Comprehensive Report: Recording Business Transactions and Analysis

VerifiedAdded on 2022/12/28

|16

|2738

|42

Report

AI Summary

This report delves into the critical process of recording business transactions, the foundation of financial accounting. It details the steps involved, from journal entries to the creation of ledger accounts, the trial balance, income statements, and statements of financial position. The report emphasizes the importance of accurate transaction recording for assessing a company's profitability. Furthermore, it includes a practical application of ratio analysis to evaluate Linda's business performance, comparing it to competitors. The analysis covers net profit margin, gross profit margin, current ratio, acid test ratio, and efficiency ratios like accounts receivable and payable collection periods. The report highlights areas for improvement, such as managing indirect expenses, optimizing asset allocation, and enhancing efficiency to boost financial performance. The conclusion emphasizes the significance of correct financial recording for insightful financial statement preparation.

RECORDING BUSINESS

TRANSACTION

TRANSACTION

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

a. Double entry recording transaction.........................................................................................3

b. Balancing accounts..................................................................................................................3

c. Trial balance............................................................................................................................7

d. Income statement....................................................................................................................8

e. Financial position....................................................................................................................9

f. Brief letter to Linda.................................................................................................................9

PART B..........................................................................................................................................10

a. Ratio calculation for Linda’s business..................................................................................10

b. Analysis of performance of Linda’s business in comparison to competitors.......................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

APPENDIX....................................................................................................................................15

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

a. Double entry recording transaction.........................................................................................3

b. Balancing accounts..................................................................................................................3

c. Trial balance............................................................................................................................7

d. Income statement....................................................................................................................8

e. Financial position....................................................................................................................9

f. Brief letter to Linda.................................................................................................................9

PART B..........................................................................................................................................10

a. Ratio calculation for Linda’s business..................................................................................10

b. Analysis of performance of Linda’s business in comparison to competitors.......................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

APPENDIX....................................................................................................................................15

INTRODUCTION

Recording business transaction is defined as recording of all the financial transaction

within the books of accounts in order to calculate and summaries the profitability of company

within the financial statements of company (OVSIUK, 2020). For any organization recording all

business transaction is the most crucial step as this is the base for making the financial statements

and articulating the profit or loss incurred. the present report is based on the recording of

transaction based on transaction occurred in business. then the report will highlight ledger

accounts prepared and after that trial balance will be extracted and profit and loss account will be

created. in addition to this the profitability of company will be assessed with help of the ratio

analysis. ratio analysis is a technique which assist company in comparing the profitability,

liquidity and solvency of company with the competitor within the industry. this will assist the

company in managing and improving its financial position to a great extent.

PART A

a. Double entry recording transaction

For the making of financial statement, the most essential thing is the recording of

business transaction in proper and effective manner. This is particularly because of the reason

that when the company will record all financial transaction in journal then they will have been

posted in ledger and trial balance will be prepared. Hence, effective making of financial

statement only crucial thing required is recording transaction in proper and effective manner.

(journal entry in appendix)

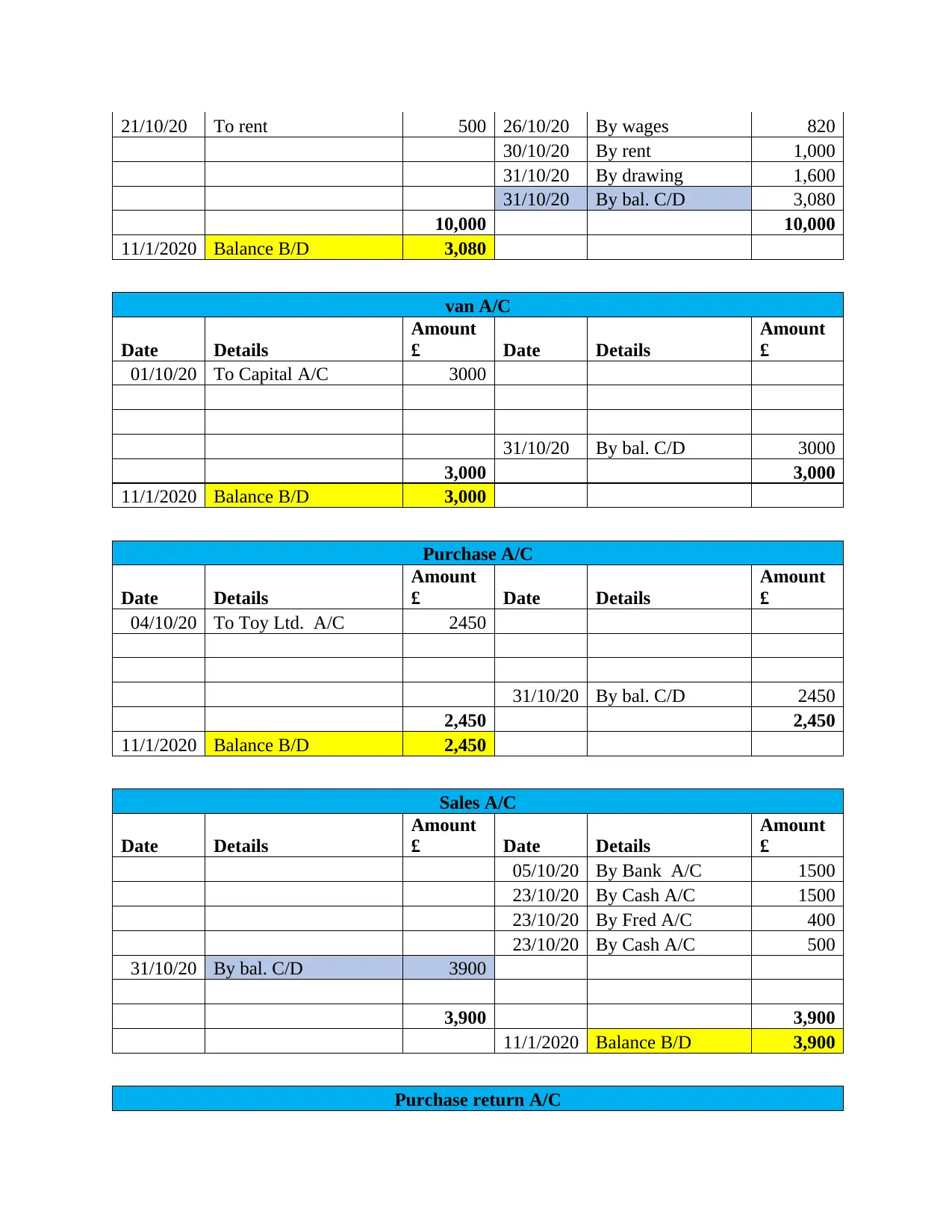

b. Balancing accounts

Just recording the business is not enough for making the financial statements rather it is

essential to post the transaction in correct manner in ledger accounts. The ledger account is a

type of account which records all entries in the particular accounts (Wulanditya and Aprillianita,

2018). From here the balance are taken and with help of this trial balance is prepared and further

financial statement is being prepared.

