Recording Business Transactions: Journal Entries, Balance Sheets, and Ratio Analysis

VerifiedAdded on 2022/12/28

|17

|2346

|156

AI Summary

This document provides a comprehensive guide to recording business transactions, including journal entries, balance sheets, and ratio analysis. It covers topics such as cash accounts, purchase returns, and comparative analysis with competitors. The content is relevant for students studying business and finance courses.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Recording

Business

Transaction

Business

Transaction

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................1

PART A...........................................................................................................................................1

Journal transactions of T- accounts:............................................................................................1

Balance the accounts and an opening balances:..........................................................................2

Trial balance:...............................................................................................................................8

Income statement for the period 31st Oct. 2020:.........................................................................8

Preparation of financial position 31st Oct. 2020:........................................................................8

PART B............................................................................................................................................9

Ratio calculation for Linda's business:........................................................................................9

Analysis of ratio analysis in comparison to its competitors:.....................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

PART A...........................................................................................................................................1

Journal transactions of T- accounts:............................................................................................1

Balance the accounts and an opening balances:..........................................................................2

Trial balance:...............................................................................................................................8

Income statement for the period 31st Oct. 2020:.........................................................................8

Preparation of financial position 31st Oct. 2020:........................................................................8

PART B............................................................................................................................................9

Ratio calculation for Linda's business:........................................................................................9

Analysis of ratio analysis in comparison to its competitors:.....................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

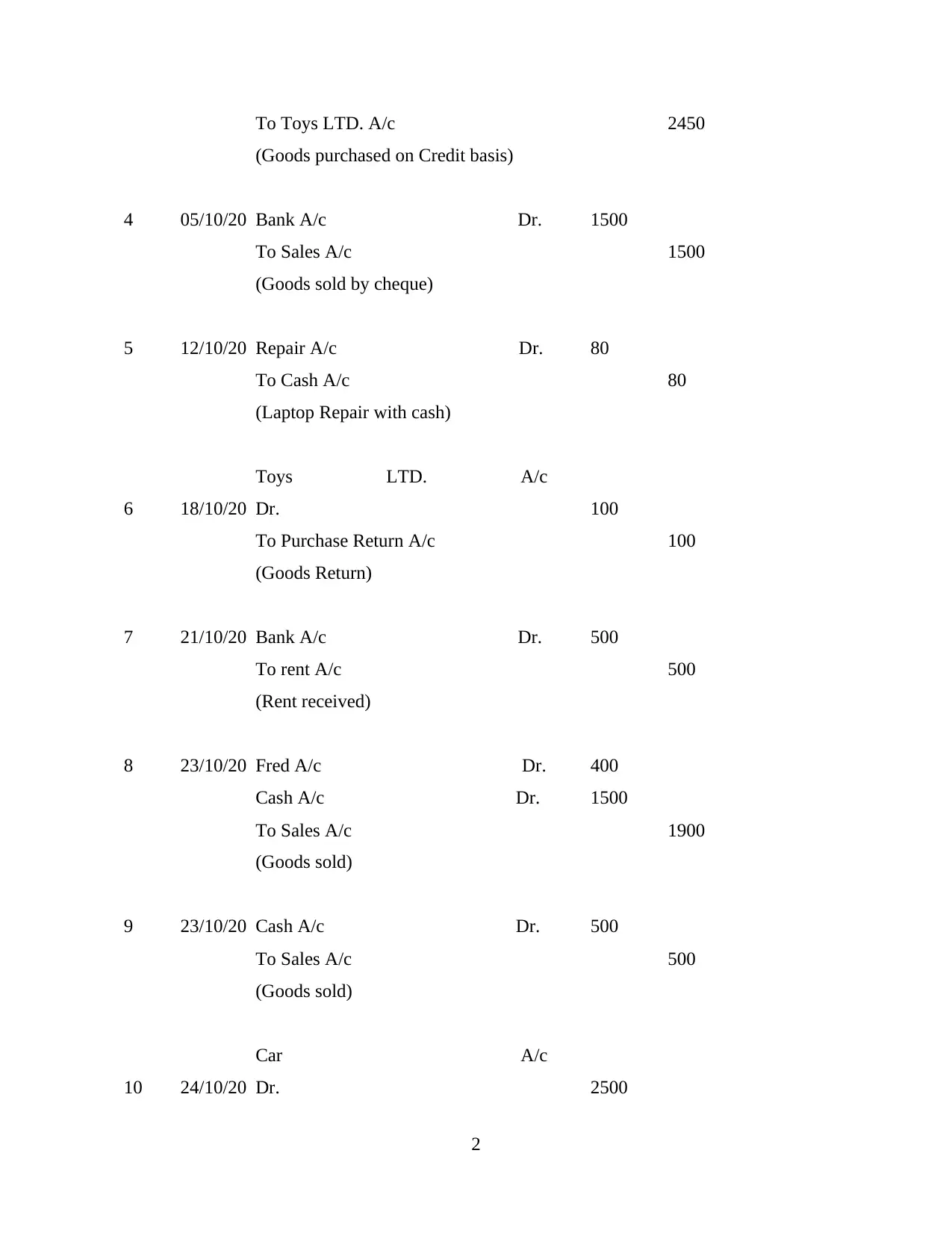

INTRODUCTION

Business transactions is the process which includes transactions for goods. Money,

services for various parties for the business. It includes various transactions which business uses

for its activities. It is about recording those transactions which the business runs for its activities

which helps its for higher profitability. Company's records its transactions for its decision

making which helps for better performance which helps for higher profitability. It is about

managing activities which helps managers for decision making. Businesses which are use

accounting methods for recording its activities it will helps it for managing financial system for

the business (Adamyk, 2017). For example, the company purchases building it is the transactions

for the business. This report is bases for recording business transactions which helps company's

for better decision making which helps for higher profitability for the businesses. This report

includes topics which are journal, ledger and trial balance. Apart from this it includes topics

which are cash account and ratio analysis in comparison for competitors for the businesses.

PART A

Journal transactions of T- accounts:

JOURNAL ENTRIES

S.NO Date Particulars L.F £ £

2020

1 01/10/20 Cash A/c Dr. 5200

Bank A/c Dr. 8000

Van A/c Dr. 3000

To Capital A/c 16200

(Capital invested into business)

2 02/10/20 Laptop A/c Dr. 1000

To Bank A/c 1000

( Purchased laptop by cheque)

3 04/10/20 Purchase A/c Dr. 2450

1

Business transactions is the process which includes transactions for goods. Money,

services for various parties for the business. It includes various transactions which business uses

for its activities. It is about recording those transactions which the business runs for its activities

which helps its for higher profitability. Company's records its transactions for its decision

making which helps for better performance which helps for higher profitability. It is about

managing activities which helps managers for decision making. Businesses which are use

accounting methods for recording its activities it will helps it for managing financial system for

the business (Adamyk, 2017). For example, the company purchases building it is the transactions

for the business. This report is bases for recording business transactions which helps company's

for better decision making which helps for higher profitability for the businesses. This report

includes topics which are journal, ledger and trial balance. Apart from this it includes topics

which are cash account and ratio analysis in comparison for competitors for the businesses.

PART A

Journal transactions of T- accounts:

JOURNAL ENTRIES

S.NO Date Particulars L.F £ £

2020

1 01/10/20 Cash A/c Dr. 5200

Bank A/c Dr. 8000

Van A/c Dr. 3000

To Capital A/c 16200

(Capital invested into business)

2 02/10/20 Laptop A/c Dr. 1000

To Bank A/c 1000

( Purchased laptop by cheque)

3 04/10/20 Purchase A/c Dr. 2450

1

To Toys LTD. A/c 2450

(Goods purchased on Credit basis)

4 05/10/20 Bank A/c Dr. 1500

To Sales A/c 1500

(Goods sold by cheque)

5 12/10/20 Repair A/c Dr. 80

To Cash A/c 80

(Laptop Repair with cash)

6 18/10/20

Toys LTD. A/c

Dr. 100

To Purchase Return A/c 100

(Goods Return)

7 21/10/20 Bank A/c Dr. 500

To rent A/c 500

(Rent received)

8 23/10/20 Fred A/c Dr. 400

Cash A/c Dr. 1500

To Sales A/c 1900

(Goods sold)

9 23/10/20 Cash A/c Dr. 500

To Sales A/c 500

(Goods sold)

