Recording Business Transactions: Steps for Starting a Sole Trading Business, Decision Makers Using Accounting Information, Journal Entries, Ledgers, and Income Statement

VerifiedAdded on 2023/06/14

|13

|2381

|453

AI Summary

This report covers the steps for starting a sole trading business, decision makers using accounting information, journal entries, ledgers, and income statement. It includes a detailed guide on starting a sole trading business, the importance of accounting information for decision makers, examples of journal entries and ledgers, and an income statement for BMoore with a prediction of next year's profit/loss.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Recording Business

transaction

transaction

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION ..........................................................................................................................3

TASK A...........................................................................................................................................3

I. Steps for starting new sole trading business as decorator by David Green........................3

II. Decision makers related to a business which uses accounting information to aid their

decisions.................................................................................................................................4

TASK B...........................................................................................................................................5

1. Recording journal entries in the books of accounts of Fpolk............................................5

2. Maintaining ledgers accounts and trial balance of Maurice and brothers ........................6

PART 4............................................................................................................................................9

(a) Preparing income statement and prediction of next year profit of BMoore.....................9

Income statement for the year ended 30 September 2021......................................................9

b) Why the profit has decreased and increased over the years and what will be the estimate of

profit/loss in 2022.................................................................................................................10

CONCLUSION .............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION ..........................................................................................................................3

TASK A...........................................................................................................................................3

I. Steps for starting new sole trading business as decorator by David Green........................3

II. Decision makers related to a business which uses accounting information to aid their

decisions.................................................................................................................................4

TASK B...........................................................................................................................................5

1. Recording journal entries in the books of accounts of Fpolk............................................5

2. Maintaining ledgers accounts and trial balance of Maurice and brothers ........................6

PART 4............................................................................................................................................9

(a) Preparing income statement and prediction of next year profit of BMoore.....................9

Income statement for the year ended 30 September 2021......................................................9

b) Why the profit has decreased and increased over the years and what will be the estimate of

profit/loss in 2022.................................................................................................................10

CONCLUSION .............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

In each business there are series of financial exchange which happens. Exchanges of business

incorporates that multitude of occasions which happens between at least two gatherings by the

product of items and services (Orthodoxou, and et.al., 2021). This report is divided into three

areas. The initial segment will cover the means for beginning a sole exchanging business of

David Green. It additionally depicts about the Aviva Plc. which is listed on the London stock

trade alongside the users of the accounting data. In Part B , the journal entries of Fpolk in the

books of records and keeping up with record records and preliminary equilibrium of ABC

undertakings. In Part C, the assessment of the Income articulation of B Moore and effect of

covid19 on the business is examined toward the end.

TASK A

I. Steps for starting new sole trading business as decorator by David Green.

A sole ownership is a type of business which can be effectively overseen on the grounds that

there is just a solitary chief and less possibilities of miscommunication. David Green needs to set

up another sole merchant business as decorator in this way, steps of starting another firm can be

clarified as given beneath

1. Put together exploration in the market: Conducting review in the commercial center assists

with gathering data about the current contentions in the field of embellishment and being familiar

with client portion who are keen on results of decoration (Davidson, 2018).

2. Drafting strategy: Before beginning real work, outline of business thoughts, plans,

methodologies of promoting, how it will run and what will be the bookkeeping systems to keep

up with fiscal reports is fundamental for smooth direct of big business.

3. Source of financing-In this progression, dealer will appraise the prerequisites of capital

required and sources from where assets can be brought needed up in working business of

improvement.

4. Deciding place of business: Location of firm likewise contributes in its prosperity it is

possible that it will situated on concentrated area or offering both on the web and disconnected

administrations (da Silva Rodrigues, 2021). The choices chose will influence the income of the

firm also.

In each business there are series of financial exchange which happens. Exchanges of business

incorporates that multitude of occasions which happens between at least two gatherings by the

product of items and services (Orthodoxou, and et.al., 2021). This report is divided into three

areas. The initial segment will cover the means for beginning a sole exchanging business of

David Green. It additionally depicts about the Aviva Plc. which is listed on the London stock

trade alongside the users of the accounting data. In Part B , the journal entries of Fpolk in the

books of records and keeping up with record records and preliminary equilibrium of ABC

undertakings. In Part C, the assessment of the Income articulation of B Moore and effect of

covid19 on the business is examined toward the end.

TASK A

I. Steps for starting new sole trading business as decorator by David Green.

A sole ownership is a type of business which can be effectively overseen on the grounds that

there is just a solitary chief and less possibilities of miscommunication. David Green needs to set

up another sole merchant business as decorator in this way, steps of starting another firm can be

clarified as given beneath

1. Put together exploration in the market: Conducting review in the commercial center assists

with gathering data about the current contentions in the field of embellishment and being familiar

with client portion who are keen on results of decoration (Davidson, 2018).

2. Drafting strategy: Before beginning real work, outline of business thoughts, plans,

methodologies of promoting, how it will run and what will be the bookkeeping systems to keep

up with fiscal reports is fundamental for smooth direct of big business.

3. Source of financing-In this progression, dealer will appraise the prerequisites of capital

required and sources from where assets can be brought needed up in working business of

improvement.

4. Deciding place of business: Location of firm likewise contributes in its prosperity it is

possible that it will situated on concentrated area or offering both on the web and disconnected

administrations (da Silva Rodrigues, 2021). The choices chose will influence the income of the

firm also.

5. Choosing name of business: To situate a firm in the personalities of individuals, choosing a

name which suitably portrays the nature and brand of business accurately will likewise upgrade

the benefit of a sole exchanging business. Guaranteeing that name picked ought not be utilized

by some other brand is hence fundamental.

6. Enrolling business: It is significant to secure a business with legitimate arrangement for

guaranteeing that design business is completed with following predefined set of cycles, for

example, rules and guidelines withstanding while at the same time working a business.

