Recording Business Transactions (Portfolio 2)

VerifiedAdded on 2023/01/03

|15

|2122

|32

AI Summary

This report discusses the recording of business transactions, preparation of ledger accounts, trial balance, income statement, financial statements, and ratio analysis. It provides a comprehensive understanding of financial information and its interpretation for evaluating the financial health of a company. The report also includes a brief letter to Linda regarding personal drawings and compares the company's financial ratios with its competitors. Solved assignments and study material are available on Desklib.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Recording Business

Transactions

(Portfolio 2)

Transactions

(Portfolio 2)

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

a. Recording journal entries of business:.....................................................................................3

b. Preparing company's ledger accounts:.....................................................................................5

c. Extraction of Trial Balance:.....................................................................................................7

d. Preparing Income Statement for year ending 31st October 2020:...........................................8

e. Preparation of Financial statement:..........................................................................................8

f. Writing brief letter to Linda in relevance to drawing:..............................................................9

PART B..........................................................................................................................................10

a. Calculation of financial ratios:...............................................................................................10

Working note:............................................................................................................................10

b. Interpretation and comparison of ratio analysis:....................................................................11

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

a. Recording journal entries of business:.....................................................................................3

b. Preparing company's ledger accounts:.....................................................................................5

c. Extraction of Trial Balance:.....................................................................................................7

d. Preparing Income Statement for year ending 31st October 2020:...........................................8

e. Preparation of Financial statement:..........................................................................................8

f. Writing brief letter to Linda in relevance to drawing:..............................................................9

PART B..........................................................................................................................................10

a. Calculation of financial ratios:...............................................................................................10

Working note:............................................................................................................................10

b. Interpretation and comparison of ratio analysis:....................................................................11

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................13

INTRODUCTION

Recording business transactions indicates noting, summarising or reporting business

transactions in terms of money (Kamburova, 2020). While considering characteristics of

business transactions it can be noted that it is a requirement for transactions in relevance to

business to entitle support of some source document , for example sales invoice, receipt etc. and

it is necessary for them to pertain two fold effect (Lessambo, 2018).

This report evaluates financial information of Linda's business and interprets it to gain

knowledge about financial health of company. In this report, journal entries of Linda's business

is recorded. Further, its ledger, trial balance and income statement is prepared. Motive is to

compute its ratio analysis and identify its financial position in comparison to competitors.

PART A

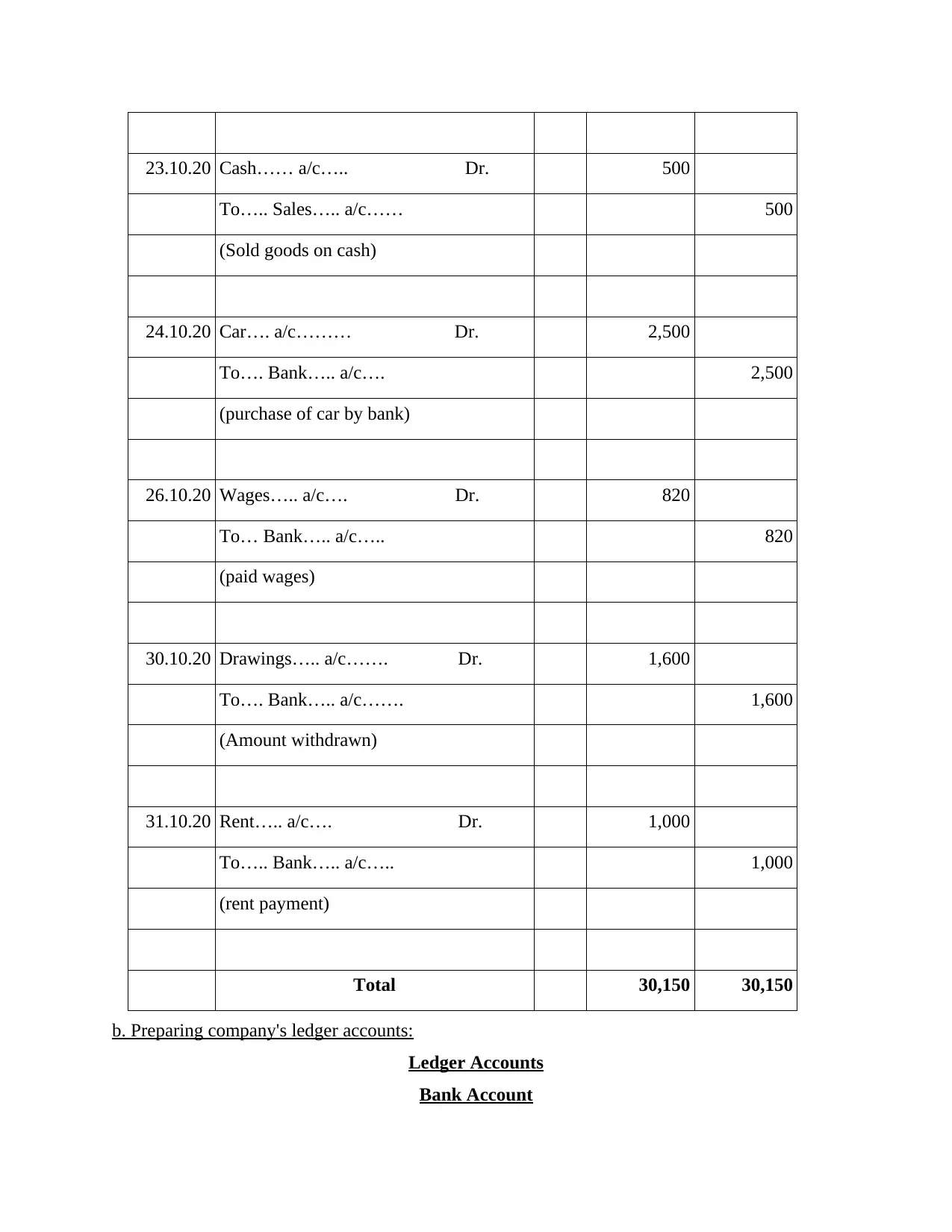

a. Recording journal entries of business:

Journal Entries of Linda's Business

Date Particulars L.F Dr. Cr.

