Recording Business Transaction

VerifiedAdded on 2022/12/26

|20

|2774

|34

AI Summary

This report discusses the process of recording business transactions and its importance in accounting. It covers topics such as journal entries, ledger, trial balance, income statement, balance sheet, and the evaluation of financial performance using ratios. The report also includes a special note on drawing accounts. The content is relevant for students studying accounting and finance.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Recording Business Transaction

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

A) Journal entries.........................................................................................................................3

B) Ledger.....................................................................................................................................6

C) Trial balance..........................................................................................................................10

D) Income statement..................................................................................................................10

E) Balance sheet.........................................................................................................................11

F) Special note regarding drawing account...............................................................................12

PART B..........................................................................................................................................13

Calculation of ratio....................................................................................................................13

Evaluation of financial performance of Linda's organization....................................................14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................17

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

A) Journal entries.........................................................................................................................3

B) Ledger.....................................................................................................................................6

C) Trial balance..........................................................................................................................10

D) Income statement..................................................................................................................10

E) Balance sheet.........................................................................................................................11

F) Special note regarding drawing account...............................................................................12

PART B..........................................................................................................................................13

Calculation of ratio....................................................................................................................13

Evaluation of financial performance of Linda's organization....................................................14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................17

INTRODUCTION

Recording business transaction is procedure in which accountant, analysis, collect, and

record each business activity in tabular format to show their monetary value. This report has

been formulated to define the relevance of accoutring approach, by solving Linda's case study. In

includes, how business operations record in the form of journal and then they classified in ledger

account, on the basis of that to find out error trial balance has been format, and it proved base to

prepare financial statement. In this report to compare performance of Linda's organization with

industry different types of ratios used to measure the performance.

PART A

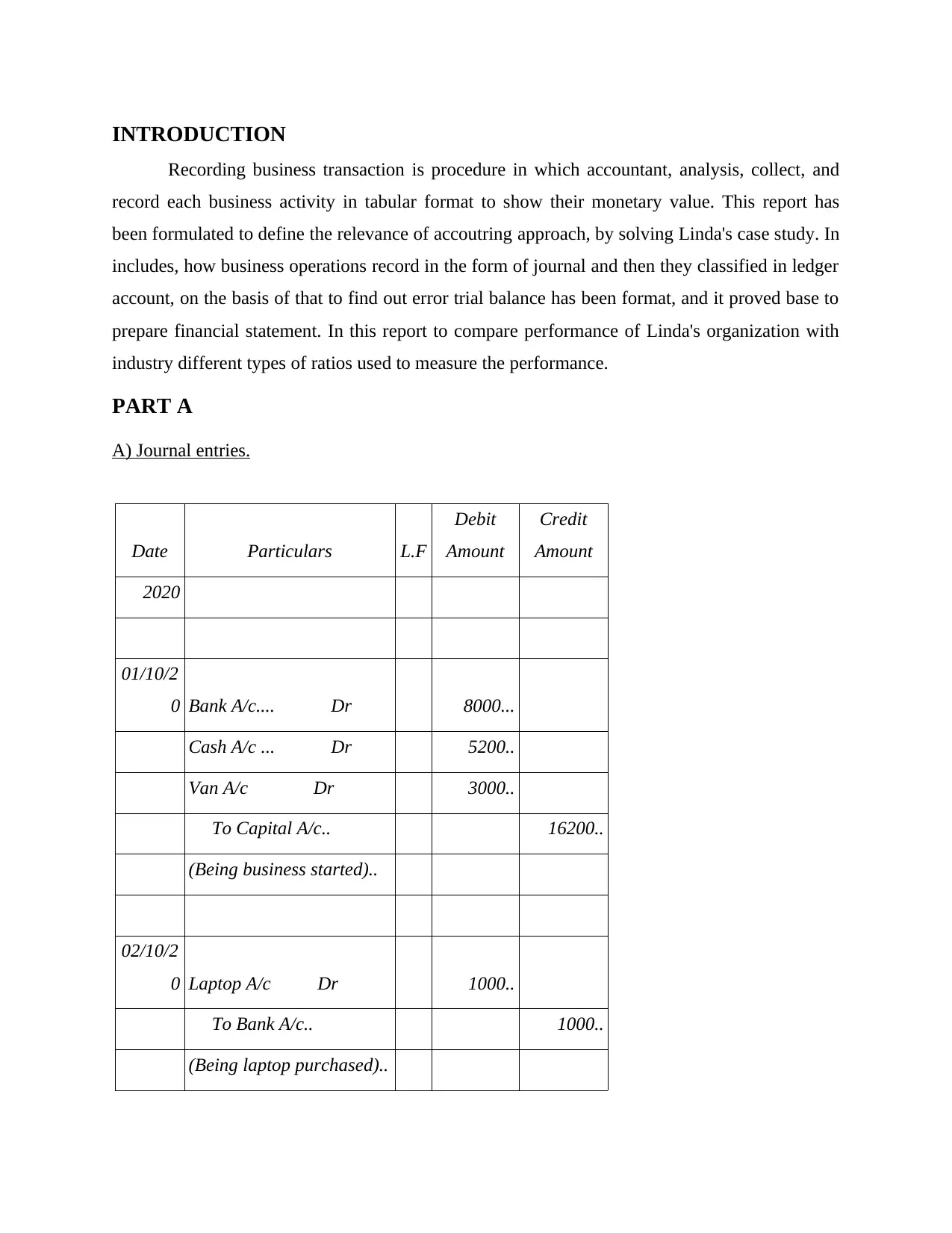

A) Journal entries.

Date Particulars L.F

Debit

Amount

Credit

Amount

2020

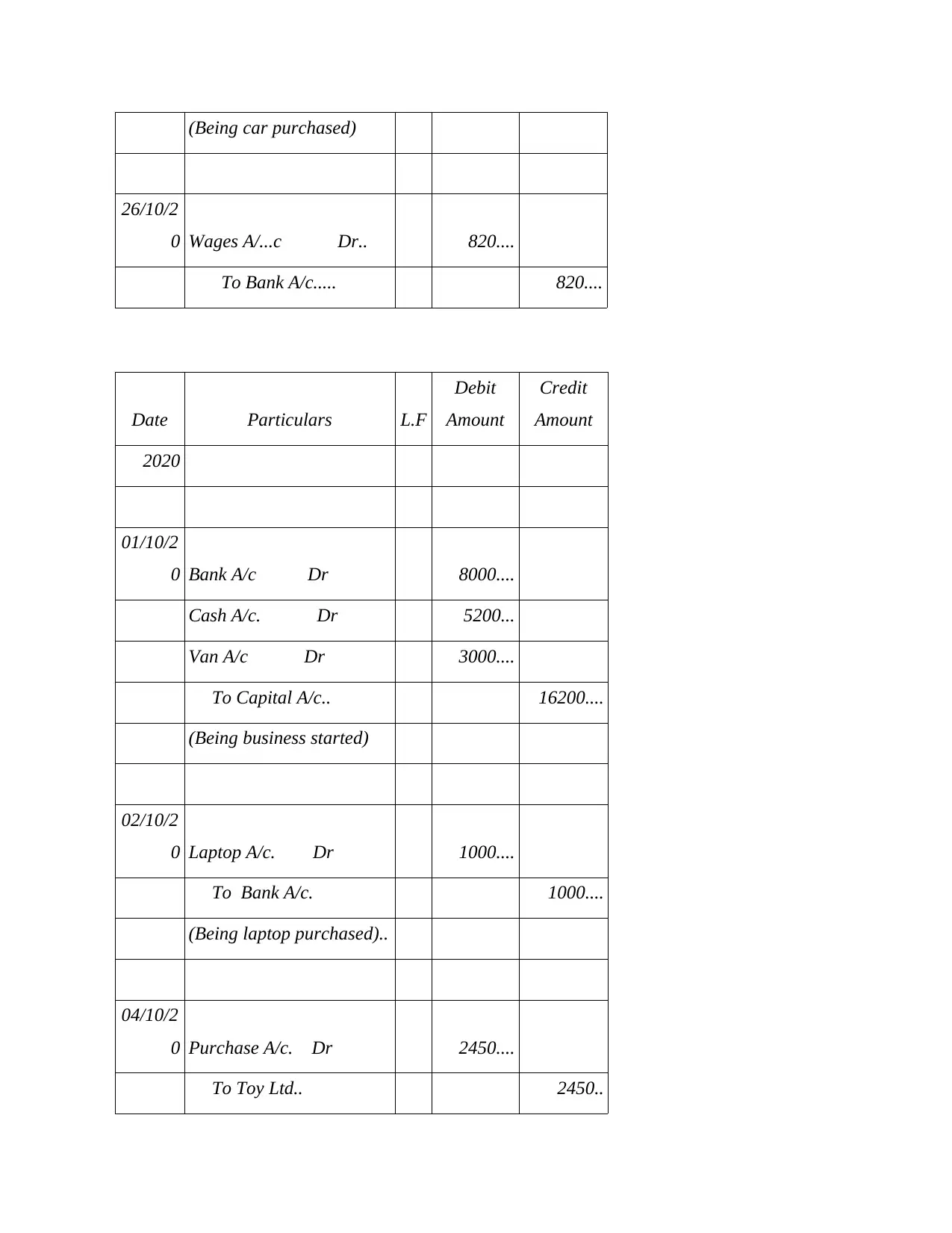

01/10/2

0 Bank A/c.... Dr 8000...

Cash A/c ... Dr 5200..