7. Applying for License and starting business account: After getting enlistment of firm, David

Green can apply for brightening sole merchant permit and when administrative work is finished

it can likewise demand for opening financial balance to set aside and pulling out cash and

numerous other business related exchanges (Helgeson, and Nierenberg, 2018).

II. Decision makers related to a business which uses accounting information to aid their

decisions.

Accounting is the method involved with recording,analysing,interpreting and summing

up the monetary exchanges of the business to watch out for the monetary exhibition of a venture.

It is essential to follow bookkeeping cycle to take choices with respect to estimating monetary

execution based on current execution (Bâtcă-Dumitru, 2020). To keep up with security in money

related terms and keep track on the incomes of the business general bookkeeping principles are

embraced while planning fiscal reports of an undertaking. Aviva Plc, British multinational

insurance company headquartered in London, England, bookkeeping data is critical for its

stakeholders. Given underneath are the leaders of the accounting information -

Investors: This incorporates people or venture having shares in load of a specific organization.

Aviva Plc, investors utilizes its bookkeeping data to acquire the bits of knowledge about

monetary wellbeing.

Government-Accounting data is important to guarantee government pretty much every one of the

recommended rules and guidelines are followed by an endeavour or not.

Creditors: Lender utilizes data of records to check about the limit of borrower, monetary position

and its taking care of capacity. Lenders of Aviva Plc, utilizes its records to be aware of capacity

to reimburse the obligations taken.

Lenders: For raising capital of a firm it requires finance for something similar, financial backers

are people who supply required assets in business (White, 2020). Bookkeeping data of Aviva

name which suitably portrays the nature and brand of business accurately will likewise upgrade

the benefit of a sole exchanging business. Guaranteeing that name picked ought not be utilized

by some other brand is hence fundamental.

6. Enrolling business: It is significant to secure a business with legitimate arrangement for

guaranteeing that design business is completed with following predefined set of cycles, for

example, rules and guidelines withstanding while at the same time working a business.

7. Applying for License and starting business account: After getting enlistment of firm, David

Green can apply for brightening sole merchant permit and when administrative work is finished

it can likewise demand for opening financial balance to set aside and pulling out cash and

numerous other business related exchanges (Helgeson, and Nierenberg, 2018).

II. Decision makers related to a business which uses accounting information to aid their

decisions.

Accounting is the method involved with recording,analysing,interpreting and summing

up the monetary exchanges of the business to watch out for the monetary exhibition of a venture.

It is essential to follow bookkeeping cycle to take choices with respect to estimating monetary

execution based on current execution (Bâtcă-Dumitru, 2020). To keep up with security in money

related terms and keep track on the incomes of the business general bookkeeping principles are

embraced while planning fiscal reports of an undertaking. Aviva Plc, British multinational

insurance company headquartered in London, England, bookkeeping data is critical for its

stakeholders. Given underneath are the leaders of the accounting information -

Investors: This incorporates people or venture having shares in load of a specific organization.

Aviva Plc, investors utilizes its bookkeeping data to acquire the bits of knowledge about

monetary wellbeing.

Government-Accounting data is important to guarantee government pretty much every one of the

recommended rules and guidelines are followed by an endeavour or not.

Creditors: Lender utilizes data of records to check about the limit of borrower, monetary position

and its taking care of capacity. Lenders of Aviva Plc, utilizes its records to be aware of capacity

to reimburse the obligations taken.

Lenders: For raising capital of a firm it requires finance for something similar, financial backers

are people who supply required assets in business (White, 2020). Bookkeeping data of Aviva

