Accounting of Business Transactions (Cai 2019)

VerifiedAdded on 2021/10/06

|21

|3846

|295

AI Summary

Recording Business Transactions Contents Introduction 3 Assessment 1 3 Part 1 3 Part 2 5 Part 3 6 Part 4 10 ASSESSEMENT 2 12 PART A 12 PART B 20 CONCLUSION 23 References 24 Introduction Accounting includes monitoring, categorizing, updating and outlining the cash transactions of the person (Cai, 2019). These documents and the reports derived from them provide the basis for the analysis of the financial statements and the position of the company. Decision-makers and need for accounting information Financial accounting includes the summaries and

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Recording Business Transactions

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Contents

Introduction.................................................................................................................................................3

Assessment 1...............................................................................................................................................3

Part 1.......................................................................................................................................................3

Part 2.......................................................................................................................................................5

Part 3.......................................................................................................................................................6

Part 4.....................................................................................................................................................10

ASSESSEMENT 2................................................................................................................................12

PART A.................................................................................................................................................12

PART B.................................................................................................................................................20

CONCLUSION.............................................................................................................................................23

References.................................................................................................................................................24

Introduction.................................................................................................................................................3

Assessment 1...............................................................................................................................................3

Part 1.......................................................................................................................................................3

Part 2.......................................................................................................................................................5

Part 3.......................................................................................................................................................6

Part 4.....................................................................................................................................................10

ASSESSEMENT 2................................................................................................................................12

PART A.................................................................................................................................................12

PART B.................................................................................................................................................20

CONCLUSION.............................................................................................................................................23

References.................................................................................................................................................24

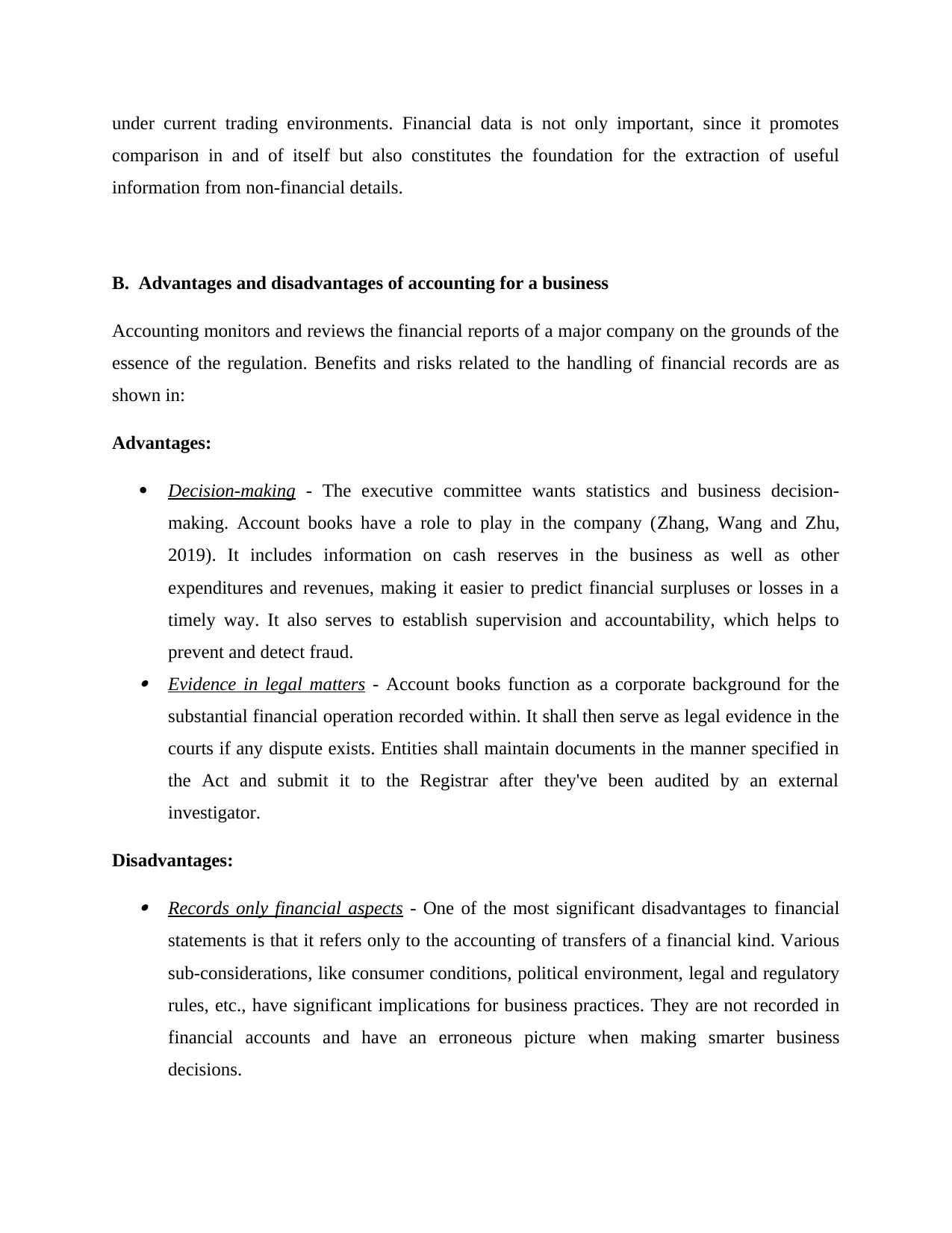

Introduction

Accounting includes monitoring, categorizing, updating and outlining the cash transactions of

the person (Cai, 2019). These documents and the reports derived from them provide the basis for

the analysis of the financial statements and the position of the company. This review concerns

the processing of financial records by the different agencies and the production of trial reports

and income statements. Costs and drawbacks in the taxation of manufacturing firms are

discussed. The impact of Covid-19 on business profits is also addressed.

Assessment 1

Part 1

A. Decision-makers and need for accounting information

Financial accounting includes the summaries and analysis of all numerical facts in such a manner

that it can be reported in the report. These findings are very helpful for smart decision. Effective

judgments from purchase to customer service decide the future of the company (Viriyasitavat

and Hoonsopon, 2019). Both decisions about the induction and dismissal of workers, the

establishment of the profit goal, the planning of news events and budgets, the use of technology

for various manufacturing operations, etc. are taken by the corporation's multiple executives. The

decision-making authority of a company is based on its control processes, governed by the

Executive Committee or the Board members. For example, the Uber Executive board, headed by

its CEO, Dara Khosrowshahi, is responsible for all the strategic vision of the business. Firm

keeps a corporate structure that takes its decisions on behalf of the ideals, mission, beliefs and

goals of the organization. These activities are then delegated to the departmental supervisors,

along with the authority required for implementing them forward.

Financial accounts have the applicable company information in objective terms, making it easy

for management and investors to make rational decisions. Accounting statements shall be drawn

up in line with general systems and policies which are consistent across the industry (Hamilton,

2020). This makes them similar to several other competitors who know their business status

through business metrics. Financial accounts also provide a basis for administrators to take

decisions on investment proposals or whether or not they will be viable and economically

sustainable. Predictions and assumptions also rely on corporate accounting information improved

Accounting includes monitoring, categorizing, updating and outlining the cash transactions of

the person (Cai, 2019). These documents and the reports derived from them provide the basis for

the analysis of the financial statements and the position of the company. This review concerns

the processing of financial records by the different agencies and the production of trial reports

and income statements. Costs and drawbacks in the taxation of manufacturing firms are

discussed. The impact of Covid-19 on business profits is also addressed.

Assessment 1

Part 1

A. Decision-makers and need for accounting information

Financial accounting includes the summaries and analysis of all numerical facts in such a manner

that it can be reported in the report. These findings are very helpful for smart decision. Effective

judgments from purchase to customer service decide the future of the company (Viriyasitavat

and Hoonsopon, 2019). Both decisions about the induction and dismissal of workers, the

establishment of the profit goal, the planning of news events and budgets, the use of technology

for various manufacturing operations, etc. are taken by the corporation's multiple executives. The

decision-making authority of a company is based on its control processes, governed by the

Executive Committee or the Board members. For example, the Uber Executive board, headed by

its CEO, Dara Khosrowshahi, is responsible for all the strategic vision of the business. Firm

keeps a corporate structure that takes its decisions on behalf of the ideals, mission, beliefs and

goals of the organization. These activities are then delegated to the departmental supervisors,

along with the authority required for implementing them forward.

Financial accounts have the applicable company information in objective terms, making it easy

for management and investors to make rational decisions. Accounting statements shall be drawn

up in line with general systems and policies which are consistent across the industry (Hamilton,

2020). This makes them similar to several other competitors who know their business status

through business metrics. Financial accounts also provide a basis for administrators to take

decisions on investment proposals or whether or not they will be viable and economically

sustainable. Predictions and assumptions also rely on corporate accounting information improved

under current trading environments. Financial data is not only important, since it promotes

comparison in and of itself but also constitutes the foundation for the extraction of useful

information from non-financial details.

B. Advantages and disadvantages of accounting for a business

Accounting monitors and reviews the financial reports of a major company on the grounds of the

essence of the regulation. Benefits and risks related to the handling of financial records are as

shown in:

Advantages:

Decision-making - The executive committee wants statistics and business decision-

making. Account books have a role to play in the company (Zhang, Wang and Zhu,

2019). It includes information on cash reserves in the business as well as other

expenditures and revenues, making it easier to predict financial surpluses or losses in a

timely way. It also serves to establish supervision and accountability, which helps to

prevent and detect fraud. Evidence in legal matters - Account books function as a corporate background for the

substantial financial operation recorded within. It shall then serve as legal evidence in the

courts if any dispute exists. Entities shall maintain documents in the manner specified in

the Act and submit it to the Registrar after they've been audited by an external

investigator.

Disadvantages:

Records only financial aspects - One of the most significant disadvantages to financial

statements is that it refers only to the accounting of transfers of a financial kind. Various

sub-considerations, like consumer conditions, political environment, legal and regulatory

rules, etc., have significant implications for business practices. They are not recorded in

financial accounts and have an erroneous picture when making smarter business

decisions.

comparison in and of itself but also constitutes the foundation for the extraction of useful

information from non-financial details.

B. Advantages and disadvantages of accounting for a business

Accounting monitors and reviews the financial reports of a major company on the grounds of the

essence of the regulation. Benefits and risks related to the handling of financial records are as

shown in:

Advantages:

Decision-making - The executive committee wants statistics and business decision-

making. Account books have a role to play in the company (Zhang, Wang and Zhu,

2019). It includes information on cash reserves in the business as well as other

expenditures and revenues, making it easier to predict financial surpluses or losses in a

timely way. It also serves to establish supervision and accountability, which helps to

prevent and detect fraud. Evidence in legal matters - Account books function as a corporate background for the

substantial financial operation recorded within. It shall then serve as legal evidence in the

courts if any dispute exists. Entities shall maintain documents in the manner specified in

the Act and submit it to the Registrar after they've been audited by an external

investigator.