Bank A/C

Date Details

Amount

£ Date Details

Amount

£

1/10/2020 To capital 8,000 2/10/2020 By laptop 1,000

5/10/2020 To sales 1,500 24/10/20 By second hand car 2,500

Recording business transaction is defined as recording of all the financial transaction

within the books of accounts in order to calculate and summaries the profitability of company

within the financial statements of company (OVSIUK, 2020). For any organization recording all

business transaction is the most crucial step as this is the base for making the financial statements

and articulating the profit or loss incurred. the present report is based on the recording of

transaction based on transaction occurred in business. then the report will highlight ledger

accounts prepared and after that trial balance will be extracted and profit and loss account will be

created. in addition to this the profitability of company will be assessed with help of the ratio

analysis. ratio analysis is a technique which assist company in comparing the profitability,

liquidity and solvency of company with the competitor within the industry. this will assist the

company in managing and improving its financial position to a great extent.

PART A

a. Double entry recording transaction

For the making of financial statement, the most essential thing is the recording of

business transaction in proper and effective manner. This is particularly because of the reason

that when the company will record all financial transaction in journal then they will have been

posted in ledger and trial balance will be prepared. Hence, effective making of financial

statement only crucial thing required is recording transaction in proper and effective manner.

(journal entry in appendix)

b. Balancing accounts

Just recording the business is not enough for making the financial statements rather it is

essential to post the transaction in correct manner in ledger accounts. The ledger account is a

type of account which records all entries in the particular accounts (Wulanditya and Aprillianita,

2018). From here the balance are taken and with help of this trial balance is prepared and further

financial statement is being prepared.

