Detailed Analysis of Business Financial Transactions and Reporting

VerifiedAdded on 2022/12/29

|16

|2353

|39

Report

AI Summary

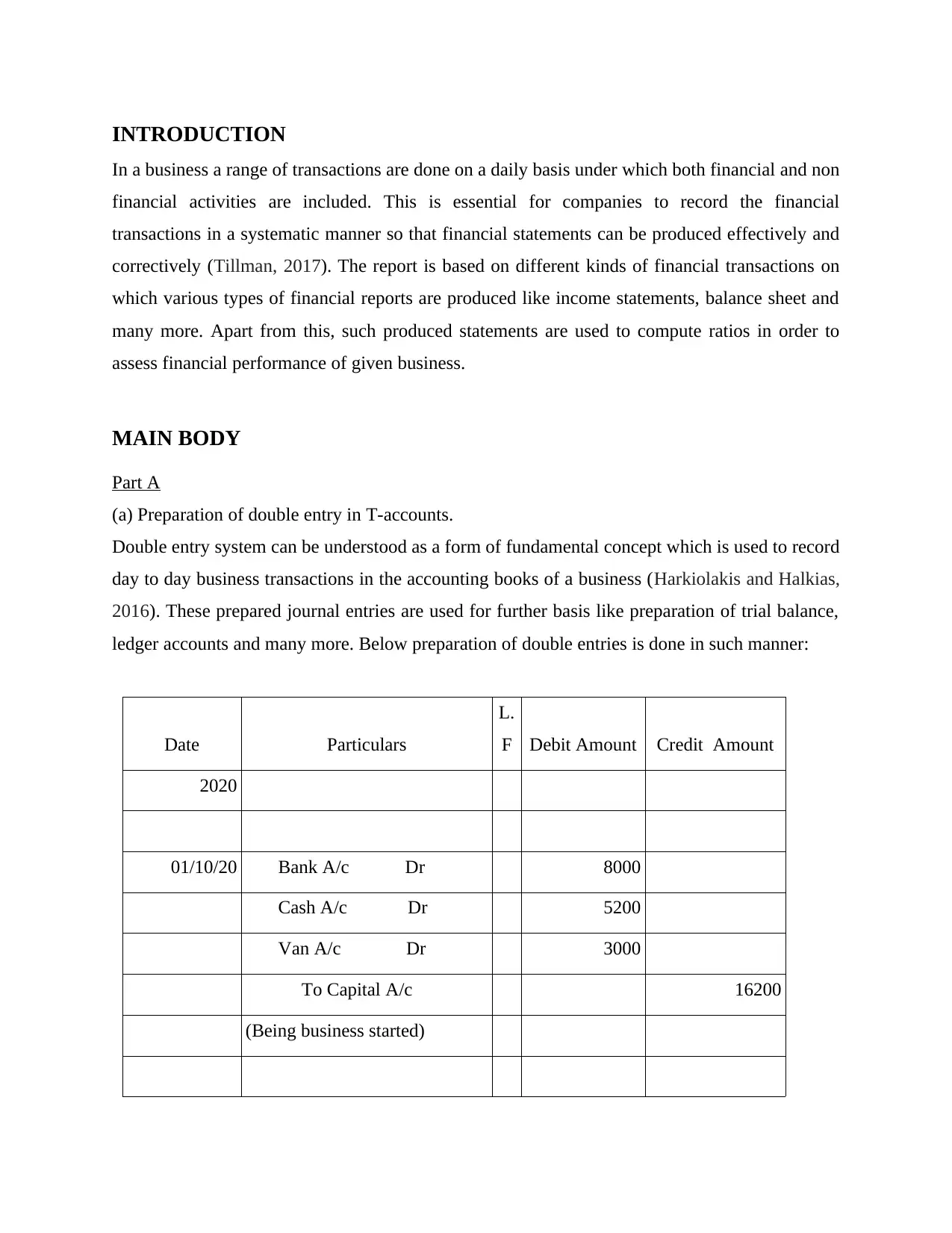

