Recording Business Transactions

VerifiedAdded on 2022/12/29

|16

|2925

|53

AI Summary

This document provides an overview of recording business transactions, including double entry transactions, balancing accounts, trial balance, income statement, and statement of financial position. It also explains the concept of drawings in small businesses and provides clarification on a specific query. The document includes examples and calculations for better understanding. Study material and expert guidance on recording business transactions are available on Desklib.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Recording Business

Transactions

Transactions

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION ..........................................................................................................................3

PART A...........................................................................................................................................3

(a) Double entry transactions in T-Accounts..............................................................................3

b) Balance the Accounts..............................................................................................................5

c) Extract of Trial Balance as on 31st October 2020..................................................................9

d) Prepare an Income Statement for the period ended 31st October 2020..................................9

e) Prepare a Statement of Financial Position as at 31st October 2020......................................10

f) What are drawings concerned for small business and clarification of the query..................11

PART B..........................................................................................................................................11

a) Ratios Calculation.................................................................................................................11

b) Ratio Analysis of Linda's firm in comparison with the Industry Ratios trends....................12

CONCLUSION .............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION ..........................................................................................................................3

PART A...........................................................................................................................................3

(a) Double entry transactions in T-Accounts..............................................................................3

b) Balance the Accounts..............................................................................................................5

c) Extract of Trial Balance as on 31st October 2020..................................................................9

d) Prepare an Income Statement for the period ended 31st October 2020..................................9

e) Prepare a Statement of Financial Position as at 31st October 2020......................................10

f) What are drawings concerned for small business and clarification of the query..................11

PART B..........................................................................................................................................11

a) Ratios Calculation.................................................................................................................11

b) Ratio Analysis of Linda's firm in comparison with the Industry Ratios trends....................12

CONCLUSION .............................................................................................................................13

REFERENCES..............................................................................................................................14

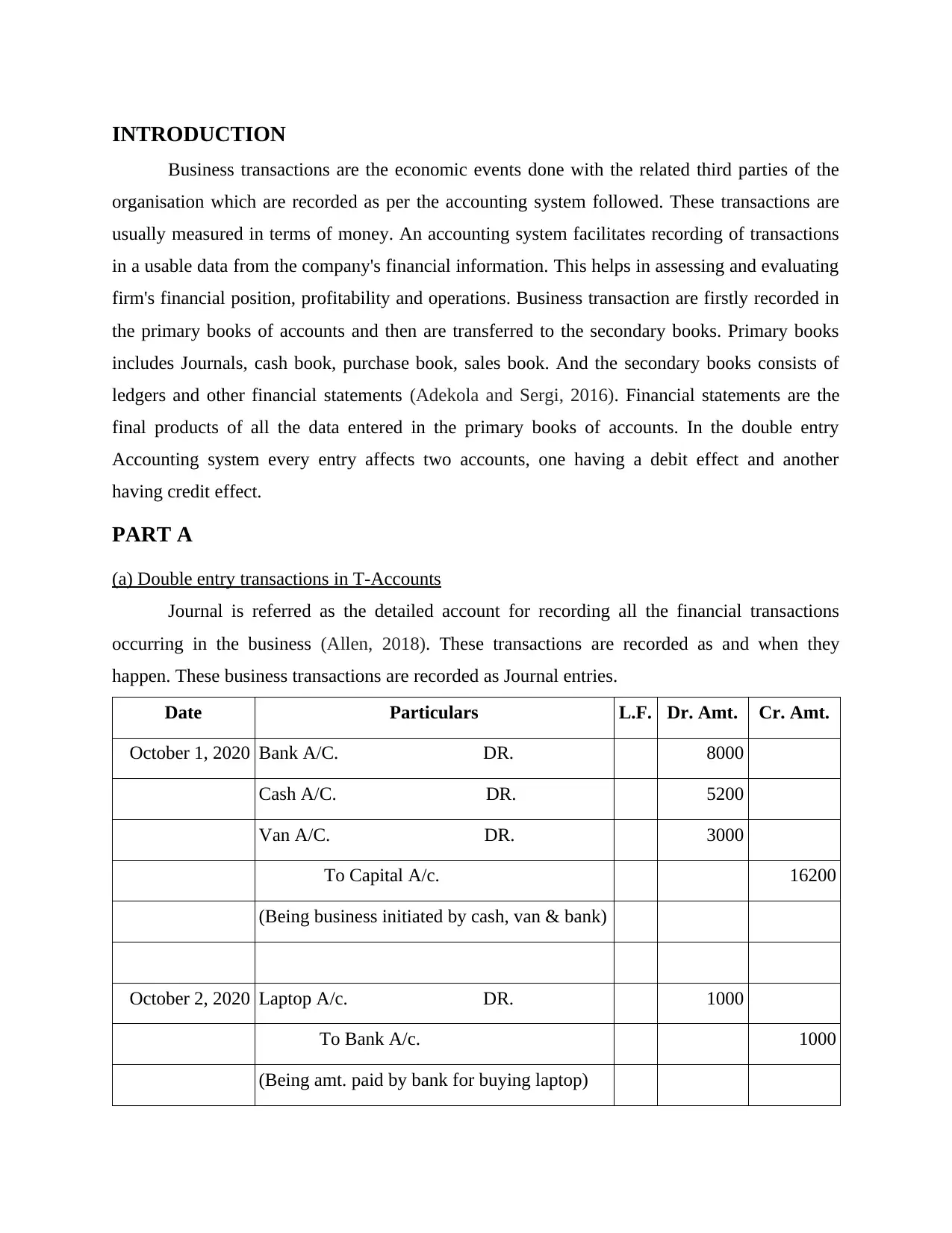

INTRODUCTION

Business transactions are the economic events done with the related third parties of the

organisation which are recorded as per the accounting system followed. These transactions are

usually measured in terms of money. An accounting system facilitates recording of transactions

in a usable data from the company's financial information. This helps in assessing and evaluating

firm's financial position, profitability and operations. Business transaction are firstly recorded in

the primary books of accounts and then are transferred to the secondary books. Primary books

includes Journals, cash book, purchase book, sales book. And the secondary books consists of

ledgers and other financial statements (Adekola and Sergi, 2016). Financial statements are the

final products of all the data entered in the primary books of accounts. In the double entry

Accounting system every entry affects two accounts, one having a debit effect and another

having credit effect.

PART A

(a) Double entry transactions in T-Accounts

Journal is referred as the detailed account for recording all the financial transactions

occurring in the business (Allen, 2018). These transactions are recorded as and when they

happen. These business transactions are recorded as Journal entries.

Date Particulars L.F. Dr. Amt. Cr. Amt.

October 1, 2020 Bank A/C. DR. 8000

Cash A/C. DR. 5200

Van A/C. DR. 3000

To Capital A/c. 16200

(Being business initiated by cash, van & bank)

October 2, 2020 Laptop A/c. DR. 1000

To Bank A/c. 1000

(Being amt. paid by bank for buying laptop)

Business transactions are the economic events done with the related third parties of the

organisation which are recorded as per the accounting system followed. These transactions are

usually measured in terms of money. An accounting system facilitates recording of transactions

in a usable data from the company's financial information. This helps in assessing and evaluating

firm's financial position, profitability and operations. Business transaction are firstly recorded in

the primary books of accounts and then are transferred to the secondary books. Primary books

includes Journals, cash book, purchase book, sales book. And the secondary books consists of

ledgers and other financial statements (Adekola and Sergi, 2016). Financial statements are the

final products of all the data entered in the primary books of accounts. In the double entry

Accounting system every entry affects two accounts, one having a debit effect and another

having credit effect.

PART A

(a) Double entry transactions in T-Accounts

Journal is referred as the detailed account for recording all the financial transactions

occurring in the business (Allen, 2018). These transactions are recorded as and when they

happen. These business transactions are recorded as Journal entries.

Date Particulars L.F. Dr. Amt. Cr. Amt.

October 1, 2020 Bank A/C. DR. 8000

Cash A/C. DR. 5200

Van A/C. DR. 3000

To Capital A/c. 16200

(Being business initiated by cash, van & bank)

October 2, 2020 Laptop A/c. DR. 1000

To Bank A/c. 1000

(Being amt. paid by bank for buying laptop)