01.10.20 Van... a/c….. Dr. 3,000

Cash a/c….. Dr. 5,200

Bank a/c…… Dr. 8,000

To Capital….. a/c…… 16,200

(Made capital investment in company)

02.10.20 Laptop a/c…… Dr. 1,000

To…. Bank….. a/c…… 1,000

(purchase of laptop )

04.10.20 Purchase….. a/c.….. Dr. 2,450

Recording business transactions indicates noting, summarising or reporting business

transactions in terms of money (Kamburova, 2020). While considering characteristics of

business transactions it can be noted that it is a requirement for transactions in relevance to

business to entitle support of some source document , for example sales invoice, receipt etc. and

it is necessary for them to pertain two fold effect (Lessambo, 2018).

This report evaluates financial information of Linda's business and interprets it to gain

knowledge about financial health of company. In this report, journal entries of Linda's business

is recorded. Further, its ledger, trial balance and income statement is prepared. Motive is to

compute its ratio analysis and identify its financial position in comparison to competitors.

PART A

a. Recording journal entries of business:

Journal Entries of Linda's Business

Date Particulars L.F Dr. Cr.

01.10.20 Van... a/c….. Dr. 3,000

Cash a/c….. Dr. 5,200

Bank a/c…… Dr. 8,000

To Capital….. a/c…… 16,200

(Made capital investment in company)

02.10.20 Laptop a/c…… Dr. 1,000

To…. Bank….. a/c…… 1,000

(purchase of laptop )

04.10.20 Purchase….. a/c.….. Dr. 2,450

To…Toys…. Ltd… a/c… 2,450

(Purchase of goods from Toy Ltd.)

05.10.20 Bank….. a/c….. Dr. 1,500

To …..Sales….. a/c……. 1,500

(Sold goods and receive amount through

bank)

12.10.20 Repair…. a/c.... Dr. 80

To Cash a/c 80

(paid cash for repair of laptop)

18.10.20 Toys….. Ltd…. a/c…… Dr. 100

To…. Purchase… Return… a/c… 100

(purchase returned)

21.10.20 Bank… a/c…. Dr. 500

To…. Rent….. a/c….. 500

(received rent by cheque)

23.10.20 Fred…. a/c….. Dr. 400

Cash…… a/c…… Dr. 1,500

To….. Sales….. a/c…… 1,900

(Goods sold)

(Purchase of goods from Toy Ltd.)

05.10.20 Bank….. a/c….. Dr. 1,500

To …..Sales….. a/c……. 1,500

(Sold goods and receive amount through

bank)

12.10.20 Repair…. a/c.... Dr. 80

To Cash a/c 80

(paid cash for repair of laptop)

18.10.20 Toys….. Ltd…. a/c…… Dr. 100

To…. Purchase… Return… a/c… 100

(purchase returned)

21.10.20 Bank… a/c…. Dr. 500

To…. Rent….. a/c….. 500

(received rent by cheque)

23.10.20 Fred…. a/c….. Dr. 400

Cash…… a/c…… Dr. 1,500

To….. Sales….. a/c…… 1,900

(Goods sold)

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

23.10.20 Cash…… a/c….. Dr. 500

To….. Sales….. a/c…… 500

(Sold goods on cash)

24.10.20 Car…. a/c……… Dr. 2,500

To…. Bank….. a/c…. 2,500

(purchase of car by bank)

26.10.20 Wages….. a/c…. Dr. 820

To… Bank….. a/c….. 820

(paid wages)

30.10.20 Drawings….. a/c……. Dr. 1,600

To…. Bank….. a/c……. 1,600

(Amount withdrawn)

31.10.20 Rent….. a/c…. Dr. 1,000

To….. Bank….. a/c….. 1,000

(rent payment)

