Recording Business Transaction

VerifiedAdded on 2022/12/26

|13

|2016

|89

AI Summary

This document provides an overview of recording business transactions in T-accounts, ledgers account, trial balance, income statement, and statement of financial position. It also explains the concept of drawings and includes a detailed analysis of the financial position of Linda Ltd through ratio analysis.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Recording Business Transaction

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

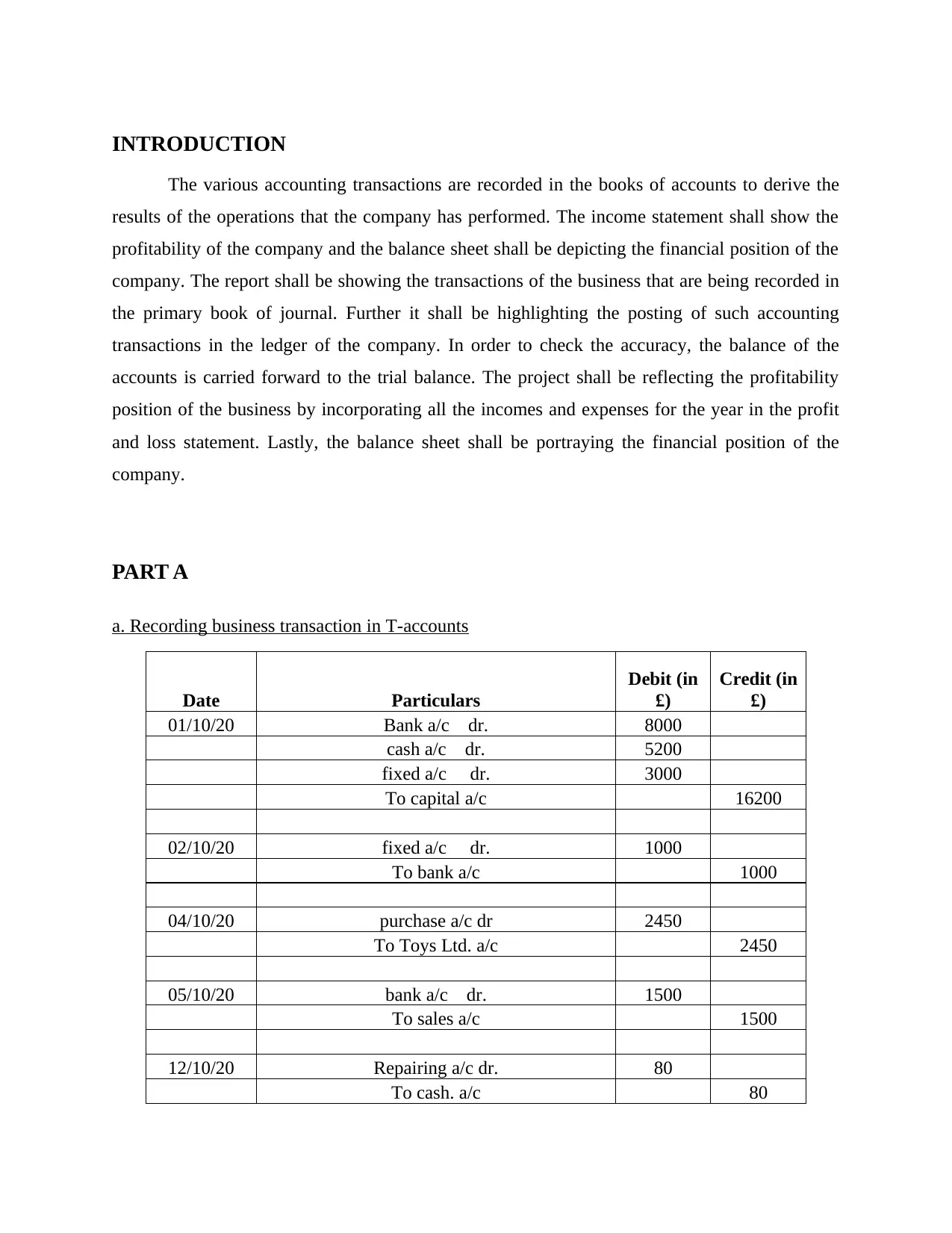

INTRODUCTION

The various accounting transactions are recorded in the books of accounts to derive the

results of the operations that the company has performed. The income statement shall show the

profitability of the company and the balance sheet shall be depicting the financial position of the

company. The report shall be showing the transactions of the business that are being recorded in

the primary book of journal. Further it shall be highlighting the posting of such accounting

transactions in the ledger of the company. In order to check the accuracy, the balance of the

accounts is carried forward to the trial balance. The project shall be reflecting the profitability

position of the business by incorporating all the incomes and expenses for the year in the profit

and loss statement. Lastly, the balance sheet shall be portraying the financial position of the

company.

PART A

a. Recording business transaction in T-accounts

Date Particulars

Debit (in

£)

Credit (in

£)

01/10/20 Bank a/c dr. 8000

cash a/c dr. 5200

fixed a/c dr. 3000

To capital a/c 16200

02/10/20 fixed a/c dr. 1000

To bank a/c 1000

04/10/20 purchase a/c dr 2450

To Toys Ltd. a/c 2450

05/10/20 bank a/c dr. 1500

To sales a/c 1500

12/10/20 Repairing a/c dr. 80

To cash. a/c 80

The various accounting transactions are recorded in the books of accounts to derive the

results of the operations that the company has performed. The income statement shall show the

profitability of the company and the balance sheet shall be depicting the financial position of the

company. The report shall be showing the transactions of the business that are being recorded in

the primary book of journal. Further it shall be highlighting the posting of such accounting

transactions in the ledger of the company. In order to check the accuracy, the balance of the

accounts is carried forward to the trial balance. The project shall be reflecting the profitability

position of the business by incorporating all the incomes and expenses for the year in the profit

and loss statement. Lastly, the balance sheet shall be portraying the financial position of the

company.

PART A

a. Recording business transaction in T-accounts

Date Particulars

Debit (in

£)

Credit (in

£)

01/10/20 Bank a/c dr. 8000

cash a/c dr. 5200

fixed a/c dr. 3000

To capital a/c 16200

02/10/20 fixed a/c dr. 1000

To bank a/c 1000

04/10/20 purchase a/c dr 2450

To Toys Ltd. a/c 2450

05/10/20 bank a/c dr. 1500

To sales a/c 1500

12/10/20 Repairing a/c dr. 80

To cash. a/c 80

18/10/20 Toys ltd. A/c dr

To purchase return a/c 100

100

21/01/20 bank a/c dr. 500

To rent A/c 500

23/10/20 cash a/c dr. 2000

Fred a/c dr 400

To sales A/c 2400

24/10/20 fixed a/c dr. 2500

to bank A/c 2500

26/02/20 Wages A/c dr. 820

To bank A/c 820

30/10/20 Rent A/c dr. 1000

To bank A/c 1000

31/10/20 Drawing A/c dr. 1600

To bank A/c 1600

Total 12950 12950

b. Ledgers account

Bank Account

Date Particular Amt. Date Particular Amt.