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

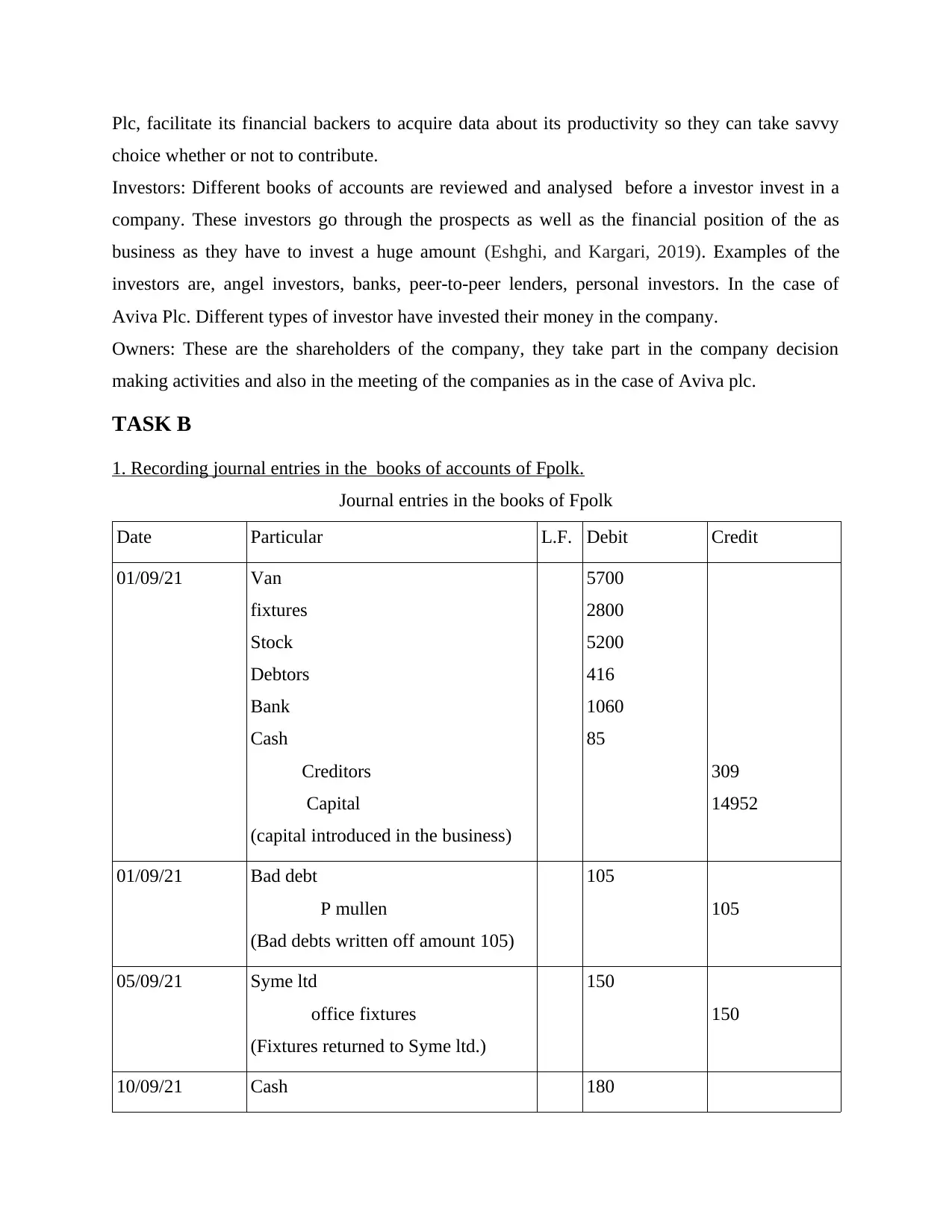

Plc, facilitate its financial backers to acquire data about its productivity so they can take savvy

choice whether or not to contribute.

Investors: Different books of accounts are reviewed and analysed before a investor invest in a

company. These investors go through the prospects as well as the financial position of the as

business as they have to invest a huge amount (Eshghi, and Kargari, 2019). Examples of the

investors are, angel investors, banks, peer-to-peer lenders, personal investors. In the case of

Aviva Plc. Different types of investor have invested their money in the company.

Owners: These are the shareholders of the company, they take part in the company decision

making activities and also in the meeting of the companies as in the case of Aviva plc.

TASK B

1. Recording journal entries in the books of accounts of Fpolk.

Journal entries in the books of Fpolk

Date Particular L.F. Debit Credit

01/09/21 Van

fixtures

Stock

Debtors

Bank

Cash

Creditors

Capital

(capital introduced in the business)

5700

2800

5200

416

1060

85

309

14952

01/09/21 Bad debt

P mullen

(Bad debts written off amount 105)

105

105

05/09/21 Syme ltd

office fixtures

(Fixtures returned to Syme ltd.)

150

150

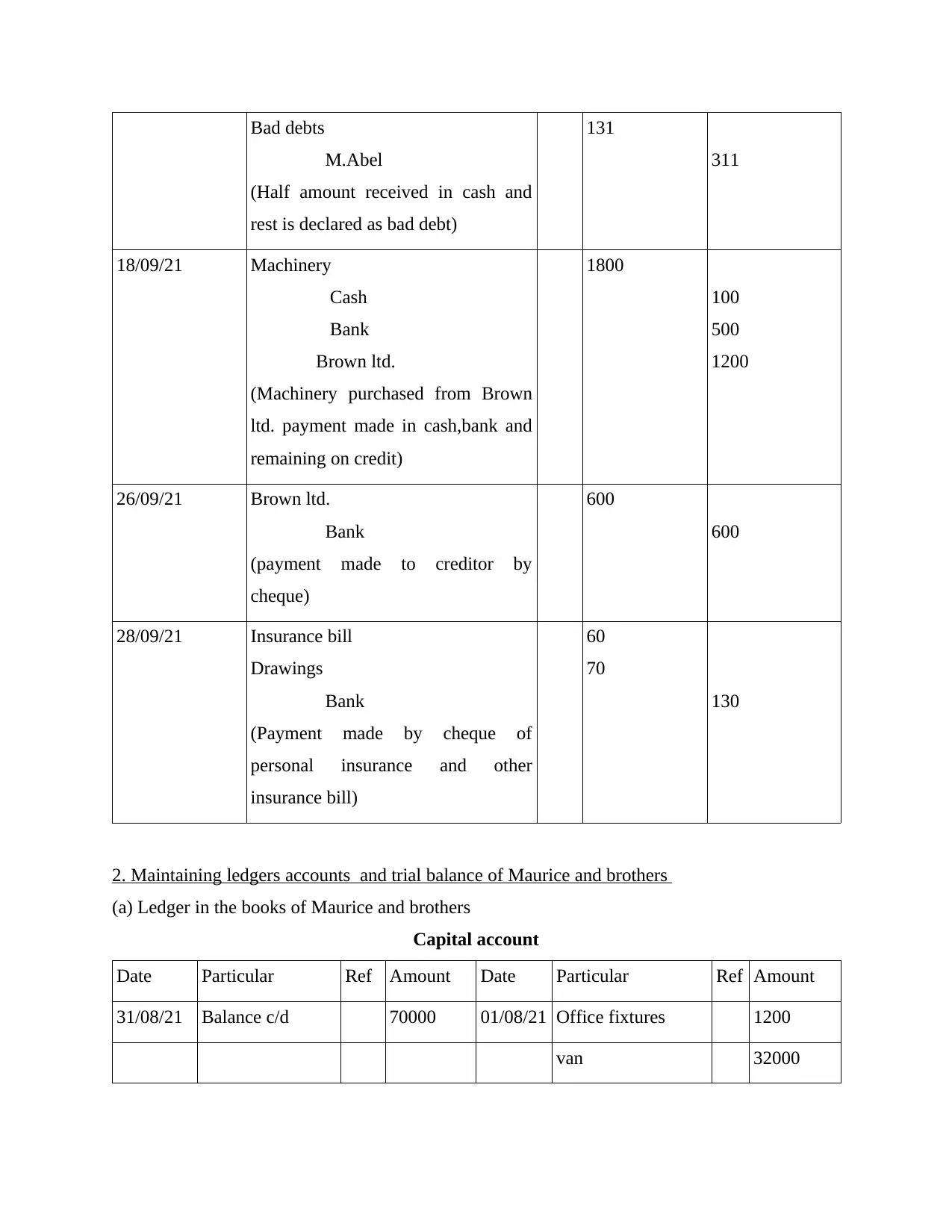

10/09/21 Cash 180

choice whether or not to contribute.