Total 30,150 30,150

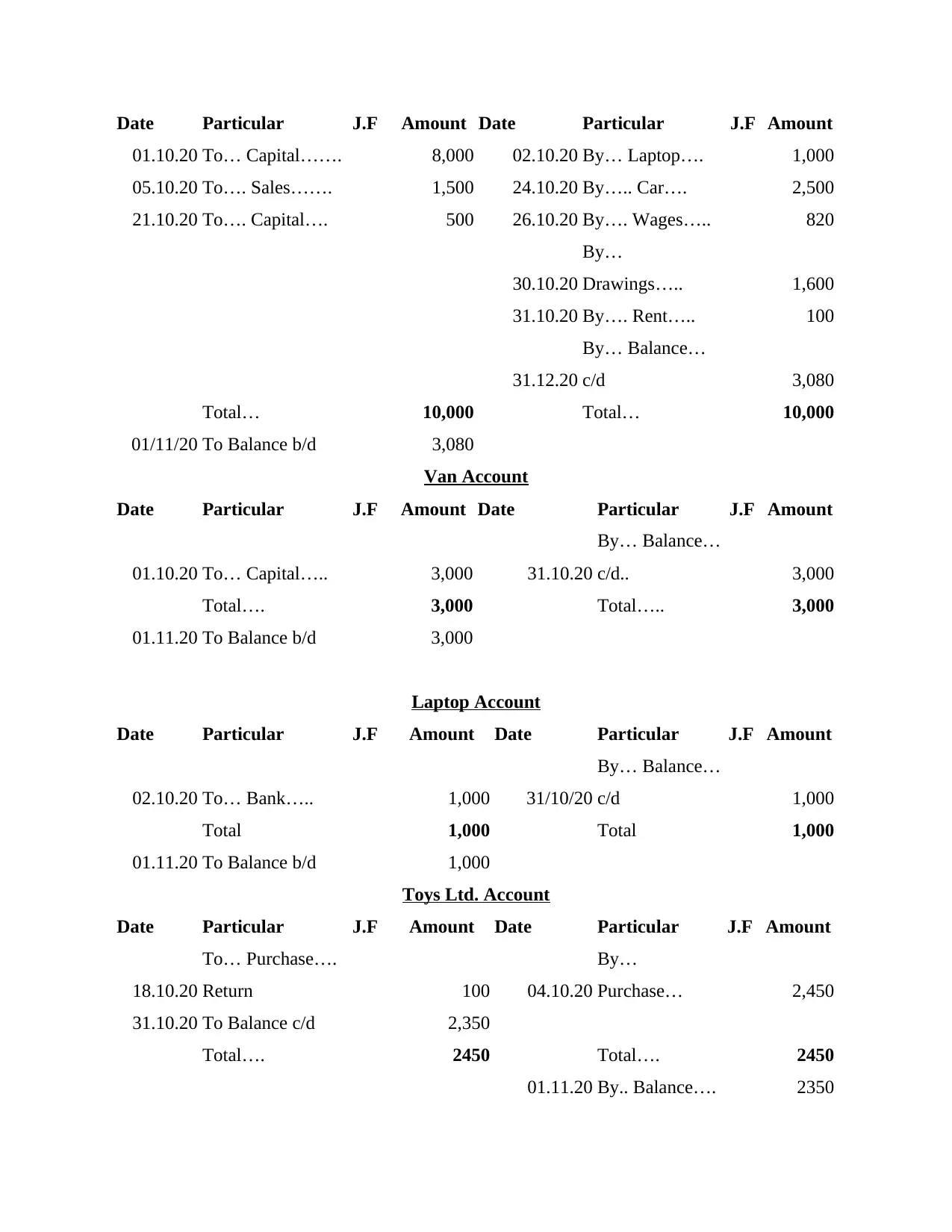

b. Preparing company's ledger accounts:

Ledger Accounts

Bank Account

To….. Sales….. a/c…… 500

(Sold goods on cash)

24.10.20 Car…. a/c……… Dr. 2,500

To…. Bank….. a/c…. 2,500

(purchase of car by bank)

26.10.20 Wages….. a/c…. Dr. 820

To… Bank….. a/c….. 820

(paid wages)

30.10.20 Drawings….. a/c……. Dr. 1,600

To…. Bank….. a/c……. 1,600

(Amount withdrawn)

31.10.20 Rent….. a/c…. Dr. 1,000

To….. Bank….. a/c….. 1,000

(rent payment)

Total 30,150 30,150

b. Preparing company's ledger accounts:

Ledger Accounts

Bank Account

Date Particular J.F Amount Date Particular J.F Amount

01.10.20 To… Capital……. 8,000 02.10.20 By… Laptop…. 1,000

05.10.20 To…. Sales……. 1,500 24.10.20 By….. Car…. 2,500

21.10.20 To…. Capital…. 500 26.10.20 By…. Wages….. 820

30.10.20

By…

Drawings….. 1,600

31.10.20 By…. Rent….. 100

31.12.20

By… Balance…

c/d 3,080

Total… 10,000 Total… 10,000

01/11/20 To Balance b/d 3,080

Van Account

Date Particular J.F Amount Date Particular J.F Amount

01.10.20 To… Capital….. 3,000 31.10.20

By… Balance…

c/d.. 3,000

Total…. 3,000 Total….. 3,000

01.11.20 To Balance b/d 3,000

Laptop Account

Date Particular J.F Amount Date Particular J.F Amount

02.10.20 To… Bank….. 1,000 31/10/20

By… Balance…

c/d 1,000

Total 1,000 Total 1,000

01.11.20 To Balance b/d 1,000

Toys Ltd. Account

Date Particular J.F Amount Date Particular J.F Amount

18.10.20

To… Purchase….

Return 100 04.10.20

By…

Purchase… 2,450

31.10.20 To Balance c/d 2,350

Total…. 2450 Total…. 2450

01.11.20 By.. Balance…. 2350

01.10.20 To… Capital……. 8,000 02.10.20 By… Laptop…. 1,000

05.10.20 To…. Sales……. 1,500 24.10.20 By….. Car…. 2,500

21.10.20 To…. Capital…. 500 26.10.20 By…. Wages….. 820

30.10.20

By…

Drawings….. 1,600

31.10.20 By…. Rent….. 100

31.12.20

By… Balance…

c/d 3,080

Total… 10,000 Total… 10,000

01/11/20 To Balance b/d 3,080

Van Account

Date Particular J.F Amount Date Particular J.F Amount

01.10.20 To… Capital….. 3,000 31.10.20

By… Balance…

c/d.. 3,000

Total…. 3,000 Total….. 3,000

01.11.20 To Balance b/d 3,000

Laptop Account

Date Particular J.F Amount Date Particular J.F Amount

02.10.20 To… Bank….. 1,000 31/10/20

By… Balance…

c/d 1,000

Total 1,000 Total 1,000

01.11.20 To Balance b/d 1,000

Toys Ltd. Account

Date Particular J.F Amount Date Particular J.F Amount

18.10.20

To… Purchase….

Return 100 04.10.20

By…

Purchase… 2,450

31.10.20 To Balance c/d 2,350

Total…. 2450 Total…. 2450

01.11.20 By.. Balance…. 2350

b/d

Purchase Return Account….

Date Particular J.F Amount Date Particular J.F Amount

31.10.20 To… Trading.. 100 18/10/20 By Toys Ltd. 100

Total 100 Total 100

Fred's Account…

Date Particular J.F Amount Date Particular J.F Amount

23. 10. 20 To Sales 400 31/10/20 By Balance c/d 400

Total 400 Total 400

400

Car Account…

Date Particular J.F Amount Date Particular J.F Amount

24. 10. 20 To Bank…. 2,500 31/10/20

By Balance…

c/d 2,500

Total…. 2,500 Total… 2,500

01. 11. 20 To Balance b/d 2,500

Drawings Account

Date Particular J.F Amount Date Particular J.F Amount

30. 10. 20 To bank 1,600

By Profit and

Loss 1,600

Total 1,600 Total 1,600

Cash Account

Date Particular J.F Amount Date Particular J.F Amount

01. 10. 20 To capital… 5,200 12. 10. 20 By Repair 80

23. 10. 20 To sales…. 1,500 31. 10. 20 By balance c/d 7,120

To sales… 500

Purchase Return Account….

