Recording Business Transactions: Advantages, Disadvantages, and Financial Statements

VerifiedAdded on 2022/12/29

|14

|2594

|34

AI Summary

This document discusses the recording of business transactions, including the advantages and disadvantages of accounting. It covers the decision makers of accounting information, such as internal and external users. The document also includes journal entries and the preparation of financial statements, such as income statements. Additionally, it explores the possible impact of COVID-19 on company income statement items.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

RECORDING BUSINESS

TRANSACTIONS

TRANSACTIONS

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENT

INTRODUCTION................................................................................................................3

PART 1.................................................................................................................................3

(a) Decision makers of accounting information..............................................................3

(b) Advantages and disadvantages of accounting............................................................4

PART 2.................................................................................................................................6

Journal entries..................................................................................................................6

PART 3.................................................................................................................................7

(a) Journal and Ledger of Pearce & Sons........................................................................7

(b) Trial balance as at 28 Feb 2020...............................................................................11

PART 4...............................................................................................................................11

(a) Income Statement for Airman Co. for the year ending 30th September 2020.........11

(b) Possible impact of COVID-19 on company Income statement items.....................12

CONCLUSION..................................................................................................................13

REFERENCES...................................................................................................................14

INTRODUCTION................................................................................................................3

PART 1.................................................................................................................................3

(a) Decision makers of accounting information..............................................................3

(b) Advantages and disadvantages of accounting............................................................4

PART 2.................................................................................................................................6

Journal entries..................................................................................................................6

PART 3.................................................................................................................................7

(a) Journal and Ledger of Pearce & Sons........................................................................7

(b) Trial balance as at 28 Feb 2020...............................................................................11

PART 4...............................................................................................................................11

(a) Income Statement for Airman Co. for the year ending 30th September 2020.........11

(b) Possible impact of COVID-19 on company Income statement items.....................12

CONCLUSION..................................................................................................................13

REFERENCES...................................................................................................................14

INTRODUCTION

Recording business transaction is defined as recording of all the transaction in

financial nature and then posting them in ledger to calculate profit or loss incurred during

a financial year. The project shall be highlighting the financial statements of the business

that is required by the users of the information for the purpose of decision-making

(Faccia, 2020). The internal as well as the external users of the accounting information

requires the data to ascertain profitability, growth prospects and credibility of the

company. It shall be reflecting the advantages and the disadvantages that are faced by the

accountants in recording such financial data.

Apart from that it shall include the recording of the business transactions in the

journal, posting in the ledger and the closing balances are then accumulated in the trial

balance. The project report shall be demonstrating the income statement of the company

and representing the profitability position of the company by incorporating all the

expenses and incomes of the business. Lastly it shall be showing the impacts of the

pandemic on the business and the simultaneous effect on its profitability.

PART 1

(a) Decision makers of accounting information

Internal and External users are the decision makers of the financial statement.

Internal users are the person who are inside the organisation while external are outside the

organisations

Internal users:

Owners- owners need financial information for making decisions on what to do

with their investment i.e. buy, hold, or sale the securities. The Sainsbury

company’s shareholders invest in the company by seeing continue growth and

profitability of the firm. Higher the profit higher the dividend paid to them.

MANAGEMENT- in small businesses sometimes there are management may

include owners. The management of the company is the first and foremost user of

the financial statements, they are the ones who prepared the financial statements.

Board and the management need to refer to them while considering the progress

and growth of the company.

Recording business transaction is defined as recording of all the transaction in

financial nature and then posting them in ledger to calculate profit or loss incurred during

a financial year. The project shall be highlighting the financial statements of the business

that is required by the users of the information for the purpose of decision-making

(Faccia, 2020). The internal as well as the external users of the accounting information

requires the data to ascertain profitability, growth prospects and credibility of the

company. It shall be reflecting the advantages and the disadvantages that are faced by the

accountants in recording such financial data.

Apart from that it shall include the recording of the business transactions in the

journal, posting in the ledger and the closing balances are then accumulated in the trial

balance. The project report shall be demonstrating the income statement of the company

and representing the profitability position of the company by incorporating all the

expenses and incomes of the business. Lastly it shall be showing the impacts of the

pandemic on the business and the simultaneous effect on its profitability.

PART 1

(a) Decision makers of accounting information

Internal and External users are the decision makers of the financial statement.

Internal users are the person who are inside the organisation while external are outside the

organisations

Internal users:

Owners- owners need financial information for making decisions on what to do

with their investment i.e. buy, hold, or sale the securities. The Sainsbury

company’s shareholders invest in the company by seeing continue growth and

profitability of the firm. Higher the profit higher the dividend paid to them.

MANAGEMENT- in small businesses sometimes there are management may

include owners. The management of the company is the first and foremost user of

the financial statements, they are the ones who prepared the financial statements.

Board and the management need to refer to them while considering the progress

and growth of the company.

EMPLOYEES- from financial statements employees need to know about the

status of bonus and increments if company earn more profit it gives more bonus to

the employees.

INVESTORS- investors are the owner of the business; Sainsbury's investors want

to know about the financial performance of the company so they make decisions

on the basis of financial statements

External Users:

CUSTOMERS- customers of the Salisbury's need to read the financial statements

of the company through which they are procuring goods or services and also

financially strong company can provide its customers with credit sales or sale

goods at discount to its long-term customers.

