Business Accounting Report: Anne York's Financial Statements Analysis

VerifiedAdded on 2023/02/06

|20

|2408

|28

Report

AI Summary

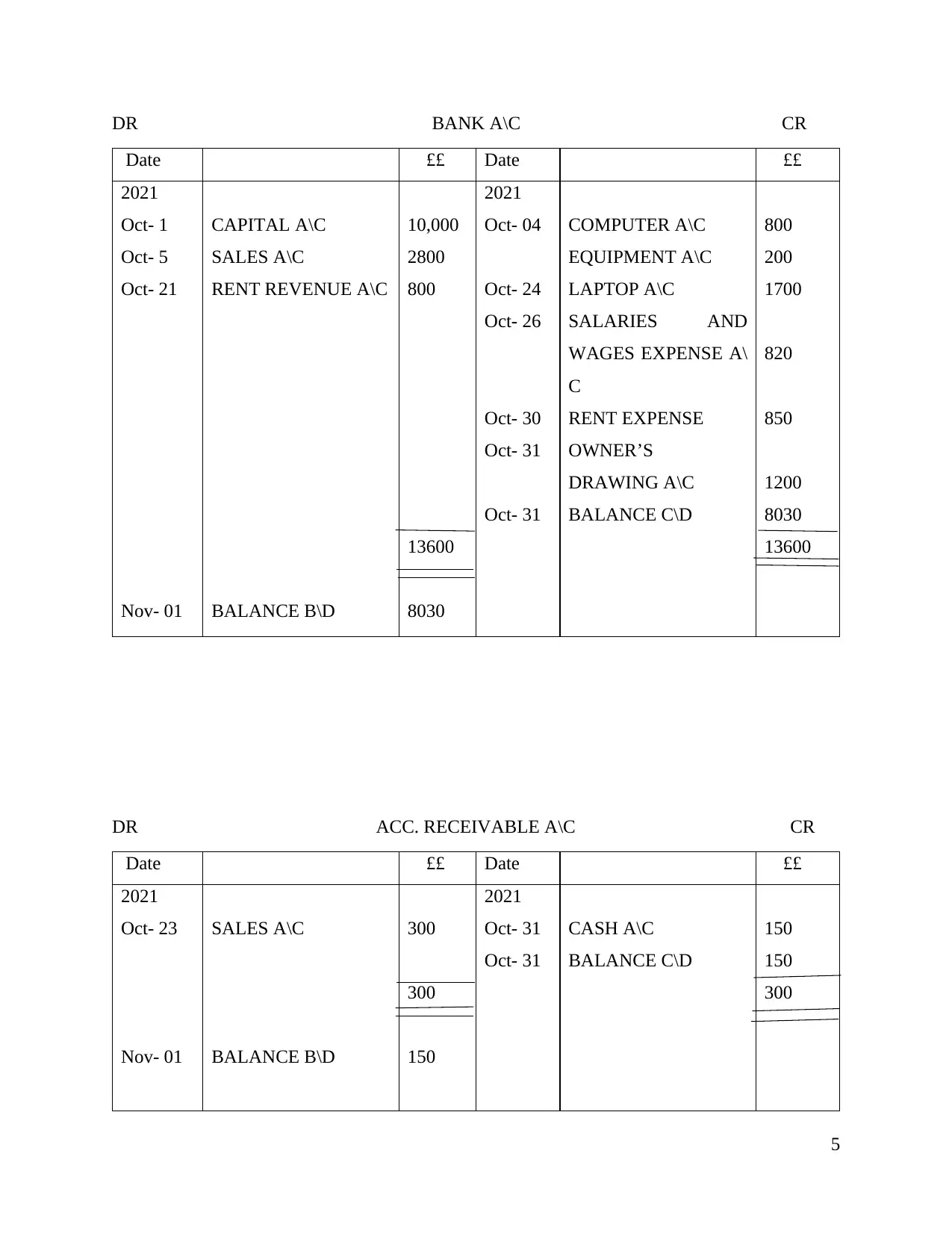

