BA30592E: Recording Business Transactions Assignment Analysis

VerifiedAdded on 2022/12/26

|16

|2691

|46

Homework Assignment

AI Summary

This assignment solution, prepared for a University of West London course, focuses on recording business transactions, preparing financial statements, and performing ratio analysis for a small toy business. The solution meticulously details the journal entries, ledger accounts, trial balance, profit and loss account, and balance sheet for Linda's toy business, covering transactions such as purchases, sales, returns, and expenses. Furthermore, the assignment includes a letter explaining the treatment of drawings and calculates various financial ratios, comparing Linda's business performance with a competitor's, highlighting areas for improvement. The analysis emphasizes the importance of financial accounting in assessing a company's profitability and solvency, providing a comprehensive overview of the financial health of the business.

RECORDING BUSINESS

TRANSACTION

TRANSACTION

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

Recording transaction.................................................................................................................3

Balancing the account.................................................................................................................3

Extraction of trial balance...........................................................................................................7

Preparation of profit and loss account.........................................................................................8

Making financial position statement...........................................................................................9

Letter explaining drawings relating to small business..............................................................10

PART B..........................................................................................................................................10

Calculation of various ratios of business..................................................................................10

Analysis and comparison of the ratios with its competitor.......................................................11

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

Recording transaction.................................................................................................................3

Balancing the account.................................................................................................................3

Extraction of trial balance...........................................................................................................7

Preparation of profit and loss account.........................................................................................8

Making financial position statement...........................................................................................9

Letter explaining drawings relating to small business..............................................................10

PART B..........................................................................................................................................10

Calculation of various ratios of business..................................................................................10

Analysis and comparison of the ratios with its competitor.......................................................11

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

For analysing success of the business accounting is very essential as it assist company in

calculating the profitability of business. Accounting is defined as the process through which

transaction of financial nature are being recorded and then posted in ledger for analysing and

assessing the financial position and profitability of the company. Present report is also based on

assessing the financial health and position of the company. For this process will start by

recording the transaction in journal and then posting them in order to make trial balance. Further

with help of the trial balance profit and loss and balance sheet will be prepared. In the end use of

ratio analysis will be done for analysing the actual profitability and solvency of the business

against the industry competitors.

PART A

Recording transaction

Recording business transaction is defined as listing out all the financial transaction and

recording them in the books of account. The recording is done in the books of account wherein

all the financial transactions are being recorded within the books. This is done in order to assess

the fact that all the transactions are being recorded in proper and effective manner so that it can

be carried forward and posted in ledger (Hanifatunnisa and Rahardjo, 2017). If the recording is

wrong, then complete transaction and its impact will affect the whole profitability of company to

a great extent.