Disadvantages:

Records only financial aspects - One of the most significant disadvantages to financial

statements is that it refers only to the accounting of transfers of a financial kind. Various

sub-considerations, like consumer conditions, political environment, legal and regulatory

rules, etc., have significant implications for business practices. They are not recorded in

financial accounts and have an erroneous picture when making smarter business

decisions.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

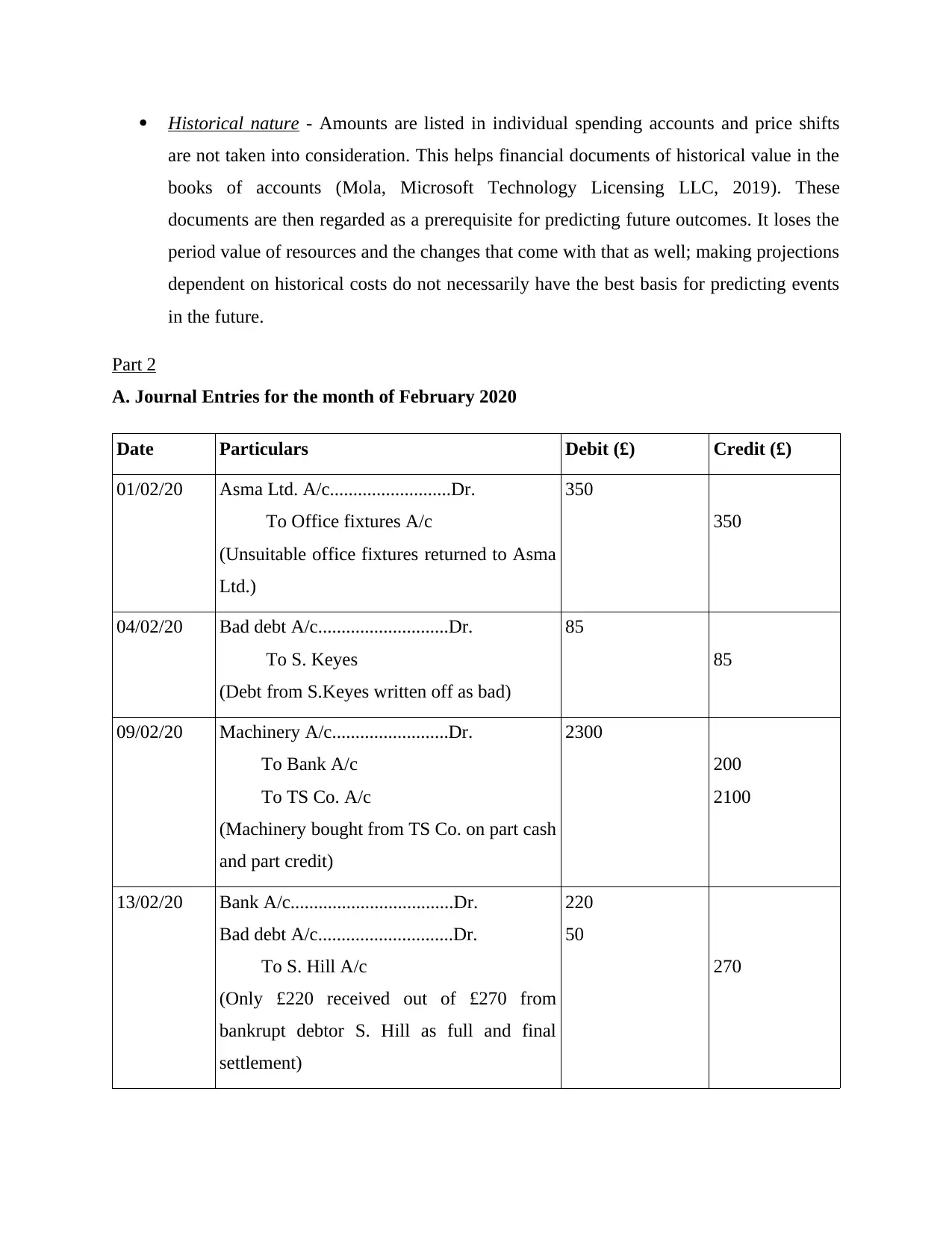

Historical nature - Amounts are listed in individual spending accounts and price shifts

are not taken into consideration. This helps financial documents of historical value in the

books of accounts (Mola, Microsoft Technology Licensing LLC, 2019). These

documents are then regarded as a prerequisite for predicting future outcomes. It loses the

period value of resources and the changes that come with that as well; making projections

dependent on historical costs do not necessarily have the best basis for predicting events

in the future.

Part 2

A. Journal Entries for the month of February 2020

Date Particulars Debit (£) Credit (£)

01/02/20 Asma Ltd. A/c..........................Dr.

To Office fixtures A/c

(Unsuitable office fixtures returned to Asma

Ltd.)

350

350

04/02/20 Bad debt A/c............................Dr.

To S. Keyes

(Debt from S.Keyes written off as bad)

85

85

09/02/20 Machinery A/c.........................Dr.

To Bank A/c

To TS Co. A/c

(Machinery bought from TS Co. on part cash

and part credit)

2300

200

2100

13/02/20 Bank A/c...................................Dr.

Bad debt A/c.............................Dr.

To S. Hill A/c

(Only £220 received out of £270 from

bankrupt debtor S. Hill as full and final

settlement)

220

50

270

are not taken into consideration. This helps financial documents of historical value in the

books of accounts (Mola, Microsoft Technology Licensing LLC, 2019). These

documents are then regarded as a prerequisite for predicting future outcomes. It loses the

period value of resources and the changes that come with that as well; making projections

dependent on historical costs do not necessarily have the best basis for predicting events

in the future.

Part 2

A. Journal Entries for the month of February 2020

Date Particulars Debit (£) Credit (£)

01/02/20 Asma Ltd. A/c..........................Dr.

To Office fixtures A/c

(Unsuitable office fixtures returned to Asma

Ltd.)

350

350

04/02/20 Bad debt A/c............................Dr.

To S. Keyes

(Debt from S.Keyes written off as bad)

85

85

09/02/20 Machinery A/c.........................Dr.

To Bank A/c

To TS Co. A/c

(Machinery bought from TS Co. on part cash

and part credit)

2300

200

2100

13/02/20 Bank A/c...................................Dr.

Bad debt A/c.............................Dr.

To S. Hill A/c

(Only £220 received out of £270 from

bankrupt debtor S. Hill as full and final

settlement)

220

50

270

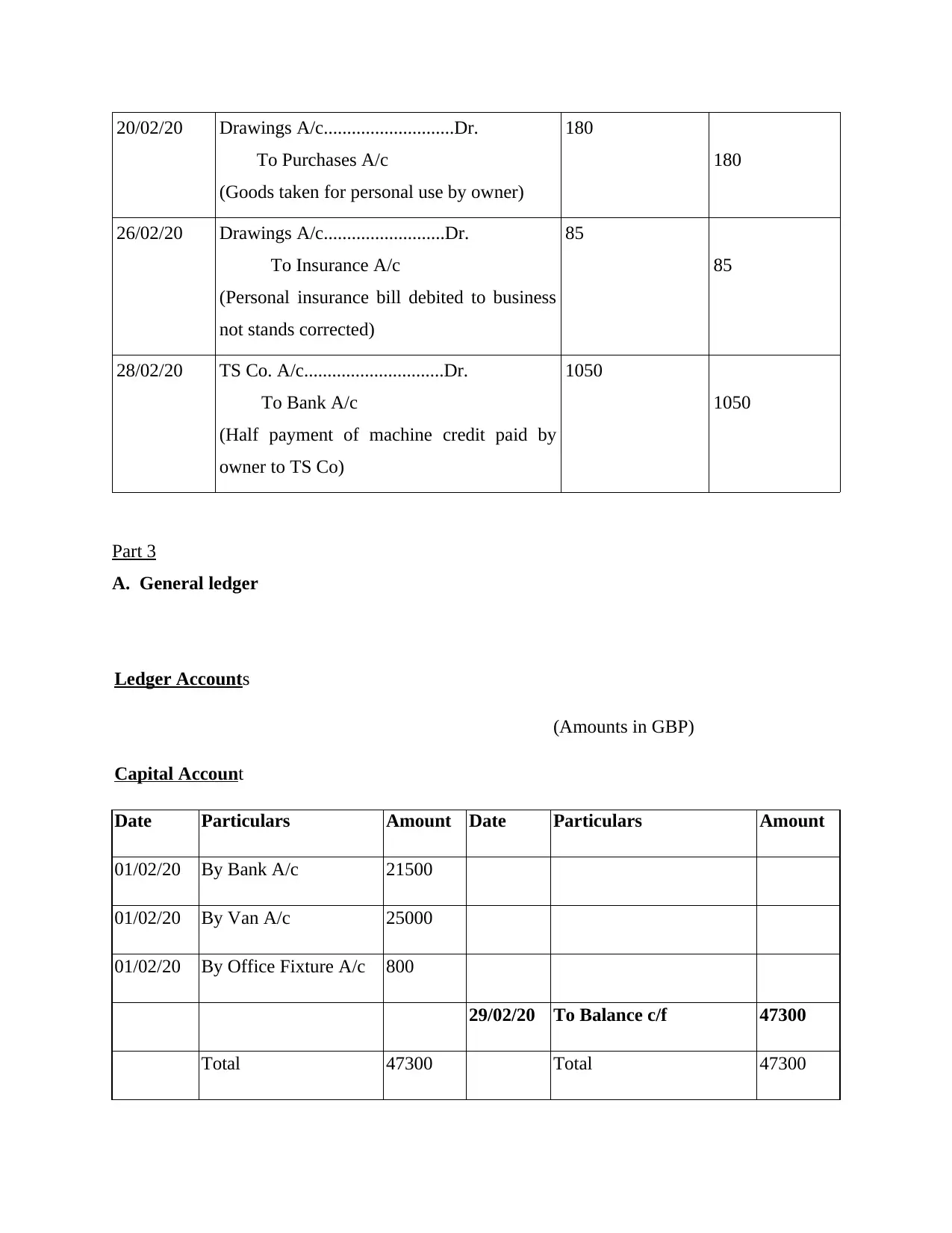

20/02/20 Drawings A/c............................Dr.

To Purchases A/c

(Goods taken for personal use by owner)

180

180

26/02/20 Drawings A/c..........................Dr.

To Insurance A/c

(Personal insurance bill debited to business

not stands corrected)

85

85

28/02/20 TS Co. A/c..............................Dr.

To Bank A/c

(Half payment of machine credit paid by

owner to TS Co)

1050

1050

Part 3

A. General ledger

Ledger Accounts

(Amounts in GBP)

Capital Account

Date Particulars Amount Date Particulars Amount

01/02/20 By Bank A/c 21500

01/02/20 By Van A/c 25000

01/02/20 By Office Fixture A/c 800

29/02/20 To Balance c/f 47300

Total 47300 Total 47300

To Purchases A/c

(Goods taken for personal use by owner)

180

180

26/02/20 Drawings A/c..........................Dr.

To Insurance A/c

(Personal insurance bill debited to business

not stands corrected)

85

85

28/02/20 TS Co. A/c..............................Dr.

