Investment Report: Financial Analysis of Redding Co. & Neaves Co.

VerifiedAdded on 2023/06/07

|16

|3844

|436

Report

AI Summary

This report provides a comprehensive financial analysis of Redding Co. and Neaves Co. to determine their suitability as investment choices. It utilizes key financial ratios related to profitability, efficiency, liquidity, gearing, and investor returns to compare the performance of the two companies. The analysis reveals that Neaves Co. generally outperforms Redding Co. in areas such as net profit margin, return on capital employed, stock turnover ratio, debtors’ turnover ratio, debt-to-equity ratio, and interest cover ratio. While Redding Co. shows a higher current ratio, Neaves Co.'s superior performance in other critical areas suggests it may be a more attractive investment option. The report concludes with insights valuable for potential investors seeking to make informed decisions based on a thorough evaluation of the companies' financial health and performance.

Running Head: Report on Redding Co. or Neaves Co. as an investment choice for potential investors

Report on Redding Co. or Neaves Co. as an investment choice for potential investors

[Document subtitle]

[DATE]

Institution Name

PROFESSOR NAME

Report on Redding Co. or Neaves Co. as an investment choice for potential investors

[Document subtitle]

[DATE]

Institution Name

PROFESSOR NAME

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Report on Redding Co. or Neaves Co. as an investment choice for potential investors

Section 1: Corporate performance analysis through financial ratios:

(a) Ratios pertaining to profitability: The significance of ratios pertaining to profitability

comes from the ability of these ratios to give an idea of how the absolute amounts of the

profits made by a business stack up vis-à-vis other amounts such as capital employed in the

business or sales effected by the business or the like. Often, the amount of profit alone may

look attractive but only when this amount is related with or linked to another number (such as

capital employed, sales, etc) does the real picture emerge in terms of whether these profits are

sufficient/justifiable or not. While profit is an absolute concept, profitability is a relative

concept.

Here, a comparison of the two companies is presented based on the following two ratios (for

computation of the ratio, please refer Appendix 1).