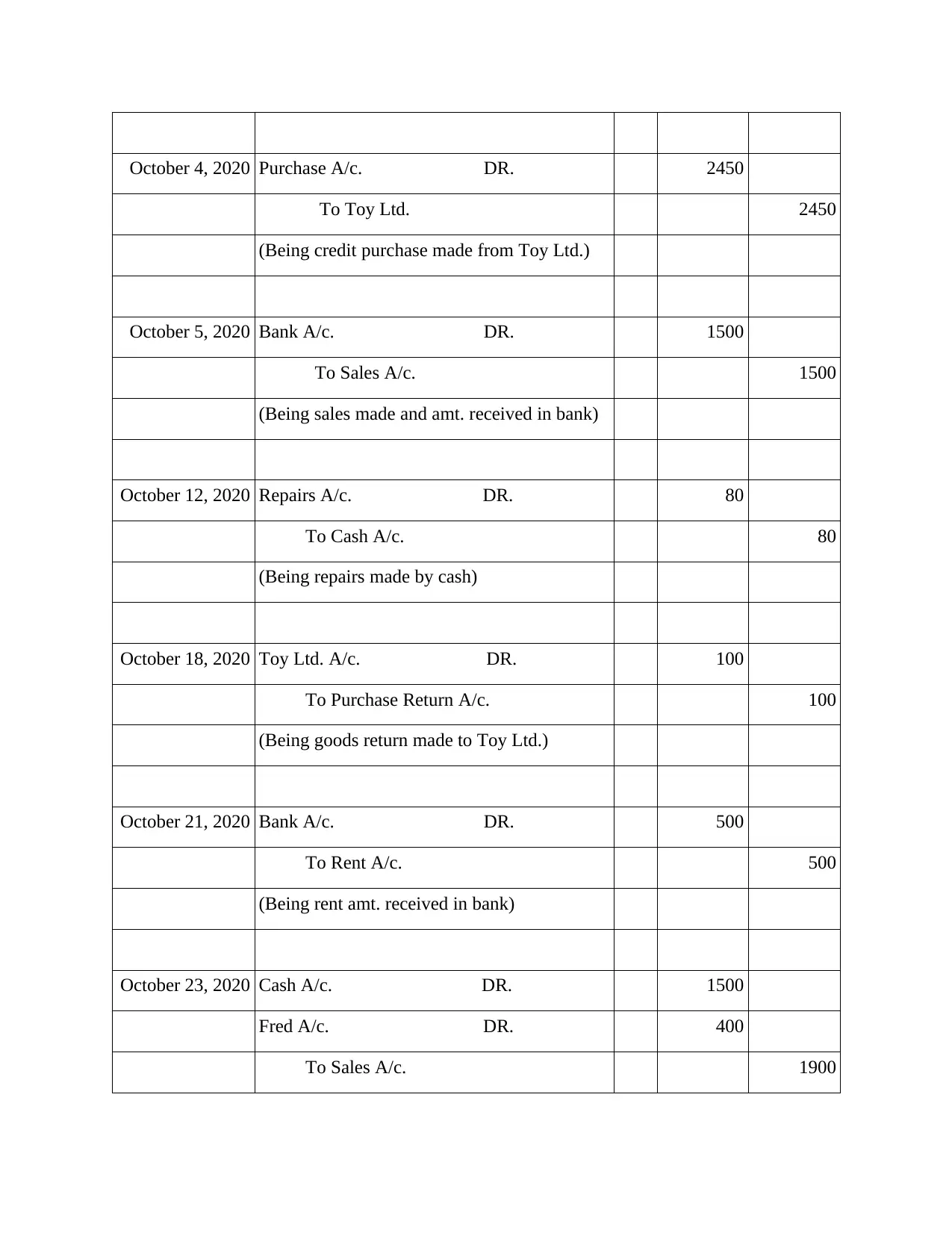

October 4, 2020 Purchase A/c. DR. 2450

To Toy Ltd. 2450

(Being credit purchase made from Toy Ltd.)

October 5, 2020 Bank A/c. DR. 1500

To Sales A/c. 1500

(Being sales made and amt. received in bank)

October 12, 2020 Repairs A/c. DR. 80

To Cash A/c. 80

(Being repairs made by cash)

October 18, 2020 Toy Ltd. A/c. DR. 100

To Purchase Return A/c. 100

(Being goods return made to Toy Ltd.)

October 21, 2020 Bank A/c. DR. 500

To Rent A/c. 500

(Being rent amt. received in bank)

October 23, 2020 Cash A/c. DR. 1500

Fred A/c. DR. 400

To Sales A/c. 1900

To Toy Ltd. 2450

(Being credit purchase made from Toy Ltd.)

October 5, 2020 Bank A/c. DR. 1500

To Sales A/c. 1500

(Being sales made and amt. received in bank)

October 12, 2020 Repairs A/c. DR. 80

To Cash A/c. 80

(Being repairs made by cash)

October 18, 2020 Toy Ltd. A/c. DR. 100

To Purchase Return A/c. 100

(Being goods return made to Toy Ltd.)

October 21, 2020 Bank A/c. DR. 500

To Rent A/c. 500

(Being rent amt. received in bank)

October 23, 2020 Cash A/c. DR. 1500

Fred A/c. DR. 400

To Sales A/c. 1900

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

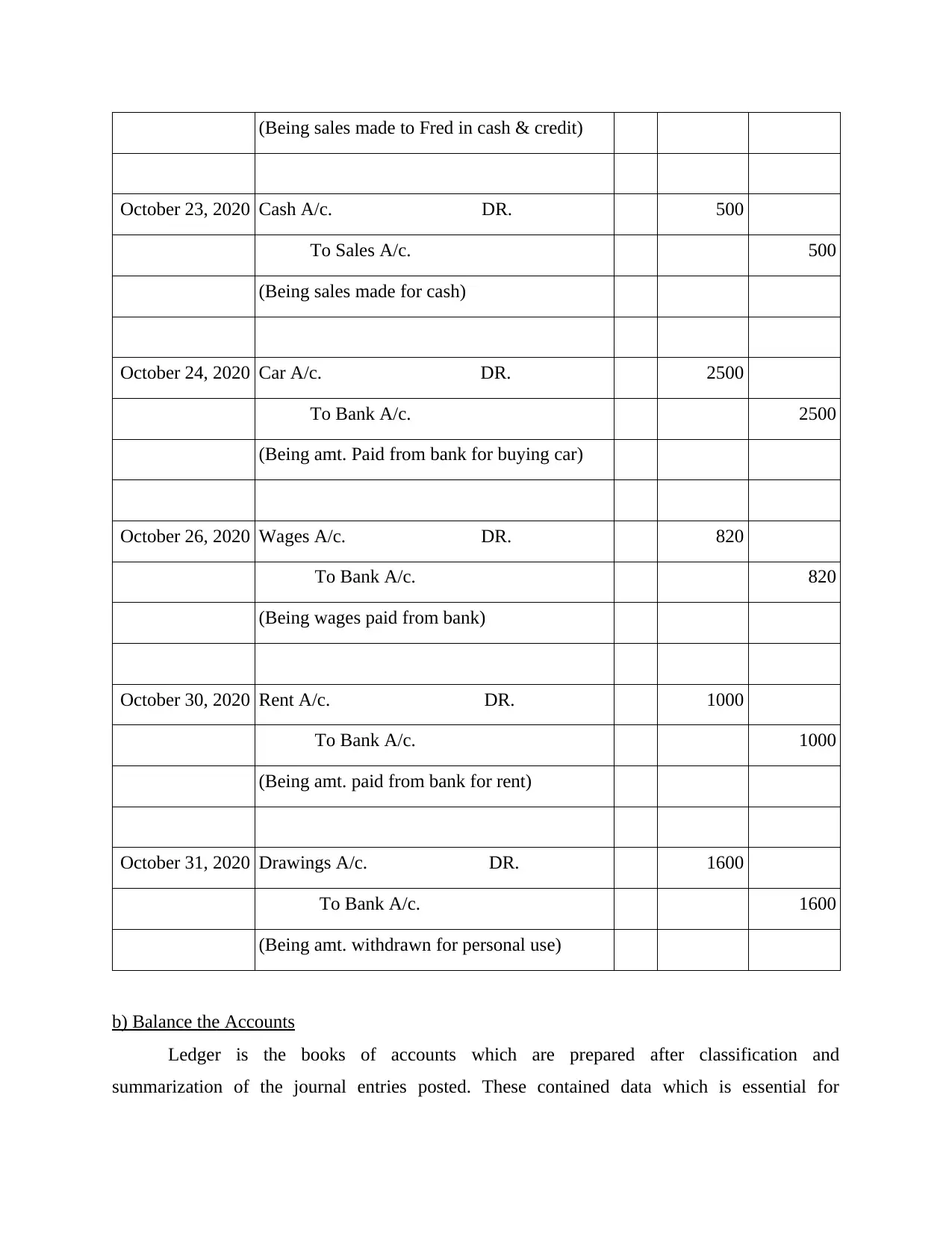

(Being sales made to Fred in cash & credit)

October 23, 2020 Cash A/c. DR. 500

To Sales A/c. 500

(Being sales made for cash)

October 24, 2020 Car A/c. DR. 2500

To Bank A/c. 2500

(Being amt. Paid from bank for buying car)

October 26, 2020 Wages A/c. DR. 820

To Bank A/c. 820

(Being wages paid from bank)

October 30, 2020 Rent A/c. DR. 1000

To Bank A/c. 1000

(Being amt. paid from bank for rent)

October 31, 2020 Drawings A/c. DR. 1600

To Bank A/c. 1600

(Being amt. withdrawn for personal use)

b) Balance the Accounts

Ledger is the books of accounts which are prepared after classification and

summarization of the journal entries posted. These contained data which is essential for

October 23, 2020 Cash A/c. DR. 500

To Sales A/c. 500

(Being sales made for cash)

October 24, 2020 Car A/c. DR. 2500

To Bank A/c. 2500

(Being amt. Paid from bank for buying car)

October 26, 2020 Wages A/c. DR. 820

To Bank A/c. 820

(Being wages paid from bank)

October 30, 2020 Rent A/c. DR. 1000

To Bank A/c. 1000

(Being amt. paid from bank for rent)

October 31, 2020 Drawings A/c. DR. 1600

To Bank A/c. 1600

(Being amt. withdrawn for personal use)

b) Balance the Accounts

Ledger is the books of accounts which are prepared after classification and

summarization of the journal entries posted. These contained data which is essential for

