University of West London: K. Green's Financial Statement Analysis

VerifiedAdded on 2023/01/12

|8

|1143

|99

Homework Assignment

AI Summary

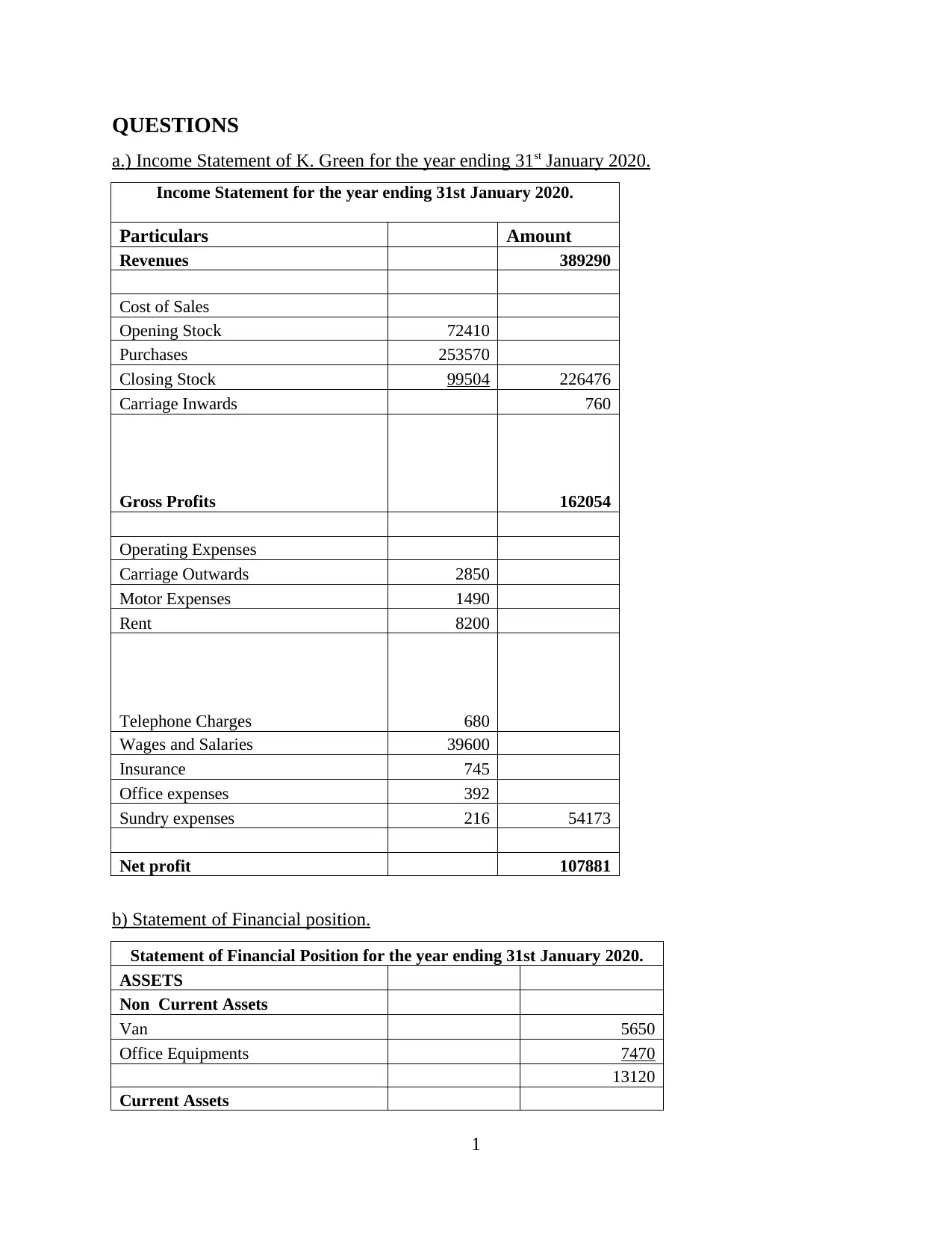

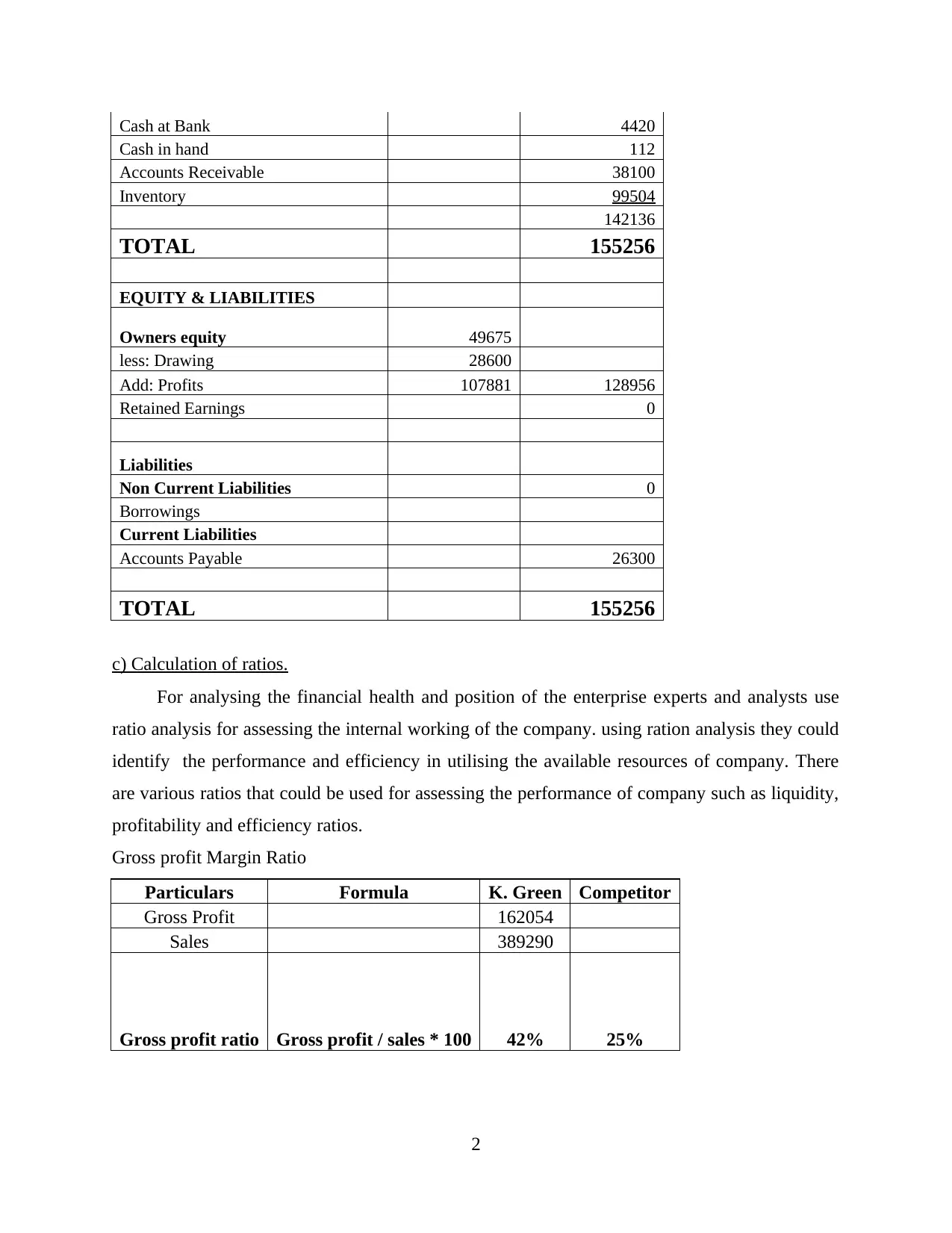

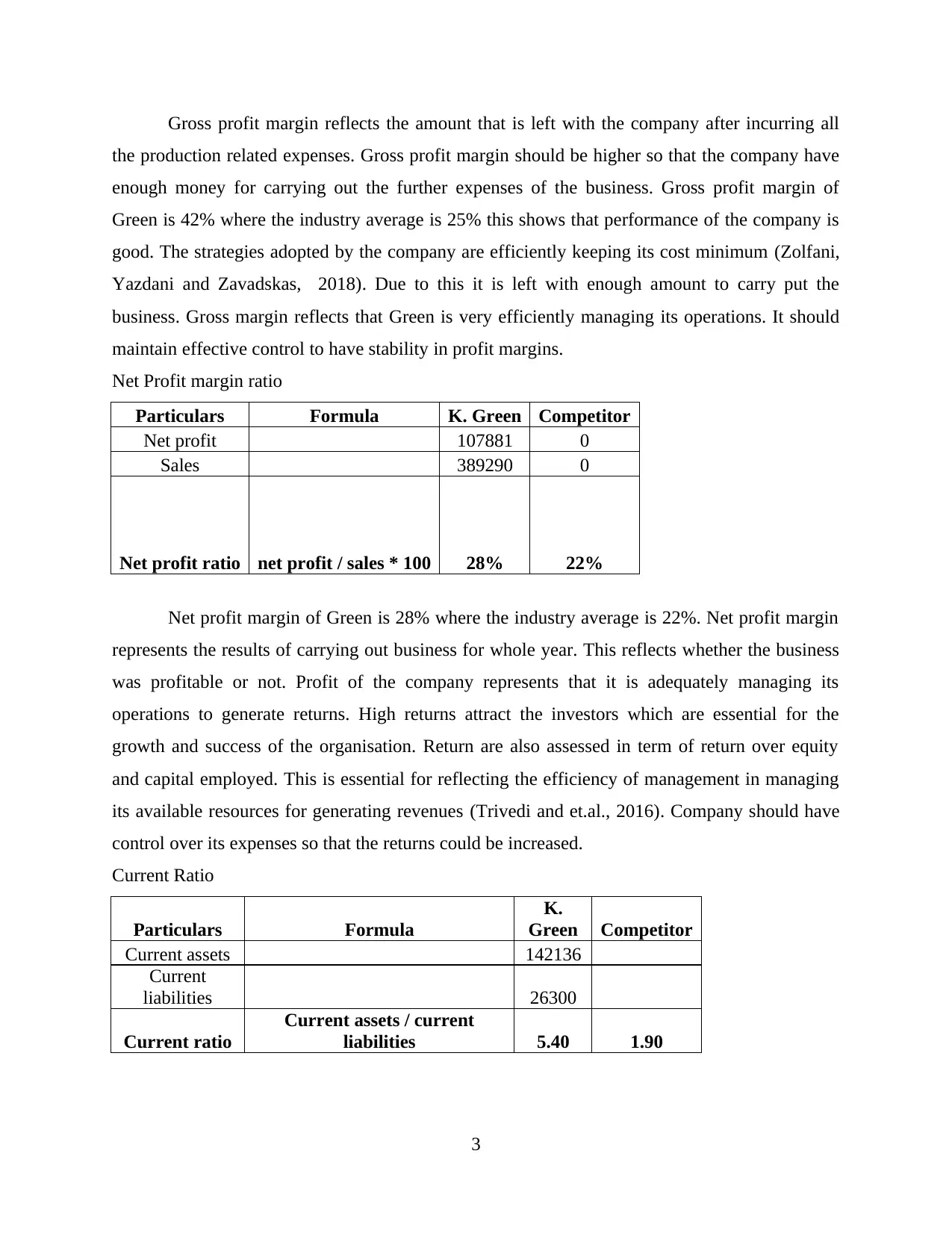

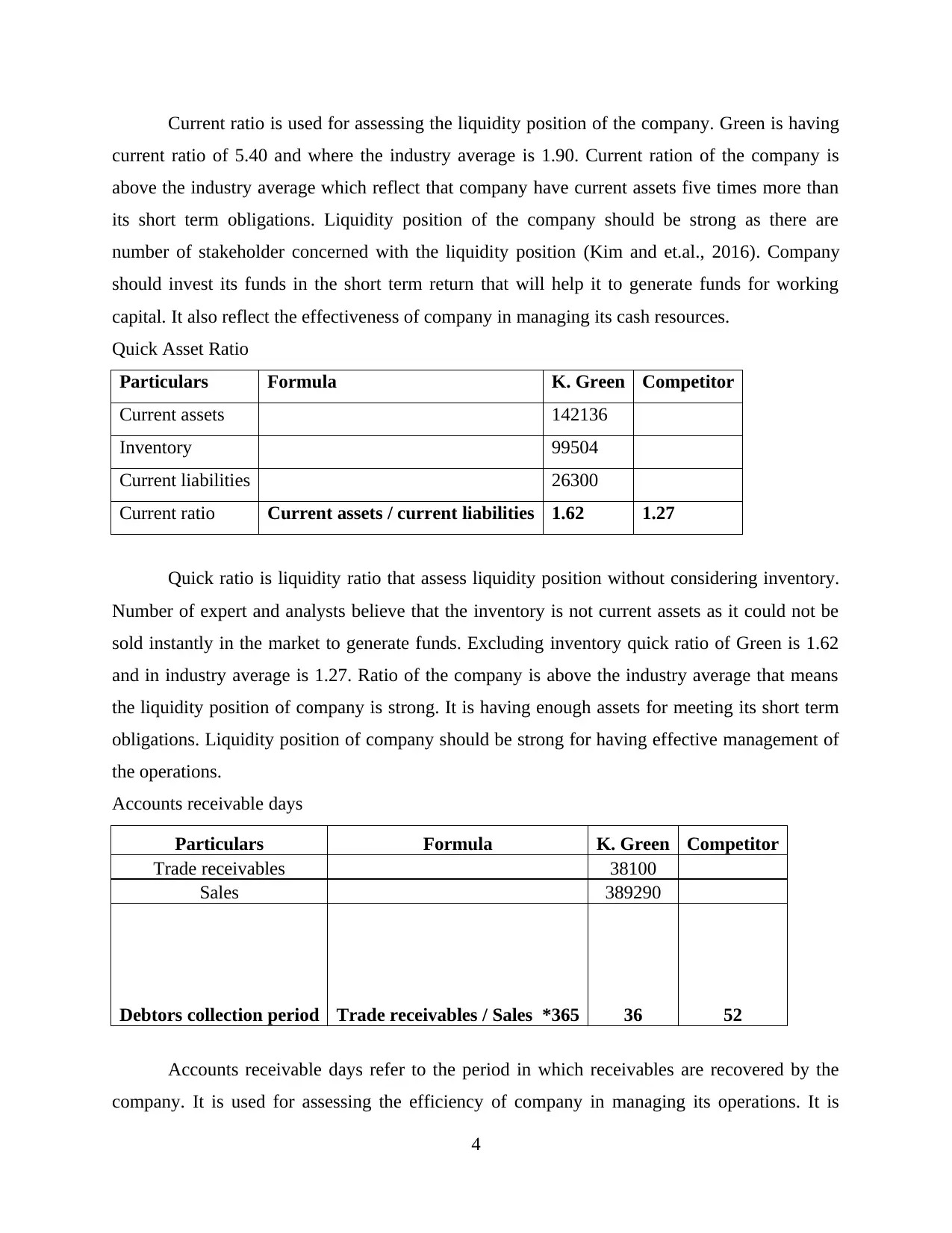

This assignment provides a detailed analysis of K. Green's financial performance based on the provided trial balance. It includes the preparation of an income statement, a statement of financial position (balance sheet), and the calculation of key financial ratios. The income statement presents revenues, cost of sales, operating expenses, and the resulting net profit. The statement of financial position outlines assets, liabilities, and equity, providing a snapshot of the company's financial position at a specific point in time. Furthermore, the assignment calculates and interprets various ratios, such as gross profit margin, net profit margin, current ratio, quick ratio, accounts receivable days, and accounts payable days, comparing them to industry averages to assess the company's liquidity, profitability, and efficiency. The analysis highlights the strengths and weaknesses of K. Green's financial management and provides insights into its operational performance.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.