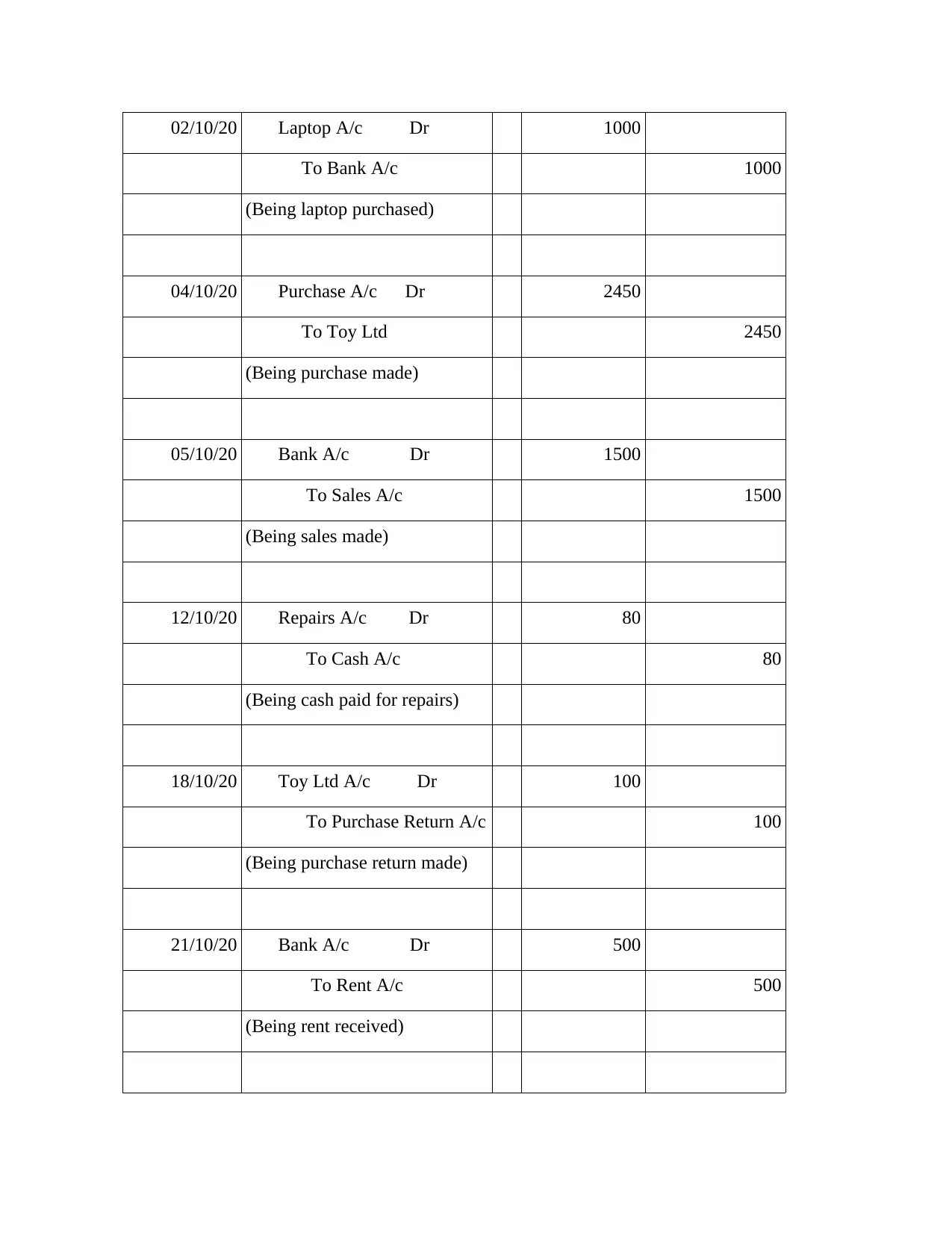

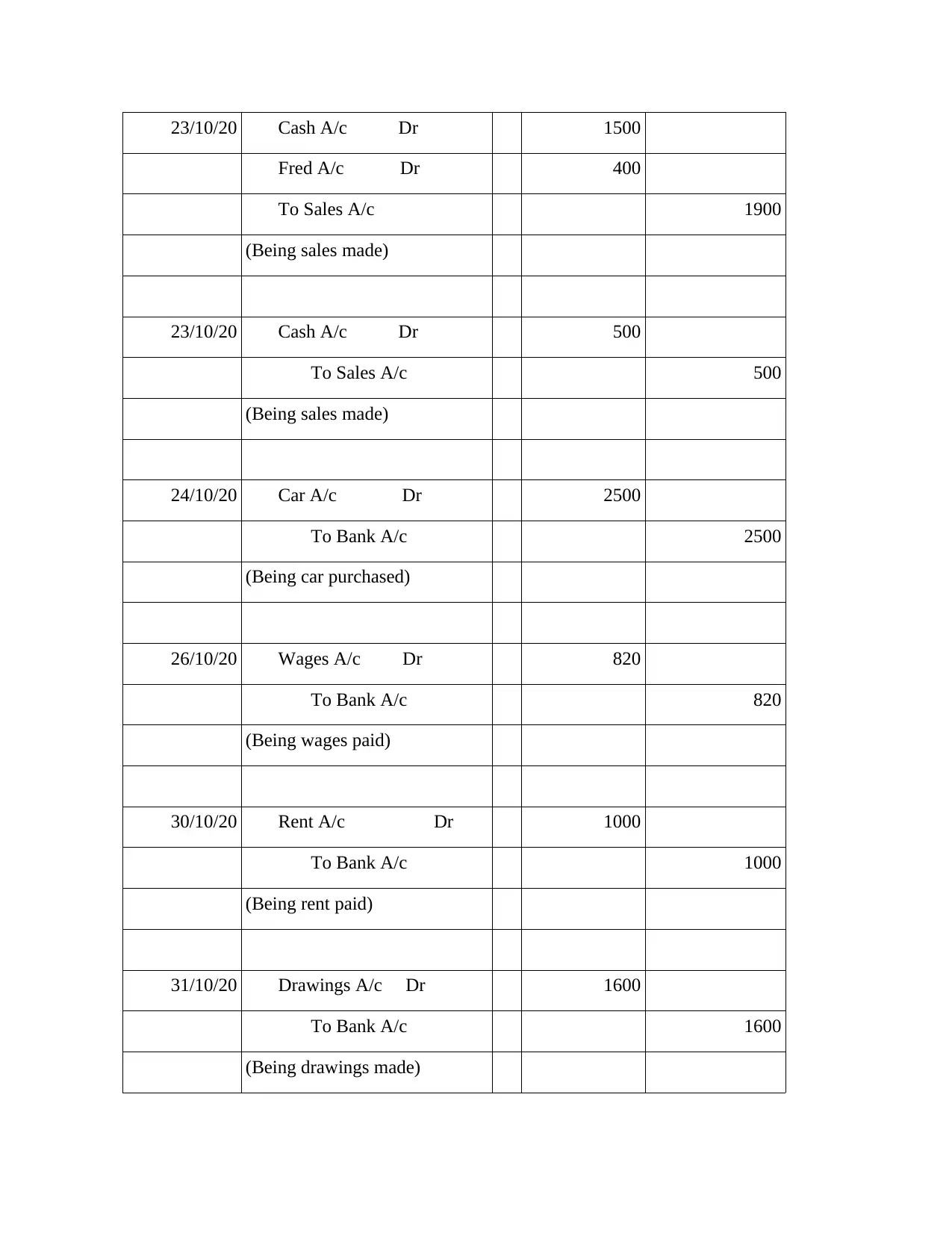

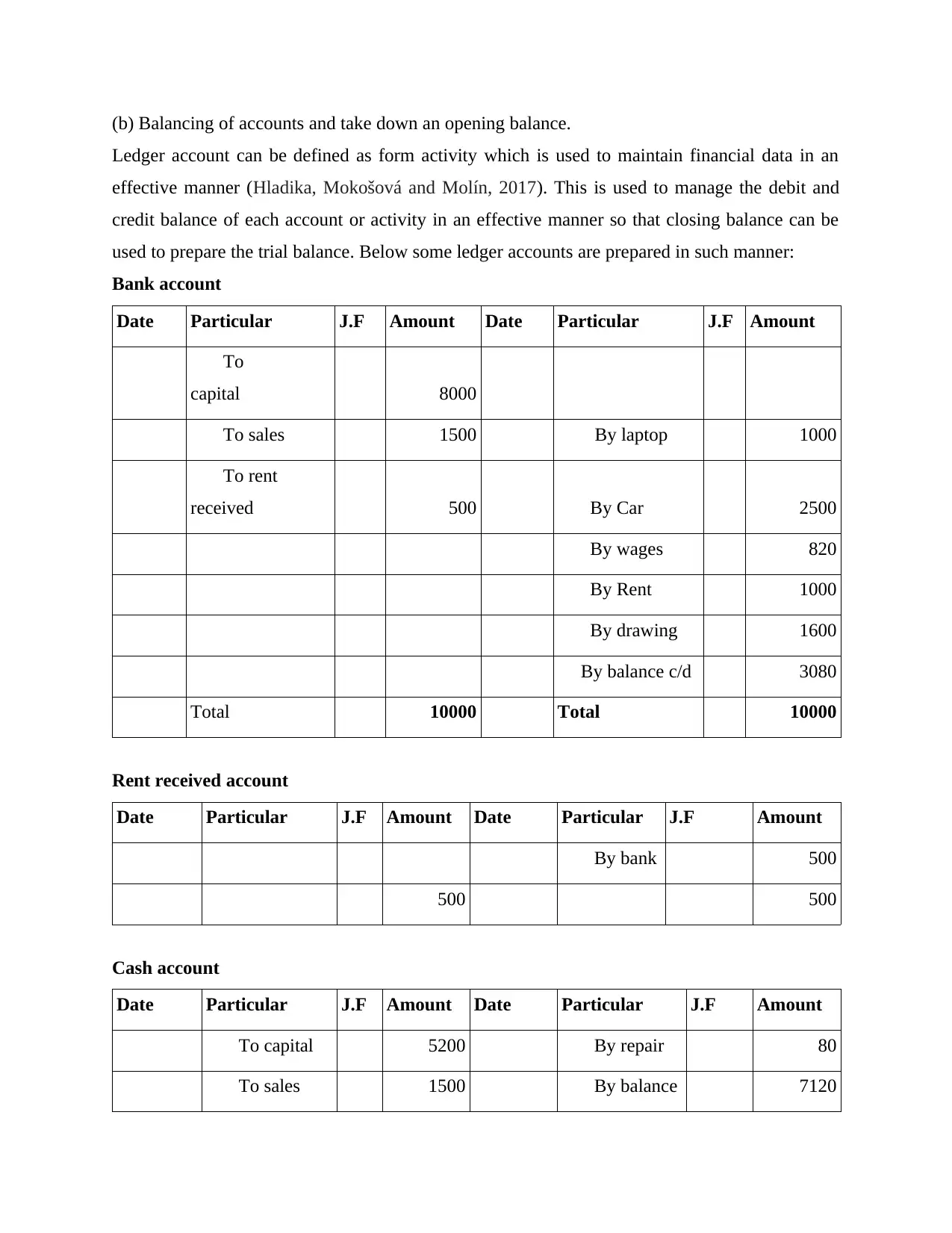

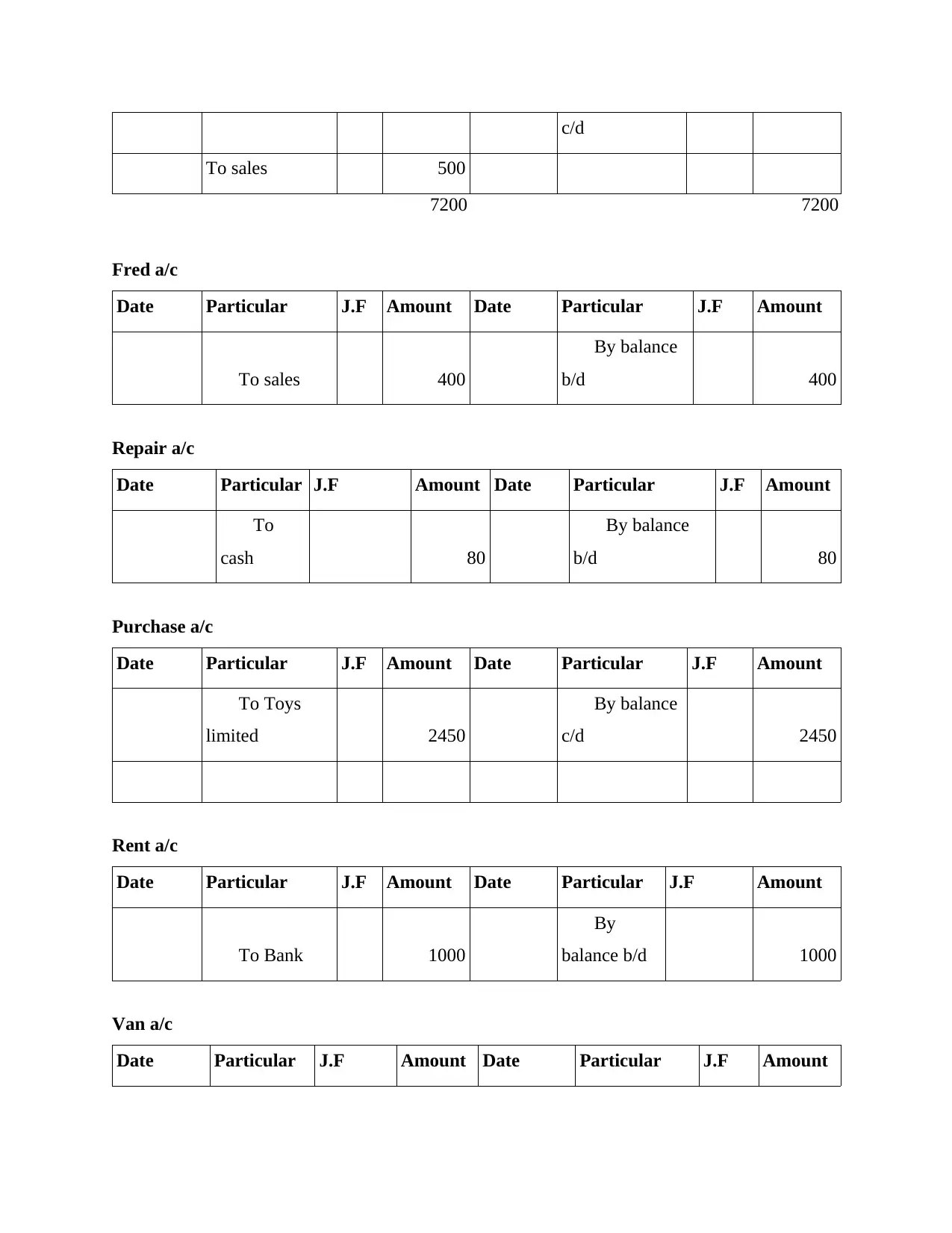

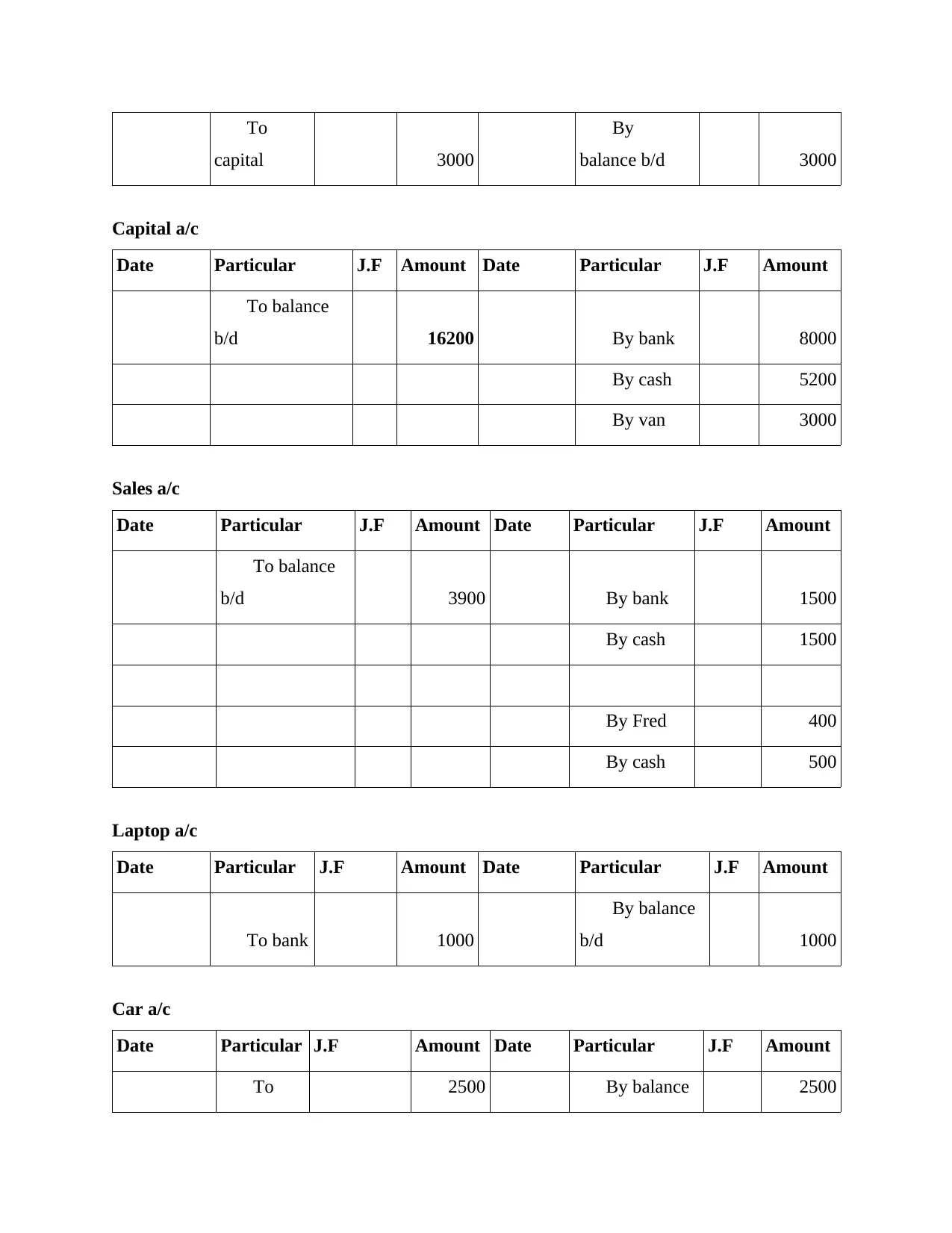