Date Particular J.F Amount Date Particular J.F Amount

31.10.20 To… Trading.. 100 18/10/20 By Toys Ltd. 100

Total 100 Total 100

Fred's Account…

Date Particular J.F Amount Date Particular J.F Amount

23. 10. 20 To Sales 400 31/10/20 By Balance c/d 400

Total 400 Total 400

400

Car Account…

Date Particular J.F Amount Date Particular J.F Amount

24. 10. 20 To Bank…. 2,500 31/10/20

By Balance…

c/d 2,500

Total…. 2,500 Total… 2,500

01. 11. 20 To Balance b/d 2,500

Drawings Account

Date Particular J.F Amount Date Particular J.F Amount

30. 10. 20 To bank 1,600

By Profit and

Loss 1,600

Total 1,600 Total 1,600

Cash Account

Date Particular J.F Amount Date Particular J.F Amount

01. 10. 20 To capital… 5,200 12. 10. 20 By Repair 80

23. 10. 20 To sales…. 1,500 31. 10. 20 By balance c/d 7,120

To sales… 500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

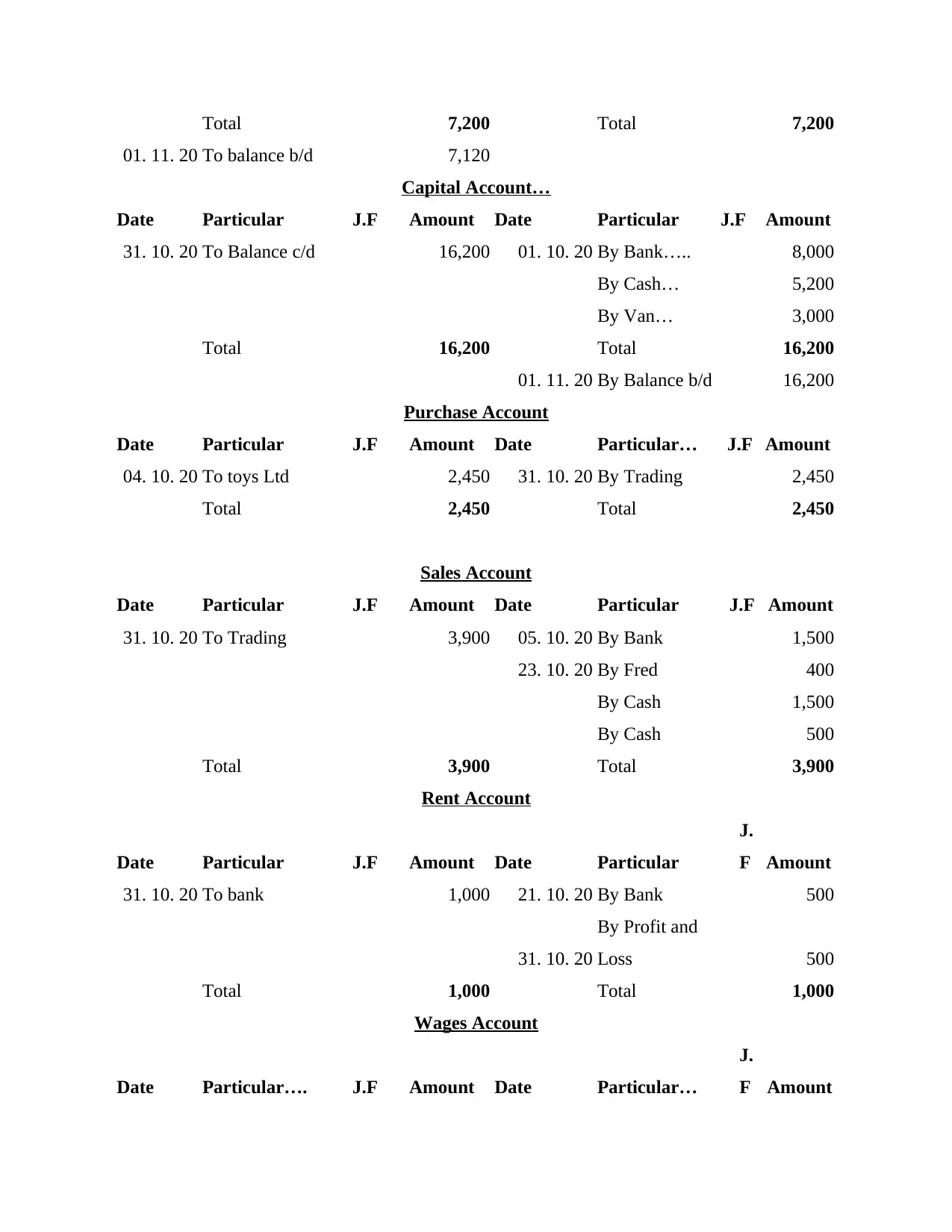

Total 7,200 Total 7,200

01. 11. 20 To balance b/d 7,120

Capital Account…

Date Particular J.F Amount Date Particular J.F Amount

31. 10. 20 To Balance c/d 16,200 01. 10. 20 By Bank….. 8,000

By Cash… 5,200

By Van… 3,000

Total 16,200 Total 16,200

01. 11. 20 By Balance b/d 16,200

Purchase Account

Date Particular J.F Amount Date Particular… J.F Amount

04. 10. 20 To toys Ltd 2,450 31. 10. 20 By Trading 2,450

Total 2,450 Total 2,450

Sales Account

Date Particular J.F Amount Date Particular J.F Amount

31. 10. 20 To Trading 3,900 05. 10. 20 By Bank 1,500

23. 10. 20 By Fred 400

By Cash 1,500

By Cash 500

Total 3,900 Total 3,900

Rent Account

Date Particular J.F Amount Date Particular

J.