Van A/c Dr 3000..

To Capital A/c.. 16200..

(Being business started)..

02/10/2

0 Laptop A/c Dr 1000..

To Bank A/c.. 1000..

(Being laptop purchased)..

Recording business transaction is procedure in which accountant, analysis, collect, and

record each business activity in tabular format to show their monetary value. This report has

been formulated to define the relevance of accoutring approach, by solving Linda's case study. In

includes, how business operations record in the form of journal and then they classified in ledger

account, on the basis of that to find out error trial balance has been format, and it proved base to

prepare financial statement. In this report to compare performance of Linda's organization with

industry different types of ratios used to measure the performance.

PART A

A) Journal entries.

Date Particulars L.F

Debit

Amount

Credit

Amount

2020

01/10/2

0 Bank A/c.... Dr 8000...

Cash A/c ... Dr 5200..

Van A/c Dr 3000..

To Capital A/c.. 16200..

(Being business started)..

02/10/2

0 Laptop A/c Dr 1000..

To Bank A/c.. 1000..

(Being laptop purchased)..

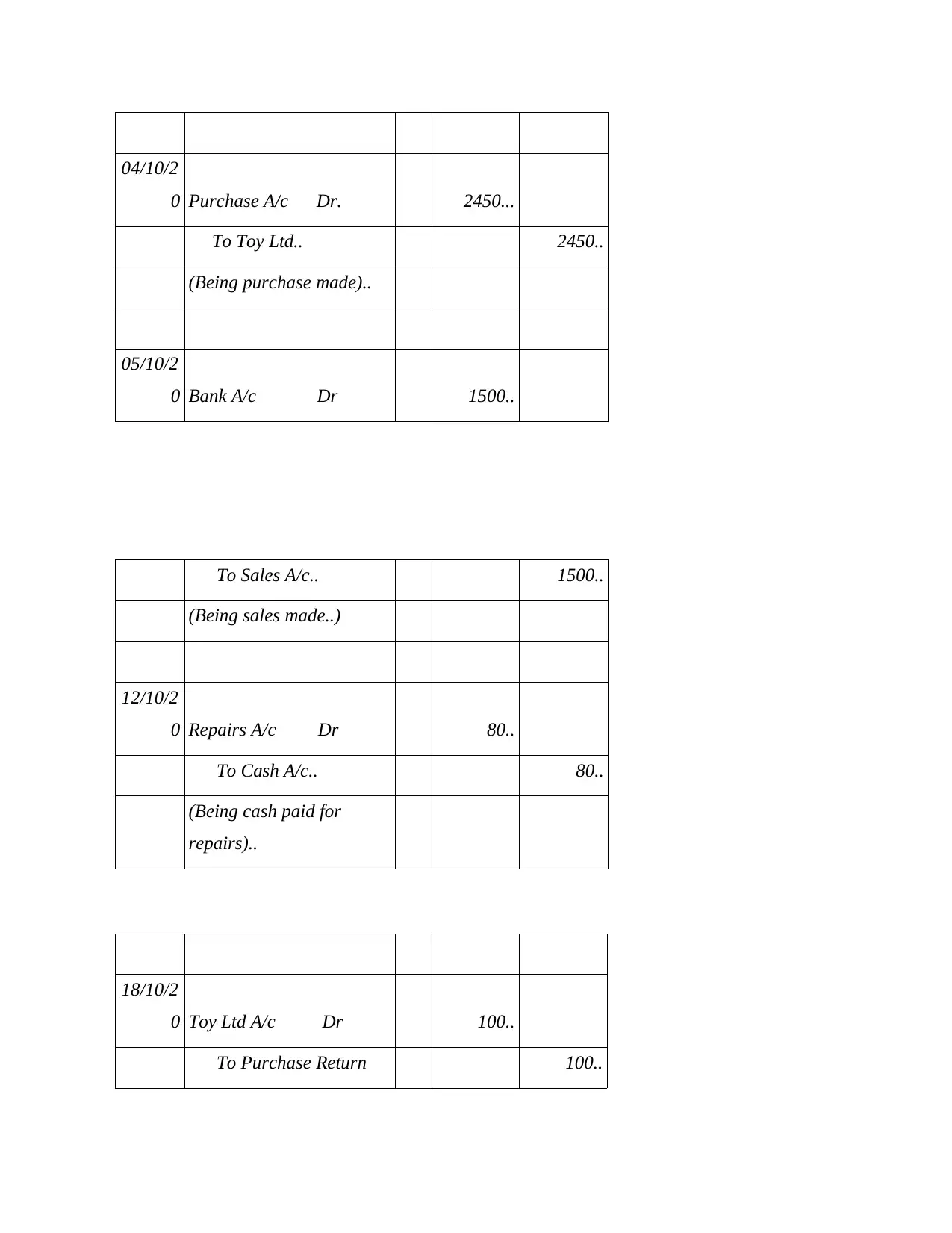

04/10/2

0 Purchase A/c Dr. 2450...

To Toy Ltd.. 2450..

(Being purchase made)..

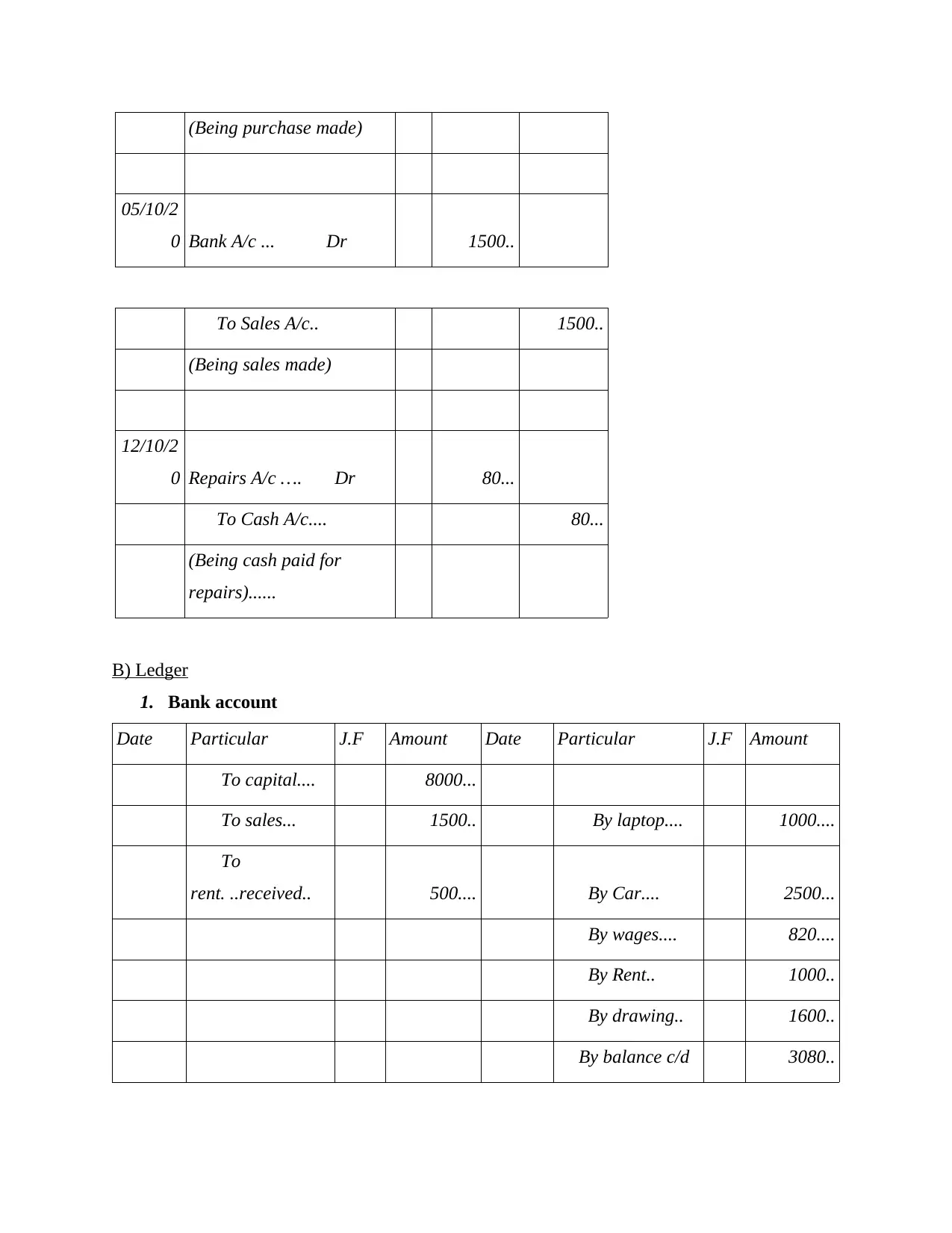

05/10/2

0 Bank A/c Dr 1500..

To Sales A/c.. 1500..

