Recording Business Transaction

VerifiedAdded on 2022/12/29

|14

|2008

|78

AI Summary

This document provides information about recording business transactions, including examples of transactions, ledger accounts, trial balance, income statement, financial position, and analysis of Linda's business performance. It also includes a letter to Linda regarding drawings and various financial ratios for Linda's business. The document is suitable for students studying accounting or business-related courses.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

RECORDING BUSINESS

TRANSACTION

TRANSACTION

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

MAIN BODY...................................................................................................................................3

Part A...............................................................................................................................................3

a) Business transaction in Linda buying and selling toys in Oxford...........................................3

b)Ledger Accounts of Linda business.........................................................................................4

c) Trial balance as on 31st oct 2020............................................................................................7

d)Income statement for year ended 31st Oct 2020......................................................................8

e) Financial Position as on 31st Oct 2020...................................................................................8

f)Letter to Linda regarding drawings..........................................................................................8

Part B...............................................................................................................................................9

1. Ratio's for Linda's Business....................................................................................................9

2. Analysis of Lind's business performance as compared to competitors.................................10

REFERENCES..............................................................................................................................12

MAIN BODY...................................................................................................................................3

Part A...............................................................................................................................................3

a) Business transaction in Linda buying and selling toys in Oxford...........................................3

b)Ledger Accounts of Linda business.........................................................................................4

c) Trial balance as on 31st oct 2020............................................................................................7

d)Income statement for year ended 31st Oct 2020......................................................................8

e) Financial Position as on 31st Oct 2020...................................................................................8

f)Letter to Linda regarding drawings..........................................................................................8

Part B...............................................................................................................................................9

1. Ratio's for Linda's Business....................................................................................................9

2. Analysis of Lind's business performance as compared to competitors.................................10

REFERENCES..............................................................................................................................12

MAIN BODY

Part A

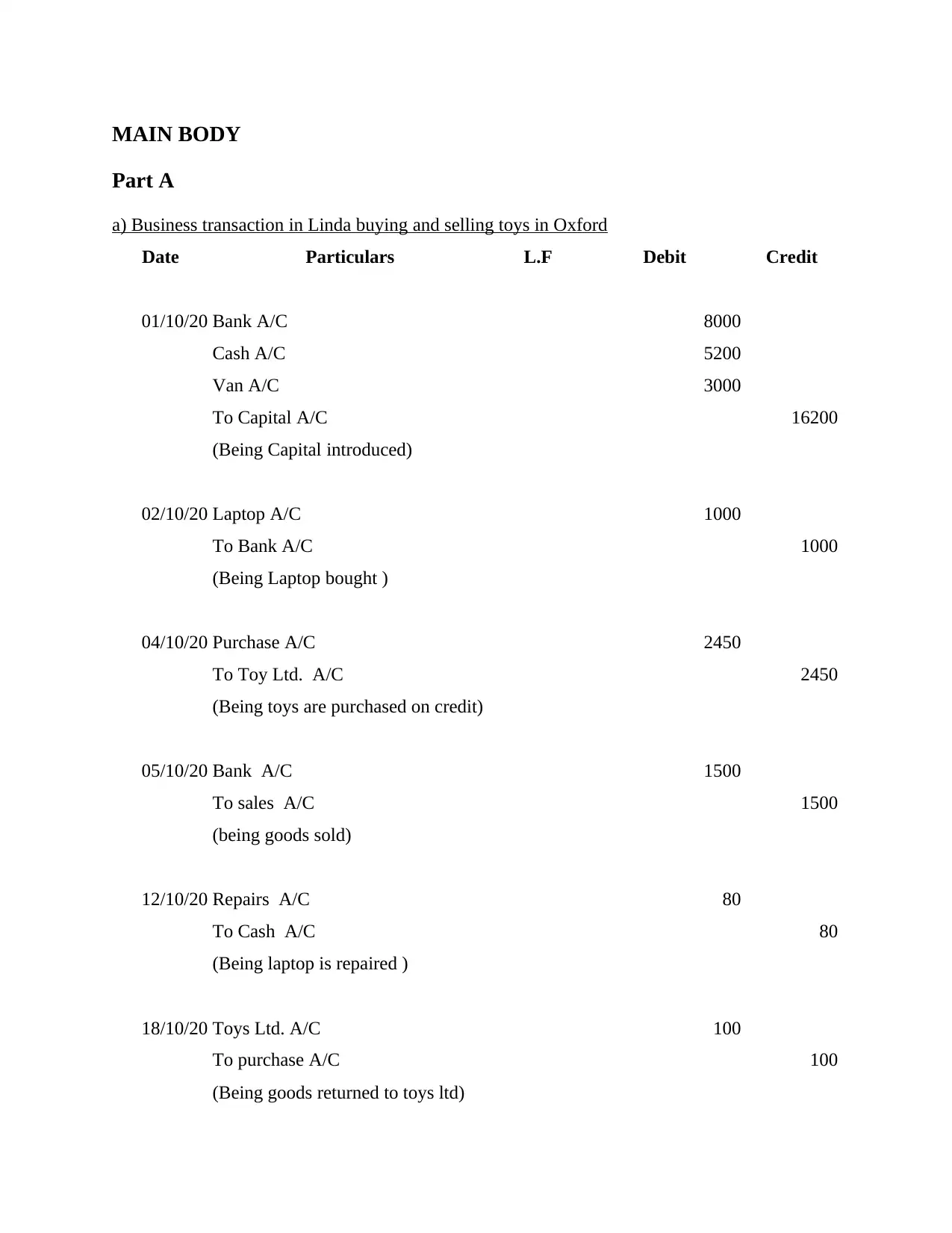

a) Business transaction in Linda buying and selling toys in Oxford

Date Particulars L.F Debit Credit

01/10/20 Bank A/C 8000

Cash A/C 5200

Van A/C 3000

To Capital A/C 16200

(Being Capital introduced)

02/10/20 Laptop A/C 1000

To Bank A/C 1000

(Being Laptop bought )

04/10/20 Purchase A/C 2450

To Toy Ltd. A/C 2450

(Being toys are purchased on credit)

05/10/20 Bank A/C 1500

To sales A/C 1500

(being goods sold)

12/10/20 Repairs A/C 80

To Cash A/C 80

(Being laptop is repaired )

18/10/20 Toys Ltd. A/C 100

To purchase A/C 100

(Being goods returned to toys ltd)

Part A

a) Business transaction in Linda buying and selling toys in Oxford

Date Particulars L.F Debit Credit

01/10/20 Bank A/C 8000

Cash A/C 5200

Van A/C 3000

To Capital A/C 16200

(Being Capital introduced)

02/10/20 Laptop A/C 1000

To Bank A/C 1000

(Being Laptop bought )

