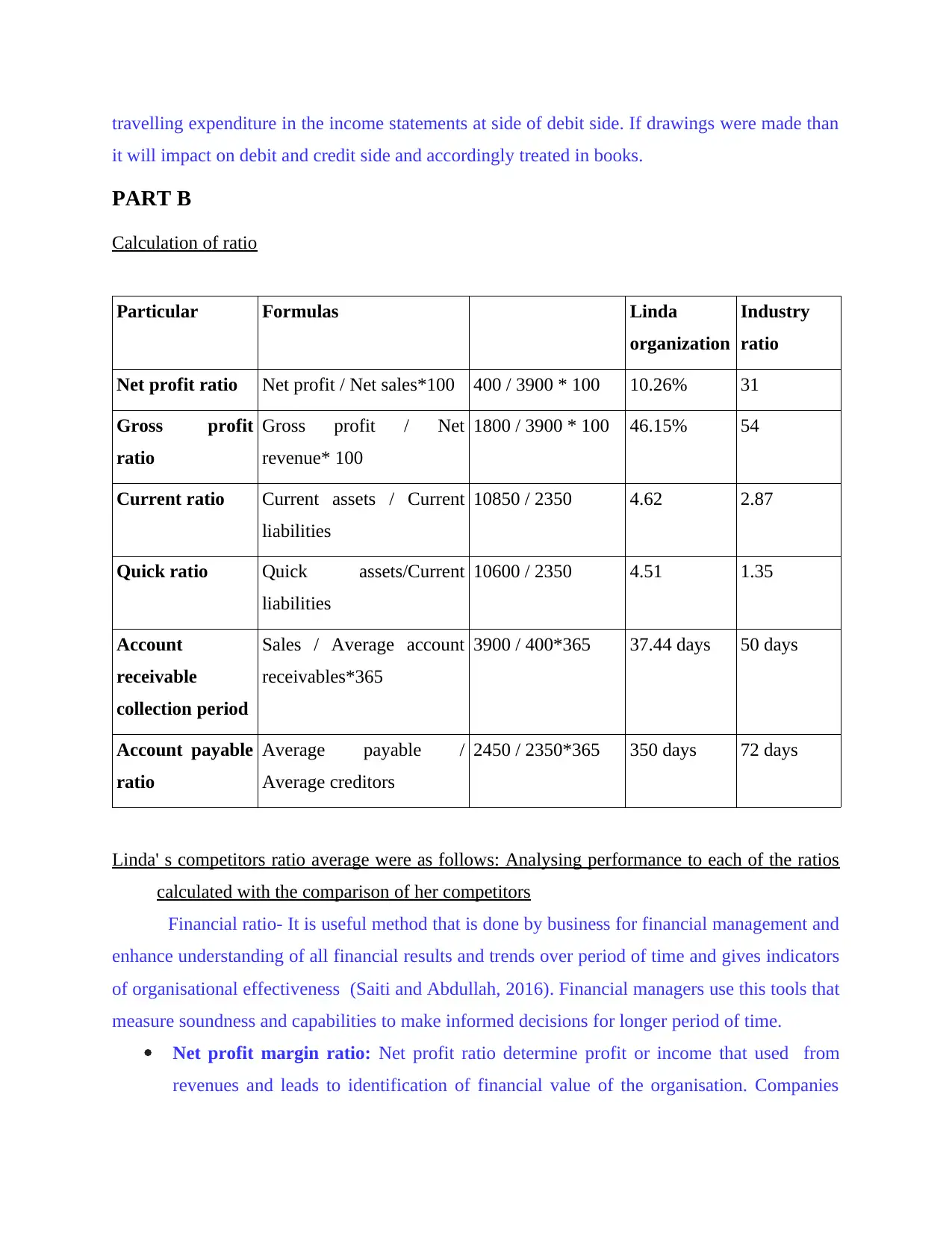

PART B

Calculation of ratio

Particular Formulas Linda

organization

Industry

ratio

Net profit ratio Net profit / Net sales*100 400 / 3900 * 100 10.26% 31

Gross profit

ratio

Gross profit / Net

revenue* 100

1800 / 3900 * 100 46.15% 54

Current ratio Current assets / Current

liabilities

10850 / 2350 4.62 2.87

Quick ratio Quick assets/Current

liabilities

10600 / 2350 4.51 1.35

Account

receivable

collection period

Sales / Average account

receivables*365

3900 / 400*365 37.44 days 50 days

Account payable

ratio

Average payable /

Average creditors

2450 / 2350*365 350 days 72 days

Linda' s competitors ratio average were as follows: Analysing performance to each of the ratios

calculated with the comparison of her competitors

Financial ratio- It is useful method that is done by business for financial management and

enhance understanding of all financial results and trends over period of time and gives indicators

of organisational effectiveness (Saiti and Abdullah, 2016). Financial managers use this tools that

measure soundness and capabilities to make informed decisions for longer period of time.

Net profit margin ratio: Net profit ratio determine profit or income that used from

revenues and leads to identification of financial value of the organisation. Companies

it will impact on debit and credit side and accordingly treated in books.

PART B

Calculation of ratio

Particular Formulas Linda

organization

Industry

ratio

Net profit ratio Net profit / Net sales*100 400 / 3900 * 100 10.26% 31

Gross profit

ratio

Gross profit / Net

revenue* 100

1800 / 3900 * 100 46.15% 54

Current ratio Current assets / Current

liabilities

10850 / 2350 4.62 2.87

Quick ratio Quick assets/Current

liabilities

10600 / 2350 4.51 1.35

Account

receivable

collection period

Sales / Average account

receivables*365

3900 / 400*365 37.44 days 50 days

Account payable

ratio

Average payable /

Average creditors

2450 / 2350*365 350 days 72 days

Linda' s competitors ratio average were as follows: Analysing performance to each of the ratios

calculated with the comparison of her competitors

Financial ratio- It is useful method that is done by business for financial management and

enhance understanding of all financial results and trends over period of time and gives indicators

