Accounting Solutions: Depreciation, Journal Entries, and Goodwill

VerifiedAdded on 2020/03/15

|7

|1031

|237

Homework Assignment

AI Summary

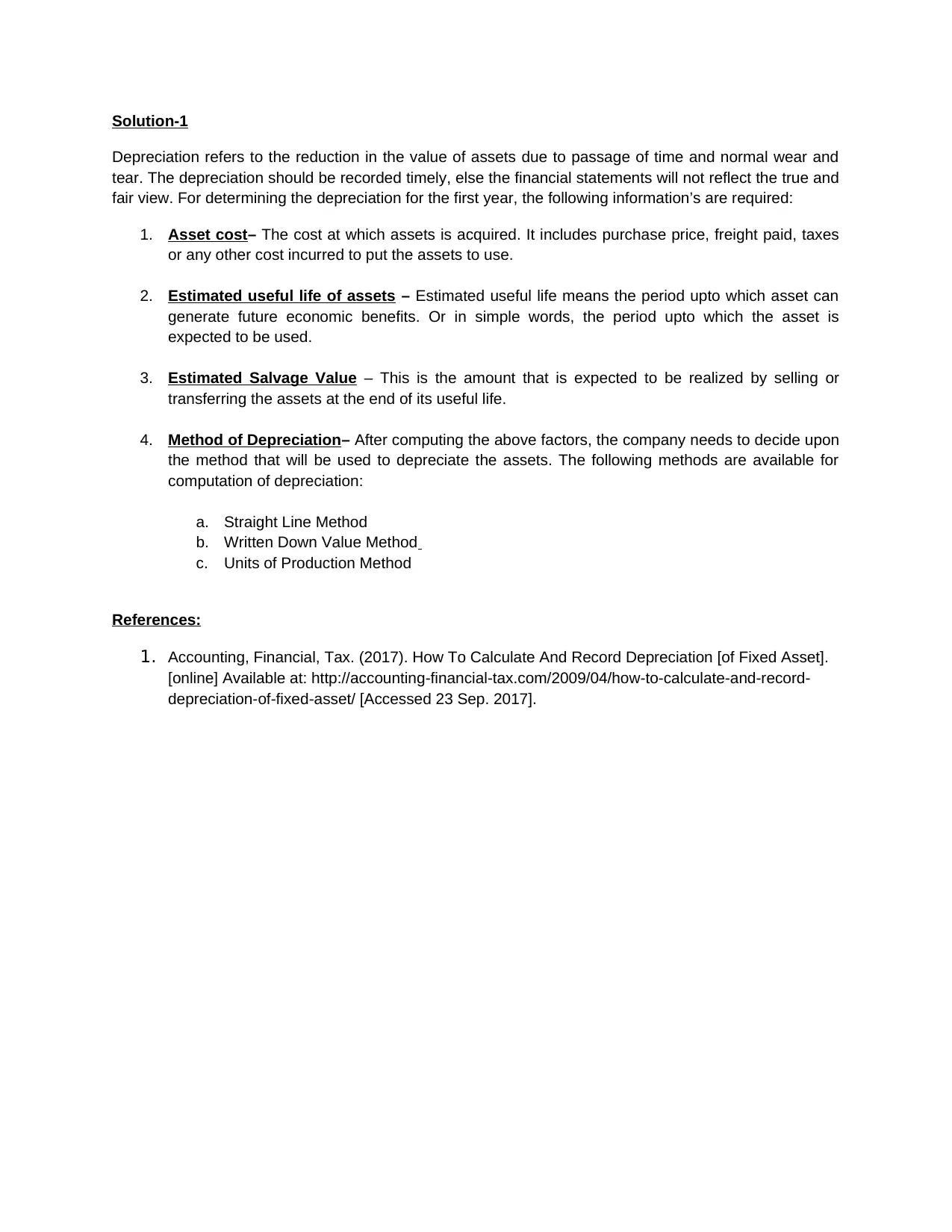

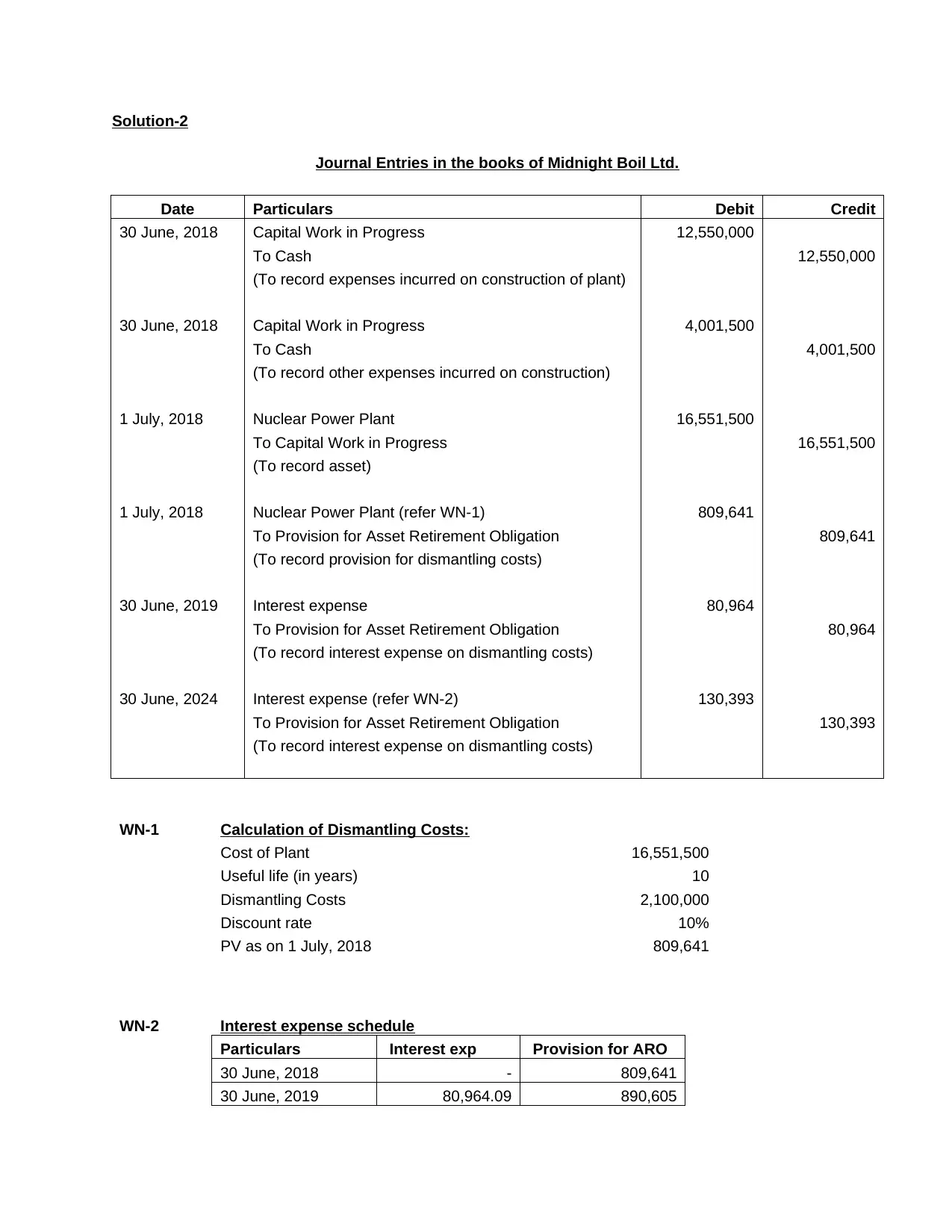