Journal is attached in appendix

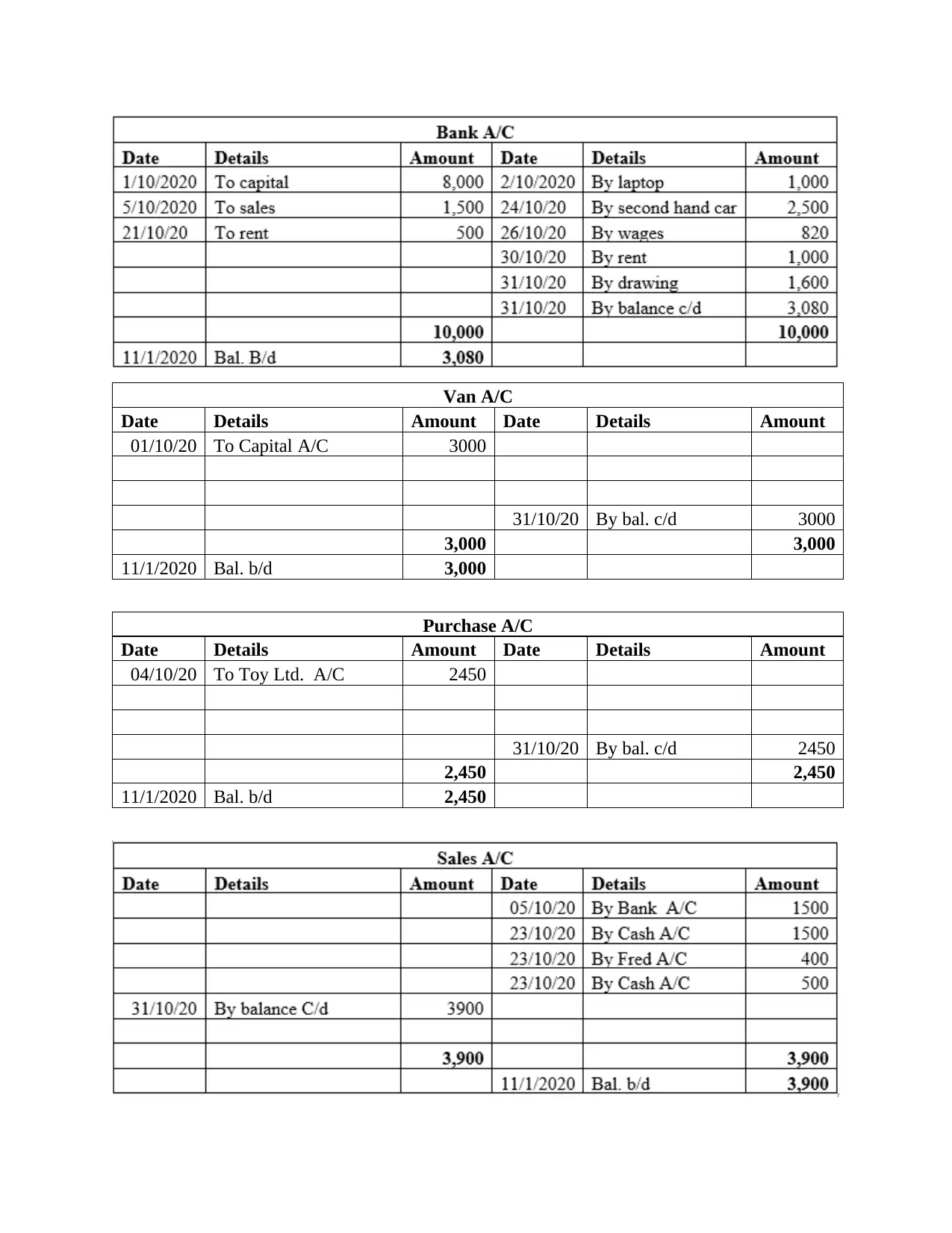

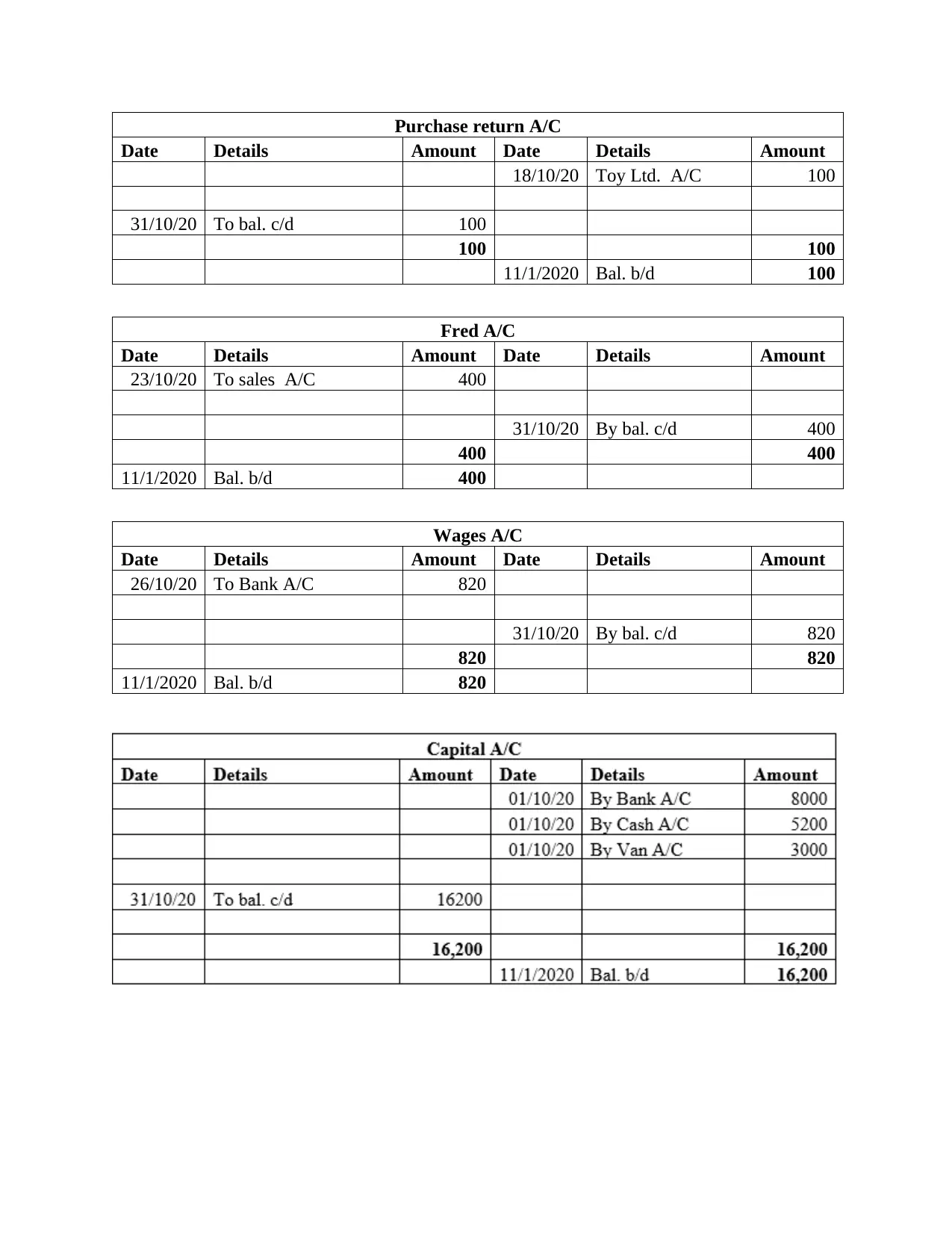

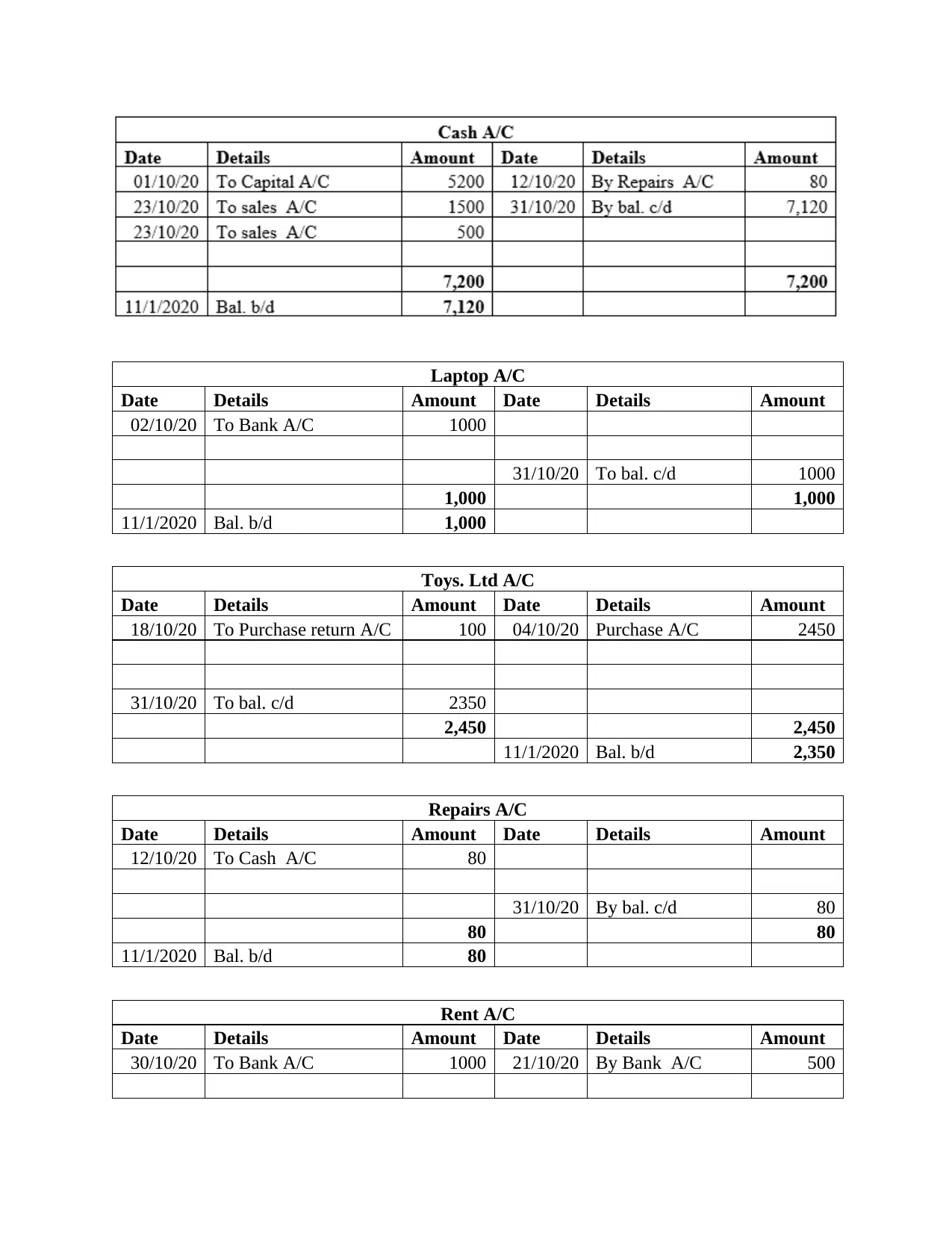

Balancing the account

After recording the business transaction in books of account, all the entries are posted in

leader accounts. This is a process through which all the journal entries are being posted in their

individual accounts (Basic accounting, 2021). Under this all the transaction are being posted and

then it is balanced and carried forward in making trial balance.

