Recording Business Transactions: Steps for Establishing a New Business of Decorator

VerifiedAdded on 2023/06/17

|15

|3448

|241

AI Summary

The article explains the steps involved in establishing a new business of decorator and recording business transactions. It also discusses the decision makers in a large organisation listed on London Stock Exchange.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Recording Business

Transactions

1

Transactions

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of content

Table of Contents

Introduction......................................................................................................................................3

Part A...............................................................................................................................................3

Explain the steps for establishing a new business of Decorator.............................................3

Accounting involves recording, analysing and summarising the transactions of each business

organisation in order to provide information for decision making. Consider a large

organisation that is listed on a London Stock Exchange and identify the decision makers that

are referred in the above decisions.........................................................................................4

Part B...............................................................................................................................................5

Journal Entry..........................................................................................................................5

General Ledger of ABC enterprise, Maurice and Brothers ...................................................7

Part 3..............................................................................................................................................10

Income statement..................................................................................................................10

Prediction of Profit and Loss of B Moore for the year 2022................................................12

Conclusion.....................................................................................................................................13

REFERENCES..............................................................................................................................14

2

Table of Contents

Introduction......................................................................................................................................3

Part A...............................................................................................................................................3

Explain the steps for establishing a new business of Decorator.............................................3

Accounting involves recording, analysing and summarising the transactions of each business

organisation in order to provide information for decision making. Consider a large

organisation that is listed on a London Stock Exchange and identify the decision makers that

are referred in the above decisions.........................................................................................4

Part B...............................................................................................................................................5

Journal Entry..........................................................................................................................5

General Ledger of ABC enterprise, Maurice and Brothers ...................................................7

Part 3..............................................................................................................................................10

Income statement..................................................................................................................10

Prediction of Profit and Loss of B Moore for the year 2022................................................12

Conclusion.....................................................................................................................................13

REFERENCES..............................................................................................................................14

2

Introduction

The process of recording business transactions is an important aspect of the business.

Business is basically referred as the economic activity that is performed with the intention of

earning profits in order to earn a living and maximise the wealth. The recording of transaction

comprises of financial statement and it is a key responsibility of every accounting department. In

order to record a specific transaction, it is very important to understand a transaction while

understanding the importance of each transaction. It is important to record the essential business

transaction as it can have a significant impact over the business and financial statements of the

business. The concept of income statement will also be covered in aspect of the business.

(Adamyk, 2017).

Part A

Explain the steps for establishing a new business of Decorator.

David Green is planning to set up a sole proprietorship business as a decorator. Sole

proprietor business is a business wherein the owner is a sole person who is responsible for all the

operations and the business activities. In order to start a business various steps are required to be

performed.

Conduct market research- David green will require to conduct a market research in

order to analyse the number of competitors in the industry. The market research will help

the business to analyse the business environment as well as the analysis of market in

terms of demand and supply (Prihanto and et.al., 2019).

Business plan- The next step after conducting a market research is to design a business

plan and according to this the business will be initiated. The business plan comprises of

various mission, vision and objectives that will be required to get accomplished by the

organisation. Fund business- The next step in order to establish a decorator business, the owner will

have to look upon various sources of funds. It is very important for the business to source

funds in order to survive and expand its business. There are various sources of funds that

can be opted by David Green in order to fund the business. The several sources of funds

have been suggested below (Thabit and Abbas, 2017).

3

The process of recording business transactions is an important aspect of the business.

Business is basically referred as the economic activity that is performed with the intention of

earning profits in order to earn a living and maximise the wealth. The recording of transaction

comprises of financial statement and it is a key responsibility of every accounting department. In

order to record a specific transaction, it is very important to understand a transaction while

understanding the importance of each transaction. It is important to record the essential business

transaction as it can have a significant impact over the business and financial statements of the

business. The concept of income statement will also be covered in aspect of the business.

(Adamyk, 2017).

Part A

Explain the steps for establishing a new business of Decorator.

David Green is planning to set up a sole proprietorship business as a decorator. Sole

proprietor business is a business wherein the owner is a sole person who is responsible for all the

operations and the business activities. In order to start a business various steps are required to be

performed.

Conduct market research- David green will require to conduct a market research in

order to analyse the number of competitors in the industry. The market research will help

the business to analyse the business environment as well as the analysis of market in

terms of demand and supply (Prihanto and et.al., 2019).

Business plan- The next step after conducting a market research is to design a business

plan and according to this the business will be initiated. The business plan comprises of

various mission, vision and objectives that will be required to get accomplished by the

organisation. Fund business- The next step in order to establish a decorator business, the owner will

have to look upon various sources of funds. It is very important for the business to source

funds in order to survive and expand its business. There are various sources of funds that

can be opted by David Green in order to fund the business. The several sources of funds

have been suggested below (Thabit and Abbas, 2017).

3

◦ Bank Loans- The banks loan is also considered as a source of funds wherein the bank

grants loan. The loan is repaid by paying interest upon the principal amount.

◦ Retained earnings- Retained earnings can be termed as personal investment that is

brought in by the entrepreneur in order to bring finances for the business. The

retained earnings are basically the savings of an individual (Aritonang and Janrosi,

2020).

◦ Government grants and subsidies- The government agencies tend to provide finances

in terms of grants and subsidies that is available for various businesses. They are

provided at the federal and provincial level.

Pick business location- The business will require to pick a location that can prove

appropriate for the business. An ideal location is the one that is easily accessible for the

people.

Choose a business structure- The owner will be required to choose a business structure

that David Green has already chosen as a sole proprietor.

Choose your business name- An attractive business name needs to chosen that defines

the business (Rahwani, 2017).

Register the business- Once the name of the business is decided, the business is required

to get registered.

Get federal and state Tax IDs- The business of decorator needs to get federal and state

tax Ids in the name of business.

Apply for licences and permits- The business will be required to apply for various

licences and permits to operate its business.

Opening business bank account- Also, there must be a current bank account in the

name of the organisation through which the transactions will take place (Rechtman,

2017).

Accounting involves recording, analysing and summarising the transactions of each business

organisation in order to provide information for decision making. Consider a large

organisation that is listed on a London Stock Exchange and identify the decision makers

that are referred in the above decisions.

The organisation that has been considered for this section is Tesco. Tesco is a multi national

organisation that is listed upon London Stock Exchange. The decision makers of Tesco are

4

grants loan. The loan is repaid by paying interest upon the principal amount.

◦ Retained earnings- Retained earnings can be termed as personal investment that is

brought in by the entrepreneur in order to bring finances for the business. The

retained earnings are basically the savings of an individual (Aritonang and Janrosi,

2020).

◦ Government grants and subsidies- The government agencies tend to provide finances

in terms of grants and subsidies that is available for various businesses. They are

provided at the federal and provincial level.

Pick business location- The business will require to pick a location that can prove

appropriate for the business. An ideal location is the one that is easily accessible for the

people.

Choose a business structure- The owner will be required to choose a business structure

that David Green has already chosen as a sole proprietor.

Choose your business name- An attractive business name needs to chosen that defines

the business (Rahwani, 2017).

Register the business- Once the name of the business is decided, the business is required

to get registered.

Get federal and state Tax IDs- The business of decorator needs to get federal and state

tax Ids in the name of business.

Apply for licences and permits- The business will be required to apply for various

licences and permits to operate its business.

Opening business bank account- Also, there must be a current bank account in the

name of the organisation through which the transactions will take place (Rechtman,

2017).

Accounting involves recording, analysing and summarising the transactions of each business

organisation in order to provide information for decision making. Consider a large

organisation that is listed on a London Stock Exchange and identify the decision makers

that are referred in the above decisions.