COMPETITORS- this are the person who would like to maintain the competitive

advantages On their competitors. Sainsbury's competitors are Tesco, Aldi UK,

Morrisons etc. The company changes their strategy by looking financial

statements of competitors for future growth.

GOVERNMENT- government agencies like the income tax department and the

sales department would like to know about the company's financial statements to

keep a check if the company is paying appropriate taxes on time or not. So

Government uses financial statement of the companies for finding out net profit

before tax.

(b) Advantages and disadvantages of accounting

Advantages:

Maintain Business Records: accounting helps in maintain business transactions

which are recorded at one place in chronological record so easy to find (Warren,

Jonick, and Schneider, 2020). while recording the transaction in the journal each

debit aspects needs a credit aspect, this will assist to easily find out financially

affected transactions.

Helps to Find out Financial Position: proper accounting records helps to find

out the profit and loss for the year end which shows financial performance of the

firms. balance sheets as on date shows financial position of the firms

status of bonus and increments if company earn more profit it gives more bonus to

the employees.

INVESTORS- investors are the owner of the business; Sainsbury's investors want

to know about the financial performance of the company so they make decisions

on the basis of financial statements

External Users:

CUSTOMERS- customers of the Salisbury's need to read the financial statements

of the company through which they are procuring goods or services and also

financially strong company can provide its customers with credit sales or sale

goods at discount to its long-term customers.

COMPETITORS- this are the person who would like to maintain the competitive

advantages On their competitors. Sainsbury's competitors are Tesco, Aldi UK,

Morrisons etc. The company changes their strategy by looking financial

statements of competitors for future growth.

GOVERNMENT- government agencies like the income tax department and the

sales department would like to know about the company's financial statements to

keep a check if the company is paying appropriate taxes on time or not. So

Government uses financial statement of the companies for finding out net profit

before tax.

(b) Advantages and disadvantages of accounting

Advantages:

Maintain Business Records: accounting helps in maintain business transactions

which are recorded at one place in chronological record so easy to find (Warren,

Jonick, and Schneider, 2020). while recording the transaction in the journal each

debit aspects needs a credit aspect, this will assist to easily find out financially

affected transactions.

Helps to Find out Financial Position: proper accounting records helps to find

out the profit and loss for the year end which shows financial performance of the

firms. balance sheets as on date shows financial position of the firms

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Recording acts as a backup at the time of Audit: good recording of the

transactions helps the tax auditors to easily make decisions. At the time of

auditing actual recording of income and expenses required, so without right

records, industries standards used as a guidance

Disadvantages:

Inconvenience: for recording financial transactions the complete knowledge of

accounting is required. sometimes the transactions may have more than two

effects so it is necessary to record all the effects so the recording is proper taken

place.

Time Consuming: Recording every business transaction may take time because

they need debit and credit both aspects at a same time. If any error occurs, then

accountant has to done the entries again.

Accuracy: Sometimes a bookkeeper can make a typing mistakes that can affect

the accuracy of the financial records and that mistakes are only found when the

financial reconciliation process will have done (Berry, 2018.). So it is the great

disadvantage of the recording transaction.

Advantages of sole proprietary business: Recording of transaction is simple and

affordable for sole proprietorship. It helps the owner in simplifying the tax regimes. Only

one person can record all accounting records so, it is beneficial for maintaining

confidentiality. This firm does not need to publish its accounts on public domain.

Disadvantages of sole Proprietary: In this type of firms there is unlimited liability and

lack of financial control so it is the main disadvantage of sole firms. In the case of sole

proprietary form of business does not have a report on financial statements so the

proprietor may not properly know where the business funds are going.

Advantages of partnership Business: If there is more than one partner than its helps in

specialization of two or more than multiple skills. If more Than one person introduced

capital, then it helps in expansion and growth

Disadvantages of Partnership Firms: in partnership there is loss of autonomy and lack

of stability.

transactions helps the tax auditors to easily make decisions. At the time of

auditing actual recording of income and expenses required, so without right

records, industries standards used as a guidance

Disadvantages:

Inconvenience: for recording financial transactions the complete knowledge of

accounting is required. sometimes the transactions may have more than two

effects so it is necessary to record all the effects so the recording is proper taken

place.

Time Consuming: Recording every business transaction may take time because

they need debit and credit both aspects at a same time. If any error occurs, then

accountant has to done the entries again.

Accuracy: Sometimes a bookkeeper can make a typing mistakes that can affect

the accuracy of the financial records and that mistakes are only found when the

financial reconciliation process will have done (Berry, 2018.). So it is the great

disadvantage of the recording transaction.

Advantages of sole proprietary business: Recording of transaction is simple and

affordable for sole proprietorship. It helps the owner in simplifying the tax regimes. Only

one person can record all accounting records so, it is beneficial for maintaining

confidentiality. This firm does not need to publish its accounts on public domain.

Disadvantages of sole Proprietary: In this type of firms there is unlimited liability and

lack of financial control so it is the main disadvantage of sole firms. In the case of sole

proprietary form of business does not have a report on financial statements so the

proprietor may not properly know where the business funds are going.

Advantages of partnership Business: If there is more than one partner than its helps in

specialization of two or more than multiple skills. If more Than one person introduced

capital, then it helps in expansion and growth

Disadvantages of Partnership Firms: in partnership there is loss of autonomy and lack

of stability.