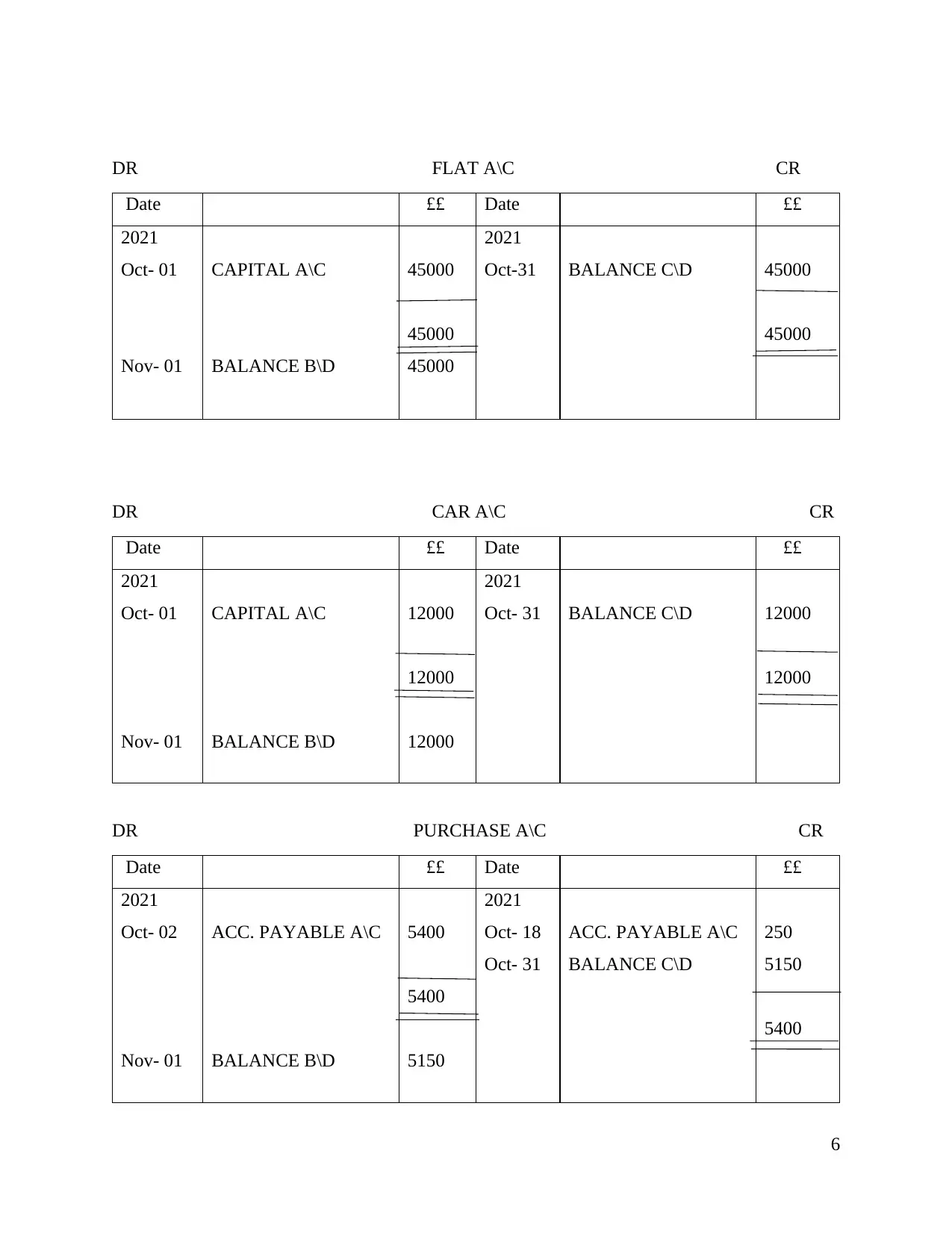

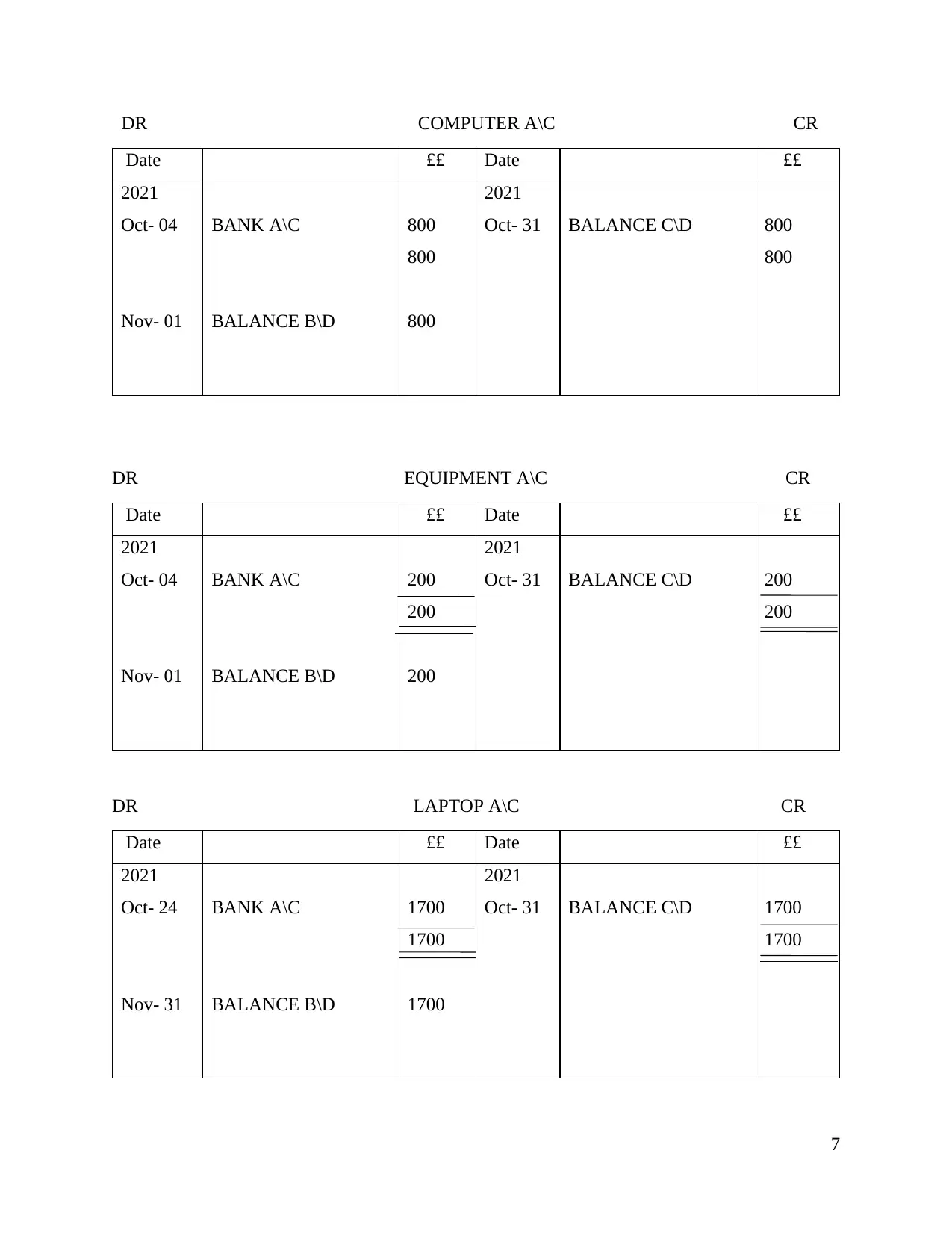

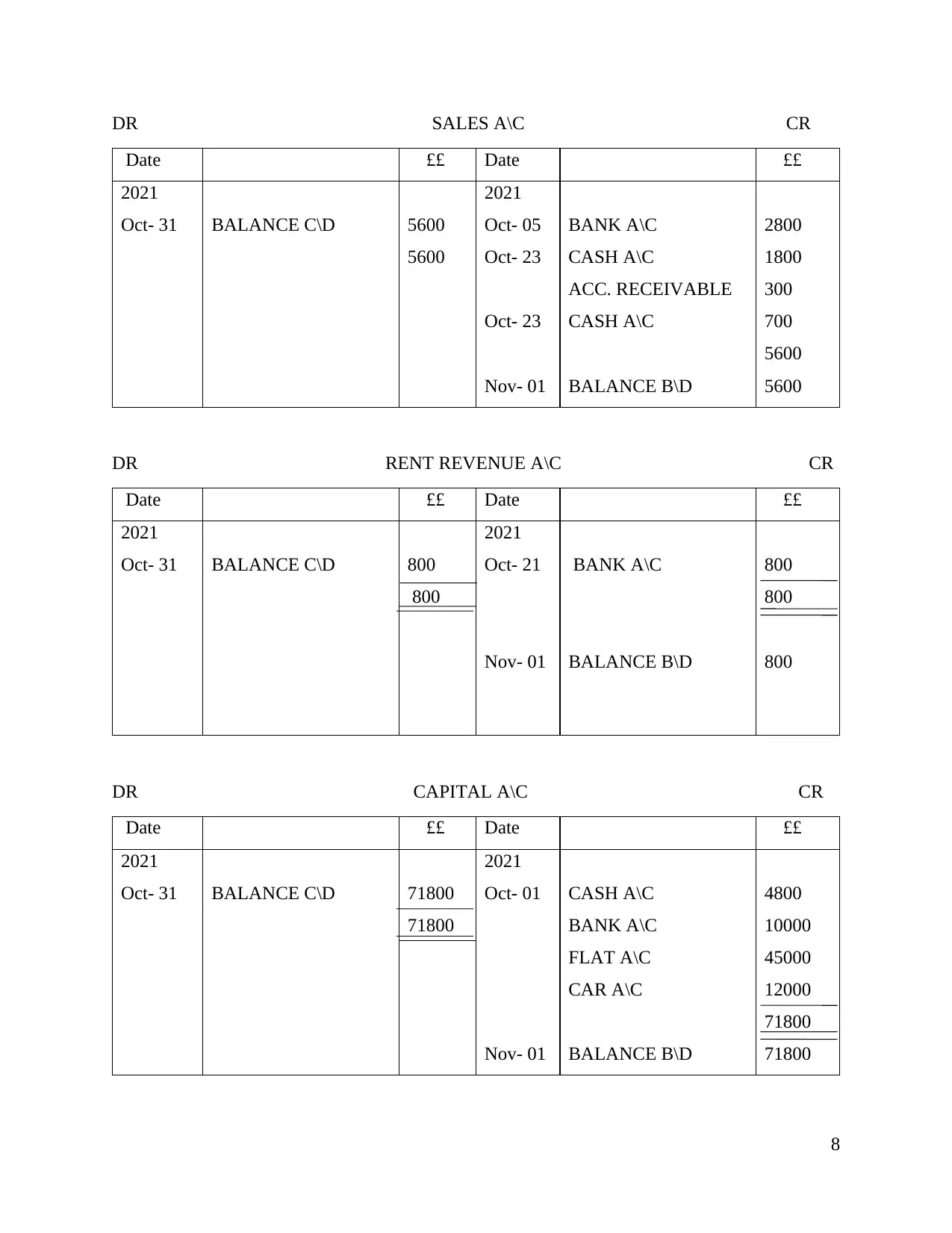

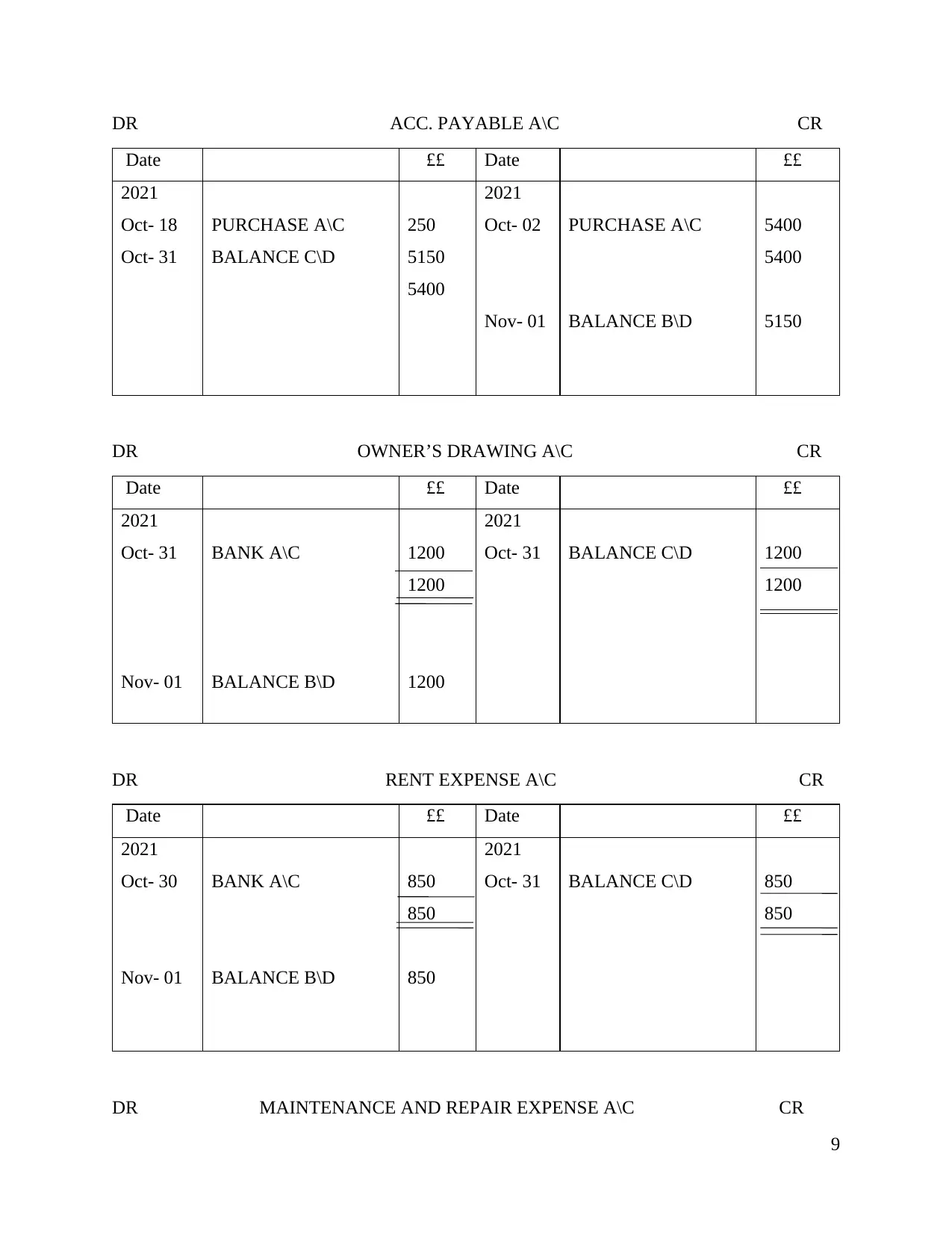