The organisation that has been considered for this section is Tesco. Tesco is a multi national

organisation that is listed upon London Stock Exchange. The decision makers of Tesco are

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

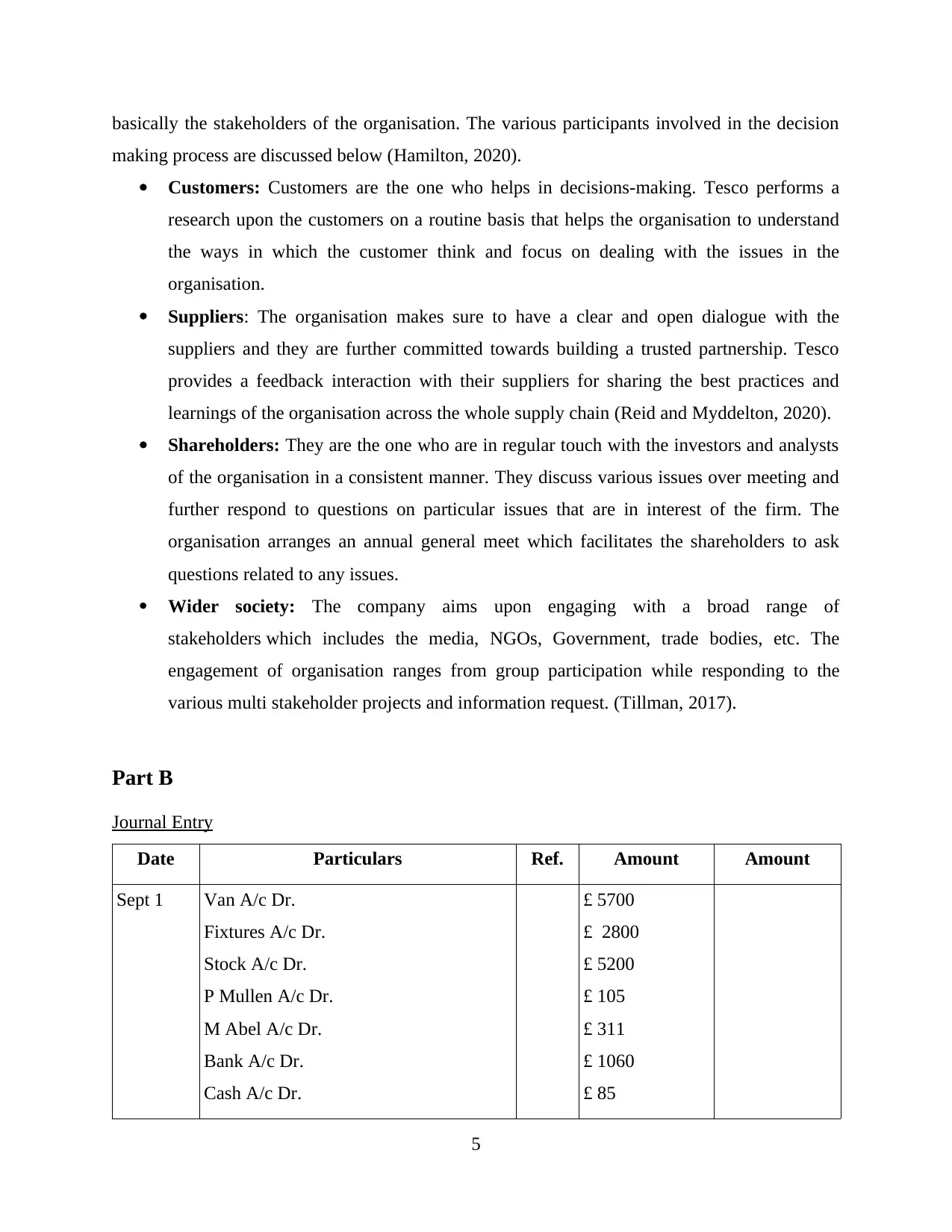

basically the stakeholders of the organisation. The various participants involved in the decision

making process are discussed below (Hamilton, 2020).

Customers: Customers are the one who helps in decisions-making. Tesco performs a

research upon the customers on a routine basis that helps the organisation to understand

the ways in which the customer think and focus on dealing with the issues in the

organisation.

Suppliers: The organisation makes sure to have a clear and open dialogue with the

suppliers and they are further committed towards building a trusted partnership. Tesco

provides a feedback interaction with their suppliers for sharing the best practices and

learnings of the organisation across the whole supply chain (Reid and Myddelton, 2020).

Shareholders: They are the one who are in regular touch with the investors and analysts

of the organisation in a consistent manner. They discuss various issues over meeting and

further respond to questions on particular issues that are in interest of the firm. The

organisation arranges an annual general meet which facilitates the shareholders to ask

questions related to any issues.

Wider society: The company aims upon engaging with a broad range of

stakeholders which includes the media, NGOs, Government, trade bodies, etc. The

engagement of organisation ranges from group participation while responding to the

various multi stakeholder projects and information request. (Tillman, 2017).

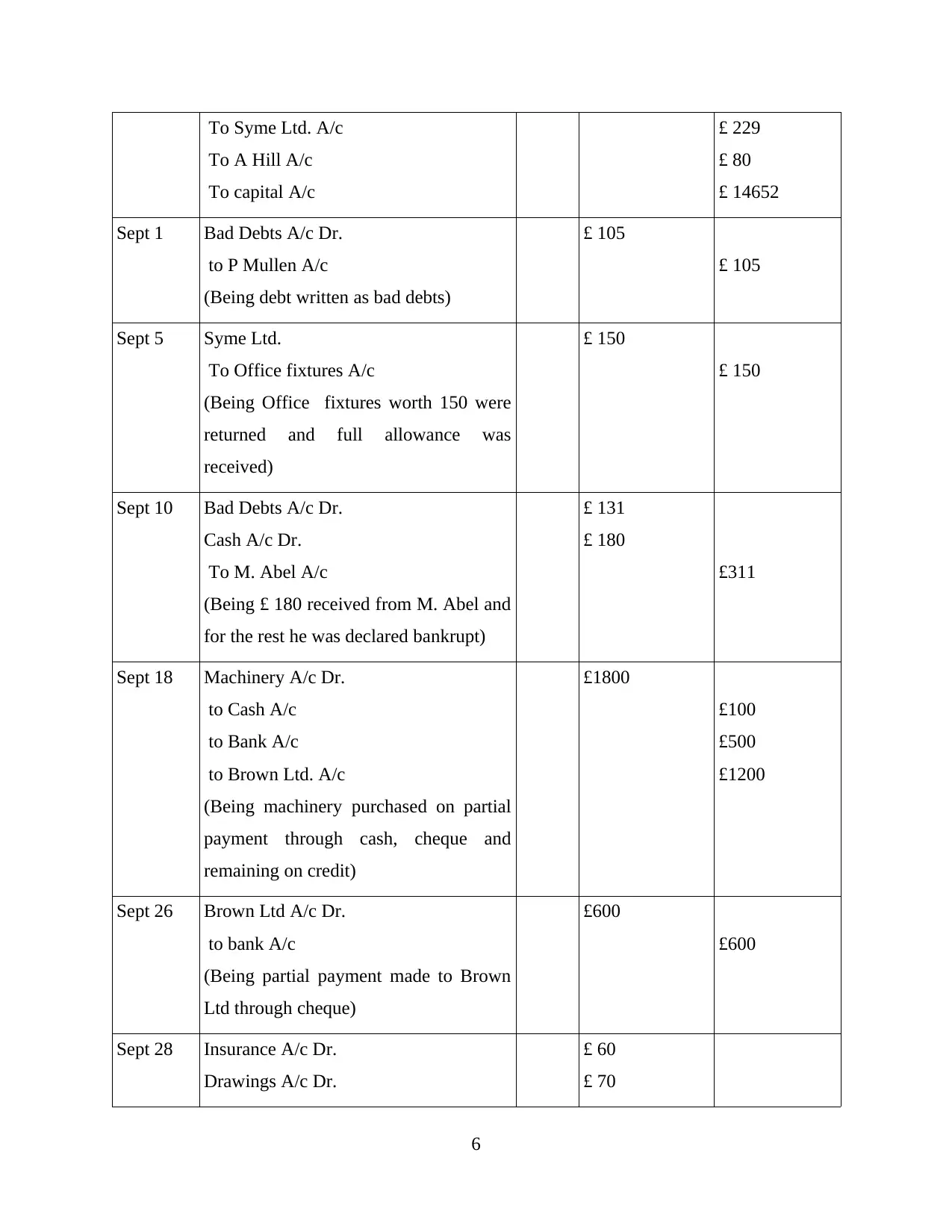

Part B

Journal Entry

Date Particulars Ref. Amount Amount

Sept 1 Van A/c Dr.

Fixtures A/c Dr.

Stock A/c Dr.

P Mullen A/c Dr.

M Abel A/c Dr.

Bank A/c Dr.

Cash A/c Dr.

£ 5700

£ 2800

£ 5200

£ 105

£ 311

£ 1060

£ 85

5

making process are discussed below (Hamilton, 2020).

Customers: Customers are the one who helps in decisions-making. Tesco performs a

research upon the customers on a routine basis that helps the organisation to understand

the ways in which the customer think and focus on dealing with the issues in the

organisation.

Suppliers: The organisation makes sure to have a clear and open dialogue with the

suppliers and they are further committed towards building a trusted partnership. Tesco

provides a feedback interaction with their suppliers for sharing the best practices and

learnings of the organisation across the whole supply chain (Reid and Myddelton, 2020).