Investors: Different books of accounts are reviewed and analysed before a investor invest in a

company. These investors go through the prospects as well as the financial position of the as

business as they have to invest a huge amount (Eshghi, and Kargari, 2019). Examples of the

investors are, angel investors, banks, peer-to-peer lenders, personal investors. In the case of

Aviva Plc. Different types of investor have invested their money in the company.

Owners: These are the shareholders of the company, they take part in the company decision

making activities and also in the meeting of the companies as in the case of Aviva plc.

TASK B

1. Recording journal entries in the books of accounts of Fpolk.

Journal entries in the books of Fpolk

Date Particular L.F. Debit Credit

01/09/21 Van

fixtures

Stock

Debtors

Bank

Cash

Creditors

Capital

(capital introduced in the business)

5700

2800

5200

416

1060

85

309

14952

01/09/21 Bad debt

P mullen

(Bad debts written off amount 105)

105

105

05/09/21 Syme ltd

office fixtures

(Fixtures returned to Syme ltd.)

150

150

10/09/21 Cash 180

Bad debts

M.Abel

(Half amount received in cash and

rest is declared as bad debt)

131

311

18/09/21 Machinery

Cash

Bank

Brown ltd.

(Machinery purchased from Brown

ltd. payment made in cash,bank and

remaining on credit)

1800

100

500

1200

26/09/21 Brown ltd.

Bank

(payment made to creditor by

cheque)

600

600

28/09/21 Insurance bill

Drawings

Bank

(Payment made by cheque of

personal insurance and other

insurance bill)

60

70

130

2. Maintaining ledgers accounts and trial balance of Maurice and brothers

(a) Ledger in the books of Maurice and brothers

Capital account

Date Particular Ref Amount Date Particular Ref Amount

31/08/21 Balance c/d 70000 01/08/21 Office fixtures 1200

van 32000

M.Abel

(Half amount received in cash and

rest is declared as bad debt)

131

311

18/09/21 Machinery

Cash

Bank

Brown ltd.

(Machinery purchased from Brown

ltd. payment made in cash,bank and

remaining on credit)

1800

100

500

1200

26/09/21 Brown ltd.

Bank

(payment made to creditor by

cheque)

600

600

28/09/21 Insurance bill

Drawings

Bank

(Payment made by cheque of

personal insurance and other

insurance bill)

