Recording Business Transaction

VerifiedAdded on 2022/12/14

|14

|2119

|37

AI Summary

This is my second assessment because the first one u make it for me I didnt get more than 50 marks please pay attention more with this one pleaseee

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Recording business

transactions

transactions

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Contents

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

PART 1............................................................................................................................................1

1. Recording the transactions of a company that Linda owns in a T- account in an effective and

efficient manner...........................................................................................................................1

2. Balancing the accounts so as to bring down an opening balance............................................2

3. Extracting a trial balance as at 31st October 2020....................................................................6

4. Preparing an Income statement................................................................................................6

5. Preparing a statement of financial position.............................................................................7

6. Detailed evaluation of all the answers in an appropriate and impactful way..........................8

PART 2............................................................................................................................................8

1. Calculation and interpretation of different ratios for the firm that is mentioned above..........8

2. Comparison of the above calculated ratios including their interpretation...............................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

PART 1............................................................................................................................................1

1. Recording the transactions of a company that Linda owns in a T- account in an effective and

efficient manner...........................................................................................................................1

2. Balancing the accounts so as to bring down an opening balance............................................2

3. Extracting a trial balance as at 31st October 2020....................................................................6

4. Preparing an Income statement................................................................................................6

5. Preparing a statement of financial position.............................................................................7

6. Detailed evaluation of all the answers in an appropriate and impactful way..........................8

PART 2............................................................................................................................................8

1. Calculation and interpretation of different ratios for the firm that is mentioned above..........8

2. Comparison of the above calculated ratios including their interpretation...............................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

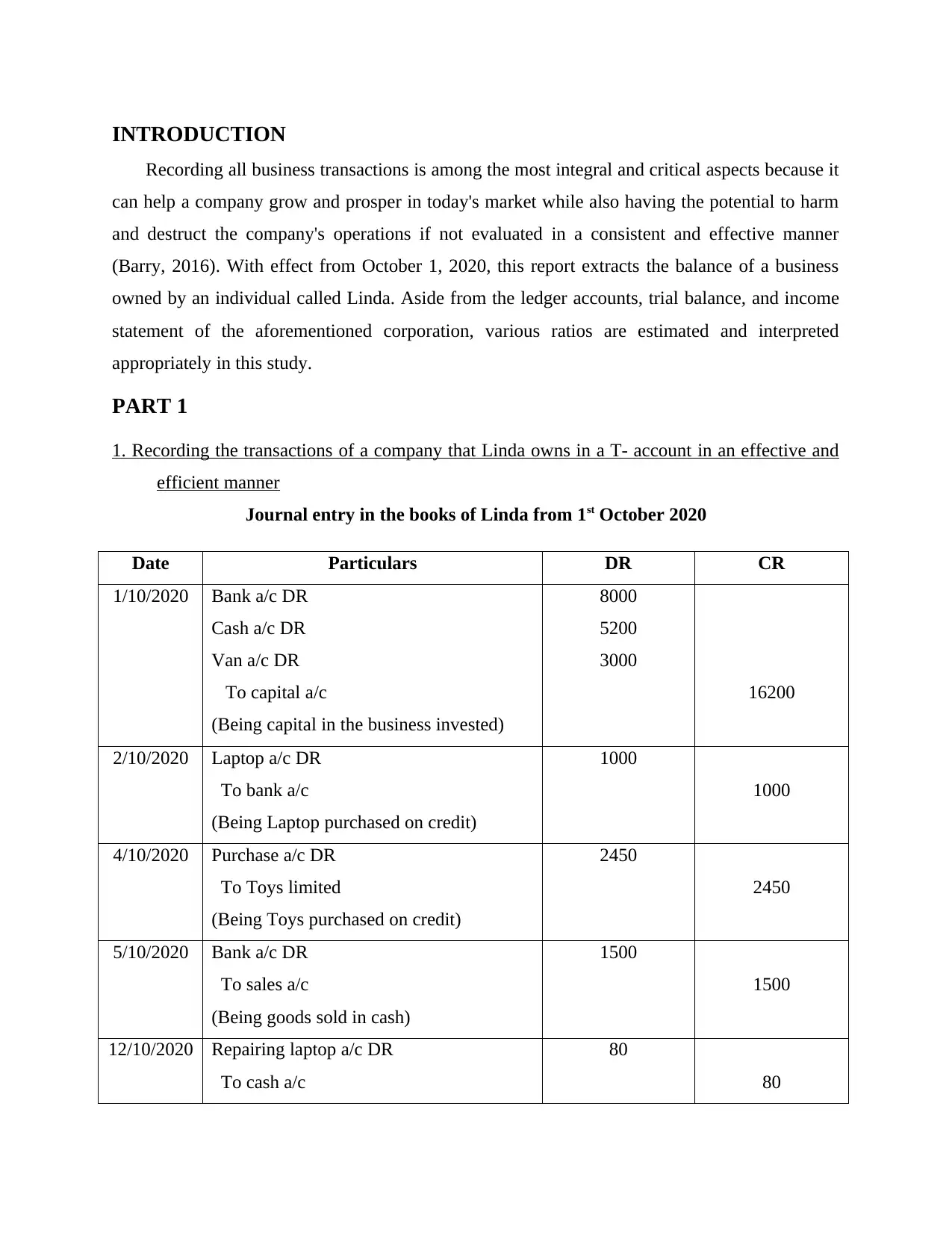

INTRODUCTION

Recording all business transactions is among the most integral and critical aspects because it

can help a company grow and prosper in today's market while also having the potential to harm

and destruct the company's operations if not evaluated in a consistent and effective manner

(Barry, 2016). With effect from October 1, 2020, this report extracts the balance of a business

owned by an individual called Linda. Aside from the ledger accounts, trial balance, and income

statement of the aforementioned corporation, various ratios are estimated and interpreted

appropriately in this study.

PART 1

1. Recording the transactions of a company that Linda owns in a T- account in an effective and

efficient manner

Journal entry in the books of Linda from 1st October 2020

Date Particulars DR CR

1/10/2020 Bank a/c DR

Cash a/c DR

Van a/c DR

To capital a/c

(Being capital in the business invested)

8000

5200

3000

16200

2/10/2020 Laptop a/c DR

To bank a/c

(Being Laptop purchased on credit)

1000

1000

4/10/2020 Purchase a/c DR

To Toys limited

(Being Toys purchased on credit)

2450

2450

5/10/2020 Bank a/c DR

To sales a/c

(Being goods sold in cash)

1500

1500

12/10/2020 Repairing laptop a/c DR

To cash a/c

80

80

Recording all business transactions is among the most integral and critical aspects because it

can help a company grow and prosper in today's market while also having the potential to harm

and destruct the company's operations if not evaluated in a consistent and effective manner

(Barry, 2016). With effect from October 1, 2020, this report extracts the balance of a business

owned by an individual called Linda. Aside from the ledger accounts, trial balance, and income

statement of the aforementioned corporation, various ratios are estimated and interpreted

appropriately in this study.