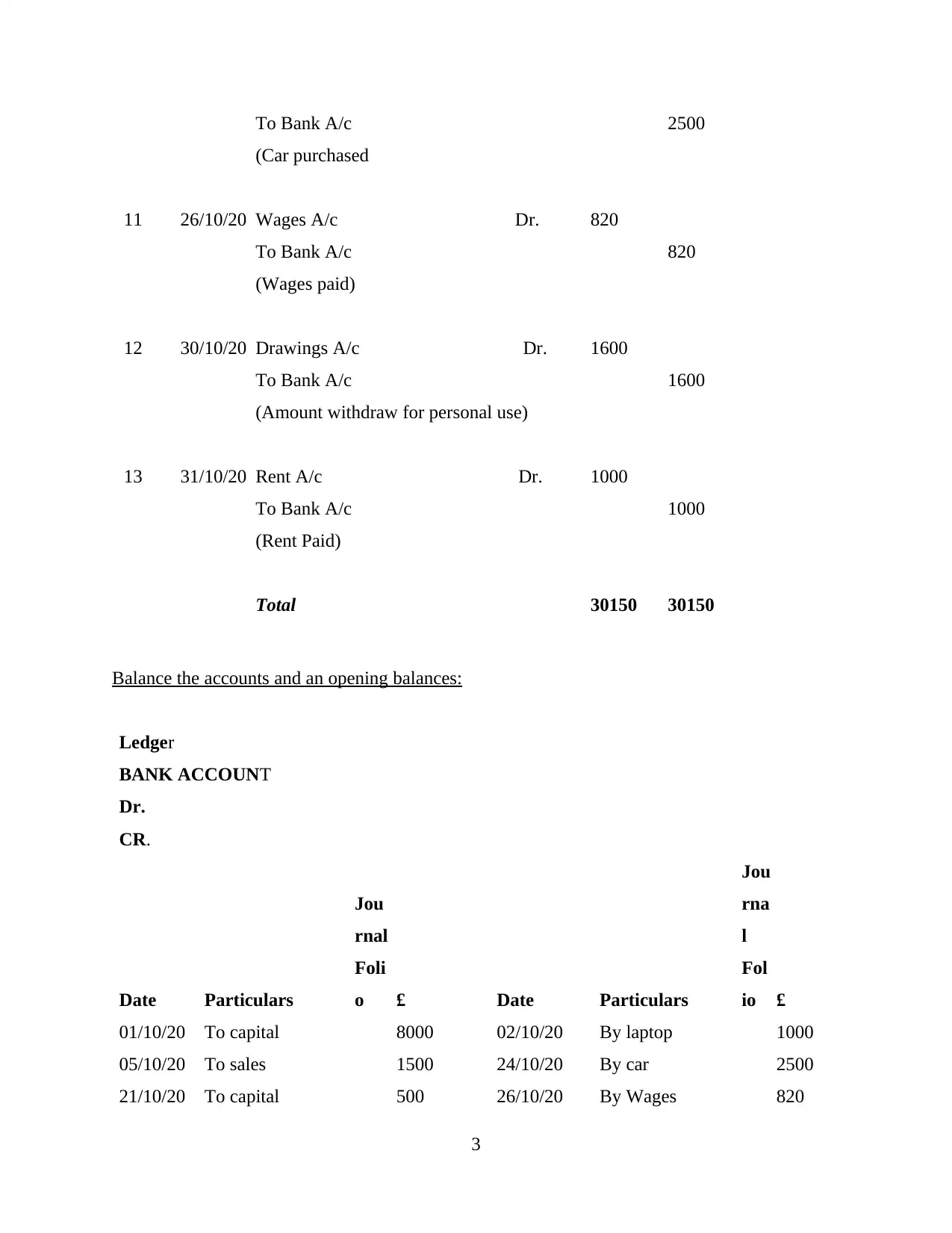

10 24/10/20

Car A/c

Dr. 2500

2

(Goods purchased on Credit basis)

4 05/10/20 Bank A/c Dr. 1500

To Sales A/c 1500

(Goods sold by cheque)

5 12/10/20 Repair A/c Dr. 80

To Cash A/c 80

(Laptop Repair with cash)

6 18/10/20

Toys LTD. A/c

Dr. 100

To Purchase Return A/c 100

(Goods Return)

7 21/10/20 Bank A/c Dr. 500

To rent A/c 500

(Rent received)

8 23/10/20 Fred A/c Dr. 400

Cash A/c Dr. 1500

To Sales A/c 1900

(Goods sold)

9 23/10/20 Cash A/c Dr. 500

To Sales A/c 500

(Goods sold)

10 24/10/20

Car A/c

Dr. 2500

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

To Bank A/c 2500

(Car purchased

11 26/10/20 Wages A/c Dr. 820

To Bank A/c 820

(Wages paid)

12 30/10/20 Drawings A/c Dr. 1600

To Bank A/c 1600

(Amount withdraw for personal use)

13 31/10/20 Rent A/c Dr. 1000

To Bank A/c 1000

(Rent Paid)

Total 30150 30150

Balance the accounts and an opening balances:

Ledger

BANK ACCOUNT

Dr.

CR.

Date Particulars

Jou

rnal

Foli

o £ Date Particulars

Jou

rna

l

Fol

io £

01/10/20 To capital 8000 02/10/20 By laptop 1000

05/10/20 To sales 1500 24/10/20 By car 2500

21/10/20 To capital 500 26/10/20 By Wages 820

3

(Car purchased

11 26/10/20 Wages A/c Dr. 820

To Bank A/c 820

(Wages paid)

12 30/10/20 Drawings A/c Dr. 1600

To Bank A/c 1600

(Amount withdraw for personal use)

13 31/10/20 Rent A/c Dr. 1000

To Bank A/c 1000

(Rent Paid)

Total 30150 30150

Balance the accounts and an opening balances:

Ledger

BANK ACCOUNT

Dr.

CR.

Date Particulars

Jou

rnal

Foli

o £ Date Particulars

Jou

rna

l

Fol

io £

01/10/20 To capital 8000 02/10/20 By laptop 1000

05/10/20 To sales 1500 24/10/20 By car 2500

21/10/20 To capital 500 26/10/20 By Wages 820

3

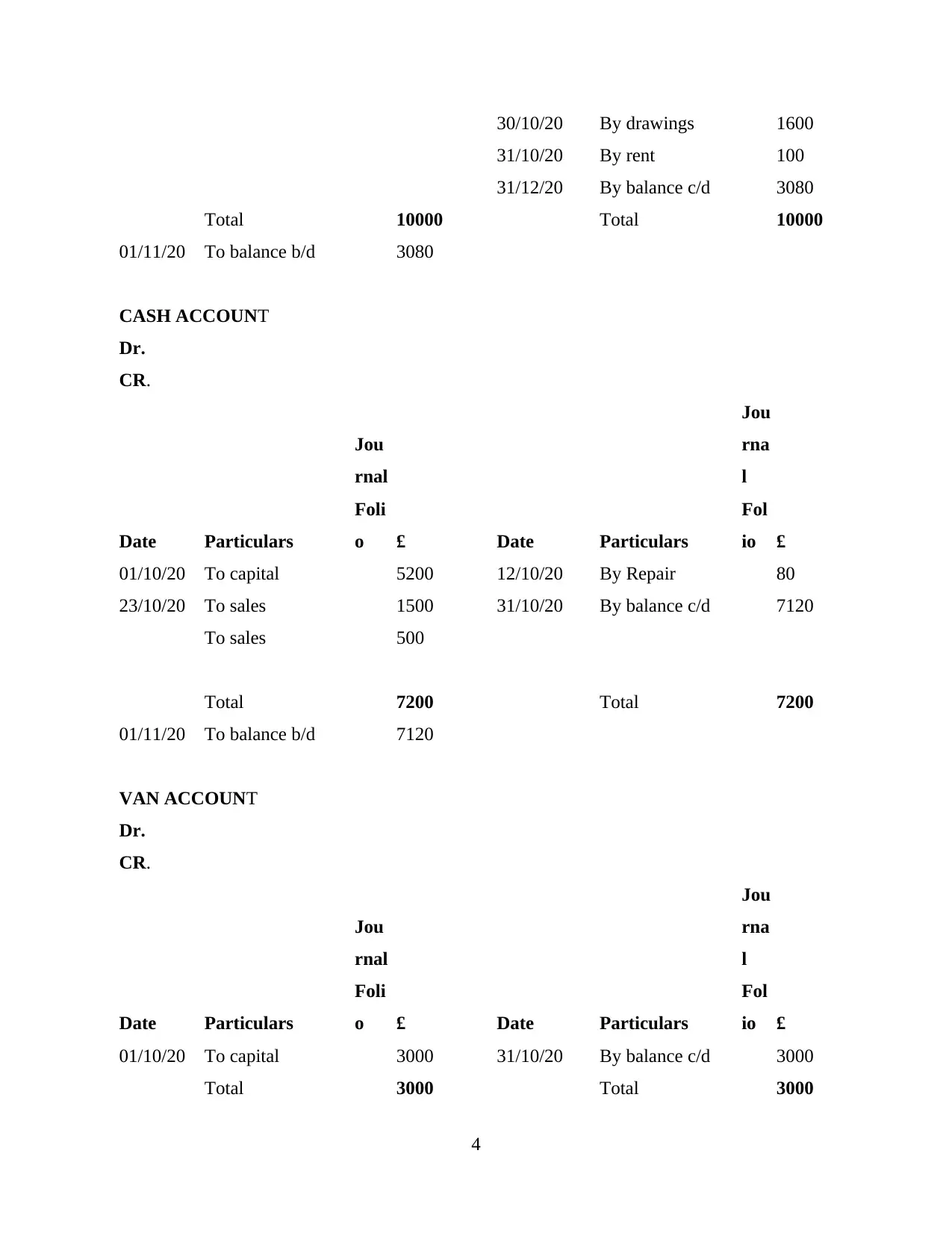

30/10/20 By drawings 1600

31/10/20 By rent 100

31/12/20 By balance c/d 3080

Total 10000 Total 10000

01/11/20 To balance b/d 3080

CASH ACCOUNT

Dr.