02/10/

20 To fixed assets A/c 1000 01/10/20 By capital A/c 8000

24/10/

20 To fixed assets A/c 2500 05/10/20 By sales A/c 1500

26/10/

20 to wages A/c 820 21/10/20 By rent A/c 500

30/10/

20 To rent A/c 1000

31/10/

20 To drawing A/c 1600

To purchase return a/c 100

100

21/01/20 bank a/c dr. 500

To rent A/c 500

23/10/20 cash a/c dr. 2000

Fred a/c dr 400

To sales A/c 2400

24/10/20 fixed a/c dr. 2500

to bank A/c 2500

26/02/20 Wages A/c dr. 820

To bank A/c 820

30/10/20 Rent A/c dr. 1000

To bank A/c 1000

31/10/20 Drawing A/c dr. 1600

To bank A/c 1600

Total 12950 12950

b. Ledgers account

Bank Account

Date Particular Amt. Date Particular Amt.

02/10/

20 To fixed assets A/c 1000 01/10/20 By capital A/c 8000

24/10/

20 To fixed assets A/c 2500 05/10/20 By sales A/c 1500

26/10/

20 to wages A/c 820 21/10/20 By rent A/c 500

30/10/

20 To rent A/c 1000

31/10/

20 To drawing A/c 1600

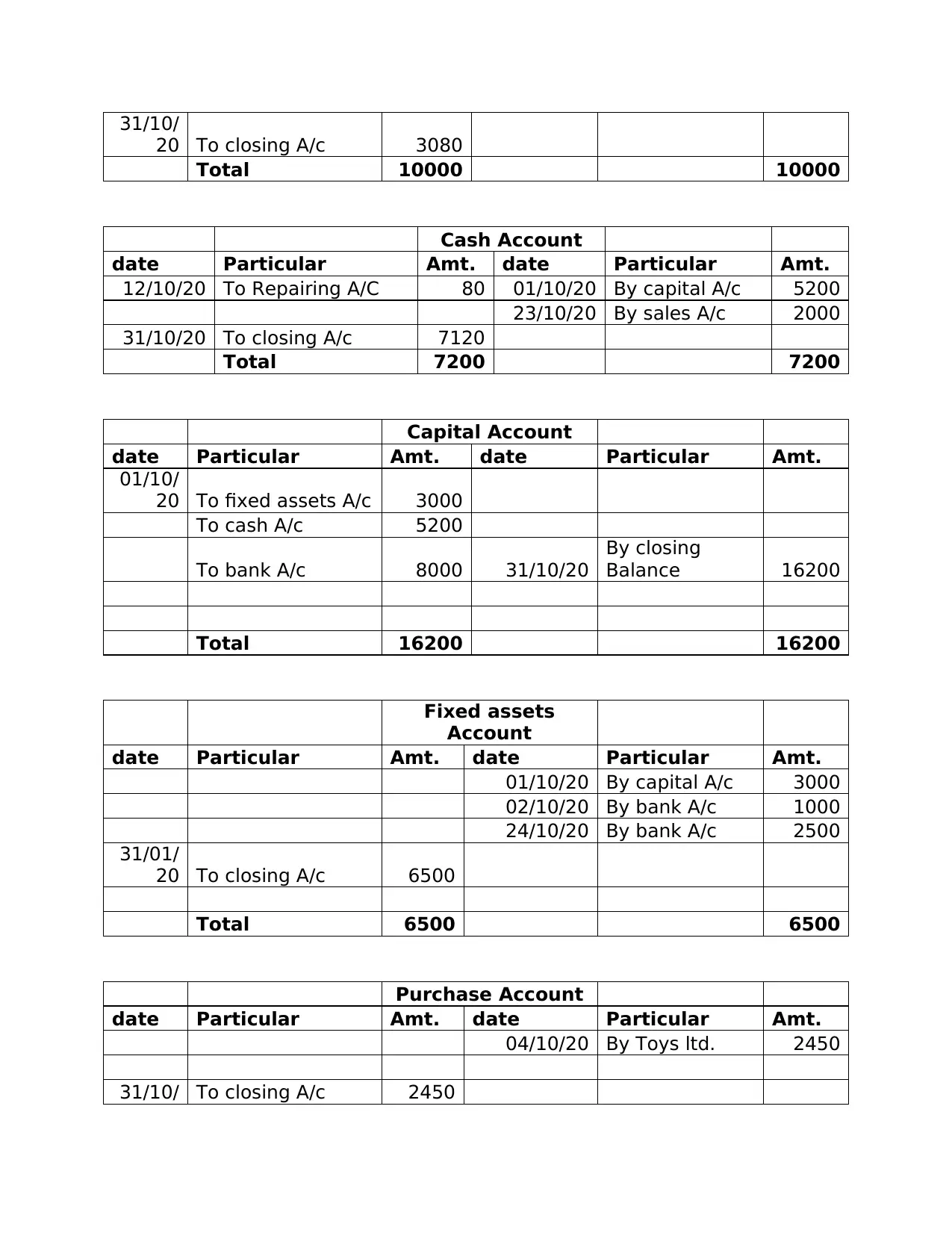

31/10/

20 To closing A/c 3080

Total 10000 10000

Cash Account

date Particular Amt. date Particular Amt.

12/10/20 To Repairing A/C 80 01/10/20 By capital A/c 5200

23/10/20 By sales A/c 2000

31/10/20 To closing A/c 7120

Total 7200 7200

Capital Account

date Particular Amt. date Particular Amt.

01/10/

20 To fixed assets A/c 3000

To cash A/c 5200

To bank A/c 8000 31/10/20

By closing

Balance 16200

Total 16200 16200

Fixed assets

Account

date Particular Amt. date Particular Amt.

01/10/20 By capital A/c 3000

02/10/20 By bank A/c 1000

24/10/20 By bank A/c 2500

31/01/

20 To closing A/c 6500

Total 6500 6500

Purchase Account

date Particular Amt. date Particular Amt.

04/10/20 By Toys ltd. 2450

31/10/ To closing A/c 2450

20 To closing A/c 3080

Total 10000 10000

Cash Account

date Particular Amt. date Particular Amt.

12/10/20 To Repairing A/C 80 01/10/20 By capital A/c 5200

23/10/20 By sales A/c 2000

31/10/20 To closing A/c 7120

Total 7200 7200

Capital Account

date Particular Amt. date Particular Amt.

01/10/

20 To fixed assets A/c 3000

To cash A/c 5200

To bank A/c 8000 31/10/20

By closing

Balance 16200

Total 16200 16200

Fixed assets

Account

date Particular Amt. date Particular Amt.

01/10/20 By capital A/c 3000

02/10/20 By bank A/c 1000

24/10/20 By bank A/c 2500

31/01/

20 To closing A/c 6500

Total 6500 6500

Purchase Account

date Particular Amt. date Particular Amt.