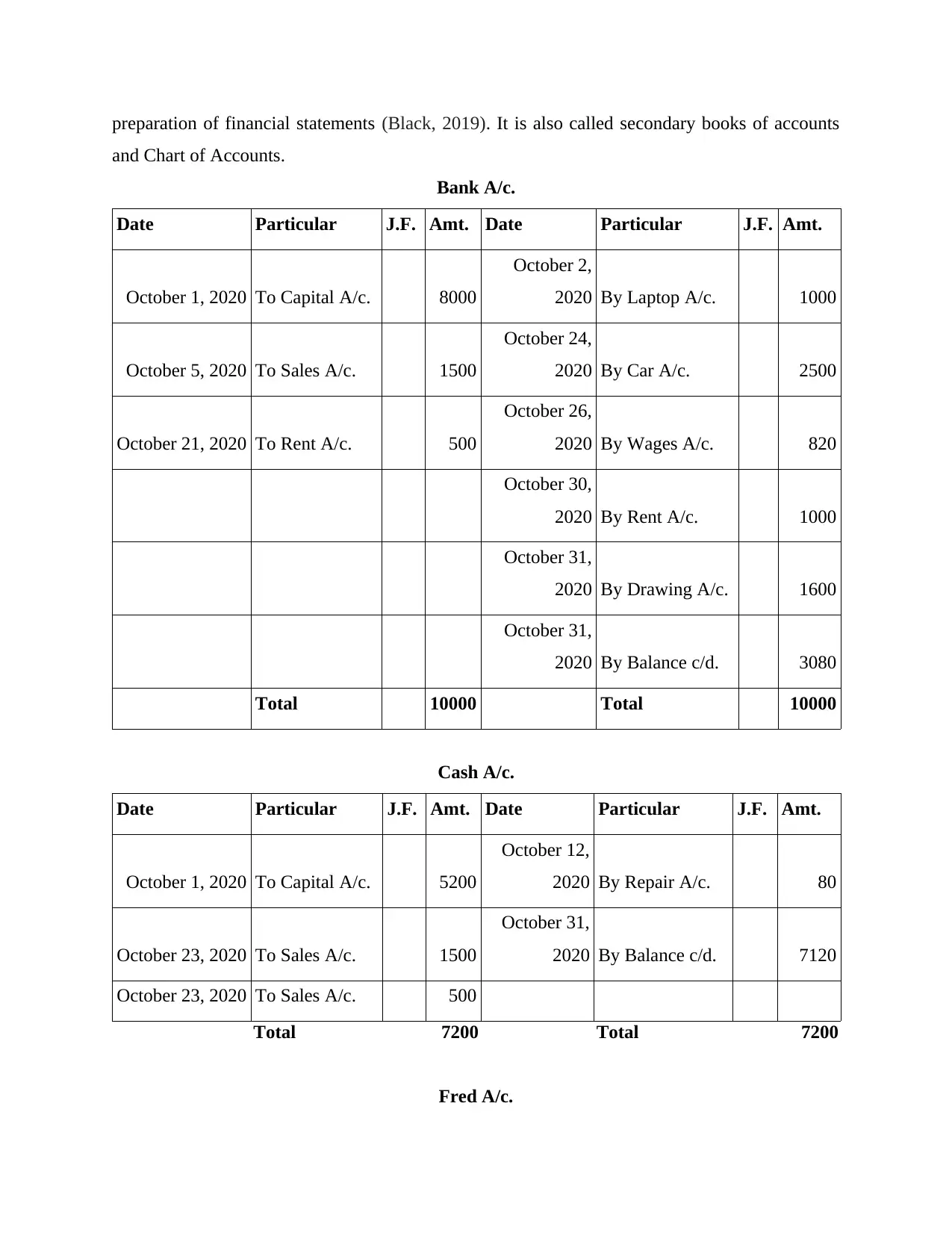

preparation of financial statements (Black, 2019). It is also called secondary books of accounts

and Chart of Accounts.

Bank A/c.

Date Particular J.F. Amt. Date Particular J.F. Amt.

October 1, 2020 To Capital A/c. 8000

October 2,

2020 By Laptop A/c. 1000

October 5, 2020 To Sales A/c. 1500

October 24,

2020 By Car A/c. 2500

October 21, 2020 To Rent A/c. 500

October 26,

2020 By Wages A/c. 820

October 30,

2020 By Rent A/c. 1000

October 31,

2020 By Drawing A/c. 1600

October 31,

2020 By Balance c/d. 3080

Total 10000 Total 10000

Cash A/c.

Date Particular J.F. Amt. Date Particular J.F. Amt.

October 1, 2020 To Capital A/c. 5200

October 12,

2020 By Repair A/c. 80

October 23, 2020 To Sales A/c. 1500

October 31,

2020 By Balance c/d. 7120

October 23, 2020 To Sales A/c. 500

Total 7200 Total 7200

Fred A/c.

and Chart of Accounts.

Bank A/c.

Date Particular J.F. Amt. Date Particular J.F. Amt.

October 1, 2020 To Capital A/c. 8000

October 2,

2020 By Laptop A/c. 1000

October 5, 2020 To Sales A/c. 1500

October 24,

2020 By Car A/c. 2500

October 21, 2020 To Rent A/c. 500

October 26,

2020 By Wages A/c. 820

October 30,

2020 By Rent A/c. 1000

October 31,

2020 By Drawing A/c. 1600

October 31,

2020 By Balance c/d. 3080

Total 10000 Total 10000

Cash A/c.

Date Particular J.F. Amt. Date Particular J.F. Amt.

October 1, 2020 To Capital A/c. 5200

October 12,

2020 By Repair A/c. 80

October 23, 2020 To Sales A/c. 1500

October 31,

2020 By Balance c/d. 7120

October 23, 2020 To Sales A/c. 500

Total 7200 Total 7200

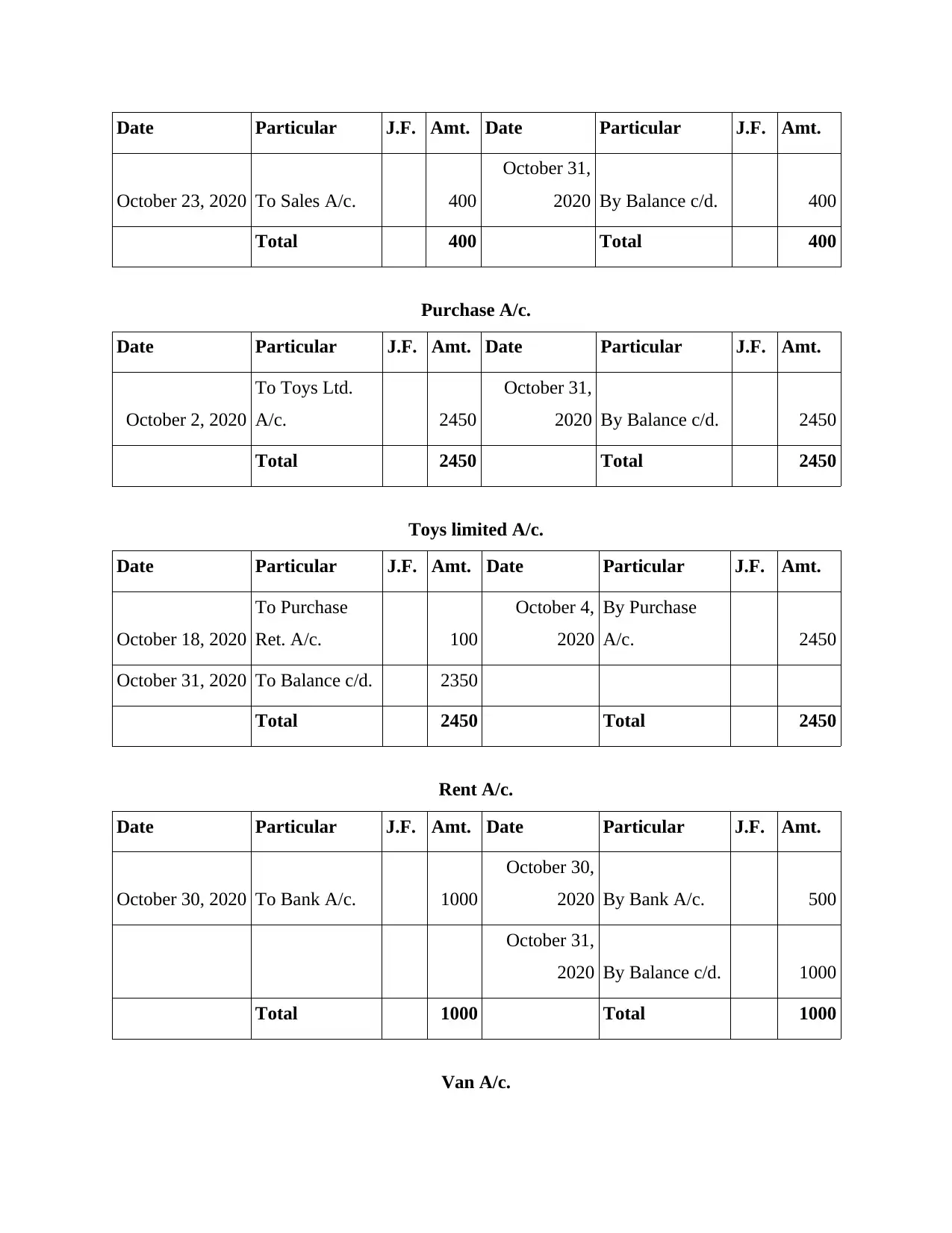

Fred A/c.

Date Particular J.F. Amt. Date Particular J.F. Amt.

October 23, 2020 To Sales A/c. 400

October 31,

2020 By Balance c/d. 400

Total 400 Total 400

Purchase A/c.

Date Particular J.F. Amt. Date Particular J.F. Amt.

October 2, 2020

To Toys Ltd.

A/c. 2450

October 31,

2020 By Balance c/d. 2450

Total 2450 Total 2450

Toys limited A/c.

Date Particular J.F. Amt. Date Particular J.F. Amt.

October 18, 2020

To Purchase

Ret. A/c. 100

October 4,

2020

By Purchase

A/c. 2450

October 31, 2020 To Balance c/d. 2350

Total 2450 Total 2450

Rent A/c.

Date Particular J.F. Amt. Date Particular J.F. Amt.

October 30, 2020 To Bank A/c. 1000

October 30,

2020 By Bank A/c. 500

October 31,

2020 By Balance c/d. 1000

Total 1000 Total 1000

Van A/c.

October 23, 2020 To Sales A/c. 400

October 31,

2020 By Balance c/d. 400

Total 400 Total 400

Purchase A/c.

Date Particular J.F. Amt. Date Particular J.F. Amt.

October 2, 2020

To Toys Ltd.