To Bank A/c

(Half payment of machine credit paid by

owner to TS Co)

1050

1050

Part 3

A. General ledger

Ledger Accounts

(Amounts in GBP)

Capital Account

Date Particulars Amount Date Particulars Amount

01/02/20 By Bank A/c 21500

01/02/20 By Van A/c 25000

01/02/20 By Office Fixture A/c 800

29/02/20 To Balance c/f 47300

Total 47300 Total 47300

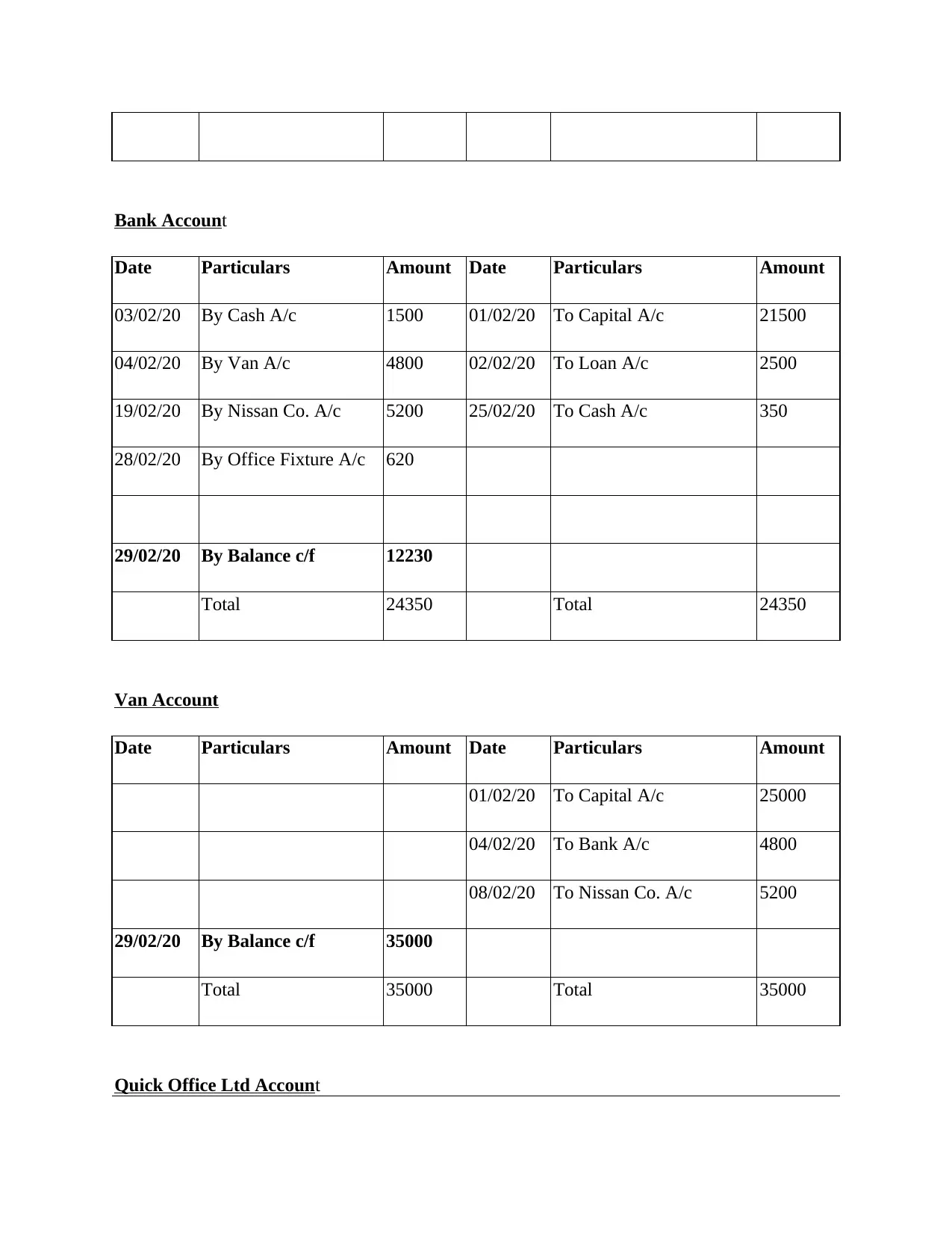

Bank Account

Date Particulars Amount Date Particulars Amount

03/02/20 By Cash A/c 1500 01/02/20 To Capital A/c 21500

04/02/20 By Van A/c 4800 02/02/20 To Loan A/c 2500

19/02/20 By Nissan Co. A/c 5200 25/02/20 To Cash A/c 350

28/02/20 By Office Fixture A/c 620

29/02/20 By Balance c/f 12230

Total 24350 Total 24350

Van Account

Date Particulars Amount Date Particulars Amount

01/02/20 To Capital A/c 25000

04/02/20 To Bank A/c 4800

08/02/20 To Nissan Co. A/c 5200

29/02/20 By Balance c/f 35000

Total 35000 Total 35000

Quick Office Ltd Account

Date Particulars Amount Date Particulars Amount

03/02/20 By Cash A/c 1500 01/02/20 To Capital A/c 21500

04/02/20 By Van A/c 4800 02/02/20 To Loan A/c 2500

19/02/20 By Nissan Co. A/c 5200 25/02/20 To Cash A/c 350

28/02/20 By Office Fixture A/c 620

29/02/20 By Balance c/f 12230

Total 24350 Total 24350

Van Account

Date Particulars Amount Date Particulars Amount

01/02/20 To Capital A/c 25000

04/02/20 To Bank A/c 4800

08/02/20 To Nissan Co. A/c 5200

29/02/20 By Balance c/f 35000

Total 35000 Total 35000

Quick Office Ltd Account

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

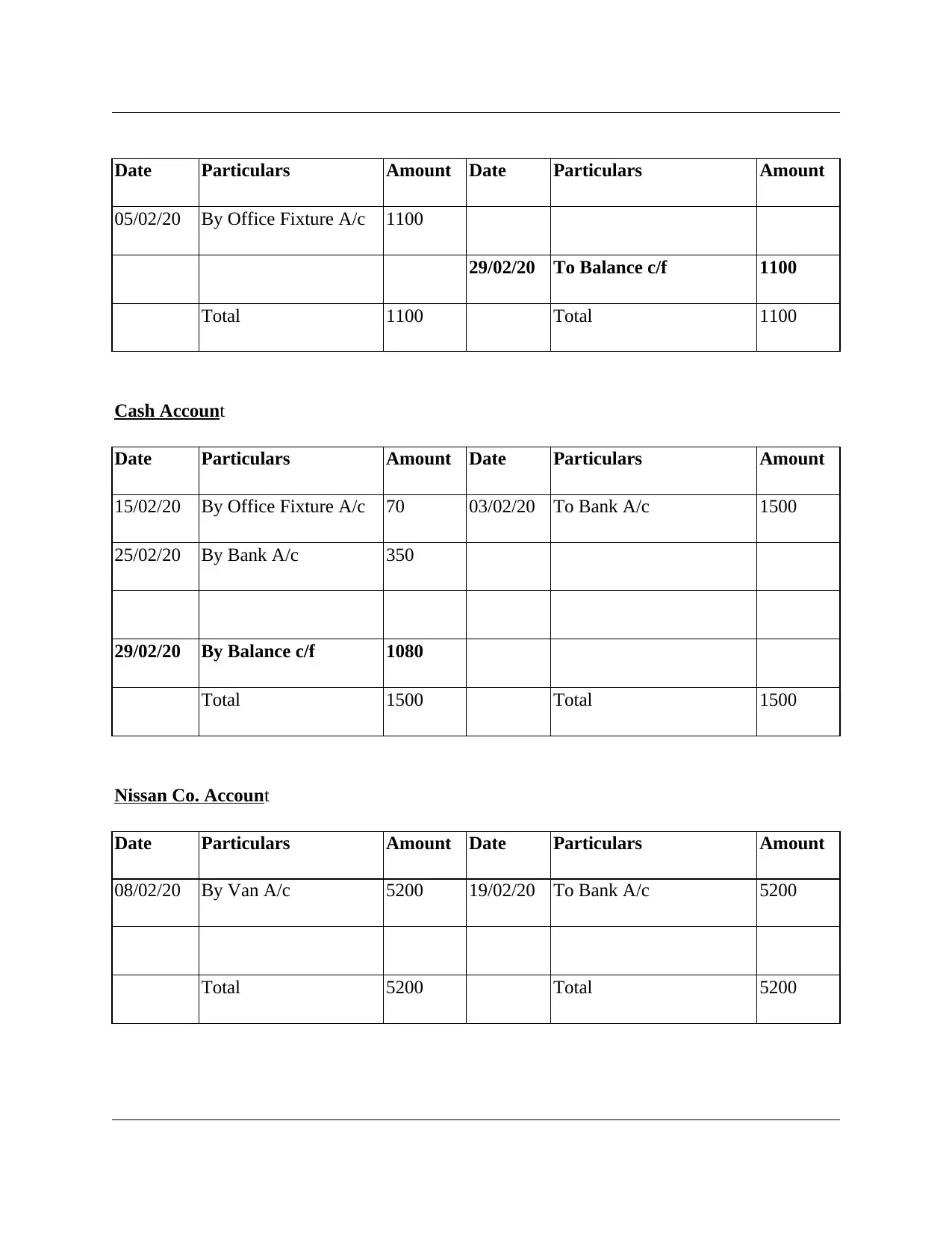

Date Particulars Amount Date Particulars Amount

05/02/20 By Office Fixture A/c 1100

29/02/20 To Balance c/f 1100

Total 1100 Total 1100

Cash Account

Date Particulars Amount Date Particulars Amount

15/02/20 By Office Fixture A/c 70 03/02/20 To Bank A/c 1500

25/02/20 By Bank A/c 350

29/02/20 By Balance c/f 1080

Total 1500 Total 1500

Nissan Co. Account

Date Particulars Amount Date Particulars Amount

08/02/20 By Van A/c 5200 19/02/20 To Bank A/c 5200

Total 5200 Total 5200

05/02/20 By Office Fixture A/c 1100

29/02/20 To Balance c/f 1100

Total 1100 Total 1100

Cash Account