Shareholders: They are the one who are in regular touch with the investors and analysts

of the organisation in a consistent manner. They discuss various issues over meeting and

further respond to questions on particular issues that are in interest of the firm. The

organisation arranges an annual general meet which facilitates the shareholders to ask

questions related to any issues.

Wider society: The company aims upon engaging with a broad range of

stakeholders which includes the media, NGOs, Government, trade bodies, etc. The

engagement of organisation ranges from group participation while responding to the

various multi stakeholder projects and information request. (Tillman, 2017).

Part B

Journal Entry

Date Particulars Ref. Amount Amount

Sept 1 Van A/c Dr.

Fixtures A/c Dr.

Stock A/c Dr.

P Mullen A/c Dr.

M Abel A/c Dr.

Bank A/c Dr.

Cash A/c Dr.

£ 5700

£ 2800

£ 5200

£ 105

£ 311

£ 1060

£ 85

5

To Syme Ltd. A/c

To A Hill A/c

To capital A/c

£ 229

£ 80

£ 14652

Sept 1 Bad Debts A/c Dr.

to P Mullen A/c

(Being debt written as bad debts)

£ 105

£ 105

Sept 5 Syme Ltd.

To Office fixtures A/c

(Being Office fixtures worth 150 were

returned and full allowance was

received)

£ 150

£ 150

Sept 10 Bad Debts A/c Dr.

Cash A/c Dr.

To M. Abel A/c

(Being £ 180 received from M. Abel and

for the rest he was declared bankrupt)

£ 131

£ 180

£311

Sept 18 Machinery A/c Dr.

to Cash A/c

to Bank A/c

to Brown Ltd. A/c

(Being machinery purchased on partial

payment through cash, cheque and

remaining on credit)

£1800

£100

£500

£1200

Sept 26 Brown Ltd A/c Dr.

to bank A/c

(Being partial payment made to Brown

Ltd through cheque)

£600

£600

Sept 28 Insurance A/c Dr.

Drawings A/c Dr.

£ 60

£ 70

6

To A Hill A/c

To capital A/c

£ 229

£ 80

£ 14652

Sept 1 Bad Debts A/c Dr.

to P Mullen A/c

(Being debt written as bad debts)

£ 105

£ 105

Sept 5 Syme Ltd.

To Office fixtures A/c

(Being Office fixtures worth 150 were

returned and full allowance was

received)

£ 150

£ 150

Sept 10 Bad Debts A/c Dr.

Cash A/c Dr.

To M. Abel A/c

(Being £ 180 received from M. Abel and

for the rest he was declared bankrupt)

£ 131

£ 180

£311

Sept 18 Machinery A/c Dr.

to Cash A/c

to Bank A/c

to Brown Ltd. A/c

(Being machinery purchased on partial

payment through cash, cheque and

remaining on credit)

£1800

£100

£500

£1200

Sept 26 Brown Ltd A/c Dr.

to bank A/c

(Being partial payment made to Brown

Ltd through cheque)

£600

£600

Sept 28 Insurance A/c Dr.

Drawings A/c Dr.

£ 60

£ 70

6

To Bank A/c

(Being insurance paid for business and

the remaining for personal house)

£ 130

£ 18057 £ 18057

General Ledger of ABC enterprise, Maurice and Brothers

Journal Entries

Date Particulars Ref. Amount Amount

01/08/21 Van A/c Dr.

Office Fixtures A/c Dr.

Bank A/c Dr.

To capital A/c

(Being assets and liabilities brought in)

£ 32000

£ 1200

£ 36800

£ 70000

02/08/21 Bank A/c Dr.

to Bank loan A/c

(Being bank loan received)

£ 12400

£ 12400

03/08/21 Cash A/c Dr

To Bank A/c

(Being cash withdrawn from bank)

£ 2800

£ 2800

04/08/21 Van A/c Dr.

To Bank A/c

(Bring van purchased through cheque)

£ 6200

£6200

05/08/21 Office fixtures A/c Dr.

to Bank A/c

to Sharp Office Ltd

(Being office fixtures purchased)

£3400

£ 1000

£ 2400

08/08/21 Van A/c Dr. £8700

7

(Being insurance paid for business and

the remaining for personal house)

£ 130

£ 18057 £ 18057

General Ledger of ABC enterprise, Maurice and Brothers

Journal Entries

Date Particulars Ref. Amount Amount

01/08/21 Van A/c Dr.

Office Fixtures A/c Dr.

Bank A/c Dr.

To capital A/c

(Being assets and liabilities brought in)

£ 32000

£ 1200

£ 36800

£ 70000

02/08/21 Bank A/c Dr.

to Bank loan A/c

(Being bank loan received)

£ 12400

£ 12400

03/08/21 Cash A/c Dr

To Bank A/c

(Being cash withdrawn from bank)

£ 2800

£ 2800

04/08/21 Van A/c Dr.

To Bank A/c

(Bring van purchased through cheque)

£ 6200

£6200

05/08/21 Office fixtures A/c Dr.

to Bank A/c

to Sharp Office Ltd

(Being office fixtures purchased)

£3400

£ 1000

£ 2400

08/08/21 Van A/c Dr. £8700

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

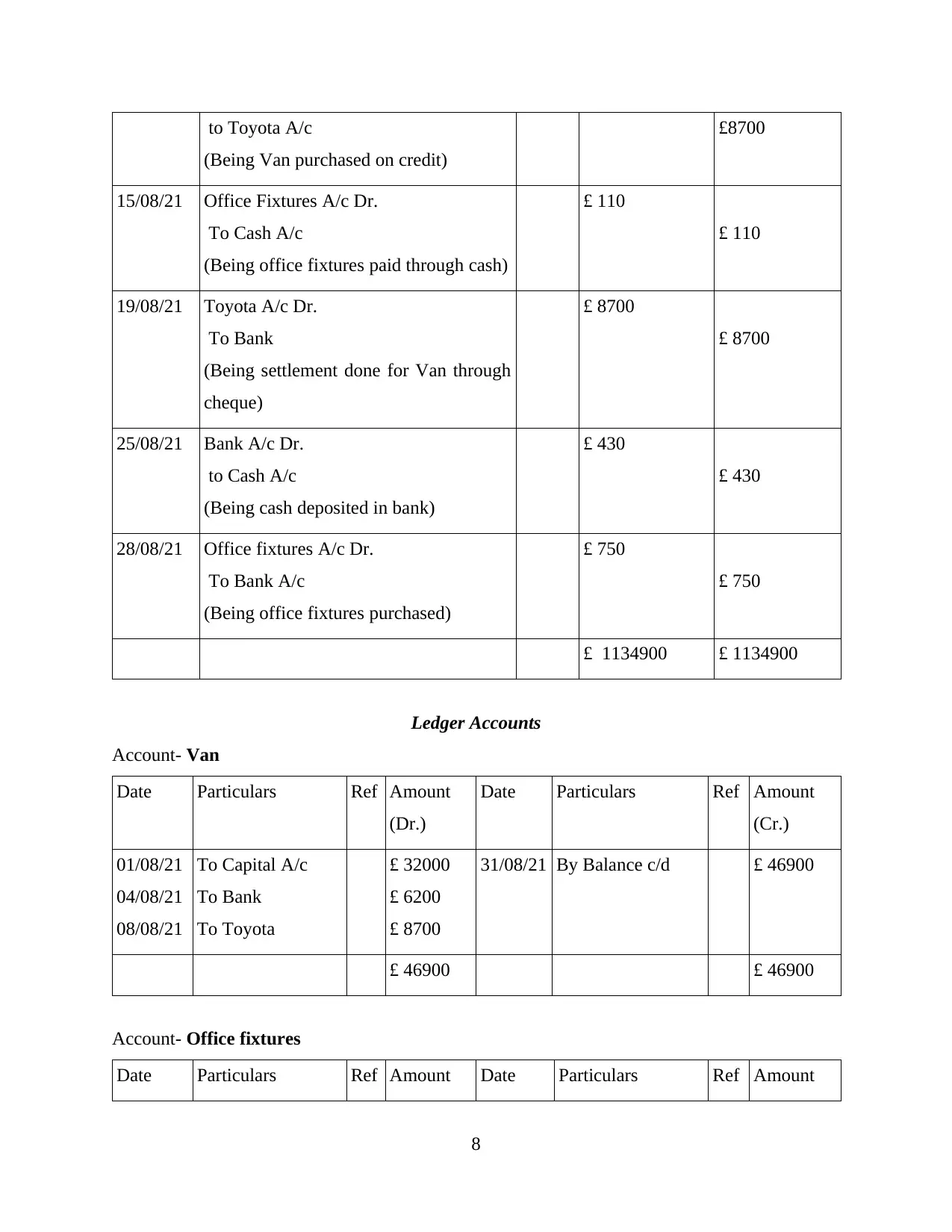

to Toyota A/c

(Being Van purchased on credit)

£8700

15/08/21 Office Fixtures A/c Dr.