A/c. 2450

October 31,

2020 By Balance c/d. 2450

Total 2450 Total 2450

Toys limited A/c.

Date Particular J.F. Amt. Date Particular J.F. Amt.

October 18, 2020

To Purchase

Ret. A/c. 100

October 4,

2020

By Purchase

A/c. 2450

October 31, 2020 To Balance c/d. 2350

Total 2450 Total 2450

Rent A/c.

Date Particular J.F. Amt. Date Particular J.F. Amt.

October 30, 2020 To Bank A/c. 1000

October 30,

2020 By Bank A/c. 500

October 31,

2020 By Balance c/d. 1000

Total 1000 Total 1000

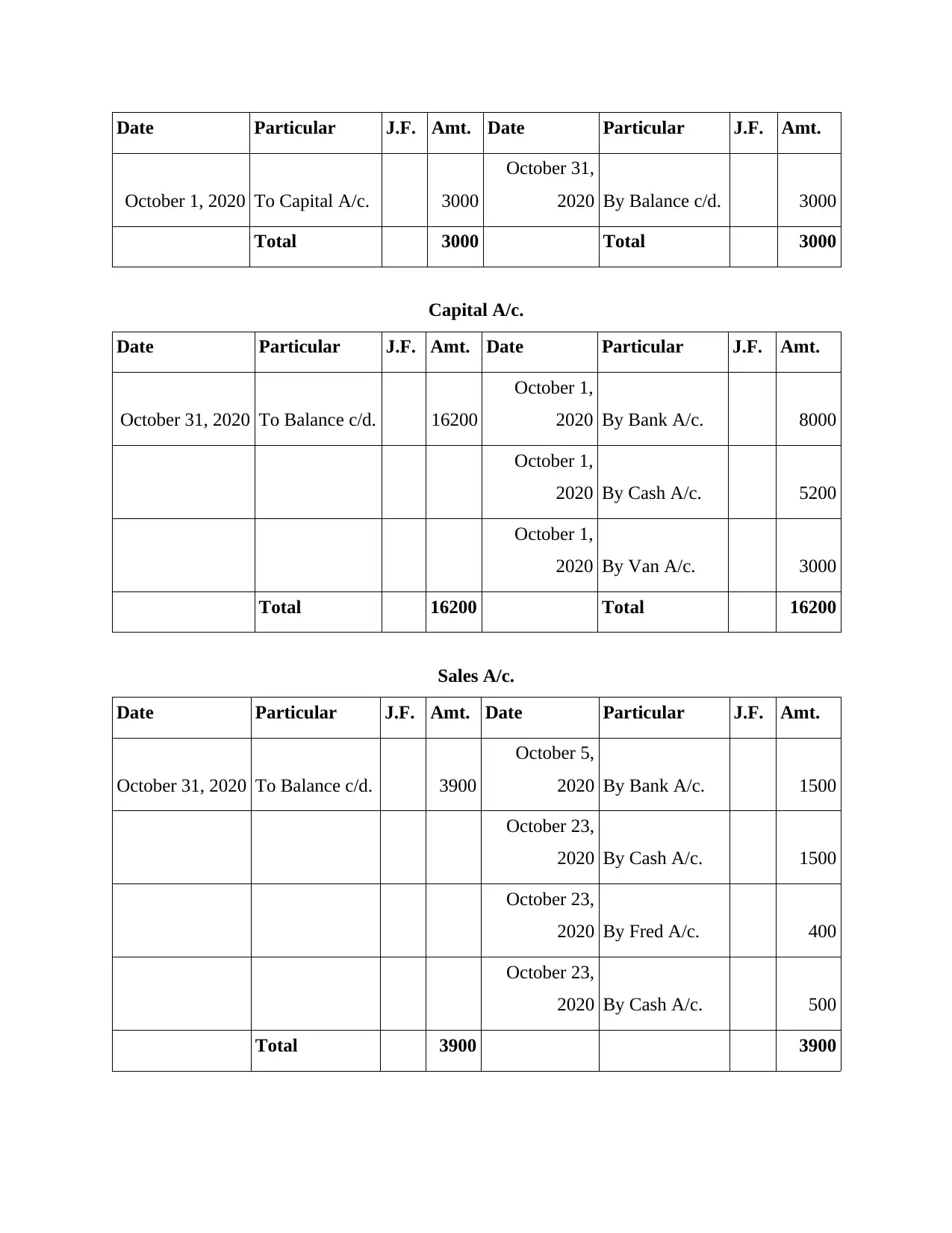

Van A/c.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Date Particular J.F. Amt. Date Particular J.F. Amt.

October 1, 2020 To Capital A/c. 3000

October 31,

2020 By Balance c/d. 3000

Total 3000 Total 3000

Capital A/c.

Date Particular J.F. Amt. Date Particular J.F. Amt.

October 31, 2020 To Balance c/d. 16200

October 1,

2020 By Bank A/c. 8000

October 1,

2020 By Cash A/c. 5200

October 1,

2020 By Van A/c. 3000

Total 16200 Total 16200

Sales A/c.

Date Particular J.F. Amt. Date Particular J.F. Amt.

October 31, 2020 To Balance c/d. 3900

October 5,

2020 By Bank A/c. 1500

October 23,

2020 By Cash A/c. 1500

October 23,

2020 By Fred A/c. 400

October 23,

2020 By Cash A/c. 500

Total 3900 3900

October 1, 2020 To Capital A/c. 3000

October 31,

2020 By Balance c/d. 3000

Total 3000 Total 3000

Capital A/c.

Date Particular J.F. Amt. Date Particular J.F. Amt.

October 31, 2020 To Balance c/d. 16200

October 1,

2020 By Bank A/c. 8000

October 1,

2020 By Cash A/c. 5200

October 1,

2020 By Van A/c. 3000

Total 16200 Total 16200

Sales A/c.

Date Particular J.F. Amt. Date Particular J.F. Amt.

October 31, 2020 To Balance c/d. 3900

October 5,

2020 By Bank A/c. 1500

October 23,

2020 By Cash A/c. 1500

October 23,

2020 By Fred A/c. 400

October 23,

2020 By Cash A/c. 500

Total 3900 3900

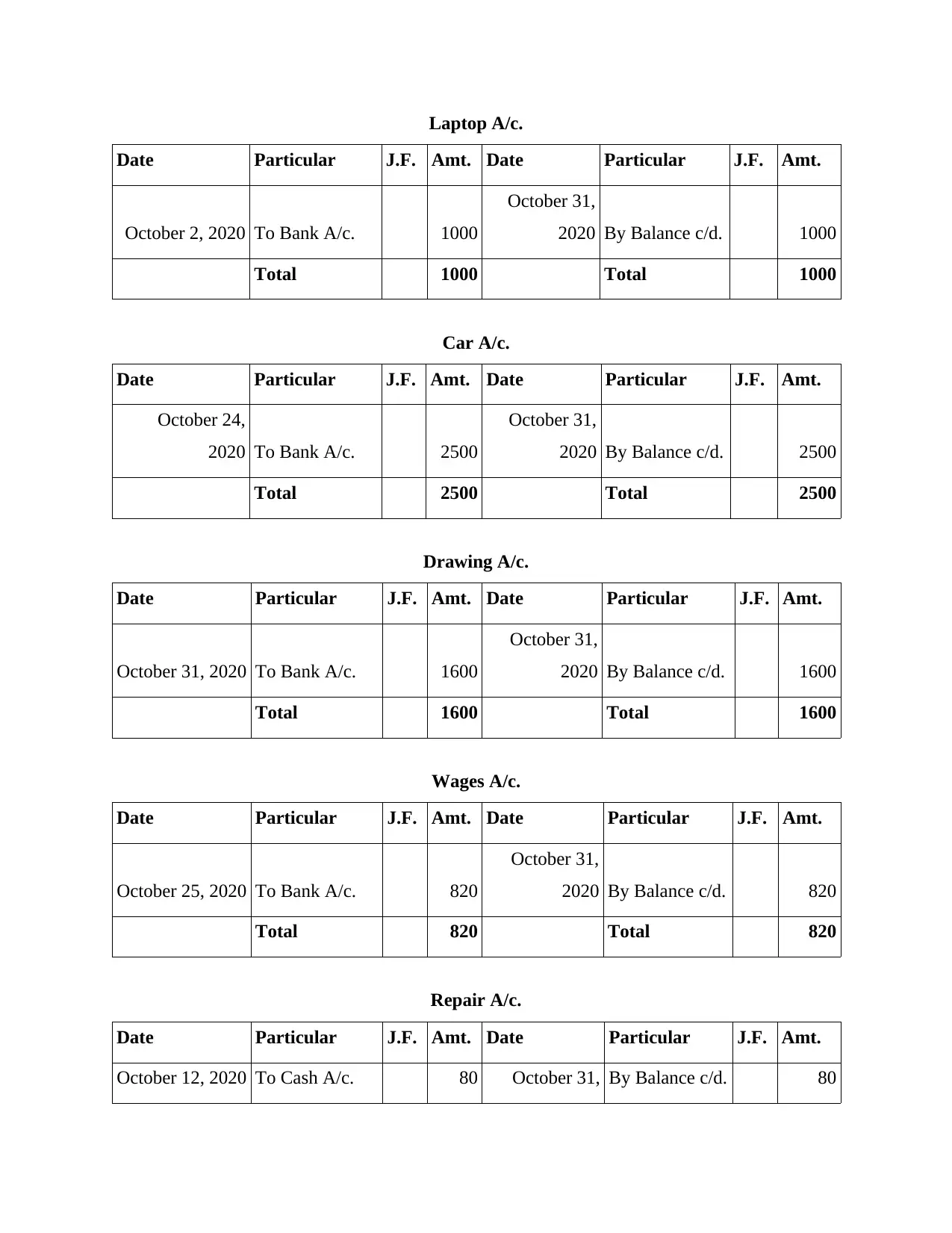

Laptop A/c.

