Recording Business Transactions - portfolio 1 and 2

VerifiedAdded on 2023/06/17

|14

|1864

|223

AI Summary

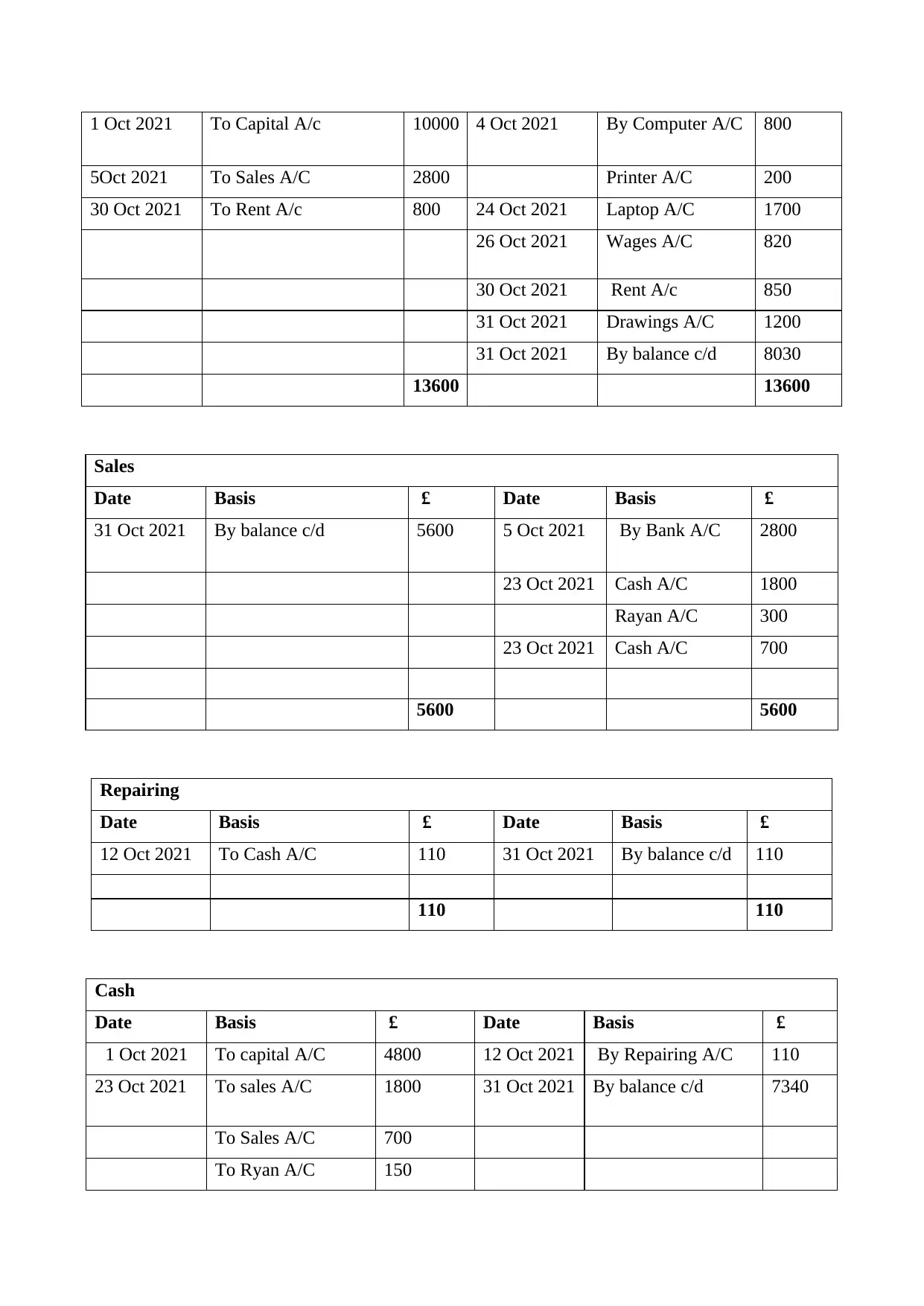

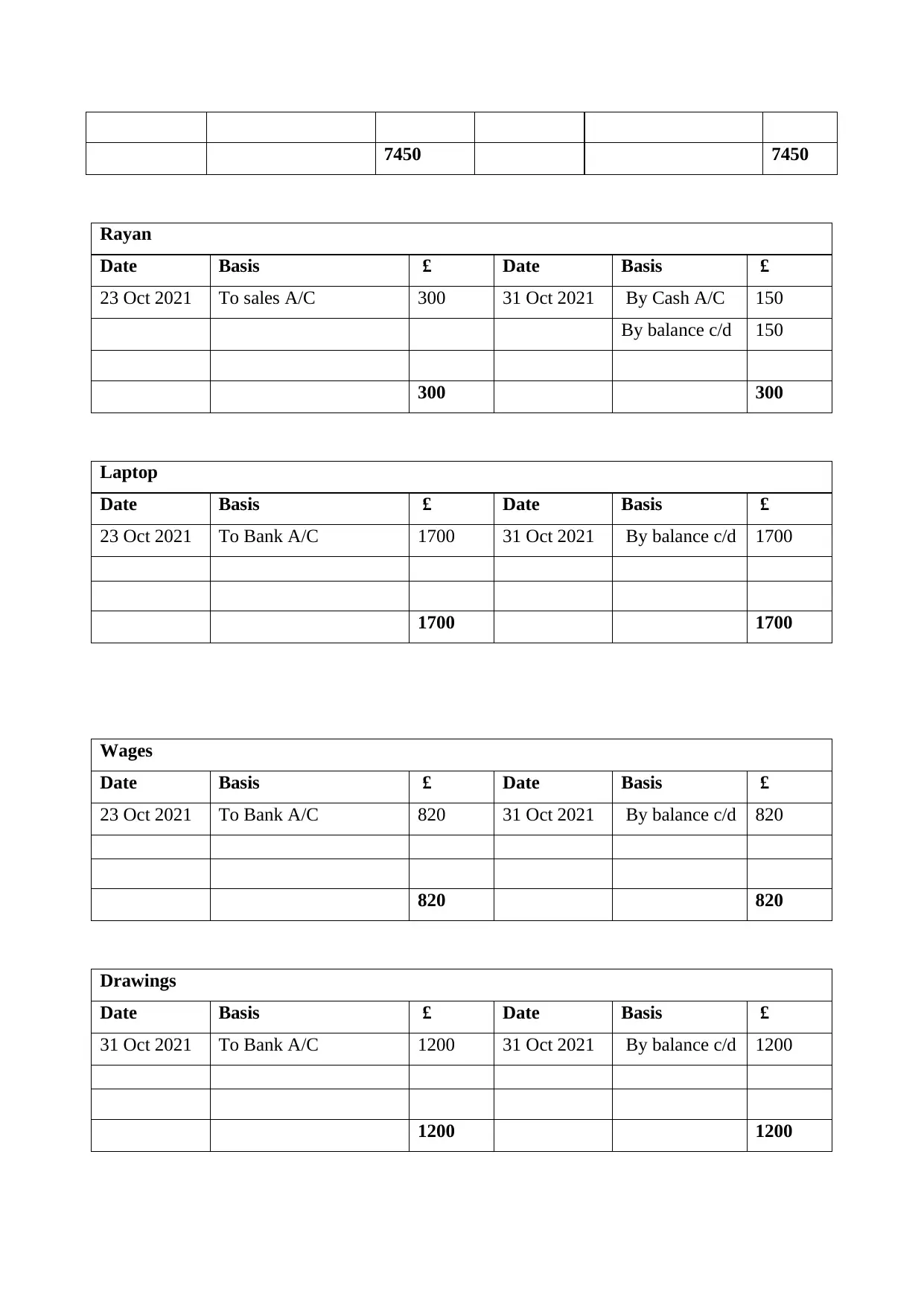