Date Particulars Amount Date Particulars Amount

15/02/20 By Office Fixture A/c 70 03/02/20 To Bank A/c 1500

25/02/20 By Bank A/c 350

29/02/20 By Balance c/f 1080

Total 1500 Total 1500

Nissan Co. Account

Date Particulars Amount Date Particulars Amount

08/02/20 By Van A/c 5200 19/02/20 To Bank A/c 5200

Total 5200 Total 5200

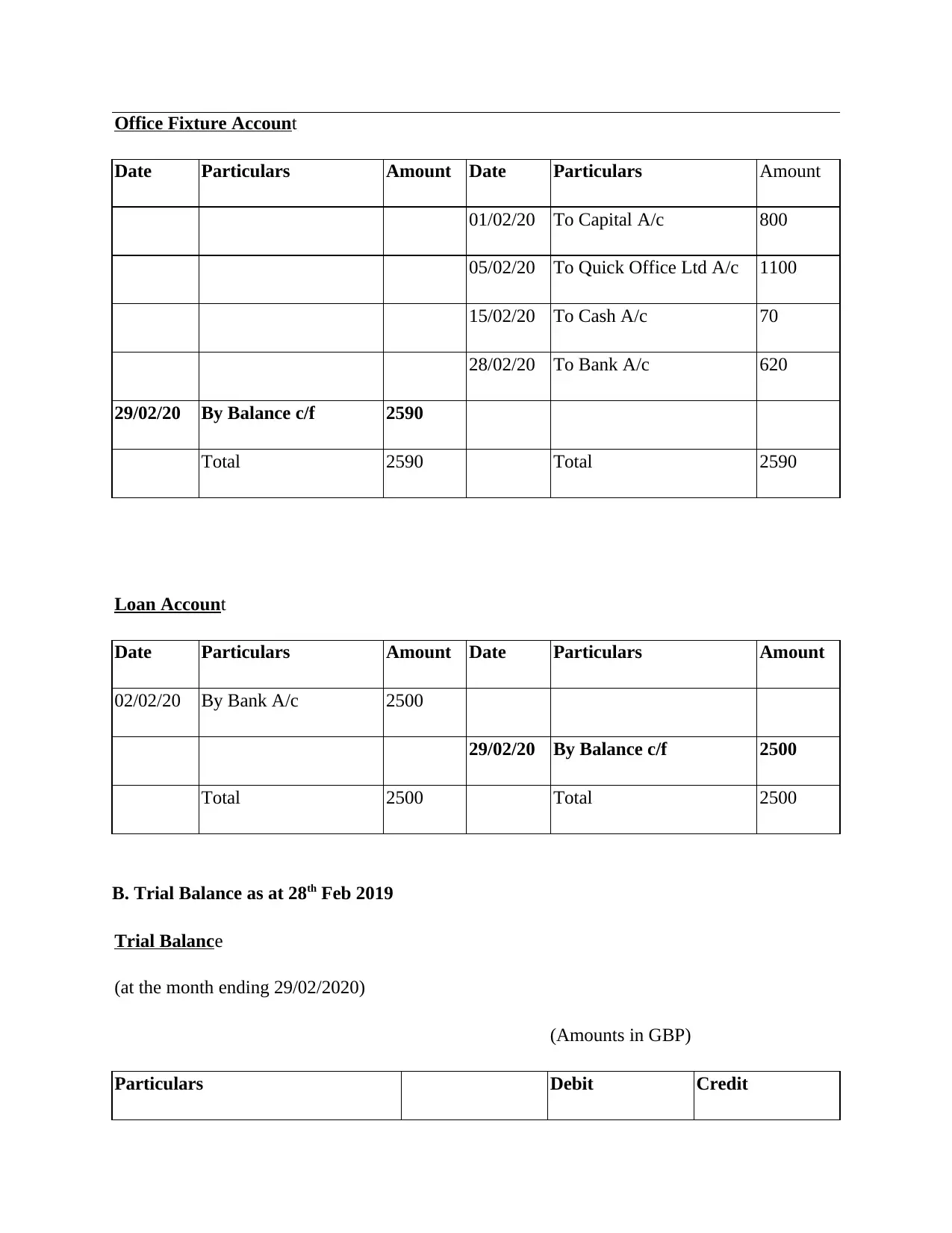

Office Fixture Account

Date Particulars Amount Date Particulars Amount

01/02/20 To Capital A/c 800

05/02/20 To Quick Office Ltd A/c 1100

15/02/20 To Cash A/c 70

28/02/20 To Bank A/c 620

29/02/20 By Balance c/f 2590

Total 2590 Total 2590

Loan Account

Date Particulars Amount Date Particulars Amount

02/02/20 By Bank A/c 2500

29/02/20 By Balance c/f 2500

Total 2500 Total 2500

B. Trial Balance as at 28th Feb 2019

Trial Balance

(at the month ending 29/02/2020)

(Amounts in GBP)

Particulars Debit Credit

Date Particulars Amount Date Particulars Amount

01/02/20 To Capital A/c 800

05/02/20 To Quick Office Ltd A/c 1100

15/02/20 To Cash A/c 70

28/02/20 To Bank A/c 620

29/02/20 By Balance c/f 2590

Total 2590 Total 2590

Loan Account

Date Particulars Amount Date Particulars Amount

02/02/20 By Bank A/c 2500

29/02/20 By Balance c/f 2500

Total 2500 Total 2500

B. Trial Balance as at 28th Feb 2019

Trial Balance

(at the month ending 29/02/2020)

(Amounts in GBP)

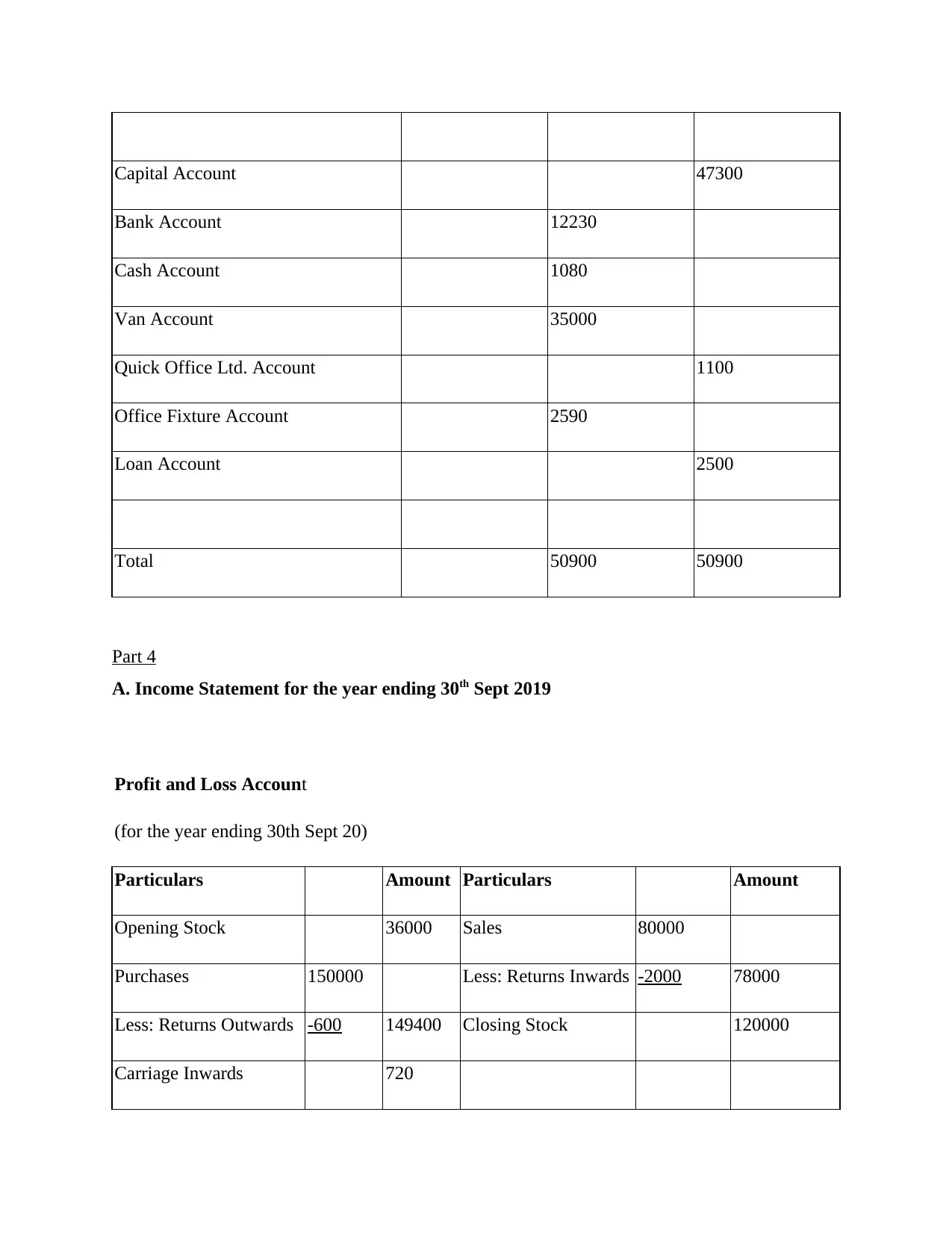

Particulars Debit Credit

Capital Account 47300

Bank Account 12230

Cash Account 1080

Van Account 35000

Quick Office Ltd. Account 1100

Office Fixture Account 2590

Loan Account 2500

Total 50900 50900

Part 4

A. Income Statement for the year ending 30th Sept 2019

Profit and Loss Account

(for the year ending 30th Sept 20)

Particulars Amount Particulars Amount

Opening Stock 36000 Sales 80000

Purchases 150000 Less: Returns Inwards -2000 78000

Less: Returns Outwards -600 149400 Closing Stock 120000

Carriage Inwards 720

Bank Account 12230

Cash Account 1080

Van Account 35000

Quick Office Ltd. Account 1100

Office Fixture Account 2590

Loan Account 2500

Total 50900 50900

Part 4

A. Income Statement for the year ending 30th Sept 2019

Profit and Loss Account

(for the year ending 30th Sept 20)