Date Particular J.F. Amt. Date Particular J.F. Amt.

October 2, 2020 To Bank A/c. 1000

October 31,

2020 By Balance c/d. 1000

Total 1000 Total 1000

Car A/c.

Date Particular J.F. Amt. Date Particular J.F. Amt.

October 24,

2020 To Bank A/c. 2500

October 31,

2020 By Balance c/d. 2500

Total 2500 Total 2500

Drawing A/c.

Date Particular J.F. Amt. Date Particular J.F. Amt.

October 31, 2020 To Bank A/c. 1600

October 31,

2020 By Balance c/d. 1600

Total 1600 Total 1600

Wages A/c.

Date Particular J.F. Amt. Date Particular J.F. Amt.

October 25, 2020 To Bank A/c. 820

October 31,

2020 By Balance c/d. 820

Total 820 Total 820

Repair A/c.

Date Particular J.F. Amt. Date Particular J.F. Amt.

October 12, 2020 To Cash A/c. 80 October 31, By Balance c/d. 80

Date Particular J.F. Amt. Date Particular J.F. Amt.

October 2, 2020 To Bank A/c. 1000

October 31,

2020 By Balance c/d. 1000

Total 1000 Total 1000

Car A/c.

Date Particular J.F. Amt. Date Particular J.F. Amt.

October 24,

2020 To Bank A/c. 2500

October 31,

2020 By Balance c/d. 2500

Total 2500 Total 2500

Drawing A/c.

Date Particular J.F. Amt. Date Particular J.F. Amt.

October 31, 2020 To Bank A/c. 1600

October 31,

2020 By Balance c/d. 1600

Total 1600 Total 1600

Wages A/c.

Date Particular J.F. Amt. Date Particular J.F. Amt.

October 25, 2020 To Bank A/c. 820

October 31,

2020 By Balance c/d. 820

Total 820 Total 820

Repair A/c.

Date Particular J.F. Amt. Date Particular J.F. Amt.

October 12, 2020 To Cash A/c. 80 October 31, By Balance c/d. 80

2020

Total 80 Total 80

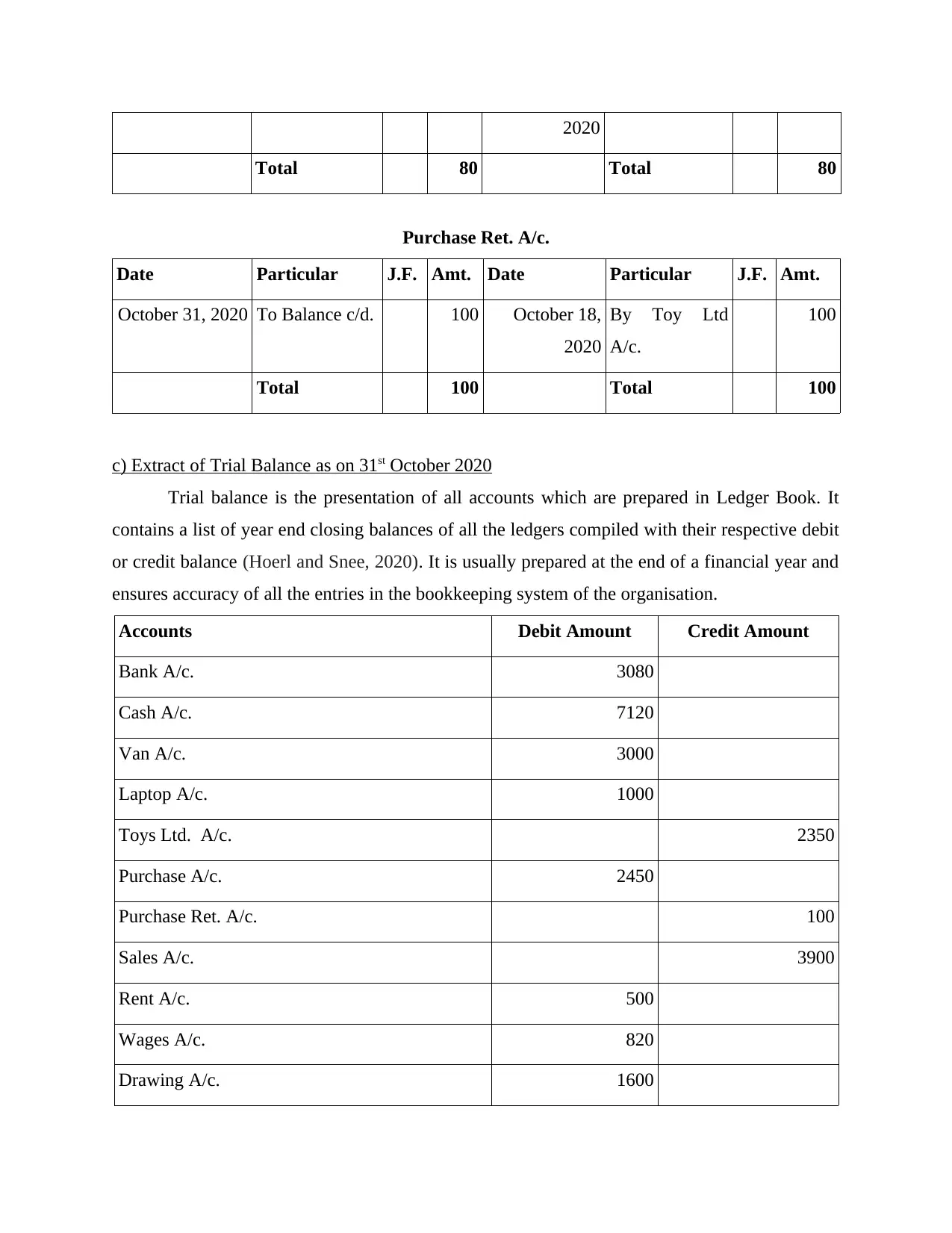

Purchase Ret. A/c.

Date Particular J.F. Amt. Date Particular J.F. Amt.

October 31, 2020 To Balance c/d. 100 October 18,

2020

By Toy Ltd

A/c.

100

Total 100 Total 100

c) Extract of Trial Balance as on 31st October 2020

Trial balance is the presentation of all accounts which are prepared in Ledger Book. It

contains a list of year end closing balances of all the ledgers compiled with their respective debit

or credit balance (Hoerl and Snee, 2020). It is usually prepared at the end of a financial year and

ensures accuracy of all the entries in the bookkeeping system of the organisation.

Accounts Debit Amount Credit Amount

Bank A/c. 3080

Cash A/c. 7120

Van A/c. 3000

Laptop A/c. 1000

Toys Ltd. A/c. 2350

Purchase A/c. 2450

Purchase Ret. A/c. 100

Sales A/c. 3900

Rent A/c. 500

Wages A/c. 820

Drawing A/c. 1600

Total 80 Total 80

Purchase Ret. A/c.

Date Particular J.F. Amt. Date Particular J.F. Amt.

October 31, 2020 To Balance c/d. 100 October 18,

2020

By Toy Ltd

A/c.

100

Total 100 Total 100

c) Extract of Trial Balance as on 31st October 2020

Trial balance is the presentation of all accounts which are prepared in Ledger Book. It

contains a list of year end closing balances of all the ledgers compiled with their respective debit

or credit balance (Hoerl and Snee, 2020). It is usually prepared at the end of a financial year and

ensures accuracy of all the entries in the bookkeeping system of the organisation.