04/10/20 Purchase A/C 2450

To Toy Ltd. A/C 2450

(Being toys are purchased on credit)

05/10/20 Bank A/C 1500

To sales A/C 1500

(being goods sold)

12/10/20 Repairs A/C 80

To Cash A/C 80

(Being laptop is repaired )

18/10/20 Toys Ltd. A/C 100

To purchase A/C 100

(Being goods returned to toys ltd)

21/10/20 Bank A/C 500

To Rent A/C 500

(Being rent received)

23/10/20 Cash A/C 1500

Fred A/C 400

To sales A/C 1900

(Being Goods sold on cash and cred

it partly )

23/10/20 Cash A/C 500

To sales A/C 500

(Being goods sold to David)

24/10/20 Second hand car A/C 2500

To Bank A/C 2500

(Being car purchased by issuing

cheque)

26/10/20 wages A/C 820

To Bank A/C 820

(Being wages paid to part time

workers )

30/10/20 Rent A/C 1000

To Bank A/C 1000

(Being rent paid)

31/10/20 Drawings A/C 1600

To Bank A/C 1600

To Rent A/C 500

(Being rent received)

23/10/20 Cash A/C 1500

Fred A/C 400

To sales A/C 1900

(Being Goods sold on cash and cred

it partly )

23/10/20 Cash A/C 500

To sales A/C 500

(Being goods sold to David)

24/10/20 Second hand car A/C 2500

To Bank A/C 2500

(Being car purchased by issuing

cheque)

26/10/20 wages A/C 820

To Bank A/C 820

(Being wages paid to part time

workers )

30/10/20 Rent A/C 1000

To Bank A/C 1000

(Being rent paid)

31/10/20 Drawings A/C 1600

To Bank A/C 1600

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

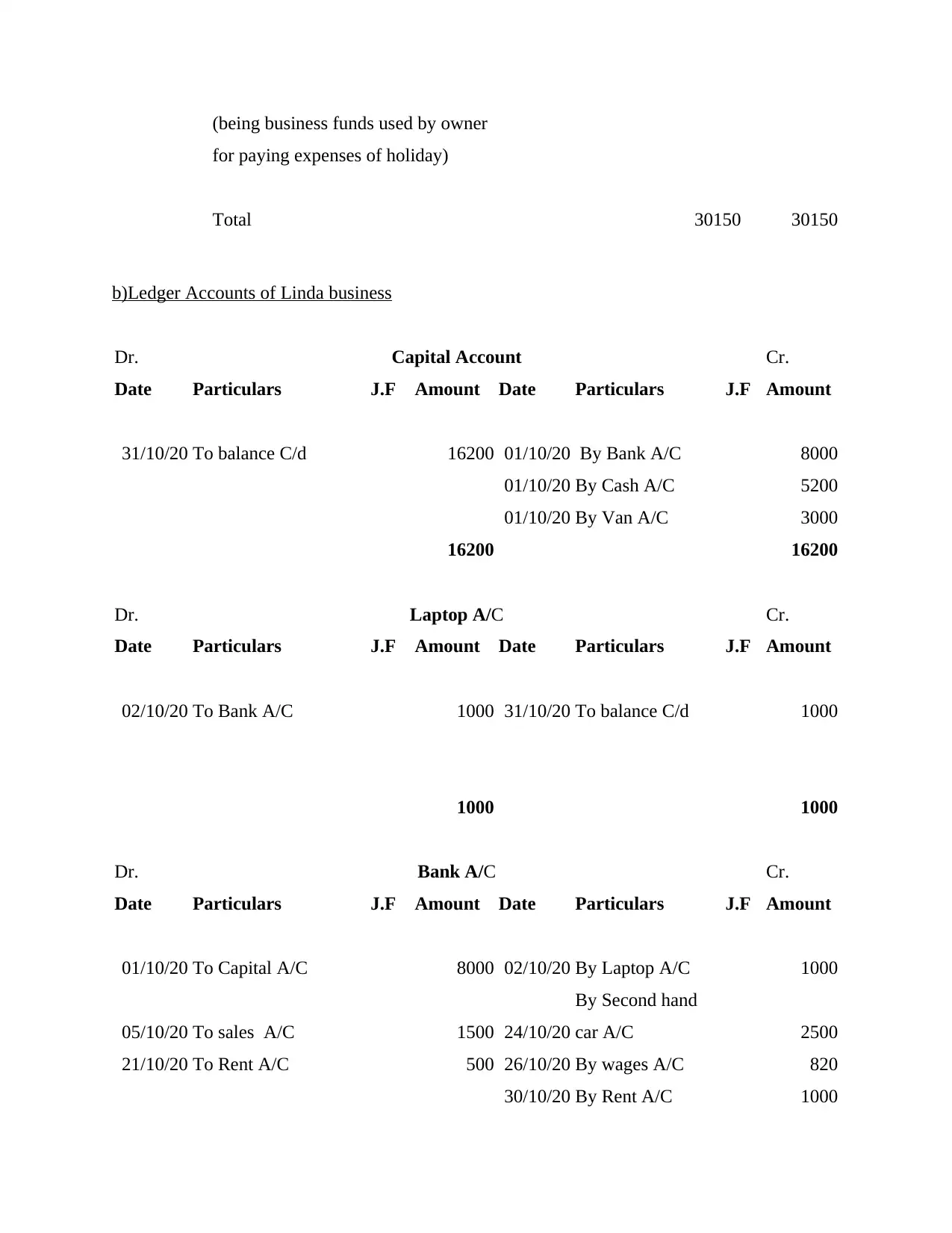

(being business funds used by owner

for paying expenses of holiday)

Total 30150 30150

b)Ledger Accounts of Linda business

Dr. Capital Account Cr.

Date Particulars J.F Amount Date Particulars J.F Amount

31/10/20 To balance C/d 16200 01/10/20 By Bank A/C 8000

01/10/20 By Cash A/C 5200

01/10/20 By Van A/C 3000

16200 16200

Dr. Laptop A/C Cr.

Date Particulars J.F Amount Date Particulars J.F Amount

02/10/20 To Bank A/C 1000 31/10/20 To balance C/d 1000

1000 1000

Dr. Bank A/C Cr.

Date Particulars J.F Amount Date Particulars J.F Amount

01/10/20 To Capital A/C 8000 02/10/20 By Laptop A/C 1000

05/10/20 To sales A/C 1500 24/10/20

By Second hand

car A/C 2500

21/10/20 To Rent A/C 500 26/10/20 By wages A/C 820

30/10/20 By Rent A/C 1000

for paying expenses of holiday)

Total 30150 30150

b)Ledger Accounts of Linda business

Dr. Capital Account Cr.

Date Particulars J.F Amount Date Particulars J.F Amount

31/10/20 To balance C/d 16200 01/10/20 By Bank A/C 8000

01/10/20 By Cash A/C 5200

01/10/20 By Van A/C 3000

16200 16200

Dr. Laptop A/C Cr.