PART 2

Journal entries

Date Particular Debit( £) Credit( £)

01/02/20 Cash A/c Dr

To Office Fixture A/c

( Being office furniture returned to Asma Ltd)

350

350

04/02/20 Bad debts A/c Dr

To S. Keys A/c

(Being bad debts written off)

85

85

09/02/20 Machinery A/c Dr

To Bank A/c

To TS Co.

(Being machine purchase and 200 paid in cheque

and left on credit )

2300

200

2100

13/02/02 Cash A/c Dr

Bad Debts A/c Dr

To S. Hill A/c

(Being S hills full and final settlement done)

220

50

270

13/02/20 Profit and loss A/c Dr

To Bad Debts A/c

(Being Bad debts transferred in profit and loss

account)

50

50

20/02/20 Drawing A/c Dr

To Inventory A/c

(Being Owner takes goods for his personal use)

180

180

26/02/20 Drawing A/c Dr

Insurance(Cash) A/c

(Being Private insurance is treated as Business

85

85

Journal entries

Date Particular Debit( £) Credit( £)

01/02/20 Cash A/c Dr

To Office Fixture A/c

( Being office furniture returned to Asma Ltd)

350

350

04/02/20 Bad debts A/c Dr

To S. Keys A/c

(Being bad debts written off)

85

85

09/02/20 Machinery A/c Dr

To Bank A/c

To TS Co.

(Being machine purchase and 200 paid in cheque

and left on credit )

2300

200

2100

13/02/02 Cash A/c Dr

Bad Debts A/c Dr

To S. Hill A/c

(Being S hills full and final settlement done)

220

50

270

13/02/20 Profit and loss A/c Dr

To Bad Debts A/c

(Being Bad debts transferred in profit and loss

account)

50

50

20/02/20 Drawing A/c Dr

To Inventory A/c

(Being Owner takes goods for his personal use)

180

180

26/02/20 Drawing A/c Dr

Insurance(Cash) A/c

(Being Private insurance is treated as Business

85

85

expenses )

28/02/20 TS Co. A/c Dr

To Bank A/c

1100

1100

PART 3

(a) Journal and Ledger of Pearce & Sons

Date Particular Debit(£) Credit(£)

01/02/20 Bank A/c Dr

Van A/c Dr

Office Fixtures A/c Dr

To Capital A/c

21500

25000

800

47300

02/02/20 Bank A/c Dr

To Loan A/c (Received from Lloyds Bank)

(Being loan taken from Lloyds Bank )

2500

2500

03/02/20 Cash in Hand A/c Dr

To Bank A/c

(Being bank Account transferred in cash in hand

Account )

1500

1500

04/02/20 Van A/c Dr

To Bank A/c

(Being Van Purchased through Cheque)

4800

4800

05/02/20 Office Fixture A/c Dr

To Quick Office Ltd A/c

(Being office furniture Purchased on credit)

1100

1100

08/02/20 Van A/c Dr

To Nissan Co. A/c

(Being Van purchased on credit from Nissan

company)

5200

5200

28/02/20 TS Co. A/c Dr

To Bank A/c

1100

1100

PART 3

(a) Journal and Ledger of Pearce & Sons

Date Particular Debit(£) Credit(£)

01/02/20 Bank A/c Dr

Van A/c Dr

Office Fixtures A/c Dr

To Capital A/c

21500

25000

800

47300

02/02/20 Bank A/c Dr

To Loan A/c (Received from Lloyds Bank)

(Being loan taken from Lloyds Bank )

2500

2500

03/02/20 Cash in Hand A/c Dr

To Bank A/c

(Being bank Account transferred in cash in hand

Account )

1500

1500

04/02/20 Van A/c Dr

To Bank A/c

(Being Van Purchased through Cheque)

4800

4800

05/02/20 Office Fixture A/c Dr

To Quick Office Ltd A/c

(Being office furniture Purchased on credit)

1100

1100

08/02/20 Van A/c Dr

To Nissan Co. A/c

(Being Van purchased on credit from Nissan

company)

5200

5200

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

15/02/20 Office Fixture A/c Dr

To Cash A/c

(Being Fixture purchase on cash)

70

70

19/02/20 Nissan Co. A/c Dr

To Bank A/c

(Being paid amount to Nissan co. through

cheque )

5200

5200

25/02/20 Bank A/c Dr

To Cash in Hand A/c

(Being cash in hand transfer to bank A/c)

350

350

28/02/20 Office Fixture A/c Dr

To Bank A/c

(being office fixture purchase and paid in cheque)

620

620

Ledger Accounts:

Bank A/c

Date particular Amount Date Particular Amount

01/02/20 To Capital a/c 21500 03/02/20 By cash in hand A/c 1500

02/02/20 To Loan A/c 2500 04/02/20 By van a/c 4800

25/02/20 To cash in hand a/c 350 19/02/20 By Nissan Co. A/c 5200

28/02/20 By Office fixture A/c 620

01/03/20 by Balance C/d 12230

24350 24350

01/03/20 To balance B/d 12230

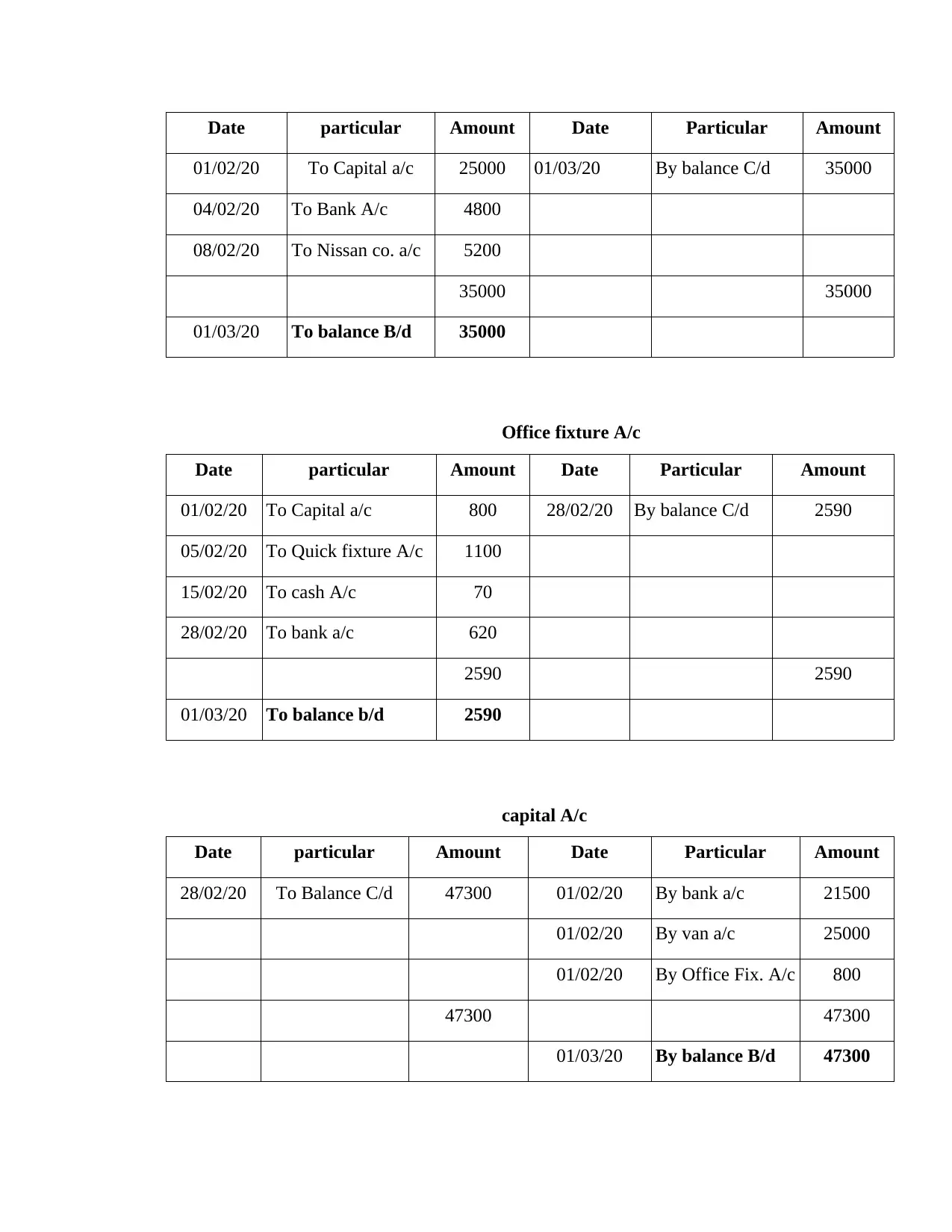

Van A/c

To Cash A/c

(Being Fixture purchase on cash)

70

70

19/02/20 Nissan Co. A/c Dr

To Bank A/c

(Being paid amount to Nissan co. through

cheque )

5200

5200

25/02/20 Bank A/c Dr

To Cash in Hand A/c

(Being cash in hand transfer to bank A/c)

350

350

28/02/20 Office Fixture A/c Dr

To Bank A/c

(being office fixture purchase and paid in cheque)

620

620

Ledger Accounts:

Bank A/c

Date particular Amount Date Particular Amount

01/02/20 To Capital a/c 21500 03/02/20 By cash in hand A/c 1500

02/02/20 To Loan A/c 2500 04/02/20 By van a/c 4800

25/02/20 To cash in hand a/c 350 19/02/20 By Nissan Co. A/c 5200

28/02/20 By Office fixture A/c 620

01/03/20 by Balance C/d 12230

24350 24350

01/03/20 To balance B/d 12230

Van A/c

Date particular Amount Date Particular Amount

01/02/20 To Capital a/c 25000 01/03/20 By balance C/d 35000

04/02/20 To Bank A/c 4800

08/02/20 To Nissan co. a/c 5200

35000 35000

01/03/20 To balance B/d 35000

Office fixture A/c

Date particular Amount Date Particular Amount

01/02/20 To Capital a/c 800 28/02/20 By balance C/d 2590

05/02/20 To Quick fixture A/c 1100

15/02/20 To cash A/c 70

28/02/20 To bank a/c 620

2590 2590

01/03/20 To balance b/d 2590

capital A/c

Date particular Amount Date Particular Amount

28/02/20 To Balance C/d 47300 01/02/20 By bank a/c 21500

01/02/20 By van a/c 25000

01/02/20 By Office Fix. A/c 800

47300 47300

01/03/20 By balance B/d 47300

01/02/20 To Capital a/c 25000 01/03/20 By balance C/d 35000

04/02/20 To Bank A/c 4800

08/02/20 To Nissan co. a/c 5200

35000 35000

01/03/20 To balance B/d 35000

Office fixture A/c

Date particular Amount Date Particular Amount

01/02/20 To Capital a/c 800 28/02/20 By balance C/d 2590

05/02/20 To Quick fixture A/c 1100

15/02/20 To cash A/c 70

28/02/20 To bank a/c 620

2590 2590

01/03/20 To balance b/d 2590

capital A/c

Date particular Amount Date Particular Amount

28/02/20 To Balance C/d 47300 01/02/20 By bank a/c 21500

01/02/20 By van a/c 25000

01/02/20 By Office Fix. A/c 800

47300 47300

01/03/20 By balance B/d 47300

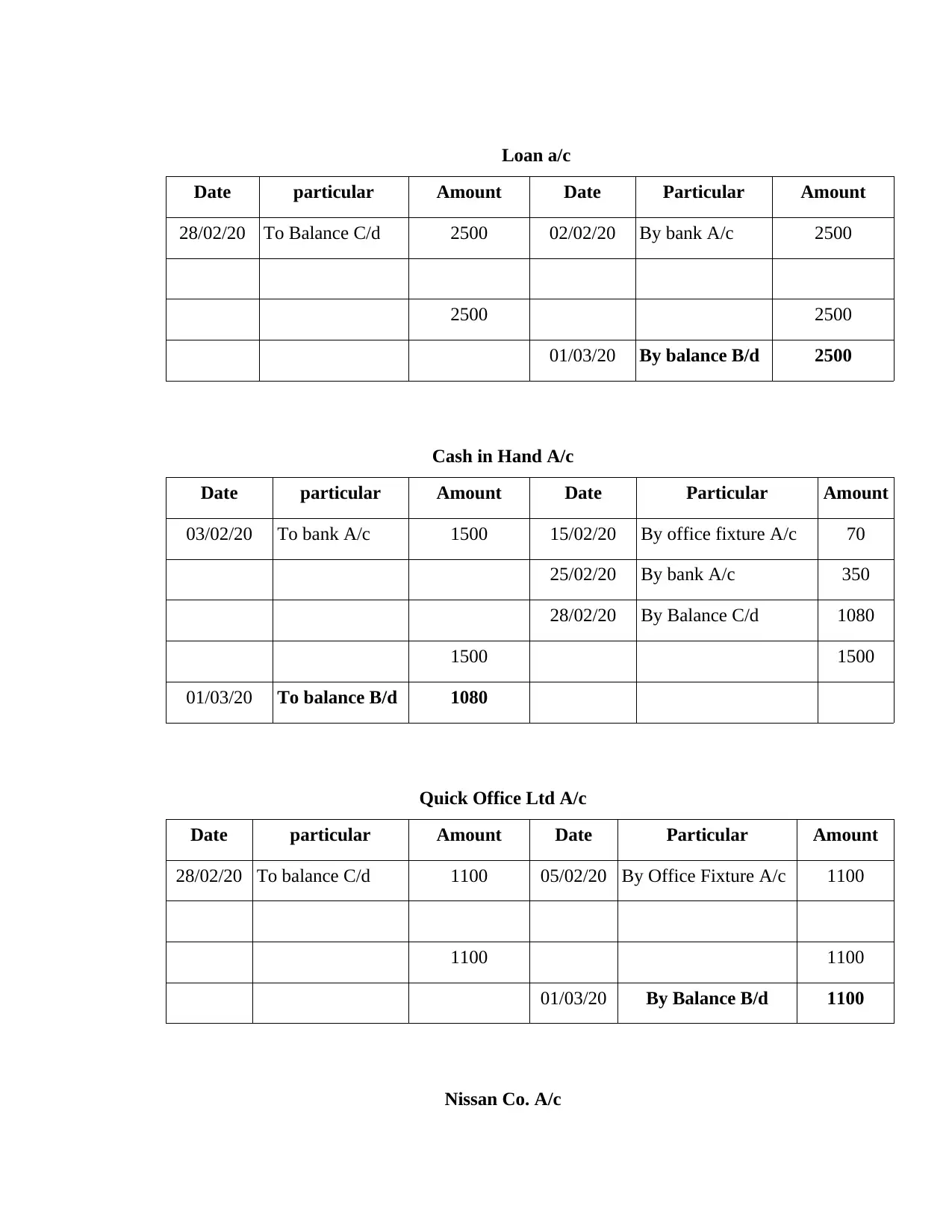

Loan a/c

Date particular Amount Date Particular Amount

28/02/20 To Balance C/d 2500 02/02/20 By bank A/c 2500

2500 2500

01/03/20 By balance B/d 2500

Cash in Hand A/c

Date particular Amount Date Particular Amount