04/10/20 By Toys ltd. 2450

31/10/ To closing A/c 2450

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

20

Total 2450 2450

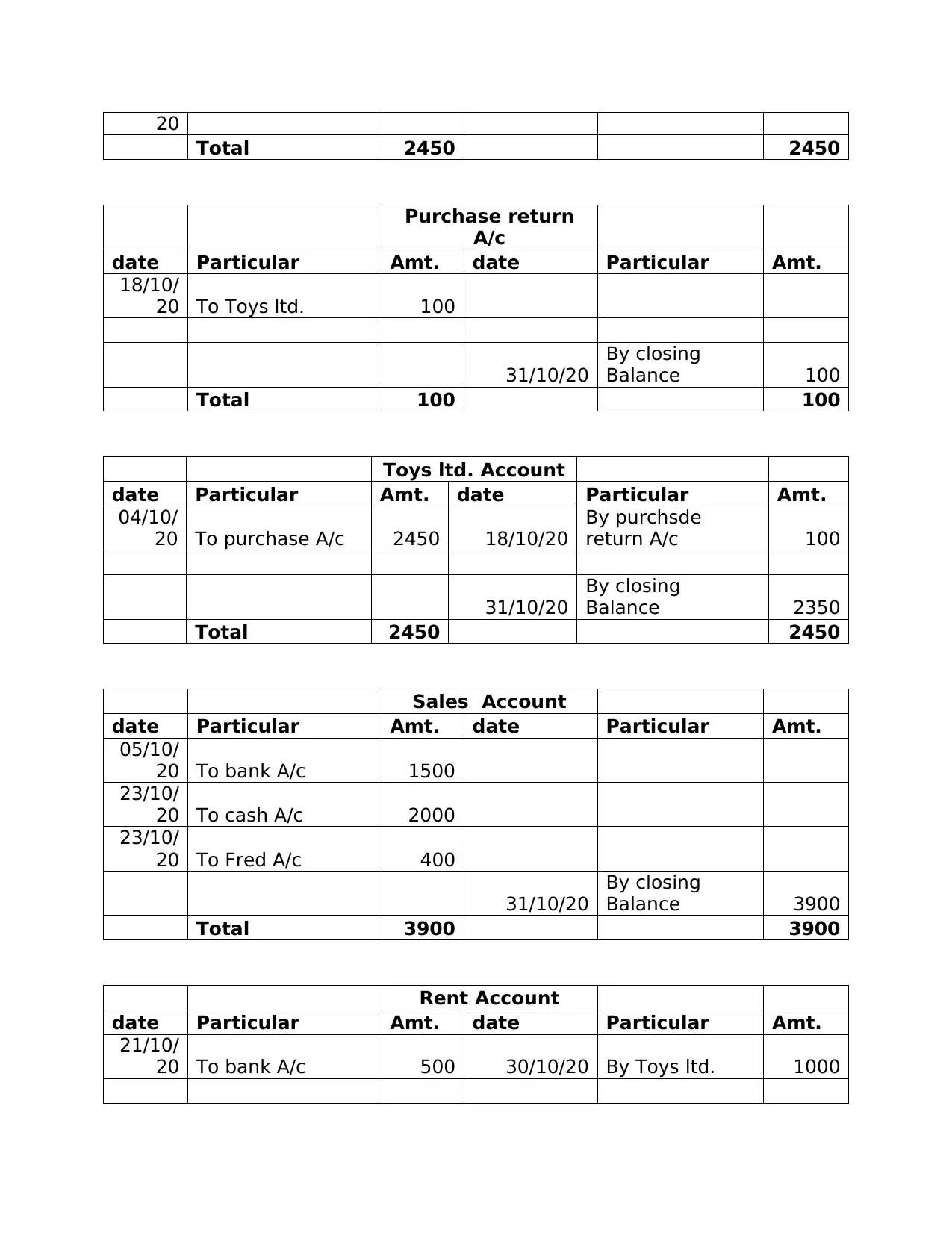

Purchase return

A/c

date Particular Amt. date Particular Amt.

18/10/

20 To Toys ltd. 100

31/10/20

By closing

Balance 100

Total 100 100

Toys ltd. Account

date Particular Amt. date Particular Amt.

04/10/

20 To purchase A/c 2450 18/10/20

By purchsde

return A/c 100

31/10/20

By closing

Balance 2350

Total 2450 2450

Sales Account

date Particular Amt. date Particular Amt.

05/10/

20 To bank A/c 1500

23/10/

20 To cash A/c 2000

23/10/

20 To Fred A/c 400

31/10/20

By closing

Balance 3900

Total 3900 3900

Rent Account

date Particular Amt. date Particular Amt.

21/10/

20 To bank A/c 500 30/10/20 By Toys ltd. 1000

Total 2450 2450

Purchase return

A/c

date Particular Amt. date Particular Amt.

18/10/

20 To Toys ltd. 100

31/10/20

By closing

Balance 100

Total 100 100

Toys ltd. Account

date Particular Amt. date Particular Amt.

04/10/

20 To purchase A/c 2450 18/10/20

By purchsde

return A/c 100

31/10/20

By closing

Balance 2350

Total 2450 2450

Sales Account

date Particular Amt. date Particular Amt.

05/10/

20 To bank A/c 1500

23/10/

20 To cash A/c 2000

23/10/

20 To Fred A/c 400

31/10/20

By closing

Balance 3900

Total 3900 3900

Rent Account

date Particular Amt. date Particular Amt.