Bank A/C

Date Details

Amount

£ Date Details

Amount

£

1/10/2020 To capital 8,000 2/10/2020 By laptop 1,000

5/10/2020 To sales 1,500 24/10/20 By second hand car 2,500

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

21/10/20 To rent 500 26/10/20 By wages 820

30/10/20 By rent 1,000

31/10/20 By drawing 1,600

31/10/20 By bal. C/D 3,080

10,000 10,000

11/1/2020 Balance B/D 3,080

van A/C

Date Details

Amount

£ Date Details

Amount

£

01/10/20 To Capital A/C 3000

31/10/20 By bal. C/D 3000

3,000 3,000

11/1/2020 Balance B/D 3,000

Purchase A/C

Date Details

Amount

£ Date Details

Amount

£

04/10/20 To Toy Ltd. A/C 2450

31/10/20 By bal. C/D 2450

2,450 2,450

11/1/2020 Balance B/D 2,450

Sales A/C

Date Details

Amount

£ Date Details

Amount

£

05/10/20 By Bank A/C 1500

23/10/20 By Cash A/C 1500

23/10/20 By Fred A/C 400

23/10/20 By Cash A/C 500

31/10/20 By bal. C/D 3900

3,900 3,900

11/1/2020 Balance B/D 3,900

Purchase return A/C

30/10/20 By rent 1,000

31/10/20 By drawing 1,600

31/10/20 By bal. C/D 3,080

10,000 10,000

11/1/2020 Balance B/D 3,080

van A/C

Date Details

Amount

£ Date Details

Amount

£

01/10/20 To Capital A/C 3000

31/10/20 By bal. C/D 3000

3,000 3,000

11/1/2020 Balance B/D 3,000

Purchase A/C

Date Details

Amount

£ Date Details

Amount

£

04/10/20 To Toy Ltd. A/C 2450

31/10/20 By bal. C/D 2450

2,450 2,450

11/1/2020 Balance B/D 2,450

Sales A/C

Date Details

Amount

£ Date Details

Amount

£

05/10/20 By Bank A/C 1500

23/10/20 By Cash A/C 1500

23/10/20 By Fred A/C 400

23/10/20 By Cash A/C 500

31/10/20 By bal. C/D 3900

3,900 3,900

11/1/2020 Balance B/D 3,900

Purchase return A/C

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Date Details

Amount

£ Date Details

Amount

£

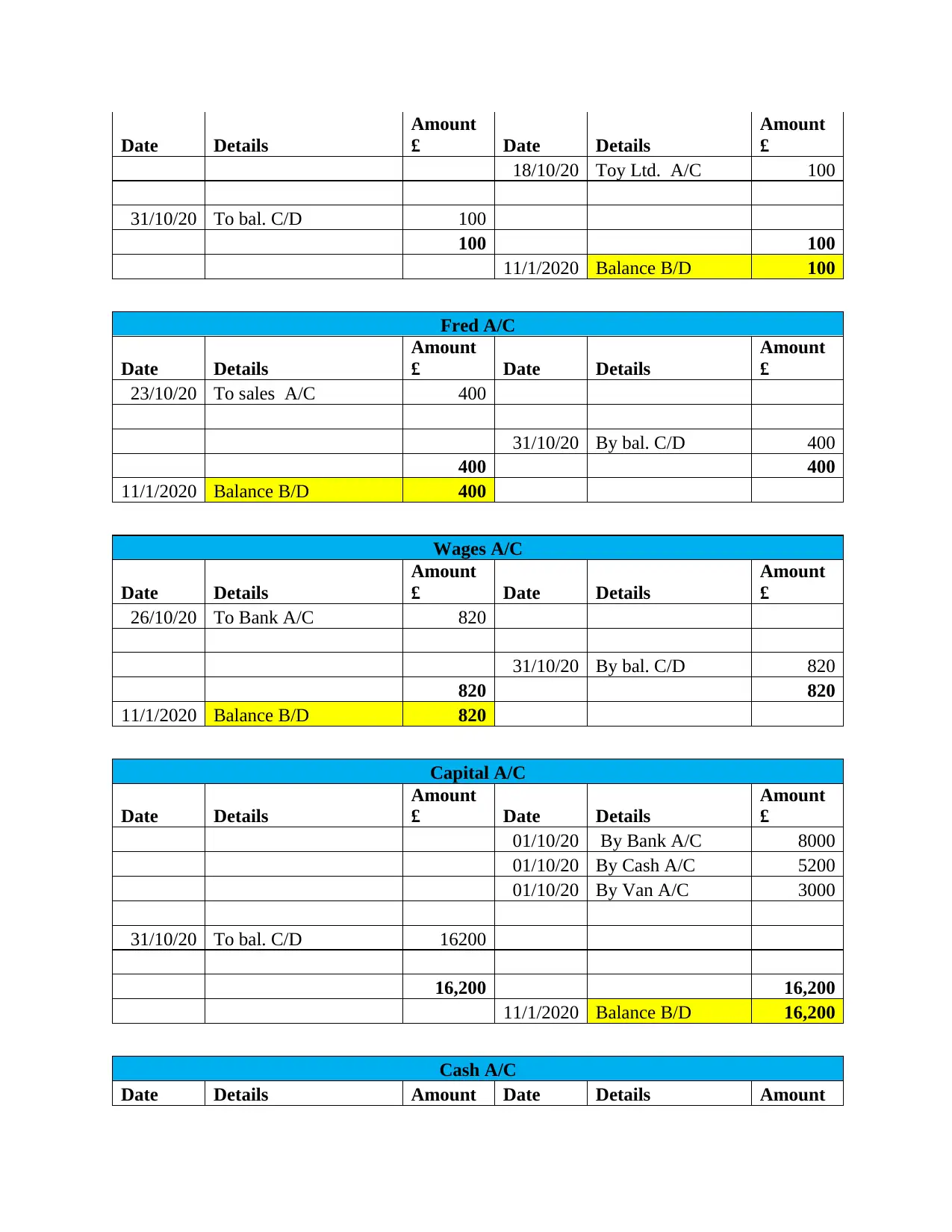

18/10/20 Toy Ltd. A/C 100

31/10/20 To bal. C/D 100

100 100

11/1/2020 Balance B/D 100

Fred A/C

Date Details

Amount

£ Date Details

Amount

£

23/10/20 To sales A/C 400

31/10/20 By bal. C/D 400

400 400

11/1/2020 Balance B/D 400

Wages A/C

Date Details

Amount

£ Date Details

Amount

£

26/10/20 To Bank A/C 820

31/10/20 By bal. C/D 820

820 820

11/1/2020 Balance B/D 820

Capital A/C

Date Details

Amount

£ Date Details

Amount

£

01/10/20 By Bank A/C 8000

01/10/20 By Cash A/C 5200

01/10/20 By Van A/C 3000

31/10/20 To bal. C/D 16200

16,200 16,200

11/1/2020 Balance B/D 16,200

Cash A/C

Date Details Amount Date Details Amount

Amount

£ Date Details

Amount

£

18/10/20 Toy Ltd. A/C 100

31/10/20 To bal. C/D 100

100 100

11/1/2020 Balance B/D 100

Fred A/C

Date Details

Amount

£ Date Details

Amount

£

23/10/20 To sales A/C 400

31/10/20 By bal. C/D 400

400 400

11/1/2020 Balance B/D 400

Wages A/C

Date Details

Amount

£ Date Details

Amount

£

26/10/20 To Bank A/C 820

31/10/20 By bal. C/D 820

820 820

11/1/2020 Balance B/D 820

Capital A/C

Date Details

Amount

£ Date Details

Amount

£

01/10/20 By Bank A/C 8000

01/10/20 By Cash A/C 5200

01/10/20 By Van A/C 3000

31/10/20 To bal. C/D 16200

16,200 16,200

11/1/2020 Balance B/D 16,200

Cash A/C

Date Details Amount Date Details Amount

£ £

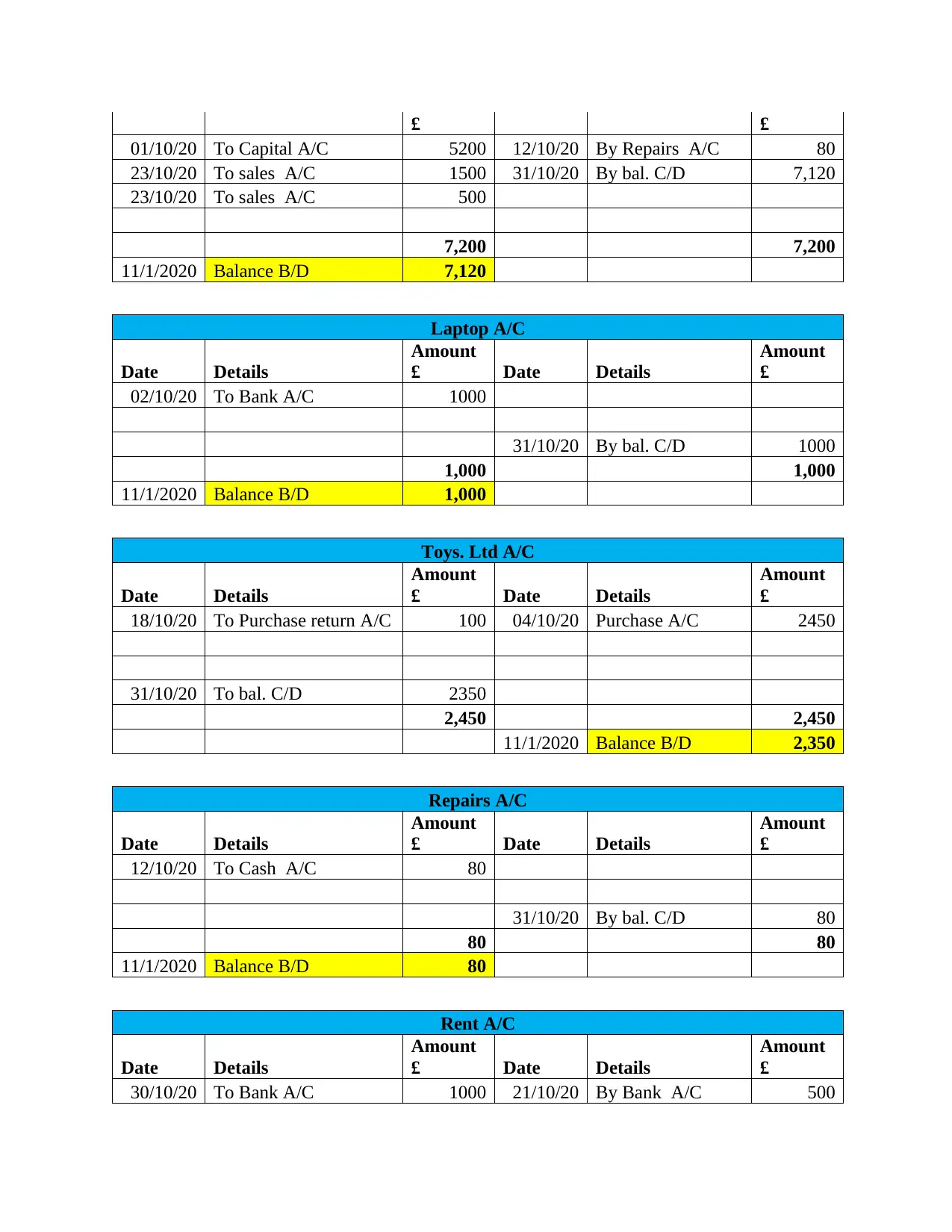