CR.

Date Particulars

Jou

rnal

Foli

o £ Date Particulars

Jou

rna

l

Fol

io £

01/10/20 To capital 5200 12/10/20 By Repair 80

23/10/20 To sales 1500 31/10/20 By balance c/d 7120

To sales 500

Total 7200 Total 7200

01/11/20 To balance b/d 7120

VAN ACCOUNT

Dr.

CR.

Date Particulars

Jou

rnal

Foli

o £ Date Particulars

Jou

rna

l

Fol

io £

01/10/20 To capital 3000 31/10/20 By balance c/d 3000

Total 3000 Total 3000

4

31/10/20 By rent 100

31/12/20 By balance c/d 3080

Total 10000 Total 10000

01/11/20 To balance b/d 3080

CASH ACCOUNT

Dr.

CR.

Date Particulars

Jou

rnal

Foli

o £ Date Particulars

Jou

rna

l

Fol

io £

01/10/20 To capital 5200 12/10/20 By Repair 80

23/10/20 To sales 1500 31/10/20 By balance c/d 7120

To sales 500

Total 7200 Total 7200

01/11/20 To balance b/d 7120

VAN ACCOUNT

Dr.

CR.

Date Particulars

Jou

rnal

Foli

o £ Date Particulars

Jou

rna

l

Fol

io £

01/10/20 To capital 3000 31/10/20 By balance c/d 3000

Total 3000 Total 3000

4

01/11/20 To balance b/d 3000

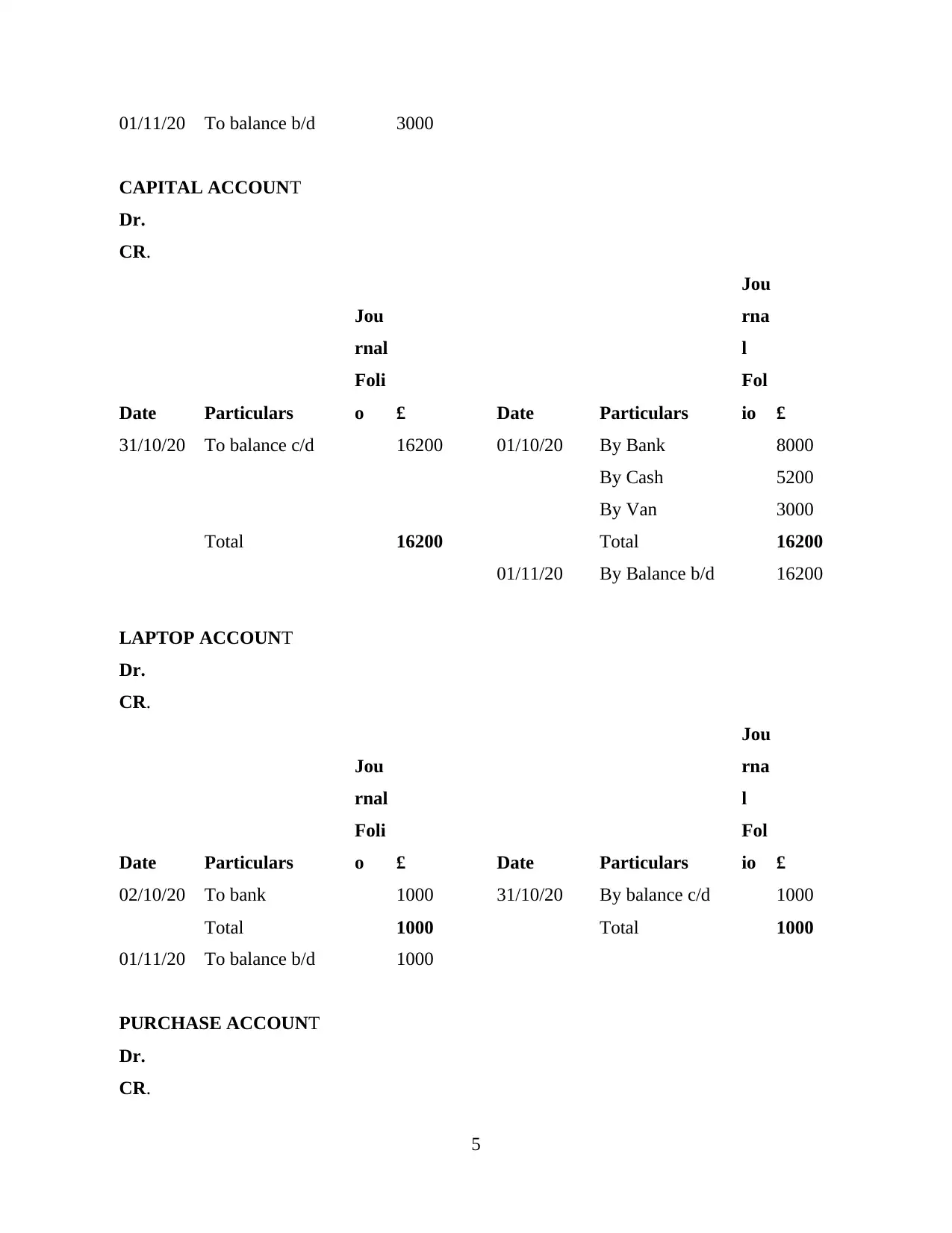

CAPITAL ACCOUNT

Dr.

CR.

Date Particulars

Jou

rnal

Foli

o £ Date Particulars

Jou

rna

l

Fol

io £

31/10/20 To balance c/d 16200 01/10/20 By Bank 8000

By Cash 5200

By Van 3000

Total 16200 Total 16200

01/11/20 By Balance b/d 16200

LAPTOP ACCOUNT

Dr.

CR.

Date Particulars

Jou

rnal

Foli

o £ Date Particulars

Jou

rna

l

Fol

io £

02/10/20 To bank 1000 31/10/20 By balance c/d 1000

Total 1000 Total 1000

01/11/20 To balance b/d 1000

PURCHASE ACCOUNT

Dr.

CR.

5

CAPITAL ACCOUNT

Dr.

CR.

Date Particulars

Jou

rnal

Foli

o £ Date Particulars

Jou

rna

l

Fol

io £

31/10/20 To balance c/d 16200 01/10/20 By Bank 8000

By Cash 5200

By Van 3000

Total 16200 Total 16200

01/11/20 By Balance b/d 16200

LAPTOP ACCOUNT

Dr.

CR.

Date Particulars

Jou

rnal

Foli

o £ Date Particulars

Jou

rna

l

Fol

io £

02/10/20 To bank 1000 31/10/20 By balance c/d 1000

Total 1000 Total 1000

01/11/20 To balance b/d 1000

PURCHASE ACCOUNT

Dr.