21/10/

20 To bank A/c 500 30/10/20 By Toys ltd. 1000

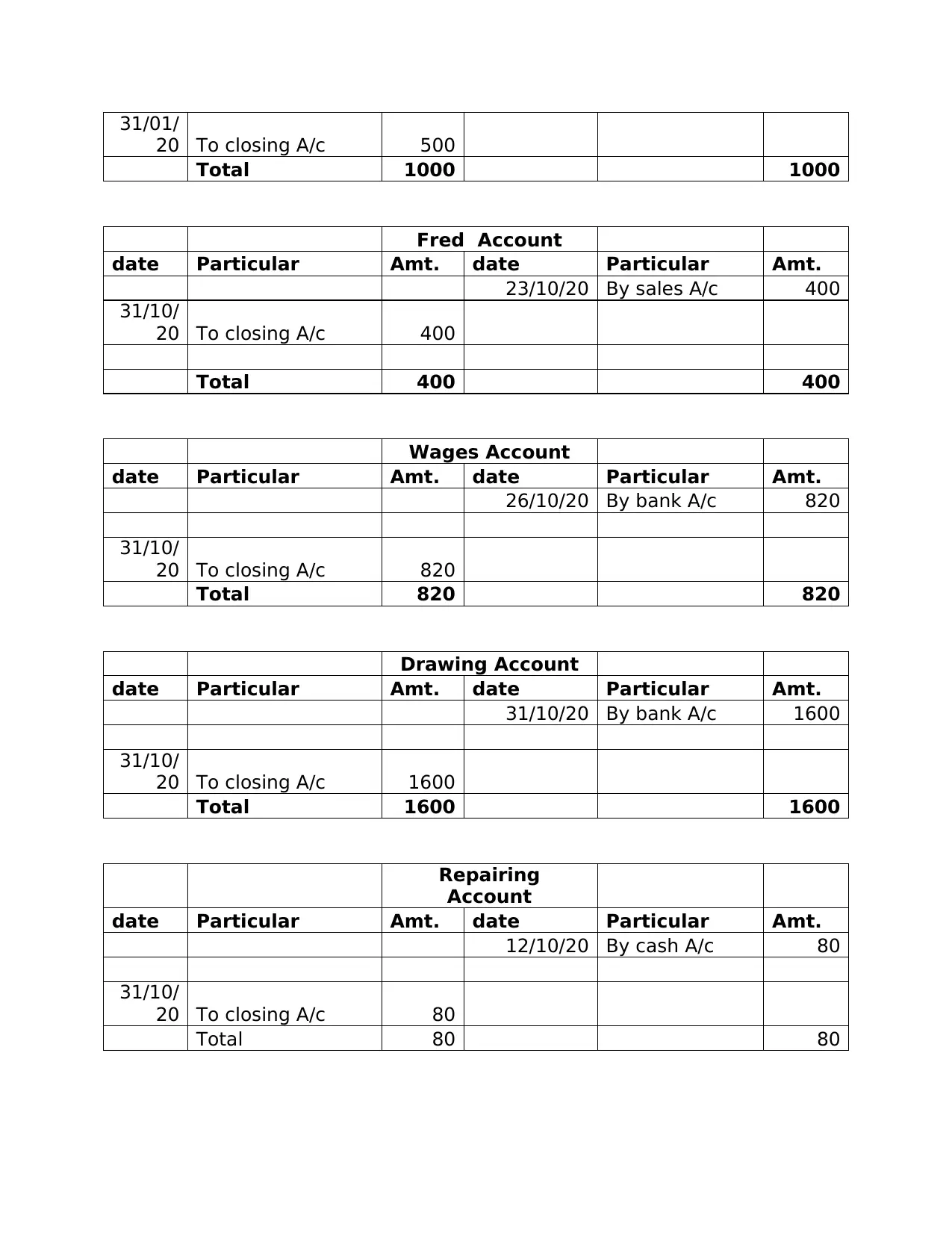

31/01/

20 To closing A/c 500

Total 1000 1000

Fred Account

date Particular Amt. date Particular Amt.

23/10/20 By sales A/c 400

31/10/

20 To closing A/c 400

Total 400 400

Wages Account

date Particular Amt. date Particular Amt.

26/10/20 By bank A/c 820

31/10/

20 To closing A/c 820

Total 820 820

Drawing Account

date Particular Amt. date Particular Amt.

31/10/20 By bank A/c 1600

31/10/

20 To closing A/c 1600

Total 1600 1600

Repairing

Account

date Particular Amt. date Particular Amt.

12/10/20 By cash A/c 80

31/10/

20 To closing A/c 80

Total 80 80

20 To closing A/c 500

Total 1000 1000

Fred Account

date Particular Amt. date Particular Amt.

23/10/20 By sales A/c 400

31/10/

20 To closing A/c 400

Total 400 400

Wages Account

date Particular Amt. date Particular Amt.

26/10/20 By bank A/c 820

31/10/

20 To closing A/c 820

Total 820 820

Drawing Account

date Particular Amt. date Particular Amt.

31/10/20 By bank A/c 1600

31/10/

20 To closing A/c 1600

Total 1600 1600

Repairing

Account

date Particular Amt. date Particular Amt.

12/10/20 By cash A/c 80

31/10/

20 To closing A/c 80

Total 80 80

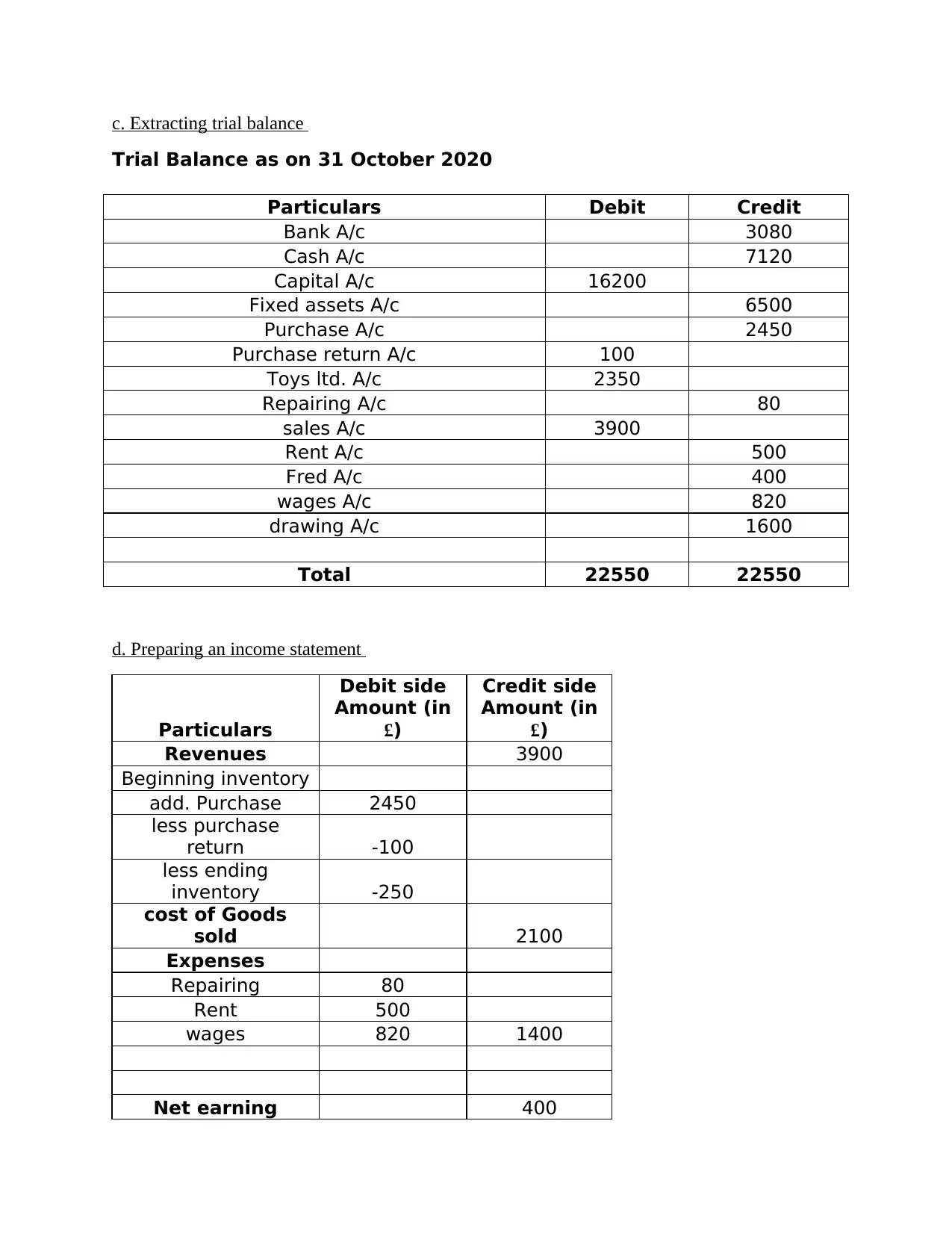

c. Extracting trial balance

Trial Balance as on 31 October 2020

Particulars Debit Credit

Bank A/c 3080

Cash A/c 7120

Capital A/c 16200

Fixed assets A/c 6500

Purchase A/c 2450

Purchase return A/c 100

Toys ltd. A/c 2350

Repairing A/c 80

sales A/c 3900

Rent A/c 500

Fred A/c 400

wages A/c 820

drawing A/c 1600

Total 22550 22550

d. Preparing an income statement

Particulars

Debit side

Amount (in

£)