60

70

130

2. Maintaining ledgers accounts and trial balance of Maurice and brothers

(a) Ledger in the books of Maurice and brothers

Capital account

Date Particular Ref Amount Date Particular Ref Amount

31/08/21 Balance c/d 70000 01/08/21 Office fixtures 1200

van 32000

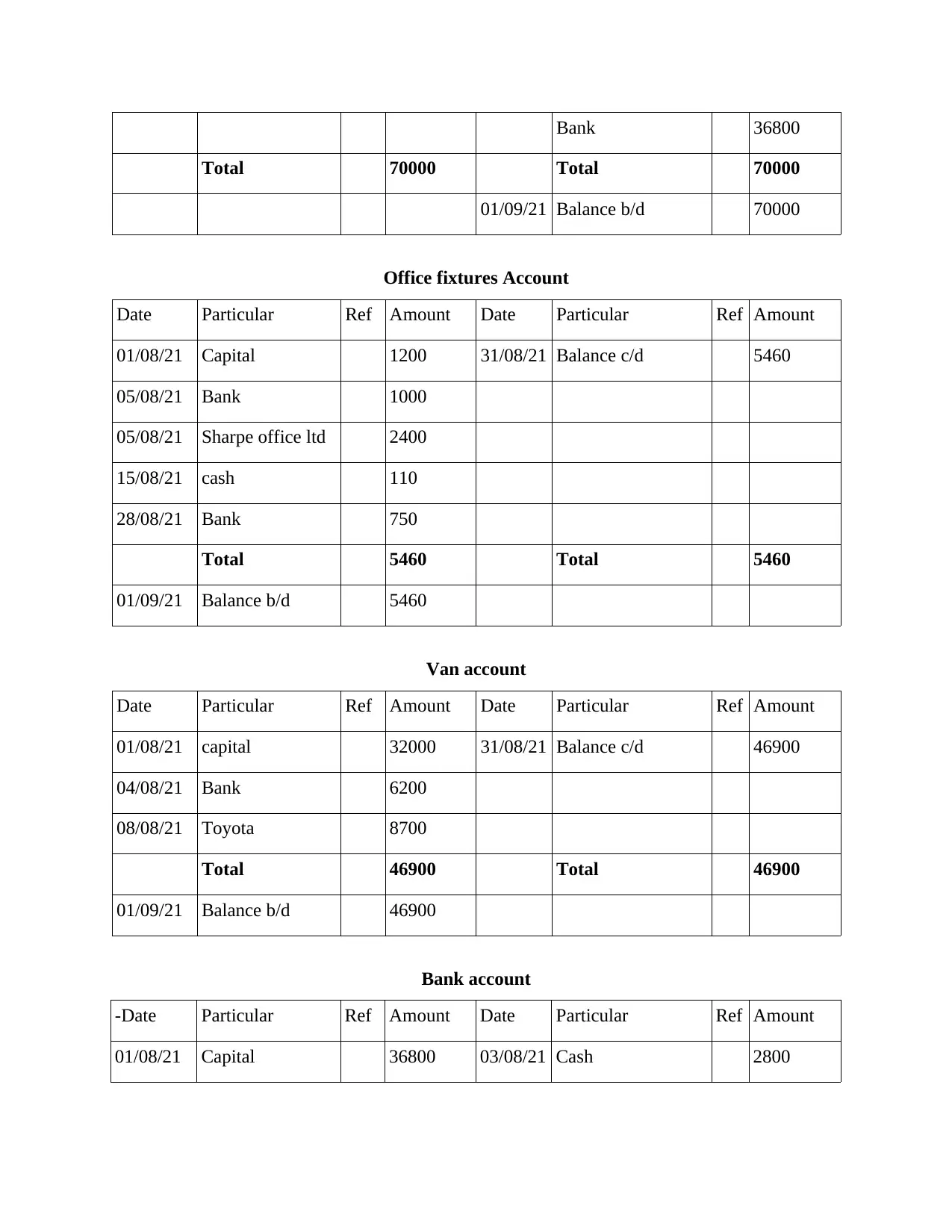

Bank 36800

Total 70000 Total 70000

01/09/21 Balance b/d 70000

Office fixtures Account

Date Particular Ref Amount Date Particular Ref Amount

01/08/21 Capital 1200 31/08/21 Balance c/d 5460

05/08/21 Bank 1000

05/08/21 Sharpe office ltd 2400

15/08/21 cash 110

28/08/21 Bank 750

Total 5460 Total 5460

01/09/21 Balance b/d 5460

Van account

Date Particular Ref Amount Date Particular Ref Amount

01/08/21 capital 32000 31/08/21 Balance c/d 46900

04/08/21 Bank 6200

08/08/21 Toyota 8700

Total 46900 Total 46900

01/09/21 Balance b/d 46900

Bank account

-Date Particular Ref Amount Date Particular Ref Amount

01/08/21 Capital 36800 03/08/21 Cash 2800

Total 70000 Total 70000

01/09/21 Balance b/d 70000

Office fixtures Account

Date Particular Ref Amount Date Particular Ref Amount

01/08/21 Capital 1200 31/08/21 Balance c/d 5460

05/08/21 Bank 1000

05/08/21 Sharpe office ltd 2400

15/08/21 cash 110

28/08/21 Bank 750

Total 5460 Total 5460

01/09/21 Balance b/d 5460

Van account

Date Particular Ref Amount Date Particular Ref Amount

01/08/21 capital 32000 31/08/21 Balance c/d 46900

04/08/21 Bank 6200

08/08/21 Toyota 8700

Total 46900 Total 46900

01/09/21 Balance b/d 46900

Bank account

-Date Particular Ref Amount Date Particular Ref Amount

01/08/21 Capital 36800 03/08/21 Cash 2800

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

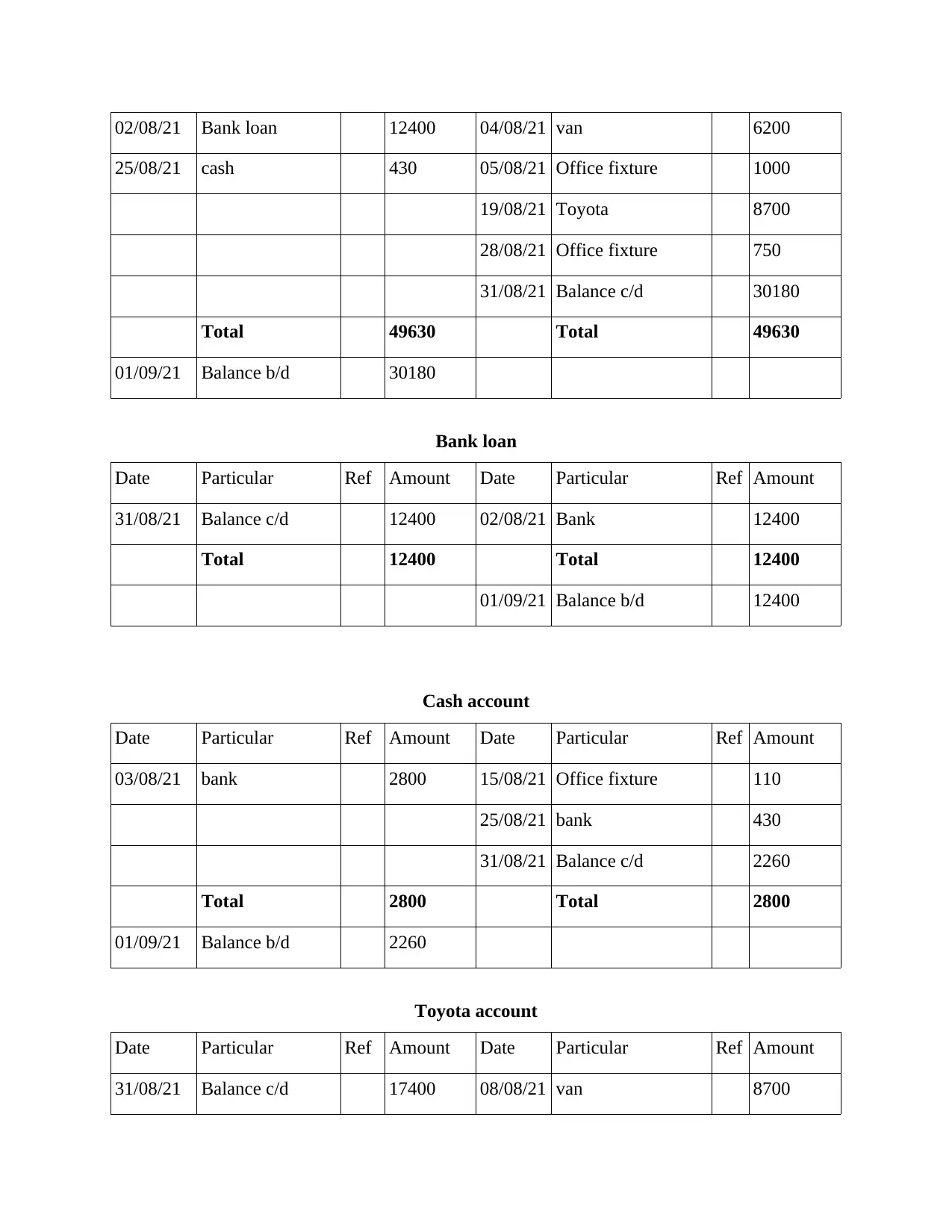

02/08/21 Bank loan 12400 04/08/21 van 6200

25/08/21 cash 430 05/08/21 Office fixture 1000

19/08/21 Toyota 8700