F Amount

31. 10. 20 To bank 1,000 21. 10. 20 By Bank 500

31. 10. 20

By Profit and

Loss 500

Total 1,000 Total 1,000

Wages Account

Date Particular…. J.F Amount Date Particular…

J.

F Amount

01. 11. 20 To balance b/d 7,120

Capital Account…

Date Particular J.F Amount Date Particular J.F Amount

31. 10. 20 To Balance c/d 16,200 01. 10. 20 By Bank….. 8,000

By Cash… 5,200

By Van… 3,000

Total 16,200 Total 16,200

01. 11. 20 By Balance b/d 16,200

Purchase Account

Date Particular J.F Amount Date Particular… J.F Amount

04. 10. 20 To toys Ltd 2,450 31. 10. 20 By Trading 2,450

Total 2,450 Total 2,450

Sales Account

Date Particular J.F Amount Date Particular J.F Amount

31. 10. 20 To Trading 3,900 05. 10. 20 By Bank 1,500

23. 10. 20 By Fred 400

By Cash 1,500

By Cash 500

Total 3,900 Total 3,900

Rent Account

Date Particular J.F Amount Date Particular

J.

F Amount

31. 10. 20 To bank 1,000 21. 10. 20 By Bank 500

31. 10. 20

By Profit and

Loss 500

Total 1,000 Total 1,000

Wages Account

Date Particular…. J.F Amount Date Particular…

J.

F Amount

26. 10. 20 To sales 820 31. 10. 20

By Profit and

Loss 820

Total 820 Total 820

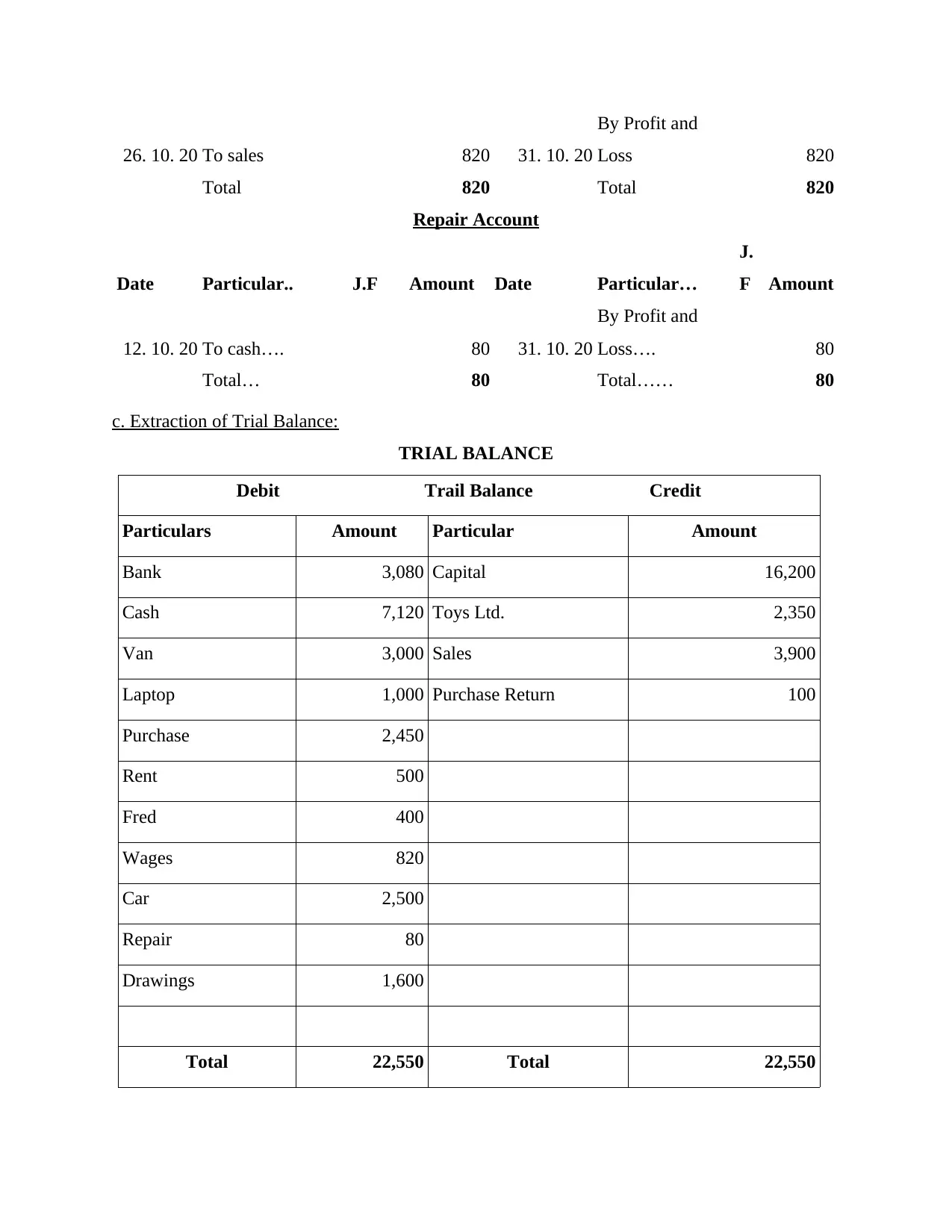

Repair Account

Date Particular.. J.F Amount Date Particular…

J.