Date Particulars J.F Amount Date Particulars J.F Amount

02/10/20 To Bank A/C 1000 31/10/20 To balance C/d 1000

1000 1000

Dr. Bank A/C Cr.

Date Particulars J.F Amount Date Particulars J.F Amount

01/10/20 To Capital A/C 8000 02/10/20 By Laptop A/C 1000

05/10/20 To sales A/C 1500 24/10/20

By Second hand

car A/C 2500

21/10/20 To Rent A/C 500 26/10/20 By wages A/C 820

30/10/20 By Rent A/C 1000

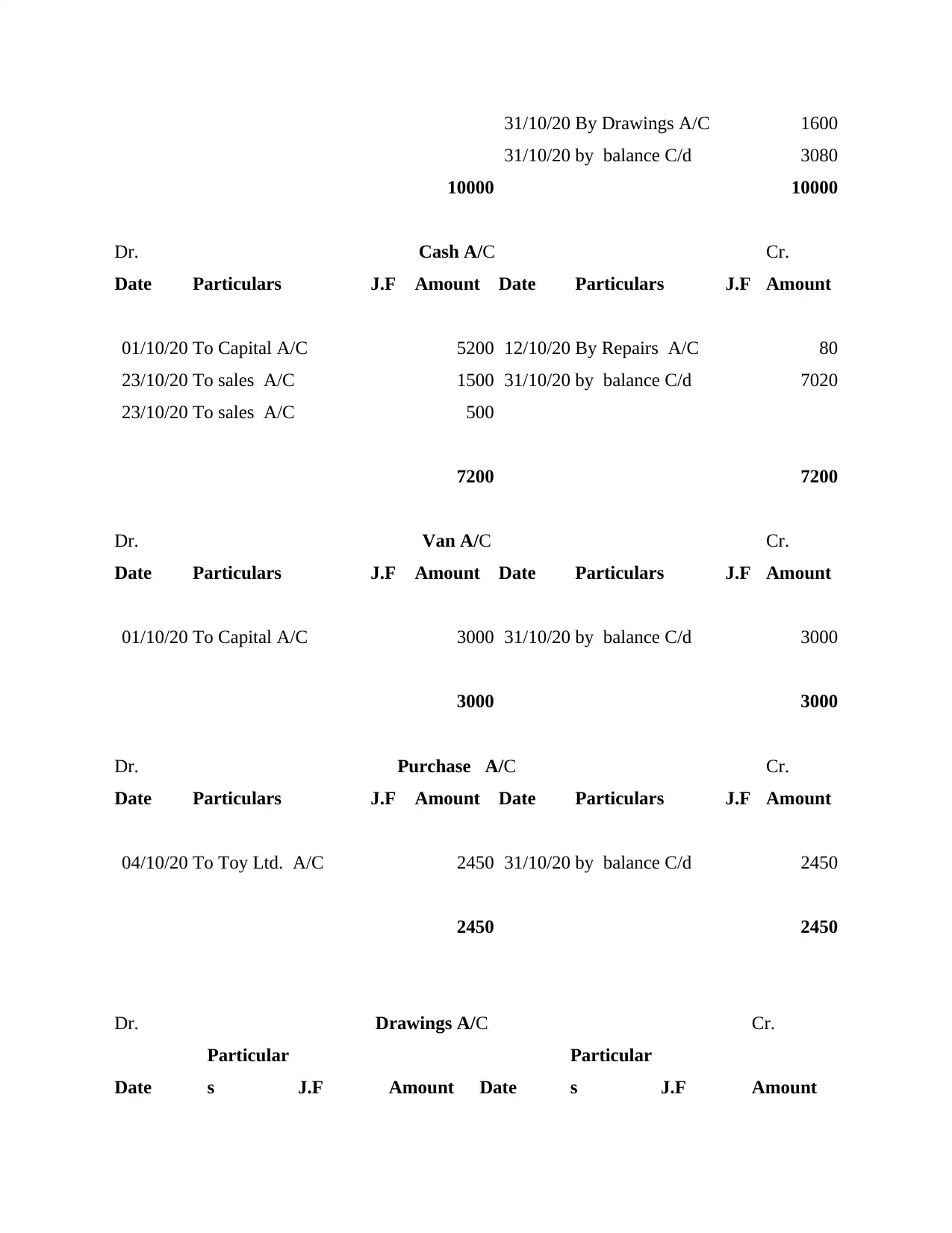

31/10/20 By Drawings A/C 1600

31/10/20 by balance C/d 3080

10000 10000

Dr. Cash A/C Cr.

Date Particulars J.F Amount Date Particulars J.F Amount

01/10/20 To Capital A/C 5200 12/10/20 By Repairs A/C 80

23/10/20 To sales A/C 1500 31/10/20 by balance C/d 7020

23/10/20 To sales A/C 500

7200 7200

Dr. Van A/C Cr.

Date Particulars J.F Amount Date Particulars J.F Amount

01/10/20 To Capital A/C 3000 31/10/20 by balance C/d 3000

3000 3000

Dr. Purchase A/C Cr.

Date Particulars J.F Amount Date Particulars J.F Amount

04/10/20 To Toy Ltd. A/C 2450 31/10/20 by balance C/d 2450

2450 2450

Dr. Drawings A/C Cr.

Date

Particular

s J.F Amount Date

Particular

s J.F Amount

31/10/20 by balance C/d 3080

10000 10000

Dr. Cash A/C Cr.

Date Particulars J.F Amount Date Particulars J.F Amount

01/10/20 To Capital A/C 5200 12/10/20 By Repairs A/C 80

23/10/20 To sales A/C 1500 31/10/20 by balance C/d 7020

23/10/20 To sales A/C 500

7200 7200

Dr. Van A/C Cr.

Date Particulars J.F Amount Date Particulars J.F Amount

01/10/20 To Capital A/C 3000 31/10/20 by balance C/d 3000

3000 3000

Dr. Purchase A/C Cr.

Date Particulars J.F Amount Date Particulars J.F Amount

04/10/20 To Toy Ltd. A/C 2450 31/10/20 by balance C/d 2450

2450 2450

Dr. Drawings A/C Cr.