PART 1

1. Recording the transactions of a company that Linda owns in a T- account in an effective and

efficient manner

Journal entry in the books of Linda from 1st October 2020

Date Particulars DR CR

1/10/2020 Bank a/c DR

Cash a/c DR

Van a/c DR

To capital a/c

(Being capital in the business invested)

8000

5200

3000

16200

2/10/2020 Laptop a/c DR

To bank a/c

(Being Laptop purchased on credit)

1000

1000

4/10/2020 Purchase a/c DR

To Toys limited

(Being Toys purchased on credit)

2450

2450

5/10/2020 Bank a/c DR

To sales a/c

(Being goods sold in cash)

1500

1500

12/10/2020 Repairing laptop a/c DR

To cash a/c

80

80

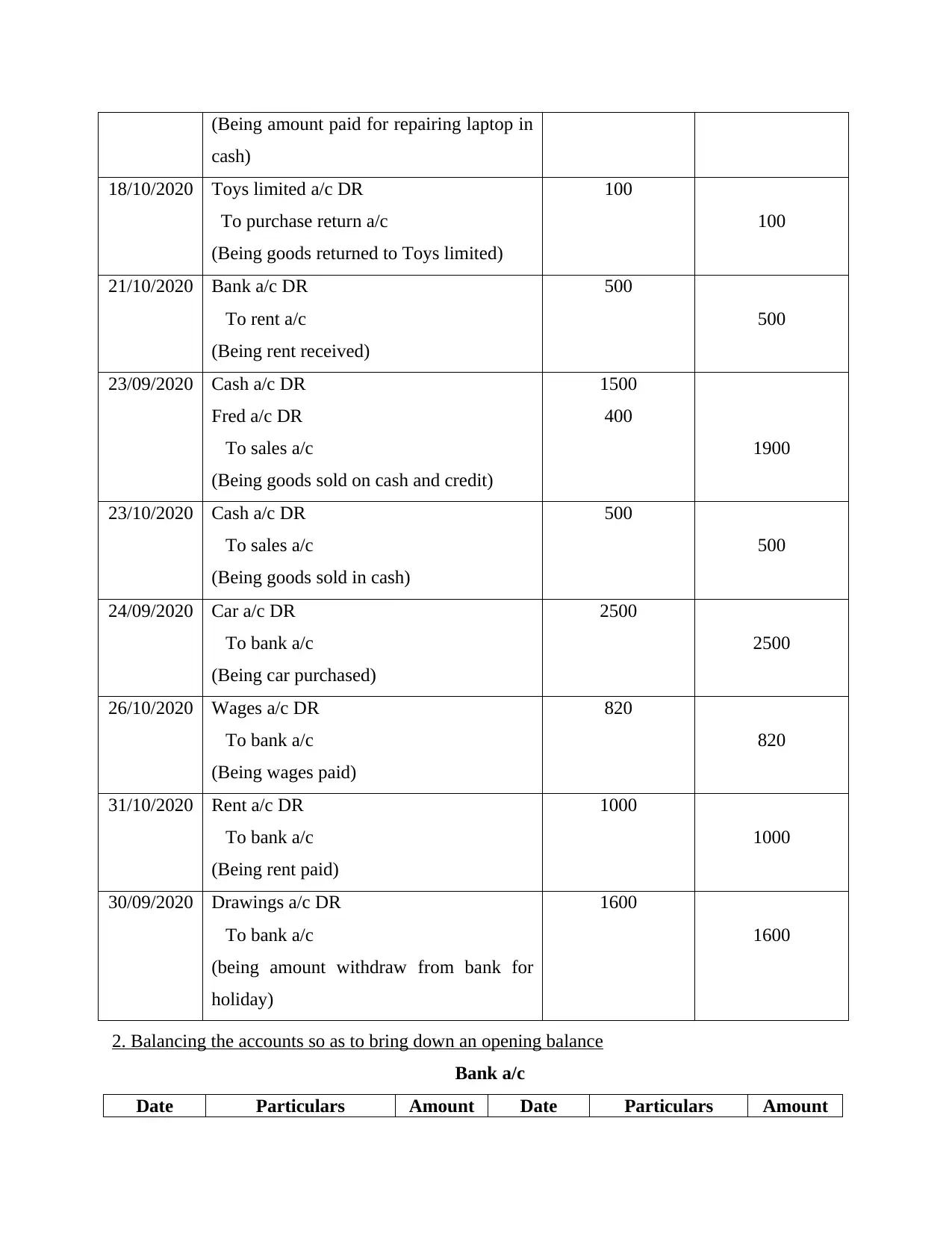

(Being amount paid for repairing laptop in

cash)

18/10/2020 Toys limited a/c DR

To purchase return a/c

(Being goods returned to Toys limited)

100

100

21/10/2020 Bank a/c DR

To rent a/c

(Being rent received)

500

500

23/09/2020 Cash a/c DR

Fred a/c DR

To sales a/c

(Being goods sold on cash and credit)

1500

400

1900

23/10/2020 Cash a/c DR

To sales a/c

(Being goods sold in cash)

500

500

24/09/2020 Car a/c DR

To bank a/c

(Being car purchased)

2500

2500

26/10/2020 Wages a/c DR

To bank a/c

(Being wages paid)

820

820

31/10/2020 Rent a/c DR

To bank a/c

(Being rent paid)

1000

1000

30/09/2020 Drawings a/c DR

To bank a/c

(being amount withdraw from bank for

holiday)