Accounts Debit Amount Credit Amount

Bank A/c. 3080

Cash A/c. 7120

Van A/c. 3000

Laptop A/c. 1000

Toys Ltd. A/c. 2350

Purchase A/c. 2450

Purchase Ret. A/c. 100

Sales A/c. 3900

Rent A/c. 500

Wages A/c. 820

Drawing A/c. 1600

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

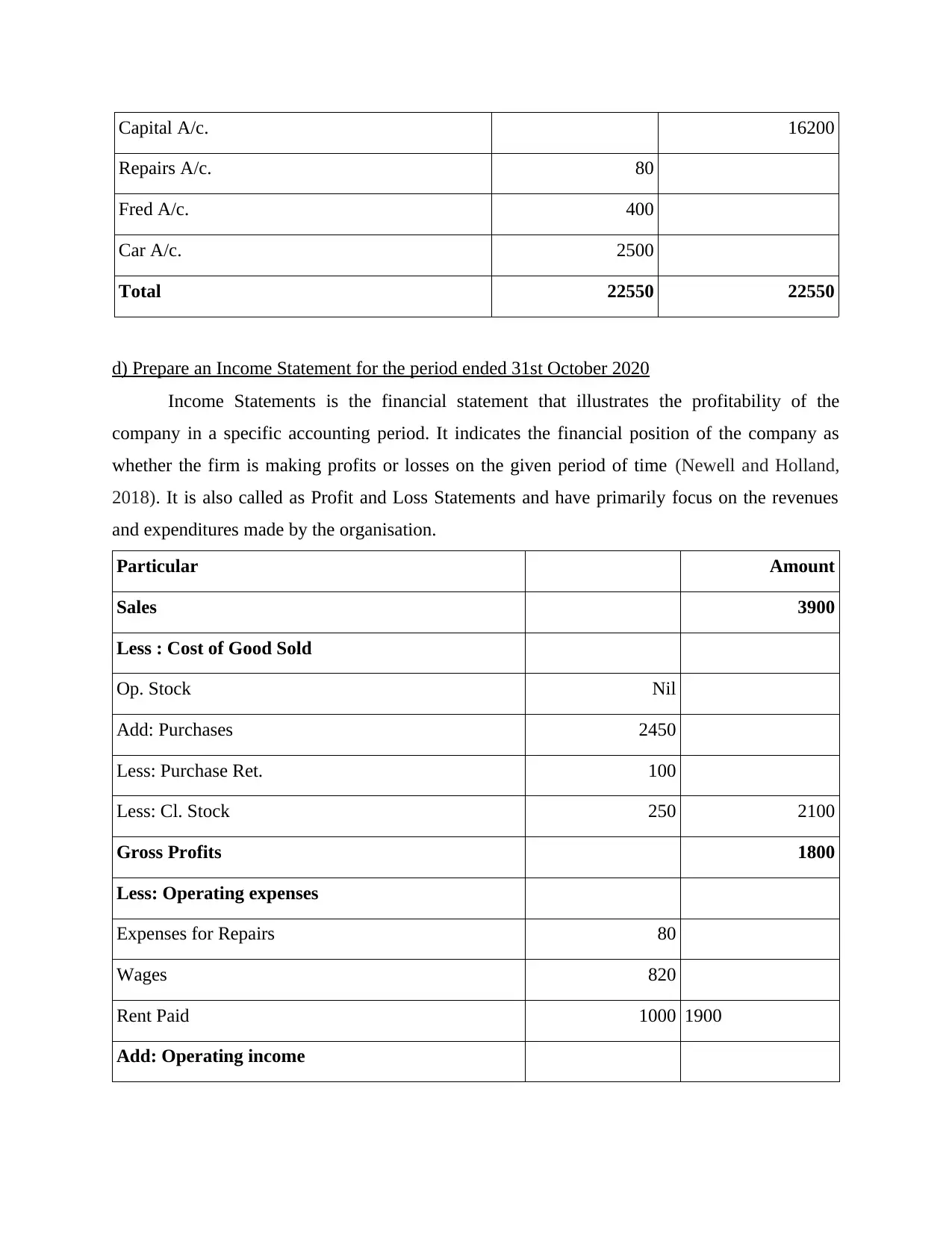

Capital A/c. 16200

Repairs A/c. 80

Fred A/c. 400

Car A/c. 2500

Total 22550 22550

d) Prepare an Income Statement for the period ended 31st October 2020

Income Statements is the financial statement that illustrates the profitability of the

company in a specific accounting period. It indicates the financial position of the company as

whether the firm is making profits or losses on the given period of time (Newell and Holland,

2018). It is also called as Profit and Loss Statements and have primarily focus on the revenues

and expenditures made by the organisation.

Particular Amount

Sales 3900

Less : Cost of Good Sold

Op. Stock Nil

Add: Purchases 2450

Less: Purchase Ret. 100

Less: Cl. Stock 250 2100

Gross Profits 1800

Less: Operating expenses

Expenses for Repairs 80

Wages 820

Rent Paid 1000 1900

Add: Operating income

Repairs A/c. 80

Fred A/c. 400

Car A/c. 2500

Total 22550 22550

d) Prepare an Income Statement for the period ended 31st October 2020

Income Statements is the financial statement that illustrates the profitability of the

company in a specific accounting period. It indicates the financial position of the company as

whether the firm is making profits or losses on the given period of time (Newell and Holland,

2018). It is also called as Profit and Loss Statements and have primarily focus on the revenues

and expenditures made by the organisation.

Particular Amount

Sales 3900

Less : Cost of Good Sold

Op. Stock Nil

Add: Purchases 2450

Less: Purchase Ret. 100

Less: Cl. Stock 250 2100

Gross Profits 1800

Less: Operating expenses

Expenses for Repairs 80

Wages 820

Rent Paid 1000 1900

Add: Operating income

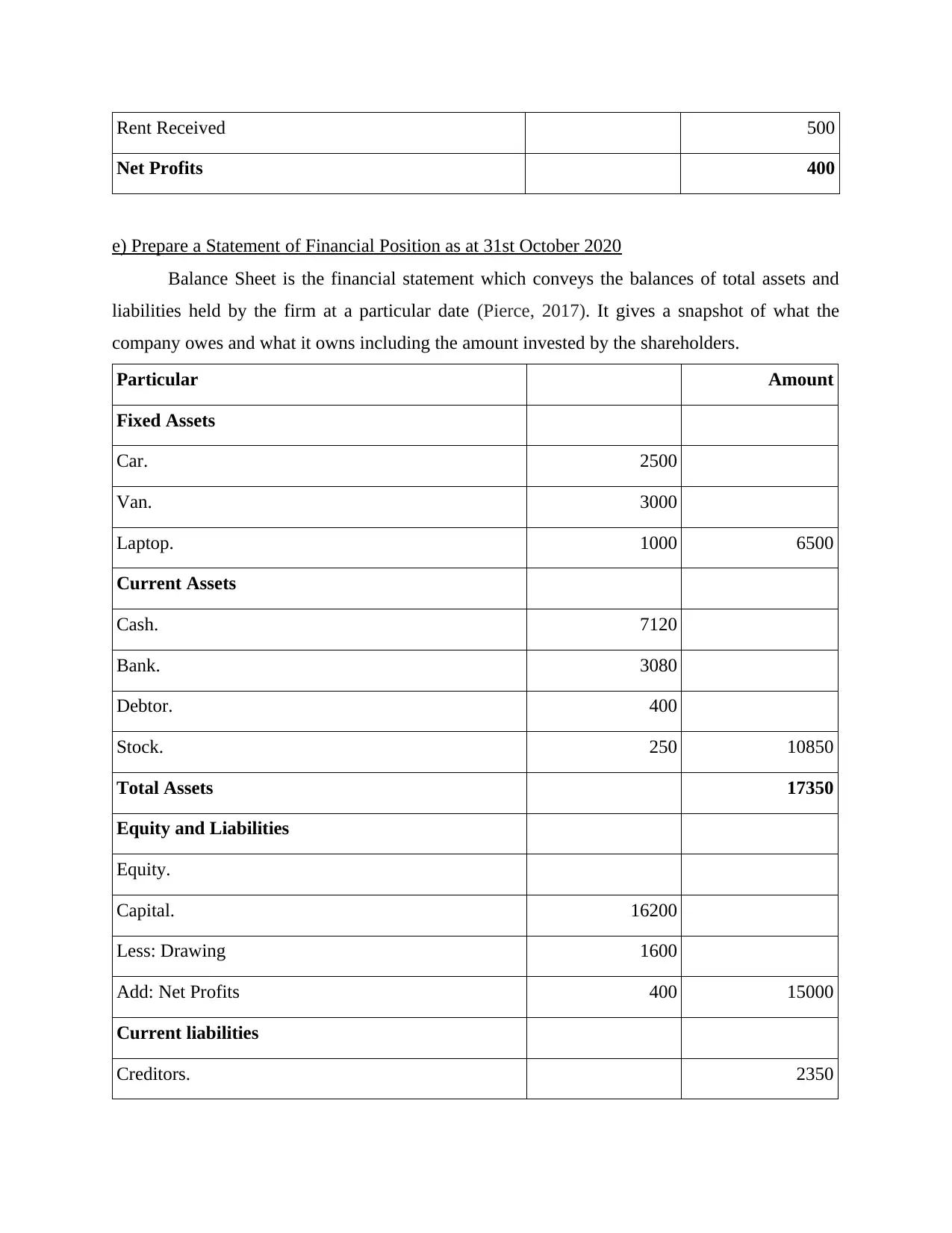

Rent Received 500

Net Profits 400

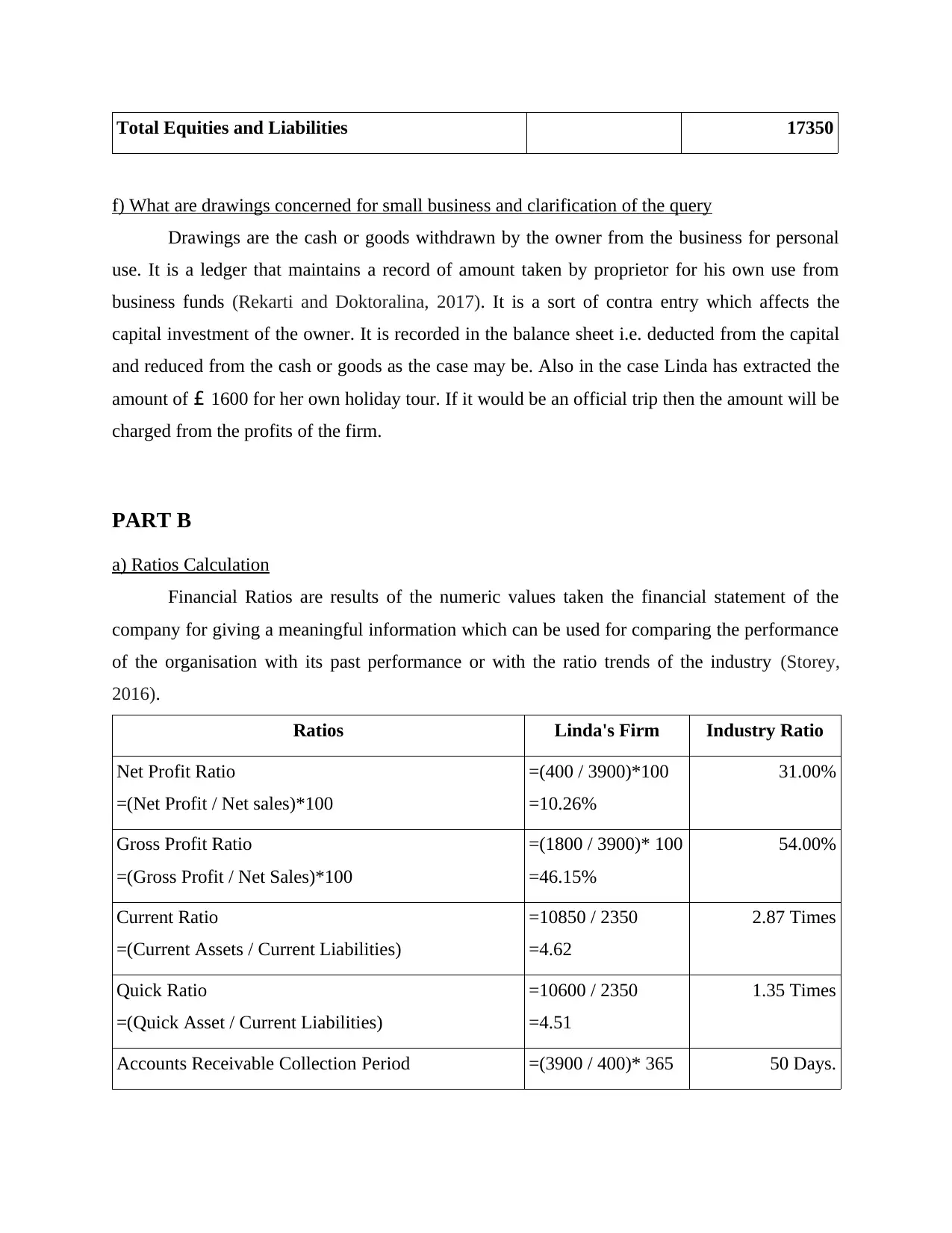

e) Prepare a Statement of Financial Position as at 31st October 2020

Balance Sheet is the financial statement which conveys the balances of total assets and

liabilities held by the firm at a particular date (Pierce, 2017). It gives a snapshot of what the

company owes and what it owns including the amount invested by the shareholders.