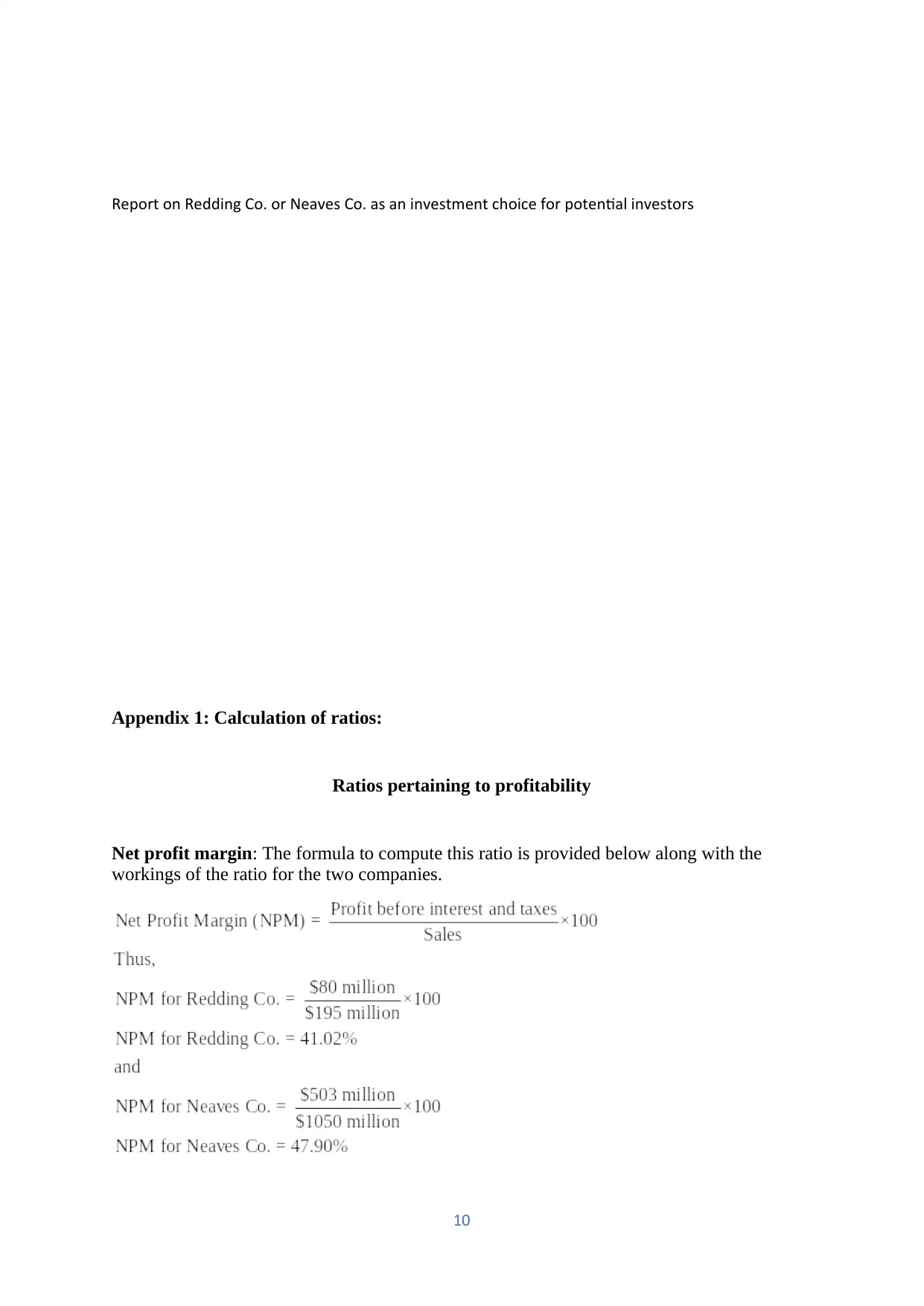

Net profit margin:

Significance in being considered for analysis and what this ratio measures:

This ratio is significant given that it measures a company’s profit which remains after the

company has met its operating costs.

Comparison between the companies and explanation for the same:

The net profit margins for Redding Co. and for Neaves Co. are respectively 41.02% and

47.90%.

Neaves Co. did a comparatively better job at managing its operating costs so that the

company ends up with a better net profit margin as compared to Redding Co. This is worth

appreciating given that this company is newer and has grown through acquisitions; the

company seems to have done well in ensuring proper control over operating costs.

Return on capital employed:

Significance in being considered for analysis and what this ratio measures:

This ratio is significant in that it reflects the percentage of profits before interest and taxes

that a company's capital employed is able to fetch to the company. Profits before interest are

considered here since this profit figure is of relevance to those expecting interest payments

from the company (debt capital providers) and those expecting dividends from the company

(shareholders).

Comparison between the companies and explanation for the same:

1

Section 1: Corporate performance analysis through financial ratios:

(a) Ratios pertaining to profitability: The significance of ratios pertaining to profitability

comes from the ability of these ratios to give an idea of how the absolute amounts of the

profits made by a business stack up vis-à-vis other amounts such as capital employed in the

business or sales effected by the business or the like. Often, the amount of profit alone may

look attractive but only when this amount is related with or linked to another number (such as

capital employed, sales, etc) does the real picture emerge in terms of whether these profits are

sufficient/justifiable or not. While profit is an absolute concept, profitability is a relative

concept.

Here, a comparison of the two companies is presented based on the following two ratios (for

computation of the ratio, please refer Appendix 1).

Net profit margin:

Significance in being considered for analysis and what this ratio measures:

This ratio is significant given that it measures a company’s profit which remains after the

company has met its operating costs.

Comparison between the companies and explanation for the same:

The net profit margins for Redding Co. and for Neaves Co. are respectively 41.02% and

47.90%.

Neaves Co. did a comparatively better job at managing its operating costs so that the

company ends up with a better net profit margin as compared to Redding Co. This is worth

appreciating given that this company is newer and has grown through acquisitions; the

company seems to have done well in ensuring proper control over operating costs.

Return on capital employed:

Significance in being considered for analysis and what this ratio measures:

This ratio is significant in that it reflects the percentage of profits before interest and taxes

that a company's capital employed is able to fetch to the company. Profits before interest are

considered here since this profit figure is of relevance to those expecting interest payments

from the company (debt capital providers) and those expecting dividends from the company

(shareholders).

Comparison between the companies and explanation for the same:

1

Report on Redding Co. or Neaves Co. as an investment choice for potential investors

The returns on capital employed for Redding Co. and for Neaves Co. are respectively 27.59%

and 47.41%.

In terms of return on capital employed, Neaves Co. seems to have done way better than

Redding Co. and a part of the reason is Neaves Co.’s management of its operating expenses

besides being able to make better use of capital.

(b) Ratios pertaining to efficiency: The significance of ratios pertaining to efficiency lies in

the fact that each company is accountable to its owners for efficiently managing the company

assets in the pursuit of attaining the ultimate goal of maximization of wealth for the company

owners. Ratios pertaining to efficiency throw light on whether or not the company has

optimally managed its assets, be they current assets or other assets. Thus, how good the

company has been at managing its short-term assets (such as debtors, inventory, etc) and its

long-lived assets is what gets measured through these ratios. Any failure in the optimum

management of these assets will imply inefficiencies which can be a drag on the company’s

profits as well as profitability.

Here, a comparison of the two companies is presented based on the following two ratios (for

computation of the ratio, please refer Appendix 1).

Stock turnover ratio:

Significance in being considered for analysis and what this ratio measures:

This ratio indicates how good or otherwise is the company in terms of turning over its

inventory and converting it into cash. This helps to understand whether or not the company's

inventory is marketable enough to assure adequate liquidity for the company.

Comparison between the companies and explanation for the same:

The stock turnover ratios for Redding Co. and for Neaves Co. are respectively 5.20 times and

8.02 times.

Neaves Co. has a higher stock turnover ratio when compared with Redding Co. This indicates

that Neaves Co. has been much more successful at being able to sell its products and convert

the inventory into cash.