1600

1600

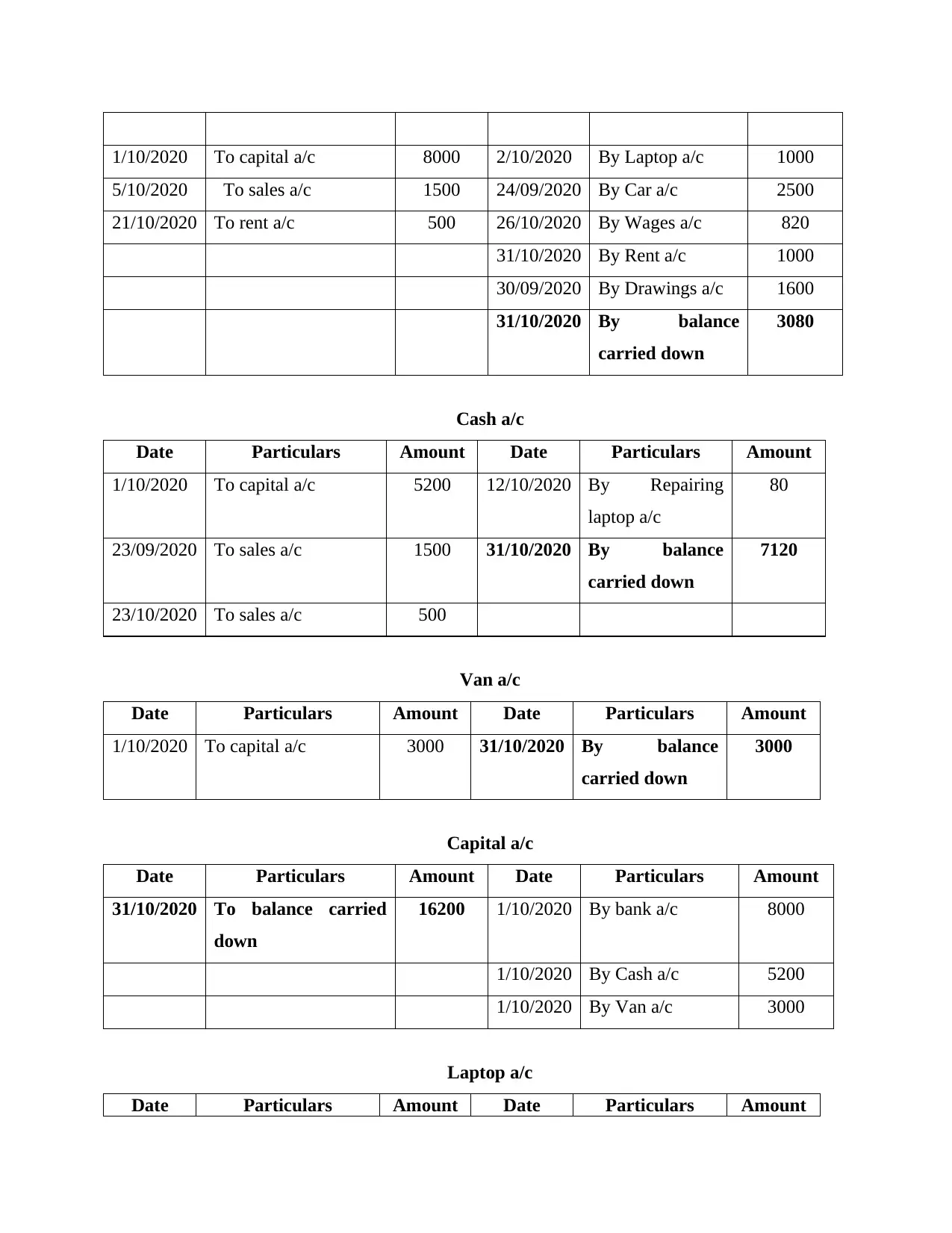

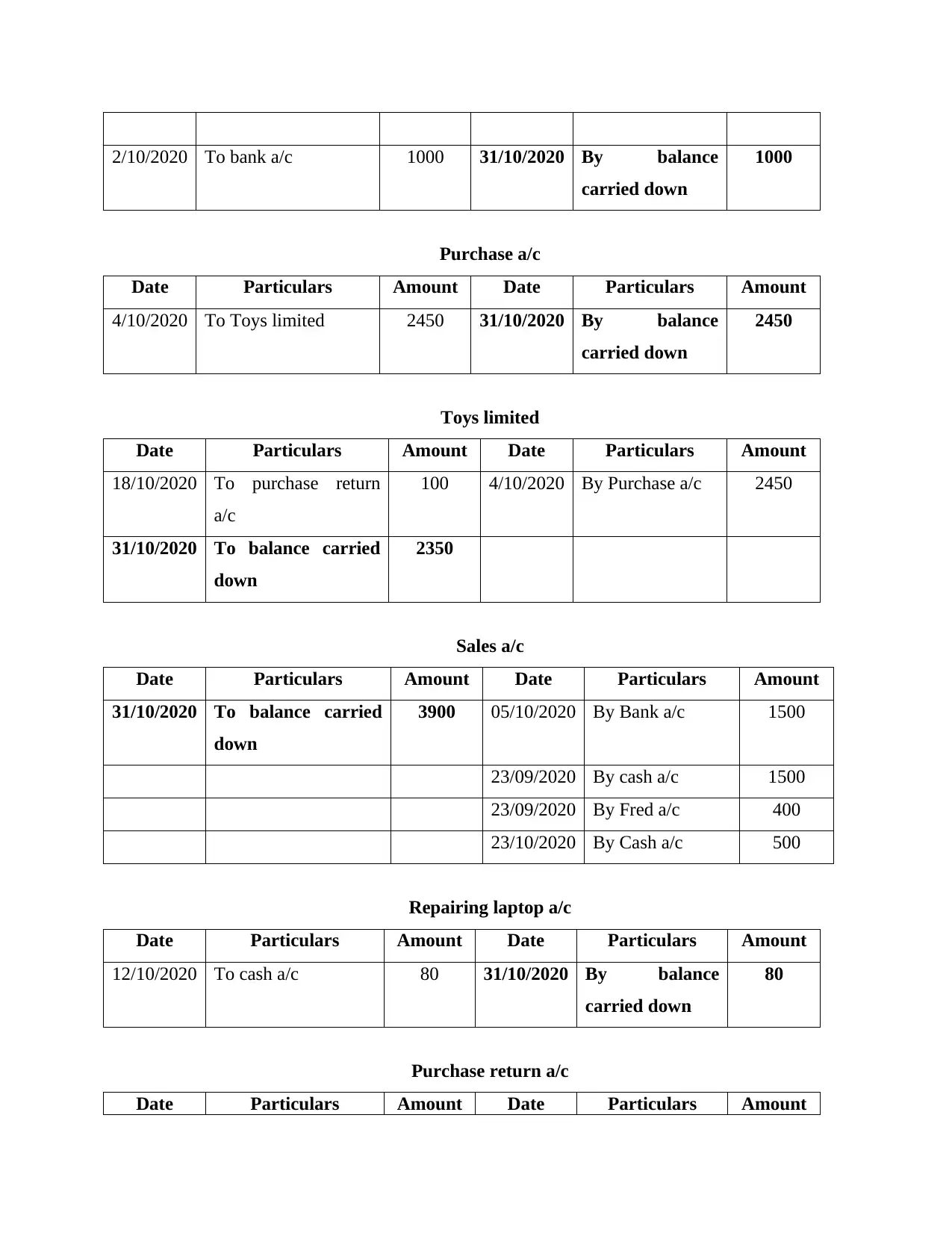

2. Balancing the accounts so as to bring down an opening balance

Bank a/c

Date Particulars Amount Date Particulars Amount

cash)

18/10/2020 Toys limited a/c DR

To purchase return a/c

(Being goods returned to Toys limited)

100

100

21/10/2020 Bank a/c DR

To rent a/c

(Being rent received)

500

500

23/09/2020 Cash a/c DR

Fred a/c DR

To sales a/c

(Being goods sold on cash and credit)

1500

400

1900

23/10/2020 Cash a/c DR

To sales a/c

(Being goods sold in cash)

500

500

24/09/2020 Car a/c DR

To bank a/c

(Being car purchased)

2500

2500

26/10/2020 Wages a/c DR

To bank a/c

(Being wages paid)

820

820

31/10/2020 Rent a/c DR

To bank a/c

(Being rent paid)

1000

1000

30/09/2020 Drawings a/c DR

To bank a/c

(being amount withdraw from bank for

holiday)

1600

1600

2. Balancing the accounts so as to bring down an opening balance

Bank a/c

Date Particulars Amount Date Particulars Amount

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1/10/2020 To capital a/c 8000 2/10/2020 By Laptop a/c 1000