Date

Particular

s J.F Amount Date

Particular

s J.F Amount

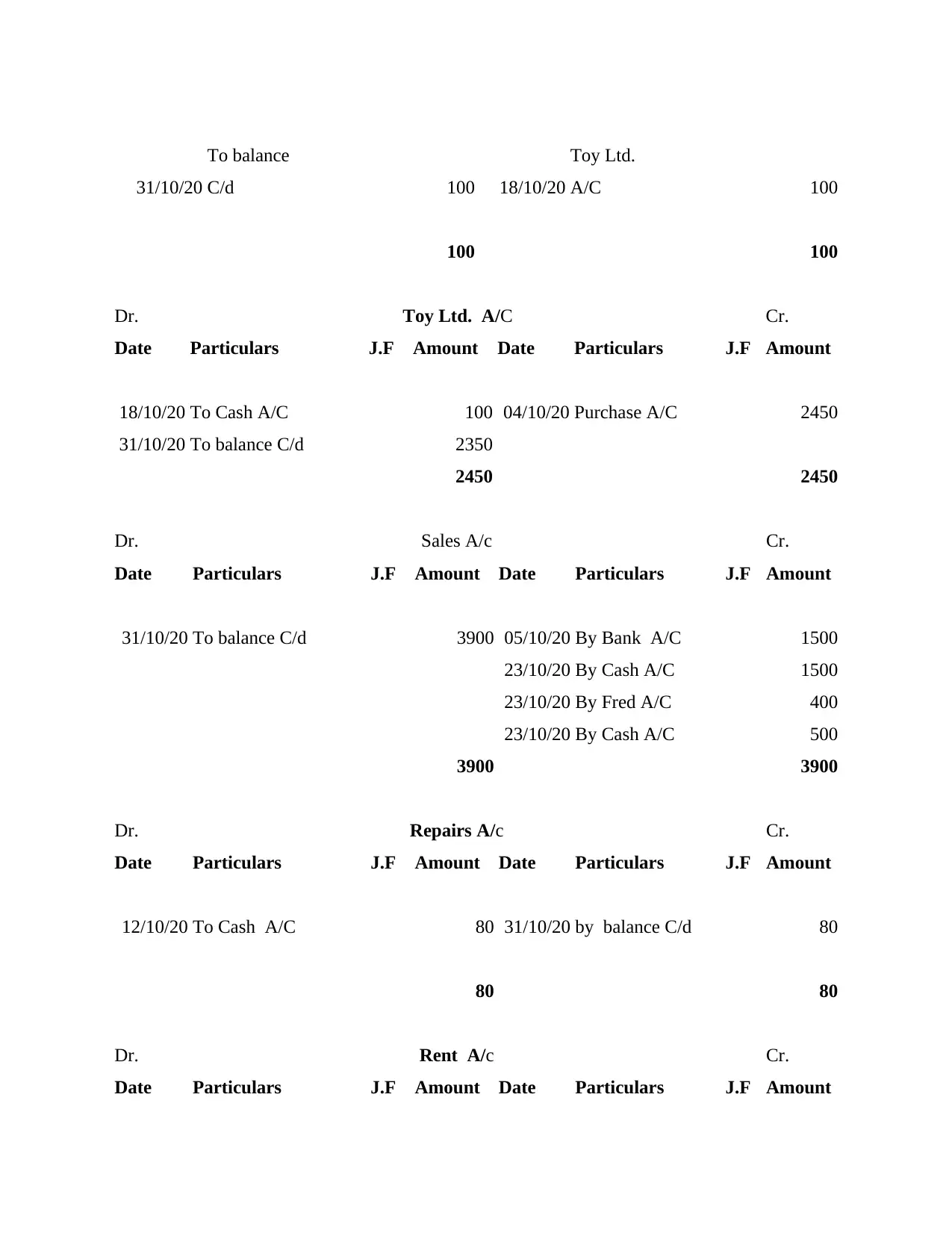

31/10/20

To balance

C/d 100 18/10/20

Toy Ltd.

A/C 100

100 100

Dr. Toy Ltd. A/C Cr.

Date Particulars J.F Amount Date Particulars J.F Amount

18/10/20 To Cash A/C 100 04/10/20 Purchase A/C 2450

31/10/20 To balance C/d 2350

2450 2450

Dr. Sales A/c Cr.

Date Particulars J.F Amount Date Particulars J.F Amount

31/10/20 To balance C/d 3900 05/10/20 By Bank A/C 1500

23/10/20 By Cash A/C 1500

23/10/20 By Fred A/C 400

23/10/20 By Cash A/C 500

3900 3900

Dr. Repairs A/c Cr.

Date Particulars J.F Amount Date Particulars J.F Amount

12/10/20 To Cash A/C 80 31/10/20 by balance C/d 80

80 80

Dr. Rent A/c Cr.

Date Particulars J.F Amount Date Particulars J.F Amount

To balance

C/d 100 18/10/20

Toy Ltd.

A/C 100

100 100

Dr. Toy Ltd. A/C Cr.

Date Particulars J.F Amount Date Particulars J.F Amount

18/10/20 To Cash A/C 100 04/10/20 Purchase A/C 2450

31/10/20 To balance C/d 2350

2450 2450

Dr. Sales A/c Cr.

Date Particulars J.F Amount Date Particulars J.F Amount

31/10/20 To balance C/d 3900 05/10/20 By Bank A/C 1500

23/10/20 By Cash A/C 1500

23/10/20 By Fred A/C 400

23/10/20 By Cash A/C 500

3900 3900

Dr. Repairs A/c Cr.

Date Particulars J.F Amount Date Particulars J.F Amount

12/10/20 To Cash A/C 80 31/10/20 by balance C/d 80

80 80

Dr. Rent A/c Cr.