28/08/21 Office fixture 750

31/08/21 Balance c/d 30180

Total 49630 Total 49630

01/09/21 Balance b/d 30180

Bank loan

Date Particular Ref Amount Date Particular Ref Amount

31/08/21 Balance c/d 12400 02/08/21 Bank 12400

Total 12400 Total 12400

01/09/21 Balance b/d 12400

Cash account

Date Particular Ref Amount Date Particular Ref Amount

03/08/21 bank 2800 15/08/21 Office fixture 110

25/08/21 bank 430

31/08/21 Balance c/d 2260

Total 2800 Total 2800

01/09/21 Balance b/d 2260

Toyota account

Date Particular Ref Amount Date Particular Ref Amount

31/08/21 Balance c/d 17400 08/08/21 van 8700

25/08/21 cash 430 05/08/21 Office fixture 1000

19/08/21 Toyota 8700

28/08/21 Office fixture 750

31/08/21 Balance c/d 30180

Total 49630 Total 49630

01/09/21 Balance b/d 30180

Bank loan

Date Particular Ref Amount Date Particular Ref Amount

31/08/21 Balance c/d 12400 02/08/21 Bank 12400

Total 12400 Total 12400

01/09/21 Balance b/d 12400

Cash account

Date Particular Ref Amount Date Particular Ref Amount

03/08/21 bank 2800 15/08/21 Office fixture 110

25/08/21 bank 430

31/08/21 Balance c/d 2260

Total 2800 Total 2800

01/09/21 Balance b/d 2260

Toyota account

Date Particular Ref Amount Date Particular Ref Amount

31/08/21 Balance c/d 17400 08/08/21 van 8700

19/08/21 bank 8700

Total 17400 Total 17400

01/09/21 Balance b/d 17400

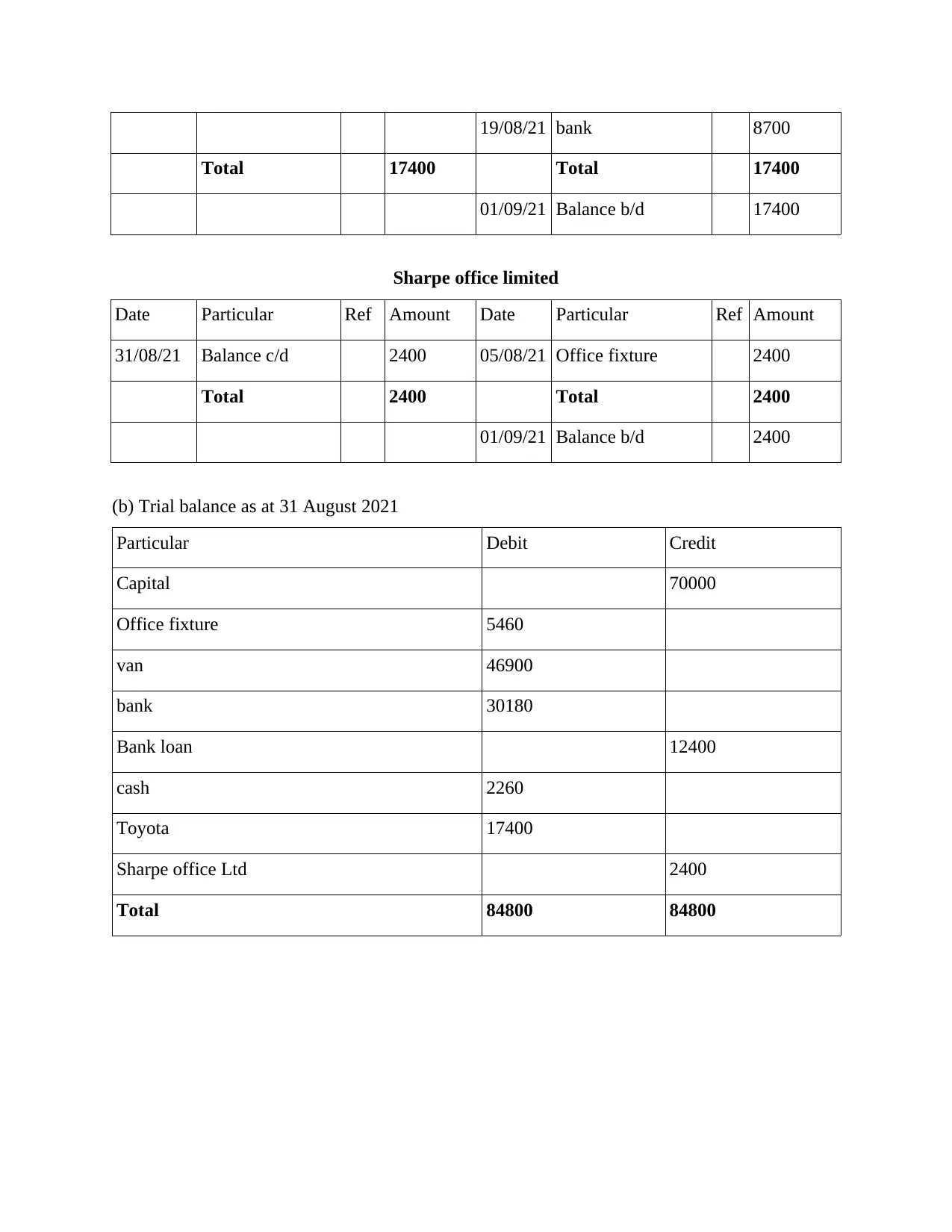

Sharpe office limited

Date Particular Ref Amount Date Particular Ref Amount

31/08/21 Balance c/d 2400 05/08/21 Office fixture 2400

Total 2400 Total 2400

01/09/21 Balance b/d 2400

(b) Trial balance as at 31 August 2021

Particular Debit Credit

Capital 70000

Office fixture 5460

van 46900

bank 30180

Bank loan 12400

cash 2260

Toyota 17400

Sharpe office Ltd 2400

Total 84800 84800

Total 17400 Total 17400