(Being sales made..)

12/10/2

0 Repairs A/c Dr 80..

To Cash A/c.. 80..

(Being cash paid for

repairs)..

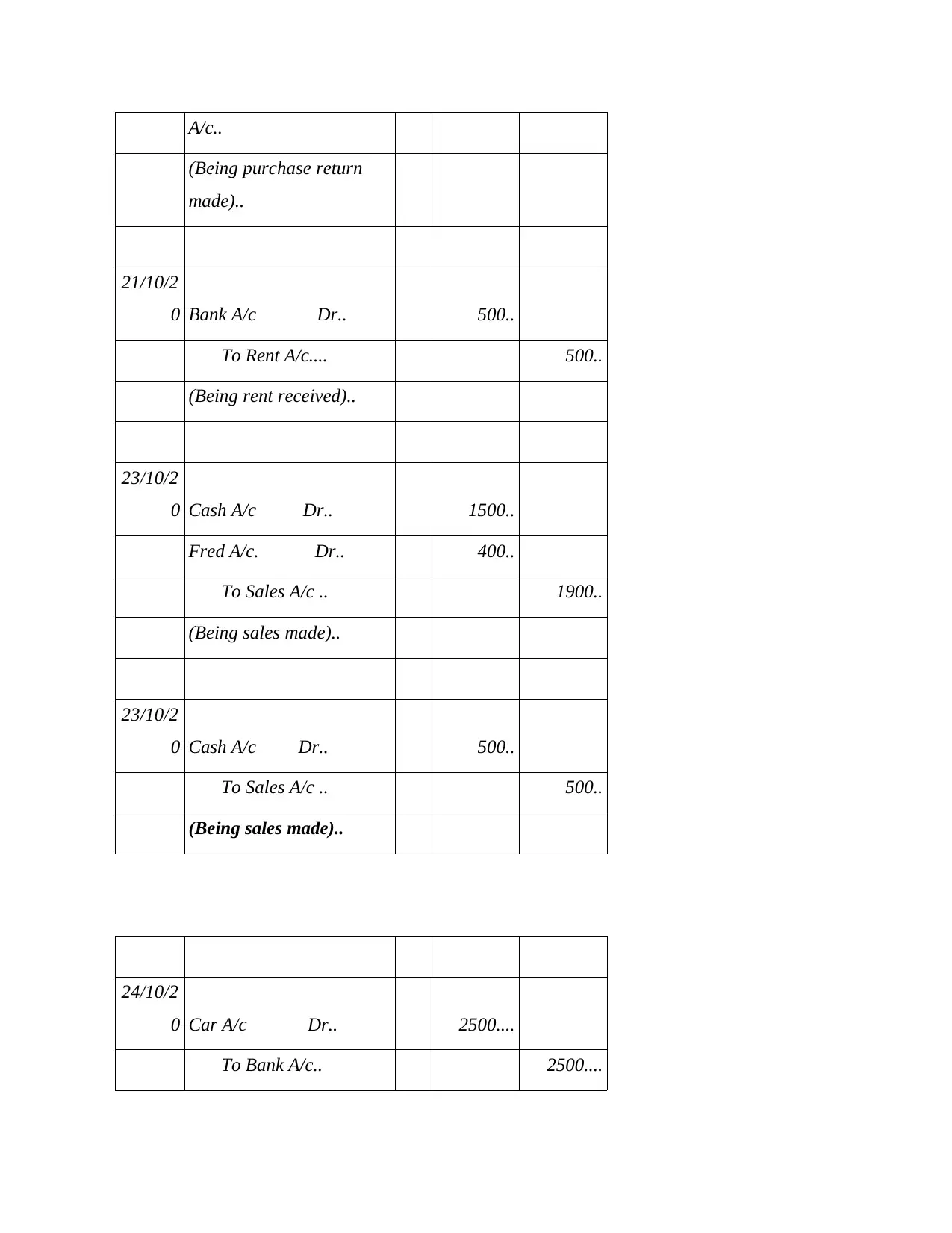

18/10/2

0 Toy Ltd A/c Dr 100..

To Purchase Return 100..

0 Purchase A/c Dr. 2450...

To Toy Ltd.. 2450..

(Being purchase made)..

05/10/2

0 Bank A/c Dr 1500..

To Sales A/c.. 1500..

(Being sales made..)

12/10/2

0 Repairs A/c Dr 80..

To Cash A/c.. 80..

(Being cash paid for

repairs)..

18/10/2

0 Toy Ltd A/c Dr 100..

To Purchase Return 100..

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

A/c..

(Being purchase return

made)..

21/10/2

0 Bank A/c Dr.. 500..

To Rent A/c.... 500..

(Being rent received)..

23/10/2

0 Cash A/c Dr.. 1500..

Fred A/c. Dr.. 400..

To Sales A/c .. 1900..

(Being sales made)..

23/10/2

0 Cash A/c Dr.. 500..

To Sales A/c .. 500..

(Being sales made)..

24/10/2

0 Car A/c Dr.. 2500....

To Bank A/c.. 2500....

(Being purchase return

made)..

21/10/2

0 Bank A/c Dr.. 500..

To Rent A/c.... 500..

(Being rent received)..

23/10/2

0 Cash A/c Dr.. 1500..

Fred A/c. Dr.. 400..

To Sales A/c .. 1900..

(Being sales made)..

23/10/2

0 Cash A/c Dr.. 500..

To Sales A/c .. 500..

(Being sales made)..

24/10/2

0 Car A/c Dr.. 2500....

To Bank A/c.. 2500....

(Being car purchased)

26/10/2

0 Wages A/...c Dr.. 820....

To Bank A/c..... 820....

Date Particulars L.F

Debit

Amount

Credit

Amount

2020

01/10/2

0 Bank A/c Dr 8000....

Cash A/c. Dr 5200...

Van A/c Dr 3000....

To Capital A/c.. 16200....

(Being business started)

02/10/2

0 Laptop A/c. Dr 1000....

To Bank A/c. 1000....

(Being laptop purchased)..

04/10/2

0 Purchase A/c. Dr 2450....

To Toy Ltd.. 2450..

26/10/2

0 Wages A/...c Dr.. 820....

To Bank A/c..... 820....

Date Particulars L.F

Debit

Amount

Credit

Amount

2020

01/10/2

0 Bank A/c Dr 8000....

Cash A/c. Dr 5200...

Van A/c Dr 3000....

To Capital A/c.. 16200....

(Being business started)

02/10/2

0 Laptop A/c. Dr 1000....

To Bank A/c. 1000....

(Being laptop purchased)..

04/10/2

0 Purchase A/c. Dr 2450....

To Toy Ltd.. 2450..

(Being purchase made)

05/10/2

0 Bank A/c ... Dr 1500..

To Sales A/c.. 1500..

(Being sales made)

12/10/2

0 Repairs A/c …. Dr 80...

To Cash A/c.... 80...

(Being cash paid for

repairs)......

B) Ledger

1. Bank account

Date Particular J.F Amount Date Particular J.F Amount

…...To capital.... 8000...

…...To sales... 1500.. …....By laptop.... 1000....

…...To

rent. ..received.. 500.... …...By Car.... 2500...

…...By wages.... 820....

…...By Rent.. 1000..

…...By drawing.. 1600..

….By balance c/d 3080..

05/10/2

0 Bank A/c ... Dr 1500..

To Sales A/c.. 1500..

(Being sales made)

12/10/2

0 Repairs A/c …. Dr 80...

To Cash A/c.... 80...

(Being cash paid for

repairs)......

B) Ledger

1. Bank account

Date Particular J.F Amount Date Particular J.F Amount

…...To capital.... 8000...

…...To sales... 1500.. …....By laptop.... 1000....

…...To

rent. ..received.. 500.... …...By Car.... 2500...

…...By wages.... 820....

…...By Rent.. 1000..

…...By drawing.. 1600..

….By balance c/d 3080..