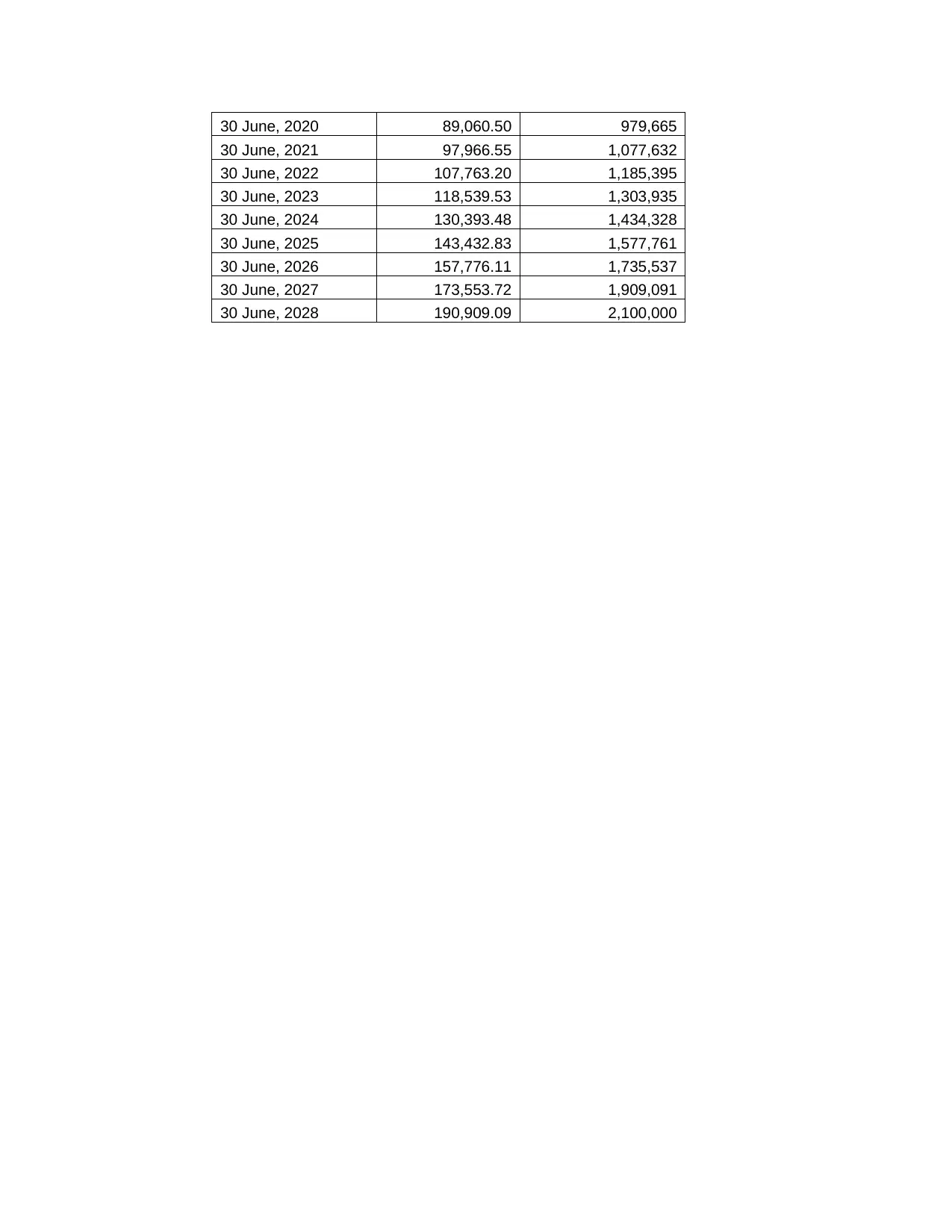

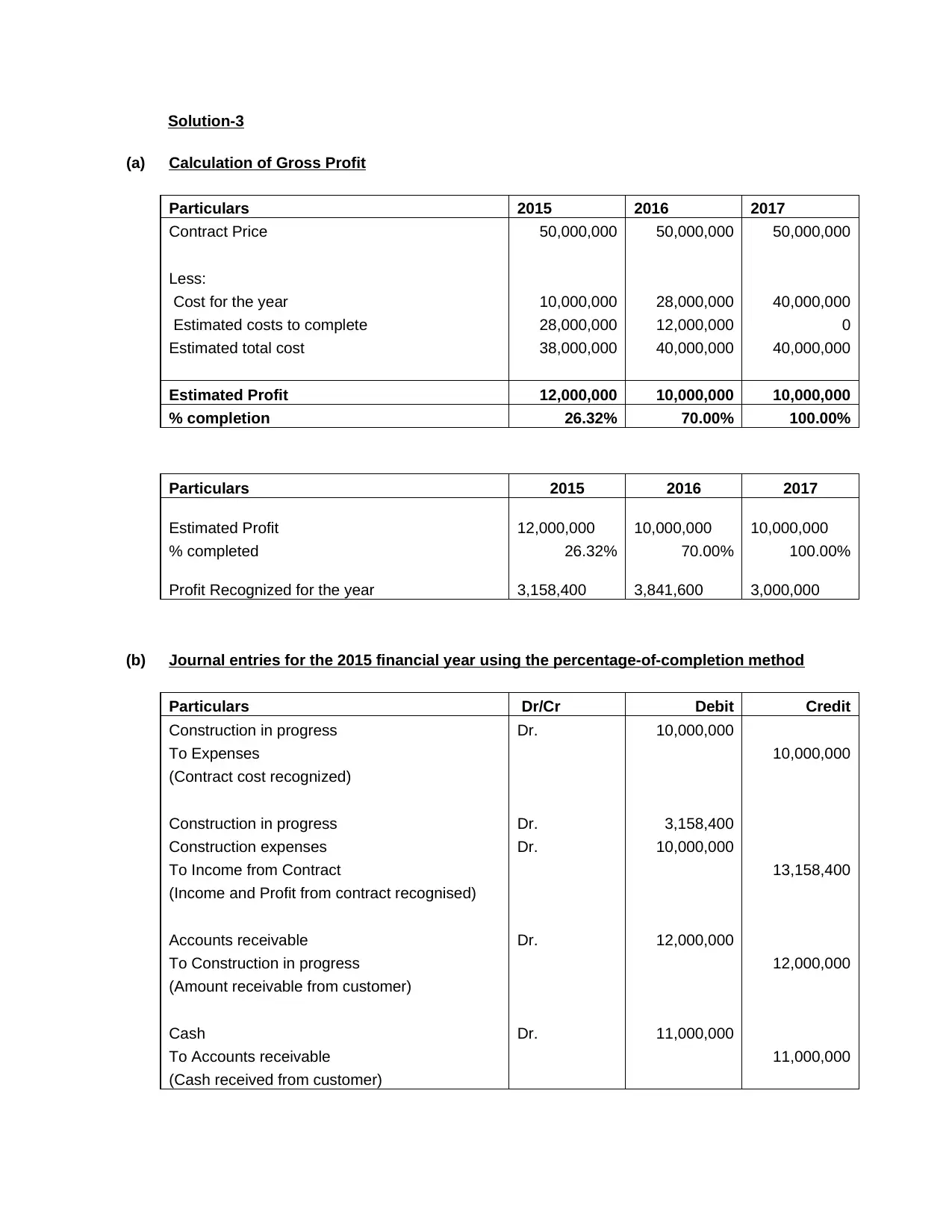

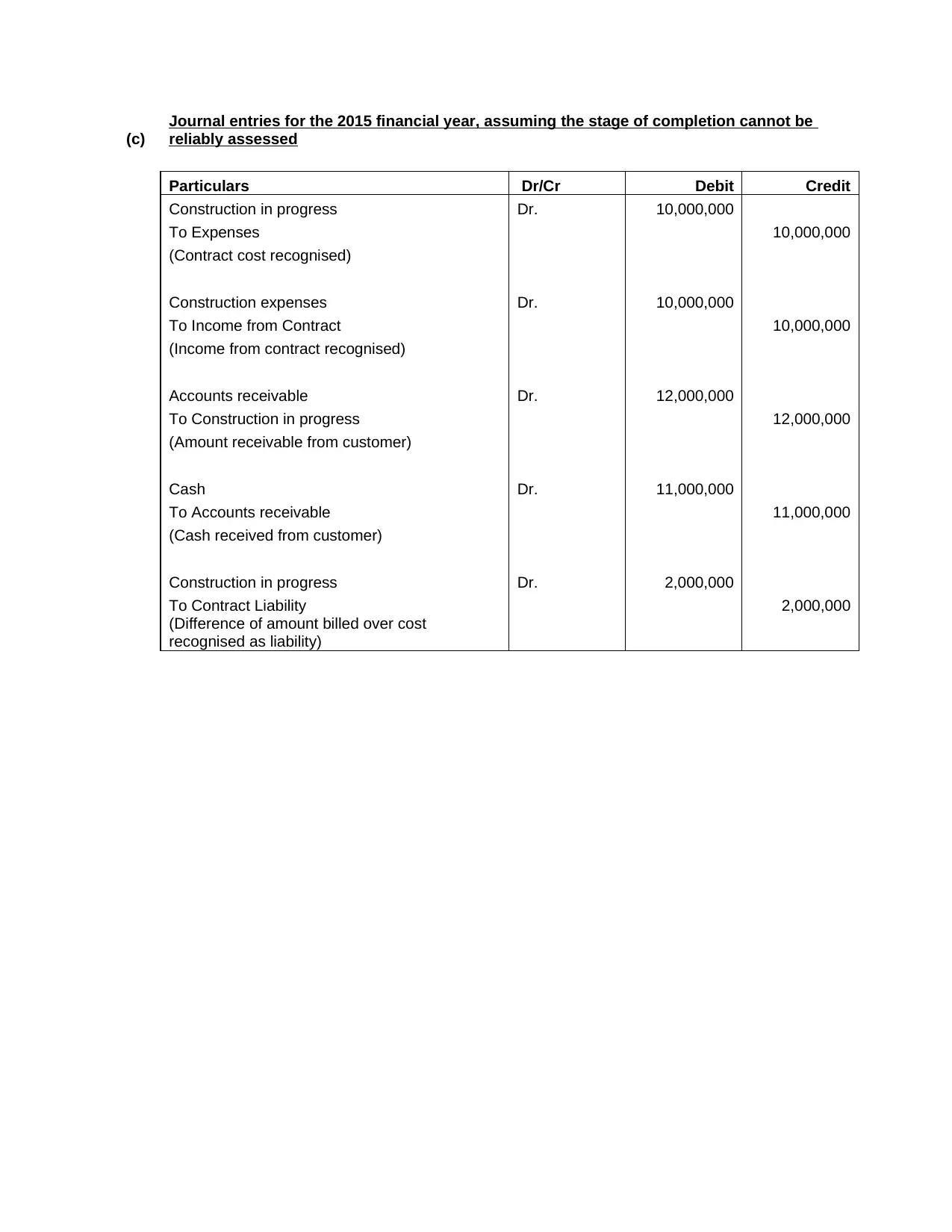

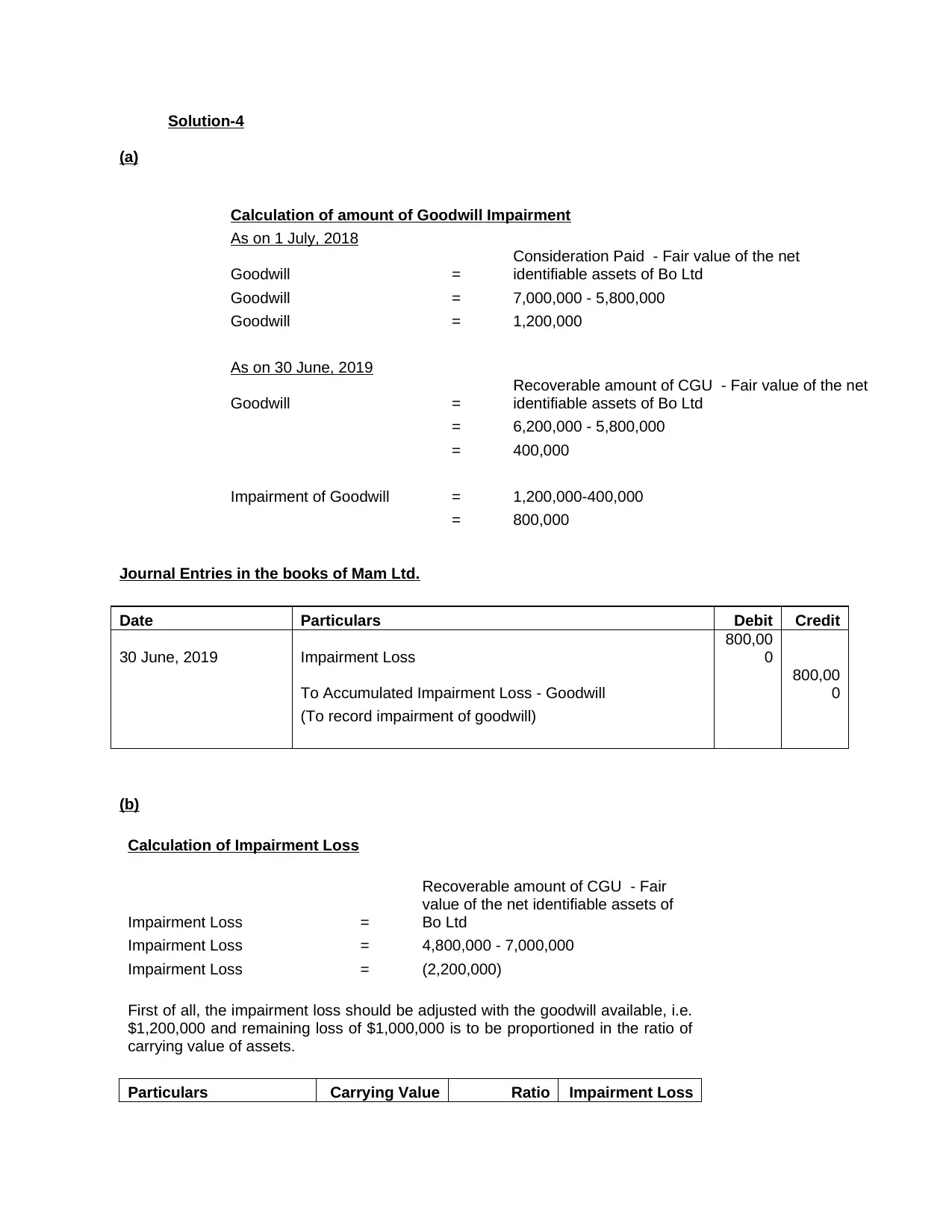

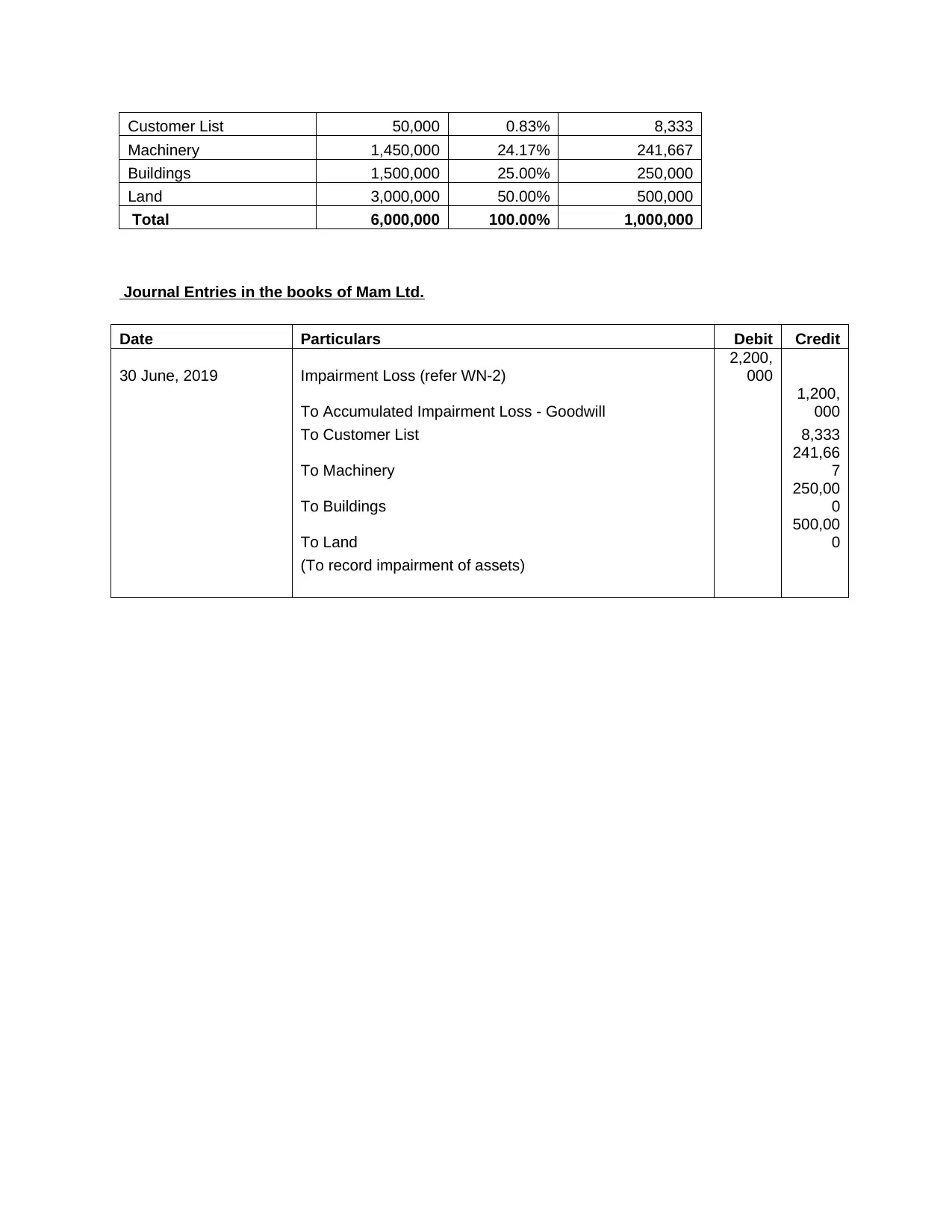

This document provides detailed solutions to several financial accounting problems. The first solution explains depreciation, covering asset cost, useful life, salvage value, and various depreciation methods. The second solution presents journal entries for a nuclear power plant project, including entries for construction costs, asset recognition, and asset retirement obligations, along with a calculation of dismantling costs and interest expense schedule. The third solution demonstrates the percentage-of-completion method for revenue recognition in a construction contract, including calculations of gross profit and journal entries for different scenarios. The fourth solution addresses goodwill impairment, including the calculation of impairment loss and related journal entries for both scenarios, where the impairment loss is less than goodwill and more than goodwill. These solutions are intended to provide a comprehensive understanding of these financial accounting concepts.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.