5/10/2020 To sales a/c 1500 24/09/2020 By Car a/c 2500

21/10/2020 To rent a/c 500 26/10/2020 By Wages a/c 820

31/10/2020 By Rent a/c 1000

30/09/2020 By Drawings a/c 1600

31/10/2020 By balance

carried down

3080

Cash a/c

Date Particulars Amount Date Particulars Amount

1/10/2020 To capital a/c 5200 12/10/2020 By Repairing

laptop a/c

80

23/09/2020 To sales a/c 1500 31/10/2020 By balance

carried down

7120

23/10/2020 To sales a/c 500

Van a/c

Date Particulars Amount Date Particulars Amount

1/10/2020 To capital a/c 3000 31/10/2020 By balance

carried down

3000

Capital a/c

Date Particulars Amount Date Particulars Amount

31/10/2020 To balance carried

down

16200 1/10/2020 By bank a/c 8000

1/10/2020 By Cash a/c 5200

1/10/2020 By Van a/c 3000

Laptop a/c

Date Particulars Amount Date Particulars Amount

5/10/2020 To sales a/c 1500 24/09/2020 By Car a/c 2500

21/10/2020 To rent a/c 500 26/10/2020 By Wages a/c 820

31/10/2020 By Rent a/c 1000

30/09/2020 By Drawings a/c 1600

31/10/2020 By balance

carried down

3080

Cash a/c

Date Particulars Amount Date Particulars Amount

1/10/2020 To capital a/c 5200 12/10/2020 By Repairing

laptop a/c

80

23/09/2020 To sales a/c 1500 31/10/2020 By balance

carried down

7120

23/10/2020 To sales a/c 500

Van a/c

Date Particulars Amount Date Particulars Amount

1/10/2020 To capital a/c 3000 31/10/2020 By balance

carried down

3000

Capital a/c

Date Particulars Amount Date Particulars Amount

31/10/2020 To balance carried

down

16200 1/10/2020 By bank a/c 8000

1/10/2020 By Cash a/c 5200

1/10/2020 By Van a/c 3000

Laptop a/c

Date Particulars Amount Date Particulars Amount

2/10/2020 To bank a/c 1000 31/10/2020 By balance

carried down

1000

Purchase a/c

Date Particulars Amount Date Particulars Amount

4/10/2020 To Toys limited 2450 31/10/2020 By balance

carried down

2450

Toys limited

Date Particulars Amount Date Particulars Amount

18/10/2020 To purchase return

a/c

100 4/10/2020 By Purchase a/c 2450

31/10/2020 To balance carried

down

2350

Sales a/c

Date Particulars Amount Date Particulars Amount

31/10/2020 To balance carried

down

3900 05/10/2020 By Bank a/c 1500

23/09/2020 By cash a/c 1500

23/09/2020 By Fred a/c 400

23/10/2020 By Cash a/c 500

Repairing laptop a/c

Date Particulars Amount Date Particulars Amount

12/10/2020 To cash a/c 80 31/10/2020 By balance