01/09/21 Balance b/d 17400

Sharpe office limited

Date Particular Ref Amount Date Particular Ref Amount

31/08/21 Balance c/d 2400 05/08/21 Office fixture 2400

Total 2400 Total 2400

01/09/21 Balance b/d 2400

(b) Trial balance as at 31 August 2021

Particular Debit Credit

Capital 70000

Office fixture 5460

van 46900

bank 30180

Bank loan 12400

cash 2260

Toyota 17400

Sharpe office Ltd 2400

Total 84800 84800

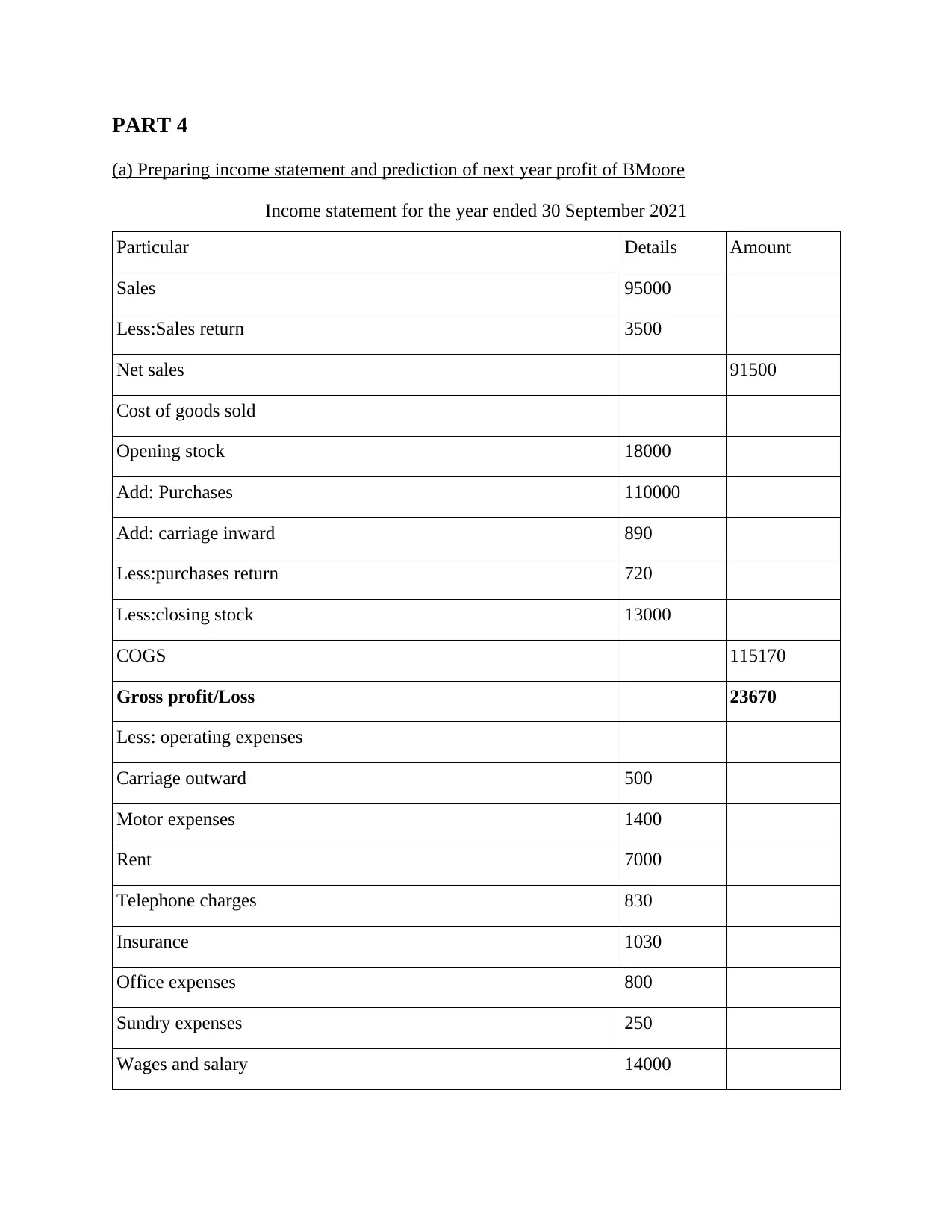

PART 4

(a) Preparing income statement and prediction of next year profit of BMoore

Income statement for the year ended 30 September 2021

Particular Details Amount

Sales 95000

Less:Sales return 3500

Net sales 91500

Cost of goods sold

Opening stock 18000

Add: Purchases 110000

Add: carriage inward 890

Less:purchases return 720

Less:closing stock 13000

COGS 115170

Gross profit/Loss 23670

Less: operating expenses

Carriage outward 500

Motor expenses 1400

Rent 7000

Telephone charges 830

Insurance 1030

Office expenses 800

Sundry expenses 250

Wages and salary 14000

(a) Preparing income statement and prediction of next year profit of BMoore

Income statement for the year ended 30 September 2021

Particular Details Amount

Sales 95000

Less:Sales return 3500

Net sales 91500

Cost of goods sold

Opening stock 18000

Add: Purchases 110000

Add: carriage inward 890

Less:purchases return 720

Less:closing stock 13000

COGS 115170

Gross profit/Loss 23670

Less: operating expenses

Carriage outward 500

Motor expenses 1400

Rent 7000

Telephone charges 830

Insurance 1030

Office expenses 800

Sundry expenses 250

Wages and salary 14000

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Operating expenses 25810

Net loss -49480

b) Why the profit has decreased and increased over the years and what will be the estimate of

profit/loss in 2022.