To Cash A/c

(Being office fixtures paid through cash)

£ 110

£ 110

19/08/21 Toyota A/c Dr.

To Bank

(Being settlement done for Van through

cheque)

£ 8700

£ 8700

25/08/21 Bank A/c Dr.

to Cash A/c

(Being cash deposited in bank)

£ 430

£ 430

28/08/21 Office fixtures A/c Dr.

To Bank A/c

(Being office fixtures purchased)

£ 750

£ 750

£ 1134900 £ 1134900

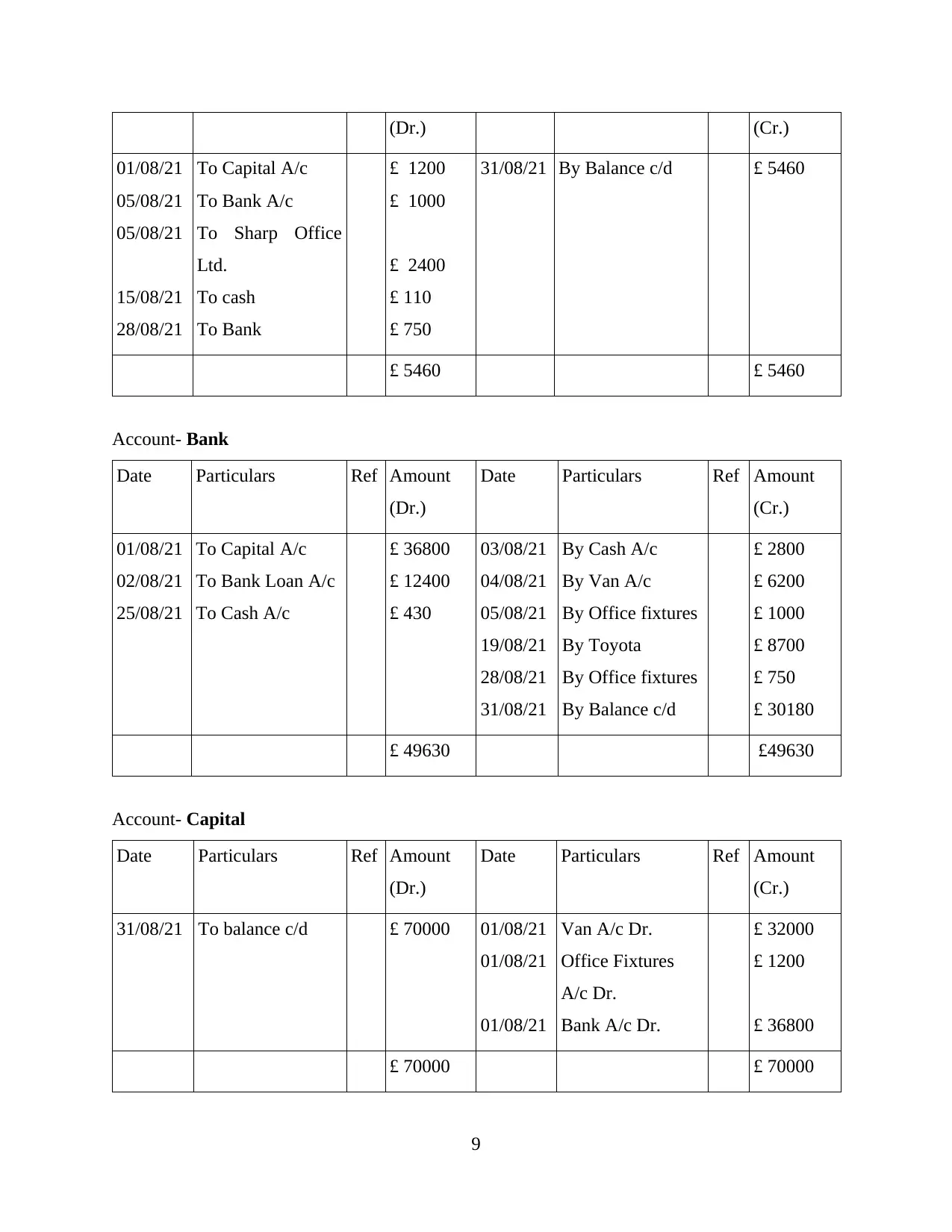

Ledger Accounts

Account- Van

Date Particulars Ref Amount

(Dr.)

Date Particulars Ref Amount

(Cr.)

01/08/21

04/08/21

08/08/21

To Capital A/c

To Bank

To Toyota

£ 32000

£ 6200

£ 8700

31/08/21 By Balance c/d £ 46900

£ 46900 £ 46900

Account- Office fixtures

Date Particulars Ref Amount Date Particulars Ref Amount

8

(Being Van purchased on credit)

£8700

15/08/21 Office Fixtures A/c Dr.

To Cash A/c

(Being office fixtures paid through cash)

£ 110

£ 110

19/08/21 Toyota A/c Dr.

To Bank

(Being settlement done for Van through

cheque)

£ 8700

£ 8700

25/08/21 Bank A/c Dr.

to Cash A/c

(Being cash deposited in bank)

£ 430

£ 430

28/08/21 Office fixtures A/c Dr.

To Bank A/c

(Being office fixtures purchased)

£ 750

£ 750

£ 1134900 £ 1134900

Ledger Accounts

Account- Van

Date Particulars Ref Amount

(Dr.)

Date Particulars Ref Amount

(Cr.)

01/08/21

04/08/21

08/08/21

To Capital A/c

To Bank

To Toyota

£ 32000

£ 6200

£ 8700

31/08/21 By Balance c/d £ 46900

£ 46900 £ 46900

Account- Office fixtures

Date Particulars Ref Amount Date Particulars Ref Amount

8

(Dr.) (Cr.)

01/08/21

05/08/21

05/08/21

15/08/21

28/08/21

To Capital A/c

To Bank A/c

To Sharp Office

Ltd.

To cash

To Bank

£ 1200

£ 1000

£ 2400

£ 110

£ 750

31/08/21 By Balance c/d £ 5460

£ 5460 £ 5460

Account- Bank

Date Particulars Ref Amount

(Dr.)

Date Particulars Ref Amount

(Cr.)

01/08/21

02/08/21

25/08/21

To Capital A/c

To Bank Loan A/c

To Cash A/c

£ 36800

£ 12400

£ 430

03/08/21

04/08/21

05/08/21

19/08/21

28/08/21

31/08/21

By Cash A/c

By Van A/c

By Office fixtures

By Toyota

By Office fixtures

By Balance c/d

£ 2800

£ 6200

£ 1000

£ 8700

£ 750

£ 30180

£ 49630 £49630

Account- Capital

Date Particulars Ref Amount

(Dr.)

Date Particulars Ref Amount

(Cr.)

31/08/21 To balance c/d £ 70000 01/08/21

01/08/21

01/08/21

Van A/c Dr.

Office Fixtures

A/c Dr.

Bank A/c Dr.

£ 32000

£ 1200

£ 36800

£ 70000 £ 70000

9

01/08/21

05/08/21

05/08/21

15/08/21

28/08/21

To Capital A/c

To Bank A/c

To Sharp Office

Ltd.

To cash

To Bank

£ 1200

£ 1000

£ 2400

£ 110

£ 750

31/08/21 By Balance c/d £ 5460

£ 5460 £ 5460

Account- Bank

Date Particulars Ref Amount

(Dr.)

Date Particulars Ref Amount

(Cr.)

01/08/21

02/08/21

25/08/21

To Capital A/c

To Bank Loan A/c

To Cash A/c

£ 36800

£ 12400

£ 430

03/08/21

04/08/21

05/08/21

19/08/21

28/08/21

31/08/21

By Cash A/c

By Van A/c

By Office fixtures

By Toyota

By Office fixtures

By Balance c/d

£ 2800

£ 6200

£ 1000

£ 8700

£ 750

£ 30180

£ 49630 £49630

Account- Capital

Date Particulars Ref Amount

(Dr.)

Date Particulars Ref Amount

(Cr.)

31/08/21 To balance c/d £ 70000 01/08/21

01/08/21

01/08/21

Van A/c Dr.

Office Fixtures

A/c Dr.

Bank A/c Dr.