01/10/20 To Capital A/C 5200 12/10/20 By Repairs A/C 80

23/10/20 To sales A/C 1500 31/10/20 By bal. C/D 7,120

23/10/20 To sales A/C 500

7,200 7,200

11/1/2020 Balance B/D 7,120

Laptop A/C

Date Details

Amount

£ Date Details

Amount

£

02/10/20 To Bank A/C 1000

31/10/20 By bal. C/D 1000

1,000 1,000

11/1/2020 Balance B/D 1,000

Toys. Ltd A/C

Date Details

Amount

£ Date Details

Amount

£

18/10/20 To Purchase return A/C 100 04/10/20 Purchase A/C 2450

31/10/20 To bal. C/D 2350

2,450 2,450

11/1/2020 Balance B/D 2,350

Repairs A/C

Date Details

Amount

£ Date Details

Amount

£

12/10/20 To Cash A/C 80

31/10/20 By bal. C/D 80

80 80

11/1/2020 Balance B/D 80

Rent A/C

Date Details

Amount

£ Date Details

Amount

£

30/10/20 To Bank A/C 1000 21/10/20 By Bank A/C 500

01/10/20 To Capital A/C 5200 12/10/20 By Repairs A/C 80

23/10/20 To sales A/C 1500 31/10/20 By bal. C/D 7,120

23/10/20 To sales A/C 500

7,200 7,200

11/1/2020 Balance B/D 7,120

Laptop A/C

Date Details

Amount

£ Date Details

Amount

£

02/10/20 To Bank A/C 1000

31/10/20 By bal. C/D 1000

1,000 1,000

11/1/2020 Balance B/D 1,000

Toys. Ltd A/C

Date Details

Amount

£ Date Details

Amount

£

18/10/20 To Purchase return A/C 100 04/10/20 Purchase A/C 2450

31/10/20 To bal. C/D 2350

2,450 2,450

11/1/2020 Balance B/D 2,350

Repairs A/C

Date Details

Amount

£ Date Details

Amount

£

12/10/20 To Cash A/C 80

31/10/20 By bal. C/D 80

80 80

11/1/2020 Balance B/D 80

Rent A/C

Date Details

Amount

£ Date Details

Amount

£

30/10/20 To Bank A/C 1000 21/10/20 By Bank A/C 500

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

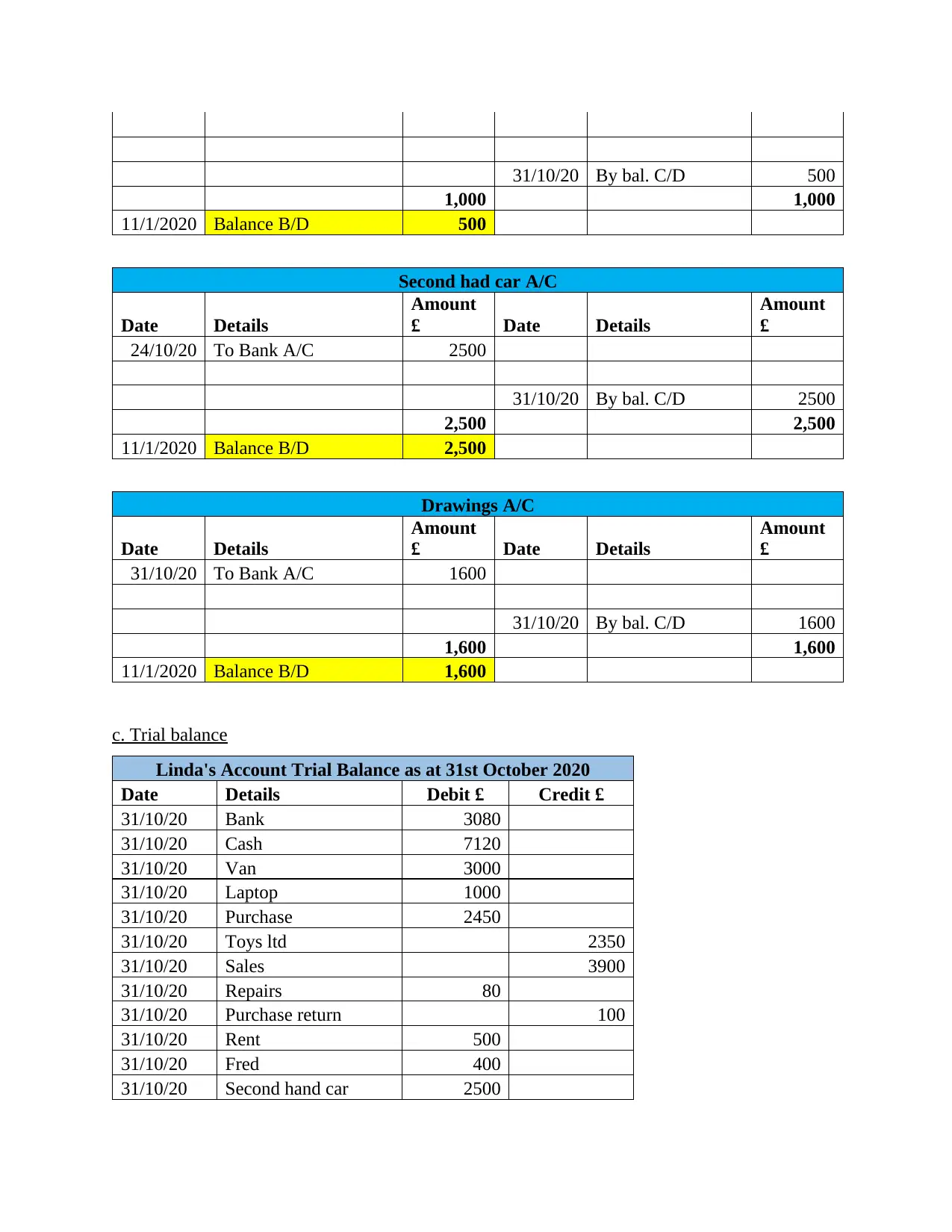

31/10/20 By bal. C/D 500

1,000 1,000

11/1/2020 Balance B/D 500

Second had car A/C

Date Details

Amount

£ Date Details

Amount

£

24/10/20 To Bank A/C 2500

31/10/20 By bal. C/D 2500

2,500 2,500

11/1/2020 Balance B/D 2,500

Drawings A/C

Date Details

Amount

£ Date Details

Amount

£

31/10/20 To Bank A/C 1600

31/10/20 By bal. C/D 1600

1,600 1,600

11/1/2020 Balance B/D 1,600

c. Trial balance

Linda's Account Trial Balance as at 31st October 2020

Date Details Debit £ Credit £

31/10/20 Bank 3080

31/10/20 Cash 7120

31/10/20 Van 3000

31/10/20 Laptop 1000

31/10/20 Purchase 2450

31/10/20 Toys ltd 2350

31/10/20 Sales 3900

31/10/20 Repairs 80

31/10/20 Purchase return 100

31/10/20 Rent 500

31/10/20 Fred 400

31/10/20 Second hand car 2500

1,000 1,000

11/1/2020 Balance B/D 500

Second had car A/C

Date Details

Amount

£ Date Details

Amount

£

24/10/20 To Bank A/C 2500

31/10/20 By bal. C/D 2500

2,500 2,500

11/1/2020 Balance B/D 2,500

Drawings A/C

Date Details

Amount

£ Date Details

Amount

£

31/10/20 To Bank A/C 1600

31/10/20 By bal. C/D 1600

1,600 1,600

11/1/2020 Balance B/D 1,600

c. Trial balance

Linda's Account Trial Balance as at 31st October 2020

Date Details Debit £ Credit £

31/10/20 Bank 3080

31/10/20 Cash 7120

31/10/20 Van 3000

31/10/20 Laptop 1000

31/10/20 Purchase 2450

31/10/20 Toys ltd 2350

31/10/20 Sales 3900

31/10/20 Repairs 80

31/10/20 Purchase return 100

31/10/20 Rent 500

31/10/20 Fred 400

31/10/20 Second hand car 2500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