carried down

80

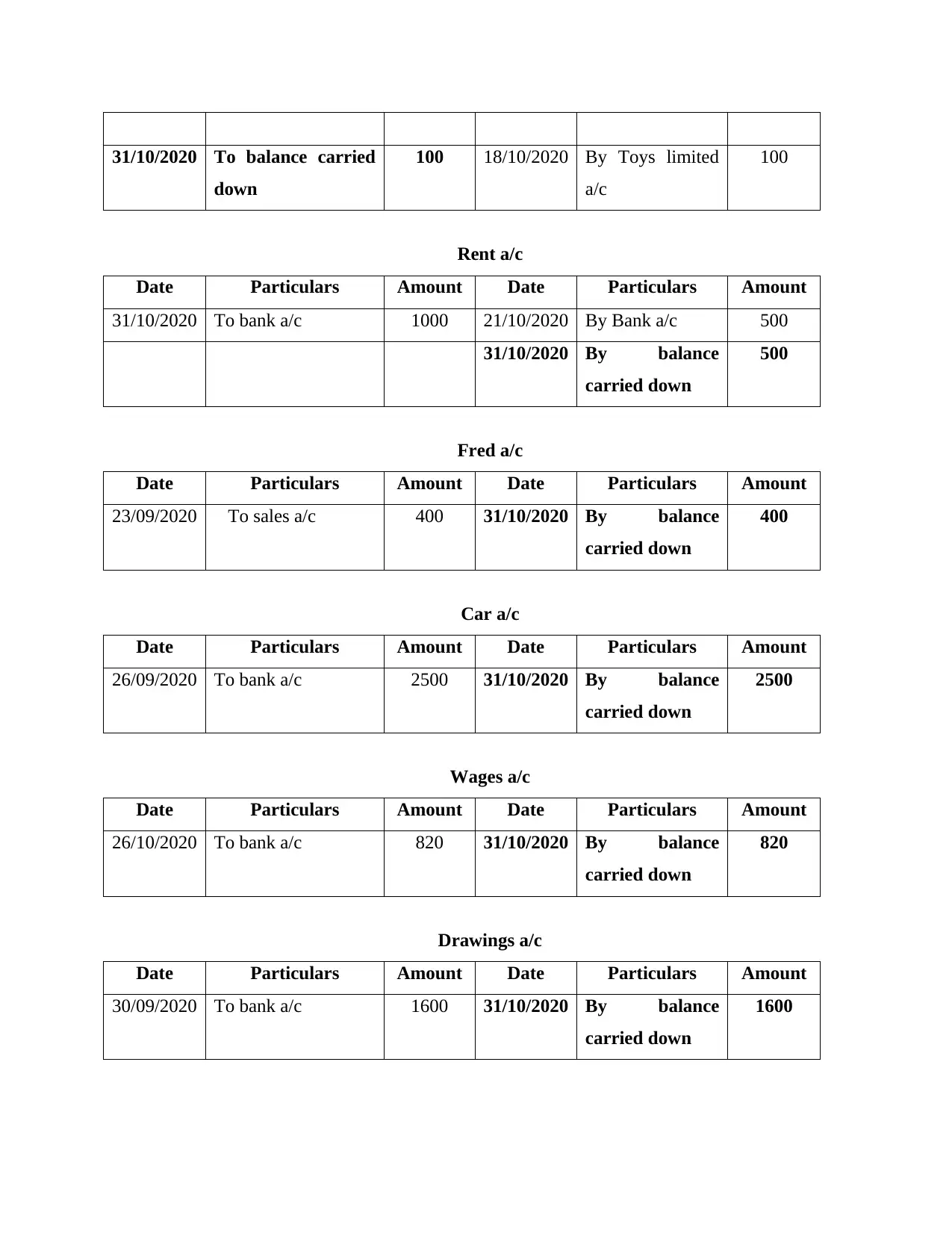

Purchase return a/c

Date Particulars Amount Date Particulars Amount

carried down

1000

Purchase a/c

Date Particulars Amount Date Particulars Amount

4/10/2020 To Toys limited 2450 31/10/2020 By balance

carried down

2450

Toys limited

Date Particulars Amount Date Particulars Amount

18/10/2020 To purchase return

a/c

100 4/10/2020 By Purchase a/c 2450

31/10/2020 To balance carried

down

2350

Sales a/c

Date Particulars Amount Date Particulars Amount

31/10/2020 To balance carried

down

3900 05/10/2020 By Bank a/c 1500

23/09/2020 By cash a/c 1500

23/09/2020 By Fred a/c 400

23/10/2020 By Cash a/c 500

Repairing laptop a/c

Date Particulars Amount Date Particulars Amount

12/10/2020 To cash a/c 80 31/10/2020 By balance

carried down

80

Purchase return a/c

Date Particulars Amount Date Particulars Amount

31/10/2020 To balance carried

down

100 18/10/2020 By Toys limited

a/c

100

Rent a/c

Date Particulars Amount Date Particulars Amount

31/10/2020 To bank a/c 1000 21/10/2020 By Bank a/c 500

31/10/2020 By balance

carried down

500

Fred a/c

Date Particulars Amount Date Particulars Amount

23/09/2020 To sales a/c 400 31/10/2020 By balance

carried down

400

Car a/c

Date Particulars Amount Date Particulars Amount

26/09/2020 To bank a/c 2500 31/10/2020 By balance

carried down

2500

Wages a/c

Date Particulars Amount Date Particulars Amount

26/10/2020 To bank a/c 820 31/10/2020 By balance

carried down

820

Drawings a/c

Date Particulars Amount Date Particulars Amount

30/09/2020 To bank a/c 1600 31/10/2020 By balance

carried down

1600

down

100 18/10/2020 By Toys limited

a/c

100

Rent a/c

Date Particulars Amount Date Particulars Amount

31/10/2020 To bank a/c 1000 21/10/2020 By Bank a/c 500

31/10/2020 By balance

carried down

500

Fred a/c

Date Particulars Amount Date Particulars Amount

23/09/2020 To sales a/c 400 31/10/2020 By balance

carried down

400

Car a/c

Date Particulars Amount Date Particulars Amount

26/09/2020 To bank a/c 2500 31/10/2020 By balance

carried down

2500

Wages a/c

Date Particulars Amount Date Particulars Amount

26/10/2020 To bank a/c 820 31/10/2020 By balance

carried down

820

Drawings a/c

Date Particulars Amount Date Particulars Amount

30/09/2020 To bank a/c 1600 31/10/2020 By balance

carried down