Debtors’ turnover ratio:

Significance in being considered for analysis and what this ratio measures:

This ratio indicates how quickly or otherwise is the company able to convert its debtors into

cash. This helps to understand whether or not the company's collection efforts are

2

The returns on capital employed for Redding Co. and for Neaves Co. are respectively 27.59%

and 47.41%.

In terms of return on capital employed, Neaves Co. seems to have done way better than

Redding Co. and a part of the reason is Neaves Co.’s management of its operating expenses

besides being able to make better use of capital.

(b) Ratios pertaining to efficiency: The significance of ratios pertaining to efficiency lies in

the fact that each company is accountable to its owners for efficiently managing the company

assets in the pursuit of attaining the ultimate goal of maximization of wealth for the company

owners. Ratios pertaining to efficiency throw light on whether or not the company has

optimally managed its assets, be they current assets or other assets. Thus, how good the

company has been at managing its short-term assets (such as debtors, inventory, etc) and its

long-lived assets is what gets measured through these ratios. Any failure in the optimum

management of these assets will imply inefficiencies which can be a drag on the company’s

profits as well as profitability.

Here, a comparison of the two companies is presented based on the following two ratios (for

computation of the ratio, please refer Appendix 1).

Stock turnover ratio:

Significance in being considered for analysis and what this ratio measures:

This ratio indicates how good or otherwise is the company in terms of turning over its

inventory and converting it into cash. This helps to understand whether or not the company's

inventory is marketable enough to assure adequate liquidity for the company.

Comparison between the companies and explanation for the same:

The stock turnover ratios for Redding Co. and for Neaves Co. are respectively 5.20 times and

8.02 times.

Neaves Co. has a higher stock turnover ratio when compared with Redding Co. This indicates

that Neaves Co. has been much more successful at being able to sell its products and convert

the inventory into cash.

Debtors’ turnover ratio:

Significance in being considered for analysis and what this ratio measures:

This ratio indicates how quickly or otherwise is the company able to convert its debtors into

cash. This helps to understand whether or not the company's collection efforts are

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Report on Redding Co. or Neaves Co. as an investment choice for potential investors

commensurate with the quality of its receivables so that the company is able to ensure the

liquidity of its receivables.

Comparison between the companies and explanation for the same:

The debtors’ turnover ratios for Redding Co. and for Neaves Co. are respectively 3.90 times

and 7.72 times.

Neaves Co. has a better debtors' turnover ratio signaling that its collection efforts are much

more successful than those of Redding Co. In fact, less satisfactory collections performance

of Redding Co. has forced the company into overdrawing from its bank accounts, as is

evident from the company’s statement of financial position.

(c) Ratios pertaining to liquidity: The significance of ratios pertaining to liquidity lies in the

fact that businesses always need to have sufficient amounts of cash or assets that can be

converted into cash if there were a need to meet short-term obligations. Thus, these ratios

measure a company’s ability to maintain the requisite levels of liquidity to pay bills in the

short term. Failure to maintain the required liquidity will compel a business to resort to short-

term borrowings which would have costs attached to the borrowed amounts. These costs

would unnecessarily go on to hurt the company’s profits and profitability.

Here, a comparison of the two companies is presented based on the following two ratios (for

computation of the ratio, please refer Appendix 1).

Current ratio:

Significance in being considered for analysis and what this ratio measures:

This ratio measures the company's ability to pay off its current or short-term obligations by

resorting to its short-term or current assets. This ratio, thus, shows the number of times a

company's current assets are able to cover its current liabilities.

Comparison between the companies and explanation for the same:

The current ratios for Redding Co. and for Neaves Co. are respectively 2.17 and 1.29.

The current ratio of Neaves Co. is lower than that of Redding Co. since Neaves Co. seems to

have been depending much more on utilizing its current liabilities and delaying payments to

the extent possible.

Quick ratio:

Significance in being considered for analysis and what this ratio measures:

3

commensurate with the quality of its receivables so that the company is able to ensure the

liquidity of its receivables.

Comparison between the companies and explanation for the same:

The debtors’ turnover ratios for Redding Co. and for Neaves Co. are respectively 3.90 times

and 7.72 times.

Neaves Co. has a better debtors' turnover ratio signaling that its collection efforts are much

more successful than those of Redding Co. In fact, less satisfactory collections performance

of Redding Co. has forced the company into overdrawing from its bank accounts, as is

evident from the company’s statement of financial position.

(c) Ratios pertaining to liquidity: The significance of ratios pertaining to liquidity lies in the

fact that businesses always need to have sufficient amounts of cash or assets that can be

converted into cash if there were a need to meet short-term obligations. Thus, these ratios

measure a company’s ability to maintain the requisite levels of liquidity to pay bills in the

short term. Failure to maintain the required liquidity will compel a business to resort to short-

term borrowings which would have costs attached to the borrowed amounts. These costs

would unnecessarily go on to hurt the company’s profits and profitability.

Here, a comparison of the two companies is presented based on the following two ratios (for

computation of the ratio, please refer Appendix 1).