03/02/20 To bank A/c 1500 15/02/20 By office fixture A/c 70

25/02/20 By bank A/c 350

28/02/20 By Balance C/d 1080

1500 1500

01/03/20 To balance B/d 1080

Quick Office Ltd A/c

Date particular Amount Date Particular Amount

28/02/20 To balance C/d 1100 05/02/20 By Office Fixture A/c 1100

1100 1100

01/03/20 By Balance B/d 1100

Nissan Co. A/c

Date particular Amount Date Particular Amount

28/02/20 To Balance C/d 2500 02/02/20 By bank A/c 2500

2500 2500

01/03/20 By balance B/d 2500

Cash in Hand A/c

Date particular Amount Date Particular Amount

03/02/20 To bank A/c 1500 15/02/20 By office fixture A/c 70

25/02/20 By bank A/c 350

28/02/20 By Balance C/d 1080

1500 1500

01/03/20 To balance B/d 1080

Quick Office Ltd A/c

Date particular Amount Date Particular Amount

28/02/20 To balance C/d 1100 05/02/20 By Office Fixture A/c 1100

1100 1100

01/03/20 By Balance B/d 1100

Nissan Co. A/c

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

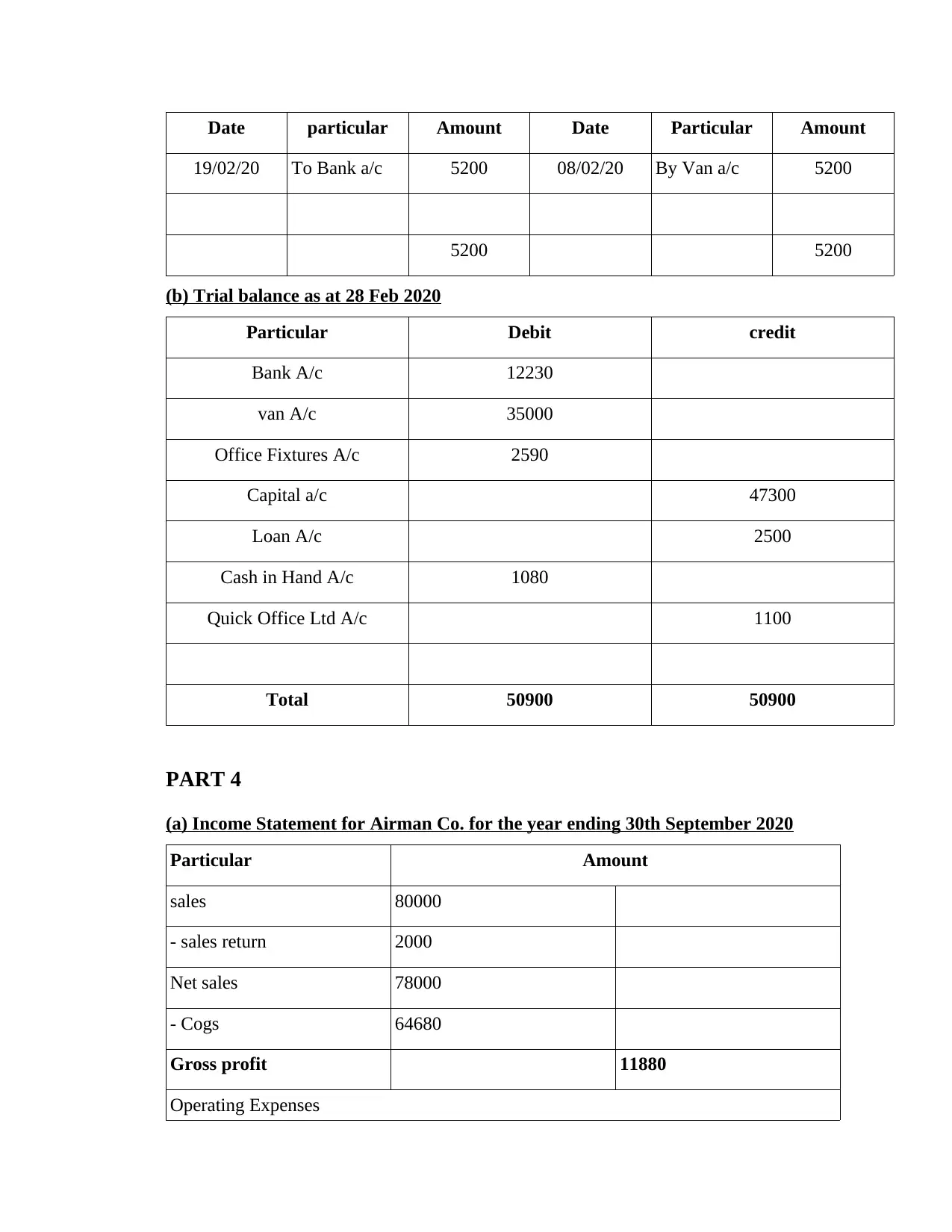

Date particular Amount Date Particular Amount

19/02/20 To Bank a/c 5200 08/02/20 By Van a/c 5200

5200 5200

(b) Trial balance as at 28 Feb 2020

Particular Debit credit

Bank A/c 12230

van A/c 35000

Office Fixtures A/c 2590

Capital a/c 47300

Loan A/c 2500

Cash in Hand A/c 1080

Quick Office Ltd A/c 1100

Total 50900 50900

PART 4

(a) Income Statement for Airman Co. for the year ending 30th September 2020

Particular Amount

sales 80000

- sales return 2000

Net sales 78000

- Cogs 64680

Gross profit 11880

Operating Expenses

19/02/20 To Bank a/c 5200 08/02/20 By Van a/c 5200

5200 5200

(b) Trial balance as at 28 Feb 2020

Particular Debit credit

Bank A/c 12230

van A/c 35000

Office Fixtures A/c 2590

Capital a/c 47300

Loan A/c 2500

Cash in Hand A/c 1080

Quick Office Ltd A/c 1100

Total 50900 50900

PART 4

(a) Income Statement for Airman Co. for the year ending 30th September 2020

Particular Amount