1600

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

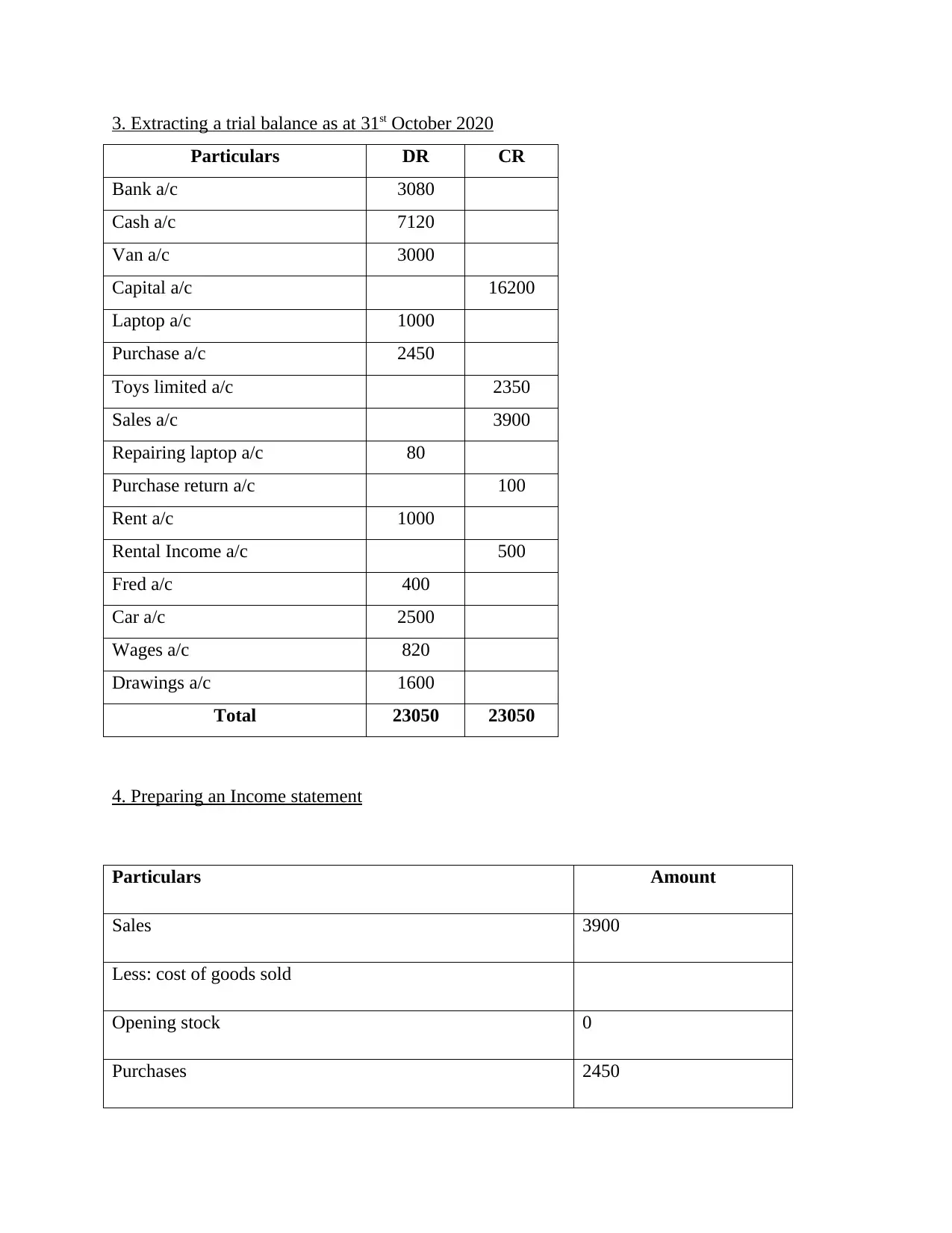

3. Extracting a trial balance as at 31st October 2020

Particulars DR CR

Bank a/c 3080

Cash a/c 7120

Van a/c 3000

Capital a/c 16200

Laptop a/c 1000

Purchase a/c 2450

Toys limited a/c 2350

Sales a/c 3900

Repairing laptop a/c 80

Purchase return a/c 100

Rent a/c 1000

Rental Income a/c 500

Fred a/c 400

Car a/c 2500

Wages a/c 820

Drawings a/c 1600

Total 23050 23050

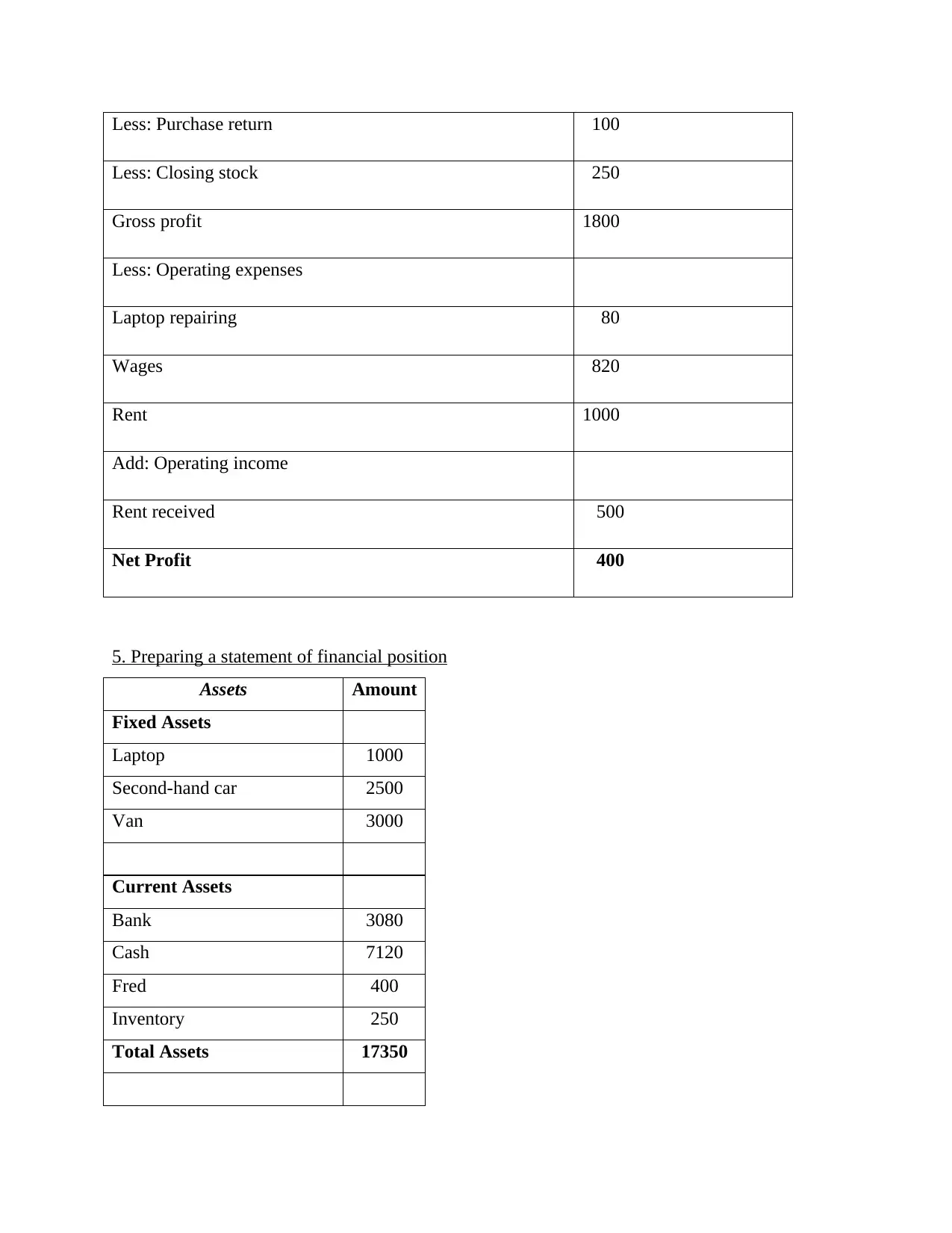

4. Preparing an Income statement

Particulars Amount

Sales 3900

Less: cost of goods sold

Opening stock 0

Purchases 2450

Particulars DR CR

Bank a/c 3080

Cash a/c 7120

Van a/c 3000

Capital a/c 16200

Laptop a/c 1000

Purchase a/c 2450

Toys limited a/c 2350

Sales a/c 3900

Repairing laptop a/c 80

Purchase return a/c 100

Rent a/c 1000

Rental Income a/c 500

Fred a/c 400

Car a/c 2500

Wages a/c 820

Drawings a/c 1600

Total 23050 23050

4. Preparing an Income statement

Particulars Amount

Sales 3900

Less: cost of goods sold

Opening stock 0

Purchases 2450

Less: Purchase return 100

Less: Closing stock 250

Gross profit 1800

Less: Operating expenses

Laptop repairing 80

Wages 820

Rent 1000

Add: Operating income

Rent received 500

Net Profit 400

5. Preparing a statement of financial position

Assets Amount

Fixed Assets

Laptop 1000

Second-hand car 2500

Van 3000

Current Assets

Bank 3080

Cash 7120

Fred 400

Inventory 250

Total Assets 17350

Less: Closing stock 250

Gross profit 1800

Less: Operating expenses

Laptop repairing 80

Wages 820

Rent 1000

Add: Operating income

Rent received 500

Net Profit 400

5. Preparing a statement of financial position

Assets Amount

Fixed Assets

Laptop 1000

Second-hand car 2500

Van 3000

Current Assets

Bank 3080

Cash 7120

Fred 400

Inventory 250

Total Assets 17350

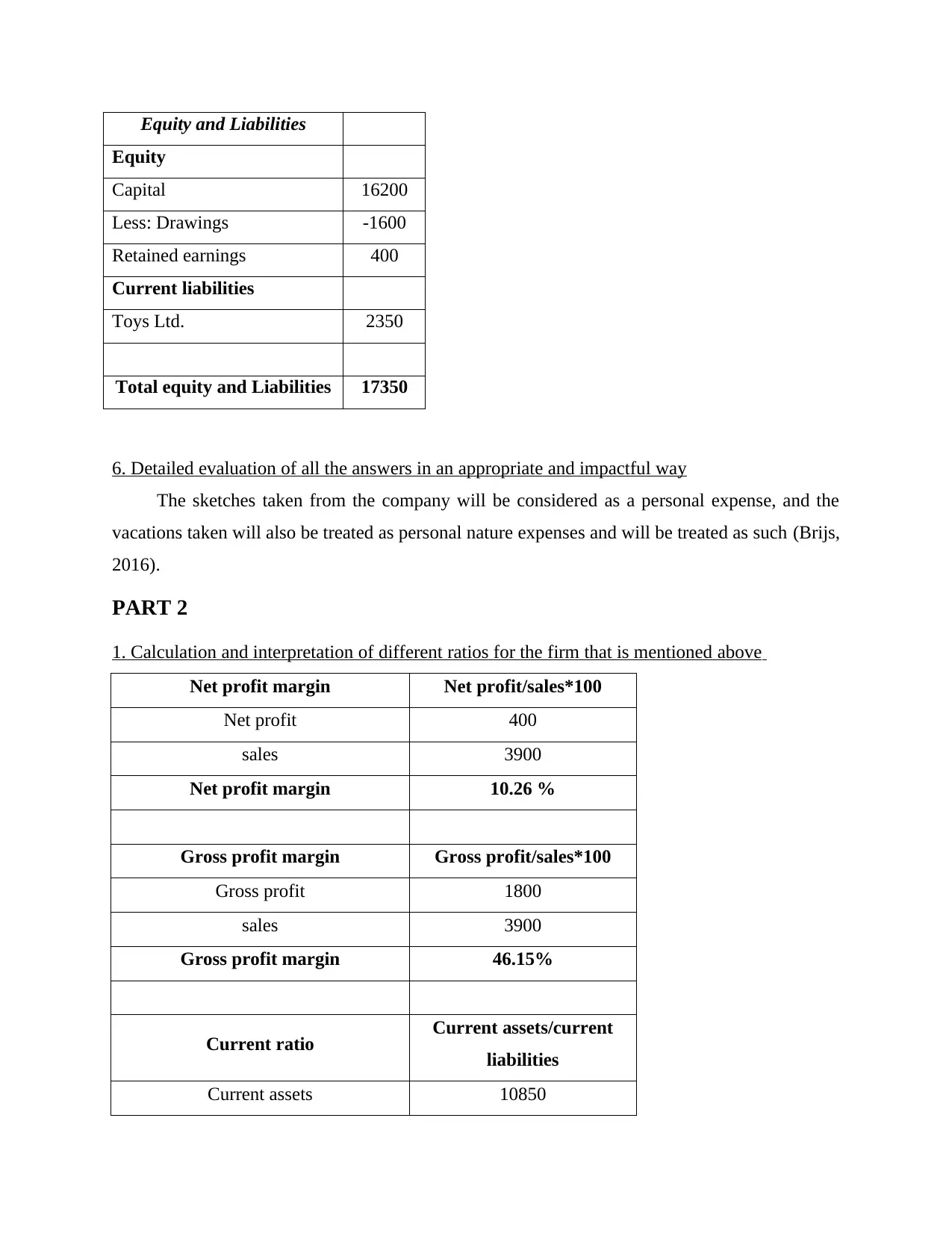

Equity and Liabilities

Equity

Capital 16200

Less: Drawings -1600

Retained earnings 400

Current liabilities

Toys Ltd. 2350

Total equity and Liabilities 17350

6. Detailed evaluation of all the answers in an appropriate and impactful way

The sketches taken from the company will be considered as a personal expense, and the

vacations taken will also be treated as personal nature expenses and will be treated as such (Brijs,

2016).