For analysing success of the business accounting is very essential as it assist company in

calculating the profitability of business. Accounting is defined as the process through which

transaction of financial nature are being recorded and then posted in ledger for analysing and

assessing the financial position and profitability of the company. Present report is also based on

assessing the financial health and position of the company. For this process will start by

recording the transaction in journal and then posting them in order to make trial balance. Further

with help of the trial balance profit and loss and balance sheet will be prepared. In the end use of

ratio analysis will be done for analysing the actual profitability and solvency of the business

against the industry competitors.

PART A

Recording transaction

Recording business transaction is defined as listing out all the financial transaction and

recording them in the books of account. The recording is done in the books of account wherein

all the financial transactions are being recorded within the books. This is done in order to assess

the fact that all the transactions are being recorded in proper and effective manner so that it can

be carried forward and posted in ledger (Hanifatunnisa and Rahardjo, 2017). If the recording is

wrong, then complete transaction and its impact will affect the whole profitability of company to

a great extent.

Journal is attached in appendix

Balancing the account

After recording the business transaction in books of account, all the entries are posted in

leader accounts. This is a process through which all the journal entries are being posted in their

individual accounts (Basic accounting, 2021). Under this all the transaction are being posted and

then it is balanced and carried forward in making trial balance.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Van A/C

Date Details Amount Date Details Amount

01/10/20 To Capital A/C 3000

31/10/20 By bal. c/d 3000

3,000 3,000

11/1/2020 Bal. b/d 3,000

Purchase A/C

Date Details Amount Date Details Amount

04/10/20 To Toy Ltd. A/C 2450

31/10/20 By bal. c/d 2450

2,450 2,450

11/1/2020 Bal. b/d 2,450

Date Details Amount Date Details Amount

01/10/20 To Capital A/C 3000

31/10/20 By bal. c/d 3000

3,000 3,000

11/1/2020 Bal. b/d 3,000

Purchase A/C

Date Details Amount Date Details Amount

04/10/20 To Toy Ltd. A/C 2450

31/10/20 By bal. c/d 2450

2,450 2,450

11/1/2020 Bal. b/d 2,450

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Purchase return A/C

Date Details Amount Date Details Amount

18/10/20 Toy Ltd. A/C 100

31/10/20 To bal. c/d 100

100 100

11/1/2020 Bal. b/d 100

Fred A/C

Date Details Amount Date Details Amount

23/10/20 To sales A/C 400

31/10/20 By bal. c/d 400

400 400

11/1/2020 Bal. b/d 400

Wages A/C

Date Details Amount Date Details Amount

26/10/20 To Bank A/C 820

31/10/20 By bal. c/d 820

820 820

11/1/2020 Bal. b/d 820

Date Details Amount Date Details Amount

18/10/20 Toy Ltd. A/C 100

31/10/20 To bal. c/d 100

100 100

11/1/2020 Bal. b/d 100

Fred A/C

Date Details Amount Date Details Amount

23/10/20 To sales A/C 400

31/10/20 By bal. c/d 400

400 400

11/1/2020 Bal. b/d 400

Wages A/C

Date Details Amount Date Details Amount

26/10/20 To Bank A/C 820

31/10/20 By bal. c/d 820

820 820

11/1/2020 Bal. b/d 820

Laptop A/C

Date Details Amount Date Details Amount

02/10/20 To Bank A/C 1000

31/10/20 To bal. c/d 1000

1,000 1,000

11/1/2020 Bal. b/d 1,000

Toys. Ltd A/C

Date Details Amount Date Details Amount

18/10/20 To Purchase return A/C 100 04/10/20 Purchase A/C 2450

31/10/20 To bal. c/d 2350

2,450 2,450

11/1/2020 Bal. b/d 2,350

Repairs A/C

Date Details Amount Date Details Amount

12/10/20 To Cash A/C 80

31/10/20 By bal. c/d 80

80 80

11/1/2020 Bal. b/d 80

Rent A/C

Date Details Amount Date Details Amount

30/10/20 To Bank A/C 1000 21/10/20 By Bank A/C 500

Date Details Amount Date Details Amount

02/10/20 To Bank A/C 1000

31/10/20 To bal. c/d 1000

1,000 1,000

11/1/2020 Bal. b/d 1,000

Toys. Ltd A/C

Date Details Amount Date Details Amount

18/10/20 To Purchase return A/C 100 04/10/20 Purchase A/C 2450

31/10/20 To bal. c/d 2350

2,450 2,450

11/1/2020 Bal. b/d 2,350

Repairs A/C

Date Details Amount Date Details Amount

12/10/20 To Cash A/C 80

31/10/20 By bal. c/d 80

80 80

11/1/2020 Bal. b/d 80

Rent A/C

Date Details Amount Date Details Amount

30/10/20 To Bank A/C 1000 21/10/20 By Bank A/C 500

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

31/10/20 By bal. c/d 500

1,000 1,000

11/1/2020 Bal. b/d 500

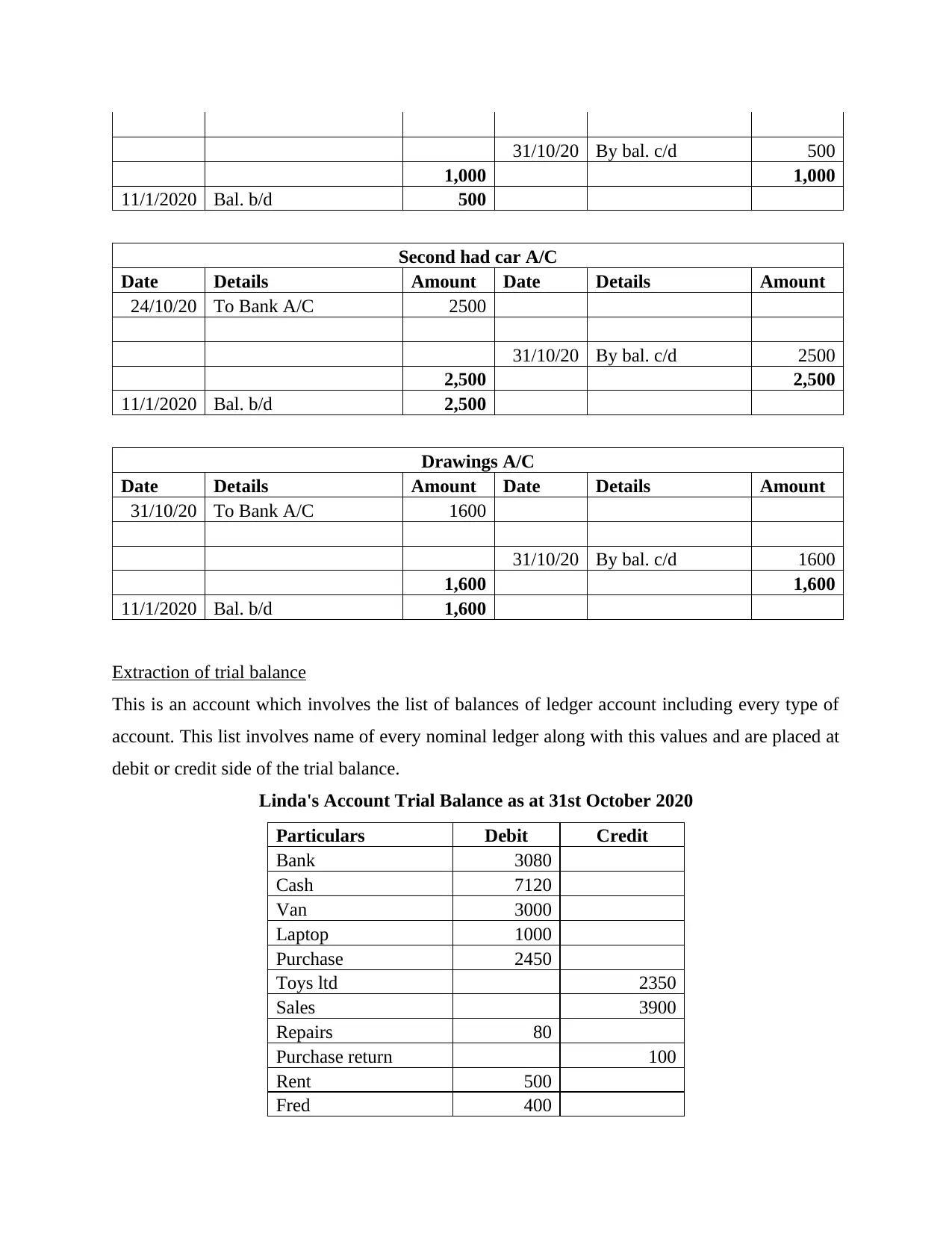

Second had car A/C

Date Details Amount Date Details Amount

24/10/20 To Bank A/C 2500

31/10/20 By bal. c/d 2500

2,500 2,500

11/1/2020 Bal. b/d 2,500

Drawings A/C

Date Details Amount Date Details Amount

31/10/20 To Bank A/C 1600

31/10/20 By bal. c/d 1600

1,600 1,600

11/1/2020 Bal. b/d 1,600

Extraction of trial balance

This is an account which involves the list of balances of ledger account including every type of

account. This list involves name of every nominal ledger along with this values and are placed at

debit or credit side of the trial balance.

Linda's Account Trial Balance as at 31st October 2020

Particulars Debit Credit

Bank 3080

Cash 7120

Van 3000

Laptop 1000

Purchase 2450

Toys ltd 2350

Sales 3900

Repairs 80

Purchase return 100

Rent 500

Fred 400

1,000 1,000

11/1/2020 Bal. b/d 500

Second had car A/C

Date Details Amount Date Details Amount

24/10/20 To Bank A/C 2500

31/10/20 By bal. c/d 2500

2,500 2,500

11/1/2020 Bal. b/d 2,500

Drawings A/C

Date Details Amount Date Details Amount

31/10/20 To Bank A/C 1600

31/10/20 By bal. c/d 1600

1,600 1,600

11/1/2020 Bal. b/d 1,600

Extraction of trial balance

This is an account which involves the list of balances of ledger account including every type of

account. This list involves name of every nominal ledger along with this values and are placed at

debit or credit side of the trial balance.