Date Particulars J.F Amount Date Particulars J.F Amount

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

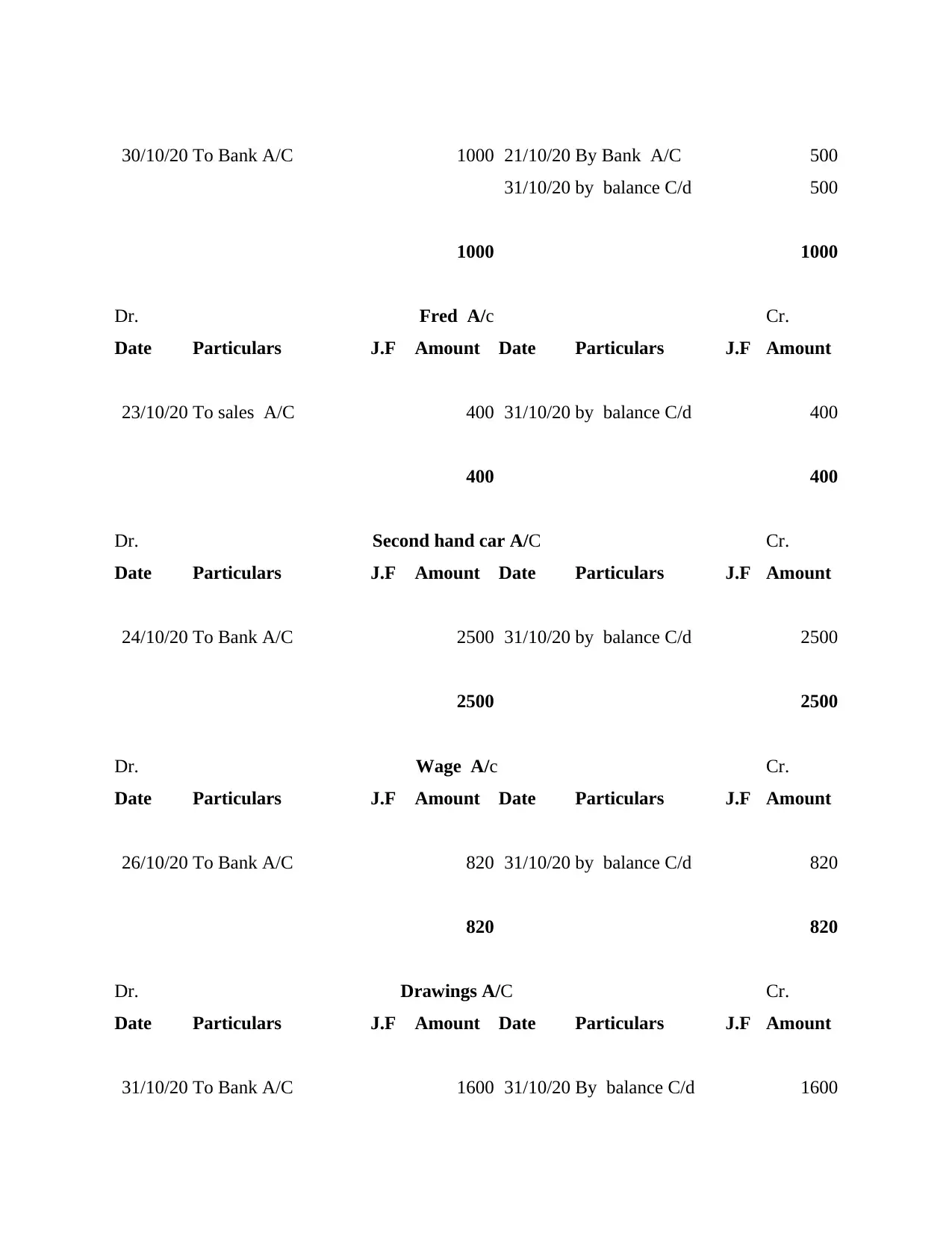

30/10/20 To Bank A/C 1000 21/10/20 By Bank A/C 500

31/10/20 by balance C/d 500

1000 1000

Dr. Fred A/c Cr.

Date Particulars J.F Amount Date Particulars J.F Amount

23/10/20 To sales A/C 400 31/10/20 by balance C/d 400

400 400

Dr. Second hand car A/C Cr.

Date Particulars J.F Amount Date Particulars J.F Amount

24/10/20 To Bank A/C 2500 31/10/20 by balance C/d 2500

2500 2500

Dr. Wage A/c Cr.

Date Particulars J.F Amount Date Particulars J.F Amount

26/10/20 To Bank A/C 820 31/10/20 by balance C/d 820

820 820

Dr. Drawings A/C Cr.

Date Particulars J.F Amount Date Particulars J.F Amount

31/10/20 To Bank A/C 1600 31/10/20 By balance C/d 1600

31/10/20 by balance C/d 500

1000 1000

Dr. Fred A/c Cr.

Date Particulars J.F Amount Date Particulars J.F Amount

23/10/20 To sales A/C 400 31/10/20 by balance C/d 400

400 400

Dr. Second hand car A/C Cr.

Date Particulars J.F Amount Date Particulars J.F Amount

24/10/20 To Bank A/C 2500 31/10/20 by balance C/d 2500

2500 2500

Dr. Wage A/c Cr.

Date Particulars J.F Amount Date Particulars J.F Amount

26/10/20 To Bank A/C 820 31/10/20 by balance C/d 820

820 820

Dr. Drawings A/C Cr.