of organisational effectiveness (Saiti and Abdullah, 2016). Financial managers use this tools that

measure soundness and capabilities to make informed decisions for longer period of time.

Net profit margin ratio: Net profit ratio determine profit or income that used from

revenues and leads to identification of financial value of the organisation. Companies

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

can use this ratio to can increase the efficiency and helps in taking decision making

process. Organisation has to consider transaction that brings certain strategies from that

we can analyse them to improve the activities and functions so that it improve the

efficiency (Pushpa, 2016). As per the calculation, it determined that net profit of Linda

business that 10.26% and industry ratio is 31%. In comparison, it is evaluated that

company is not performing better than industries.

Gross profit ratio- This ratio helps in maintaining the relationship between gross profit

and net sales. This helps the companies to take measurable actions about future strategies

and operation after assessing the ratio of organisation and accordingly frame whole

process. The industry has greater gross profit as compared to the Linda business which is

54% and it is being important for the company to foster revenue and reduces the cosy of

sales.

Current ratio- This ratio reflects the ability of organisation to generate the revenue to

overcome the expenses or debts which are due to company (Ilayperuma and Zdravkovic,

2020). This deals with short-term period and that determine their obligations to pay off

debts within one year. It shows the liquidity of company and capacity to pay short term

obligations and this computation it reflects that Linda has too much liquidity 4:62 that is

not good for organisation as they need to generate with nearest ideal ratio that is 2:1.

Quick ratio- This states that if company can pay short term debts from liquid assets. It

measure that how efficiently company able to pay current liabilities. This reflect the

financial security of company and useful for creditors and investor in terms of risk

evaluations as they want to invest in risk free company. The ideal ratio of quick ratio is

1:1. As per the calculation it is evaluated that Linda has 4:61 which is shows excess in

liquidity as compare to industry ratio is 1:89 (Wu, and et.al., 2016).