Linda's Account Trial Balance as at 31st October 2020

Particulars Debit Credit

Bank 3080

Cash 7120

Van 3000

Laptop 1000

Purchase 2450

Toys ltd 2350

Sales 3900

Repairs 80

Purchase return 100

Rent 500

Fred 400

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

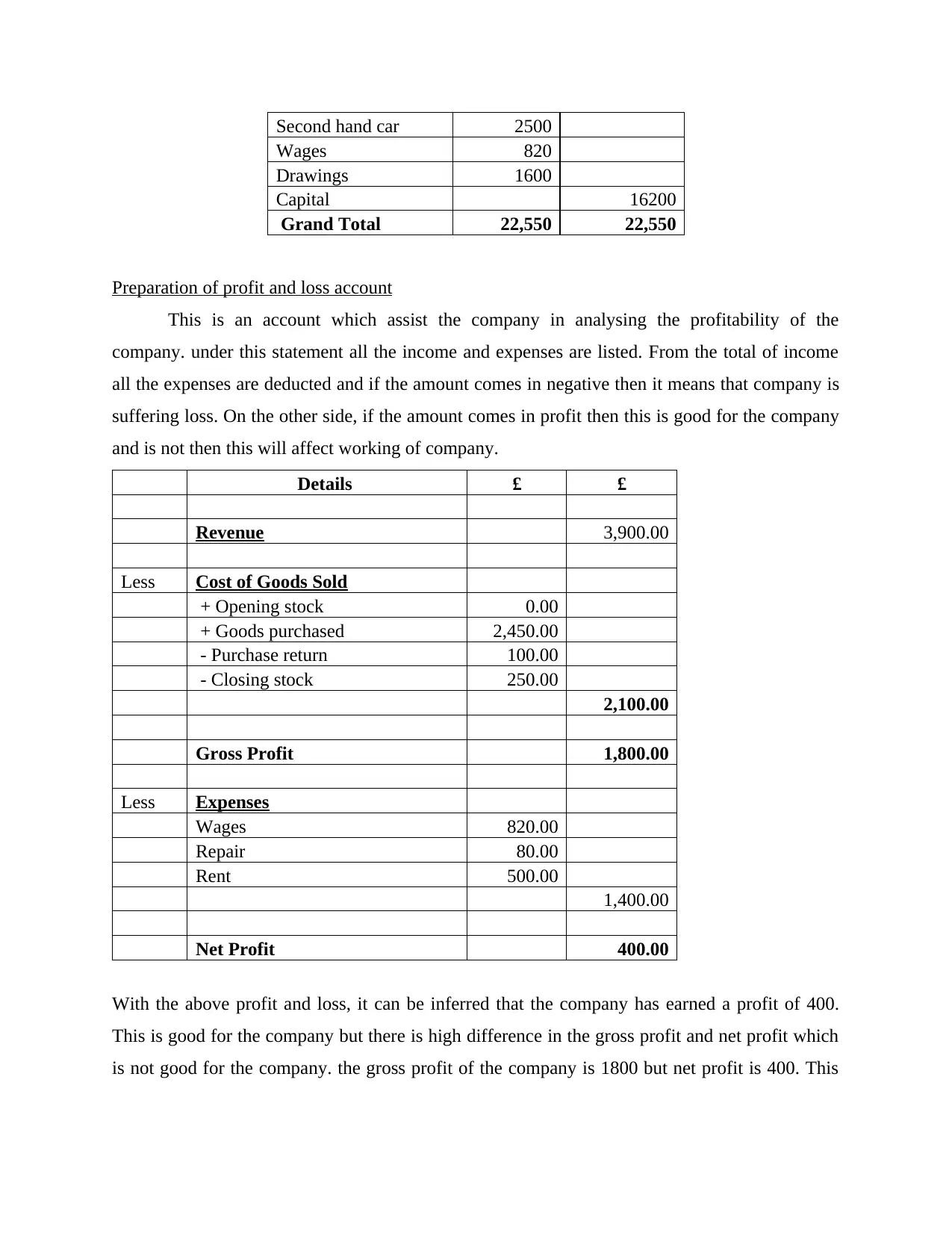

Second hand car 2500

Wages 820

Drawings 1600

Capital 16200

Grand Total 22,550 22,550

Preparation of profit and loss account

This is an account which assist the company in analysing the profitability of the

company. under this statement all the income and expenses are listed. From the total of income

all the expenses are deducted and if the amount comes in negative then it means that company is

suffering loss. On the other side, if the amount comes in profit then this is good for the company

and is not then this will affect working of company.

Details £ £

Revenue 3,900.00

Less Cost of Goods Sold

+ Opening stock 0.00

+ Goods purchased 2,450.00

- Purchase return 100.00

- Closing stock 250.00

2,100.00

Gross Profit 1,800.00

Less Expenses

Wages 820.00

Repair 80.00

Rent 500.00

1,400.00

Net Profit 400.00

With the above profit and loss, it can be inferred that the company has earned a profit of 400.

This is good for the company but there is high difference in the gross profit and net profit which

is not good for the company. the gross profit of the company is 1800 but net profit is 400. This

Wages 820

Drawings 1600

Capital 16200

Grand Total 22,550 22,550

Preparation of profit and loss account

This is an account which assist the company in analysing the profitability of the

company. under this statement all the income and expenses are listed. From the total of income

all the expenses are deducted and if the amount comes in negative then it means that company is

suffering loss. On the other side, if the amount comes in profit then this is good for the company

and is not then this will affect working of company.

Details £ £

Revenue 3,900.00

Less Cost of Goods Sold

+ Opening stock 0.00

+ Goods purchased 2,450.00

- Purchase return 100.00

- Closing stock 250.00

2,100.00

Gross Profit 1,800.00

Less Expenses

Wages 820.00

Repair 80.00

Rent 500.00

1,400.00

Net Profit 400.00

With the above profit and loss, it can be inferred that the company has earned a profit of 400.

This is good for the company but there is high difference in the gross profit and net profit which

is not good for the company. the gross profit of the company is 1800 but net profit is 400. This

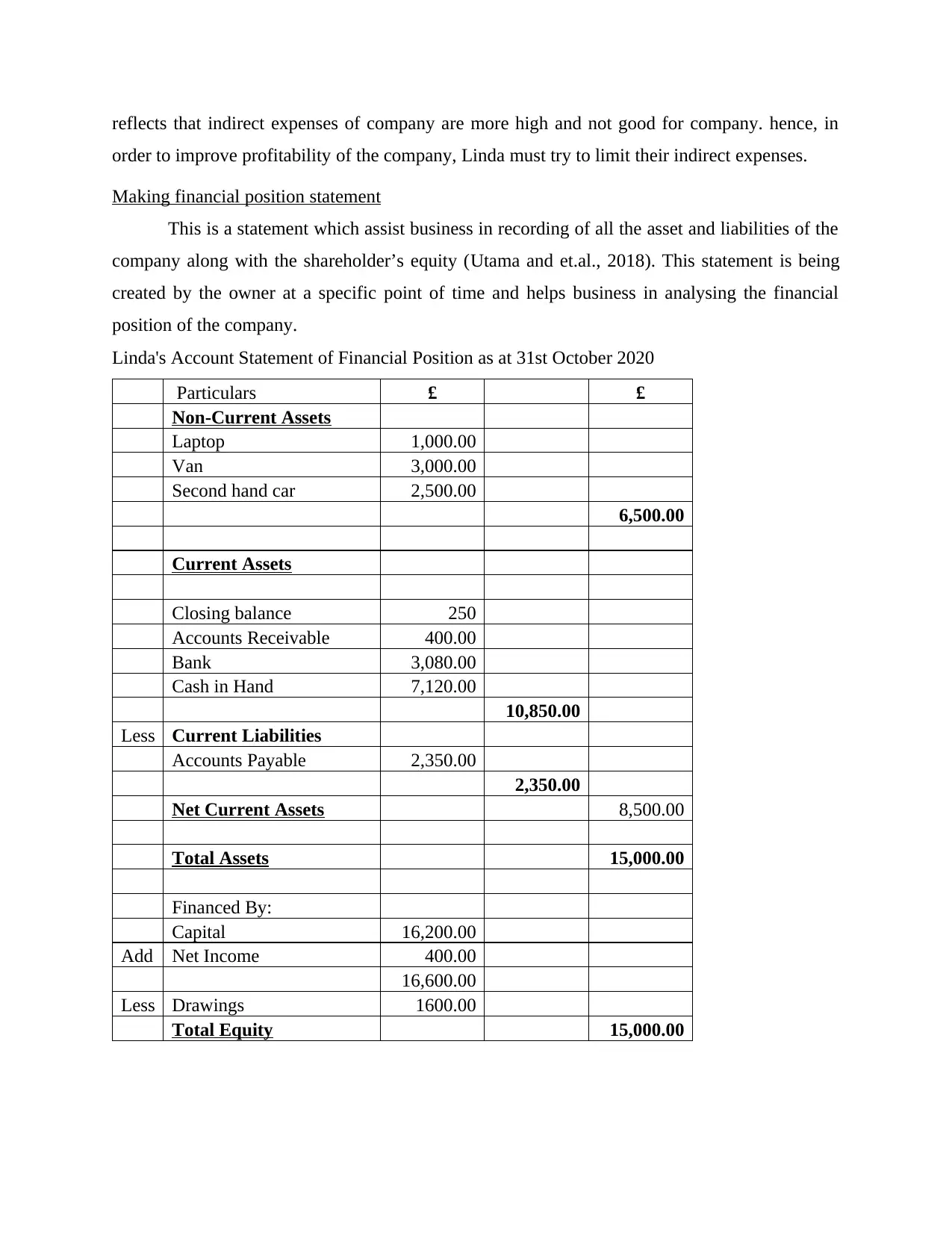

reflects that indirect expenses of company are more high and not good for company. hence, in

order to improve profitability of the company, Linda must try to limit their indirect expenses.