F Amount

12. 10. 20 To cash…. 80 31. 10. 20

By Profit and

Loss…. 80

Total… 80 Total…… 80

c. Extraction of Trial Balance:

TRIAL BALANCE

Debit Trail Balance Credit

Particulars Amount Particular Amount

Bank 3,080 Capital 16,200

Cash 7,120 Toys Ltd. 2,350

Van 3,000 Sales 3,900

Laptop 1,000 Purchase Return 100

Purchase 2,450

Rent 500

Fred 400

Wages 820

Car 2,500

Repair 80

Drawings 1,600

Total 22,550 Total 22,550

By Profit and

Loss 820

Total 820 Total 820

Repair Account

Date Particular.. J.F Amount Date Particular…

J.

F Amount

12. 10. 20 To cash…. 80 31. 10. 20

By Profit and

Loss…. 80

Total… 80 Total…… 80

c. Extraction of Trial Balance:

TRIAL BALANCE

Debit Trail Balance Credit

Particulars Amount Particular Amount

Bank 3,080 Capital 16,200

Cash 7,120 Toys Ltd. 2,350

Van 3,000 Sales 3,900

Laptop 1,000 Purchase Return 100

Purchase 2,450

Rent 500

Fred 400

Wages 820

Car 2,500

Repair 80

Drawings 1,600

Total 22,550 Total 22,550

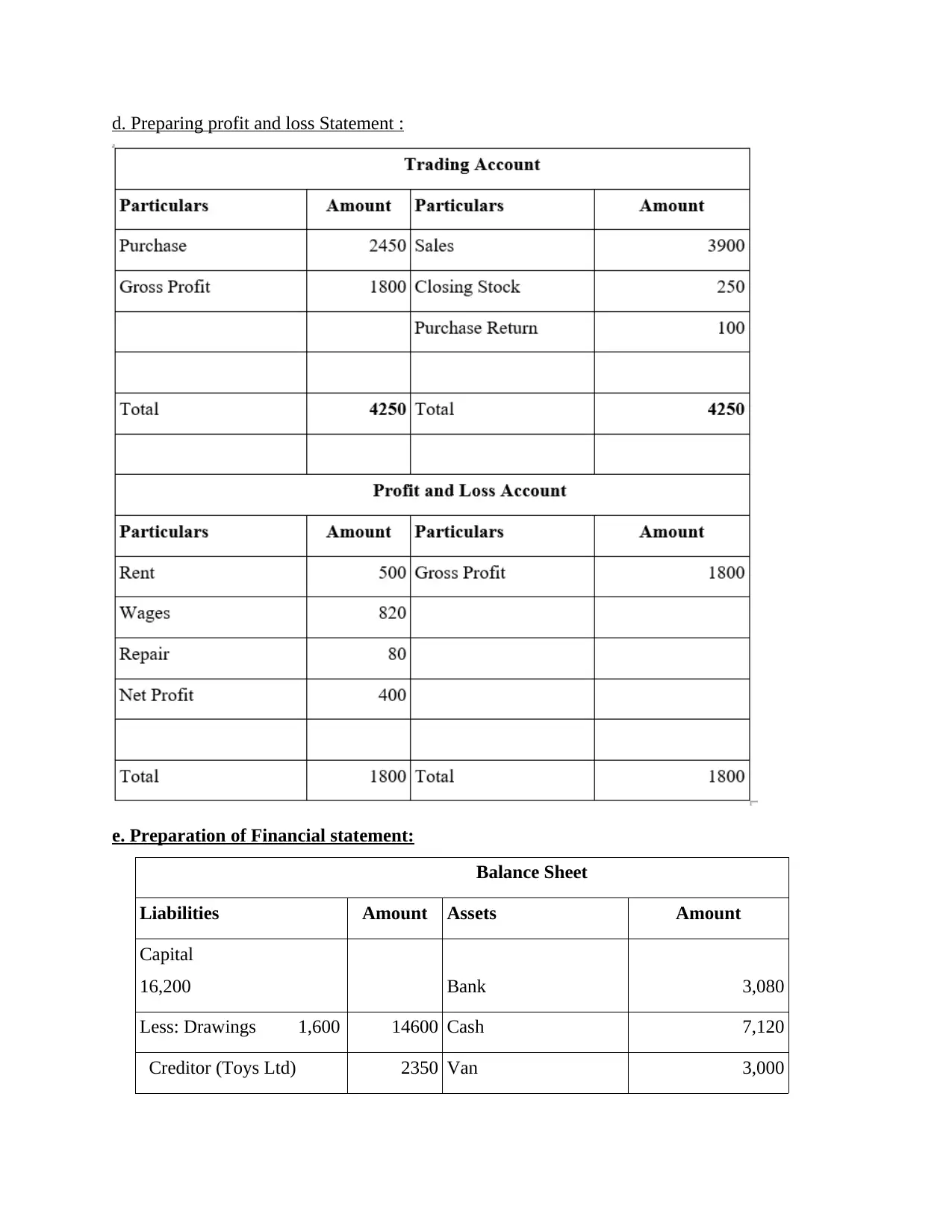

d. Preparing profit and loss Statement :

e. Preparation of Financial statement:

Balance Sheet

Liabilities Amount Assets Amount

Capital

16,200 Bank 3,080

Less: Drawings 1,600 14600 Cash 7,120

Creditor (Toys Ltd) 2350 Van 3,000

e. Preparation of Financial statement:

Balance Sheet

Liabilities Amount Assets Amount

Capital

16,200 Bank 3,080

Less: Drawings 1,600 14600 Cash 7,120

Creditor (Toys Ltd) 2350 Van 3,000

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Net Profit 400 Laptop 1,000

Car 2,500

Debtor (Fred) 400

Closing Inventory 250

Total 17,350 Total 17,350

f. Writing brief letter to Linda in relevance to drawing:

BRIEF LETTER

Dear Linda,

In context to your drawing of £1600 for holiday in Florida, it is necessary to explain you that

this amount will be considered as personal drawing. As, owner and company are two separate

entity as per accounting concept. According to which, owner's personal expenses should not be

involved in financial transactions of business.