CR.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Date Particulars

Jou

rnal

Foli

o £ Date Particulars

Jou

rna

l

Fol

io £

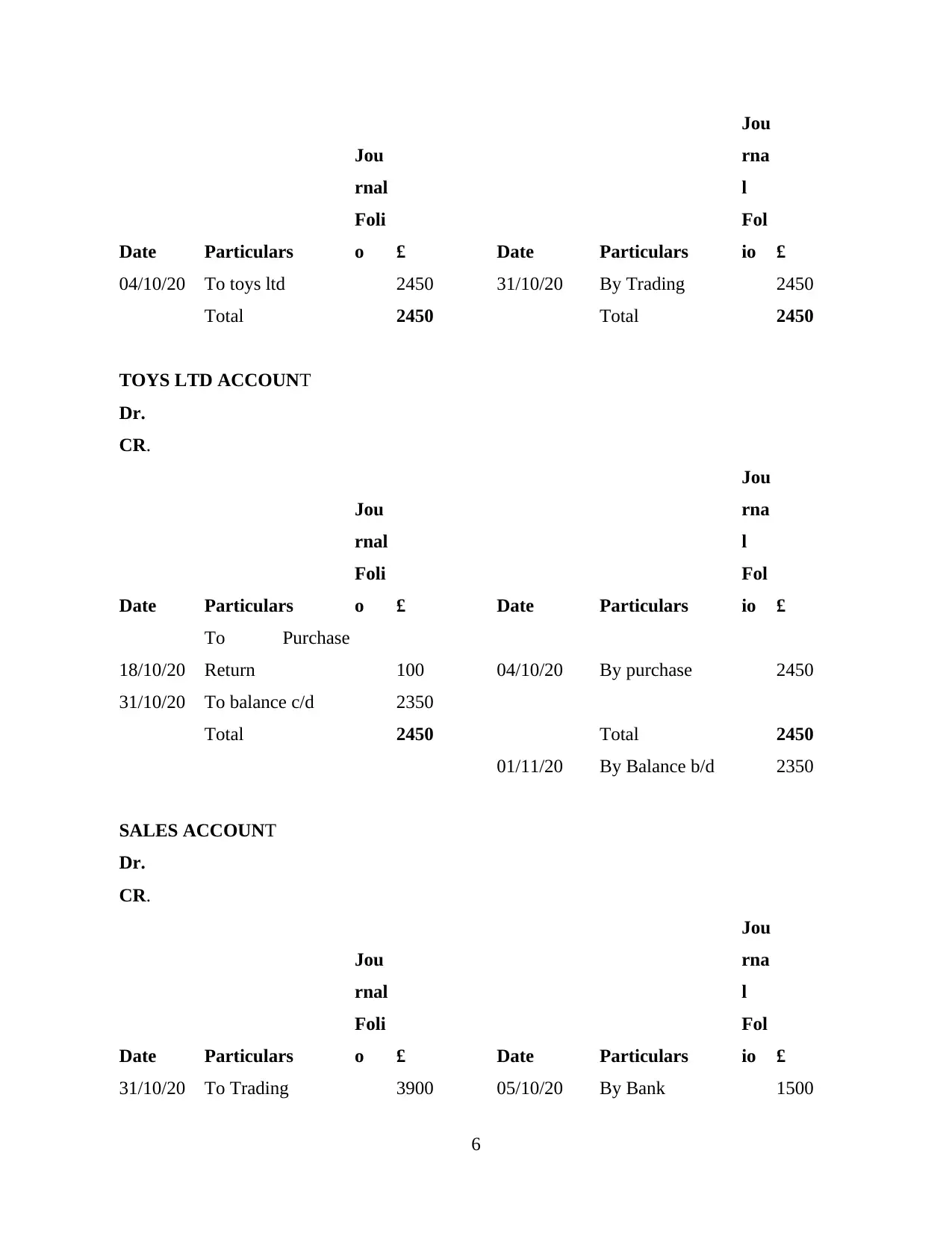

04/10/20 To toys ltd 2450 31/10/20 By Trading 2450

Total 2450 Total 2450

TOYS LTD ACCOUNT

Dr.

CR.

Date Particulars

Jou

rnal

Foli

o £ Date Particulars

Jou

rna

l

Fol

io £

18/10/20

To Purchase

Return 100 04/10/20 By purchase 2450

31/10/20 To balance c/d 2350

Total 2450 Total 2450

01/11/20 By Balance b/d 2350

SALES ACCOUNT

Dr.

CR.

Date Particulars

Jou

rnal

Foli

o £ Date Particulars

Jou

rna

l

Fol

io £

31/10/20 To Trading 3900 05/10/20 By Bank 1500

6

Jou

rnal

Foli

o £ Date Particulars

Jou

rna

l

Fol

io £

04/10/20 To toys ltd 2450 31/10/20 By Trading 2450

Total 2450 Total 2450

TOYS LTD ACCOUNT

Dr.

CR.

Date Particulars

Jou

rnal

Foli

o £ Date Particulars

Jou

rna

l

Fol

io £

18/10/20

To Purchase

Return 100 04/10/20 By purchase 2450

31/10/20 To balance c/d 2350

Total 2450 Total 2450

01/11/20 By Balance b/d 2350

SALES ACCOUNT

Dr.

CR.

Date Particulars

Jou

rnal

Foli

o £ Date Particulars

Jou

rna

l

Fol

io £

31/10/20 To Trading 3900 05/10/20 By Bank 1500

6

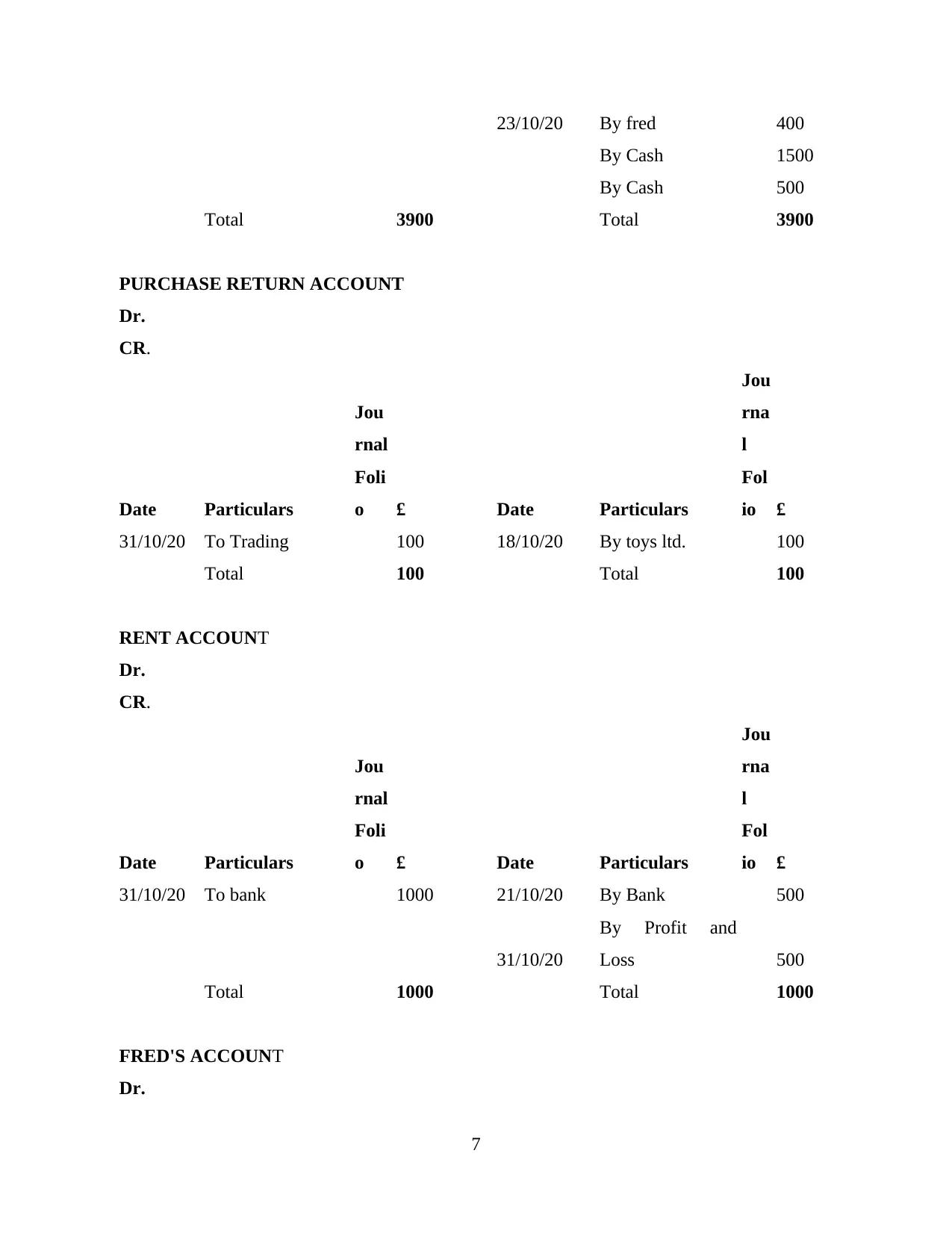

23/10/20 By fred 400

By Cash 1500

By Cash 500

Total 3900 Total 3900

PURCHASE RETURN ACCOUNT

Dr.

CR.

Date Particulars

Jou

rnal

Foli

o £ Date Particulars

Jou

rna

l

Fol

io £

31/10/20 To Trading 100 18/10/20 By toys ltd. 100

Total 100 Total 100

RENT ACCOUNT

Dr.

CR.

Date Particulars

Jou

rnal

Foli

o £ Date Particulars

Jou

rna

l

Fol

io £

31/10/20 To bank 1000 21/10/20 By Bank 500

31/10/20

By Profit and

Loss 500

Total 1000 Total 1000

FRED'S ACCOUNT

Dr.

7

By Cash 1500

By Cash 500

Total 3900 Total 3900

PURCHASE RETURN ACCOUNT

Dr.

CR.

Date Particulars

Jou

rnal

Foli

o £ Date Particulars

Jou

rna

l

Fol

io £

31/10/20 To Trading 100 18/10/20 By toys ltd. 100

Total 100 Total 100

RENT ACCOUNT

Dr.

CR.