Particulars Amount Particulars Amount

Opening Stock 36000 Sales 80000

Purchases 150000 Less: Returns Inwards -2000 78000

Less: Returns Outwards -600 149400 Closing Stock 120000

Carriage Inwards 720

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

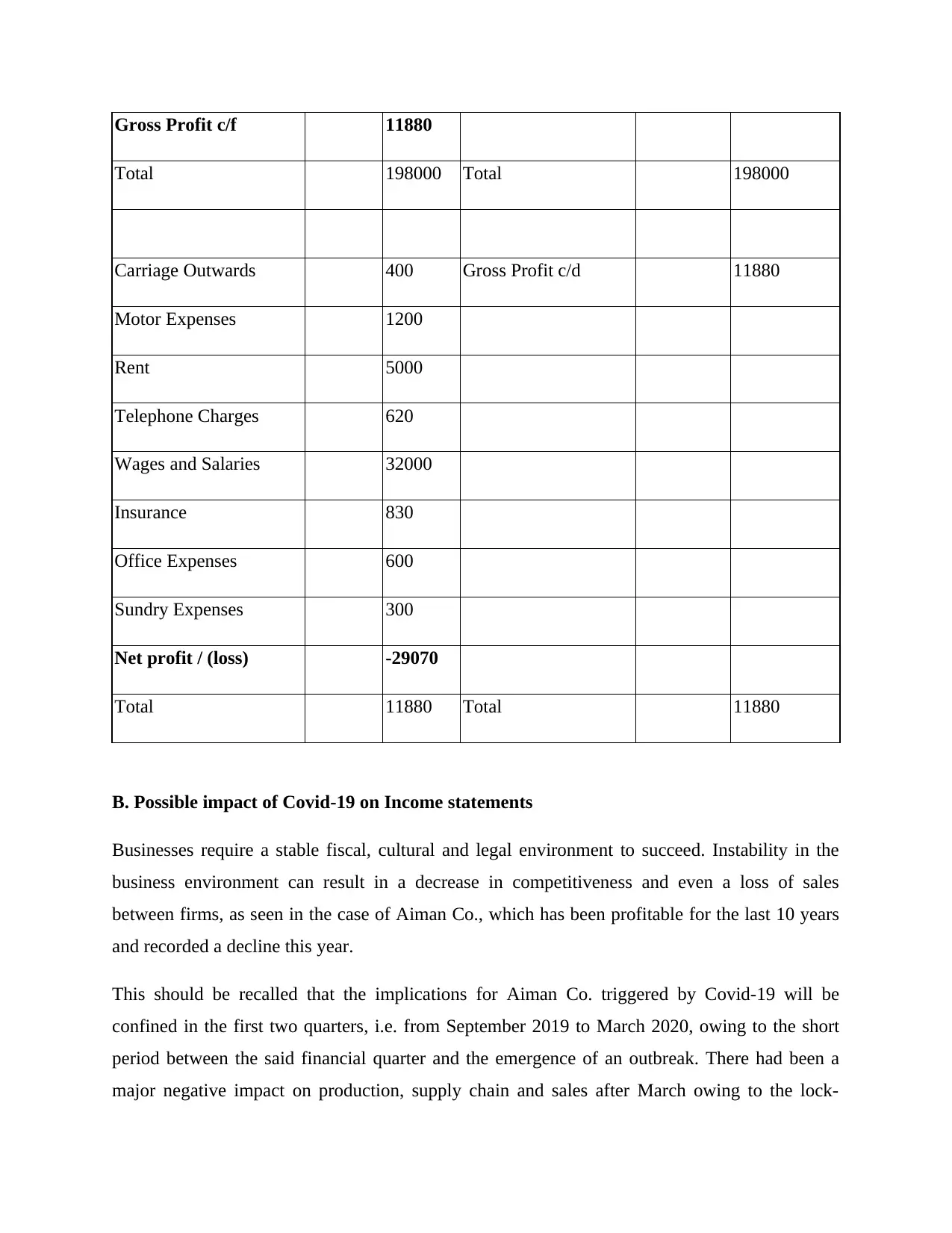

Gross Profit c/f 11880

Total 198000 Total 198000

Carriage Outwards 400 Gross Profit c/d 11880

Motor Expenses 1200

Rent 5000

Telephone Charges 620

Wages and Salaries 32000

Insurance 830

Office Expenses 600

Sundry Expenses 300

Net profit / (loss) -29070

Total 11880 Total 11880

B. Possible impact of Covid-19 on Income statements

Businesses require a stable fiscal, cultural and legal environment to succeed. Instability in the

business environment can result in a decrease in competitiveness and even a loss of sales

between firms, as seen in the case of Aiman Co., which has been profitable for the last 10 years

and recorded a decline this year.

This should be recalled that the implications for Aiman Co. triggered by Covid-19 will be

confined in the first two quarters, i.e. from September 2019 to March 2020, owing to the short

period between the said financial quarter and the emergence of an outbreak. There had been a

major negative impact on production, supply chain and sales after March owing to the lock-

Total 198000 Total 198000

Carriage Outwards 400 Gross Profit c/d 11880

Motor Expenses 1200

Rent 5000

Telephone Charges 620

Wages and Salaries 32000

Insurance 830

Office Expenses 600

Sundry Expenses 300

Net profit / (loss) -29070

Total 11880 Total 11880

B. Possible impact of Covid-19 on Income statements

Businesses require a stable fiscal, cultural and legal environment to succeed. Instability in the

business environment can result in a decrease in competitiveness and even a loss of sales

between firms, as seen in the case of Aiman Co., which has been profitable for the last 10 years

and recorded a decline this year.

This should be recalled that the implications for Aiman Co. triggered by Covid-19 will be

confined in the first two quarters, i.e. from September 2019 to March 2020, owing to the short

period between the said financial quarter and the emergence of an outbreak. There had been a

major negative impact on production, supply chain and sales after March owing to the lock-

down. Owing to the disruption in the production process, the amount and time needed for inward

and outward freight increased and income declined due to lower demand, while running

expenses had to be paid accordingly (Aladejebi and Oladimeji, 2019). This has seen the impact

on operating results, and Aiman Co. may have announced a failure due to this fiscal year. The

circumstances of the lock-down of Covid-19 are unique and peculiar. It is not possible to

determine how long the impact would are and how far the economic conditions for the business

would've been. Nor is it reasonable to associate the results of the last year at the trends of the last

ten years. Besides that, it can be assumed to have a bearing on the outcome of the next fiscal

year.

ASSESSEMENT 2

PART A

(a) Journal entries

Dates Particulars/details Dr. Cr.

1/10/2020 Bank a/c DR

Cash a/c DR

Van a/c DR

To Capital a/c

(Being capital fund invested in business)

8000

5200

3000

16200

2/10/2020 Laptop a/c DR

To bank a/c

(Being Laptop for business bought on

credit)

1000

1000

4/10/2020 Purchase a/c DR

To Toys limited

(Being Toys purchased on credit)

2450

2450

5/10/2020 Bank a/c DR

To sales a/c

(Being goods sold)

1500

1500

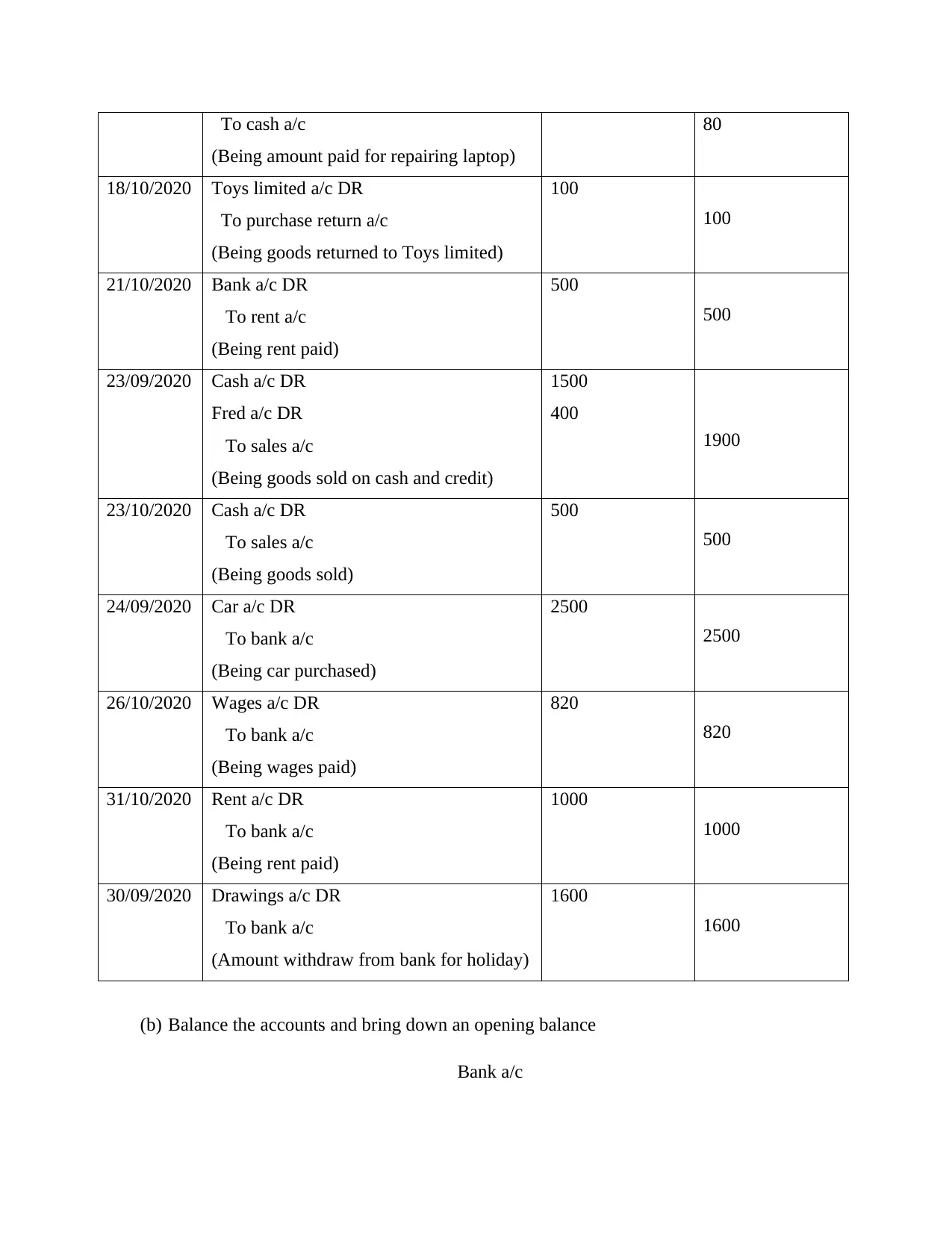

12/10/2020 Repairing laptop a/c DR 80

and outward freight increased and income declined due to lower demand, while running

expenses had to be paid accordingly (Aladejebi and Oladimeji, 2019). This has seen the impact

on operating results, and Aiman Co. may have announced a failure due to this fiscal year. The

circumstances of the lock-down of Covid-19 are unique and peculiar. It is not possible to

determine how long the impact would are and how far the economic conditions for the business

would've been. Nor is it reasonable to associate the results of the last year at the trends of the last

ten years. Besides that, it can be assumed to have a bearing on the outcome of the next fiscal

year.

ASSESSEMENT 2

PART A

(a) Journal entries

Dates Particulars/details Dr. Cr.