Date Particulars J.F Amount Date Particulars J.F Amount

31/10/20 To Bank A/C 1600 31/10/20 By balance C/d 1600

1600 1600

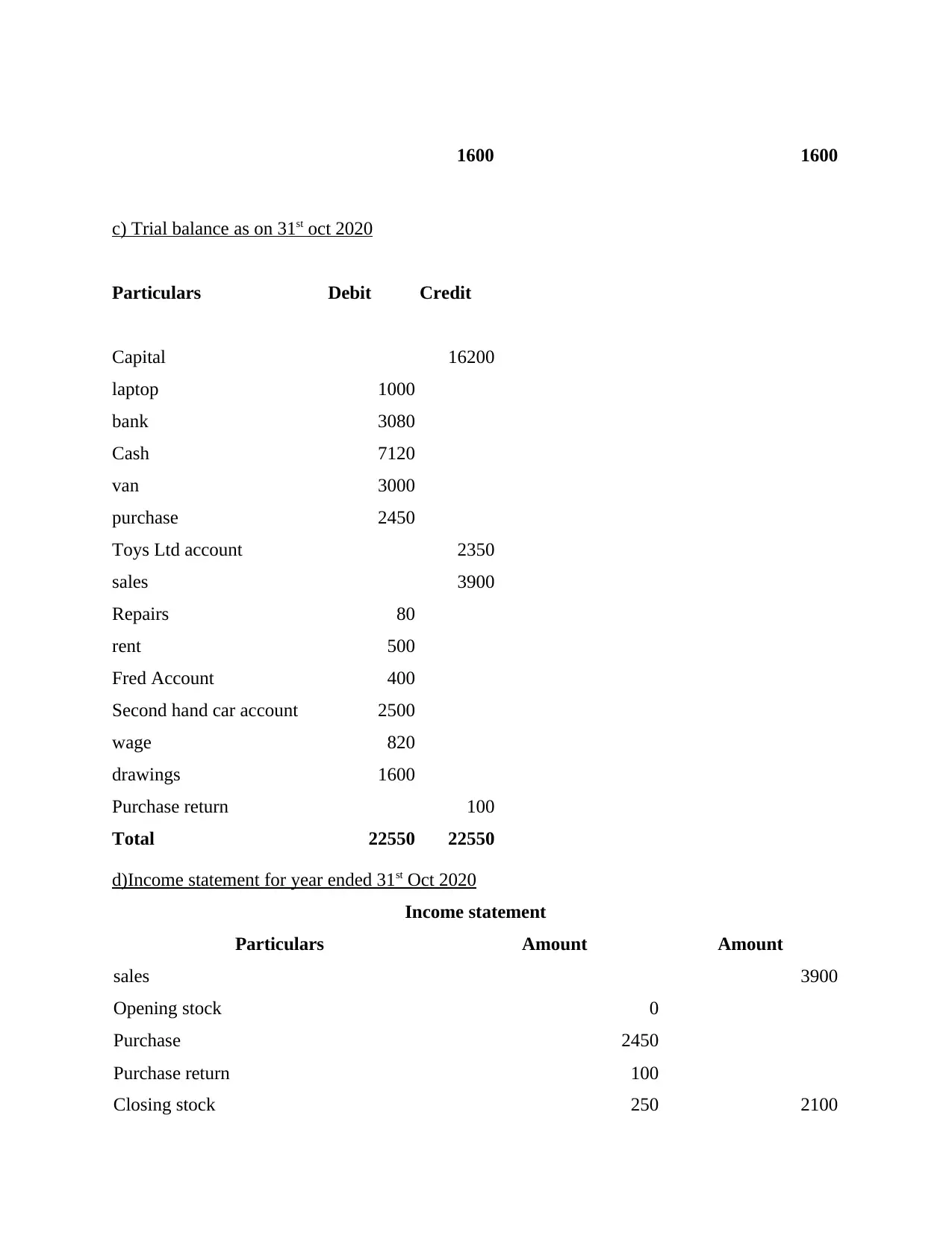

c) Trial balance as on 31st oct 2020

Particulars Debit Credit

Capital 16200

laptop 1000

bank 3080

Cash 7120

van 3000

purchase 2450

Toys Ltd account 2350

sales 3900

Repairs 80

rent 500

Fred Account 400

Second hand car account 2500

wage 820

drawings 1600

Purchase return 100

Total 22550 22550

d)Income statement for year ended 31st Oct 2020

Income statement

Particulars Amount Amount

sales 3900

Opening stock 0

Purchase 2450

Purchase return 100

Closing stock 250 2100

c) Trial balance as on 31st oct 2020

Particulars Debit Credit

Capital 16200

laptop 1000

bank 3080

Cash 7120

van 3000

purchase 2450

Toys Ltd account 2350

sales 3900

Repairs 80

rent 500

Fred Account 400

Second hand car account 2500

wage 820

drawings 1600

Purchase return 100

Total 22550 22550

d)Income statement for year ended 31st Oct 2020

Income statement

Particulars Amount Amount

sales 3900

Opening stock 0

Purchase 2450

Purchase return 100

Closing stock 250 2100

Gross Profit 1800

Repairs 80

rent 500

wage 820 1400

Net Profit 400

e) Financial Position as on 31st Oct 2020

Liabilities Amount Assets Amount

Capital 16200 laptop 1000

(Drawings) -1600 bank 3080

Net Profit 400 Cash 7120

van 3000

creditor 2350 Fred Account 400

Second hand car account 2500

Closing Account 250

17350 17350

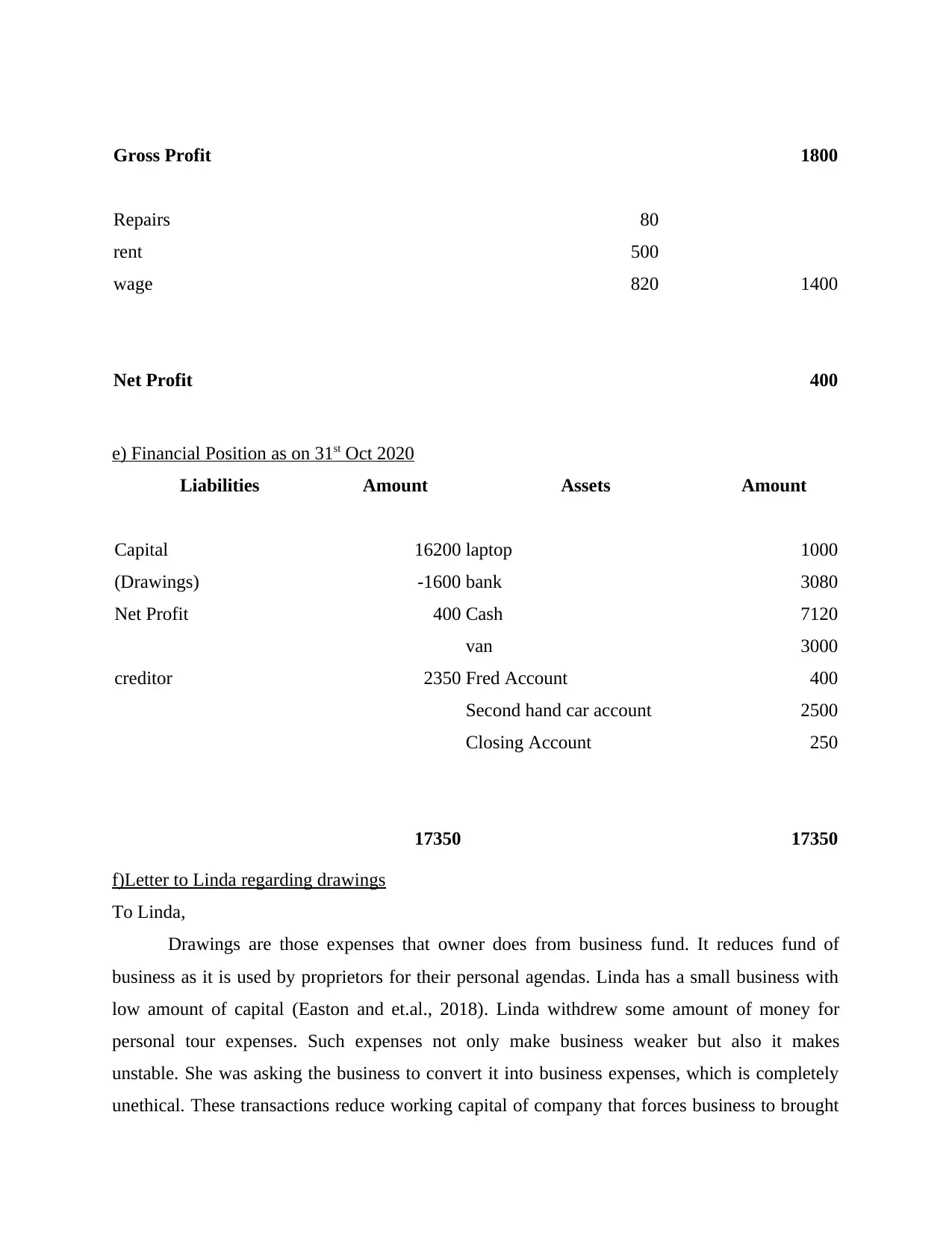

f)Letter to Linda regarding drawings

To Linda,

Drawings are those expenses that owner does from business fund. It reduces fund of

business as it is used by proprietors for their personal agendas. Linda has a small business with

low amount of capital (Easton and et.al., 2018). Linda withdrew some amount of money for

personal tour expenses. Such expenses not only make business weaker but also it makes

unstable. She was asking the business to convert it into business expenses, which is completely

unethical. These transactions reduce working capital of company that forces business to brought

Repairs 80

rent 500

wage 820 1400

Net Profit 400

e) Financial Position as on 31st Oct 2020

Liabilities Amount Assets Amount

Capital 16200 laptop 1000

(Drawings) -1600 bank 3080

Net Profit 400 Cash 7120

van 3000

creditor 2350 Fred Account 400

Second hand car account 2500

Closing Account 250

17350 17350

f)Letter to Linda regarding drawings

To Linda,

Drawings are those expenses that owner does from business fund. It reduces fund of

business as it is used by proprietors for their personal agendas. Linda has a small business with

low amount of capital (Easton and et.al., 2018). Linda withdrew some amount of money for

personal tour expenses. Such expenses not only make business weaker but also it makes

unstable. She was asking the business to convert it into business expenses, which is completely

unethical. These transactions reduce working capital of company that forces business to brought

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

money from external resources. These external resources charge interest from firm for using

these resources for the motive of earning profit.