Thanking you,

Financial Advisor

Car 2,500

Debtor (Fred) 400

Closing Inventory 250

Total 17,350 Total 17,350

f. Writing brief letter to Linda in relevance to drawing:

BRIEF LETTER

Dear Linda,

In context to your drawing of £1600 for holiday in Florida, it is necessary to explain you that

this amount will be considered as personal drawing. As, owner and company are two separate

entity as per accounting concept. According to which, owner's personal expenses should not be

involved in financial transactions of business.

Thanking you,

Financial Advisor

PART B

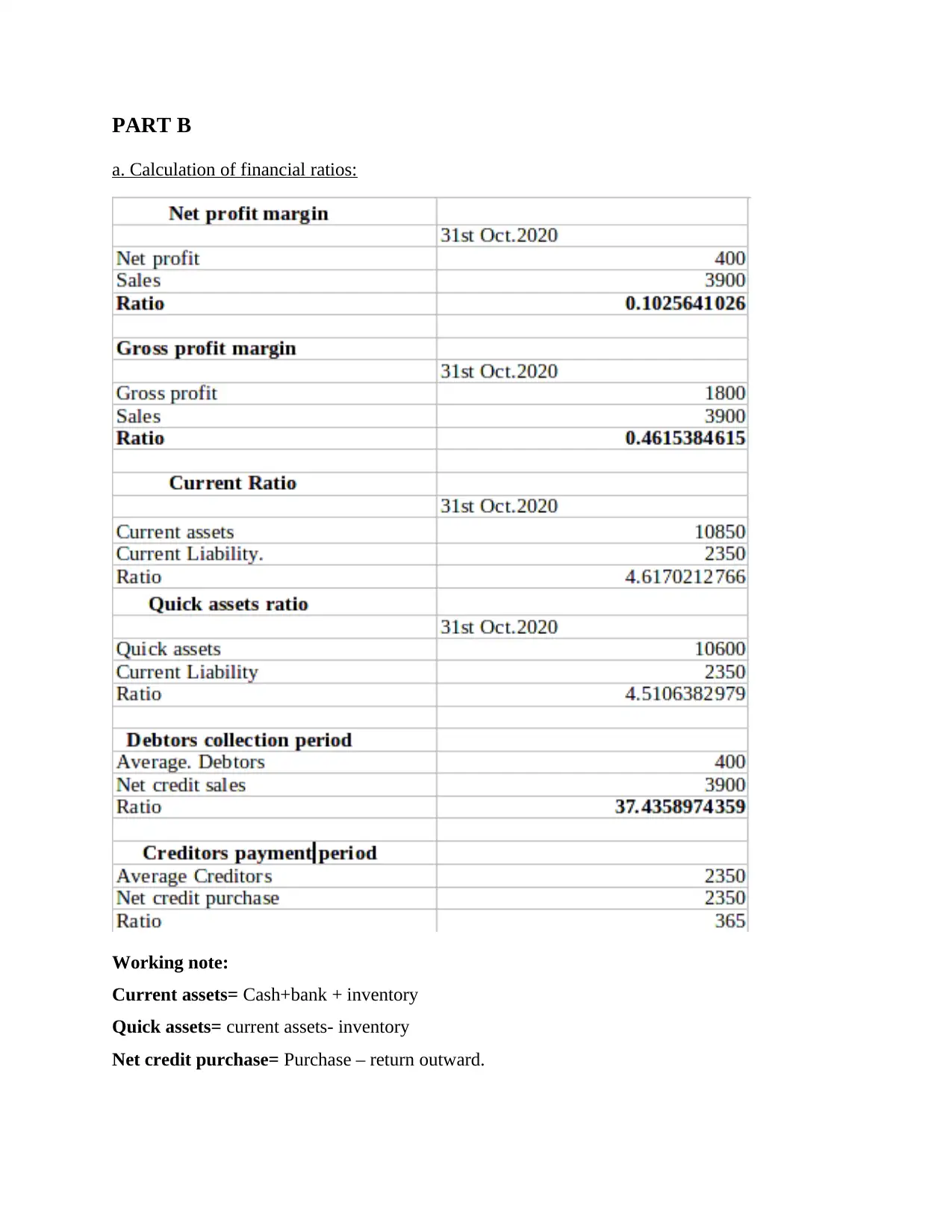

a. Calculation of financial ratios:

Working note:

Current assets= Cash+bank + inventory

Quick assets= current assets- inventory

Net credit purchase= Purchase – return outward.

a. Calculation of financial ratios:

Working note:

Current assets= Cash+bank + inventory

Quick assets= current assets- inventory

Net credit purchase= Purchase – return outward.

b. Interpretation and comparison of ratio analysis:

Ratio analysis can be defined as a technique or method of analysing of financial

statements of a company (Schmidt, 2018). This tool helps in comparing financial status of

company with its competitors., which enables firm to identify its position and gain financial

sustainability. Ratio analysis provides broader picture about financial health of an organization

(Martins Noriller and Tibúrcio Silva, 2019). It pertains management of an enterprise to overview

interpreted financial information and formulate best strategies for further expansion or growth of

entity.

While comparing ratio analysis of Linda's business with its competitors it is interpreted

that net profit of Linda's business is 10.26% while net profit margin of competitors is 31%. It

states that operating expenses of company is high as compared to competitors. Hence, firm

should focus on eliminated or deducting unnecessary costs. Further, gross profit shows that

efficiency of an entity in generating revenue from its core competencies. Gross profit on Linda's

business is 46.15% while that of competitors is 54%. hence, management team of business

should focus more on reducing production expenses and improving its proficiency. While

discussing about current ratio, it can be seen that current ratio of company is higher than its

competitors, that is, current ratio of Linda's business is 4.6 while current ratio of competitors is

2.87. it pinpoints that liquidity of business is highly capable of paying short term obligations.