Date Particulars

Jou

rnal

Foli

o £ Date Particulars

Jou

rna

l

Fol

io £

31/10/20 To bank 1000 21/10/20 By Bank 500

31/10/20

By Profit and

Loss 500

Total 1000 Total 1000

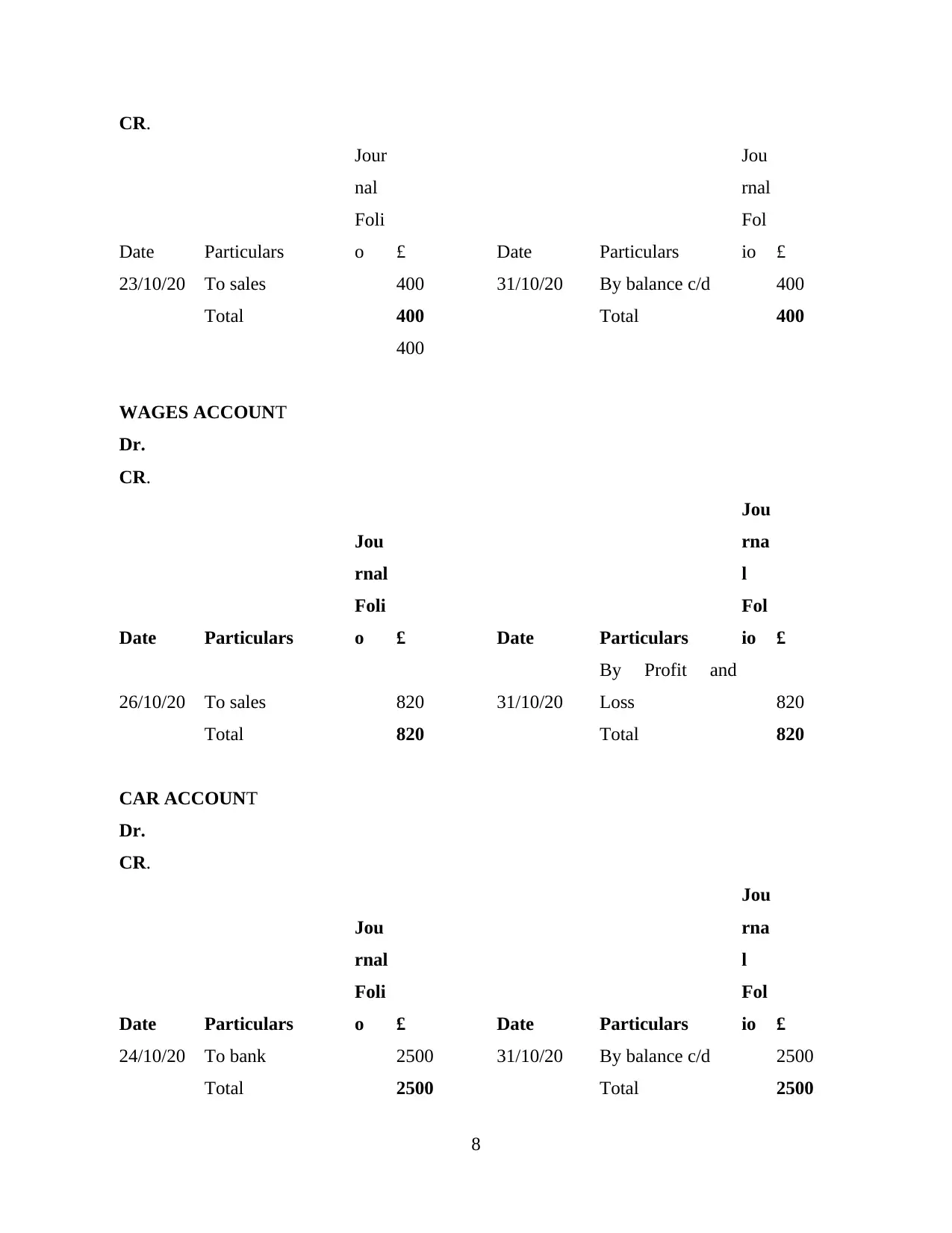

FRED'S ACCOUNT

Dr.

7

CR.

Date Particulars

Jour

nal

Foli

o £ Date Particulars

Jou

rnal

Fol

io £

23/10/20 To sales 400 31/10/20 By balance c/d 400

Total 400 Total 400

400

WAGES ACCOUNT

Dr.

CR.

Date Particulars

Jou

rnal

Foli

o £ Date Particulars

Jou

rna

l

Fol

io £

26/10/20 To sales 820 31/10/20

By Profit and

Loss 820

Total 820 Total 820

CAR ACCOUNT

Dr.

CR.

Date Particulars

Jou

rnal

Foli

o £ Date Particulars

Jou

rna

l

Fol

io £

24/10/20 To bank 2500 31/10/20 By balance c/d 2500

Total 2500 Total 2500

8

Date Particulars

Jour

nal

Foli

o £ Date Particulars

Jou

rnal

Fol

io £

23/10/20 To sales 400 31/10/20 By balance c/d 400

Total 400 Total 400

400

WAGES ACCOUNT

Dr.

CR.

Date Particulars

Jou

rnal

Foli

o £ Date Particulars

Jou

rna

l

Fol

io £

26/10/20 To sales 820 31/10/20

By Profit and

Loss 820

Total 820 Total 820

CAR ACCOUNT

Dr.

CR.

Date Particulars

Jou

rnal

Foli

o £ Date Particulars

Jou

rna

l

Fol

io £

24/10/20 To bank 2500 31/10/20 By balance c/d 2500

Total 2500 Total 2500

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

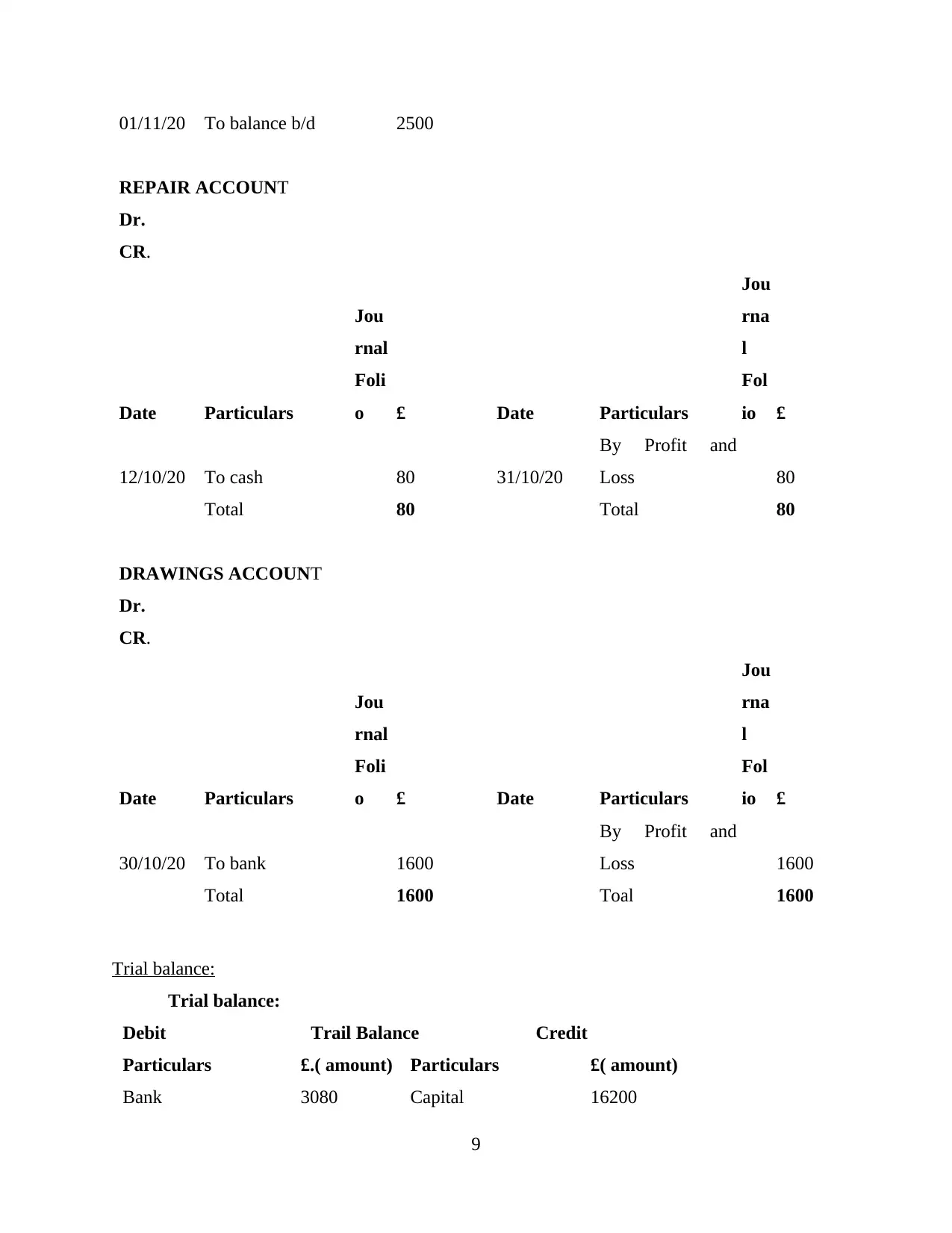

01/11/20 To balance b/d 2500

REPAIR ACCOUNT

Dr.

CR.

Date Particulars

Jou

rnal

Foli

o £ Date Particulars

Jou

rna

l

Fol

io £

12/10/20 To cash 80 31/10/20

By Profit and

Loss 80

Total 80 Total 80

DRAWINGS ACCOUNT

Dr.

CR.

Date Particulars

Jou

rnal

Foli

o £ Date Particulars

Jou

rna

l

Fol

io £

30/10/20 To bank 1600

By Profit and

Loss 1600

Total 1600 Toal 1600

Trial balance:

Trial balance:

Debit Trail Balance Credit

Particulars £.( amount) Particulars £( amount)

Bank 3080 Capital 16200

9

REPAIR ACCOUNT

Dr.

CR.

Date Particulars

Jou

rnal

Foli

o £ Date Particulars

Jou

rna

l

Fol

io £

12/10/20 To cash 80 31/10/20

By Profit and

Loss 80

Total 80 Total 80

DRAWINGS ACCOUNT

Dr.

CR.