Accounts receivable ratio- It is important for the debtors turnover ratio and part of

efficiency ratio and used to measure business collective manner and determine that how

effectively they manage their clients by analysing the outstanding debt in accounting

period and will help the organisation in strengthen their system. In the calculation, Linda

business provides time 37.44 days for collection of amount and industry gives 50 days

for the collections.

process. Organisation has to consider transaction that brings certain strategies from that

we can analyse them to improve the activities and functions so that it improve the

efficiency (Pushpa, 2016). As per the calculation, it determined that net profit of Linda

business that 10.26% and industry ratio is 31%. In comparison, it is evaluated that

company is not performing better than industries.

Gross profit ratio- This ratio helps in maintaining the relationship between gross profit

and net sales. This helps the companies to take measurable actions about future strategies

and operation after assessing the ratio of organisation and accordingly frame whole

process. The industry has greater gross profit as compared to the Linda business which is

54% and it is being important for the company to foster revenue and reduces the cosy of

sales.

Current ratio- This ratio reflects the ability of organisation to generate the revenue to

overcome the expenses or debts which are due to company (Ilayperuma and Zdravkovic,

2020). This deals with short-term period and that determine their obligations to pay off

debts within one year. It shows the liquidity of company and capacity to pay short term

obligations and this computation it reflects that Linda has too much liquidity 4:62 that is

not good for organisation as they need to generate with nearest ideal ratio that is 2:1.

Quick ratio- This states that if company can pay short term debts from liquid assets. It

measure that how efficiently company able to pay current liabilities. This reflect the

financial security of company and useful for creditors and investor in terms of risk

evaluations as they want to invest in risk free company. The ideal ratio of quick ratio is

1:1. As per the calculation it is evaluated that Linda has 4:61 which is shows excess in

liquidity as compare to industry ratio is 1:89 (Wu, and et.al., 2016).

Accounts receivable ratio- It is important for the debtors turnover ratio and part of

efficiency ratio and used to measure business collective manner and determine that how

effectively they manage their clients by analysing the outstanding debt in accounting

period and will help the organisation in strengthen their system. In the calculation, Linda

business provides time 37.44 days for collection of amount and industry gives 50 days

for the collections.

Accounts payable ratio- It is part of liquidity ratio that shows that how can business can

pay off the debts and will need to be analyse adequately to balance the payments. The

calculation ratio of Linda is 350 days to pay their creditors and industry take 72 days in

same process (O'Leary, 2018).

CONCLUSION

From the above report it is concluded that business performance based on financial and

non- financial performance and it is very important to record all relevant monetary transaction to

keep all records in systematic manner. Through making records it become essential to keep them

maintained and has to be properly analysed to make further plans. In recording all transaction,

the need of preparation of Journal, ledger, trial balance and after evaluating them thoroughly the

need of further statements is possible. After the preparation of income statements and financial

statements helps in analysing the financial position of organisation and evaluating the

performance in proper manner. Calculation of financial ratios also helps in assessing the liquidity

and overall position of organisation and these were helpful for investor and shareholders to make

decisions regarding investment in the respective organisation.

pay off the debts and will need to be analyse adequately to balance the payments. The

calculation ratio of Linda is 350 days to pay their creditors and industry take 72 days in

same process (O'Leary, 2018).

CONCLUSION

From the above report it is concluded that business performance based on financial and

non- financial performance and it is very important to record all relevant monetary transaction to

keep all records in systematic manner. Through making records it become essential to keep them

maintained and has to be properly analysed to make further plans. In recording all transaction,

the need of preparation of Journal, ledger, trial balance and after evaluating them thoroughly the

need of further statements is possible. After the preparation of income statements and financial

statements helps in analysing the financial position of organisation and evaluating the

performance in proper manner. Calculation of financial ratios also helps in assessing the liquidity

and overall position of organisation and these were helpful for investor and shareholders to make

decisions regarding investment in the respective organisation.