PART 2

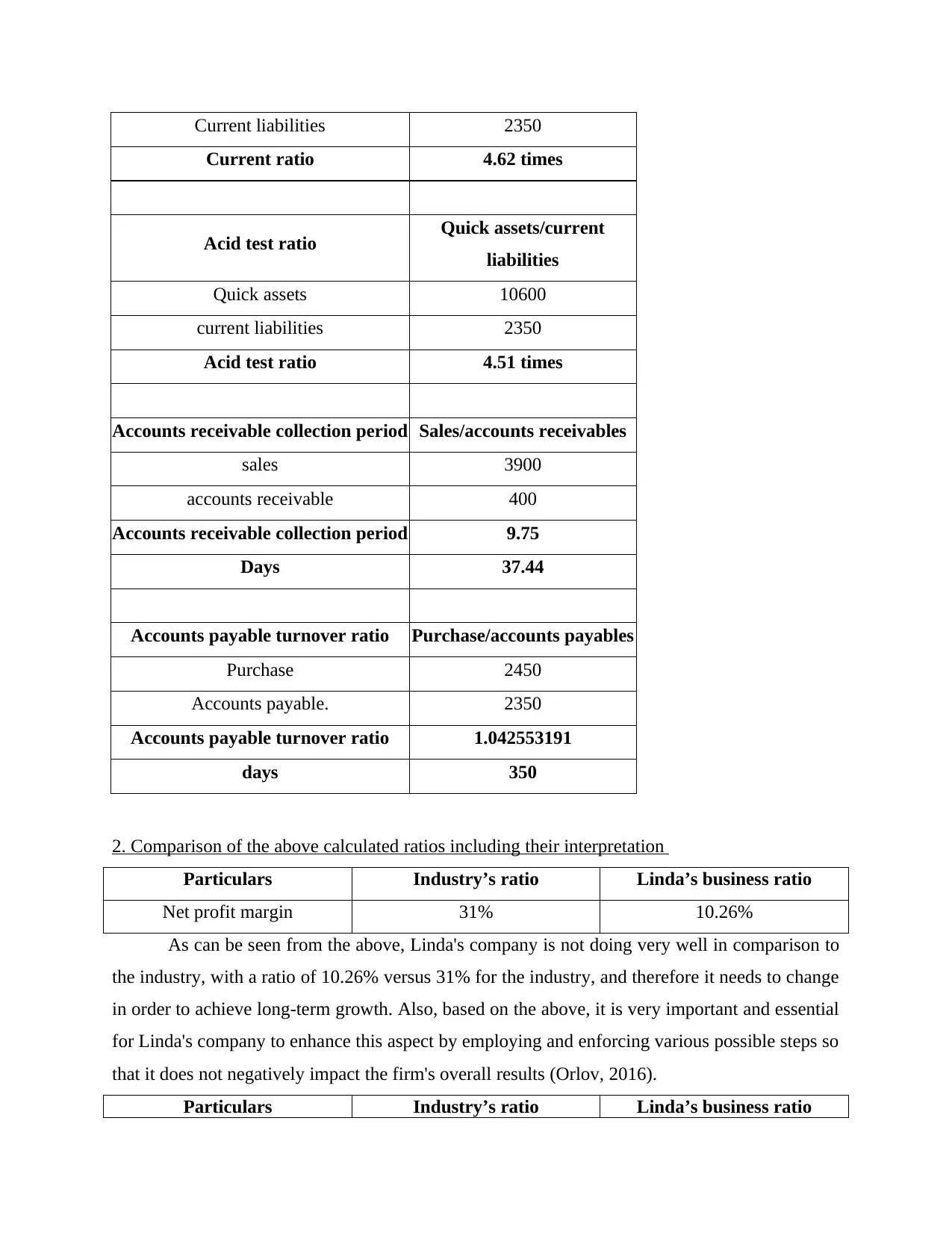

1. Calculation and interpretation of different ratios for the firm that is mentioned above

Net profit margin Net profit/sales*100

Net profit 400

sales 3900

Net profit margin 10.26 %

Gross profit margin Gross profit/sales*100

Gross profit 1800

sales 3900

Gross profit margin 46.15%

Current ratio Current assets/current

liabilities

Current assets 10850

Equity

Capital 16200

Less: Drawings -1600

Retained earnings 400

Current liabilities

Toys Ltd. 2350

Total equity and Liabilities 17350

6. Detailed evaluation of all the answers in an appropriate and impactful way

The sketches taken from the company will be considered as a personal expense, and the

vacations taken will also be treated as personal nature expenses and will be treated as such (Brijs,

2016).

PART 2

1. Calculation and interpretation of different ratios for the firm that is mentioned above

Net profit margin Net profit/sales*100

Net profit 400

sales 3900

Net profit margin 10.26 %

Gross profit margin Gross profit/sales*100

Gross profit 1800

sales 3900

Gross profit margin 46.15%

Current ratio Current assets/current

liabilities

Current assets 10850

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Current liabilities 2350

Current ratio 4.62 times

Acid test ratio Quick assets/current

liabilities

Quick assets 10600

current liabilities 2350

Acid test ratio 4.51 times

Accounts receivable collection period Sales/accounts receivables

sales 3900

accounts receivable 400

Accounts receivable collection period 9.75

Days 37.44

Accounts payable turnover ratio Purchase/accounts payables

Purchase 2450

Accounts payable. 2350

Accounts payable turnover ratio 1.042553191

days 350

2. Comparison of the above calculated ratios including their interpretation

Particulars Industry’s ratio Linda’s business ratio

Net profit margin 31% 10.26%

As can be seen from the above, Linda's company is not doing very well in comparison to

the industry, with a ratio of 10.26% versus 31% for the industry, and therefore it needs to change

in order to achieve long-term growth. Also, based on the above, it is very important and essential

for Linda's company to enhance this aspect by employing and enforcing various possible steps so

that it does not negatively impact the firm's overall results (Orlov, 2016).