£ 32000

£ 1200

£ 36800

£ 70000 £ 70000

9

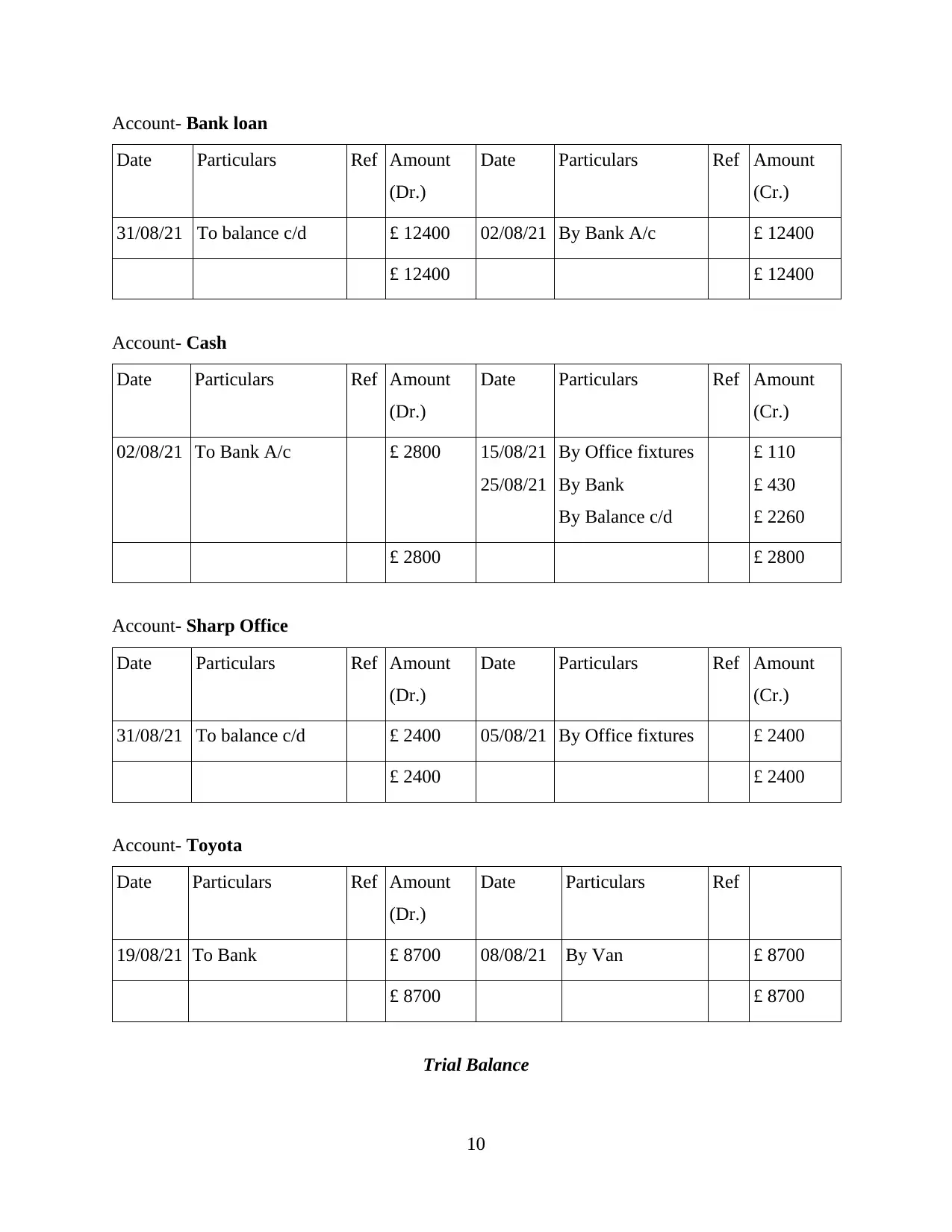

Account- Bank loan

Date Particulars Ref Amount

(Dr.)

Date Particulars Ref Amount

(Cr.)

31/08/21 To balance c/d £ 12400 02/08/21 By Bank A/c £ 12400

£ 12400 £ 12400

Account- Cash

Date Particulars Ref Amount

(Dr.)

Date Particulars Ref Amount

(Cr.)

02/08/21 To Bank A/c £ 2800 15/08/21

25/08/21

By Office fixtures

By Bank

By Balance c/d

£ 110

£ 430

£ 2260

£ 2800 £ 2800

Account- Sharp Office

Date Particulars Ref Amount

(Dr.)

Date Particulars Ref Amount

(Cr.)

31/08/21 To balance c/d £ 2400 05/08/21 By Office fixtures £ 2400

£ 2400 £ 2400

Account- Toyota

Date Particulars Ref Amount

(Dr.)

Date Particulars Ref

19/08/21 To Bank £ 8700 08/08/21 By Van £ 8700

£ 8700 £ 8700

Trial Balance

10

Date Particulars Ref Amount

(Dr.)

Date Particulars Ref Amount

(Cr.)

31/08/21 To balance c/d £ 12400 02/08/21 By Bank A/c £ 12400

£ 12400 £ 12400

Account- Cash

Date Particulars Ref Amount

(Dr.)

Date Particulars Ref Amount

(Cr.)

02/08/21 To Bank A/c £ 2800 15/08/21

25/08/21

By Office fixtures

By Bank

By Balance c/d

£ 110

£ 430

£ 2260

£ 2800 £ 2800

Account- Sharp Office

Date Particulars Ref Amount

(Dr.)

Date Particulars Ref Amount

(Cr.)

31/08/21 To balance c/d £ 2400 05/08/21 By Office fixtures £ 2400

£ 2400 £ 2400

Account- Toyota

Date Particulars Ref Amount

(Dr.)