31/10/20 Wages 820

31/10/20 Drawings 1600

31/10/20 Capital 16200

Grand

Total 22,550 22,550

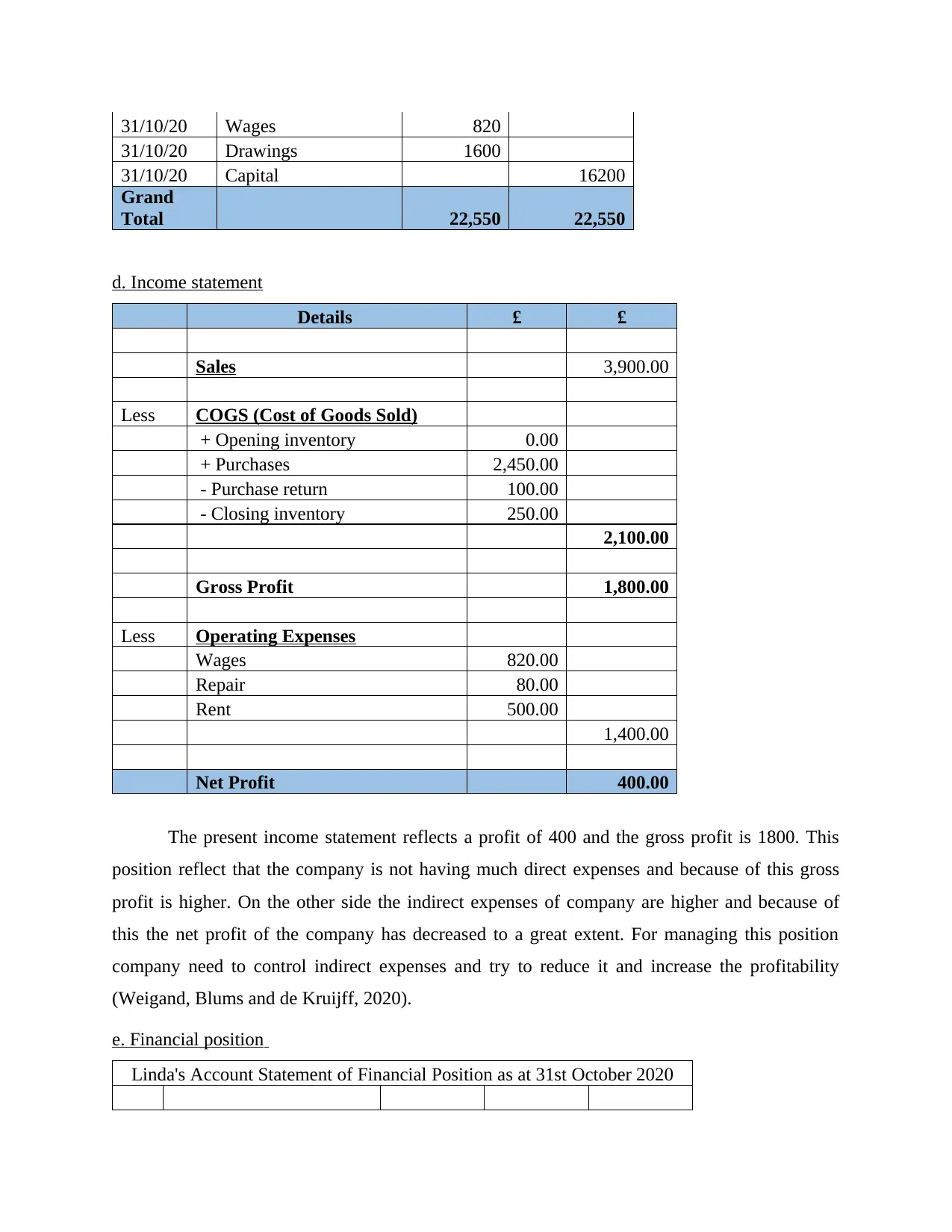

d. Income statement

Details £ £

Sales 3,900.00

Less COGS (Cost of Goods Sold)

+ Opening inventory 0.00

+ Purchases 2,450.00

- Purchase return 100.00

- Closing inventory 250.00

2,100.00

Gross Profit 1,800.00

Less Operating Expenses

Wages 820.00

Repair 80.00

Rent 500.00

1,400.00

Net Profit 400.00

The present income statement reflects a profit of 400 and the gross profit is 1800. This

position reflect that the company is not having much direct expenses and because of this gross

profit is higher. On the other side the indirect expenses of company are higher and because of

this the net profit of the company has decreased to a great extent. For managing this position

company need to control indirect expenses and try to reduce it and increase the profitability

(Weigand, Blums and de Kruijff, 2020).