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

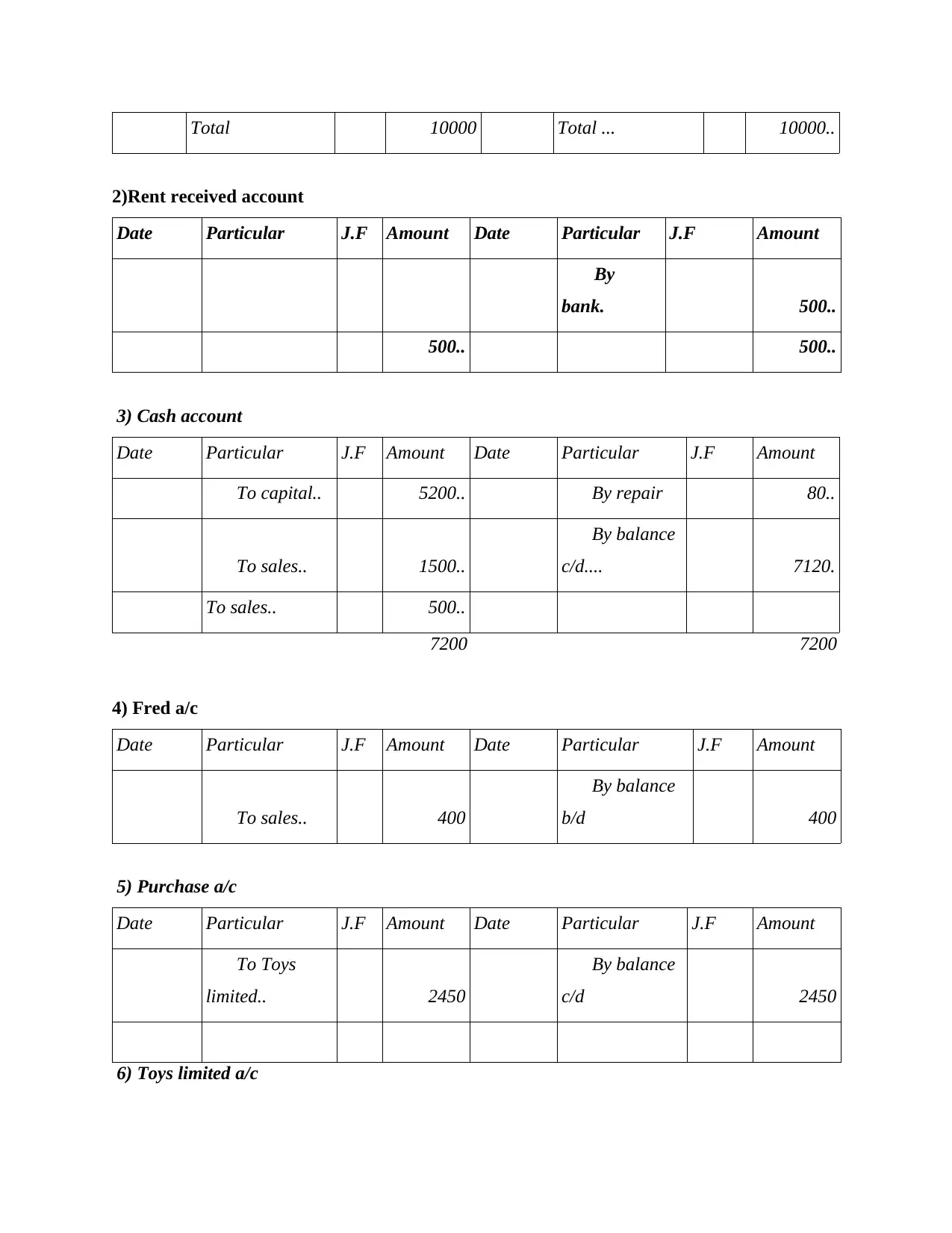

Total 10000 Total ... 10000..

2)Rent received account

Date Particular J.F Amount Date Particular J.F Amount

…...By

bank. 500..

500.. 500..

3) Cash account

Date Particular J.F Amount Date Particular J.F Amount

…...To capital.. 5200.. …...By repair 80..

…...To sales.. 1500..

…...By balance

c/d.... 7120.

To sales.. 500..

7200 7200

4) Fred a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To sales.. 400

…...By balance

b/d 400

5) Purchase a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To Toys

limited.. 2450

…...By balance

c/d 2450

6) Toys limited a/c

2)Rent received account

Date Particular J.F Amount Date Particular J.F Amount

…...By

bank. 500..

500.. 500..

3) Cash account

Date Particular J.F Amount Date Particular J.F Amount

…...To capital.. 5200.. …...By repair 80..

…...To sales.. 1500..

…...By balance

c/d.... 7120.

To sales.. 500..

7200 7200

4) Fred a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To sales.. 400

…...By balance

b/d 400

5) Purchase a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To Toys

limited.. 2450

…...By balance

c/d 2450

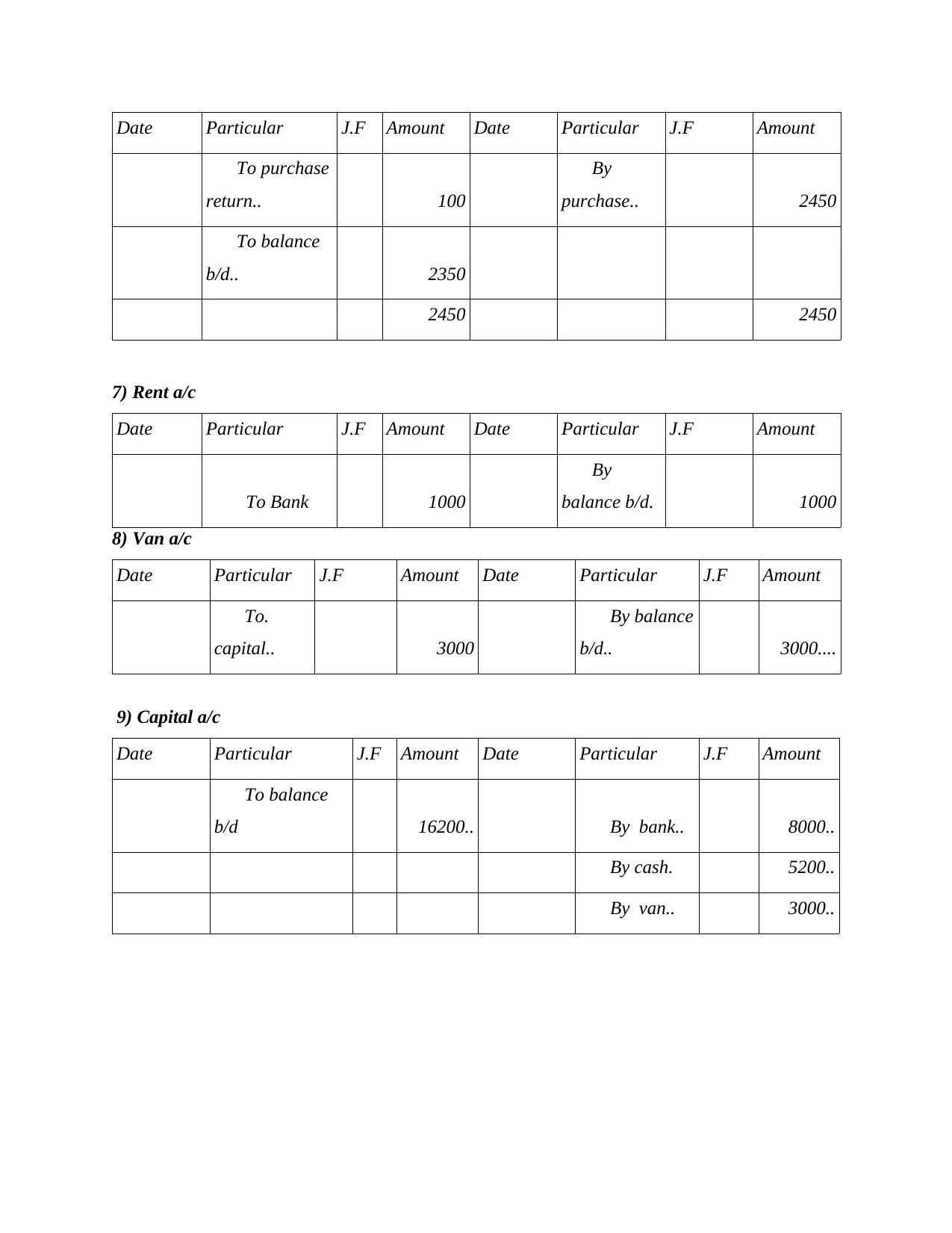

6) Toys limited a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To purchase

return.. 100

…...By

purchase.. 2450

…...To balance

b/d.. 2350

2450 2450

7) Rent a/c

Date Particular J.F Amount Date Particular J.F Amount

..…...To Bank 1000

…...By

balance b/d. 1000

8) Van a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To.

capital.. 3000

…...By balance

b/d.. 3000....

9) Capital a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To balance

b/d 16200.. …...By bank.. 8000..

…...By cash. 5200..

…...By van.. 3000..

…...To purchase

return.. 100

…...By

purchase.. 2450

…...To balance

b/d.. 2350

2450 2450

7) Rent a/c

Date Particular J.F Amount Date Particular J.F Amount

..…...To Bank 1000

…...By

balance b/d. 1000

8) Van a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To.

capital.. 3000

…...By balance

b/d.. 3000....