sales 80000

- sales return 2000

Net sales 78000

- Cogs 64680

Gross profit 11880

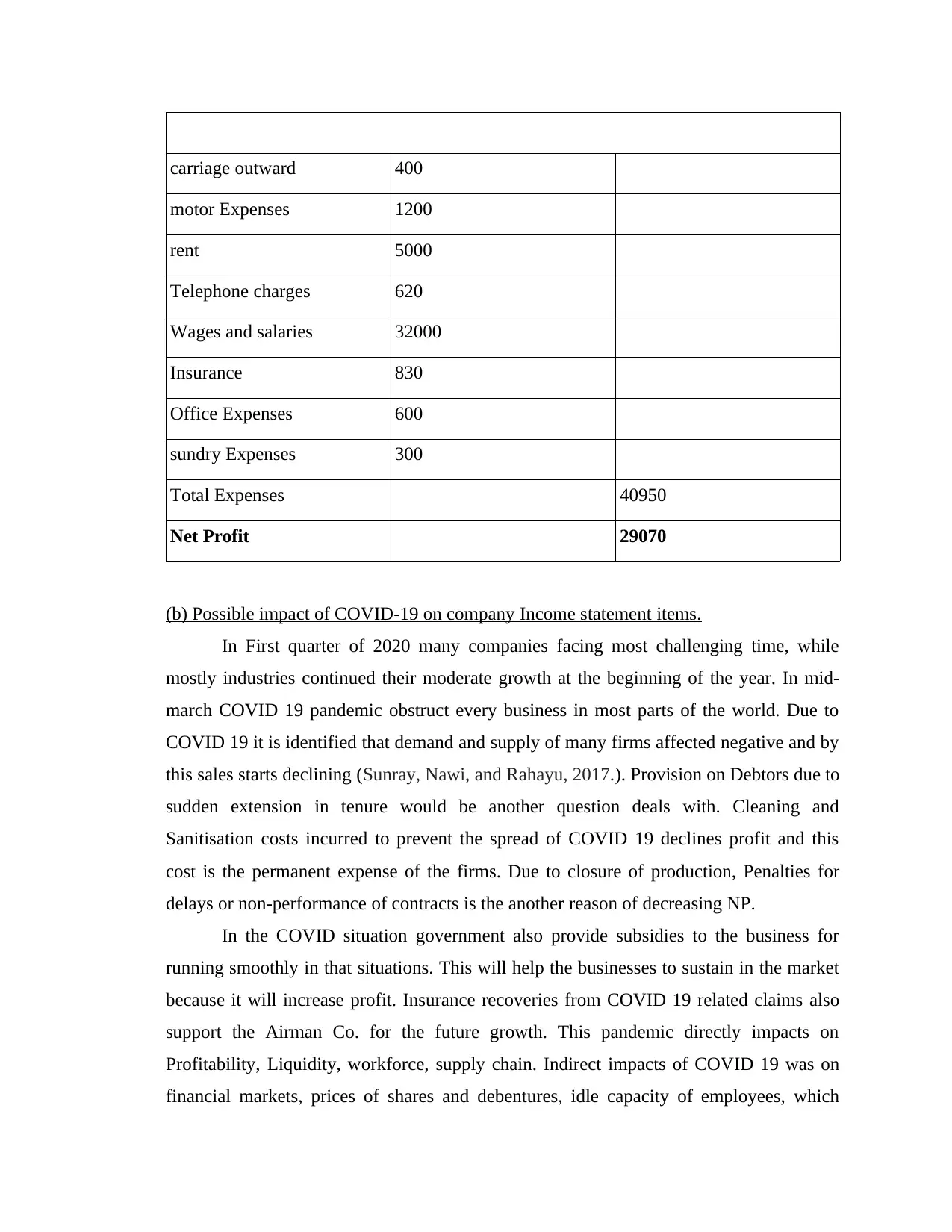

Operating Expenses

carriage outward 400

motor Expenses 1200

rent 5000

Telephone charges 620

Wages and salaries 32000

Insurance 830

Office Expenses 600

sundry Expenses 300

Total Expenses 40950

Net Profit 29070

(b) Possible impact of COVID-19 on company Income statement items.

In First quarter of 2020 many companies facing most challenging time, while

mostly industries continued their moderate growth at the beginning of the year. In mid-

march COVID 19 pandemic obstruct every business in most parts of the world. Due to

COVID 19 it is identified that demand and supply of many firms affected negative and by

this sales starts declining (Sunray, Nawi, and Rahayu, 2017.). Provision on Debtors due to

sudden extension in tenure would be another question deals with. Cleaning and

Sanitisation costs incurred to prevent the spread of COVID 19 declines profit and this

cost is the permanent expense of the firms. Due to closure of production, Penalties for

delays or non-performance of contracts is the another reason of decreasing NP.

In the COVID situation government also provide subsidies to the business for

running smoothly in that situations. This will help the businesses to sustain in the market

because it will increase profit. Insurance recoveries from COVID 19 related claims also

support the Airman Co. for the future growth. This pandemic directly impacts on

Profitability, Liquidity, workforce, supply chain. Indirect impacts of COVID 19 was on

financial markets, prices of shares and debentures, idle capacity of employees, which

motor Expenses 1200

rent 5000

Telephone charges 620

Wages and salaries 32000

Insurance 830

Office Expenses 600

sundry Expenses 300

Total Expenses 40950

Net Profit 29070

(b) Possible impact of COVID-19 on company Income statement items.