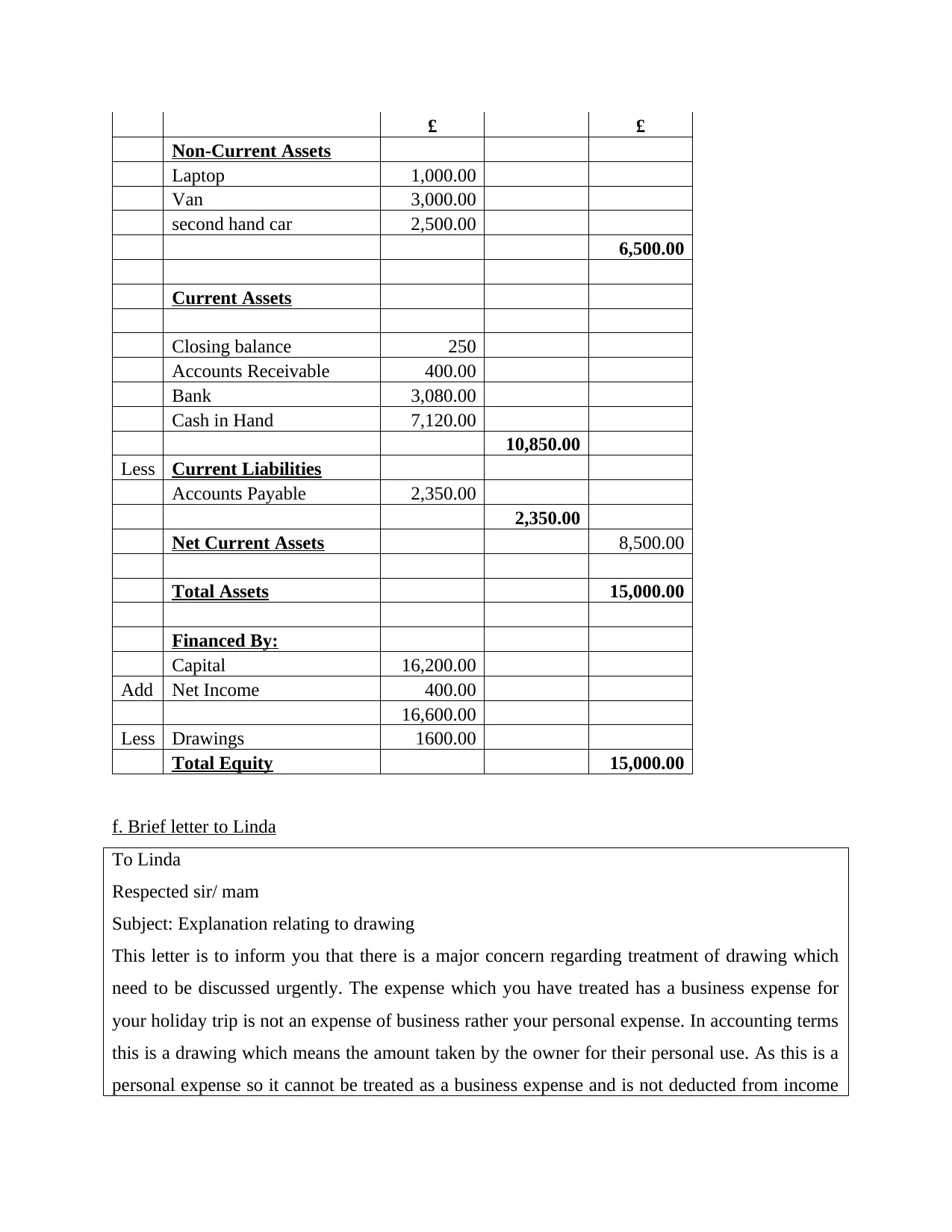

e. Financial position

Linda's Account Statement of Financial Position as at 31st October 2020

31/10/20 Drawings 1600

31/10/20 Capital 16200

Grand

Total 22,550 22,550

d. Income statement

Details £ £

Sales 3,900.00

Less COGS (Cost of Goods Sold)

+ Opening inventory 0.00

+ Purchases 2,450.00

- Purchase return 100.00

- Closing inventory 250.00

2,100.00

Gross Profit 1,800.00

Less Operating Expenses

Wages 820.00

Repair 80.00

Rent 500.00

1,400.00

Net Profit 400.00

The present income statement reflects a profit of 400 and the gross profit is 1800. This

position reflect that the company is not having much direct expenses and because of this gross

profit is higher. On the other side the indirect expenses of company are higher and because of

this the net profit of the company has decreased to a great extent. For managing this position

company need to control indirect expenses and try to reduce it and increase the profitability

(Weigand, Blums and de Kruijff, 2020).

e. Financial position

Linda's Account Statement of Financial Position as at 31st October 2020

£ £

Non-Current Assets

Laptop 1,000.00

Van 3,000.00

second hand car 2,500.00

6,500.00

Current Assets

Closing balance 250

Accounts Receivable 400.00

Bank 3,080.00

Cash in Hand 7,120.00

10,850.00

Less Current Liabilities

Accounts Payable 2,350.00

2,350.00

Net Current Assets 8,500.00

Total Assets 15,000.00

Financed By:

Capital 16,200.00

Add Net Income 400.00

16,600.00

Less Drawings 1600.00

Total Equity 15,000.00

f. Brief letter to Linda

To Linda

Respected sir/ mam

Subject: Explanation relating to drawing

This letter is to inform you that there is a major concern regarding treatment of drawing which

need to be discussed urgently. The expense which you have treated has a business expense for

your holiday trip is not an expense of business rather your personal expense. In accounting terms

this is a drawing which means the amount taken by the owner for their personal use. As this is a

personal expense so it cannot be treated as a business expense and is not deducted from income

Non-Current Assets

Laptop 1,000.00

Van 3,000.00

second hand car 2,500.00

6,500.00

Current Assets

Closing balance 250

Accounts Receivable 400.00

Bank 3,080.00

Cash in Hand 7,120.00

10,850.00

Less Current Liabilities

Accounts Payable 2,350.00

2,350.00

Net Current Assets 8,500.00

Total Assets 15,000.00

Financed By:

Capital 16,200.00

Add Net Income 400.00

16,600.00

Less Drawings 1600.00

Total Equity 15,000.00

f. Brief letter to Linda

To Linda

Respected sir/ mam

Subject: Explanation relating to drawing

This letter is to inform you that there is a major concern regarding treatment of drawing which

need to be discussed urgently. The expense which you have treated has a business expense for

your holiday trip is not an expense of business rather your personal expense. In accounting terms

this is a drawing which means the amount taken by the owner for their personal use. As this is a

personal expense so it cannot be treated as a business expense and is not deducted from income