Current ratio:

Significance in being considered for analysis and what this ratio measures:

This ratio measures the company's ability to pay off its current or short-term obligations by

resorting to its short-term or current assets. This ratio, thus, shows the number of times a

company's current assets are able to cover its current liabilities.

Comparison between the companies and explanation for the same:

The current ratios for Redding Co. and for Neaves Co. are respectively 2.17 and 1.29.

The current ratio of Neaves Co. is lower than that of Redding Co. since Neaves Co. seems to

have been depending much more on utilizing its current liabilities and delaying payments to

the extent possible.

Quick ratio:

Significance in being considered for analysis and what this ratio measures:

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Report on Redding Co. or Neaves Co. as an investment choice for potential investors

This ratio, just as current ratio does, measures the company’s ability to pay of its current or

short-term liabilities but differs from the current ratio as the quick ratio only allows current

assets other than inventory and prepaid expenses to be considered in determining the

company’s ability to meet its short-term liabilities.

Comparison between the companies and explanation for the same:

The quick ratios for Redding Co. and for Neaves Co. are respectively 1.67 and 1.07.

While there was a larger difference between the two companies’ current ratios, there is not

that large a difference between the two companies’ quick ratios. This is attributable to the fact

that for Neaves Co. inventory is just about 17% of its current assets while for Redding Co.

inventory is close to 23% of its current assets. This observation is in line with the fact that

Redding Co.’s inventory turnover ratio was lower than that of Neaves Co.

(d) Ratios pertaining to gearing: Ratios pertaining to gearing gain significance for the fact

that they may help one set of capital providers (holders of ordinary shares) get an idea of

what they can expect from the company once it has fulfilled its obligations towards the other

set of capital providers (those who have either lent funds to the company or hold its

preference shares). Those who have lent funds to the company are effectively its creditors

and have a preferential treatment in getting paid the interest amounts over the shareholders of

the company. A company always has to first meet its obligations in servicing its interest

payments and only then would it be able to pay dividends. Again, for payment of dividends,

the preference shareholders get a preferential treatment and then comes the turn of ordinary

shareholders. Thus, ordinary shareholders are risk takers and while they assume risk (that

they may or may not get paid any dividends), they do have a reasonable expectation that the

company will be able to pay them some dividends. This is why, the more debt a company

assumes, the more concerned the company’s ordinary shareholders would be about their own

investment in the company and about receiving some returns for what they have invested in

the company.

Here, a comparison of the two companies is presented based on the following two ratios (for

computation of the ratio, please refer Appendix 1).

Debt-to-equity ratio:

Significance in being considered for analysis and what this ratio measures:

This ratio indicates how much long-term debt the company has assumed relative to the capital

invested by the shareholders. Ideally, a shareholder would like to see a company assume less

of debt in its capital structure.

Comparison between the companies and explanation for the same:

4

This ratio, just as current ratio does, measures the company’s ability to pay of its current or

short-term liabilities but differs from the current ratio as the quick ratio only allows current

assets other than inventory and prepaid expenses to be considered in determining the

company’s ability to meet its short-term liabilities.

Comparison between the companies and explanation for the same:

The quick ratios for Redding Co. and for Neaves Co. are respectively 1.67 and 1.07.

While there was a larger difference between the two companies’ current ratios, there is not

that large a difference between the two companies’ quick ratios. This is attributable to the fact

that for Neaves Co. inventory is just about 17% of its current assets while for Redding Co.

inventory is close to 23% of its current assets. This observation is in line with the fact that

Redding Co.’s inventory turnover ratio was lower than that of Neaves Co.

(d) Ratios pertaining to gearing: Ratios pertaining to gearing gain significance for the fact

that they may help one set of capital providers (holders of ordinary shares) get an idea of

what they can expect from the company once it has fulfilled its obligations towards the other

set of capital providers (those who have either lent funds to the company or hold its

preference shares). Those who have lent funds to the company are effectively its creditors

and have a preferential treatment in getting paid the interest amounts over the shareholders of

the company. A company always has to first meet its obligations in servicing its interest

payments and only then would it be able to pay dividends. Again, for payment of dividends,

the preference shareholders get a preferential treatment and then comes the turn of ordinary

shareholders. Thus, ordinary shareholders are risk takers and while they assume risk (that

they may or may not get paid any dividends), they do have a reasonable expectation that the

company will be able to pay them some dividends. This is why, the more debt a company

assumes, the more concerned the company’s ordinary shareholders would be about their own

investment in the company and about receiving some returns for what they have invested in

the company.

Here, a comparison of the two companies is presented based on the following two ratios (for

computation of the ratio, please refer Appendix 1).

Debt-to-equity ratio:

Significance in being considered for analysis and what this ratio measures:

This ratio indicates how much long-term debt the company has assumed relative to the capital

invested by the shareholders. Ideally, a shareholder would like to see a company assume less

of debt in its capital structure.