9) Capital a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To balance

b/d 16200.. …...By bank.. 8000..

…...By cash. 5200..

…...By van.. 3000..

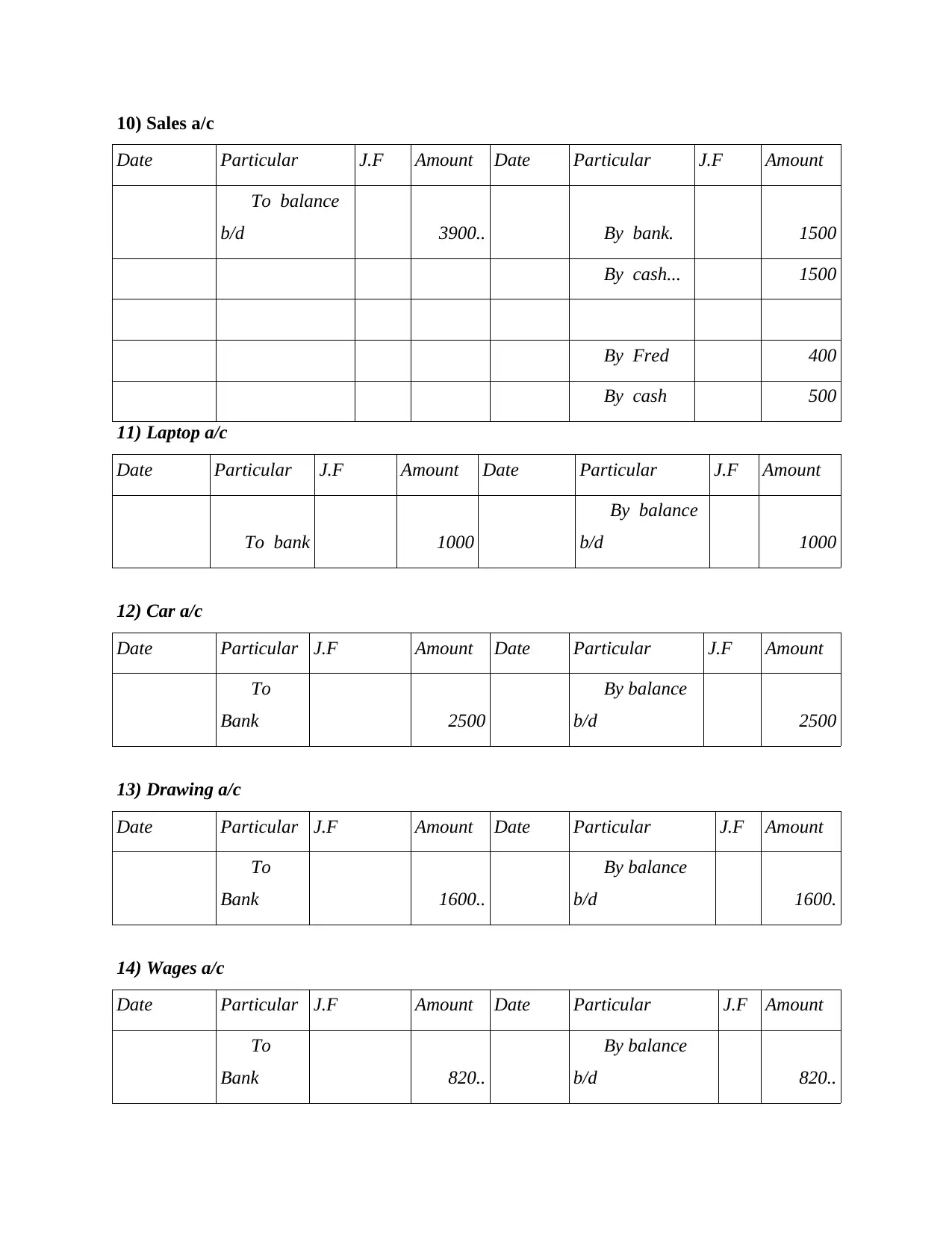

10) Sales a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To balance

b/d 3900.. …...By bank. 1500

…...By cash... 1500

…...By Fred 400

…...By cash 500

11) Laptop a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To bank 1000

…...By balance

b/d 1000

12) Car a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To

Bank 2500

…...By balance

b/d 2500

13) Drawing a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To

Bank 1600..

…...By balance

b/d 1600.

14) Wages a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To

Bank 820..

…...By balance

b/d 820..

Date Particular J.F Amount Date Particular J.F Amount

…...To balance

b/d 3900.. …...By bank. 1500

…...By cash... 1500

…...By Fred 400

…...By cash 500

11) Laptop a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To bank 1000

…...By balance

b/d 1000

12) Car a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To

Bank 2500

…...By balance

b/d 2500

13) Drawing a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To

Bank 1600..

…...By balance

b/d 1600.

14) Wages a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To

Bank 820..

…...By balance

b/d 820..

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

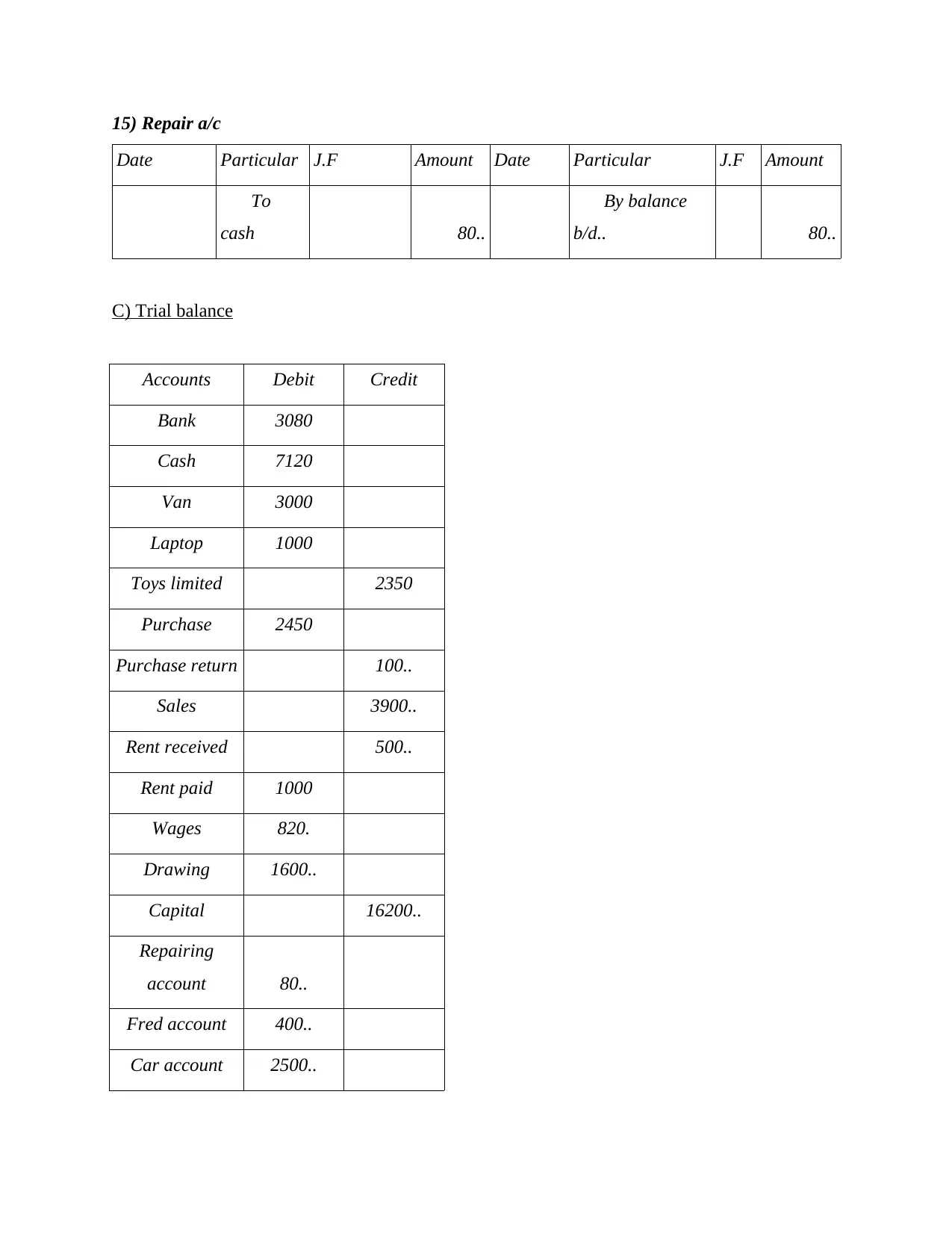

15) Repair a/c

Date Particular J.F Amount Date Particular J.F Amount

…...To

cash 80..

…...By balance

b/d.. 80..