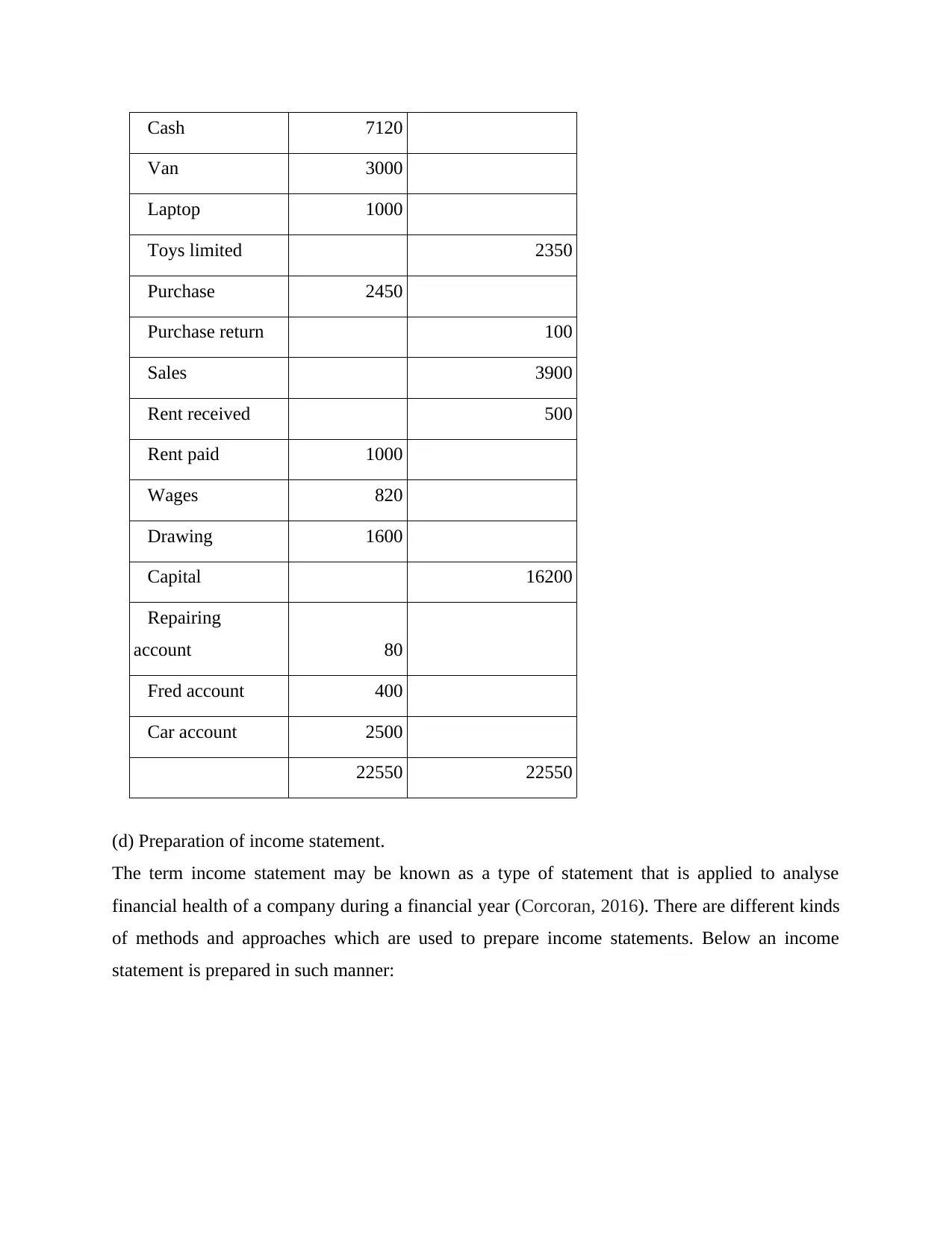

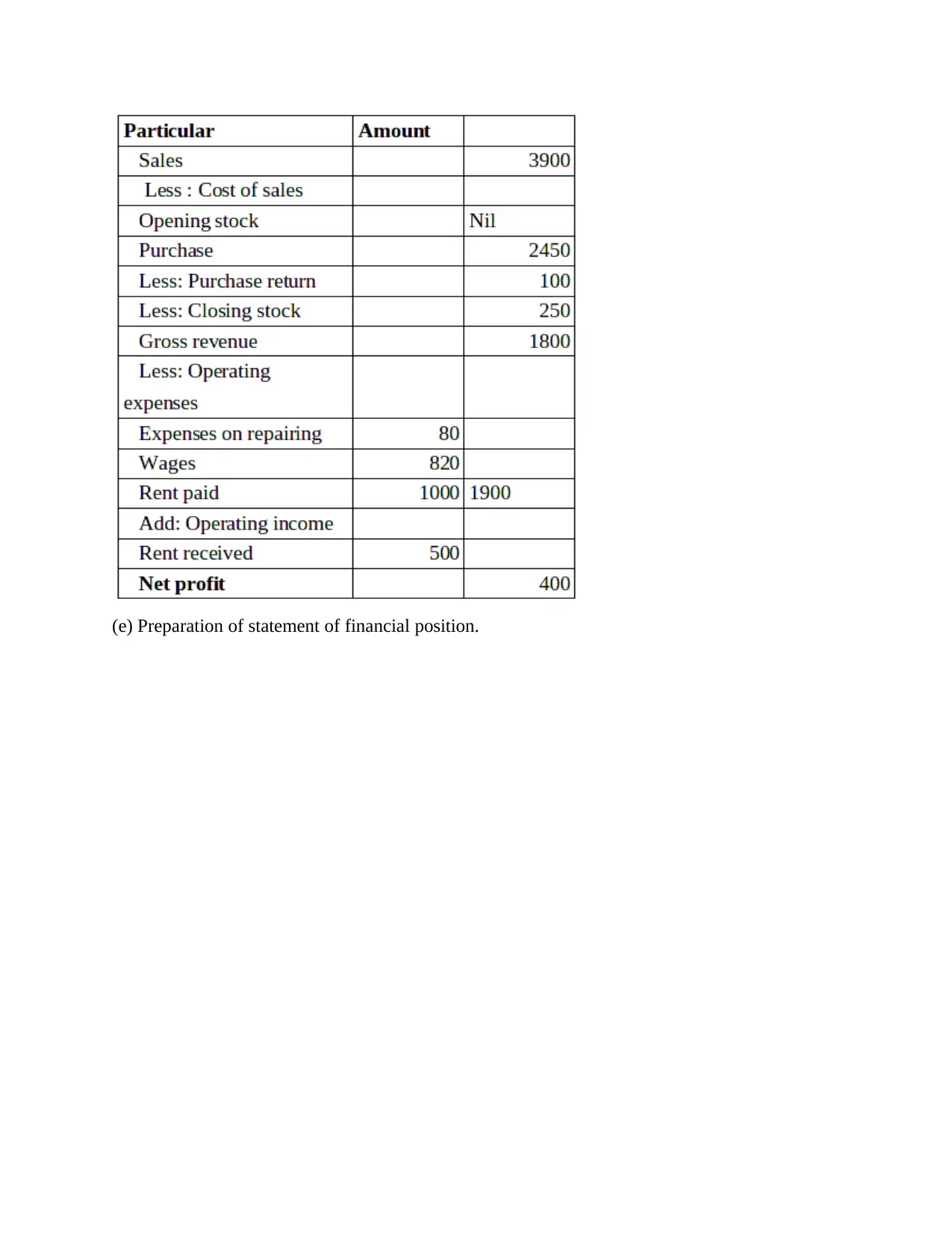

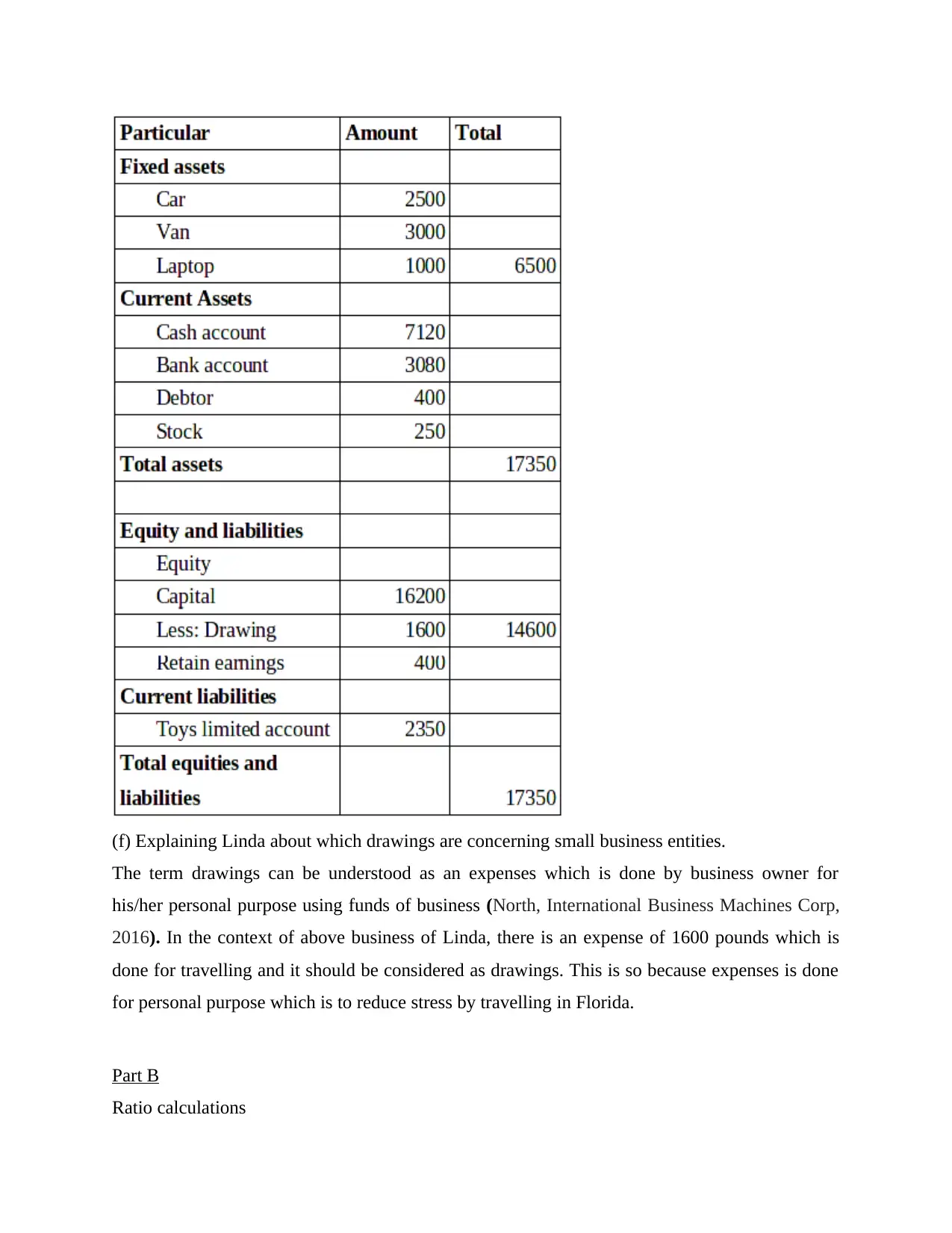

This report meticulously examines the process of recording and analyzing business financial transactions. It begins with an introduction to financial transactions and their importance, followed by a detailed explanation of the double-entry system. The main body of the report includes the preparation of T-accounts, balancing accounts, and taking down opening balances. It also covers the creation of a trial balance, income statement, and statement of financial position. Furthermore, the report analyzes the financial performance of a business using ratio calculations, including net profit, gross profit, current, and quick ratios, as well as accounts receivable and payable collection periods. The report concludes with an analysis of the business's performance compared to industry standards, offering insights into areas for improvement. References to relevant literature are also provided.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.