Date Particulars Ref

19/08/21 To Bank £ 8700 08/08/21 By Van £ 8700

£ 8700 £ 8700

Trial Balance

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

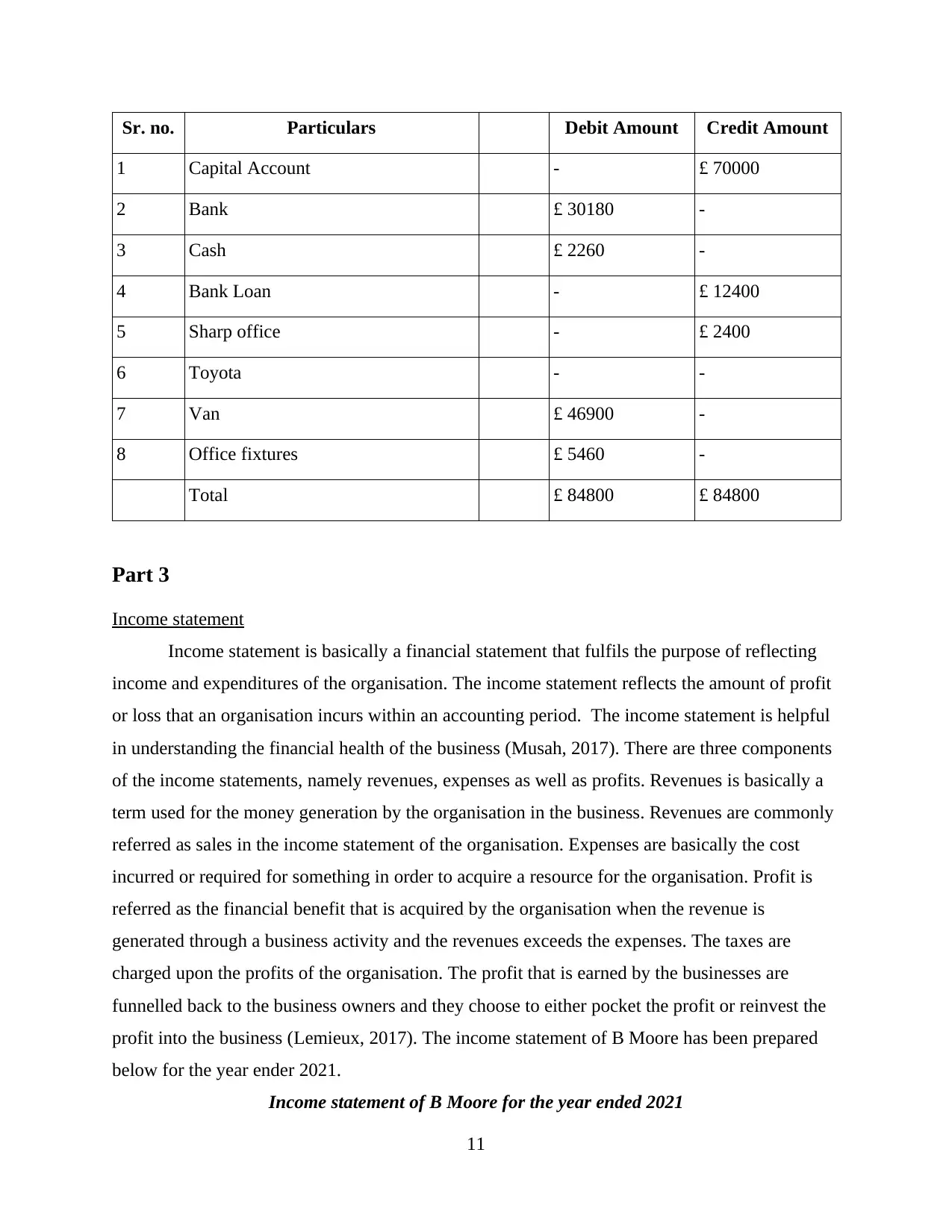

Sr. no. Particulars Debit Amount Credit Amount

1 Capital Account - £ 70000

2 Bank £ 30180 -

3 Cash £ 2260 -

4 Bank Loan - £ 12400

5 Sharp office - £ 2400

6 Toyota - -

7 Van £ 46900 -

8 Office fixtures £ 5460 -

Total £ 84800 £ 84800

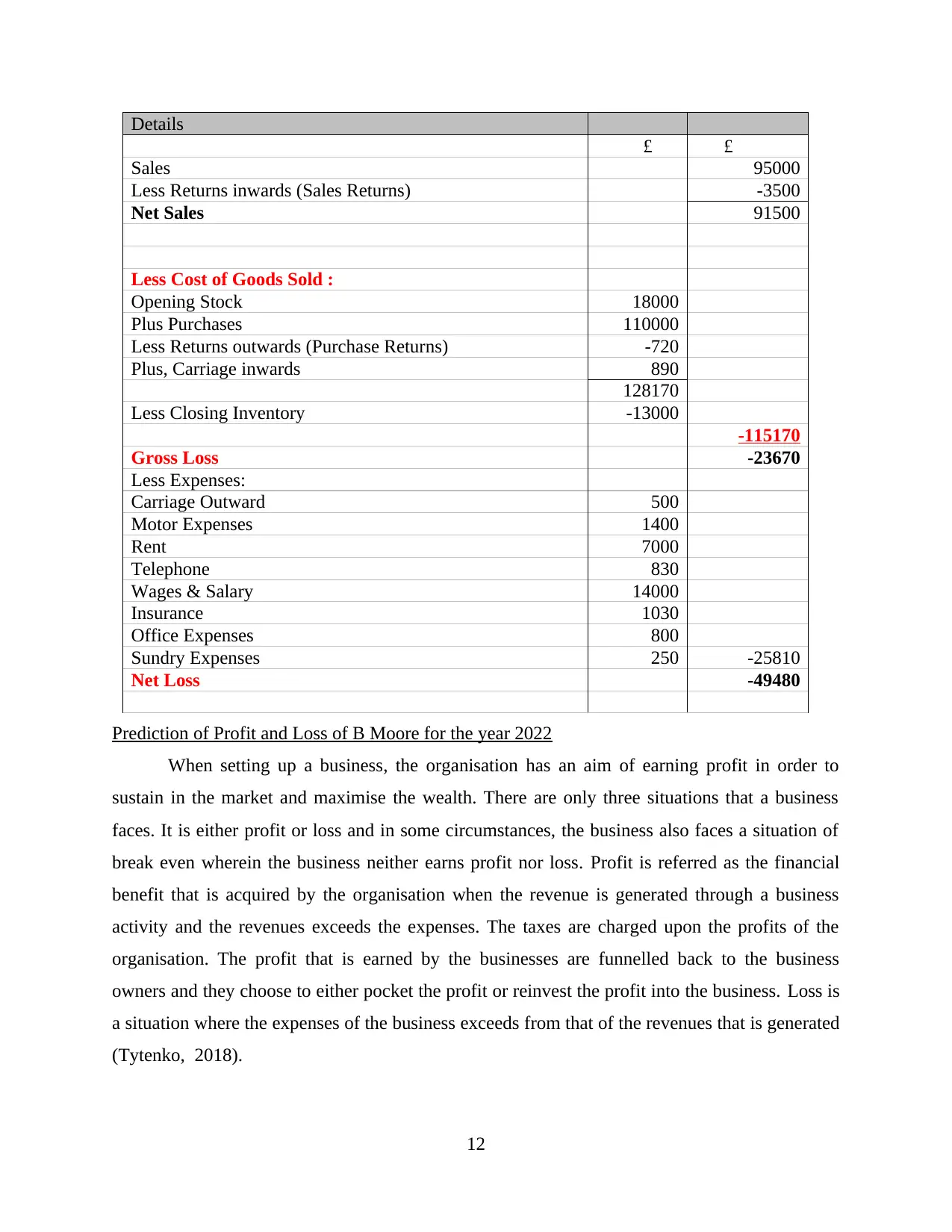

Part 3

Income statement

Income statement is basically a financial statement that fulfils the purpose of reflecting

income and expenditures of the organisation. The income statement reflects the amount of profit

or loss that an organisation incurs within an accounting period. The income statement is helpful

in understanding the financial health of the business (Musah, 2017). There are three components

of the income statements, namely revenues, expenses as well as profits. Revenues is basically a

term used for the money generation by the organisation in the business. Revenues are commonly

referred as sales in the income statement of the organisation. Expenses are basically the cost

incurred or required for something in order to acquire a resource for the organisation. Profit is

referred as the financial benefit that is acquired by the organisation when the revenue is

generated through a business activity and the revenues exceeds the expenses. The taxes are

charged upon the profits of the organisation. The profit that is earned by the businesses are

funnelled back to the business owners and they choose to either pocket the profit or reinvest the

profit into the business (Lemieux, 2017). The income statement of B Moore has been prepared

below for the year ender 2021.

Income statement of B Moore for the year ended 2021

11

1 Capital Account - £ 70000

2 Bank £ 30180 -

3 Cash £ 2260 -

4 Bank Loan - £ 12400

5 Sharp office - £ 2400

6 Toyota - -

7 Van £ 46900 -

8 Office fixtures £ 5460 -

Total £ 84800 £ 84800

Part 3

Income statement

Income statement is basically a financial statement that fulfils the purpose of reflecting

income and expenditures of the organisation. The income statement reflects the amount of profit

or loss that an organisation incurs within an accounting period. The income statement is helpful

in understanding the financial health of the business (Musah, 2017). There are three components

of the income statements, namely revenues, expenses as well as profits. Revenues is basically a

term used for the money generation by the organisation in the business. Revenues are commonly

referred as sales in the income statement of the organisation. Expenses are basically the cost

incurred or required for something in order to acquire a resource for the organisation. Profit is

referred as the financial benefit that is acquired by the organisation when the revenue is

generated through a business activity and the revenues exceeds the expenses. The taxes are

charged upon the profits of the organisation. The profit that is earned by the businesses are

funnelled back to the business owners and they choose to either pocket the profit or reinvest the

profit into the business (Lemieux, 2017). The income statement of B Moore has been prepared

below for the year ender 2021.

Income statement of B Moore for the year ended 2021

11

Details

£ £

Sales 95000

Less Returns inwards (Sales Returns) -3500

Net Sales 91500

Less Cost of Goods Sold :

Opening Stock 18000

Plus Purchases 110000

Less Returns outwards (Purchase Returns) -720

Plus, Carriage inwards 890

128170

Less Closing Inventory -13000

-115170

Gross Loss -23670

Less Expenses:

Carriage Outward 500

Motor Expenses 1400

Rent 7000

Telephone 830

Wages & Salary 14000

Insurance 1030

Office Expenses 800

Sundry Expenses 250 -25810

Net Loss -49480

Prediction of Profit and Loss of B Moore for the year 2022

When setting up a business, the organisation has an aim of earning profit in order to

sustain in the market and maximise the wealth. There are only three situations that a business

faces. It is either profit or loss and in some circumstances, the business also faces a situation of

break even wherein the business neither earns profit nor loss. Profit is referred as the financial

benefit that is acquired by the organisation when the revenue is generated through a business

activity and the revenues exceeds the expenses. The taxes are charged upon the profits of the

organisation. The profit that is earned by the businesses are funnelled back to the business

owners and they choose to either pocket the profit or reinvest the profit into the business. Loss is

a situation where the expenses of the business exceeds from that of the revenues that is generated

(Tytenko, 2018).