C) Trial balance

Accounts Debit Credit

Bank 3080

Cash 7120

Van 3000

Laptop 1000

Toys limited 2350

Purchase 2450

Purchase return 100..

Sales 3900..

Rent received 500..

Rent paid 1000

Wages 820.

Drawing 1600..

Capital 16200..

Repairing

account 80..

Fred account 400..

Car account 2500..

Date Particular J.F Amount Date Particular J.F Amount

…...To

cash 80..

…...By balance

b/d.. 80..

C) Trial balance

Accounts Debit Credit

Bank 3080

Cash 7120

Van 3000

Laptop 1000

Toys limited 2350

Purchase 2450

Purchase return 100..

Sales 3900..

Rent received 500..

Rent paid 1000

Wages 820.

Drawing 1600..

Capital 16200..

Repairing

account 80..

Fred account 400..

Car account 2500..

22550.. 22550

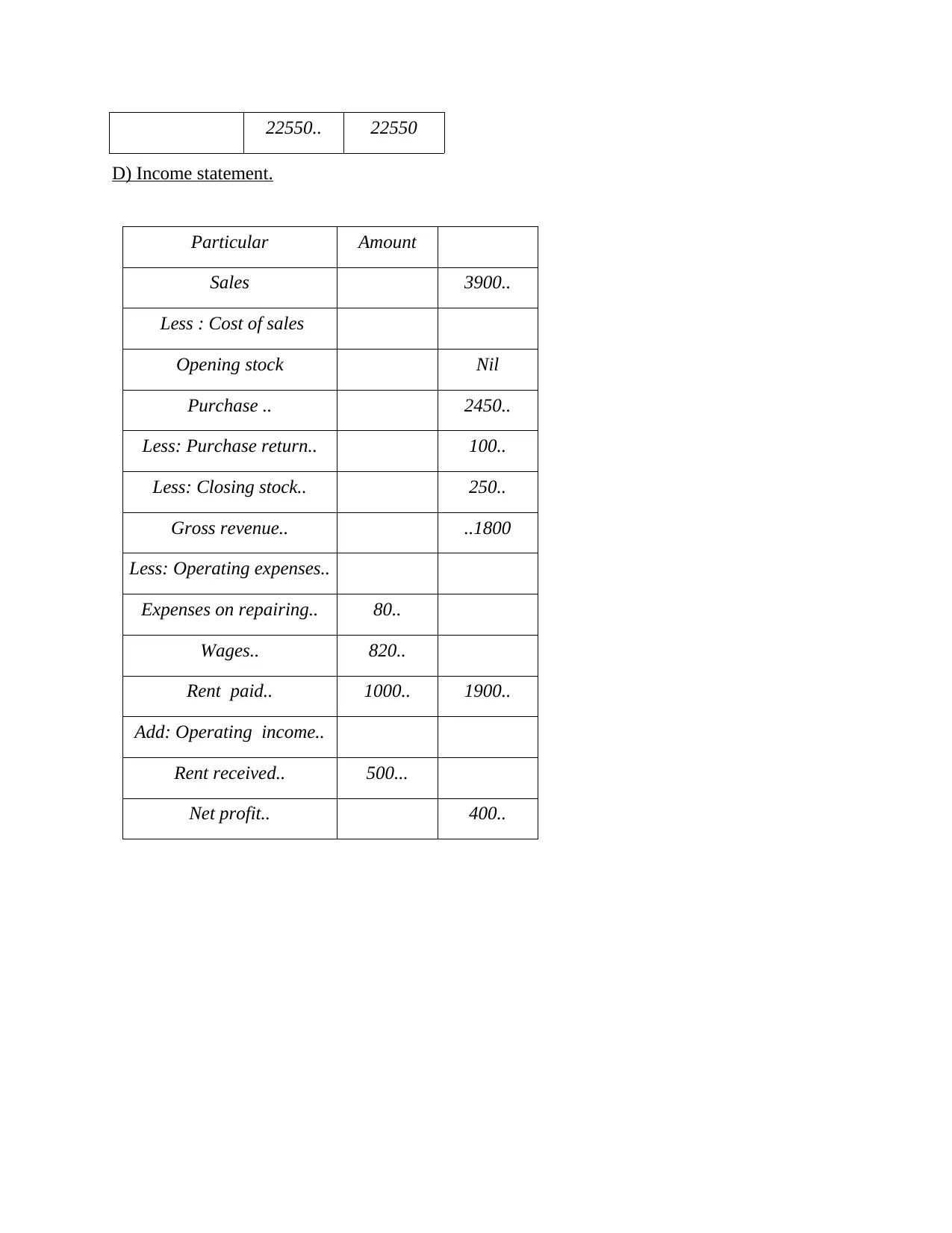

D) Income statement.

Particular Amount

Sales 3900..

Less : Cost of sales

Opening stock Nil

Purchase .. 2450..

Less: Purchase return.. 100..

Less: Closing stock.. 250..

Gross revenue.. ..1800

Less: Operating expenses..

Expenses on repairing.. 80..

Wages.. 820..

Rent paid.. 1000.. 1900..

Add: Operating income..

Rent received.. 500...

Net profit.. 400..

D) Income statement.

Particular Amount

Sales 3900..

Less : Cost of sales

Opening stock Nil

Purchase .. 2450..

Less: Purchase return.. 100..

Less: Closing stock.. 250..

Gross revenue.. ..1800

Less: Operating expenses..

Expenses on repairing.. 80..

Wages.. 820..

Rent paid.. 1000.. 1900..

Add: Operating income..

Rent received.. 500...

Net profit.. 400..

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

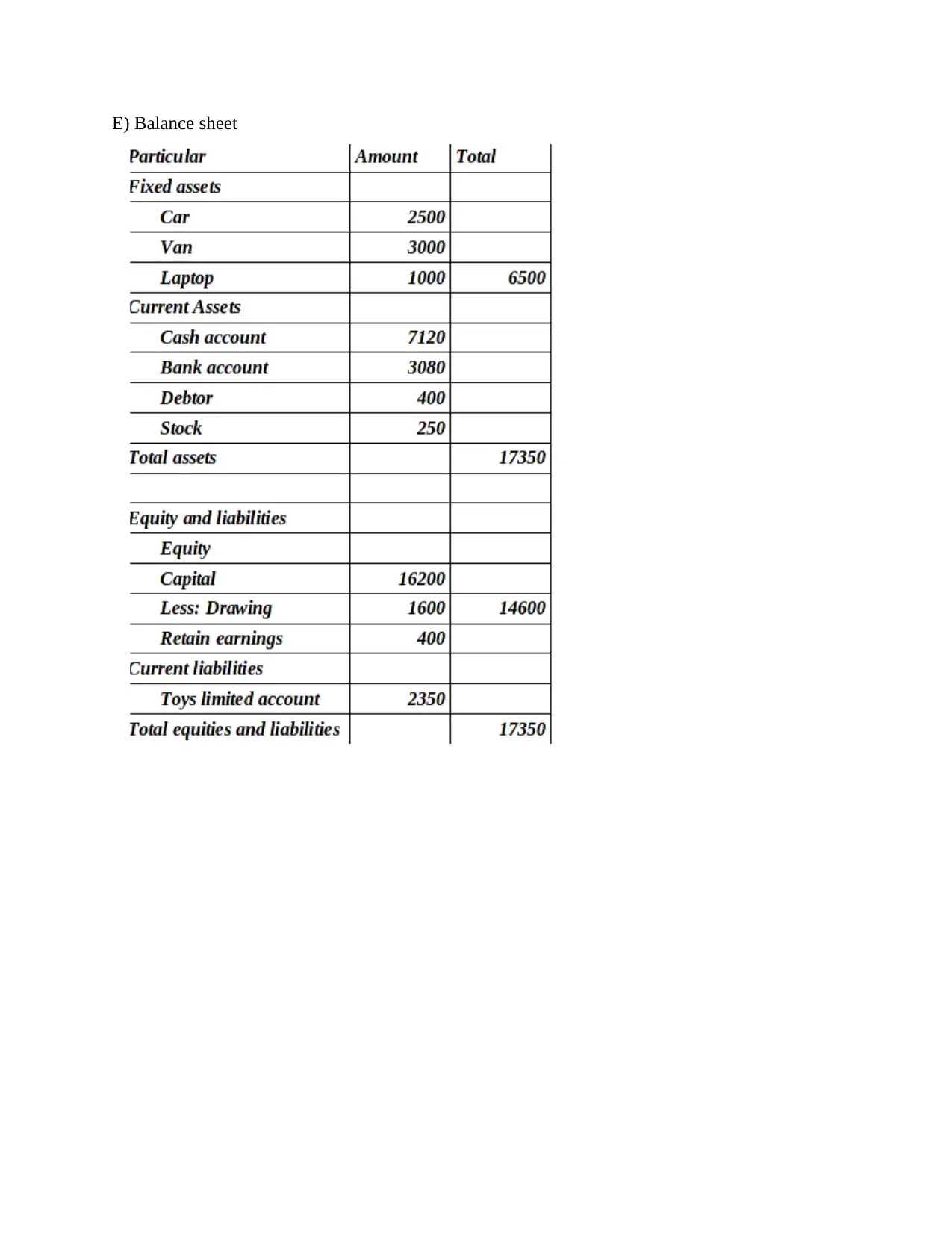

E) Balance sheet

F) Special note regarding drawing account.