Credit side

Amount (in

£)

Revenues 3900

Beginning inventory

add. Purchase 2450

less purchase

return -100

less ending

inventory -250

cost of Goods

sold 2100

Expenses

Repairing 80

Rent 500

wages 820 1400

Net earning 400

Trial Balance as on 31 October 2020

Particulars Debit Credit

Bank A/c 3080

Cash A/c 7120

Capital A/c 16200

Fixed assets A/c 6500

Purchase A/c 2450

Purchase return A/c 100

Toys ltd. A/c 2350

Repairing A/c 80

sales A/c 3900

Rent A/c 500

Fred A/c 400

wages A/c 820

drawing A/c 1600

Total 22550 22550

d. Preparing an income statement

Particulars

Debit side

Amount (in

£)

Credit side

Amount (in

£)

Revenues 3900

Beginning inventory

add. Purchase 2450

less purchase

return -100

less ending

inventory -250

cost of Goods

sold 2100

Expenses

Repairing 80

Rent 500

wages 820 1400

Net earning 400

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

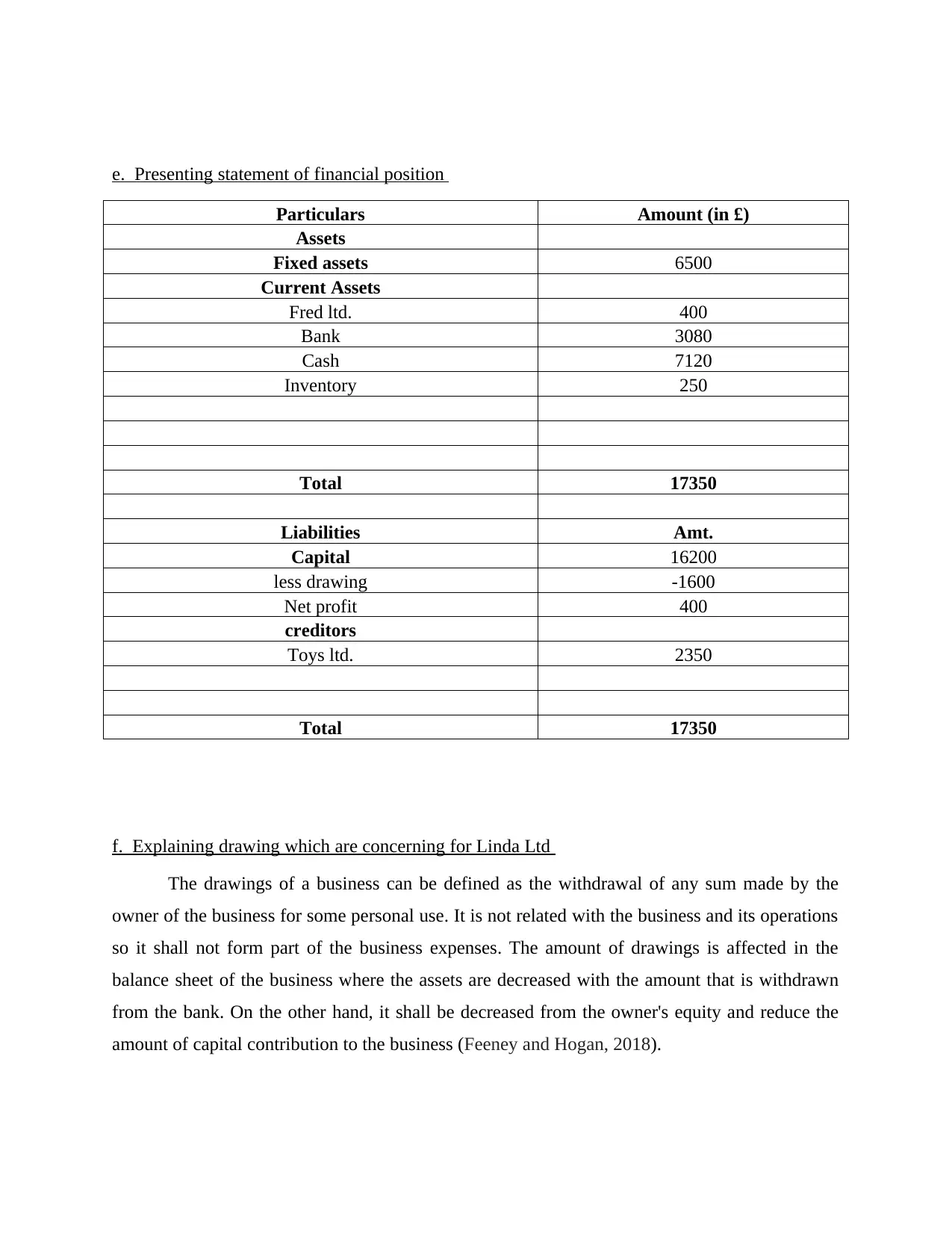

e. Presenting statement of financial position

Particulars Amount (in £)

Assets

Fixed assets 6500

Current Assets

Fred ltd. 400

Bank 3080

Cash 7120

Inventory 250

Total 17350

Liabilities Amt.

Capital 16200

less drawing -1600

Net profit 400

creditors

Toys ltd. 2350

Total 17350

f. Explaining drawing which are concerning for Linda Ltd

The drawings of a business can be defined as the withdrawal of any sum made by the

owner of the business for some personal use. It is not related with the business and its operations

so it shall not form part of the business expenses. The amount of drawings is affected in the

balance sheet of the business where the assets are decreased with the amount that is withdrawn

from the bank. On the other hand, it shall be decreased from the owner's equity and reduce the

amount of capital contribution to the business (Feeney and Hogan, 2018).

Particulars Amount (in £)

Assets

Fixed assets 6500

Current Assets

Fred ltd. 400

Bank 3080

Cash 7120

Inventory 250

Total 17350

Liabilities Amt.

Capital 16200

less drawing -1600

Net profit 400

creditors

Toys ltd. 2350

Total 17350

f. Explaining drawing which are concerning for Linda Ltd

The drawings of a business can be defined as the withdrawal of any sum made by the

owner of the business for some personal use. It is not related with the business and its operations

so it shall not form part of the business expenses. The amount of drawings is affected in the

balance sheet of the business where the assets are decreased with the amount that is withdrawn

from the bank. On the other hand, it shall be decreased from the owner's equity and reduce the

amount of capital contribution to the business (Feeney and Hogan, 2018).