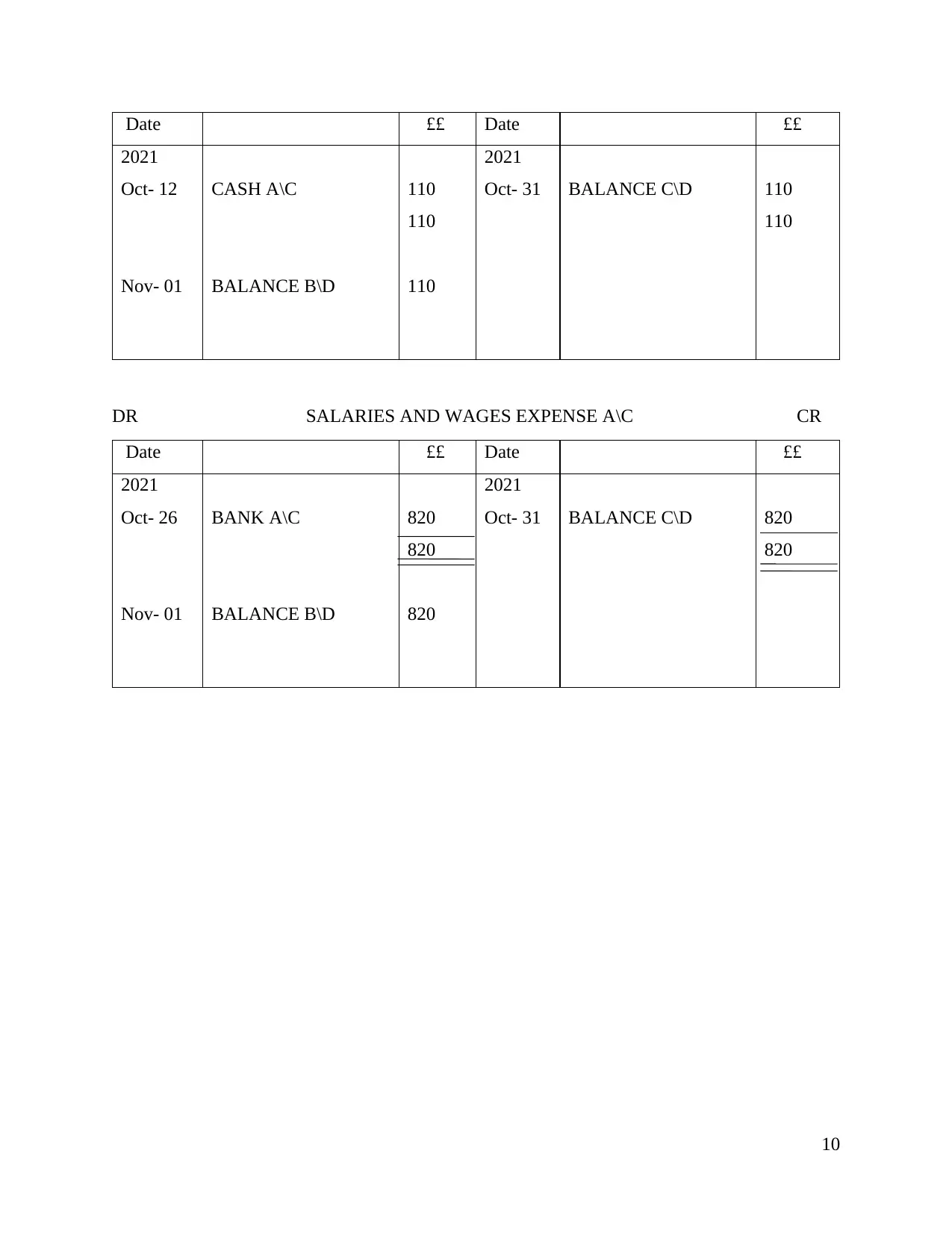

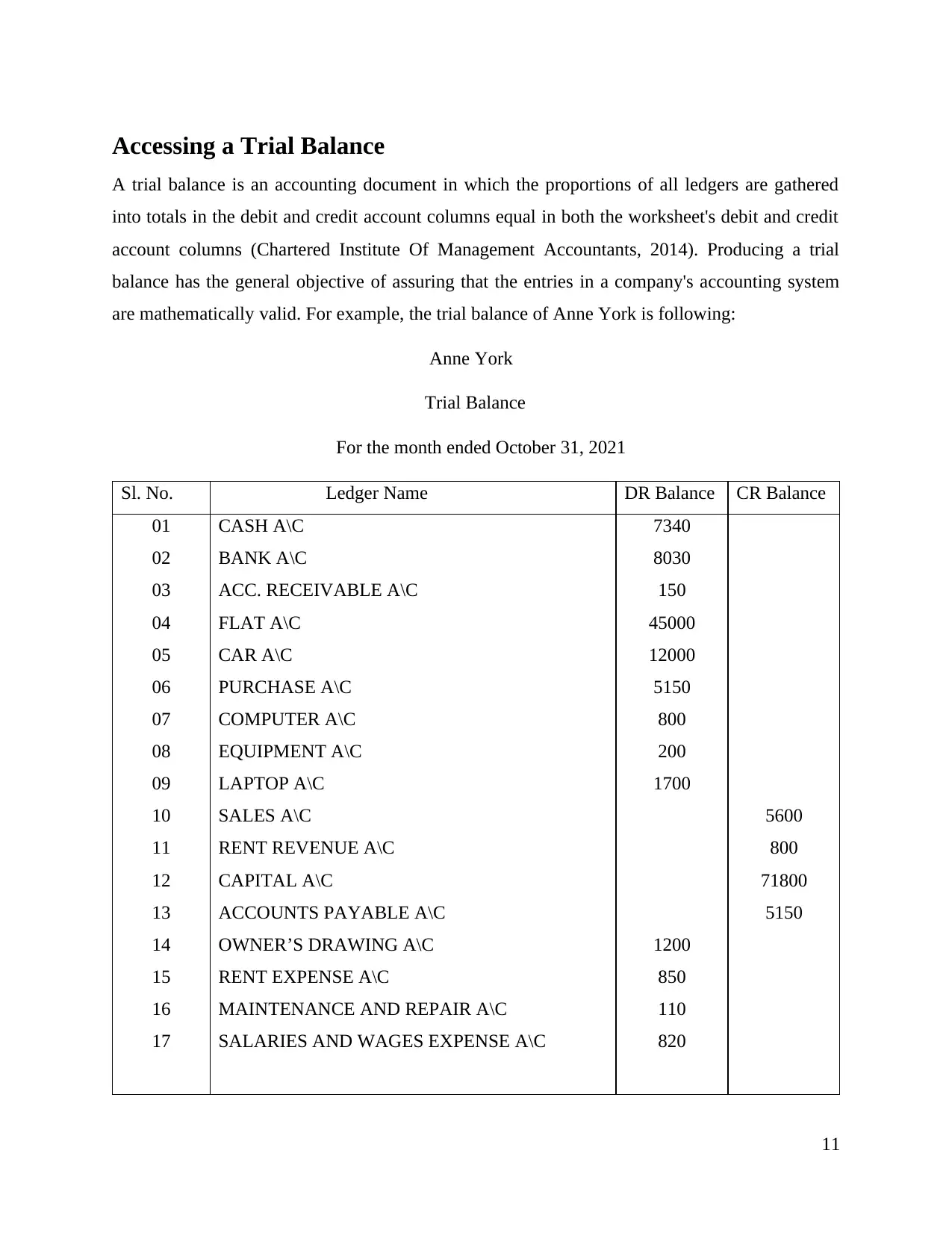

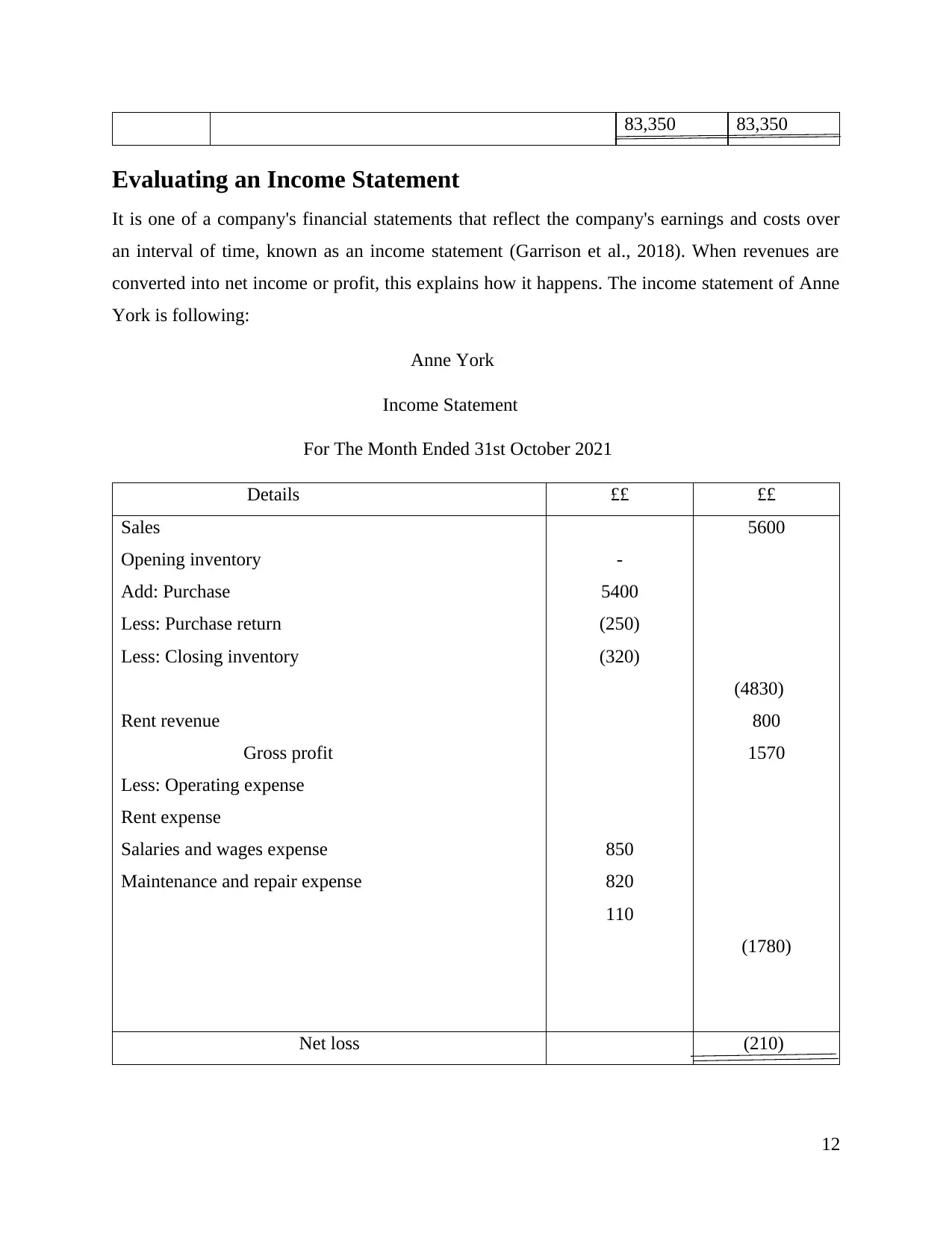

This report provides a comprehensive analysis of Anne York's accounting and bookkeeping practices. It begins with an examination of double-entry recording, utilizing T-accounts to illustrate transaction postings and balance calculations. The report then progresses to a trial balance, followed by evaluations of the income statement and the statement of financial position. A key section delves into the impact of drawings on small businesses, followed by a detailed calculation and analysis of various financial ratios, including profitability, current, and acid-test ratios, as well as accounts receivable collection and accounts payable payment periods. The report also addresses the impact of the COVID-19 pandemic on these ratios. Overall, the report offers insights into Anne York's financial performance, liquidity, and efficiency, providing a basis for recommendations to improve financial outcomes.

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.