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

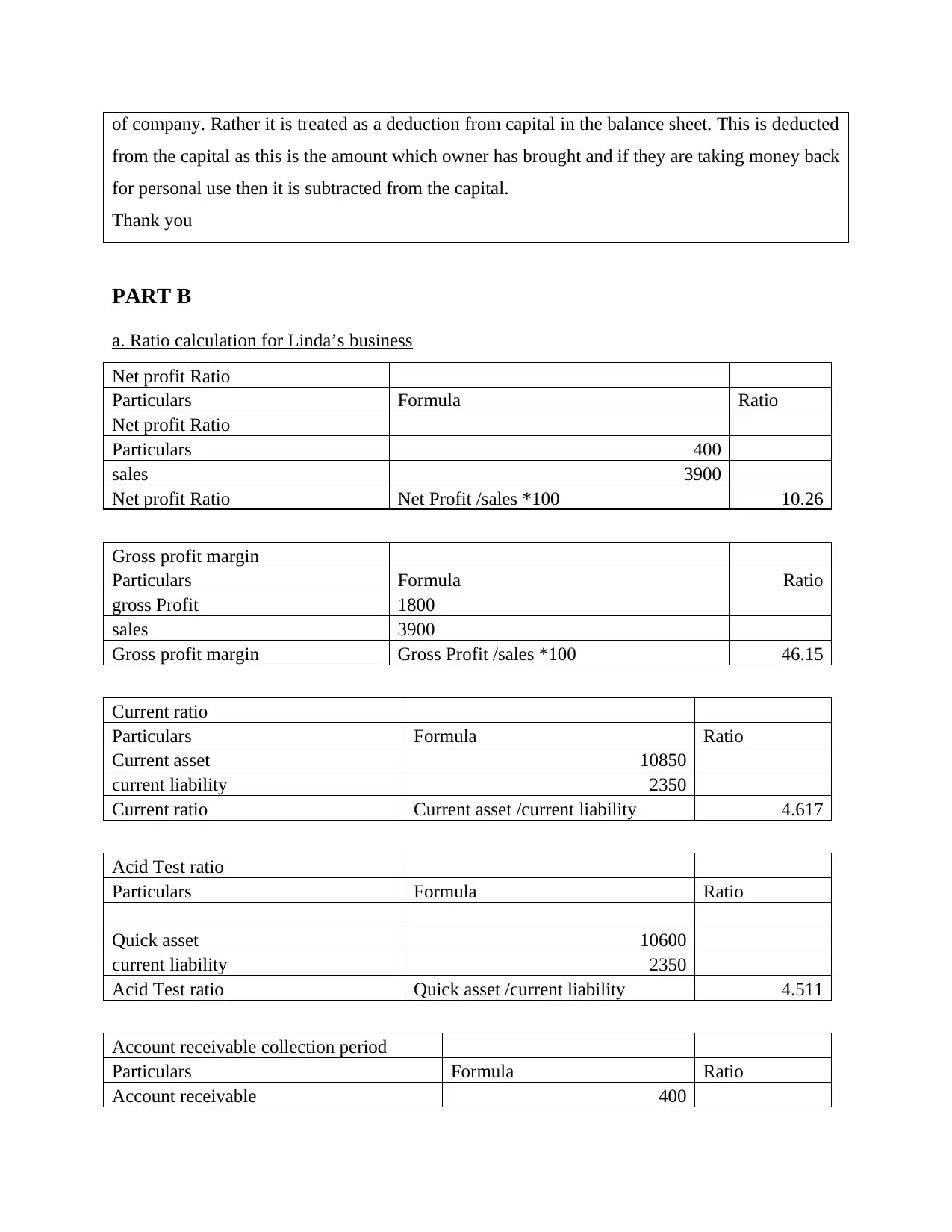

of company. Rather it is treated as a deduction from capital in the balance sheet. This is deducted

from the capital as this is the amount which owner has brought and if they are taking money back

for personal use then it is subtracted from the capital.

Thank you

PART B

a. Ratio calculation for Linda’s business

Net profit Ratio

Particulars Formula Ratio

Net profit Ratio

Particulars 400

sales 3900

Net profit Ratio Net Profit /sales *100 10.26

Gross profit margin

Particulars Formula Ratio

gross Profit 1800

sales 3900

Gross profit margin Gross Profit /sales *100 46.15

Current ratio

Particulars Formula Ratio

Current asset 10850

current liability 2350

Current ratio Current asset /current liability 4.617

Acid Test ratio

Particulars Formula Ratio

Quick asset 10600

current liability 2350

Acid Test ratio Quick asset /current liability 4.511

Account receivable collection period

Particulars Formula Ratio

Account receivable 400

from the capital as this is the amount which owner has brought and if they are taking money back

for personal use then it is subtracted from the capital.