Comparison between the companies and explanation for the same:

4

Report on Redding Co. or Neaves Co. as an investment choice for potential investors

The debt-to-equity ratios for Redding Co. and for Neaves Co. are respectively 1.40 and 0.83.

While Redding Co. seems to have taken more long-term debt for every dollar of equity,

Neaves Co. has assumed relatively lesser long-term debt for every dollar of equity. Neaves

Co. seems to be having enough cash to finance its operations while this is not the case with

Redding Co.

Interest cover ratio:

Significance in being considered for analysis and what this ratio measures:

This ratio measures how many times a company’s fixed obligations towards interest payment

is covered by its profits before such interest charges. The higher this ratio, the greater is the

ability of the company to service its interest obligations and the more likely the company

would be to be in a position wherein it would be able to provide returns to ordinary

shareholders by way of dividends.

Comparison between the companies and explanation for the same:

The interest cover ratios for Redding Co. and for Neaves Co. are respectively 4.21 times and

17.34 times.

Neaves Co. has a very comfortable interest cover ratio and this means that it is much better

placed to consider giving out dividends to its shareholders after having serviced its interest

charges.

(e) Ratios pertaining to investors: Ratios pertaining to investors are clearly significant in

any case where a potential investor is evaluating a company for its suitability or otherwise as

an investment choice. These ratios measure the success or otherwise of a company in terms of

providing adequate and acceptable returns against the capital of the ordinary shareholders

which is at stake with the company. If a company appears to be weak in terms of ratios which

specifically pertain to investors, no potential investor would want to invest in the company.

Here, a comparison of the two companies is presented based on the following two ratios (for

computation of the ratio, please refer Appendix 1).

Return on equity:

Significance in being considered for analysis and what this ratio measures:

This ratio measures the post-tax earnings as a percentage of the capital of ordinary

shareholders at stake with the company. Post-tax earnings are relevant in computing this ratio

since only these earnings are actually available with the company to pay out as dividends to

5

The debt-to-equity ratios for Redding Co. and for Neaves Co. are respectively 1.40 and 0.83.

While Redding Co. seems to have taken more long-term debt for every dollar of equity,

Neaves Co. has assumed relatively lesser long-term debt for every dollar of equity. Neaves

Co. seems to be having enough cash to finance its operations while this is not the case with

Redding Co.

Interest cover ratio:

Significance in being considered for analysis and what this ratio measures:

This ratio measures how many times a company’s fixed obligations towards interest payment

is covered by its profits before such interest charges. The higher this ratio, the greater is the

ability of the company to service its interest obligations and the more likely the company

would be to be in a position wherein it would be able to provide returns to ordinary

shareholders by way of dividends.

Comparison between the companies and explanation for the same:

The interest cover ratios for Redding Co. and for Neaves Co. are respectively 4.21 times and

17.34 times.

Neaves Co. has a very comfortable interest cover ratio and this means that it is much better

placed to consider giving out dividends to its shareholders after having serviced its interest

charges.

(e) Ratios pertaining to investors: Ratios pertaining to investors are clearly significant in

any case where a potential investor is evaluating a company for its suitability or otherwise as

an investment choice. These ratios measure the success or otherwise of a company in terms of

providing adequate and acceptable returns against the capital of the ordinary shareholders

which is at stake with the company. If a company appears to be weak in terms of ratios which

specifically pertain to investors, no potential investor would want to invest in the company.

Here, a comparison of the two companies is presented based on the following two ratios (for

computation of the ratio, please refer Appendix 1).

Return on equity:

Significance in being considered for analysis and what this ratio measures:

This ratio measures the post-tax earnings as a percentage of the capital of ordinary

shareholders at stake with the company. Post-tax earnings are relevant in computing this ratio

since only these earnings are actually available with the company to pay out as dividends to

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Report on Redding Co. or Neaves Co. as an investment choice for potential investors

ordinary shareholders, if the company were to so decide about paying their dividends. The

higher this ratio, the more impressive will the company be to a potential investor.

Comparison between the companies and explanation for the same:

The return on equity ratios for Redding Co. and for Neaves Co. are respectively 40.50% and

78.96%.

Given the obvious better management of operating costs and assets, Neaves Co. has been able

to ensure a much better return on equity to its ordinary shareholders.

Earnings per share:

Significance in being considered for analysis and what this ratio measures:

This ratio indicates the post-tax earnings that are available for every ordinary share that is

outstanding. The higher this ratio, the more earning each ordinary share of the company is

getting to the investor.

Comparison between the companies and explanation for the same:

The earnings per share for Redding Co. and for Neaves Co. are respectively $2.45 and $2.92.

Neaves Co. has outperformed Redding Co. in terms of fetching the ordinary shareholders

more post-tax earnings for every share held by them.

Evaluation of financial ratios as a tool for assessing performance and further suggestions:

Financial ratios, while helpful in assessing and comparing business performance, do suffer

from their inherent limitations. However, they can be made more meaningful through further

information in addition to the financial information already made available in this instance.

Thus, it is suggested that notes to the annual accounts be made available so that a deeper

analysis can be done to understand the ratios better. Besides, non-financial measures of

performance also must be consulted to better judge a company’s performance.