Particular Amount

Fixed Assets

Car. 2500

Van. 3000

Laptop. 1000 6500

Current Assets

Cash. 7120

Bank. 3080

Debtor. 400

Stock. 250 10850

Total Assets 17350

Equity and Liabilities

Equity.

Capital. 16200

Less: Drawing 1600

Add: Net Profits 400 15000

Current liabilities

Creditors. 2350

Net Profits 400

e) Prepare a Statement of Financial Position as at 31st October 2020

Balance Sheet is the financial statement which conveys the balances of total assets and

liabilities held by the firm at a particular date (Pierce, 2017). It gives a snapshot of what the

company owes and what it owns including the amount invested by the shareholders.

Particular Amount

Fixed Assets

Car. 2500

Van. 3000

Laptop. 1000 6500

Current Assets

Cash. 7120

Bank. 3080

Debtor. 400

Stock. 250 10850

Total Assets 17350

Equity and Liabilities

Equity.

Capital. 16200

Less: Drawing 1600

Add: Net Profits 400 15000

Current liabilities

Creditors. 2350

Total Equities and Liabilities 17350

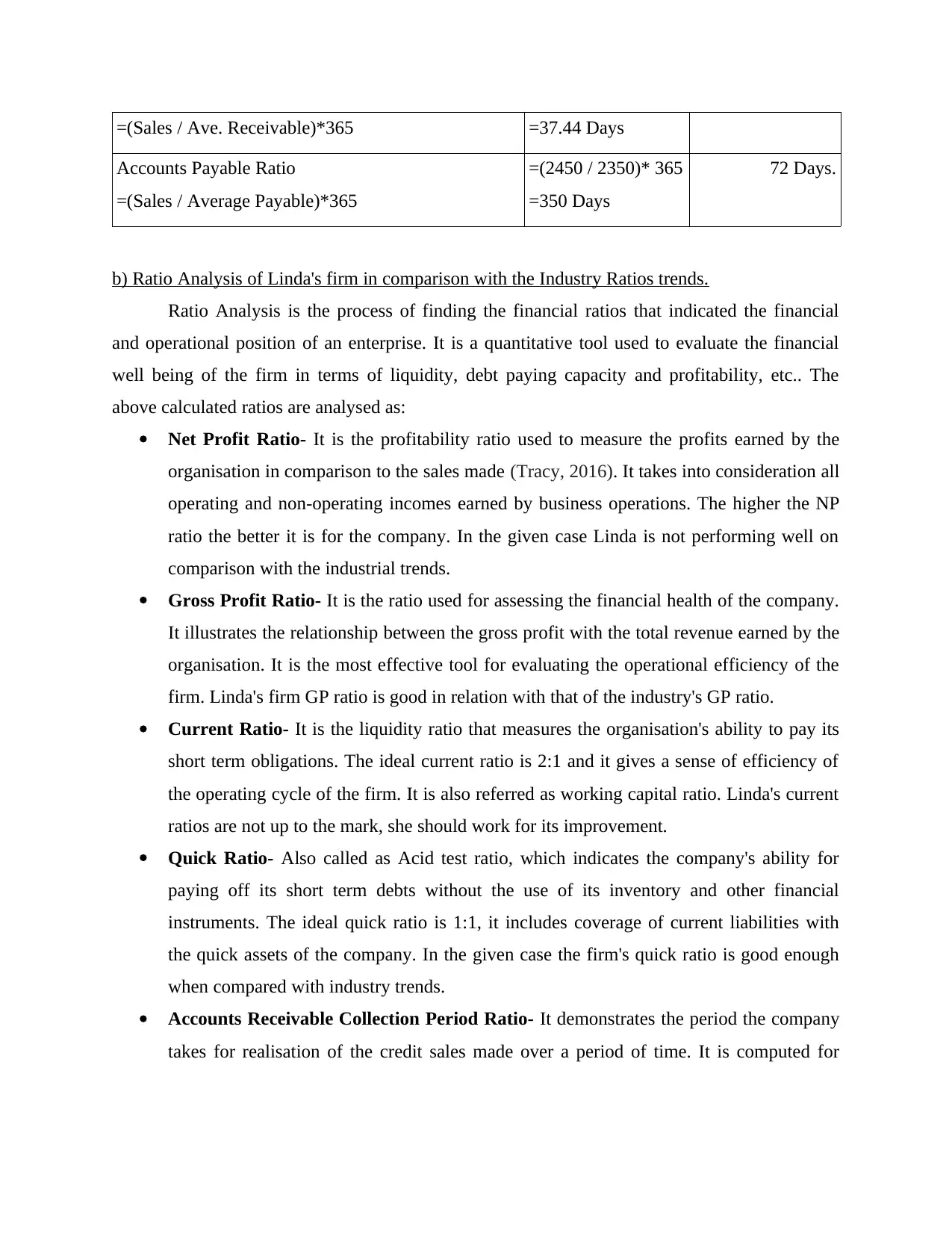

f) What are drawings concerned for small business and clarification of the query

Drawings are the cash or goods withdrawn by the owner from the business for personal

use. It is a ledger that maintains a record of amount taken by proprietor for his own use from

business funds (Rekarti and Doktoralina, 2017). It is a sort of contra entry which affects the

capital investment of the owner. It is recorded in the balance sheet i.e. deducted from the capital

and reduced from the cash or goods as the case may be. Also in the case Linda has extracted the

amount of £ 1600 for her own holiday tour. If it would be an official trip then the amount will be

charged from the profits of the firm.

PART B

a) Ratios Calculation

Financial Ratios are results of the numeric values taken the financial statement of the

company for giving a meaningful information which can be used for comparing the performance

of the organisation with its past performance or with the ratio trends of the industry (Storey,

2016).

Ratios Linda's Firm Industry Ratio

Net Profit Ratio

=(Net Profit / Net sales)*100

=(400 / 3900)*100

=10.26%

31.00%

Gross Profit Ratio

=(Gross Profit / Net Sales)*100

=(1800 / 3900)* 100

=46.15%

54.00%

Current Ratio

=(Current Assets / Current Liabilities)

=10850 / 2350

=4.62

2.87 Times

Quick Ratio

=(Quick Asset / Current Liabilities)

=10600 / 2350

=4.51

1.35 Times

Accounts Receivable Collection Period =(3900 / 400)* 365 50 Days.

f) What are drawings concerned for small business and clarification of the query

Drawings are the cash or goods withdrawn by the owner from the business for personal

use. It is a ledger that maintains a record of amount taken by proprietor for his own use from

business funds (Rekarti and Doktoralina, 2017). It is a sort of contra entry which affects the

capital investment of the owner. It is recorded in the balance sheet i.e. deducted from the capital

and reduced from the cash or goods as the case may be. Also in the case Linda has extracted the

amount of £ 1600 for her own holiday tour. If it would be an official trip then the amount will be

charged from the profits of the firm.

PART B

a) Ratios Calculation

Financial Ratios are results of the numeric values taken the financial statement of the

company for giving a meaningful information which can be used for comparing the performance

of the organisation with its past performance or with the ratio trends of the industry (Storey,

2016).