Thank you

PART B

a. Ratio calculation for Linda’s business

Net profit Ratio

Particulars Formula Ratio

Net profit Ratio

Particulars 400

sales 3900

Net profit Ratio Net Profit /sales *100 10.26

Gross profit margin

Particulars Formula Ratio

gross Profit 1800

sales 3900

Gross profit margin Gross Profit /sales *100 46.15

Current ratio

Particulars Formula Ratio

Current asset 10850

current liability 2350

Current ratio Current asset /current liability 4.617

Acid Test ratio

Particulars Formula Ratio

Quick asset 10600

current liability 2350

Acid Test ratio Quick asset /current liability 4.511

Account receivable collection period

Particulars Formula Ratio

Account receivable 400

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

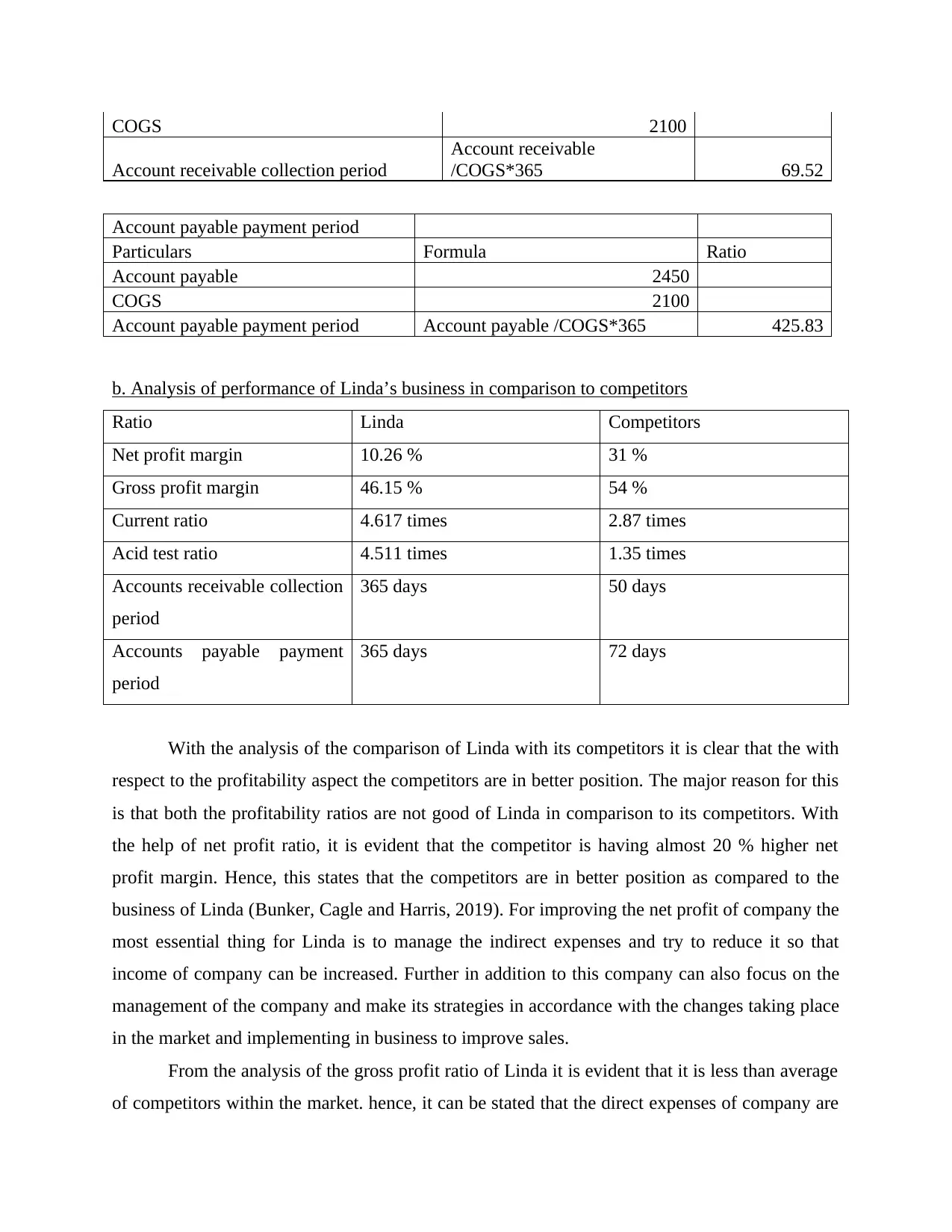

COGS 2100

Account receivable collection period

Account receivable

/COGS*365 69.52

Account payable payment period

Particulars Formula Ratio

Account payable 2450

COGS 2100

Account payable payment period Account payable /COGS*365 425.83

b. Analysis of performance of Linda’s business in comparison to competitors

Ratio Linda Competitors

Net profit margin 10.26 % 31 %

Gross profit margin 46.15 % 54 %

Current ratio 4.617 times 2.87 times

Acid test ratio 4.511 times 1.35 times

Accounts receivable collection

period

365 days 50 days

Accounts payable payment

period

365 days 72 days

With the analysis of the comparison of Linda with its competitors it is clear that the with

respect to the profitability aspect the competitors are in better position. The major reason for this

is that both the profitability ratios are not good of Linda in comparison to its competitors. With

the help of net profit ratio, it is evident that the competitor is having almost 20 % higher net

profit margin. Hence, this states that the competitors are in better position as compared to the

business of Linda (Bunker, Cagle and Harris, 2019). For improving the net profit of company the

most essential thing for Linda is to manage the indirect expenses and try to reduce it so that

income of company can be increased. Further in addition to this company can also focus on the

management of the company and make its strategies in accordance with the changes taking place

in the market and implementing in business to improve sales.

From the analysis of the gross profit ratio of Linda it is evident that it is less than average

of competitors within the market. hence, it can be stated that the direct expenses of company are

Account receivable collection period

Account receivable

/COGS*365 69.52

Account payable payment period

Particulars Formula Ratio

Account payable 2450

COGS 2100

Account payable payment period Account payable /COGS*365 425.83

b. Analysis of performance of Linda’s business in comparison to competitors

Ratio Linda Competitors

Net profit margin 10.26 % 31 %

Gross profit margin 46.15 % 54 %

Current ratio 4.617 times 2.87 times

Acid test ratio 4.511 times 1.35 times

Accounts receivable collection

period

365 days 50 days

Accounts payable payment

period

365 days 72 days

With the analysis of the comparison of Linda with its competitors it is clear that the with

respect to the profitability aspect the competitors are in better position. The major reason for this

is that both the profitability ratios are not good of Linda in comparison to its competitors. With

the help of net profit ratio, it is evident that the competitor is having almost 20 % higher net

profit margin. Hence, this states that the competitors are in better position as compared to the

business of Linda (Bunker, Cagle and Harris, 2019). For improving the net profit of company the

most essential thing for Linda is to manage the indirect expenses and try to reduce it so that

income of company can be increased. Further in addition to this company can also focus on the

management of the company and make its strategies in accordance with the changes taking place

in the market and implementing in business to improve sales.

From the analysis of the gross profit ratio of Linda it is evident that it is less than average

of competitors within the market. hence, it can be stated that the direct expenses of company are

higher and because of this the profitability of company is low (Purba and Septian, 2019). For this

it is recommended to the company that they must focus on managing their direct expenses so that

they can increase their profitability. in addition to this it is essential for Linda to also try to

increase its sales by different ways like working on marketing strategy and improving sales of

company.

Further the performance was evaluated on basis of the liquidity ratios which is essential

to be monitored. Under this the current ratio and acid test ratio was high of Linda’s business in

comparison to the competitors which is not good. This is particularly because of the fact that if

the current and acid test ratio is too high then this reflects that the company is not in position to

effectively allocate and use current asset. For this it is suggested to company that they must take

out their investment from current asset and use that cash in some productive areas and improve

efficiency of company.

In addition to this with the help of the efficiency ratios it was evident that the

performance of competitor is much better. For Linda both account payable and receivable is 365

days and this is not that good for the company. in addition to this high receivable and payable

ratio reduces the credibility of company (Amalina, Amelia and Alfatah, 2019). This is due to the

reason that creditors and debtors might think that company will take a lot of time to pay off their

liabilities.

CONCLUSION

The above report summarized that for assessing the profit earned or loss incurred the

most important thing is the proper recording of business transaction within the books of

accounts. under the books of account all the financial transaction is recorded and posted in ledger

and further with help of trial balance income statement and balance sheet is being prepared. from

the above report it was summarized that for the proper assessment of profitability every

transaction need to be recorded in proper manner. this is due to the reason that if the transaction

will not be recorded in correct manner then profit will not be calculated in right way. further with

help of the report it was also reflected that for comparing the performance with the competitor it

is essential for company to effectively calculate all the ratios. this is particularly because under

this two or more companies are compared on a single common basis such as profitability or

liquidity.

it is recommended to the company that they must focus on managing their direct expenses so that

they can increase their profitability. in addition to this it is essential for Linda to also try to

increase its sales by different ways like working on marketing strategy and improving sales of

company.

Further the performance was evaluated on basis of the liquidity ratios which is essential

to be monitored. Under this the current ratio and acid test ratio was high of Linda’s business in

comparison to the competitors which is not good. This is particularly because of the fact that if

the current and acid test ratio is too high then this reflects that the company is not in position to

effectively allocate and use current asset. For this it is suggested to company that they must take

out their investment from current asset and use that cash in some productive areas and improve

efficiency of company.

In addition to this with the help of the efficiency ratios it was evident that the

performance of competitor is much better. For Linda both account payable and receivable is 365

days and this is not that good for the company. in addition to this high receivable and payable

ratio reduces the credibility of company (Amalina, Amelia and Alfatah, 2019). This is due to the

reason that creditors and debtors might think that company will take a lot of time to pay off their

liabilities.

CONCLUSION

The above report summarized that for assessing the profit earned or loss incurred the

most important thing is the proper recording of business transaction within the books of

accounts. under the books of account all the financial transaction is recorded and posted in ledger

and further with help of trial balance income statement and balance sheet is being prepared. from

the above report it was summarized that for the proper assessment of profitability every

transaction need to be recorded in proper manner. this is due to the reason that if the transaction

will not be recorded in correct manner then profit will not be calculated in right way. further with

help of the report it was also reflected that for comparing the performance with the competitor it

is essential for company to effectively calculate all the ratios. this is particularly because under

this two or more companies are compared on a single common basis such as profitability or

liquidity.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.