The term drawing is considering when personal use capital of business for their person

use. These expenditures are not beneficial for organization and they are not even generating

profit for future business activities. Thus these type of expense are consider as drawing account

and this amount is deducted from capital of owner of the organization (Choudhary Virmani, and

Juneja, 2020).

The main objective formulates this account for the purpose of control or mitigate issue

arise related with creation of secret profit. In this case, Linda use 16000 for her holiday trip, she

is not going for official purpose and this trip is essential to control her mental stress problem.

Thus it is incudes and consider as drawing ad all the expenditure of trip is deducted from her

capital account.

The term drawing is considering when personal use capital of business for their person

use. These expenditures are not beneficial for organization and they are not even generating

profit for future business activities. Thus these type of expense are consider as drawing account

and this amount is deducted from capital of owner of the organization (Choudhary Virmani, and

Juneja, 2020).

The main objective formulates this account for the purpose of control or mitigate issue

arise related with creation of secret profit. In this case, Linda use 16000 for her holiday trip, she

is not going for official purpose and this trip is essential to control her mental stress problem.

Thus it is incudes and consider as drawing ad all the expenditure of trip is deducted from her

capital account.

PART B

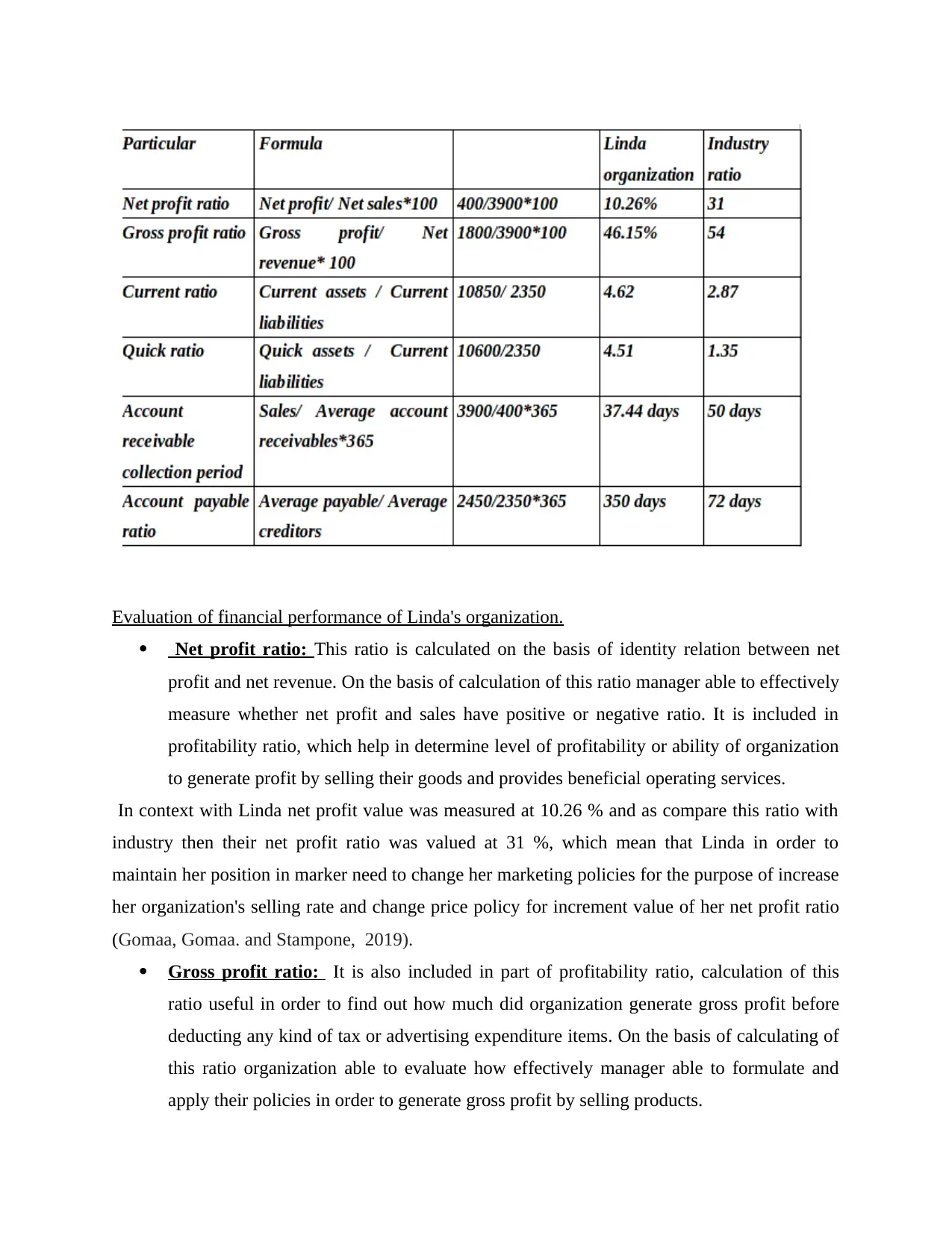

Calculation of ratio.

Ratio: In every business organization there are various types of method and approach are

available which manager use in order to analysis and compare their organization's performance.

Most of organizations use or apply ratio it is the most easy and universally acceptable method

which most of business organization has been used in order to find out and compare value of

their organization (Gichuki, and Mulu-Mutuku, 2018).

Ratio is considering as the tool of financial management which also used in mathematical

approach for the purpose of define relationship between 2 variables. On the basis of that positive

or negative ration of variables can be determine. Manager used this approach to find out relevant

ratio between different items of balance sheet and income statement and on the basis of that they

are able to formulate different management strategies which useful for further business activities.

Linda use to calculate different types of ratio in order to measure her organizations performance

with industry's performance, these are defining below:

Calculation of ratio.

Ratio: In every business organization there are various types of method and approach are

available which manager use in order to analysis and compare their organization's performance.

Most of organizations use or apply ratio it is the most easy and universally acceptable method

which most of business organization has been used in order to find out and compare value of

their organization (Gichuki, and Mulu-Mutuku, 2018).

Ratio is considering as the tool of financial management which also used in mathematical

approach for the purpose of define relationship between 2 variables. On the basis of that positive

or negative ration of variables can be determine. Manager used this approach to find out relevant

ratio between different items of balance sheet and income statement and on the basis of that they

are able to formulate different management strategies which useful for further business activities.

Linda use to calculate different types of ratio in order to measure her organizations performance

with industry's performance, these are defining below:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Evaluation of financial performance of Linda's organization.

Net profit ratio: This ratio is calculated on the basis of identity relation between net

profit and net revenue. On the basis of calculation of this ratio manager able to effectively

measure whether net profit and sales have positive or negative ratio. It is included in

profitability ratio, which help in determine level of profitability or ability of organization

to generate profit by selling their goods and provides beneficial operating services.

In context with Linda net profit value was measured at 10.26 % and as compare this ratio with

industry then their net profit ratio was valued at 31 %, which mean that Linda in order to

maintain her position in marker need to change her marketing policies for the purpose of increase

her organization's selling rate and change price policy for increment value of her net profit ratio

(Gomaa, Gomaa. and Stampone, 2019).

Gross profit ratio: It is also included in part of profitability ratio, calculation of this

ratio useful in order to find out how much did organization generate gross profit before

deducting any kind of tax or advertising expenditure items. On the basis of calculating of

this ratio organization able to evaluate how effectively manager able to formulate and

apply their policies in order to generate gross profit by selling products.

Net profit ratio: This ratio is calculated on the basis of identity relation between net

profit and net revenue. On the basis of calculation of this ratio manager able to effectively

measure whether net profit and sales have positive or negative ratio. It is included in

profitability ratio, which help in determine level of profitability or ability of organization

to generate profit by selling their goods and provides beneficial operating services.

In context with Linda net profit value was measured at 10.26 % and as compare this ratio with

industry then their net profit ratio was valued at 31 %, which mean that Linda in order to

maintain her position in marker need to change her marketing policies for the purpose of increase

her organization's selling rate and change price policy for increment value of her net profit ratio

(Gomaa, Gomaa. and Stampone, 2019).

Gross profit ratio: It is also included in part of profitability ratio, calculation of this

ratio useful in order to find out how much did organization generate gross profit before

deducting any kind of tax or advertising expenditure items. On the basis of calculating of

this ratio organization able to evaluate how effectively manager able to formulate and

apply their policies in order to generate gross profit by selling products.