12

£ £

Sales 95000

Less Returns inwards (Sales Returns) -3500

Net Sales 91500

Less Cost of Goods Sold :

Opening Stock 18000

Plus Purchases 110000

Less Returns outwards (Purchase Returns) -720

Plus, Carriage inwards 890

128170

Less Closing Inventory -13000

-115170

Gross Loss -23670

Less Expenses:

Carriage Outward 500

Motor Expenses 1400

Rent 7000

Telephone 830

Wages & Salary 14000

Insurance 1030

Office Expenses 800

Sundry Expenses 250 -25810

Net Loss -49480

Prediction of Profit and Loss of B Moore for the year 2022

When setting up a business, the organisation has an aim of earning profit in order to

sustain in the market and maximise the wealth. There are only three situations that a business

faces. It is either profit or loss and in some circumstances, the business also faces a situation of

break even wherein the business neither earns profit nor loss. Profit is referred as the financial

benefit that is acquired by the organisation when the revenue is generated through a business

activity and the revenues exceeds the expenses. The taxes are charged upon the profits of the

organisation. The profit that is earned by the businesses are funnelled back to the business

owners and they choose to either pocket the profit or reinvest the profit into the business. Loss is

a situation where the expenses of the business exceeds from that of the revenues that is generated

(Tytenko, 2018).

12

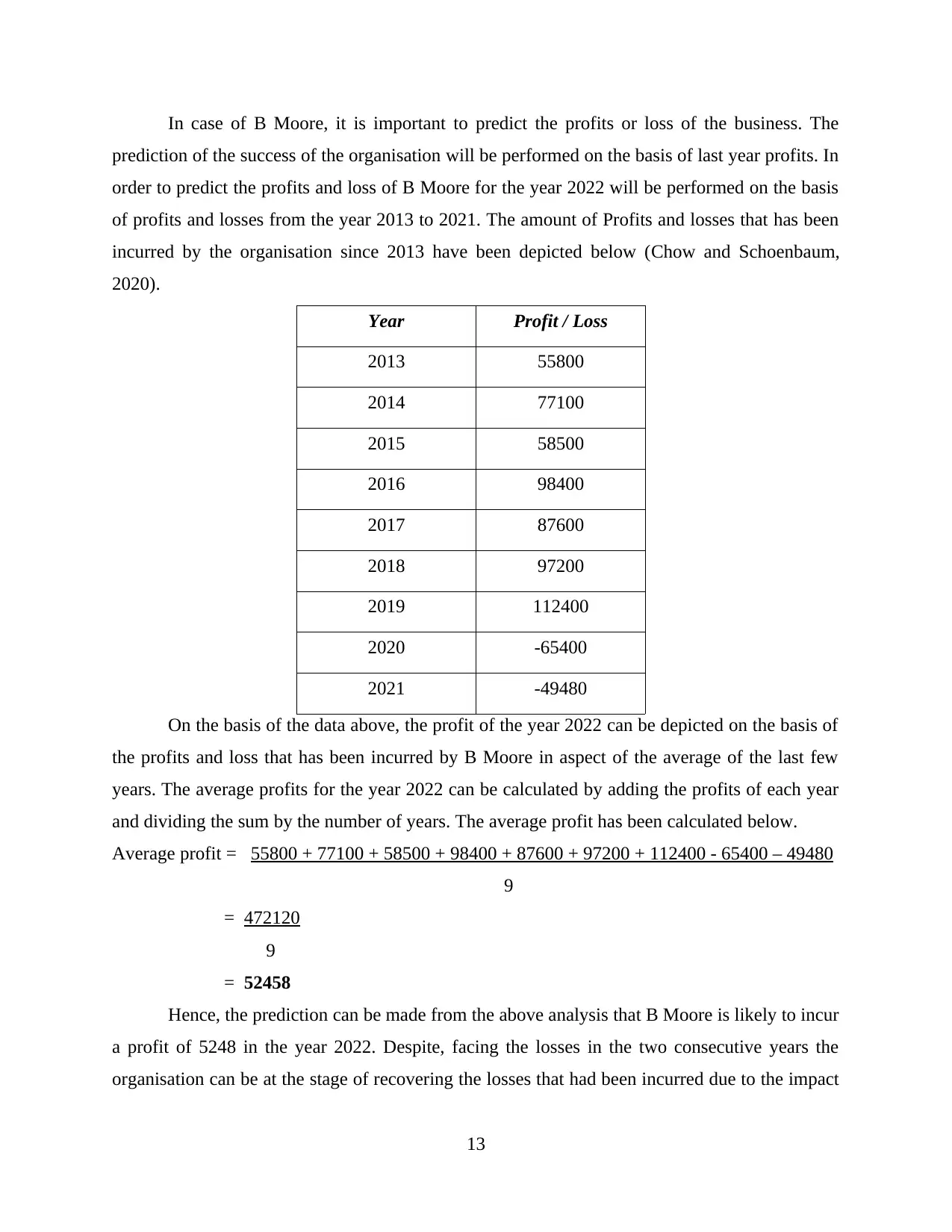

In case of B Moore, it is important to predict the profits or loss of the business. The

prediction of the success of the organisation will be performed on the basis of last year profits. In

order to predict the profits and loss of B Moore for the year 2022 will be performed on the basis

of profits and losses from the year 2013 to 2021. The amount of Profits and losses that has been

incurred by the organisation since 2013 have been depicted below (Chow and Schoenbaum,

2020).

Year Profit / Loss

2013 55800

2014 77100

2015 58500

2016 98400

2017 87600

2018 97200

2019 112400

2020 -65400

2021 -49480

On the basis of the data above, the profit of the year 2022 can be depicted on the basis of

the profits and loss that has been incurred by B Moore in aspect of the average of the last few

years. The average profits for the year 2022 can be calculated by adding the profits of each year

and dividing the sum by the number of years. The average profit has been calculated below.

Average profit = 55800 + 77100 + 58500 + 98400 + 87600 + 97200 + 112400 - 65400 – 49480

9

= 472120

9

= 52458

Hence, the prediction can be made from the above analysis that B Moore is likely to incur

a profit of 5248 in the year 2022. Despite, facing the losses in the two consecutive years the

organisation can be at the stage of recovering the losses that had been incurred due to the impact

13

prediction of the success of the organisation will be performed on the basis of last year profits. In

order to predict the profits and loss of B Moore for the year 2022 will be performed on the basis

of profits and losses from the year 2013 to 2021. The amount of Profits and losses that has been

incurred by the organisation since 2013 have been depicted below (Chow and Schoenbaum,

2020).

Year Profit / Loss

2013 55800

2014 77100

2015 58500

2016 98400

2017 87600

2018 97200

2019 112400

2020 -65400

2021 -49480

On the basis of the data above, the profit of the year 2022 can be depicted on the basis of

the profits and loss that has been incurred by B Moore in aspect of the average of the last few

years. The average profits for the year 2022 can be calculated by adding the profits of each year

and dividing the sum by the number of years. The average profit has been calculated below.

Average profit = 55800 + 77100 + 58500 + 98400 + 87600 + 97200 + 112400 - 65400 – 49480

9

= 472120

9

= 52458

Hence, the prediction can be made from the above analysis that B Moore is likely to incur

a profit of 5248 in the year 2022. Despite, facing the losses in the two consecutive years the

organisation can be at the stage of recovering the losses that had been incurred due to the impact

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

of pandemic. As now the situations are turning back to normal, the situation is likely to turn

positive for B Moore as well (Durach And et.al., 2021).

Conclusion

It can be concluded from the above report that it is essential for every organisation to

record its business transactions. The recording of transaction comprises of financial statement

and it is a key responsibility of every accounting department. In order to record a specific

transaction, it is very important to understand a transaction while understanding the importance

of each transaction. The recording of business transaction are helpful in determining the financial

position of the organisation. The report has discussed the various steps for establishing a

business as a decorator. Further the report has also highlighted various decision makers in an

organisation. The part C of the assessment report comprises of the income statement for the

organisation of the year 2021. Further, the prediction of profit and loss for the year 2022 has

been made in accordance of the profits and loss incurred by the organisation from 2013 to 2021.

14

positive for B Moore as well (Durach And et.al., 2021).

Conclusion

It can be concluded from the above report that it is essential for every organisation to

record its business transactions. The recording of transaction comprises of financial statement

and it is a key responsibility of every accounting department. In order to record a specific

transaction, it is very important to understand a transaction while understanding the importance

of each transaction. The recording of business transaction are helpful in determining the financial

position of the organisation. The report has discussed the various steps for establishing a

business as a decorator. Further the report has also highlighted various decision makers in an

organisation. The part C of the assessment report comprises of the income statement for the

organisation of the year 2021. Further, the prediction of profit and loss for the year 2022 has

been made in accordance of the profits and loss incurred by the organisation from 2013 to 2021.