In First quarter of 2020 many companies facing most challenging time, while

mostly industries continued their moderate growth at the beginning of the year. In mid-

march COVID 19 pandemic obstruct every business in most parts of the world. Due to

COVID 19 it is identified that demand and supply of many firms affected negative and by

this sales starts declining (Sunray, Nawi, and Rahayu, 2017.). Provision on Debtors due to

sudden extension in tenure would be another question deals with. Cleaning and

Sanitisation costs incurred to prevent the spread of COVID 19 declines profit and this

cost is the permanent expense of the firms. Due to closure of production, Penalties for

delays or non-performance of contracts is the another reason of decreasing NP.

In the COVID situation government also provide subsidies to the business for

running smoothly in that situations. This will help the businesses to sustain in the market

because it will increase profit. Insurance recoveries from COVID 19 related claims also

support the Airman Co. for the future growth. This pandemic directly impacts on

Profitability, Liquidity, workforce, supply chain. Indirect impacts of COVID 19 was on

financial markets, prices of shares and debentures, idle capacity of employees, which

reduces the profit of the organisations. Estimating future cash flows could also be

challenging for Airman Co. due to Increases in economic uncertainty.

Hygiene is the another reason for change after the COVID pandemic customers

wants to use hygienic products and it incurred higher cost of production. After this

pandemic Airman Co. starts selling goods in Online market which escalate the cost of

technological advancement.

Rent, wages and other expenditure incurred during temporary closures which declines the

profit of Airman Company. COVID Impact on every part of the society which may

include either social, economic or geographical areas would take its own time and cost to

turn back to normal.

CONCLUSION

It can be summarized from the above project that financial statements prove to be

very essential for the business and the users of its information. It assists in the decision-

making process and shall evaluate the position of the company in respect of the

profitability and the future growth opportunities. There are certain advantages like it helps

in knowing the results and improve the inefficiencies whereas the disadvantages like time

consuming and less accurate. Also the business has been highly impacted in terms of the

profitability because of the outbreak of the covid-19.

challenging for Airman Co. due to Increases in economic uncertainty.

Hygiene is the another reason for change after the COVID pandemic customers

wants to use hygienic products and it incurred higher cost of production. After this

pandemic Airman Co. starts selling goods in Online market which escalate the cost of

technological advancement.

Rent, wages and other expenditure incurred during temporary closures which declines the

profit of Airman Company. COVID Impact on every part of the society which may

include either social, economic or geographical areas would take its own time and cost to

turn back to normal.

CONCLUSION

It can be summarized from the above project that financial statements prove to be

very essential for the business and the users of its information. It assists in the decision-

making process and shall evaluate the position of the company in respect of the

profitability and the future growth opportunities. There are certain advantages like it helps

in knowing the results and improve the inefficiencies whereas the disadvantages like time

consuming and less accurate. Also the business has been highly impacted in terms of the

profitability because of the outbreak of the covid-19.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Berry, L.E., 2018. Financial accounting demystified. McGraw-Hill,.

Faccia, A., 2020. X-Accounting®-Towards a new Accounting System. Blockchain

applied accounting. How robots will overcome humans in accounting Recording.

Fischer-Pauzenberger, C. and Schwaiger, W.S., 2017. The OntoREA Accounting Model:

Ontology-based Modeling of the Accounting Domain. CSIMQ, 11. pp.20-37.

Sunarya, P. A., Nawi, M. N. M. and Rahayu, S., 2017. Analyze and Record a series of

Purchase Transactions on Companies using Online Accounting Software. Aptisi

Transactions On Management, 1(1). pp.38-43.

Warren, C .S., Jonick, C. and Schneider, J., 2020. Accounting. Cengage Learning.

Webster, W., 2020. Accounting for managers.

Weygandt, J. J., Kimmel, P. D. and Kieso, D. E ., 2019. Financial accounting. John

Wiley & Sons.

Yu, T., Lin, Z. and Tang, Q., 2018. Blockchain: The introduction and its application in

financial accounting. Journal of Corporate Accounting & Finance, 29(4). pp.37-

47.

Books and Journals

Berry, L.E., 2018. Financial accounting demystified. McGraw-Hill,.

Faccia, A., 2020. X-Accounting®-Towards a new Accounting System. Blockchain

applied accounting. How robots will overcome humans in accounting Recording.

Fischer-Pauzenberger, C. and Schwaiger, W.S., 2017. The OntoREA Accounting Model:

Ontology-based Modeling of the Accounting Domain. CSIMQ, 11. pp.20-37.

Sunarya, P. A., Nawi, M. N. M. and Rahayu, S., 2017. Analyze and Record a series of

Purchase Transactions on Companies using Online Accounting Software. Aptisi

Transactions On Management, 1(1). pp.38-43.

Warren, C .S., Jonick, C. and Schneider, J., 2020. Accounting. Cengage Learning.

Webster, W., 2020. Accounting for managers.

Weygandt, J. J., Kimmel, P. D. and Kieso, D. E ., 2019. Financial accounting. John

Wiley & Sons.

Yu, T., Lin, Z. and Tang, Q., 2018. Blockchain: The introduction and its application in

financial accounting. Journal of Corporate Accounting & Finance, 29(4). pp.37-

47.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.