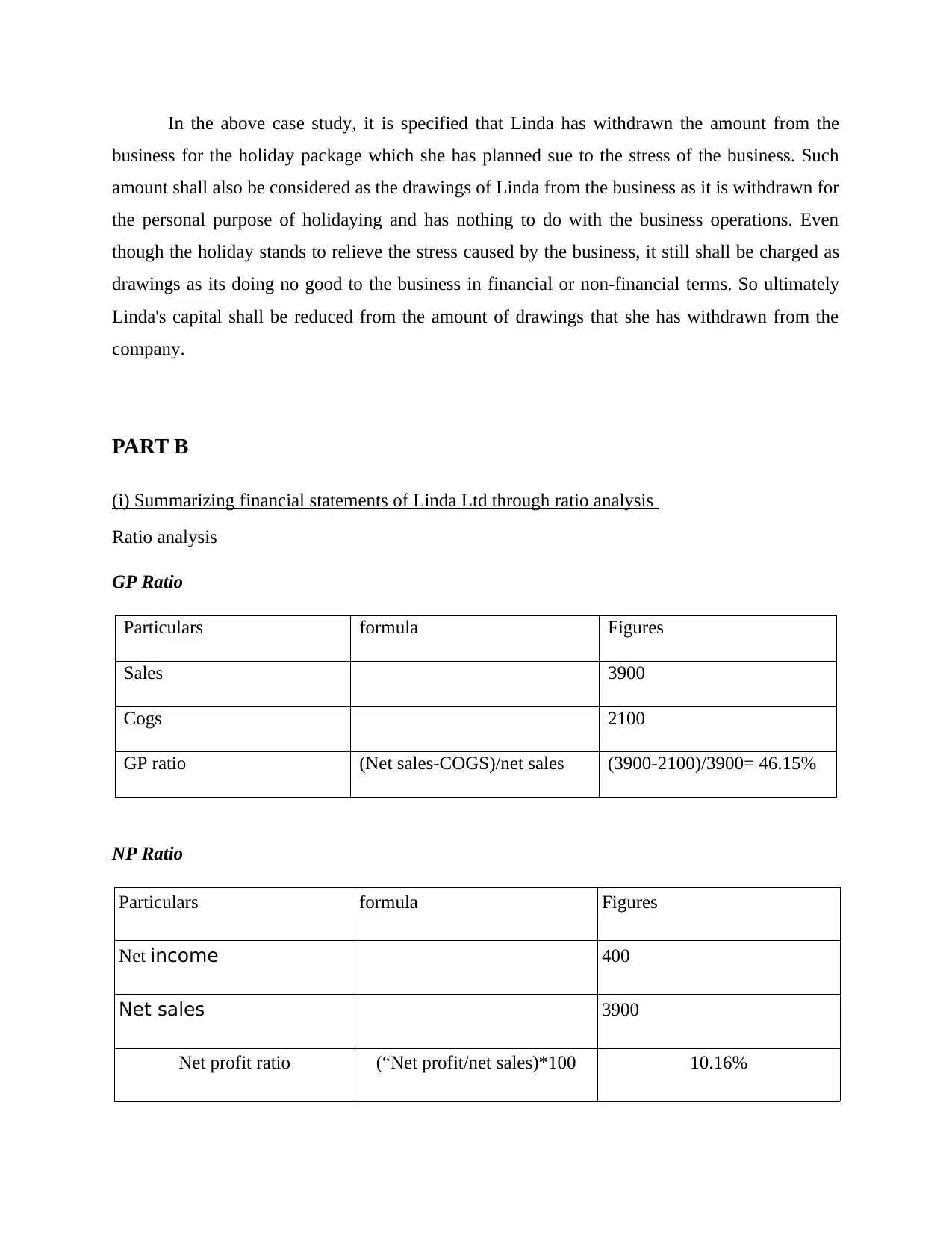

In the above case study, it is specified that Linda has withdrawn the amount from the

business for the holiday package which she has planned sue to the stress of the business. Such

amount shall also be considered as the drawings of Linda from the business as it is withdrawn for

the personal purpose of holidaying and has nothing to do with the business operations. Even

though the holiday stands to relieve the stress caused by the business, it still shall be charged as

drawings as its doing no good to the business in financial or non-financial terms. So ultimately

Linda's capital shall be reduced from the amount of drawings that she has withdrawn from the

company.

PART B

(i) Summarizing financial statements of Linda Ltd through ratio analysis

Ratio analysis

GP Ratio

Particulars formula Figures

Sales 3900

Cogs 2100

GP ratio (Net sales-COGS)/net sales (3900-2100)/3900= 46.15%

NP Ratio

Particulars formula Figures

Net income 400

Net sales 3900

Net profit ratio (“Net profit/net sales)*100 10.16%

business for the holiday package which she has planned sue to the stress of the business. Such

amount shall also be considered as the drawings of Linda from the business as it is withdrawn for

the personal purpose of holidaying and has nothing to do with the business operations. Even

though the holiday stands to relieve the stress caused by the business, it still shall be charged as

drawings as its doing no good to the business in financial or non-financial terms. So ultimately

Linda's capital shall be reduced from the amount of drawings that she has withdrawn from the

company.