Particulars Industry’s ratio Linda’s business ratio

Current ratio 4.62 times

Acid test ratio Quick assets/current

liabilities

Quick assets 10600

current liabilities 2350

Acid test ratio 4.51 times

Accounts receivable collection period Sales/accounts receivables

sales 3900

accounts receivable 400

Accounts receivable collection period 9.75

Days 37.44

Accounts payable turnover ratio Purchase/accounts payables

Purchase 2450

Accounts payable. 2350

Accounts payable turnover ratio 1.042553191

days 350

2. Comparison of the above calculated ratios including their interpretation

Particulars Industry’s ratio Linda’s business ratio

Net profit margin 31% 10.26%

As can be seen from the above, Linda's company is not doing very well in comparison to

the industry, with a ratio of 10.26% versus 31% for the industry, and therefore it needs to change

in order to achieve long-term growth. Also, based on the above, it is very important and essential

for Linda's company to enhance this aspect by employing and enforcing various possible steps so

that it does not negatively impact the firm's overall results (Orlov, 2016).

Particulars Industry’s ratio Linda’s business ratio

Gross profit margin 54% 46.15%

This ratio is almost identical in both, but Linda's business is still lagging behind, with a

ratio of 46.15 percent compared to 54 percent for the industry. Although this small margin is

often overlooked, it is critical for the above listed company to increase these ratios in order to

expand and succeed in a highly competitive and diverse industry (Pipattanasomporn, Kuzlu and

Rahman, 2018).

Particulars Industry’s ratio Linda’s business ratio

Current ratio 2.87 times 4.62 times

Linda's company has performed extremely well in this regard, with a high ratio of 4.62

times compared to the industry's 2.87 times. This ratio aids in assessing an enterprise's short-term

paying potential, and Linda's company has done an outstanding job in this regard, which is one

of the reasons for its enormous business success.

Particulars Industry’s ratio Linda’s business ratio

Quick ratio 1.35 times 4.51 times

Linda's company is also doing well in the industry, with a 4.51 times return compared to

1.35 times. Similarly to the previous ratio, the firm has performed admirably in this one,

indicating that it has a high repayment potential (Reid, 2020).

Particulars Industry’s ratio Linda’s business ratio

Account receivable days 50 days 37 days

Linda's company collects the money owed within a short period of time, on average 37

days versus 50 days for the industry, indicating that the former is doing a good job of recovering

money from its debtors and, as a result, it is also useful in maintaining the supply chain, which is

critical in the current situation.

Particulars Industry’s ratio Linda’s business ratio

Account payable days 72 days 350 days

Linda's company keeps the money from creditors for a longer period of time, which adds to

the firm's value, as its average is 350 days, compared to the industry's average of 72 days. The

money that is kept can be reinvested in a place that will yield higher returns, which will benefit

the firm in the long run (Ryu and Kim, 2016).

This ratio is almost identical in both, but Linda's business is still lagging behind, with a

ratio of 46.15 percent compared to 54 percent for the industry. Although this small margin is

often overlooked, it is critical for the above listed company to increase these ratios in order to

expand and succeed in a highly competitive and diverse industry (Pipattanasomporn, Kuzlu and

Rahman, 2018).

Particulars Industry’s ratio Linda’s business ratio

Current ratio 2.87 times 4.62 times

Linda's company has performed extremely well in this regard, with a high ratio of 4.62

times compared to the industry's 2.87 times. This ratio aids in assessing an enterprise's short-term

paying potential, and Linda's company has done an outstanding job in this regard, which is one

of the reasons for its enormous business success.

Particulars Industry’s ratio Linda’s business ratio

Quick ratio 1.35 times 4.51 times

Linda's company is also doing well in the industry, with a 4.51 times return compared to

1.35 times. Similarly to the previous ratio, the firm has performed admirably in this one,

indicating that it has a high repayment potential (Reid, 2020).

Particulars Industry’s ratio Linda’s business ratio

Account receivable days 50 days 37 days

Linda's company collects the money owed within a short period of time, on average 37

days versus 50 days for the industry, indicating that the former is doing a good job of recovering

money from its debtors and, as a result, it is also useful in maintaining the supply chain, which is

critical in the current situation.

Particulars Industry’s ratio Linda’s business ratio

Account payable days 72 days 350 days

Linda's company keeps the money from creditors for a longer period of time, which adds to

the firm's value, as its average is 350 days, compared to the industry's average of 72 days. The

money that is kept can be reinvested in a place that will yield higher returns, which will benefit

the firm in the long run (Ryu and Kim, 2016).

Overall analysis- Overall, Linda's business is doing a decent job in the market, but there is

always room for improvement, which will help it develop as a company in the long run. Apart

from that, the company is far ahead of its competitors operating in similar market conditions,

which is a very positive sign for the company because it shows that it can effectively and

efficiently withstand and survive the current market conditions (Turner, Weickgenannt and

Copeland, 2016).

CONCLUSION

From the foregoing, it can be concluded that the aforementioned business firm is well-

positioned in the market and is performing admirably in the industry in which it operates. Apart

from that, it can be concluded that if additional measures are taken in the operation of Linda's

business, it will flourish in the current market conditions in an excellent way, as its current

position is far superior to that of its competitors in the same industry.

always room for improvement, which will help it develop as a company in the long run. Apart

from that, the company is far ahead of its competitors operating in similar market conditions,

which is a very positive sign for the company because it shows that it can effectively and

efficiently withstand and survive the current market conditions (Turner, Weickgenannt and

Copeland, 2016).

CONCLUSION

From the foregoing, it can be concluded that the aforementioned business firm is well-

positioned in the market and is performing admirably in the industry in which it operates. Apart

from that, it can be concluded that if additional measures are taken in the operation of Linda's

business, it will flourish in the current market conditions in an excellent way, as its current

position is far superior to that of its competitors in the same industry.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and journals

Barry, N., 2016. Business ethics. Springer.

Brijs, B., 2016. Business analysis for business intelligence. CRC Press.

Orlov, V., 2016. Introduction to business law in Russia. Routledge.

Pipattanasomporn, M., Kuzlu, M. and Rahman, S., 2018, October. A blockchain-based platform

for exchange of solar energy: Laboratory-scale implementation. In 2018 International

Conference and Utility Exhibition on Green Energy for Sustainable Development

(ICUE) (pp. 1-9). IEEE.

Reid, W., 2020. The meaning of company accounts. Routledge.

Ryu, S. and Kim, Y.G., 2016. A typology of crowdfunding sponsors: Birds of a feather flock

together?. Electronic Commerce Research and Applications, 16, pp.43-54.

Turner, L., Weickgenannt, A.B. and Copeland, M.K., 2016. Accounting information systems: the

processes and controls. John Wiley & Sons.

Books and journals

Barry, N., 2016. Business ethics. Springer.

Brijs, B., 2016. Business analysis for business intelligence. CRC Press.

Orlov, V., 2016. Introduction to business law in Russia. Routledge.

Pipattanasomporn, M., Kuzlu, M. and Rahman, S., 2018, October. A blockchain-based platform

for exchange of solar energy: Laboratory-scale implementation. In 2018 International

Conference and Utility Exhibition on Green Energy for Sustainable Development

(ICUE) (pp. 1-9). IEEE.

Reid, W., 2020. The meaning of company accounts. Routledge.

Ryu, S. and Kim, Y.G., 2016. A typology of crowdfunding sponsors: Birds of a feather flock

together?. Electronic Commerce Research and Applications, 16, pp.43-54.

Turner, L., Weickgenannt, A.B. and Copeland, M.K., 2016. Accounting information systems: the

processes and controls. John Wiley & Sons.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.