REFERENCES

Books and Journals:

Chow, D. C. and Schoenbaum, T. J., 2020. International business transactions: problems, cases,

and materials. Wolters Kluwer Law & Business.

TORSELLO, M. and WINKLER, M. M., 2020. Coronavirus-infected international business

transactions: a preliminary diagnosis. European Journal of Risk Regulation.11(2).

pp.396-401.

Painuly, P. and Rathi, S., 2016. Mobile wallet: An upcoming mode of business transactions.

International Journal in Management & Social Science.4(5). pp.356-363.

Ekici, A. and Ekici, Ş. Ö., 2019. Understanding and managing complexity through Bayesian

network approach: The case of bribery in business transactions. Journal of Business

Research.

Cuniberti, G., 2016. The Laws of Asian International Business Transactions. Wash. Int'l LJ.25.

p.35.

Saiti, B. and Abdullah, A., 2016. Prohibited elements in islamic financial transactions: a

comprehensive review. Al-Shajarah: Journal of the International Institute of Islamic

Thought and Civilization (ISTAC).21(3).

Pushpa, P. V., 2016, November. Customer context based transactions in mobile commerce

business environment. In 2016 IEEE 13th International Conference on e-Business

Engineering (ICEBE) (pp. 208-213). IEEE.

Ilayperuma, T. and Zdravkovic, J., 2020. Using business value models to elicit services

conducting business transactions. In Sustainable Business: Concepts, Methodologies,

Tools, and Applications. (pp. 1392-1418). IGI Global.

Wu, J., and et.al., 2016. Inventory models for deteriorating items with maximum lifetime under

downstream partial trade credits to credit-risk customers by discounted cash-flow

analysis. International Journal of Production Economics.171. pp.105-115.

O'Leary, D. E., 2018. Open information enterprise transactions: Business intelligence and wash

and spoof transactions in blockchain and social commerce. Intelligent Systems in

Accounting, Finance and Management. 25(3). pp.148-158.

1

Books and Journals:

Chow, D. C. and Schoenbaum, T. J., 2020. International business transactions: problems, cases,

and materials. Wolters Kluwer Law & Business.

TORSELLO, M. and WINKLER, M. M., 2020. Coronavirus-infected international business

transactions: a preliminary diagnosis. European Journal of Risk Regulation.11(2).

pp.396-401.

Painuly, P. and Rathi, S., 2016. Mobile wallet: An upcoming mode of business transactions.

International Journal in Management & Social Science.4(5). pp.356-363.

Ekici, A. and Ekici, Ş. Ö., 2019. Understanding and managing complexity through Bayesian

network approach: The case of bribery in business transactions. Journal of Business

Research.

Cuniberti, G., 2016. The Laws of Asian International Business Transactions. Wash. Int'l LJ.25.

p.35.

Saiti, B. and Abdullah, A., 2016. Prohibited elements in islamic financial transactions: a

comprehensive review. Al-Shajarah: Journal of the International Institute of Islamic

Thought and Civilization (ISTAC).21(3).

Pushpa, P. V., 2016, November. Customer context based transactions in mobile commerce

business environment. In 2016 IEEE 13th International Conference on e-Business

Engineering (ICEBE) (pp. 208-213). IEEE.

Ilayperuma, T. and Zdravkovic, J., 2020. Using business value models to elicit services

conducting business transactions. In Sustainable Business: Concepts, Methodologies,

Tools, and Applications. (pp. 1392-1418). IGI Global.

Wu, J., and et.al., 2016. Inventory models for deteriorating items with maximum lifetime under

downstream partial trade credits to credit-risk customers by discounted cash-flow

analysis. International Journal of Production Economics.171. pp.105-115.

O'Leary, D. E., 2018. Open information enterprise transactions: Business intelligence and wash

and spoof transactions in blockchain and social commerce. Intelligent Systems in

Accounting, Finance and Management. 25(3). pp.148-158.

1

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.