Acid test ratio of competitors is 1.35 while that of Linda's business is 4.51, which is again a good

sign as it shows that liquidity position of company is good. Organization takes 37 days for

collecting receivables, on the other hand, its competitors takes 50 days. It indicates that payments

are collected faster, hence, chances of bad debts reduces. On the contrary, creditors payment

period of an organization is high in comparison to competitors which declines its credit

worthiness (Zaidi, Akhter and Akhtar, 2018). Overall, company financial health of company is

good and its liquidity position is also better. But, management of firm need to focus more on

reducing expenses and improving profit margin.

CONCLUSION

Above report concludes that business transactions must be recorded in monetary terms to

gain information about firm's financial transactions. For this purpose journal entries are recorded

in the books of account by accounting department. On the basis of these entries, ledger accounts

are prepared. Further, trial balance of company is prepared to list or summarise such ledger

Ratio analysis can be defined as a technique or method of analysing of financial

statements of a company (Schmidt, 2018). This tool helps in comparing financial status of

company with its competitors., which enables firm to identify its position and gain financial

sustainability. Ratio analysis provides broader picture about financial health of an organization

(Martins Noriller and Tibúrcio Silva, 2019). It pertains management of an enterprise to overview

interpreted financial information and formulate best strategies for further expansion or growth of

entity.

While comparing ratio analysis of Linda's business with its competitors it is interpreted

that net profit of Linda's business is 10.26% while net profit margin of competitors is 31%. It

states that operating expenses of company is high as compared to competitors. Hence, firm

should focus on eliminated or deducting unnecessary costs. Further, gross profit shows that

efficiency of an entity in generating revenue from its core competencies. Gross profit on Linda's

business is 46.15% while that of competitors is 54%. hence, management team of business

should focus more on reducing production expenses and improving its proficiency. While

discussing about current ratio, it can be seen that current ratio of company is higher than its

competitors, that is, current ratio of Linda's business is 4.6 while current ratio of competitors is

2.87. it pinpoints that liquidity of business is highly capable of paying short term obligations.

Acid test ratio of competitors is 1.35 while that of Linda's business is 4.51, which is again a good

sign as it shows that liquidity position of company is good. Organization takes 37 days for

collecting receivables, on the other hand, its competitors takes 50 days. It indicates that payments

are collected faster, hence, chances of bad debts reduces. On the contrary, creditors payment

period of an organization is high in comparison to competitors which declines its credit

worthiness (Zaidi, Akhter and Akhtar, 2018). Overall, company financial health of company is

good and its liquidity position is also better. But, management of firm need to focus more on

reducing expenses and improving profit margin.

CONCLUSION

Above report concludes that business transactions must be recorded in monetary terms to

gain information about firm's financial transactions. For this purpose journal entries are recorded

in the books of account by accounting department. On the basis of these entries, ledger accounts

are prepared. Further, trial balance of company is prepared to list or summarise such ledger

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

accounts. Income statements shows the profitability position of company and balance sheet is an

indicators of liability and assets that company holds. These are termed as financial statements,

which conveys the financial status of business. For interpreting such statement, ratio analysis is

conducted. Ratio analysis is the indicator of company's financial position.

indicators of liability and assets that company holds. These are termed as financial statements,

which conveys the financial status of business. For interpreting such statement, ratio analysis is

conducted. Ratio analysis is the indicator of company's financial position.

REFERENCES

Books and Journals:

Kamburova, L., 2020. The Development of Practices for the Preparation of Consolidated

Financial Statements. Ikonomiceski i Sotsialni Alternativi. (1). pp. 123-133.

Lessambo, F. I., 2018. Analysis of the Statements of Cash Flows. In Financial Statements (pp.

195-206). Palgrave Macmillan, Cham.

Martins Noriller, R. and Tibúrcio Silva, C. A., 2019. IMPACT OF MACROECONOMIC

VARIABLES ON THE COMPONENTS OF FINANCIAL STATEMENTS OF LATIN

AMERICAN PUBLIC COMPANIES. Revista Universo Contábil. 15(3).

Schmidt, M., 2018. A Note on the Proprietary and Entity Perspectives in Financial Statements:

The Implications for two Current Controversial Issues. Accounting in Europe. 15(1), pp.

134-147.

Servicing, M., Notes to the Financial Statements. Policy. 1(1,136), pp. 1-136.

Yuesti, A., Adnyana, I. M. D. and Pramesti, I. G. A. A., Management information systems and

the quality of financial statements in local government. Journal of Public Affairs,

p.e2462.

Zaidi, U. K., Akhter, J. and Akhtar, A., 2018. Window Dressing of Financial Statements in the

Era of Digital Finance: A Study of Small Cap Indian Companies. Metamorphosis.

17(2). pp. 67-75.

Books and Journals:

Kamburova, L., 2020. The Development of Practices for the Preparation of Consolidated

Financial Statements. Ikonomiceski i Sotsialni Alternativi. (1). pp. 123-133.

Lessambo, F. I., 2018. Analysis of the Statements of Cash Flows. In Financial Statements (pp.

195-206). Palgrave Macmillan, Cham.

Martins Noriller, R. and Tibúrcio Silva, C. A., 2019. IMPACT OF MACROECONOMIC

VARIABLES ON THE COMPONENTS OF FINANCIAL STATEMENTS OF LATIN

AMERICAN PUBLIC COMPANIES. Revista Universo Contábil. 15(3).

Schmidt, M., 2018. A Note on the Proprietary and Entity Perspectives in Financial Statements:

The Implications for two Current Controversial Issues. Accounting in Europe. 15(1), pp.

134-147.

Servicing, M., Notes to the Financial Statements. Policy. 1(1,136), pp. 1-136.

Yuesti, A., Adnyana, I. M. D. and Pramesti, I. G. A. A., Management information systems and

the quality of financial statements in local government. Journal of Public Affairs,

p.e2462.

Zaidi, U. K., Akhter, J. and Akhtar, A., 2018. Window Dressing of Financial Statements in the

Era of Digital Finance: A Study of Small Cap Indian Companies. Metamorphosis.

17(2). pp. 67-75.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.