It is expected from the owner of business to pay its drawings on time with interest.

Proprietor (Craja, Kim and Lessmann, 2020). It is ethical principle of accounting to maintain fair

transaction. To fulfil this principle paying drawings to organization becomes necessary for owner

of firm. It expected from you to pay this obligation for safeguard of business.

Part B

1. Ratio's for Linda's Business

Net profit ratio

Particulars Formula Ratio

Net Profit 400

sales 3900

Net profit Ratio Net Profit /sales *100 10.25

Gross profit ratio

Particulars Formula Ratio

gross Profit 1800

sales 3900

Gross profit margin Gross Profit /sales *100 46.15

Current Ratio

Particulars Formula Ratio

Current asset 10850

current liability 2350

Current ratio Current asset /current liability 4.6

Acid Test Ratio

Particulars Formula Ratio

these resources for the motive of earning profit.

It is expected from the owner of business to pay its drawings on time with interest.

Proprietor (Craja, Kim and Lessmann, 2020). It is ethical principle of accounting to maintain fair

transaction. To fulfil this principle paying drawings to organization becomes necessary for owner

of firm. It expected from you to pay this obligation for safeguard of business.

Part B

1. Ratio's for Linda's Business

Net profit ratio

Particulars Formula Ratio

Net Profit 400

sales 3900

Net profit Ratio Net Profit /sales *100 10.25

Gross profit ratio

Particulars Formula Ratio

gross Profit 1800

sales 3900

Gross profit margin Gross Profit /sales *100 46.15

Current Ratio

Particulars Formula Ratio

Current asset 10850

current liability 2350

Current ratio Current asset /current liability 4.6

Acid Test Ratio

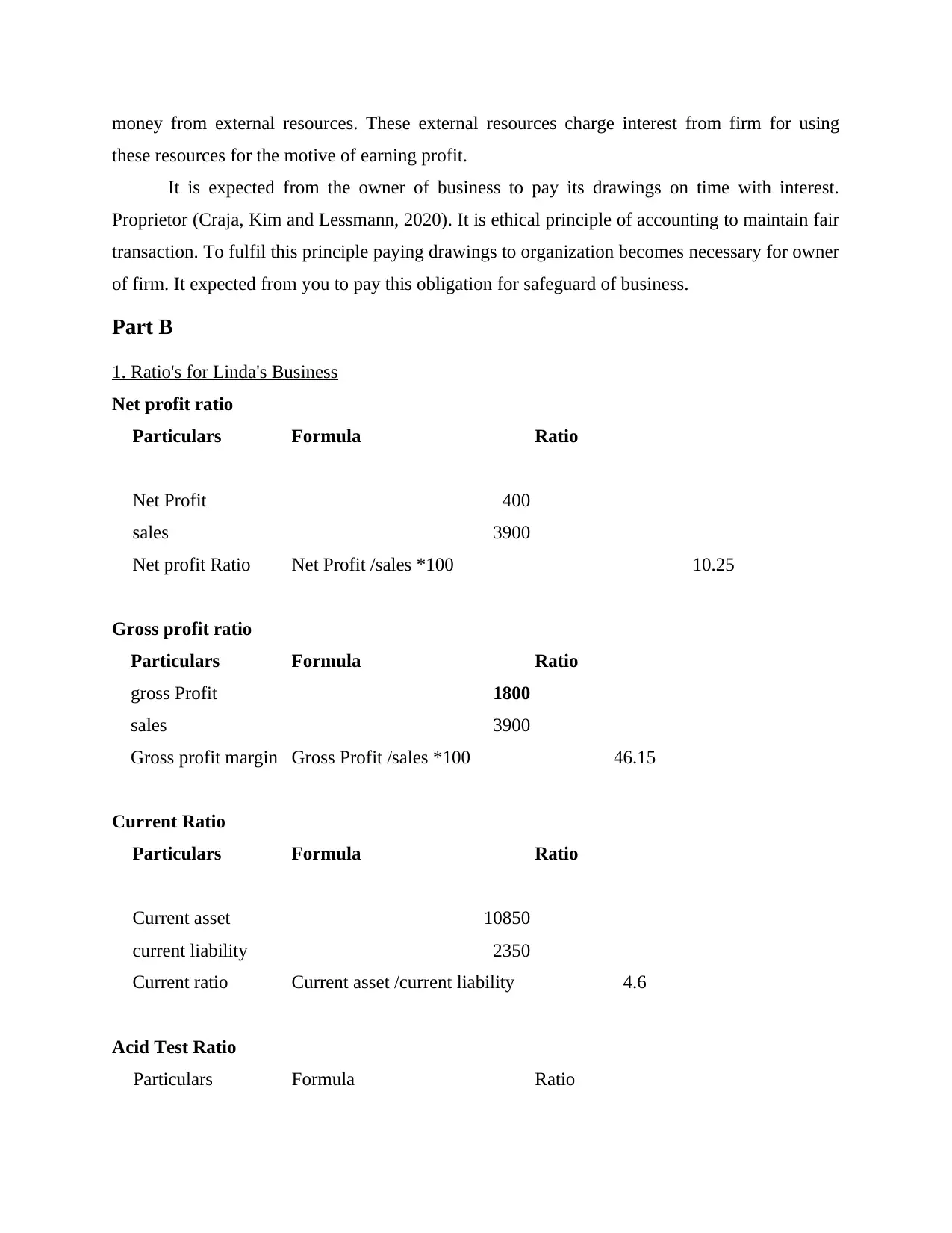

Particulars Formula Ratio

Quick asset 10600

current liability 2350

Acid Test ratio Quick asset /current liability 4.5

Account Receivable collection period

Particulars Formula Ratio

Account receivable 400

net credit sales 400

Account receivable collection period Account receivable /COGS*365 365

Account payable payment period

Particulars Formula Ratio

Account payable 2450

COGS 2100

Account payable payment period Account payable /COGS*365 425.83

2. Analysis of Lind's business performance as compared to competitors

Net profit ratio of Linda's company for the year 2020 is 10.25%. An ideal net profit ratio

of any company should be between 10-20%. So from theoretical perspective ratio of Linda's

business is good. From competitors point of view net profit ratio of Linda's firm is too less as

ratio of competitors is 31% (Robinson, 2020) . so difference between company and others firm

ratio is approx 21% which is indicating low profitability of organisation in industry.