Many of the companies found it difficult to maintain their financial records smooth as

before. Because of the occurrence of the Covid in the first quarter of the year the businesses has

effected significantly and it effected each and every business (Davies, 2022). In the month of

march all the activities of the businesses got stop all of the sudden and the loss is to be bear by

the common people of living and earnings both. Thus the expenses exceeds the incomes of the

organisation and thus not able to meet its fixed expenses during the period. This all caused the

decrease in the demand of the product and so thus revenue of the organisation declined. This

directly or indirectly impacted on the businesses and which indirectly lead them to closure. The

business have earned a good amount of profit in the last 8 years and acquired a significant

market share. If the business continue its operations with new ideas so that, new market demand

and different marketing strategies that can contribute to the increase in the sales and also become

profitable. With the new market strategies the organisation can boost up their sales and also the

turn over so that the can achieve their organisational goals. The primary objective of a business

is to earn profit which has been ruined due to pandemic situation. As of the now the government

has taken back the different regulations implemented, which have caused increase in the demand

of the product. The upliftment of the regulations has shown a positive impact on the market and

the demand has also risen. Various majors are taken to boost the economy as well as the

vaccination have helped the economy to rise.

CONCLUSION

From the above mentioned report it can be concluded that business transactions are necessary to

be recorded in the business and the formation of income statement and the statement of financial

position is vital to determine how the business is performing in the market. The preparation of

journal, ledger, trial balance and the income statement is shown in the above report. The impact

of Covid-19 on the business and its profit has been worse but the trend analysis of the profit

helps the business formulate plans to get better in its working.

Net loss -49480

b) Why the profit has decreased and increased over the years and what will be the estimate of

profit/loss in 2022.

Many of the companies found it difficult to maintain their financial records smooth as

before. Because of the occurrence of the Covid in the first quarter of the year the businesses has

effected significantly and it effected each and every business (Davies, 2022). In the month of

march all the activities of the businesses got stop all of the sudden and the loss is to be bear by

the common people of living and earnings both. Thus the expenses exceeds the incomes of the

organisation and thus not able to meet its fixed expenses during the period. This all caused the

decrease in the demand of the product and so thus revenue of the organisation declined. This

directly or indirectly impacted on the businesses and which indirectly lead them to closure. The

business have earned a good amount of profit in the last 8 years and acquired a significant

market share. If the business continue its operations with new ideas so that, new market demand

and different marketing strategies that can contribute to the increase in the sales and also become

profitable. With the new market strategies the organisation can boost up their sales and also the

turn over so that the can achieve their organisational goals. The primary objective of a business

is to earn profit which has been ruined due to pandemic situation. As of the now the government

has taken back the different regulations implemented, which have caused increase in the demand

of the product. The upliftment of the regulations has shown a positive impact on the market and

the demand has also risen. Various majors are taken to boost the economy as well as the

vaccination have helped the economy to rise.

CONCLUSION

From the above mentioned report it can be concluded that business transactions are necessary to

be recorded in the business and the formation of income statement and the statement of financial

position is vital to determine how the business is performing in the market. The preparation of

journal, ledger, trial balance and the income statement is shown in the above report. The impact

of Covid-19 on the business and its profit has been worse but the trend analysis of the profit

helps the business formulate plans to get better in its working.

REFERENCES

Books and Journals

Davidson, R., 2018. Business events. Routledge.

Orthodoxou, D.L., and et.al., 2021, August. Sustainable business events: The perceptions of

service providers, attendees, and stakeholders in decision-making positions. In Journal

of Convention & Event Tourism (pp. 1-25). Routledge.

Helgeson, J. and Nierenberg, C., 2018, December. Business Disruption Associated with Extreme

Events and Pathways to Planning for more Robust Recovery. In AGU Fall Meeting

Abstracts (Vol. 2018, pp. PA43F-1398).

Bâtcă-Dumitru, C.G., 2020. Accounting for Events and Transactions Regarding

Equity. CECCAR Business Review. 1(7). pp.19-29.

White, T., 2020. Direct producer ‚Ä" consumer transactions: Community Supported Agriculture

and its offshoots. In The Handbook of Diverse Economies. Edward Elgar Publishing.

Eshghi, A. and Kargari, M., 2019. Introducing a new method for the fusion of fraud evidence in

banking transactions with regards to uncertainty. Expert Systems with Applications. 121.

pp.382-392.

Davies, P., 2022. Related Party Transactions on the London Stock Exchange: What Works and

What Does Not?. Business Law Review. 43(1).

da Silva Rodrigues, C.K., 2021. Analyzing Blockchain integrated architectures for effective

handling of IoT-ecosystem transactions. Computer Networks. 201. p.108610.

Books and Journals

Davidson, R., 2018. Business events. Routledge.

Orthodoxou, D.L., and et.al., 2021, August. Sustainable business events: The perceptions of

service providers, attendees, and stakeholders in decision-making positions. In Journal

of Convention & Event Tourism (pp. 1-25). Routledge.

Helgeson, J. and Nierenberg, C., 2018, December. Business Disruption Associated with Extreme

Events and Pathways to Planning for more Robust Recovery. In AGU Fall Meeting

Abstracts (Vol. 2018, pp. PA43F-1398).

Bâtcă-Dumitru, C.G., 2020. Accounting for Events and Transactions Regarding

Equity. CECCAR Business Review. 1(7). pp.19-29.

White, T., 2020. Direct producer ‚Ä" consumer transactions: Community Supported Agriculture

and its offshoots. In The Handbook of Diverse Economies. Edward Elgar Publishing.

Eshghi, A. and Kargari, M., 2019. Introducing a new method for the fusion of fraud evidence in

banking transactions with regards to uncertainty. Expert Systems with Applications. 121.

pp.382-392.

Davies, P., 2022. Related Party Transactions on the London Stock Exchange: What Works and

What Does Not?. Business Law Review. 43(1).

da Silva Rodrigues, C.K., 2021. Analyzing Blockchain integrated architectures for effective

handling of IoT-ecosystem transactions. Computer Networks. 201. p.108610.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.