PART B

(i) Summarizing financial statements of Linda Ltd through ratio analysis

Ratio analysis

GP Ratio

Particulars formula Figures

Sales 3900

Cogs 2100

GP ratio (Net sales-COGS)/net sales (3900-2100)/3900= 46.15%

NP Ratio

Particulars formula Figures

Net income 400

Net sales 3900

Net profit ratio (“Net profit/net sales)*100 10.16%

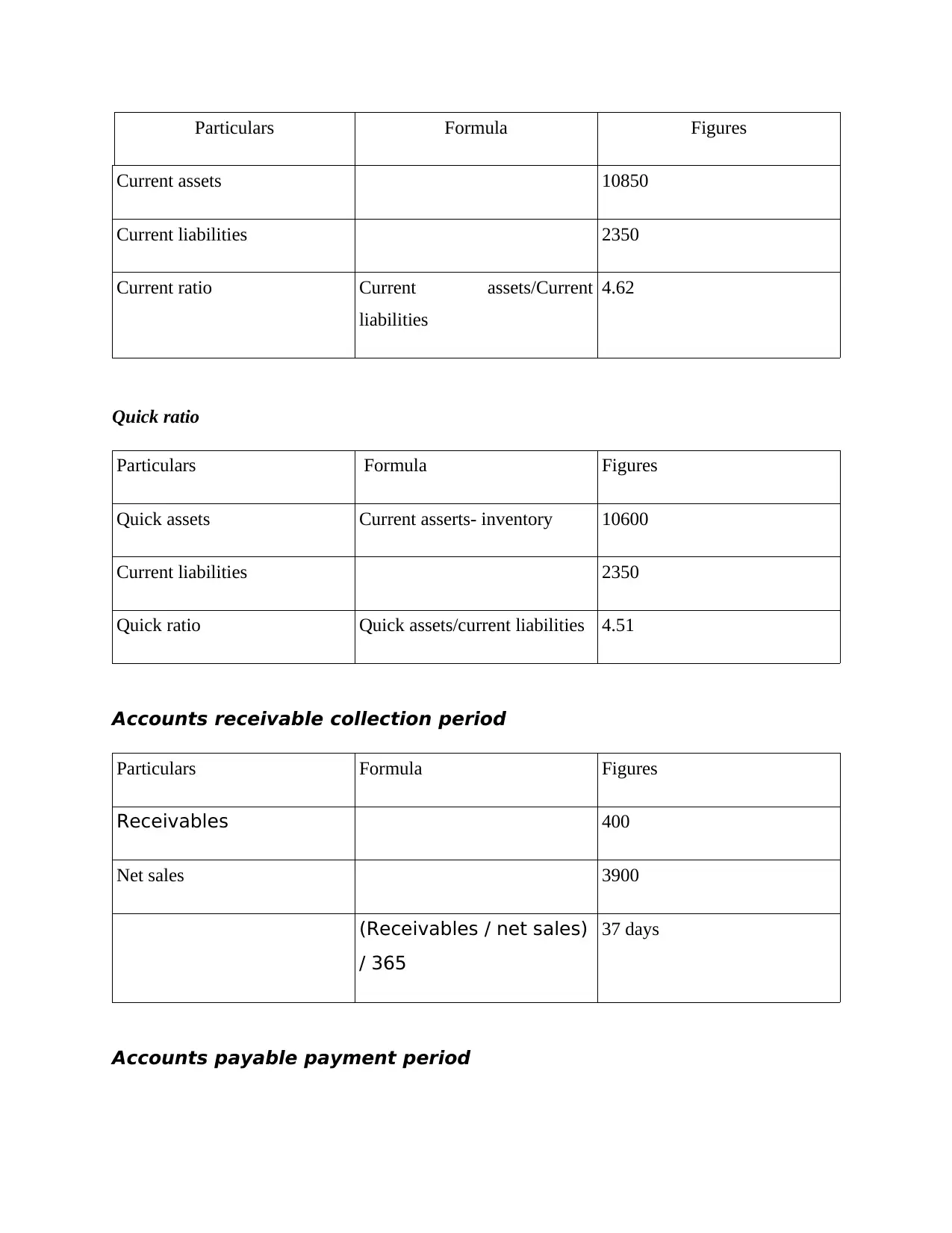

Particulars Formula Figures

Current assets 10850

Current liabilities 2350

Current ratio Current assets/Current

liabilities

4.62

Quick ratio

Particulars Formula Figures

Quick assets Current asserts- inventory 10600

Current liabilities 2350

Quick ratio Quick assets/current liabilities 4.51

Accounts receivable collection period

Particulars Formula Figures

Receivables 400

Net sales 3900

(Receivables / net sales)

/ 365

37 days

Accounts payable payment period

Current assets 10850

Current liabilities 2350

Current ratio Current assets/Current

liabilities

4.62

Quick ratio

Particulars Formula Figures

Quick assets Current asserts- inventory 10600

Current liabilities 2350

Quick ratio Quick assets/current liabilities 4.51

Accounts receivable collection period

Particulars Formula Figures

Receivables 400

Net sales 3900

(Receivables / net sales)

/ 365

37 days

Accounts payable payment period

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

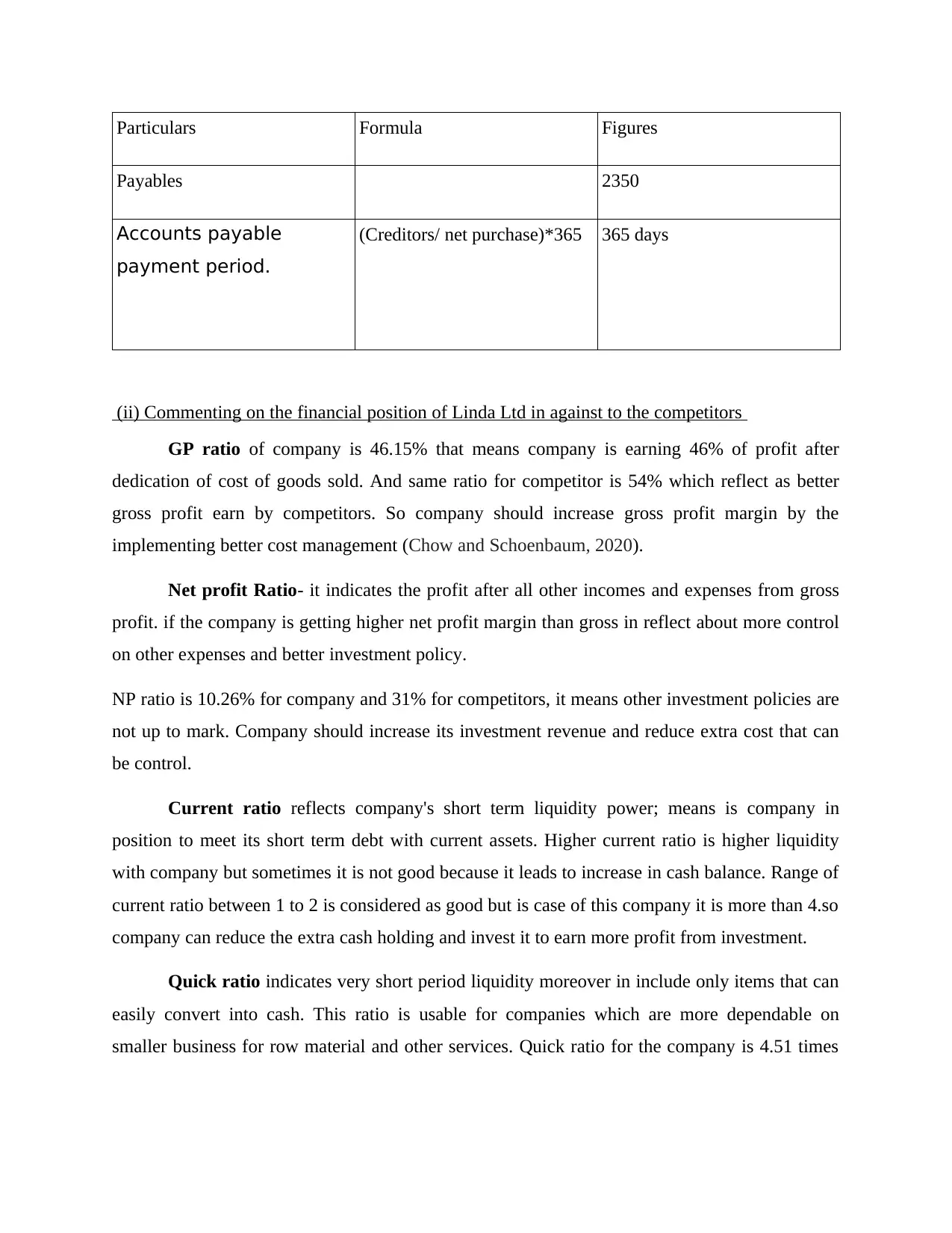

Particulars Formula Figures

Payables 2350

Accounts payable

payment period.