An ideal gross profit Ratio any industry is 15-20%. while ratio of mentioned company is

46.75% which is outstanding when it is compared to ideal ratio. Ratio of competitors is 54% . in

industry Linda is too back in case of earning gross profit. Ratio of profit is 10% approximately

less when it is compared to its industry's participant. This shows that company should take

important actions to improve its profitability to maintain interest of stakeholders.

Current ratio of company is 4.6 times. while a perfect ratio is 1.2-2 , which means that

company have assets two times more than its liabilities. In case of Linda's firm, assets are four

times better than its liabilities that increases investors interest to invest their fund. So that it can

easily pay-off its current obligations (Bergner and et.al., 2020). Current ratio of competitors is

current liability 2350

Acid Test ratio Quick asset /current liability 4.5

Account Receivable collection period

Particulars Formula Ratio

Account receivable 400

net credit sales 400

Account receivable collection period Account receivable /COGS*365 365

Account payable payment period

Particulars Formula Ratio

Account payable 2450

COGS 2100

Account payable payment period Account payable /COGS*365 425.83

2. Analysis of Lind's business performance as compared to competitors

Net profit ratio of Linda's company for the year 2020 is 10.25%. An ideal net profit ratio

of any company should be between 10-20%. So from theoretical perspective ratio of Linda's

business is good. From competitors point of view net profit ratio of Linda's firm is too less as

ratio of competitors is 31% (Robinson, 2020) . so difference between company and others firm

ratio is approx 21% which is indicating low profitability of organisation in industry.

An ideal gross profit Ratio any industry is 15-20%. while ratio of mentioned company is

46.75% which is outstanding when it is compared to ideal ratio. Ratio of competitors is 54% . in

industry Linda is too back in case of earning gross profit. Ratio of profit is 10% approximately

less when it is compared to its industry's participant. This shows that company should take

important actions to improve its profitability to maintain interest of stakeholders.

Current ratio of company is 4.6 times. while a perfect ratio is 1.2-2 , which means that

company have assets two times more than its liabilities. In case of Linda's firm, assets are four

times better than its liabilities that increases investors interest to invest their fund. So that it can

easily pay-off its current obligations (Bergner and et.al., 2020). Current ratio of competitors is

2.87 times which is less than Linda's business. It can be interpreted that company is properly

managing its assets and liabilities.

Quick test ratio of any firm should be 1 so that company can be in position to avoid its

short term obligation easily. Acid test ratio of the Company is 4.5 times (Amadi and Ejiogu,

2021). Higher the ratio more favourable the situation for company as it has more liquid assets to

meet out its non long term liabilities. It is more than competitors in industry as their ratio is 1.35

times. Having good capacity to pay its liability without struggle is good representative of

company.

Account receivable collection period is the duration that company allow its debtor for

paying amount. There is no perfect days specified. It differs from company to company. It is

always suggested to keep collection period short to avoid bad debts. The competitors allow 50

days to their debtors which is may be suitable for their business processing. The Linda company

allows 365 days. This requires changes as no company should allow one year for account

receivable. In such case occurring of bad debt can rise so to neglect such unwanted

circumstances collection period should be less.

Account payable period of Linda company is 425.83 which is good for organisation it

does not need to worry to collect money soon to pay its debts (Samuelson, 2021). Competitors

ratio of Account payable is 72 days which increases their creditworthiness. So being able to pay

debts in shorter time enhances company's ability to pay its obligations easily.

managing its assets and liabilities.

Quick test ratio of any firm should be 1 so that company can be in position to avoid its

short term obligation easily. Acid test ratio of the Company is 4.5 times (Amadi and Ejiogu,

2021). Higher the ratio more favourable the situation for company as it has more liquid assets to

meet out its non long term liabilities. It is more than competitors in industry as their ratio is 1.35

times. Having good capacity to pay its liability without struggle is good representative of

company.

Account receivable collection period is the duration that company allow its debtor for

paying amount. There is no perfect days specified. It differs from company to company. It is

always suggested to keep collection period short to avoid bad debts. The competitors allow 50

days to their debtors which is may be suitable for their business processing. The Linda company

allows 365 days. This requires changes as no company should allow one year for account

receivable. In such case occurring of bad debt can rise so to neglect such unwanted

circumstances collection period should be less.

Account payable period of Linda company is 425.83 which is good for organisation it

does not need to worry to collect money soon to pay its debts (Samuelson, 2021). Competitors

ratio of Account payable is 72 days which increases their creditworthiness. So being able to pay

debts in shorter time enhances company's ability to pay its obligations easily.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Amadi, C. and Ejiogu, A., 2021. Introduction to Financial Accounting. Financial and

Managerial Aspects in Human Resource Management: A Practical Guide, Emerald

Publishing Limited. pp.3-9.

Bergner, R. A. and et.al., 2020. Method and system for recording point to point transaction

processing. U.S. Patent Application 16/842,886.

Craja, P., Kim, A. and Lessmann, S., 2020. Deep learning for detecting financial statement

fraud. Decision Support Systems. 139. p.113421.

Easton, P. D. and et.al., 2018. Financial statement analysis & valuation. Boston, MA:

Cambridge Business Publishers.

Robinson, T. R., 2020. International financial statement analysis. John Wiley & Sons.

Samuelson, J., 2021. The Six New Rules of Business: Creating Real Value in a Changing World.

Berrett-Koehler Publishers.

Books and Journals

Amadi, C. and Ejiogu, A., 2021. Introduction to Financial Accounting. Financial and

Managerial Aspects in Human Resource Management: A Practical Guide, Emerald

Publishing Limited. pp.3-9.

Bergner, R. A. and et.al., 2020. Method and system for recording point to point transaction

processing. U.S. Patent Application 16/842,886.

Craja, P., Kim, A. and Lessmann, S., 2020. Deep learning for detecting financial statement

fraud. Decision Support Systems. 139. p.113421.

Easton, P. D. and et.al., 2018. Financial statement analysis & valuation. Boston, MA:

Cambridge Business Publishers.

Robinson, T. R., 2020. International financial statement analysis. John Wiley & Sons.

Samuelson, J., 2021. The Six New Rules of Business: Creating Real Value in a Changing World.

Berrett-Koehler Publishers.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.