Making financial position statement

This is a statement which assist business in recording of all the asset and liabilities of the

company along with the shareholder’s equity (Utama and et.al., 2018). This statement is being

created by the owner at a specific point of time and helps business in analysing the financial

position of the company.

Linda's Account Statement of Financial Position as at 31st October 2020

Particulars £ £

Non-Current Assets

Laptop 1,000.00

Van 3,000.00

Second hand car 2,500.00

6,500.00

Current Assets

Closing balance 250

Accounts Receivable 400.00

Bank 3,080.00

Cash in Hand 7,120.00

10,850.00

Less Current Liabilities

Accounts Payable 2,350.00

2,350.00

Net Current Assets 8,500.00

Total Assets 15,000.00

Financed By:

Capital 16,200.00

Add Net Income 400.00

16,600.00

Less Drawings 1600.00

Total Equity 15,000.00

order to improve profitability of the company, Linda must try to limit their indirect expenses.

Making financial position statement

This is a statement which assist business in recording of all the asset and liabilities of the

company along with the shareholder’s equity (Utama and et.al., 2018). This statement is being

created by the owner at a specific point of time and helps business in analysing the financial

position of the company.

Linda's Account Statement of Financial Position as at 31st October 2020

Particulars £ £

Non-Current Assets

Laptop 1,000.00

Van 3,000.00

Second hand car 2,500.00

6,500.00

Current Assets

Closing balance 250

Accounts Receivable 400.00

Bank 3,080.00

Cash in Hand 7,120.00

10,850.00

Less Current Liabilities

Accounts Payable 2,350.00

2,350.00

Net Current Assets 8,500.00

Total Assets 15,000.00

Financed By:

Capital 16,200.00

Add Net Income 400.00

16,600.00

Less Drawings 1600.00

Total Equity 15,000.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

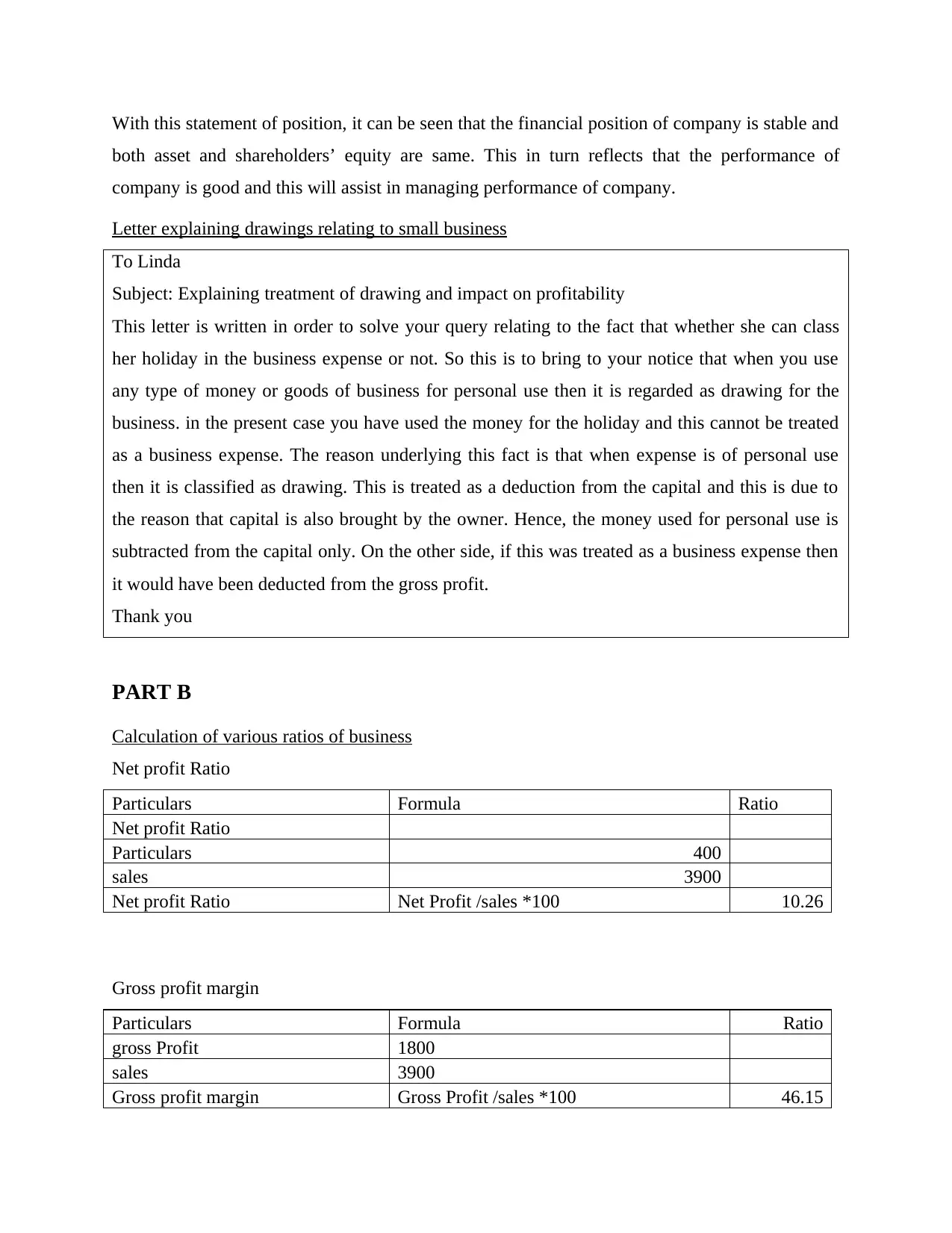

With this statement of position, it can be seen that the financial position of company is stable and

both asset and shareholders’ equity are same. This in turn reflects that the performance of

company is good and this will assist in managing performance of company.

Letter explaining drawings relating to small business

To Linda

Subject: Explaining treatment of drawing and impact on profitability

This letter is written in order to solve your query relating to the fact that whether she can class

her holiday in the business expense or not. So this is to bring to your notice that when you use

any type of money or goods of business for personal use then it is regarded as drawing for the

business. in the present case you have used the money for the holiday and this cannot be treated

as a business expense. The reason underlying this fact is that when expense is of personal use

then it is classified as drawing. This is treated as a deduction from the capital and this is due to

the reason that capital is also brought by the owner. Hence, the money used for personal use is

subtracted from the capital only. On the other side, if this was treated as a business expense then

it would have been deducted from the gross profit.

Thank you

PART B

Calculation of various ratios of business

Net profit Ratio

Particulars Formula Ratio

Net profit Ratio

Particulars 400

sales 3900

Net profit Ratio Net Profit /sales *100 10.26

Gross profit margin

Particulars Formula Ratio

gross Profit 1800

sales 3900

Gross profit margin Gross Profit /sales *100 46.15

both asset and shareholders’ equity are same. This in turn reflects that the performance of

company is good and this will assist in managing performance of company.