(Creditors/ net purchase)*365 365 days

(ii) Commenting on the financial position of Linda Ltd in against to the competitors

GP ratio of company is 46.15% that means company is earning 46% of profit after

dedication of cost of goods sold. And same ratio for competitor is 54% which reflect as better

gross profit earn by competitors. So company should increase gross profit margin by the

implementing better cost management (Chow and Schoenbaum, 2020).

Net profit Ratio- it indicates the profit after all other incomes and expenses from gross

profit. if the company is getting higher net profit margin than gross in reflect about more control

on other expenses and better investment policy.

NP ratio is 10.26% for company and 31% for competitors, it means other investment policies are

not up to mark. Company should increase its investment revenue and reduce extra cost that can

be control.

Current ratio reflects company's short term liquidity power; means is company in

position to meet its short term debt with current assets. Higher current ratio is higher liquidity

with company but sometimes it is not good because it leads to increase in cash balance. Range of

current ratio between 1 to 2 is considered as good but is case of this company it is more than 4.so

company can reduce the extra cash holding and invest it to earn more profit from investment.

Quick ratio indicates very short period liquidity moreover in include only items that can

easily convert into cash. This ratio is usable for companies which are more dependable on

smaller business for row material and other services. Quick ratio for the company is 4.51 times

Payables 2350

Accounts payable

payment period.

(Creditors/ net purchase)*365 365 days

(ii) Commenting on the financial position of Linda Ltd in against to the competitors

GP ratio of company is 46.15% that means company is earning 46% of profit after

dedication of cost of goods sold. And same ratio for competitor is 54% which reflect as better

gross profit earn by competitors. So company should increase gross profit margin by the

implementing better cost management (Chow and Schoenbaum, 2020).

Net profit Ratio- it indicates the profit after all other incomes and expenses from gross

profit. if the company is getting higher net profit margin than gross in reflect about more control

on other expenses and better investment policy.

NP ratio is 10.26% for company and 31% for competitors, it means other investment policies are

not up to mark. Company should increase its investment revenue and reduce extra cost that can

be control.

Current ratio reflects company's short term liquidity power; means is company in

position to meet its short term debt with current assets. Higher current ratio is higher liquidity

with company but sometimes it is not good because it leads to increase in cash balance. Range of

current ratio between 1 to 2 is considered as good but is case of this company it is more than 4.so

company can reduce the extra cash holding and invest it to earn more profit from investment.

Quick ratio indicates very short period liquidity moreover in include only items that can

easily convert into cash. This ratio is usable for companies which are more dependable on

smaller business for row material and other services. Quick ratio for the company is 4.51 times

and for competitors it is1.35 times so clearly company needs to decrease it and investment more

money it production activities and investment.

Average collection period shows time will be taken by debtors to company to get money

back lower period reflect more efficient working capital management. If company has lower

collection period than it need not carry extra cash for payment. The ratio is 37 days for company

and 50 days for competitors it is good, means company is getting money from debtors faster than

competitors.

Average payable period it shows the negotiation power of company, how to

convenience the creditors to get delay in making payment (Manehat, Irianto and Purwanti, 2019).

So company can enjoy liquidity for longer period. Ratio is 72 days for competitors that shows

competitors has to pay money in 72 days to creditors but for Linda company it is 365 days that

means they are in better position to reduce the more liquidity and make other function strong.

Form comparison of these we can clearly understand that company need to reduce it

liquidity and use cost accountancy to improve cost part. Extra liquidity can be invested to get

some extra return

CONCLUSION

It can be summarized from the above report that accounting the transactions of the

business is very important for the business decision-making process and to serve to the internal

and the external users of these statements of accounts. The profitability and the financial position

of the company can be known and also it facilitates in knowing the profitable and the non-

profitable ventures of the business. The drawings from the business for personal use shall

decrease the capital contribution that is made by the owner. The ratio analysis also facilitates

knowing the liquidity, efficiency and financial position of the business. It also facilitates

comparison internally with the other departments and externally with the competitors in the

industry. This shall help in the decisions that are to be taken in the future so that the profitability

and growth prospects of the business can be maximized.

money it production activities and investment.

Average collection period shows time will be taken by debtors to company to get money

back lower period reflect more efficient working capital management. If company has lower

collection period than it need not carry extra cash for payment. The ratio is 37 days for company

and 50 days for competitors it is good, means company is getting money from debtors faster than

competitors.

Average payable period it shows the negotiation power of company, how to

convenience the creditors to get delay in making payment (Manehat, Irianto and Purwanti, 2019).

So company can enjoy liquidity for longer period. Ratio is 72 days for competitors that shows

competitors has to pay money in 72 days to creditors but for Linda company it is 365 days that

means they are in better position to reduce the more liquidity and make other function strong.

Form comparison of these we can clearly understand that company need to reduce it

liquidity and use cost accountancy to improve cost part. Extra liquidity can be invested to get

some extra return

CONCLUSION

It can be summarized from the above report that accounting the transactions of the

business is very important for the business decision-making process and to serve to the internal

and the external users of these statements of accounts. The profitability and the financial position

of the company can be known and also it facilitates in knowing the profitable and the non-

profitable ventures of the business. The drawings from the business for personal use shall

decrease the capital contribution that is made by the owner. The ratio analysis also facilitates

knowing the liquidity, efficiency and financial position of the business. It also facilitates

comparison internally with the other departments and externally with the competitors in the

industry. This shall help in the decisions that are to be taken in the future so that the profitability

and growth prospects of the business can be maximized.

REFERENCES

Books and Journals

Feeney, S. and Hogan, J., 2018. Drawings of Corporate Social Responsibility: a Picture Draws a

Thousand Words. Irish Journal of Academic Practice. 7(1). p.1.

Chow, D. C. and Schoenbaum, T. J., 2020. International business transactions: problems, cases,

and materials. Wolters Kluwer Law & Business.

Manehat, B. Y., Irianto, G. and Purwanti, L., 2019. Payment System and Brideprice Recording in

Belu-Indonesia. International Journal of Multicultural and Multireligious

Understanding. 6(2). pp.303-310.

Online

Books and Journals

Feeney, S. and Hogan, J., 2018. Drawings of Corporate Social Responsibility: a Picture Draws a

Thousand Words. Irish Journal of Academic Practice. 7(1). p.1.

Chow, D. C. and Schoenbaum, T. J., 2020. International business transactions: problems, cases,

and materials. Wolters Kluwer Law & Business.

Manehat, B. Y., Irianto, G. and Purwanti, L., 2019. Payment System and Brideprice Recording in

Belu-Indonesia. International Journal of Multicultural and Multireligious

Understanding. 6(2). pp.303-310.

Online

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.