Value of gross profit of Linda's organization was evaluated at 46015 % and on the other side

industry's organization able to generate 54 % of gross profit ratio, which represent that even

though Linda able to effectively gain gross profit ratio at higher rate however she needs to

implement this ratio to maintain organization position in market because as compare to industry's

ratio it was lower than rival organization's ratio.

Current ratio: This is included in calculating liquidity position of business entity. On

the basis of determining value of current ratio, manager find out relation between

working capital items which includes, current assets & current business liabilities. This

ratio useful in identify ability of working capital to pay short term debt liability

(Markovic, Edwards, and Jacobs, 2019).

Value of current ratio of industry was measured at 2.87 and on the other side Linda's

organization current ratio was 4.62 which showcase that Linda not use her financial capital in

effective manner thus she has access of current asset as ideal current ratio was 2:1, thus in order

to maintain the ratio she needs to implement management of her organizations assets strategy. As

industry's ratio was evaluated at 2.87 which represent that rival industry have sufficient capital

and they no misuses or wastage their assets during the time of running business operations.

Quick ratio: This ratio is evaluated on the basis of determine value of quick assets &

current liabilities Value of quick assets is determining on the basis of deducting stock or

inventory amount from current assets value. This ratio is used for represent ability of

business entity to pay short term debt within given time period. They find out relevance

of availability of cash related items. Value of quick assets was 4.51 and on the other side

industry's quick ratio was 1.35 which means that Linda have access of availability of cash

asset to pay their debt amount and she easily pay their debt liability however she need to

implement policies to manager her organisations cash& cash relevant assets (Rouxelin,

Wongsunwai. and Yehuda, 2018).

Account receivable collection period: This ratio of determine for find out, time required

by business organization to collect amount from their debtors. This ratio useful in

recognize efficiency level of organization to generate cash inflow from collect money

through their relevant customers. Linda take 37 days to collect funds from her debtor and

on the other side industry's took 50 days which means that Linda adopt effective strategy

of collection of funds from debtor as compare to other organizations.

industry's organization able to generate 54 % of gross profit ratio, which represent that even

though Linda able to effectively gain gross profit ratio at higher rate however she needs to

implement this ratio to maintain organization position in market because as compare to industry's

ratio it was lower than rival organization's ratio.

Current ratio: This is included in calculating liquidity position of business entity. On

the basis of determining value of current ratio, manager find out relation between

working capital items which includes, current assets & current business liabilities. This

ratio useful in identify ability of working capital to pay short term debt liability

(Markovic, Edwards, and Jacobs, 2019).

Value of current ratio of industry was measured at 2.87 and on the other side Linda's

organization current ratio was 4.62 which showcase that Linda not use her financial capital in

effective manner thus she has access of current asset as ideal current ratio was 2:1, thus in order

to maintain the ratio she needs to implement management of her organizations assets strategy. As

industry's ratio was evaluated at 2.87 which represent that rival industry have sufficient capital

and they no misuses or wastage their assets during the time of running business operations.

Quick ratio: This ratio is evaluated on the basis of determine value of quick assets &

current liabilities Value of quick assets is determining on the basis of deducting stock or

inventory amount from current assets value. This ratio is used for represent ability of

business entity to pay short term debt within given time period. They find out relevance

of availability of cash related items. Value of quick assets was 4.51 and on the other side

industry's quick ratio was 1.35 which means that Linda have access of availability of cash

asset to pay their debt amount and she easily pay their debt liability however she need to

implement policies to manager her organisations cash& cash relevant assets (Rouxelin,

Wongsunwai. and Yehuda, 2018).

Account receivable collection period: This ratio of determine for find out, time required

by business organization to collect amount from their debtors. This ratio useful in

recognize efficiency level of organization to generate cash inflow from collect money

through their relevant customers. Linda take 37 days to collect funds from her debtor and

on the other side industry's took 50 days which means that Linda adopt effective strategy

of collection of funds from debtor as compare to other organizations.

Account payable ratio: Manager calculate account payable ratio for find out time

require by organization to pay their creditors liability. With the measurement of this ratio

manager formulate effective business policies which help in reduce days require to

payable creditors liability. Linda took 350 days for pay short liability of their creditors or

supplier, however on the other side industry take 72 days to pay money to their suppliers

and creditor, it define that Linda needs to change their payment policy and mould

management structure which help in reduce account payable ratio (Schmidt, C. G. and

Wagner, 2019).

From the calculation of these ratio is to measured that Linda able to run their business operation

in effective manner as their liquidity and portability ratio is higher however to provide toughest

competition to rival companies she needs to change her management structure and financial

policies to increase her organization performance.

CONCLUSION

From the above analysis it has been concluded that accounting is consider as essential

approach to run business operations. This is used for record every operation detail in systematic

way. By formulation of journal and ledger each transaction is recorded in monetary terms. And

on these data help in proved base for formulation of financial statement. On the basis of

collecting data from income statement & balance sheet manager able to evaluate value and

measure financial performance of organization by using financial ratio technique.

require by organization to pay their creditors liability. With the measurement of this ratio

manager formulate effective business policies which help in reduce days require to

payable creditors liability. Linda took 350 days for pay short liability of their creditors or

supplier, however on the other side industry take 72 days to pay money to their suppliers

and creditor, it define that Linda needs to change their payment policy and mould

management structure which help in reduce account payable ratio (Schmidt, C. G. and

Wagner, 2019).

From the calculation of these ratio is to measured that Linda able to run their business operation

in effective manner as their liquidity and portability ratio is higher however to provide toughest

competition to rival companies she needs to change her management structure and financial

policies to increase her organization performance.

CONCLUSION

From the above analysis it has been concluded that accounting is consider as essential

approach to run business operations. This is used for record every operation detail in systematic

way. By formulation of journal and ledger each transaction is recorded in monetary terms. And

on these data help in proved base for formulation of financial statement. On the basis of

collecting data from income statement & balance sheet manager able to evaluate value and

measure financial performance of organization by using financial ratio technique.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and journal

Choudhary, T., Virmani, C. and Juneja, D., 2020. Convergence of Blockchain and IoT: An Edge

Over Technologies. In Toward Social Internet of Things (SIoT): Enabling Technologies,

Architectures and Applications (pp. 299-316). Springer, Cham.

Gichuki, C. N. and Mulu-Mutuku, M., 2018, March. Determinants of awareness and adoption of

mobile money technologies: Evidence from women micro entrepreneurs in Kenya.

In Women's Studies International Forum (Vol. 67, pp. 18-22). Pergamon.

Gomaa, A. A., Gomaa, M.I. and Stampone, A., 2019. A transaction on the blockchain: An AIS

perspective, intro case to explain transactions on the ERP and the role of the internal and

external auditor. Journal of Emerging Technologies in Accounting. 16(1). pp.47-64.

Markovic, M., Edwards, P. and Jacobs, N., 2019, October. Recording Provenance of Food

Delivery Using IoT, Semantics and Business Blockchain Networks. In 2019 Sixth

International Conference on Internet of Things: Systems, Management and Security

(IOTSMS) (pp. 116-118). IEEE.

Rouxelin, F., Wongsunwai, W. and Yehuda, N., 2018. Aggregate cost stickiness in GAAP

financial statements and future unemployment rate. The Accounting Review .93(3).

pp.299-325.

Schmidt, C. G. and Wagner, S. M., 2019. Blockchain and supply chain relations: A transaction

cost theory perspective. Journal of Purchasing and Supply Management. 25(4).

p.100552.

Books and journal

Choudhary, T., Virmani, C. and Juneja, D., 2020. Convergence of Blockchain and IoT: An Edge

Over Technologies. In Toward Social Internet of Things (SIoT): Enabling Technologies,

Architectures and Applications (pp. 299-316). Springer, Cham.

Gichuki, C. N. and Mulu-Mutuku, M., 2018, March. Determinants of awareness and adoption of

mobile money technologies: Evidence from women micro entrepreneurs in Kenya.

In Women's Studies International Forum (Vol. 67, pp. 18-22). Pergamon.

Gomaa, A. A., Gomaa, M.I. and Stampone, A., 2019. A transaction on the blockchain: An AIS

perspective, intro case to explain transactions on the ERP and the role of the internal and

external auditor. Journal of Emerging Technologies in Accounting. 16(1). pp.47-64.

Markovic, M., Edwards, P. and Jacobs, N., 2019, October. Recording Provenance of Food

Delivery Using IoT, Semantics and Business Blockchain Networks. In 2019 Sixth

International Conference on Internet of Things: Systems, Management and Security

(IOTSMS) (pp. 116-118). IEEE.

Rouxelin, F., Wongsunwai, W. and Yehuda, N., 2018. Aggregate cost stickiness in GAAP

financial statements and future unemployment rate. The Accounting Review .93(3).

pp.299-325.

Schmidt, C. G. and Wagner, S. M., 2019. Blockchain and supply chain relations: A transaction

cost theory perspective. Journal of Purchasing and Supply Management. 25(4).

p.100552.

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.