1/10/2020 Bank a/c DR

Cash a/c DR

Van a/c DR

To Capital a/c

(Being capital fund invested in business)

8000

5200

3000

16200

2/10/2020 Laptop a/c DR

To bank a/c

(Being Laptop for business bought on

credit)

1000

1000

4/10/2020 Purchase a/c DR

To Toys limited

(Being Toys purchased on credit)

2450

2450

5/10/2020 Bank a/c DR

To sales a/c

(Being goods sold)

1500

1500

12/10/2020 Repairing laptop a/c DR 80

To cash a/c

(Being amount paid for repairing laptop)

80

18/10/2020 Toys limited a/c DR

To purchase return a/c

(Being goods returned to Toys limited)

100

100

21/10/2020 Bank a/c DR

To rent a/c

(Being rent paid)

500

500

23/09/2020 Cash a/c DR

Fred a/c DR

To sales a/c

(Being goods sold on cash and credit)

1500

400

1900

23/10/2020 Cash a/c DR

To sales a/c

(Being goods sold)

500

500

24/09/2020 Car a/c DR

To bank a/c

(Being car purchased)

2500

2500

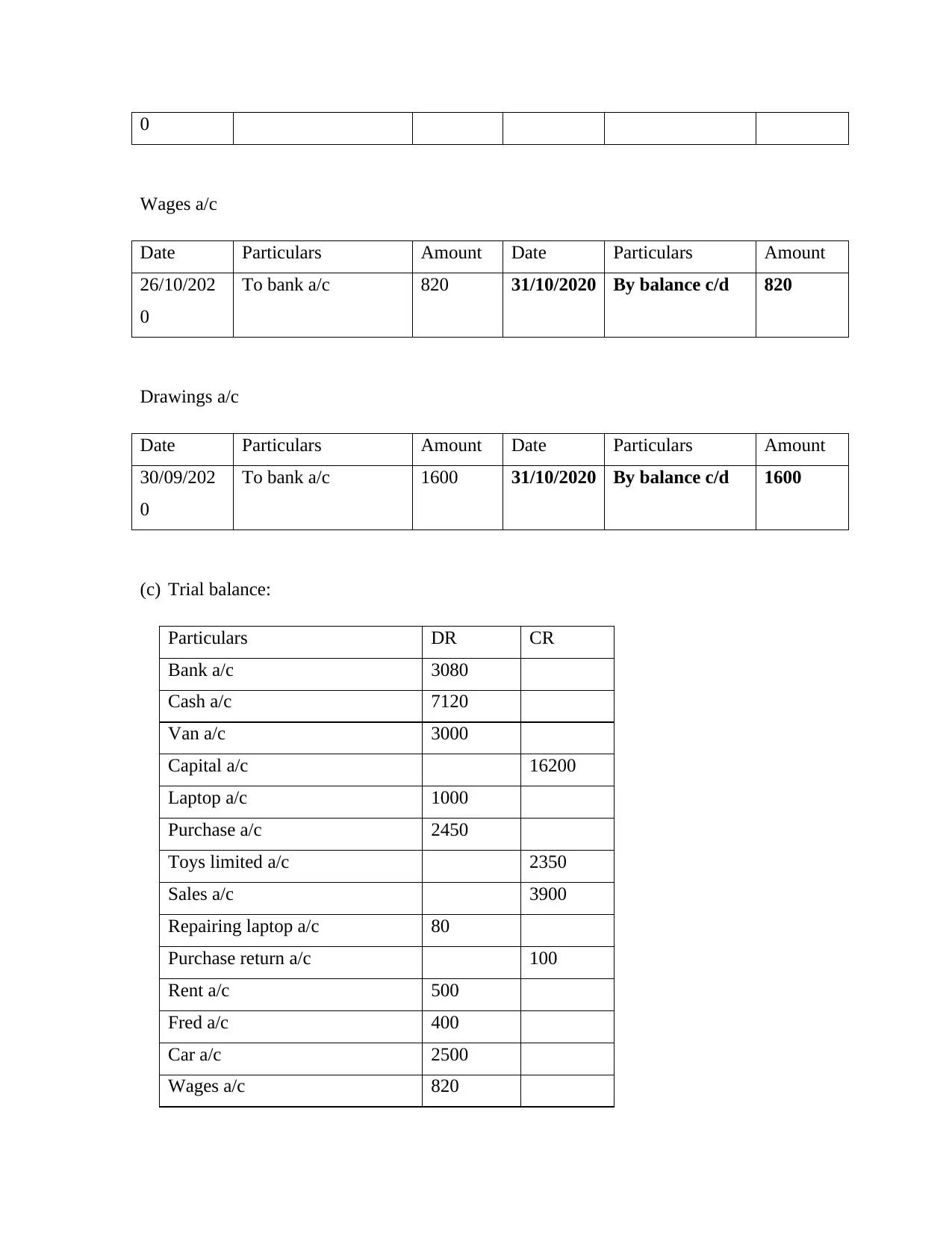

26/10/2020 Wages a/c DR

To bank a/c

(Being wages paid)

820

820

31/10/2020 Rent a/c DR

To bank a/c

(Being rent paid)

1000

1000

30/09/2020 Drawings a/c DR

To bank a/c

(Amount withdraw from bank for holiday)

1600

1600

(b) Balance the accounts and bring down an opening balance

Bank a/c

(Being amount paid for repairing laptop)

80

18/10/2020 Toys limited a/c DR

To purchase return a/c

(Being goods returned to Toys limited)

100

100

21/10/2020 Bank a/c DR

To rent a/c

(Being rent paid)

500

500

23/09/2020 Cash a/c DR

Fred a/c DR

To sales a/c

(Being goods sold on cash and credit)

1500

400

1900

23/10/2020 Cash a/c DR

To sales a/c

(Being goods sold)

500

500

24/09/2020 Car a/c DR

To bank a/c

(Being car purchased)

2500

2500

26/10/2020 Wages a/c DR

To bank a/c

(Being wages paid)

820

820

31/10/2020 Rent a/c DR

To bank a/c

(Being rent paid)

1000

1000

30/09/2020 Drawings a/c DR

To bank a/c

(Amount withdraw from bank for holiday)