Section 2: Agency in the context of listed companies and its usefulness in helping the

companies in question attain their objectives:

Agency theory depends on the contractual relationship of an agent with its principal. Agency

theory, thus, states that a company’s owner is the principal who relies on the company’s

agent (the directors and the managers) to operate the company on behalf of the company

owner (principal). In case of listed companies, it is the company’s shareholders who become

the company’s owners. No matter how small their shareholding, these shareholders

individually own a part of the company and collectively own the whole company. Being in

6

ordinary shareholders, if the company were to so decide about paying their dividends. The

higher this ratio, the more impressive will the company be to a potential investor.

Comparison between the companies and explanation for the same:

The return on equity ratios for Redding Co. and for Neaves Co. are respectively 40.50% and

78.96%.

Given the obvious better management of operating costs and assets, Neaves Co. has been able

to ensure a much better return on equity to its ordinary shareholders.

Earnings per share:

Significance in being considered for analysis and what this ratio measures:

This ratio indicates the post-tax earnings that are available for every ordinary share that is

outstanding. The higher this ratio, the more earning each ordinary share of the company is

getting to the investor.

Comparison between the companies and explanation for the same:

The earnings per share for Redding Co. and for Neaves Co. are respectively $2.45 and $2.92.

Neaves Co. has outperformed Redding Co. in terms of fetching the ordinary shareholders

more post-tax earnings for every share held by them.

Evaluation of financial ratios as a tool for assessing performance and further suggestions:

Financial ratios, while helpful in assessing and comparing business performance, do suffer

from their inherent limitations. However, they can be made more meaningful through further

information in addition to the financial information already made available in this instance.

Thus, it is suggested that notes to the annual accounts be made available so that a deeper

analysis can be done to understand the ratios better. Besides, non-financial measures of

performance also must be consulted to better judge a company’s performance.

Section 2: Agency in the context of listed companies and its usefulness in helping the

companies in question attain their objectives:

Agency theory depends on the contractual relationship of an agent with its principal. Agency

theory, thus, states that a company’s owner is the principal who relies on the company’s

agent (the directors and the managers) to operate the company on behalf of the company

owner (principal). In case of listed companies, it is the company’s shareholders who become

the company’s owners. No matter how small their shareholding, these shareholders

individually own a part of the company and collectively own the whole company. Being in

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Report on Redding Co. or Neaves Co. as an investment choice for potential investors

the position of an agent, a director or a manager has a considerable extent of freedom to

exercise while pursuing the objectives laid down by the company’s owner (the principal). The

prime objective, from a financial management perspective, is that the wealth of the

shareholders must get maximized through the operating of the company. Besides, there may

be many other objectives that the companies in question would be desirous of getting

achieved. Since owners of a listed company (i.e. the shareholders) are scattered everywhere,

it is the agents (the directors and managers) who are best placed to take optimal business

decisions and ensure that the objectives of the companies are attained. Thus, the concept of

agency is helpful to listed companies in the attainment of their objectives (so long as the

agents do not misuse the authority given to them).

Section 3: Assessment of how Redding Co. will be impacted if it raises additional loans

to fund the refurbishment:

Redding Co. is already running a bank overdraft which is a short-term liability that it will

eventually need to meet. Besides not-so-impressive asset management, its long-term debt

position has also strained its capacity to service interest charges in a way that will allow it to

consider giving out dividends to the real risk takers – the ordinary shareholders. If Redding

Co. funds its expenditure by resorting to additional loans, the company’s debt-to-equity ratio

will worsen and its interest cover will worsen as well. Both the ordinary shareholders as well

as the new lenders will view the company as being a much riskier bet and will likely demand

greater returns for providing capital to the company. The already existing loan and the fact

that the bank account remains overdrawn will only put into question the company’s ability to

pay off its short-term and long-term obligations. If the company’s ability to settle its creditors

itself is questionable, there is no reason why any potential investor would want to invest in

this company.

Conclusion:

Even though Redding Co. is older than Neaves Co., the latter seems to be a better investment

than the former. One reason could be that Neaves Co. has much better agents in place (i.e.

leading specialists) when compared to the agents (directors from related circles who may not

necessarily be leading specialists) which Redding Co. has put in place. Thus, while Redding

Co. needs to learn a lesson or two in managing its operating costs and assets, Neaves Co.

seems to be an attractive choice available to potential buyers of its ordinary shares.

7

the position of an agent, a director or a manager has a considerable extent of freedom to

exercise while pursuing the objectives laid down by the company’s owner (the principal). The

prime objective, from a financial management perspective, is that the wealth of the

shareholders must get maximized through the operating of the company. Besides, there may

be many other objectives that the companies in question would be desirous of getting

achieved. Since owners of a listed company (i.e. the shareholders) are scattered everywhere,

it is the agents (the directors and managers) who are best placed to take optimal business

decisions and ensure that the objectives of the companies are attained. Thus, the concept of

agency is helpful to listed companies in the attainment of their objectives (so long as the

agents do not misuse the authority given to them).