Date Particulars

Jou

rnal

Foli

o £ Date Particulars

Jou

rna

l

Fol

io £

30/10/20 To bank 1600

By Profit and

Loss 1600

Total 1600 Toal 1600

Trial balance:

Trial balance:

Debit Trail Balance Credit

Particulars £.( amount) Particulars £( amount)

Bank 3080 Capital 16200

9

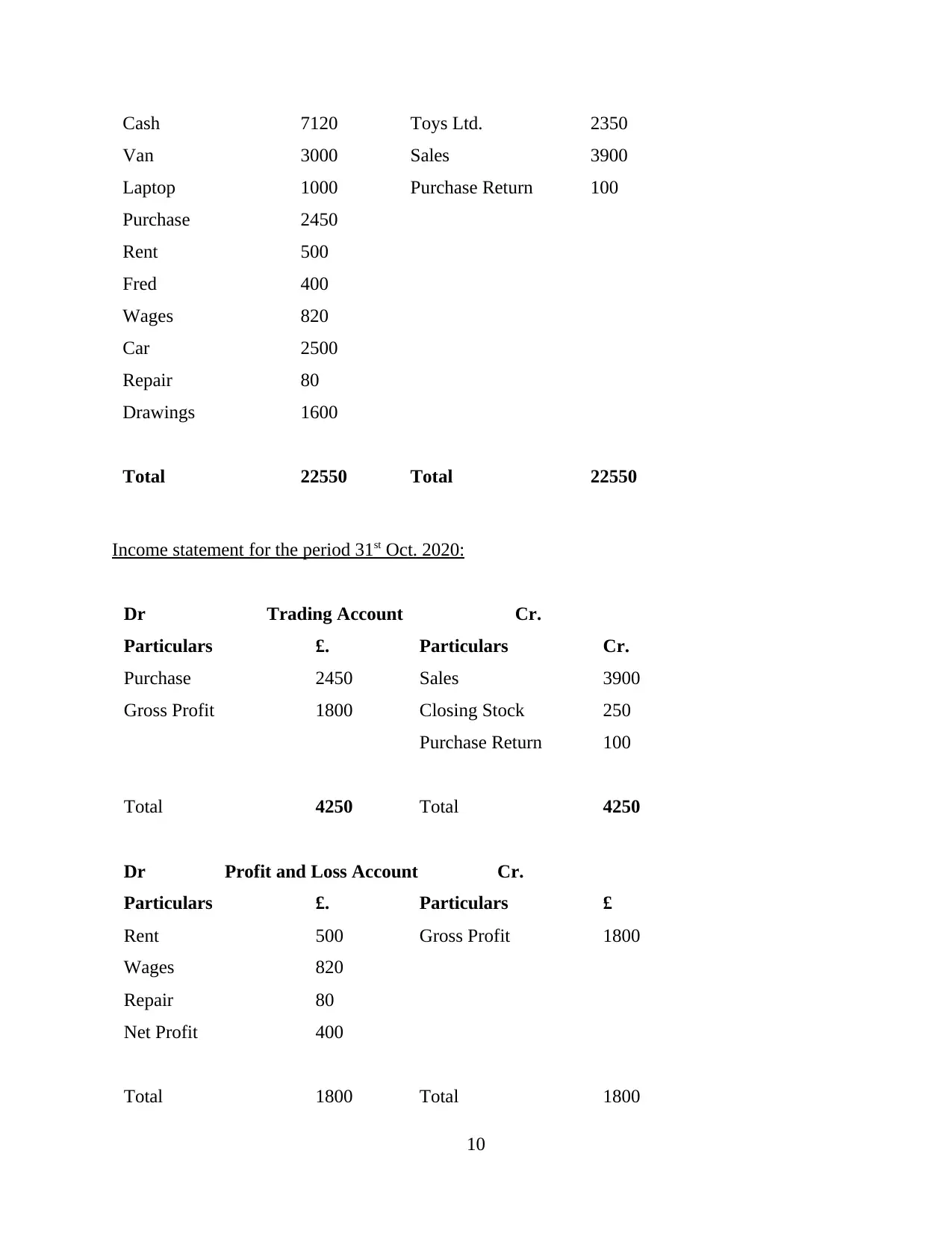

Cash 7120 Toys Ltd. 2350

Van 3000 Sales 3900

Laptop 1000 Purchase Return 100

Purchase 2450

Rent 500

Fred 400

Wages 820

Car 2500

Repair 80

Drawings 1600

Total 22550 Total 22550

Income statement for the period 31st Oct. 2020:

Dr Trading Account Cr.

Particulars £. Particulars Cr.

Purchase 2450 Sales 3900

Gross Profit 1800 Closing Stock 250

Purchase Return 100

Total 4250 Total 4250

Dr Profit and Loss Account Cr.

Particulars £. Particulars £

Rent 500 Gross Profit 1800

Wages 820

Repair 80

Net Profit 400

Total 1800 Total 1800

10

Van 3000 Sales 3900

Laptop 1000 Purchase Return 100

Purchase 2450

Rent 500

Fred 400

Wages 820

Car 2500

Repair 80

Drawings 1600

Total 22550 Total 22550

Income statement for the period 31st Oct. 2020:

Dr Trading Account Cr.

Particulars £. Particulars Cr.

Purchase 2450 Sales 3900

Gross Profit 1800 Closing Stock 250

Purchase Return 100

Total 4250 Total 4250

Dr Profit and Loss Account Cr.

Particulars £. Particulars £

Rent 500 Gross Profit 1800

Wages 820

Repair 80

Net Profit 400

Total 1800 Total 1800

10

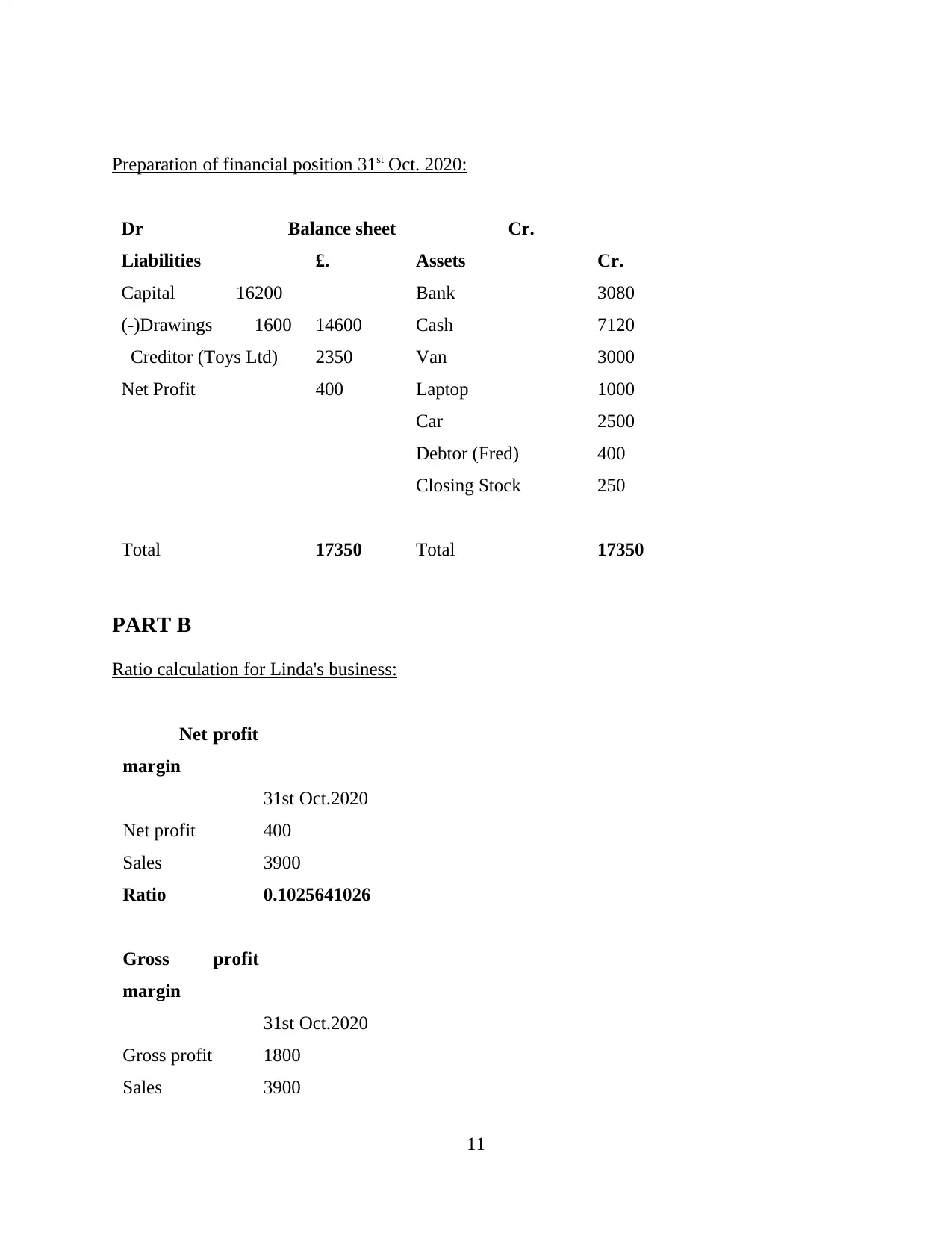

Preparation of financial position 31st Oct. 2020:

Dr Balance sheet Cr.

Liabilities £. Assets Cr.