Letter explaining drawings relating to small business

To Linda

Subject: Explaining treatment of drawing and impact on profitability

This letter is written in order to solve your query relating to the fact that whether she can class

her holiday in the business expense or not. So this is to bring to your notice that when you use

any type of money or goods of business for personal use then it is regarded as drawing for the

business. in the present case you have used the money for the holiday and this cannot be treated

as a business expense. The reason underlying this fact is that when expense is of personal use

then it is classified as drawing. This is treated as a deduction from the capital and this is due to

the reason that capital is also brought by the owner. Hence, the money used for personal use is

subtracted from the capital only. On the other side, if this was treated as a business expense then

it would have been deducted from the gross profit.

Thank you

PART B

Calculation of various ratios of business

Net profit Ratio

Particulars Formula Ratio

Net profit Ratio

Particulars 400

sales 3900

Net profit Ratio Net Profit /sales *100 10.26

Gross profit margin

Particulars Formula Ratio

gross Profit 1800

sales 3900

Gross profit margin Gross Profit /sales *100 46.15

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

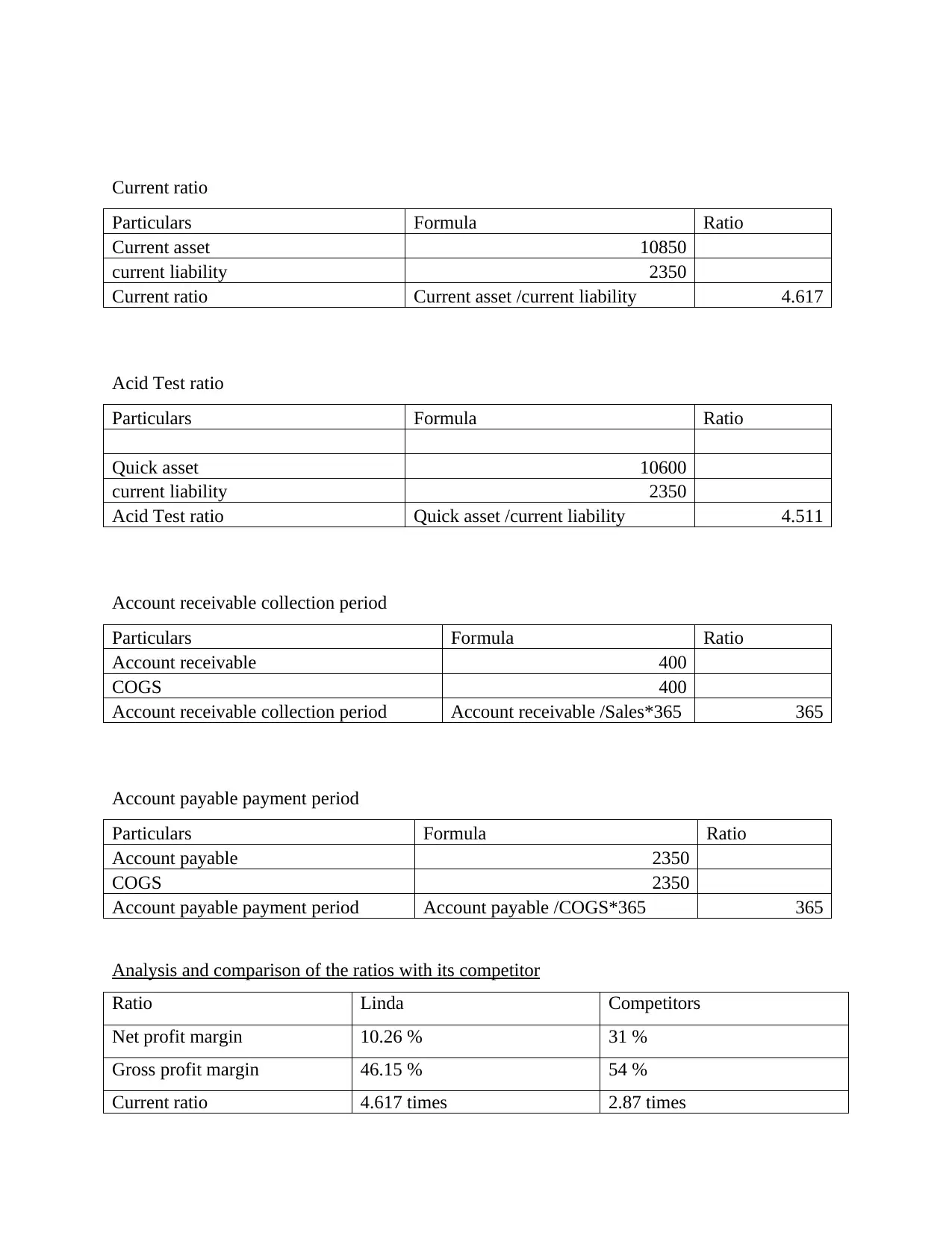

Current ratio

Particulars Formula Ratio

Current asset 10850

current liability 2350

Current ratio Current asset /current liability 4.617

Acid Test ratio

Particulars Formula Ratio

Quick asset 10600

current liability 2350

Acid Test ratio Quick asset /current liability 4.511

Account receivable collection period

Particulars Formula Ratio

Account receivable 400

COGS 400

Account receivable collection period Account receivable /Sales*365 365

Account payable payment period

Particulars Formula Ratio

Account payable 2350

COGS 2350

Account payable payment period Account payable /COGS*365 365

Analysis and comparison of the ratios with its competitor

Ratio Linda Competitors

Net profit margin 10.26 % 31 %

Gross profit margin 46.15 % 54 %

Current ratio 4.617 times 2.87 times

Particulars Formula Ratio

Current asset 10850

current liability 2350

Current ratio Current asset /current liability 4.617

Acid Test ratio

Particulars Formula Ratio

Quick asset 10600

current liability 2350

Acid Test ratio Quick asset /current liability 4.511

Account receivable collection period

Particulars Formula Ratio

Account receivable 400

COGS 400

Account receivable collection period Account receivable /Sales*365 365

Account payable payment period

Particulars Formula Ratio

Account payable 2350

COGS 2350

Account payable payment period Account payable /COGS*365 365

Analysis and comparison of the ratios with its competitor

Ratio Linda Competitors

Net profit margin 10.26 % 31 %

Gross profit margin 46.15 % 54 %

Current ratio 4.617 times 2.87 times

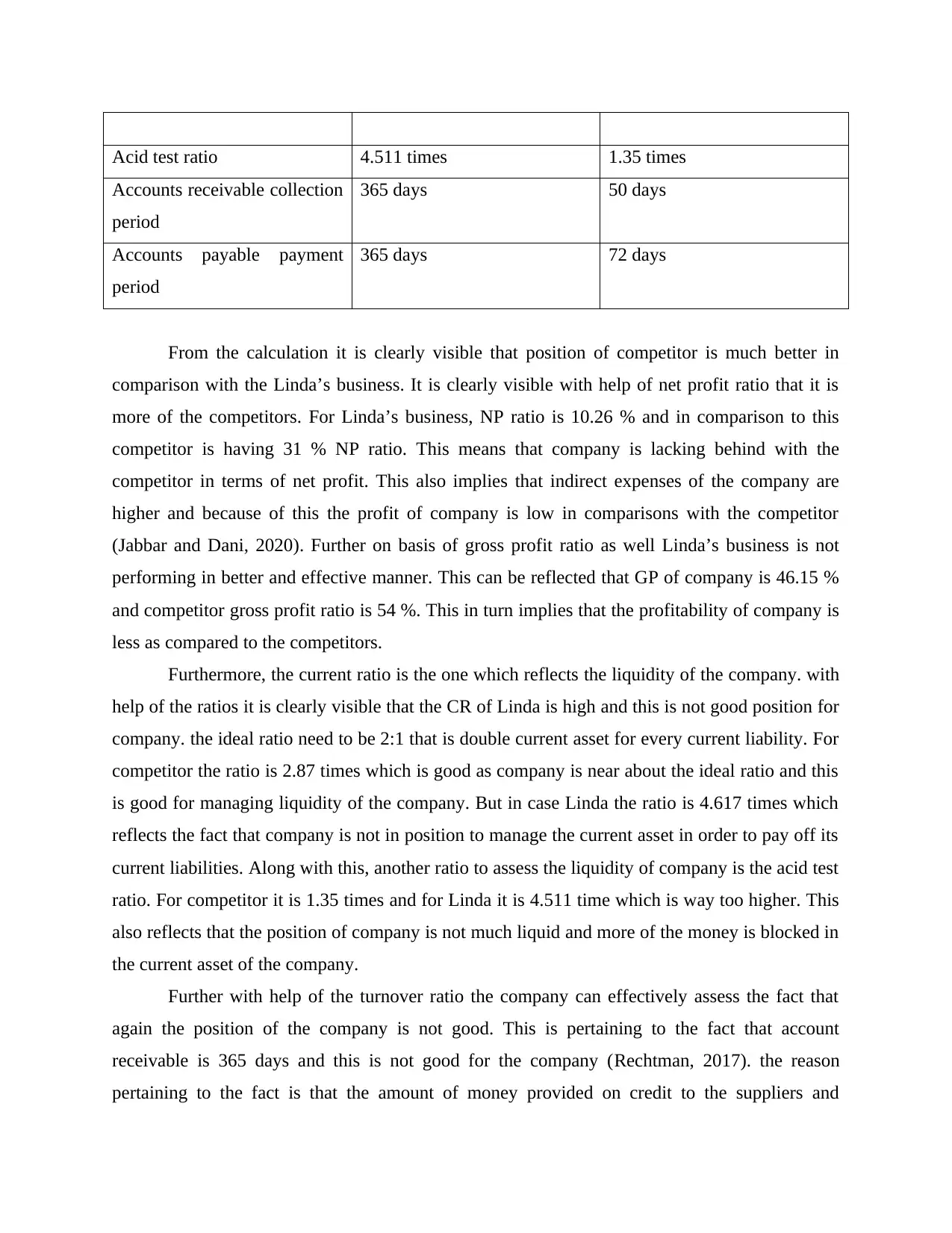

Acid test ratio 4.511 times 1.35 times

Accounts receivable collection

period

365 days 50 days

Accounts payable payment

period

365 days 72 days

From the calculation it is clearly visible that position of competitor is much better in

comparison with the Linda’s business. It is clearly visible with help of net profit ratio that it is

more of the competitors. For Linda’s business, NP ratio is 10.26 % and in comparison to this

competitor is having 31 % NP ratio. This means that company is lacking behind with the

competitor in terms of net profit. This also implies that indirect expenses of the company are

higher and because of this the profit of company is low in comparisons with the competitor

(Jabbar and Dani, 2020). Further on basis of gross profit ratio as well Linda’s business is not