14

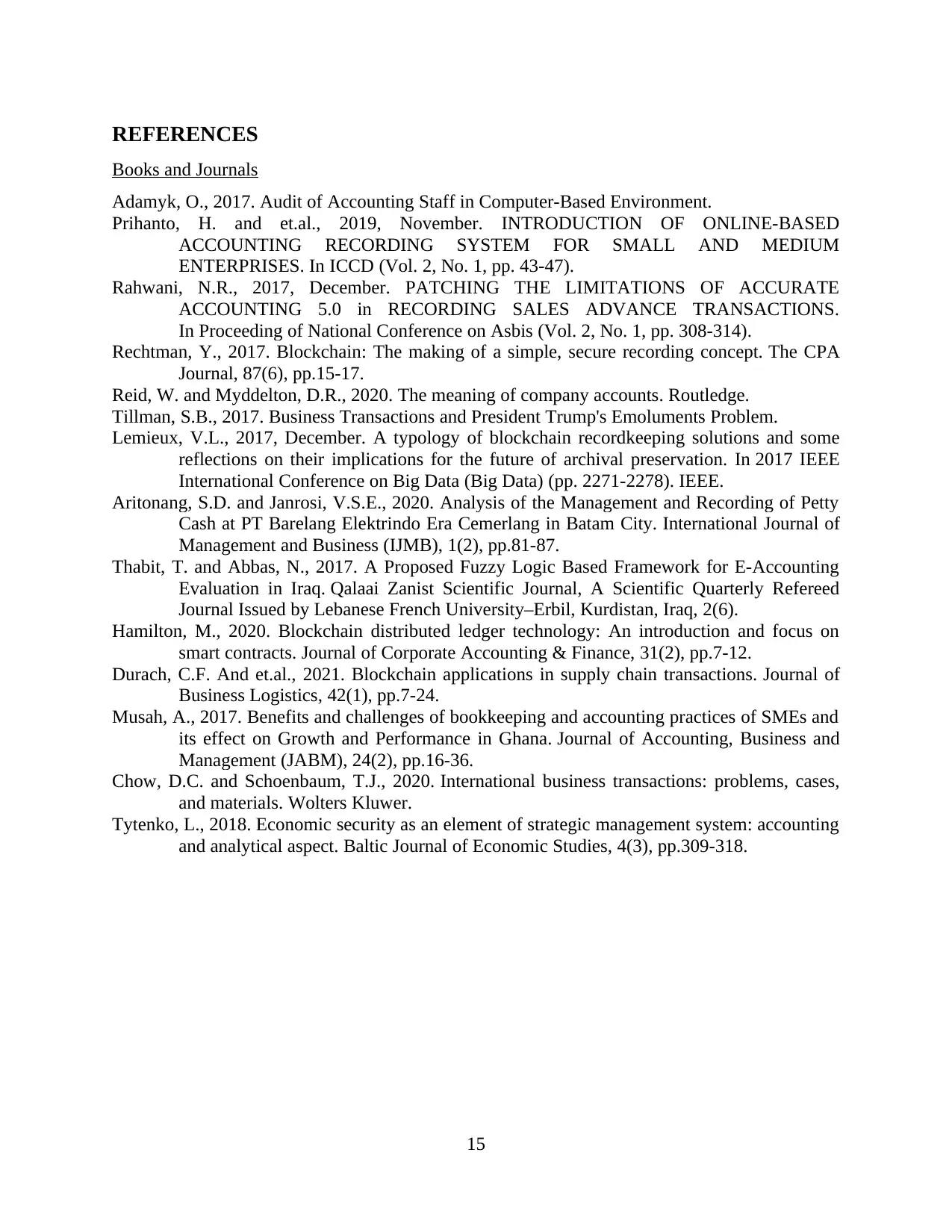

REFERENCES

Books and Journals

Adamyk, O., 2017. Audit of Accounting Staff in Computer-Based Environment.

Prihanto, H. and et.al., 2019, November. INTRODUCTION OF ONLINE-BASED

ACCOUNTING RECORDING SYSTEM FOR SMALL AND MEDIUM

ENTERPRISES. In ICCD (Vol. 2, No. 1, pp. 43-47).

Rahwani, N.R., 2017, December. PATCHING THE LIMITATIONS OF ACCURATE

ACCOUNTING 5.0 in RECORDING SALES ADVANCE TRANSACTIONS.

In Proceeding of National Conference on Asbis (Vol. 2, No. 1, pp. 308-314).

Rechtman, Y., 2017. Blockchain: The making of a simple, secure recording concept. The CPA

Journal, 87(6), pp.15-17.

Reid, W. and Myddelton, D.R., 2020. The meaning of company accounts. Routledge.

Tillman, S.B., 2017. Business Transactions and President Trump's Emoluments Problem.

Lemieux, V.L., 2017, December. A typology of blockchain recordkeeping solutions and some

reflections on their implications for the future of archival preservation. In 2017 IEEE

International Conference on Big Data (Big Data) (pp. 2271-2278). IEEE.

Aritonang, S.D. and Janrosi, V.S.E., 2020. Analysis of the Management and Recording of Petty

Cash at PT Barelang Elektrindo Era Cemerlang in Batam City. International Journal of

Management and Business (IJMB), 1(2), pp.81-87.

Thabit, T. and Abbas, N., 2017. A Proposed Fuzzy Logic Based Framework for E-Accounting

Evaluation in Iraq. Qalaai Zanist Scientific Journal, A Scientific Quarterly Refereed

Journal Issued by Lebanese French University–Erbil, Kurdistan, Iraq, 2(6).

Hamilton, M., 2020. Blockchain distributed ledger technology: An introduction and focus on

smart contracts. Journal of Corporate Accounting & Finance, 31(2), pp.7-12.

Durach, C.F. And et.al., 2021. Blockchain applications in supply chain transactions. Journal of

Business Logistics, 42(1), pp.7-24.

Musah, A., 2017. Benefits and challenges of bookkeeping and accounting practices of SMEs and

its effect on Growth and Performance in Ghana. Journal of Accounting, Business and

Management (JABM), 24(2), pp.16-36.

Chow, D.C. and Schoenbaum, T.J., 2020. International business transactions: problems, cases,

and materials. Wolters Kluwer.

Tytenko, L., 2018. Economic security as an element of strategic management system: accounting

and analytical aspect. Baltic Journal of Economic Studies, 4(3), pp.309-318.

15

Books and Journals

Adamyk, O., 2017. Audit of Accounting Staff in Computer-Based Environment.

Prihanto, H. and et.al., 2019, November. INTRODUCTION OF ONLINE-BASED

ACCOUNTING RECORDING SYSTEM FOR SMALL AND MEDIUM

ENTERPRISES. In ICCD (Vol. 2, No. 1, pp. 43-47).

Rahwani, N.R., 2017, December. PATCHING THE LIMITATIONS OF ACCURATE

ACCOUNTING 5.0 in RECORDING SALES ADVANCE TRANSACTIONS.

In Proceeding of National Conference on Asbis (Vol. 2, No. 1, pp. 308-314).

Rechtman, Y., 2017. Blockchain: The making of a simple, secure recording concept. The CPA

Journal, 87(6), pp.15-17.

Reid, W. and Myddelton, D.R., 2020. The meaning of company accounts. Routledge.

Tillman, S.B., 2017. Business Transactions and President Trump's Emoluments Problem.

Lemieux, V.L., 2017, December. A typology of blockchain recordkeeping solutions and some

reflections on their implications for the future of archival preservation. In 2017 IEEE

International Conference on Big Data (Big Data) (pp. 2271-2278). IEEE.

Aritonang, S.D. and Janrosi, V.S.E., 2020. Analysis of the Management and Recording of Petty

Cash at PT Barelang Elektrindo Era Cemerlang in Batam City. International Journal of

Management and Business (IJMB), 1(2), pp.81-87.

Thabit, T. and Abbas, N., 2017. A Proposed Fuzzy Logic Based Framework for E-Accounting

Evaluation in Iraq. Qalaai Zanist Scientific Journal, A Scientific Quarterly Refereed

Journal Issued by Lebanese French University–Erbil, Kurdistan, Iraq, 2(6).

Hamilton, M., 2020. Blockchain distributed ledger technology: An introduction and focus on

smart contracts. Journal of Corporate Accounting & Finance, 31(2), pp.7-12.

Durach, C.F. And et.al., 2021. Blockchain applications in supply chain transactions. Journal of

Business Logistics, 42(1), pp.7-24.

Musah, A., 2017. Benefits and challenges of bookkeeping and accounting practices of SMEs and

its effect on Growth and Performance in Ghana. Journal of Accounting, Business and

Management (JABM), 24(2), pp.16-36.

Chow, D.C. and Schoenbaum, T.J., 2020. International business transactions: problems, cases,

and materials. Wolters Kluwer.

Tytenko, L., 2018. Economic security as an element of strategic management system: accounting

and analytical aspect. Baltic Journal of Economic Studies, 4(3), pp.309-318.

15

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.