Capital 16200 Bank 3080

(-)Drawings 1600 14600 Cash 7120

Creditor (Toys Ltd) 2350 Van 3000

Net Profit 400 Laptop 1000

Car 2500

Debtor (Fred) 400

Closing Stock 250

Total 17350 Total 17350

PART B

Ratio calculation for Linda's business:

Net profit

margin

31st Oct.2020

Net profit 400

Sales 3900

Ratio 0.1025641026

Gross profit

margin

31st Oct.2020

Gross profit 1800

Sales 3900

11

Dr Balance sheet Cr.

Liabilities £. Assets Cr.

Capital 16200 Bank 3080

(-)Drawings 1600 14600 Cash 7120

Creditor (Toys Ltd) 2350 Van 3000

Net Profit 400 Laptop 1000

Car 2500

Debtor (Fred) 400

Closing Stock 250

Total 17350 Total 17350

PART B

Ratio calculation for Linda's business:

Net profit

margin

31st Oct.2020

Net profit 400

Sales 3900

Ratio 0.1025641026

Gross profit

margin

31st Oct.2020

Gross profit 1800

Sales 3900

11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

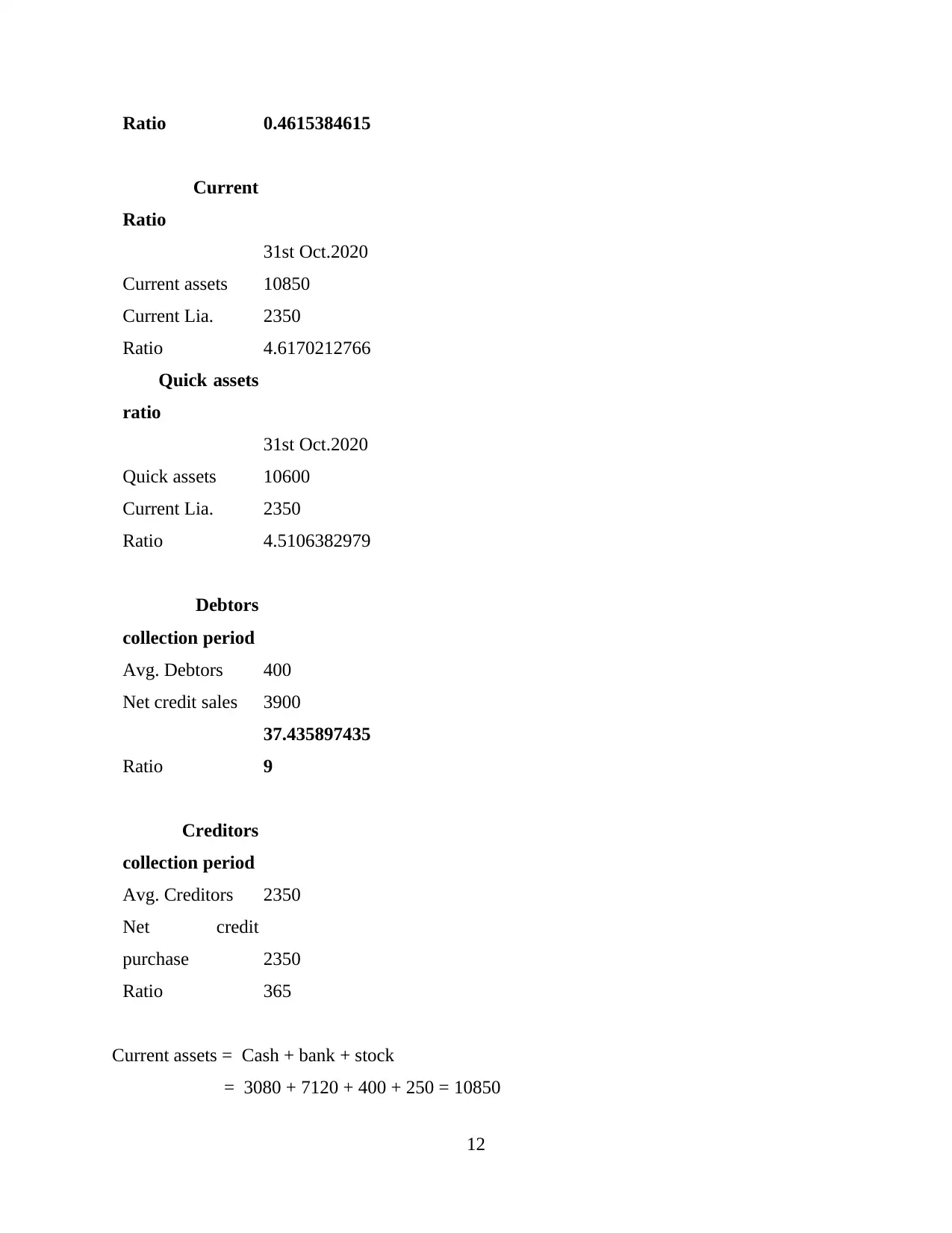

Ratio 0.4615384615

Current

Ratio

31st Oct.2020

Current assets 10850

Current Lia. 2350

Ratio 4.6170212766

Quick assets

ratio

31st Oct.2020

Quick assets 10600

Current Lia. 2350

Ratio 4.5106382979

Debtors

collection period

Avg. Debtors 400

Net credit sales 3900

Ratio

37.435897435

9

Creditors

collection period

Avg. Creditors 2350

Net credit

purchase 2350

Ratio 365

Current assets = Cash + bank + stock

= 3080 + 7120 + 400 + 250 = 10850

12

Current

Ratio

31st Oct.2020

Current assets 10850

Current Lia. 2350

Ratio 4.6170212766

Quick assets

ratio

31st Oct.2020

Quick assets 10600

Current Lia. 2350

Ratio 4.5106382979

Debtors

collection period

Avg. Debtors 400

Net credit sales 3900

Ratio

37.435897435

9

Creditors

collection period

Avg. Creditors 2350

Net credit

purchase 2350

Ratio 365

Current assets = Cash + bank + stock

= 3080 + 7120 + 400 + 250 = 10850

12

Quick Assets = Current assets – Stock

= 10850 -250 = 10600

Net Credit Purchase = Purchase – purchase return

= 2450 – 100 = 2350

Analysis of ratio analysis in comparison to its competitors:

Ratio analysis is the process for analysing business position which helps company for

decision making. It views company's position which includes liquidity, solvency, profitability

etc. Ratio analysis is allabo9ut which helps company for making profitable for the business. The

company use ratio analysis for comparing its performance & known for the performance for the

company. Ratio analysis helps business for better decision making which helps for higher

profitability for the businesses (Atah and Bessong, 2018). This analysis about Linda's company

& its competitor. It views about the company Linda's for its various ratios. Standard gross profit

shows 25%, the company has 46% that is good but in comparison to other it has less than 54%.

current ratio of the business is good than its competitors as it shows 4.44 approx that shows firm

has sufficient cash for its business activities because the standard ratio shows 2:1. current ratio is

about higher liquidity for the company which views for current liabilities & current assets for the

company. Liquid ratio about liquidity assets which includes cash & bank.

13

= 10850 -250 = 10600

Net Credit Purchase = Purchase – purchase return

= 2450 – 100 = 2350

Analysis of ratio analysis in comparison to its competitors:

Ratio analysis is the process for analysing business position which helps company for

decision making. It views company's position which includes liquidity, solvency, profitability

etc. Ratio analysis is allabo9ut which helps company for making profitable for the business. The

company use ratio analysis for comparing its performance & known for the performance for the

company. Ratio analysis helps business for better decision making which helps for higher

profitability for the businesses (Atah and Bessong, 2018). This analysis about Linda's company

& its competitor. It views about the company Linda's for its various ratios. Standard gross profit

shows 25%, the company has 46% that is good but in comparison to other it has less than 54%.

current ratio of the business is good than its competitors as it shows 4.44 approx that shows firm

has sufficient cash for its business activities because the standard ratio shows 2:1. current ratio is

about higher liquidity for the company which views for current liabilities & current assets for the

company. Liquid ratio about liquidity assets which includes cash & bank.