performing in better and effective manner. This can be reflected that GP of company is 46.15 %

and competitor gross profit ratio is 54 %. This in turn implies that the profitability of company is

less as compared to the competitors.

Furthermore, the current ratio is the one which reflects the liquidity of the company. with

help of the ratios it is clearly visible that the CR of Linda is high and this is not good position for

company. the ideal ratio need to be 2:1 that is double current asset for every current liability. For

competitor the ratio is 2.87 times which is good as company is near about the ideal ratio and this

is good for managing liquidity of the company. But in case Linda the ratio is 4.617 times which

reflects the fact that company is not in position to manage the current asset in order to pay off its

current liabilities. Along with this, another ratio to assess the liquidity of company is the acid test

ratio. For competitor it is 1.35 times and for Linda it is 4.511 time which is way too higher. This

also reflects that the position of company is not much liquid and more of the money is blocked in

the current asset of the company.

Further with help of the turnover ratio the company can effectively assess the fact that

again the position of the company is not good. This is pertaining to the fact that account

receivable is 365 days and this is not good for the company (Rechtman, 2017). the reason

pertaining to the fact is that the amount of money provided on credit to the suppliers and

Accounts receivable collection

period

365 days 50 days

Accounts payable payment

period

365 days 72 days

From the calculation it is clearly visible that position of competitor is much better in

comparison with the Linda’s business. It is clearly visible with help of net profit ratio that it is

more of the competitors. For Linda’s business, NP ratio is 10.26 % and in comparison to this

competitor is having 31 % NP ratio. This means that company is lacking behind with the

competitor in terms of net profit. This also implies that indirect expenses of the company are

higher and because of this the profit of company is low in comparisons with the competitor

(Jabbar and Dani, 2020). Further on basis of gross profit ratio as well Linda’s business is not

performing in better and effective manner. This can be reflected that GP of company is 46.15 %

and competitor gross profit ratio is 54 %. This in turn implies that the profitability of company is

less as compared to the competitors.

Furthermore, the current ratio is the one which reflects the liquidity of the company. with

help of the ratios it is clearly visible that the CR of Linda is high and this is not good position for

company. the ideal ratio need to be 2:1 that is double current asset for every current liability. For

competitor the ratio is 2.87 times which is good as company is near about the ideal ratio and this

is good for managing liquidity of the company. But in case Linda the ratio is 4.617 times which

reflects the fact that company is not in position to manage the current asset in order to pay off its

current liabilities. Along with this, another ratio to assess the liquidity of company is the acid test

ratio. For competitor it is 1.35 times and for Linda it is 4.511 time which is way too higher. This

also reflects that the position of company is not much liquid and more of the money is blocked in

the current asset of the company.

Further with help of the turnover ratio the company can effectively assess the fact that

again the position of the company is not good. This is pertaining to the fact that account

receivable is 365 days and this is not good for the company (Rechtman, 2017). the reason

pertaining to the fact is that the amount of money provided on credit to the suppliers and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.