Ratios Linda's Firm Industry Ratio

Net Profit Ratio

=(Net Profit / Net sales)*100

=(400 / 3900)*100

=10.26%

31.00%

Gross Profit Ratio

=(Gross Profit / Net Sales)*100

=(1800 / 3900)* 100

=46.15%

54.00%

Current Ratio

=(Current Assets / Current Liabilities)

=10850 / 2350

=4.62

2.87 Times

Quick Ratio

=(Quick Asset / Current Liabilities)

=10600 / 2350

=4.51

1.35 Times

Accounts Receivable Collection Period =(3900 / 400)* 365 50 Days.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

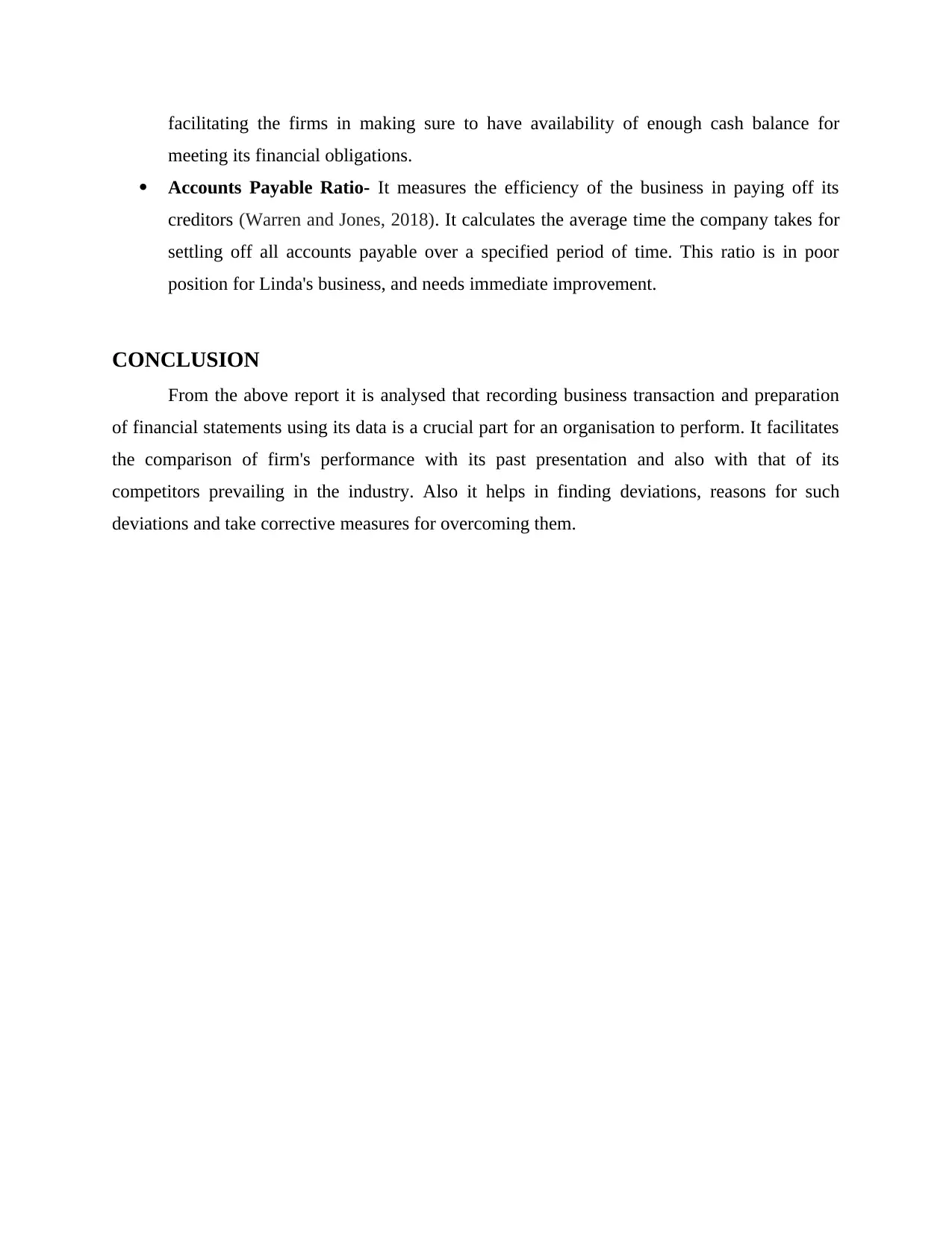

=(Sales / Ave. Receivable)*365 =37.44 Days

Accounts Payable Ratio

=(Sales / Average Payable)*365

=(2450 / 2350)* 365

=350 Days

72 Days.

b) Ratio Analysis of Linda's firm in comparison with the Industry Ratios trends.

Ratio Analysis is the process of finding the financial ratios that indicated the financial

and operational position of an enterprise. It is a quantitative tool used to evaluate the financial

well being of the firm in terms of liquidity, debt paying capacity and profitability, etc.. The

above calculated ratios are analysed as:

Net Profit Ratio- It is the profitability ratio used to measure the profits earned by the

organisation in comparison to the sales made (Tracy, 2016). It takes into consideration all

operating and non-operating incomes earned by business operations. The higher the NP

ratio the better it is for the company. In the given case Linda is not performing well on

comparison with the industrial trends.

Gross Profit Ratio- It is the ratio used for assessing the financial health of the company.

It illustrates the relationship between the gross profit with the total revenue earned by the

organisation. It is the most effective tool for evaluating the operational efficiency of the

firm. Linda's firm GP ratio is good in relation with that of the industry's GP ratio.

Current Ratio- It is the liquidity ratio that measures the organisation's ability to pay its

short term obligations. The ideal current ratio is 2:1 and it gives a sense of efficiency of

the operating cycle of the firm. It is also referred as working capital ratio. Linda's current

ratios are not up to the mark, she should work for its improvement.

Quick Ratio- Also called as Acid test ratio, which indicates the company's ability for

paying off its short term debts without the use of its inventory and other financial

instruments. The ideal quick ratio is 1:1, it includes coverage of current liabilities with

the quick assets of the company. In the given case the firm's quick ratio is good enough

when compared with industry trends.

Accounts Receivable Collection Period Ratio- It demonstrates the period the company

takes for realisation of the credit sales made over a period of time. It is computed for

Accounts Payable Ratio

=(Sales / Average Payable)*365

=(2450 / 2350)* 365

=350 Days

72 Days.

b) Ratio Analysis of Linda's firm in comparison with the Industry Ratios trends.

Ratio Analysis is the process of finding the financial ratios that indicated the financial

and operational position of an enterprise. It is a quantitative tool used to evaluate the financial

well being of the firm in terms of liquidity, debt paying capacity and profitability, etc.. The

above calculated ratios are analysed as:

Net Profit Ratio- It is the profitability ratio used to measure the profits earned by the

organisation in comparison to the sales made (Tracy, 2016). It takes into consideration all

operating and non-operating incomes earned by business operations. The higher the NP

ratio the better it is for the company. In the given case Linda is not performing well on

comparison with the industrial trends.

Gross Profit Ratio- It is the ratio used for assessing the financial health of the company.

It illustrates the relationship between the gross profit with the total revenue earned by the

organisation. It is the most effective tool for evaluating the operational efficiency of the

firm. Linda's firm GP ratio is good in relation with that of the industry's GP ratio.

Current Ratio- It is the liquidity ratio that measures the organisation's ability to pay its

short term obligations. The ideal current ratio is 2:1 and it gives a sense of efficiency of

the operating cycle of the firm. It is also referred as working capital ratio. Linda's current

ratios are not up to the mark, she should work for its improvement.

Quick Ratio- Also called as Acid test ratio, which indicates the company's ability for

paying off its short term debts without the use of its inventory and other financial

instruments. The ideal quick ratio is 1:1, it includes coverage of current liabilities with

the quick assets of the company. In the given case the firm's quick ratio is good enough

when compared with industry trends.

Accounts Receivable Collection Period Ratio- It demonstrates the period the company

takes for realisation of the credit sales made over a period of time. It is computed for

facilitating the firms in making sure to have availability of enough cash balance for

meeting its financial obligations.

Accounts Payable Ratio- It measures the efficiency of the business in paying off its

creditors (Warren and Jones, 2018). It calculates the average time the company takes for

settling off all accounts payable over a specified period of time. This ratio is in poor

position for Linda's business, and needs immediate improvement.

CONCLUSION

From the above report it is analysed that recording business transaction and preparation

of financial statements using its data is a crucial part for an organisation to perform. It facilitates

the comparison of firm's performance with its past presentation and also with that of its

competitors prevailing in the industry. Also it helps in finding deviations, reasons for such

deviations and take corrective measures for overcoming them.

meeting its financial obligations.

Accounts Payable Ratio- It measures the efficiency of the business in paying off its

creditors (Warren and Jones, 2018). It calculates the average time the company takes for

settling off all accounts payable over a specified period of time. This ratio is in poor

position for Linda's business, and needs immediate improvement.

CONCLUSION

From the above report it is analysed that recording business transaction and preparation

of financial statements using its data is a crucial part for an organisation to perform. It facilitates

the comparison of firm's performance with its past presentation and also with that of its

competitors prevailing in the industry. Also it helps in finding deviations, reasons for such

deviations and take corrective measures for overcoming them.

REFERENCES

Books and Journals

Adekola, A. and Sergi, B.S., 2016. Global business management: A cross-cultural perspective.

Routledge.

Allen, P., 2018. Artist management for the music business. Routledge.

Black, K., 2019. Business statistics: for contemporary decision making. John Wiley & Sons.

Hoerl, R.W. and Snee, R.D., 2020. Statistical thinking: Improving business performance. John

Wiley & Sons.

Newell, P. and Holland, K., 2018. Loudspeakers: For music recording and reproduction.

Routledge.

Pierce, J.M., 2017. Writing at the Speed of Sound: Music Stenography and Recording beyond

the Phonograph. 19th-Century Music. 41(2). pp.121-150.

Rekarti, E. and Doktoralina, C.M., 2017. Improving business performance: A proposed model

for SMEs.

Storey, D.J., 2016. Understanding the small business sector. Routledge.

Tracy, J.A., 2016. Accounting for dummies. John Wiley & Sons.

Warren, C.S. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

Books and Journals

Adekola, A. and Sergi, B.S., 2016. Global business management: A cross-cultural perspective.

Routledge.

Allen, P., 2018. Artist management for the music business. Routledge.

Black, K., 2019. Business statistics: for contemporary decision making. John Wiley & Sons.

Hoerl, R.W. and Snee, R.D., 2020. Statistical thinking: Improving business performance. John

Wiley & Sons.

Newell, P. and Holland, K., 2018. Loudspeakers: For music recording and reproduction.

Routledge.

Pierce, J.M., 2017. Writing at the Speed of Sound: Music Stenography and Recording beyond

the Phonograph. 19th-Century Music. 41(2). pp.121-150.

Rekarti, E. and Doktoralina, C.M., 2017. Improving business performance: A proposed model

for SMEs.

Storey, D.J., 2016. Understanding the small business sector. Routledge.

Tracy, J.A., 2016. Accounting for dummies. John Wiley & Sons.

Warren, C.S. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.