1600

1600

(b) Balance the accounts and bring down an opening balance

Bank a/c

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

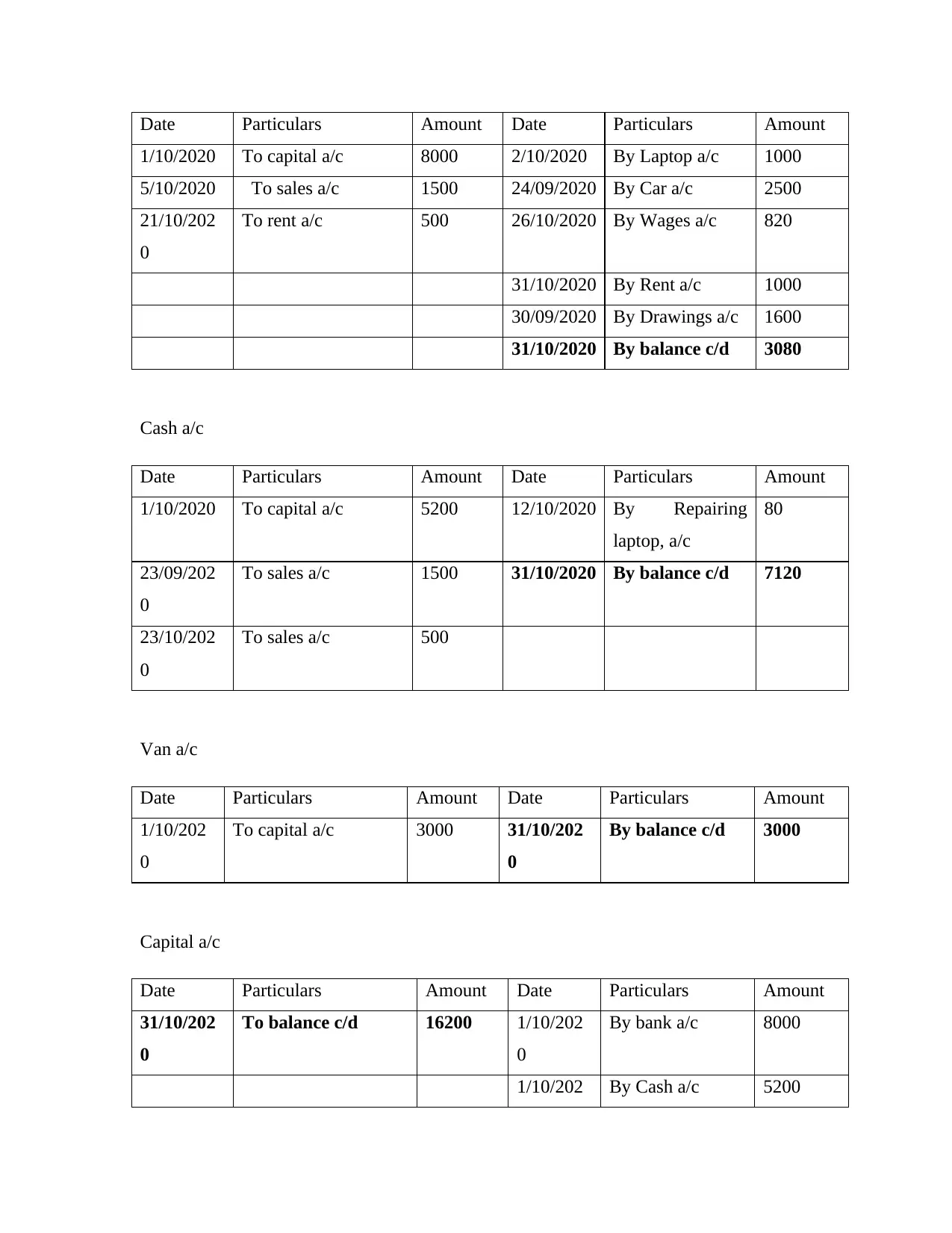

Date Particulars Amount Date Particulars Amount

1/10/2020 To capital a/c 8000 2/10/2020 By Laptop a/c 1000

5/10/2020 To sales a/c 1500 24/09/2020 By Car a/c 2500

21/10/202

0

To rent a/c 500 26/10/2020 By Wages a/c 820

31/10/2020 By Rent a/c 1000

30/09/2020 By Drawings a/c 1600

31/10/2020 By balance c/d 3080

Cash a/c

Date Particulars Amount Date Particulars Amount

1/10/2020 To capital a/c 5200 12/10/2020 By Repairing

laptop, a/c

80

23/09/202

0

To sales a/c 1500 31/10/2020 By balance c/d 7120

23/10/202

0

To sales a/c 500

Van a/c

Date Particulars Amount Date Particulars Amount

1/10/202

0

To capital a/c 3000 31/10/202

0

By balance c/d 3000

Capital a/c

Date Particulars Amount Date Particulars Amount

31/10/202

0

To balance c/d 16200 1/10/202

0

By bank a/c 8000

1/10/202 By Cash a/c 5200

1/10/2020 To capital a/c 8000 2/10/2020 By Laptop a/c 1000

5/10/2020 To sales a/c 1500 24/09/2020 By Car a/c 2500

21/10/202

0

To rent a/c 500 26/10/2020 By Wages a/c 820

31/10/2020 By Rent a/c 1000

30/09/2020 By Drawings a/c 1600

31/10/2020 By balance c/d 3080

Cash a/c

Date Particulars Amount Date Particulars Amount

1/10/2020 To capital a/c 5200 12/10/2020 By Repairing

laptop, a/c

80

23/09/202

0

To sales a/c 1500 31/10/2020 By balance c/d 7120

23/10/202

0

To sales a/c 500

Van a/c

Date Particulars Amount Date Particulars Amount

1/10/202

0

To capital a/c 3000 31/10/202

0

By balance c/d 3000

Capital a/c

Date Particulars Amount Date Particulars Amount

31/10/202

0

To balance c/d 16200 1/10/202

0

By bank a/c 8000

1/10/202 By Cash a/c 5200

0

1/10/202

0

By Van a/c 3000

Laptop a/c

Date Particulars Amount Date Particulars Amount

2/10/202

0

To bank a/c 1000 31/10/202

0

By balance c/d 1000

Purchase a/c

Date Particulars Amount Date Particulars Amount

4/10/202

0

To Toys limited 2450 31/10/202

0

By balance c/d 2450

Toys limited

Date Particulars Amount Date Particulars Amount

18/10/202

0

To purchase return

a/c

100 4/10/202

0

By Purchase a/c 2450

31/10/202

0

To balance c/d 2350

Sales a/c

Date Particulars Amount Date Particulars Amount

31/10/202

0

To balance c/d 3900 05/10/2020 By Bank a/c 1500

23/09/2020 By cash a/c 1500

23/09/2020 By Fred a/c 400

1/10/202

0

By Van a/c 3000

Laptop a/c

Date Particulars Amount Date Particulars Amount

2/10/202

0

To bank a/c 1000 31/10/202

0

By balance c/d 1000

Purchase a/c

Date Particulars Amount Date Particulars Amount

4/10/202

0

To Toys limited 2450 31/10/202

0

By balance c/d 2450

Toys limited

Date Particulars Amount Date Particulars Amount

18/10/202

0

To purchase return

a/c

100 4/10/202

0

By Purchase a/c 2450

31/10/202

0

To balance c/d 2350

Sales a/c

Date Particulars Amount Date Particulars Amount

31/10/202

0

To balance c/d 3900 05/10/2020 By Bank a/c 1500

23/09/2020 By cash a/c 1500

23/09/2020 By Fred a/c 400

23/10/2020 By Cash a/c 500

Repairing laptop a/c

Date Particulars Amount Date Particulars Amount

12/10/202

0

To cash a/c 80 31/10/2020 By balance c/d 80

Purchase return a/c

Date Particulars Amount Date Particulars Amount

31/10/202

0

To balance c/d 100 18/10/2020 By Toys limited

a/c

100

Rent a/c

Date Particulars Amount Date Particulars Amount

31/10/202

0

To bank a/c 1000 21/10/2020 By Bank a/c 500

31/10/2020 By balance c/d 500

Fred a/c

Date Particulars Amount Date Particulars Amount

23/09/202

0

To sales a/c 400 31/10/2020 By balance c/d 400

Car a/c

Date Particulars Amount Date Particulars Amount

26/09/202 To bank a/c 2500 31/10/2020 By balance c/d 2500

Repairing laptop a/c

Date Particulars Amount Date Particulars Amount

12/10/202

0

To cash a/c 80 31/10/2020 By balance c/d 80

Purchase return a/c

Date Particulars Amount Date Particulars Amount

31/10/202

0

To balance c/d 100 18/10/2020 By Toys limited

a/c

100

Rent a/c

Date Particulars Amount Date Particulars Amount

31/10/202

0

To bank a/c 1000 21/10/2020 By Bank a/c 500

31/10/2020 By balance c/d 500

Fred a/c

Date Particulars Amount Date Particulars Amount

23/09/202

0

To sales a/c 400 31/10/2020 By balance c/d 400

Car a/c

Date Particulars Amount Date Particulars Amount

26/09/202 To bank a/c 2500 31/10/2020 By balance c/d 2500

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

0

Wages a/c

Date Particulars Amount Date Particulars Amount

26/10/202

0

To bank a/c 820 31/10/2020 By balance c/d 820

Drawings a/c

Date Particulars Amount Date Particulars Amount

30/09/202

0

To bank a/c 1600 31/10/2020 By balance c/d 1600

(c) Trial balance:

Particulars DR CR

Bank a/c 3080

Cash a/c 7120

Van a/c 3000

Capital a/c 16200

Laptop a/c 1000

Purchase a/c 2450

Toys limited a/c 2350

Sales a/c 3900

Repairing laptop a/c 80

Purchase return a/c 100

Rent a/c 500

Fred a/c 400

Car a/c 2500

Wages a/c 820

Wages a/c

Date Particulars Amount Date Particulars Amount

26/10/202

0

To bank a/c 820 31/10/2020 By balance c/d 820

Drawings a/c

Date Particulars Amount Date Particulars Amount

30/09/202

0

To bank a/c 1600 31/10/2020 By balance c/d 1600

(c) Trial balance:

Particulars DR CR

Bank a/c 3080

Cash a/c 7120

Van a/c 3000

Capital a/c 16200

Laptop a/c 1000

Purchase a/c 2450

Toys limited a/c 2350

Sales a/c 3900

Repairing laptop a/c 80

Purchase return a/c 100

Rent a/c 500

Fred a/c 400

Car a/c 2500

Wages a/c 820

Drawings a/c 1600

22550 22550

(d) Income statement:

Particulars Amount

Sales 3900

Less: cost of goods sold

Opening stock 0

Purchases 2450

Less: Purchase return 100

Less: Closing stock 250

Gross profit 1800

Less: Operating expenses

Laptop repairing 80

Wages 820

Rent 1000

Add: Operating income

Rent received 500

Net Profit 400

(e) Statement of financial position

Assets

Fixed Assets

Laptop 1000

Second-hand car 2500

Van 3000

Current Assets

22550 22550

(d) Income statement:

Particulars Amount

Sales 3900

Less: cost of goods sold

Opening stock 0

Purchases 2450

Less: Purchase return 100

Less: Closing stock 250

Gross profit 1800

Less: Operating expenses

Laptop repairing 80

Wages 820

Rent 1000

Add: Operating income

Rent received 500

Net Profit 400

(e) Statement of financial position

Assets

Fixed Assets

Laptop 1000

Second-hand car 2500

Van 3000

Current Assets

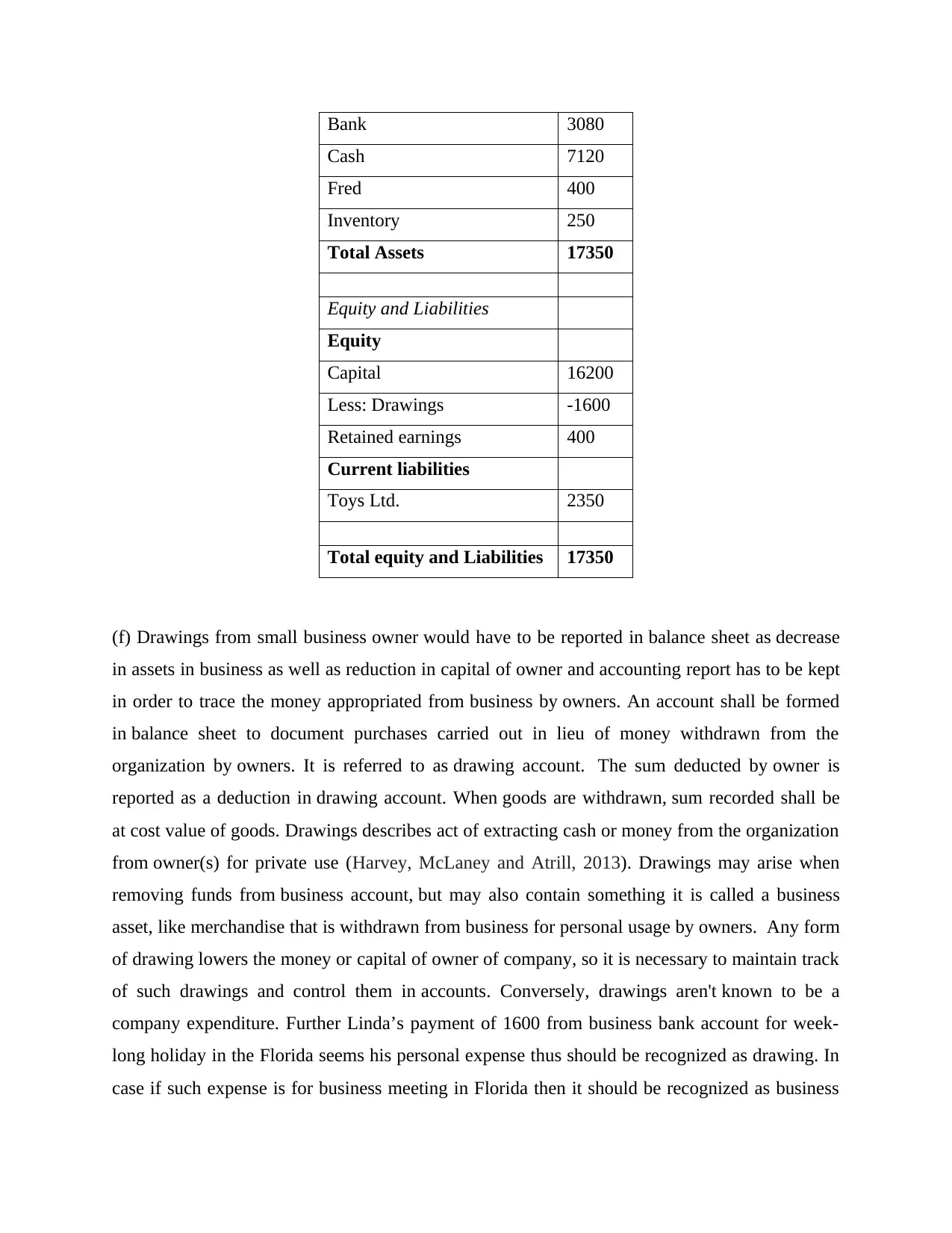

Bank 3080

Cash 7120

Fred 400

Inventory 250

Total Assets 17350

Equity and Liabilities

Equity

Capital 16200

Less: Drawings -1600

Retained earnings 400

Current liabilities

Toys Ltd. 2350

Total equity and Liabilities 17350

(f) Drawings from small business owner would have to be reported in balance sheet as decrease

in assets in business as well as reduction in capital of owner and accounting report has to be kept

in order to trace the money appropriated from business by owners. An account shall be formed

in balance sheet to document purchases carried out in lieu of money withdrawn from the

organization by owners. It is referred to as drawing account. The sum deducted by owner is

reported as a deduction in drawing account. When goods are withdrawn, sum recorded shall be

at cost value of goods. Drawings describes act of extracting cash or money from the organization

from owner(s) for private use (Harvey, McLaney and Atrill, 2013). Drawings may arise when

removing funds from business account, but may also contain something it is called a business

asset, like merchandise that is withdrawn from business for personal usage by owners. Any form

of drawing lowers the money or capital of owner of company, so it is necessary to maintain track

of such drawings and control them in accounts. Conversely, drawings aren't known to be a

company expenditure. Further Linda’s payment of 1600 from business bank account for week-

long holiday in the Florida seems his personal expense thus should be recognized as drawing. In

case if such expense is for business meeting in Florida then it should be recognized as business

Cash 7120

Fred 400

Inventory 250

Total Assets 17350

Equity and Liabilities

Equity

Capital 16200

Less: Drawings -1600

Retained earnings 400

Current liabilities

Toys Ltd. 2350

Total equity and Liabilities 17350

(f) Drawings from small business owner would have to be reported in balance sheet as decrease

in assets in business as well as reduction in capital of owner and accounting report has to be kept

in order to trace the money appropriated from business by owners. An account shall be formed

in balance sheet to document purchases carried out in lieu of money withdrawn from the

organization by owners. It is referred to as drawing account. The sum deducted by owner is

reported as a deduction in drawing account. When goods are withdrawn, sum recorded shall be

at cost value of goods. Drawings describes act of extracting cash or money from the organization

from owner(s) for private use (Harvey, McLaney and Atrill, 2013). Drawings may arise when

removing funds from business account, but may also contain something it is called a business

asset, like merchandise that is withdrawn from business for personal usage by owners. Any form

of drawing lowers the money or capital of owner of company, so it is necessary to maintain track

of such drawings and control them in accounts. Conversely, drawings aren't known to be a

company expenditure. Further Linda’s payment of 1600 from business bank account for week-

long holiday in the Florida seems his personal expense thus should be recognized as drawing. In

case if such expense is for business meeting in Florida then it should be recognized as business

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

expense there for recognition of a payment as business expense or drawing depends upon its

main purpose whether personal or business.