Section 3: Assessment of how Redding Co. will be impacted if it raises additional loans

to fund the refurbishment:

Redding Co. is already running a bank overdraft which is a short-term liability that it will

eventually need to meet. Besides not-so-impressive asset management, its long-term debt

position has also strained its capacity to service interest charges in a way that will allow it to

consider giving out dividends to the real risk takers – the ordinary shareholders. If Redding

Co. funds its expenditure by resorting to additional loans, the company’s debt-to-equity ratio

will worsen and its interest cover will worsen as well. Both the ordinary shareholders as well

as the new lenders will view the company as being a much riskier bet and will likely demand

greater returns for providing capital to the company. The already existing loan and the fact

that the bank account remains overdrawn will only put into question the company’s ability to

pay off its short-term and long-term obligations. If the company’s ability to settle its creditors

itself is questionable, there is no reason why any potential investor would want to invest in

this company.

Conclusion:

Even though Redding Co. is older than Neaves Co., the latter seems to be a better investment

than the former. One reason could be that Neaves Co. has much better agents in place (i.e.

leading specialists) when compared to the agents (directors from related circles who may not

necessarily be leading specialists) which Redding Co. has put in place. Thus, while Redding

Co. needs to learn a lesson or two in managing its operating costs and assets, Neaves Co.

seems to be an attractive choice available to potential buyers of its ordinary shares.

7

Report on Redding Co. or Neaves Co. as an investment choice for potential investors

References:

8

References:

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Report on Redding Co. or Neaves Co. as an investment choice for potential investors

Edwards, C. (2003). Fundamentals of Corporate Finance. Available at:

http://highered.mheducation.com/sites/dl/free/0070898669/65177/Chapter17.ppt.

[Accessed: 03 September 2018]

Freeman, R.E. and Reed, D.L. (1983). Stockholders and Stakeholders: A New

Perspective on Corporate Governance. California Management Review. Available at:

http://journals.sagepub.com/doi/10.2307/41165018 [Accessed: 03 September 2018].

Tirole, J. (2006). The Theory of Corporate Finance. Princeton University Press. New

Jersey.

Quiry, P., Dallocchio, M., Fur, Y. L., & Salvi, A. (2009). Corporate Finance: Theory

and Practice. John Wiley & Sons Ltd. United Kingdom.

Kim, K. A. (2011). Global Corporate Finance: A Focused Approach. World Scientific

Publishing Co. Pte. Ltd. Singapore.

Peterson, P. & Fabozzi, F. (1999). Analysis of Financial Statements. John Wiley &

Sons. New Jersey.

Bragg, S. (2012). Business Ratios and Formulas: A Comprehensive Guide. John

Wiley & Sons. New Jersey.

Baker, H. K. & Powell, G. E. (2005). Understanding Financial Management: A

Practical Guide. Blackwell Publishing. United Kingdom.

Clayman, M. R., Fridson, M. S., & Troughton, G. H. (2012). Corporate Finance: A

Practical Approach. John Wiley & Sons. New Jersey.

Vance, D. E. (2003). Financial Analysis and Decision Making. Tata McGraw-Hill.

USA

Clauss, F. J. (2010). Corporate Financial Analysis with Microsoft Excel. Tata

McGraw-Hill. USA.

9

Edwards, C. (2003). Fundamentals of Corporate Finance. Available at:

http://highered.mheducation.com/sites/dl/free/0070898669/65177/Chapter17.ppt.

[Accessed: 03 September 2018]

Freeman, R.E. and Reed, D.L. (1983). Stockholders and Stakeholders: A New

Perspective on Corporate Governance. California Management Review. Available at:

http://journals.sagepub.com/doi/10.2307/41165018 [Accessed: 03 September 2018].

Tirole, J. (2006). The Theory of Corporate Finance. Princeton University Press. New

Jersey.

Quiry, P., Dallocchio, M., Fur, Y. L., & Salvi, A. (2009). Corporate Finance: Theory

and Practice. John Wiley & Sons Ltd. United Kingdom.

Kim, K. A. (2011). Global Corporate Finance: A Focused Approach. World Scientific

Publishing Co. Pte. Ltd. Singapore.

Peterson, P. & Fabozzi, F. (1999). Analysis of Financial Statements. John Wiley &

Sons. New Jersey.

Bragg, S. (2012). Business Ratios and Formulas: A Comprehensive Guide. John

Wiley & Sons. New Jersey.

Baker, H. K. & Powell, G. E. (2005). Understanding Financial Management: A

Practical Guide. Blackwell Publishing. United Kingdom.

Clayman, M. R., Fridson, M. S., & Troughton, G. H. (2012). Corporate Finance: A

Practical Approach. John Wiley & Sons. New Jersey.

Vance, D. E. (2003). Financial Analysis and Decision Making. Tata McGraw-Hill.

USA

Clauss, F. J. (2010). Corporate Financial Analysis with Microsoft Excel. Tata

McGraw-Hill. USA.