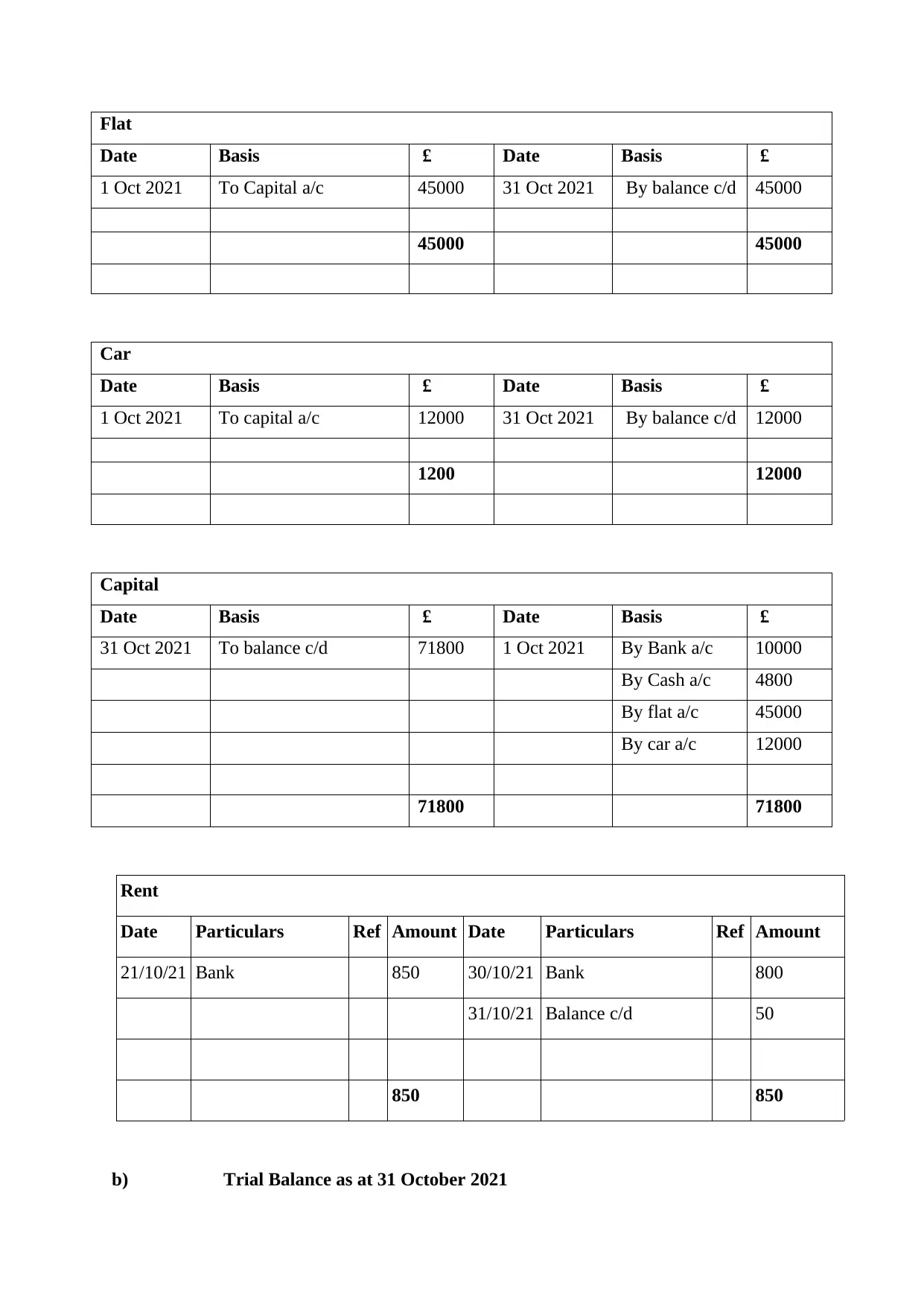

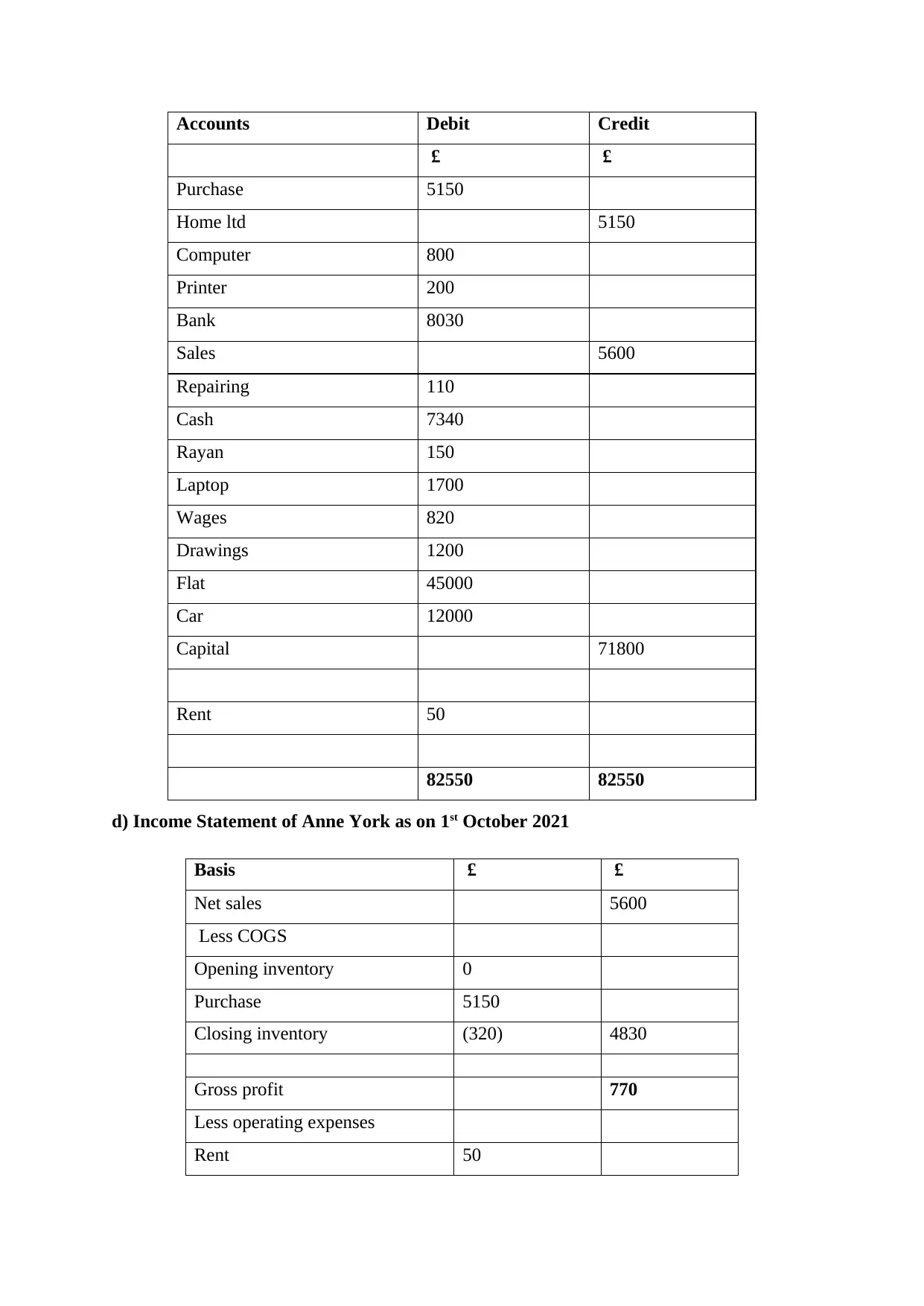

This report provides a detailed analysis of Recording Business Transactions for Anne York. It includes journal entries, ledger accounts, trial balance, income statement, balance sheet, and ratio calculation. The report also explains the concept of drawings and its impact on the business. The subject is Accounting and the course code is ACC101. The report is relevant for students pursuing Accounting courses in any college or university.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.