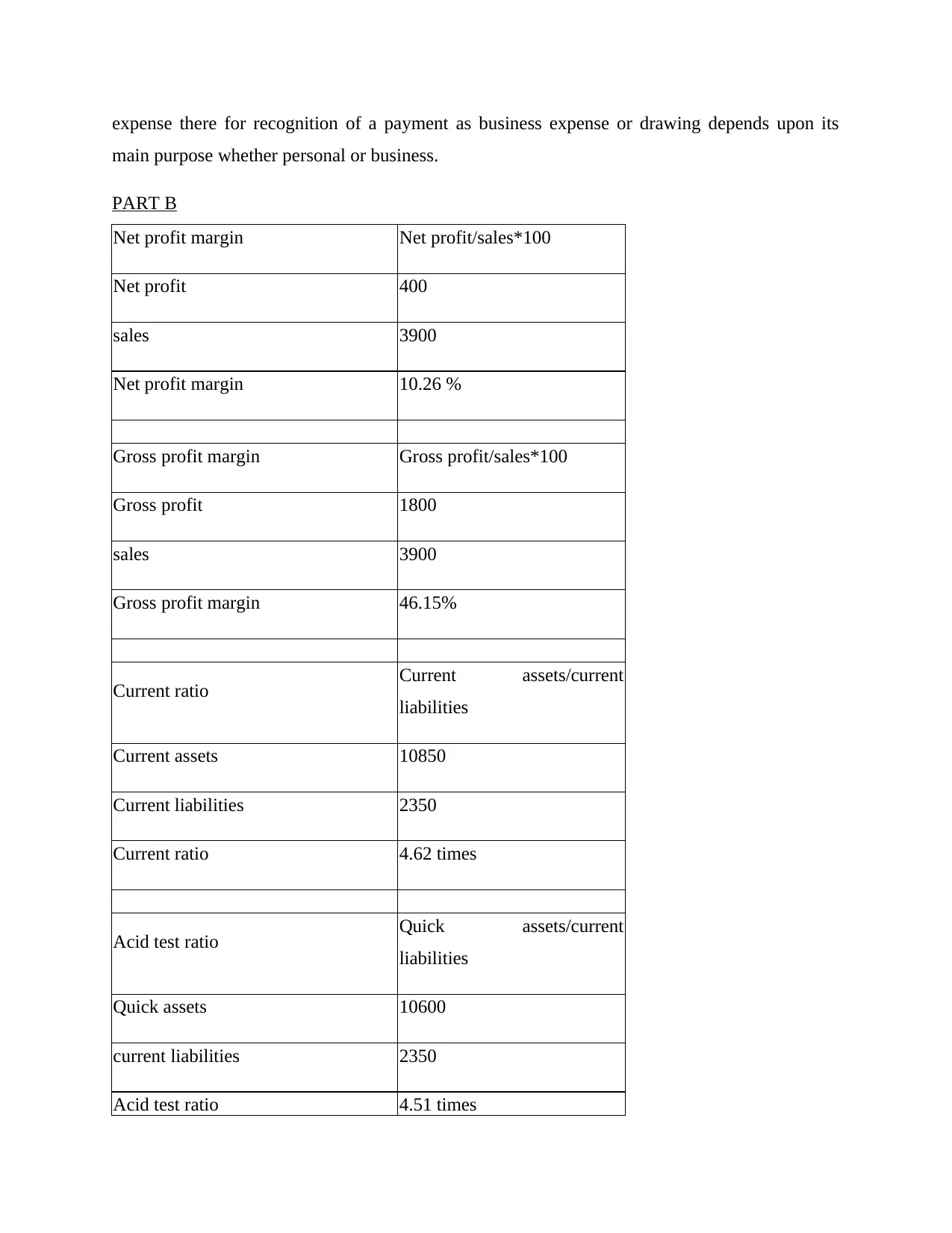

PART B

Net profit margin Net profit/sales*100

Net profit 400

sales 3900

Net profit margin 10.26 %

Gross profit margin Gross profit/sales*100

Gross profit 1800

sales 3900

Gross profit margin 46.15%

Current ratio Current assets/current

liabilities

Current assets 10850

Current liabilities 2350

Current ratio 4.62 times

Acid test ratio Quick assets/current

liabilities

Quick assets 10600

current liabilities 2350

Acid test ratio 4.51 times

main purpose whether personal or business.

PART B

Net profit margin Net profit/sales*100

Net profit 400

sales 3900

Net profit margin 10.26 %

Gross profit margin Gross profit/sales*100

Gross profit 1800

sales 3900

Gross profit margin 46.15%

Current ratio Current assets/current

liabilities

Current assets 10850

Current liabilities 2350

Current ratio 4.62 times

Acid test ratio Quick assets/current

liabilities

Quick assets 10600

current liabilities 2350

Acid test ratio 4.51 times

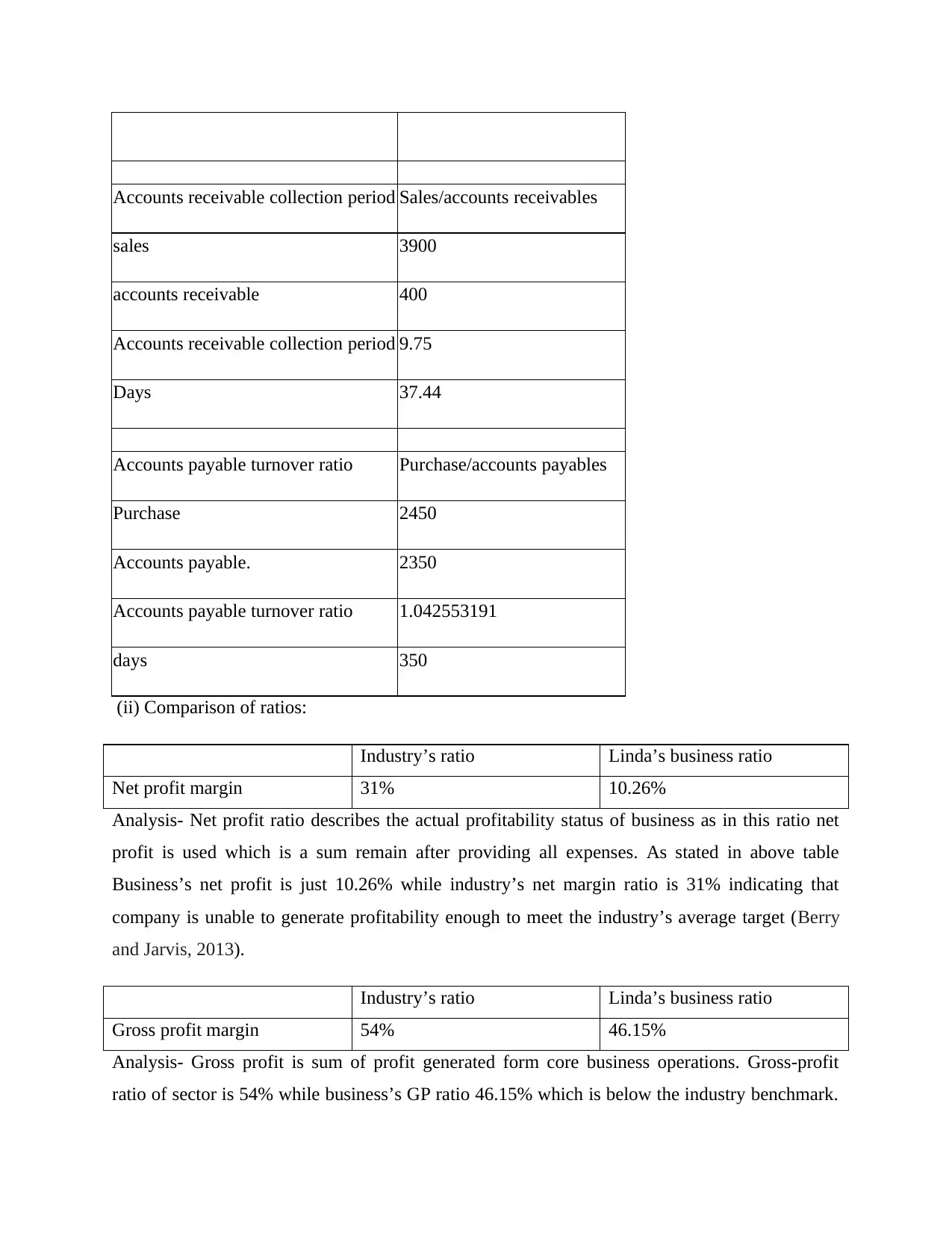

Accounts receivable collection period Sales/accounts receivables

sales 3900

accounts receivable 400

Accounts receivable collection period 9.75

Days 37.44

Accounts payable turnover ratio Purchase/accounts payables

Purchase 2450

Accounts payable. 2350

Accounts payable turnover ratio 1.042553191

days 350

(ii) Comparison of ratios:

Industry’s ratio Linda’s business ratio

Net profit margin 31% 10.26%

Analysis- Net profit ratio describes the actual profitability status of business as in this ratio net

profit is used which is a sum remain after providing all expenses. As stated in above table

Business’s net profit is just 10.26% while industry’s net margin ratio is 31% indicating that

company is unable to generate profitability enough to meet the industry’s average target (Berry

and Jarvis, 2013).

Industry’s ratio Linda’s business ratio

Gross profit margin 54% 46.15%

Analysis- Gross profit is sum of profit generated form core business operations. Gross-profit

ratio of sector is 54% while business’s GP ratio 46.15% which is below the industry benchmark.

sales 3900

accounts receivable 400

Accounts receivable collection period 9.75

Days 37.44

Accounts payable turnover ratio Purchase/accounts payables

Purchase 2450

Accounts payable. 2350

Accounts payable turnover ratio 1.042553191

days 350

(ii) Comparison of ratios:

Industry’s ratio Linda’s business ratio

Net profit margin 31% 10.26%

Analysis- Net profit ratio describes the actual profitability status of business as in this ratio net

profit is used which is a sum remain after providing all expenses. As stated in above table

Business’s net profit is just 10.26% while industry’s net margin ratio is 31% indicating that

company is unable to generate profitability enough to meet the industry’s average target (Berry

and Jarvis, 2013).

Industry’s ratio Linda’s business ratio

Gross profit margin 54% 46.15%

Analysis- Gross profit is sum of profit generated form core business operations. Gross-profit

ratio of sector is 54% while business’s GP ratio 46.15% which is below the industry benchmark.

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.