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Report on Redding Co. or Neaves Co. as an investment choice for potential investors

Appendix 1: Calculation of ratios:

Ratios pertaining to profitability

Net profit margin: The formula to compute this ratio is provided below along with the

workings of the ratio for the two companies.

10

Appendix 1: Calculation of ratios:

Ratios pertaining to profitability

Net profit margin: The formula to compute this ratio is provided below along with the

workings of the ratio for the two companies.

10

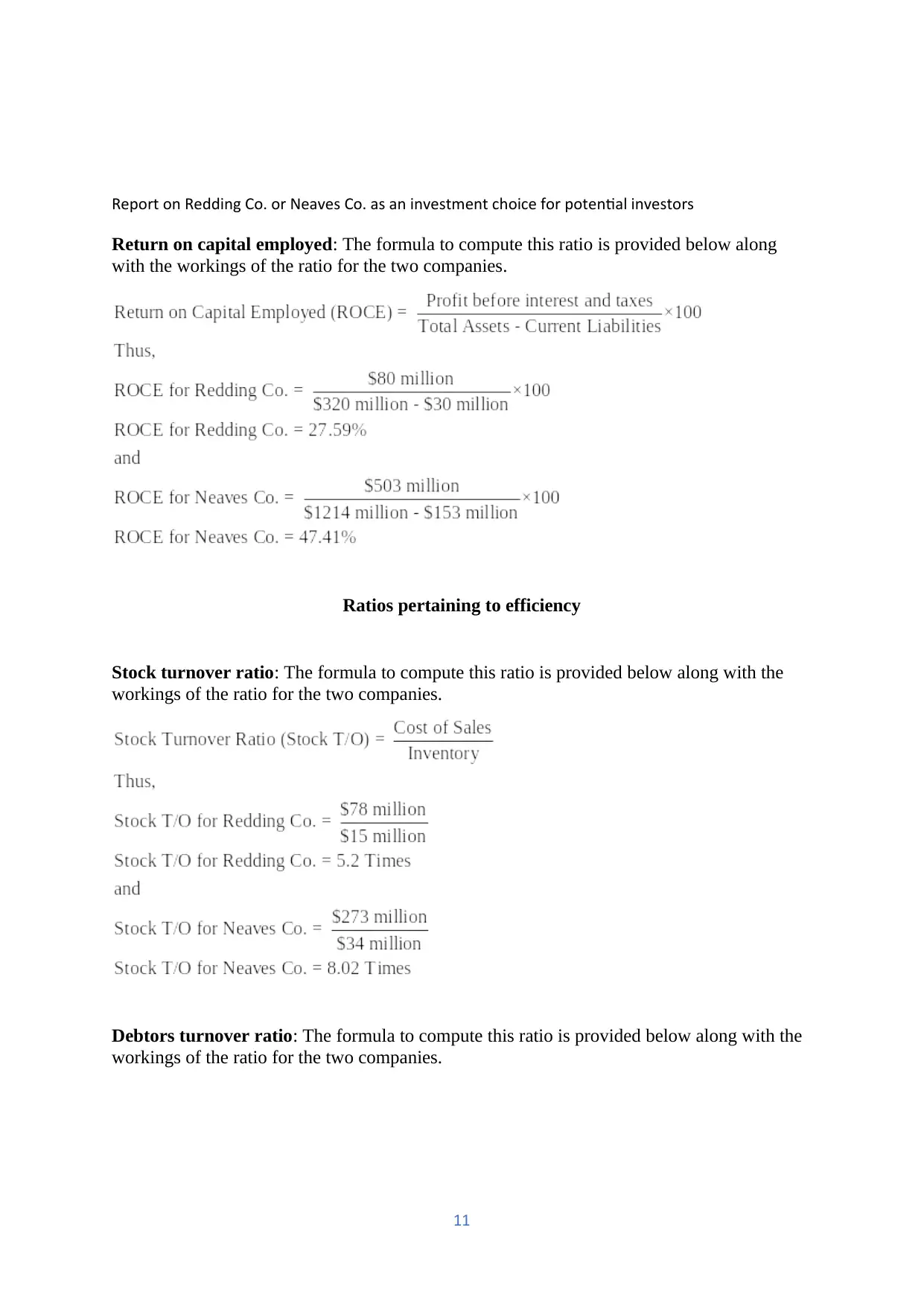

Report on Redding Co. or Neaves Co. as an investment choice for potential investors

Return on capital employed: The formula to compute this ratio is provided below along

with the workings of the ratio for the two companies.

Ratios pertaining to efficiency

Stock turnover ratio: The formula to compute this ratio is provided below along with the

workings of the ratio for the two companies.

Debtors turnover ratio: The formula to compute this ratio is provided below along with the

workings of the ratio for the two companies.

11

Return on capital employed: The formula to compute this ratio is provided below along

with the workings of the ratio for the two companies.

Ratios pertaining to efficiency

Stock turnover ratio: The formula to compute this ratio is provided below along with the

workings of the ratio for the two companies.

Debtors turnover ratio: The formula to compute this ratio is provided below along with the

workings of the ratio for the two companies.

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.