13

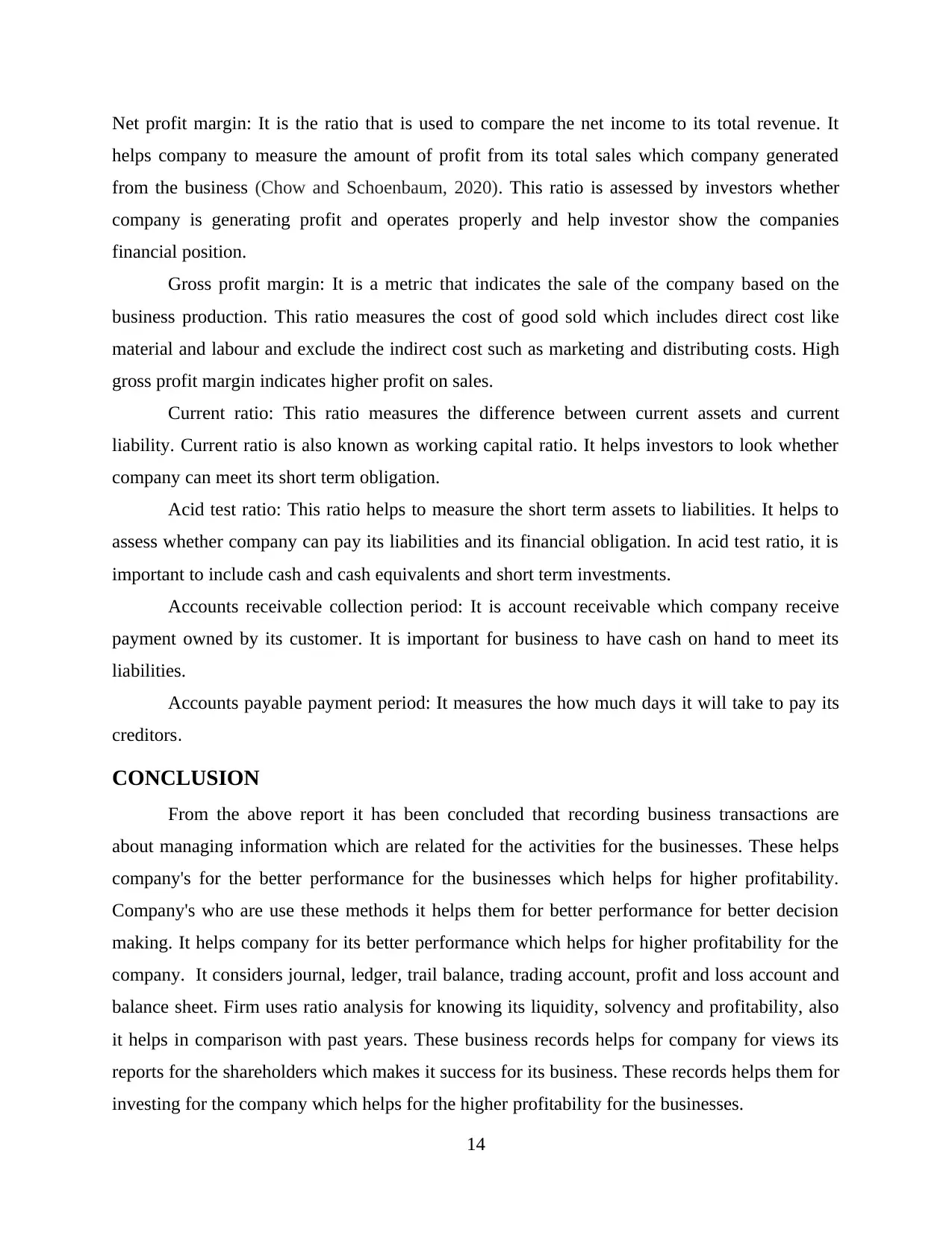

Net profit margin: It is the ratio that is used to compare the net income to its total revenue. It

helps company to measure the amount of profit from its total sales which company generated

from the business (Chow and Schoenbaum, 2020). This ratio is assessed by investors whether

company is generating profit and operates properly and help investor show the companies

financial position.

Gross profit margin: It is a metric that indicates the sale of the company based on the

business production. This ratio measures the cost of good sold which includes direct cost like

material and labour and exclude the indirect cost such as marketing and distributing costs. High

gross profit margin indicates higher profit on sales.

Current ratio: This ratio measures the difference between current assets and current

liability. Current ratio is also known as working capital ratio. It helps investors to look whether

company can meet its short term obligation.

Acid test ratio: This ratio helps to measure the short term assets to liabilities. It helps to

assess whether company can pay its liabilities and its financial obligation. In acid test ratio, it is

important to include cash and cash equivalents and short term investments.

Accounts receivable collection period: It is account receivable which company receive

payment owned by its customer. It is important for business to have cash on hand to meet its

liabilities.

Accounts payable payment period: It measures the how much days it will take to pay its

creditors.

CONCLUSION

From the above report it has been concluded that recording business transactions are

about managing information which are related for the activities for the businesses. These helps

company's for the better performance for the businesses which helps for higher profitability.

Company's who are use these methods it helps them for better performance for better decision

making. It helps company for its better performance which helps for higher profitability for the

company. It considers journal, ledger, trail balance, trading account, profit and loss account and

balance sheet. Firm uses ratio analysis for knowing its liquidity, solvency and profitability, also

it helps in comparison with past years. These business records helps for company for views its

reports for the shareholders which makes it success for its business. These records helps them for

investing for the company which helps for the higher profitability for the businesses.

14

helps company to measure the amount of profit from its total sales which company generated

from the business (Chow and Schoenbaum, 2020). This ratio is assessed by investors whether

company is generating profit and operates properly and help investor show the companies

financial position.

Gross profit margin: It is a metric that indicates the sale of the company based on the

business production. This ratio measures the cost of good sold which includes direct cost like

material and labour and exclude the indirect cost such as marketing and distributing costs. High

gross profit margin indicates higher profit on sales.

Current ratio: This ratio measures the difference between current assets and current

liability. Current ratio is also known as working capital ratio. It helps investors to look whether

company can meet its short term obligation.

Acid test ratio: This ratio helps to measure the short term assets to liabilities. It helps to

assess whether company can pay its liabilities and its financial obligation. In acid test ratio, it is

important to include cash and cash equivalents and short term investments.

Accounts receivable collection period: It is account receivable which company receive

payment owned by its customer. It is important for business to have cash on hand to meet its

liabilities.

Accounts payable payment period: It measures the how much days it will take to pay its

creditors.

CONCLUSION

From the above report it has been concluded that recording business transactions are

about managing information which are related for the activities for the businesses. These helps

company's for the better performance for the businesses which helps for higher profitability.

Company's who are use these methods it helps them for better performance for better decision

making. It helps company for its better performance which helps for higher profitability for the

company. It considers journal, ledger, trail balance, trading account, profit and loss account and

balance sheet. Firm uses ratio analysis for knowing its liquidity, solvency and profitability, also

it helps in comparison with past years. These business records helps for company for views its

reports for the shareholders which makes it success for its business. These records helps them for

investing for the company which helps for the higher profitability for the businesses.

14

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REFERENCES

Books and journals:

Adamyk. O. 2017. Audit of Accounting Staff in Computer-Based Environment.

Atah, C. A. and Bessong, B. E. 2018. IMPACT OF RECORD KEEPING FOR

SUSTAINABILITY OFSMALL SCALE BUSINESS OPERATORS FOR NATIONAL

ECONOMY DEVELOPMENTIN NIGERIA. Nigerian Journal of Business Education

(NIGJBED). 5(1). pp. 102-114.

Chow. D. C. and Schoenbaum, T. J., 2020. International business transactions: problems, cases,

and materials. Wolters Kluwer Law & Business.

Corcoran, D. 2016. The Case under the GDPR for Video and Audio Recording in Commercial

Spaces and Interactions: An Example of Fitting Legacy Systems and Practices into a

Forward-Looking Compliance Regime. Int'l. In-House Counsel J. 10. p.1.

Harahap, H. H. and Zulkarnain, N. J. R. 2020. THE ONLINE BUSINESS TRANSACTIONS IN

PERSPECTIVE POSITIVE LAW IN INDONESIA. PalArch's Journal of Archaeology

of Egypt/Egyptology, 17(7). pp.15102-15111.

Li, J. 2020. Globalization of Anglo-American common law vs. strong nation state: Evidence

from the use of legal counsel in cross-border business transactions involving China. The

International Lawyer. 53(3). pp 383-415.

OVSIUK. N. 2020. Valuation and Recording the Value of Innovation Objects in the Accounting

System. Scientific Bulletin of the National Academy of Statistics, Accounting and Audit.

(3). pp.47-54.

Tillman. S. B. 2017. Business Transactions and President Trump's Emoluments Problem.

15

Books and journals:

Adamyk. O. 2017. Audit of Accounting Staff in Computer-Based Environment.

Atah, C. A. and Bessong, B. E. 2018. IMPACT OF RECORD KEEPING FOR

SUSTAINABILITY OFSMALL SCALE BUSINESS OPERATORS FOR NATIONAL

ECONOMY DEVELOPMENTIN NIGERIA. Nigerian Journal of Business Education

(NIGJBED). 5(1). pp. 102-114.

Chow. D. C. and Schoenbaum, T. J., 2020. International business transactions: problems, cases,

and materials. Wolters Kluwer Law & Business.

Corcoran, D. 2016. The Case under the GDPR for Video and Audio Recording in Commercial

Spaces and Interactions: An Example of Fitting Legacy Systems and Practices into a

Forward-Looking Compliance Regime. Int'l. In-House Counsel J. 10. p.1.

Harahap, H. H. and Zulkarnain, N. J. R. 2020. THE ONLINE BUSINESS TRANSACTIONS IN

PERSPECTIVE POSITIVE LAW IN INDONESIA. PalArch's Journal of Archaeology

of Egypt/Egyptology, 17(7). pp.15102-15111.

Li, J. 2020. Globalization of Anglo-American common law vs. strong nation state: Evidence

from the use of legal counsel in cross-border business transactions involving China. The

International Lawyer. 53(3). pp 383-415.

OVSIUK. N. 2020. Valuation and Recording the Value of Innovation Objects in the Accounting

System. Scientific Bulletin of the National Academy of Statistics, Accounting and Audit.

(3). pp.47-54.

Tillman. S. B. 2017. Business Transactions and President Trump's Emoluments Problem.

15

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.