Analyzing Janet Brown's Taxable Income and Deductible Expenses

VerifiedAdded on 2020/02/18

|5

|1303

|41

Homework Assignment

AI Summary

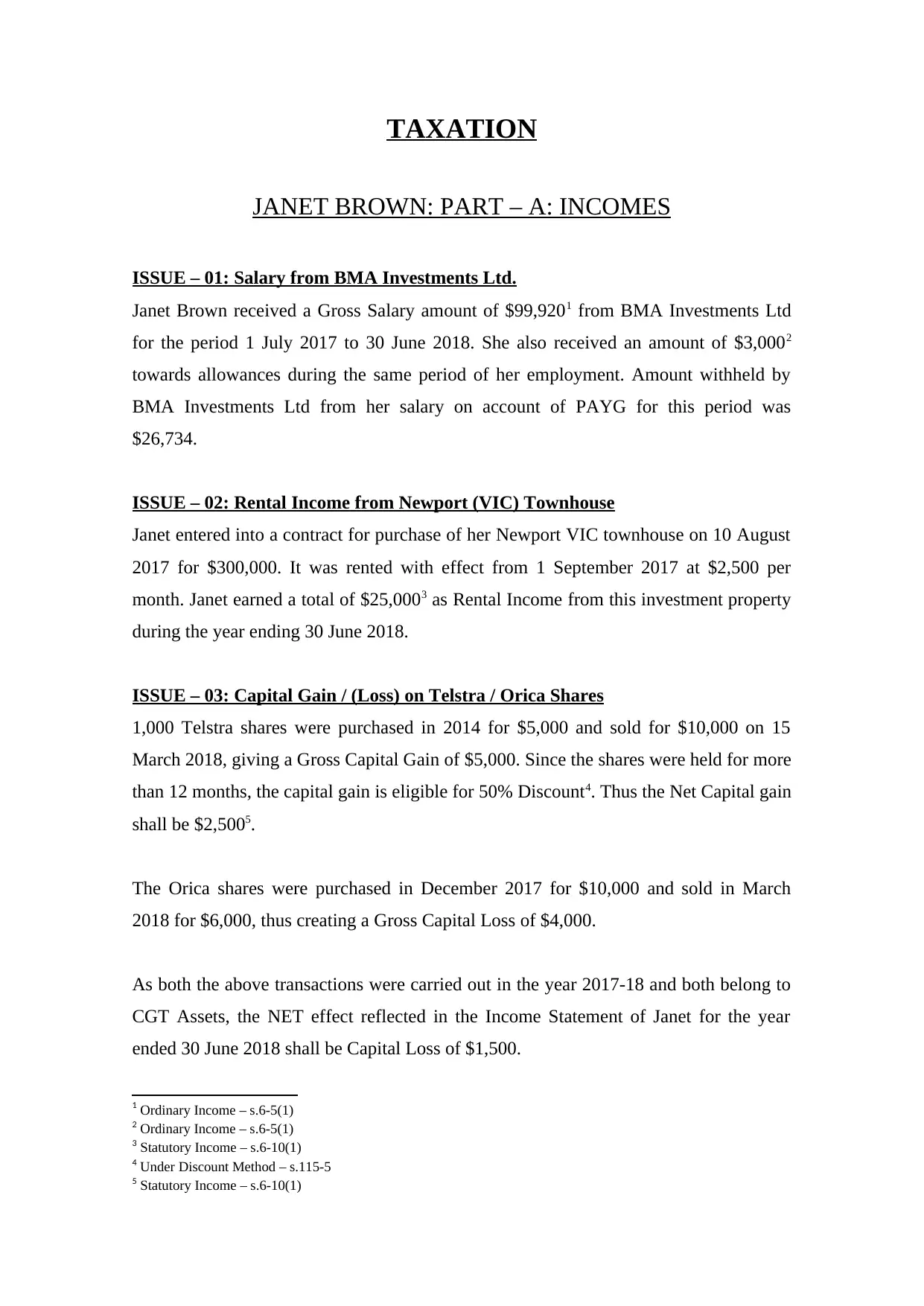

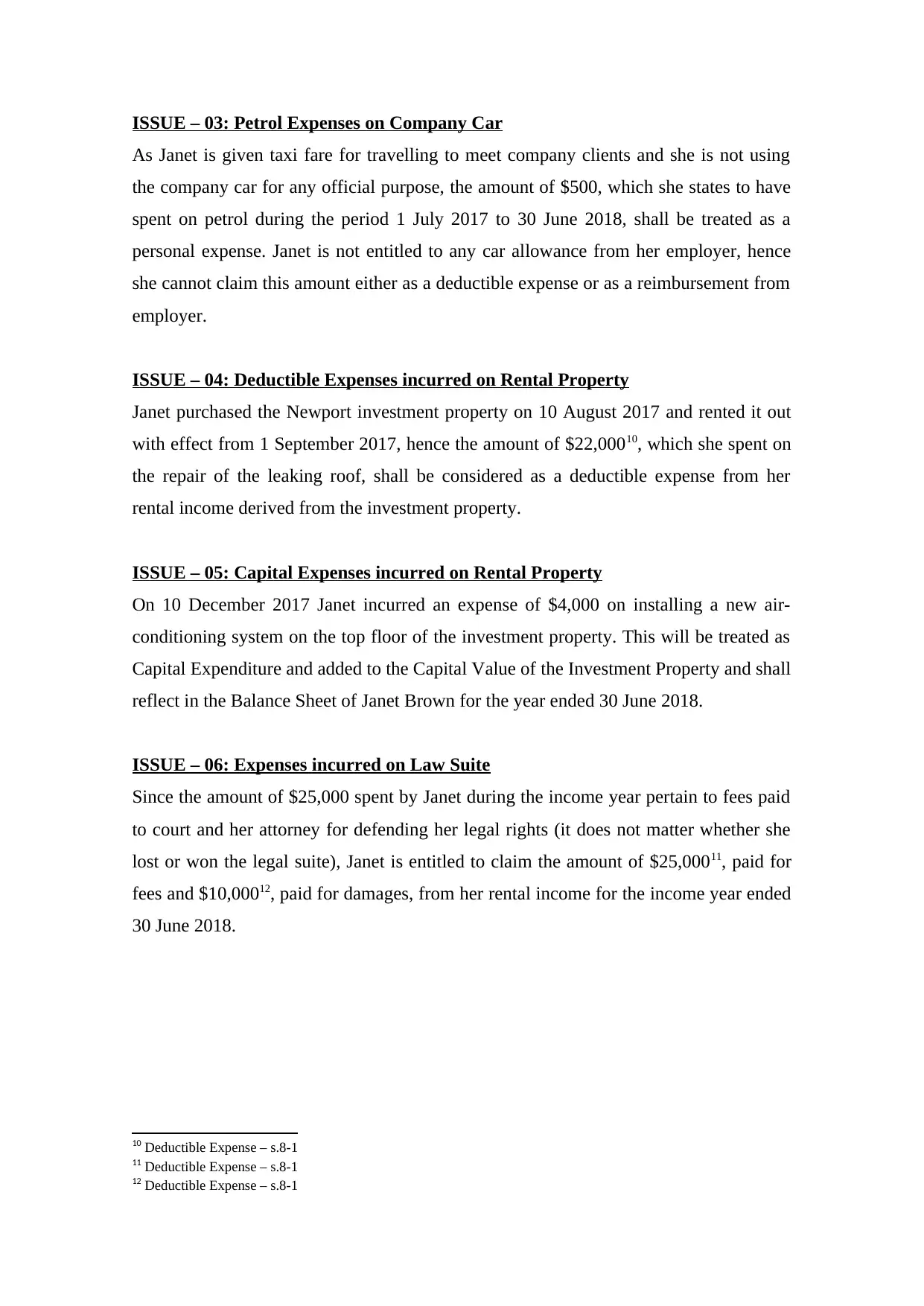

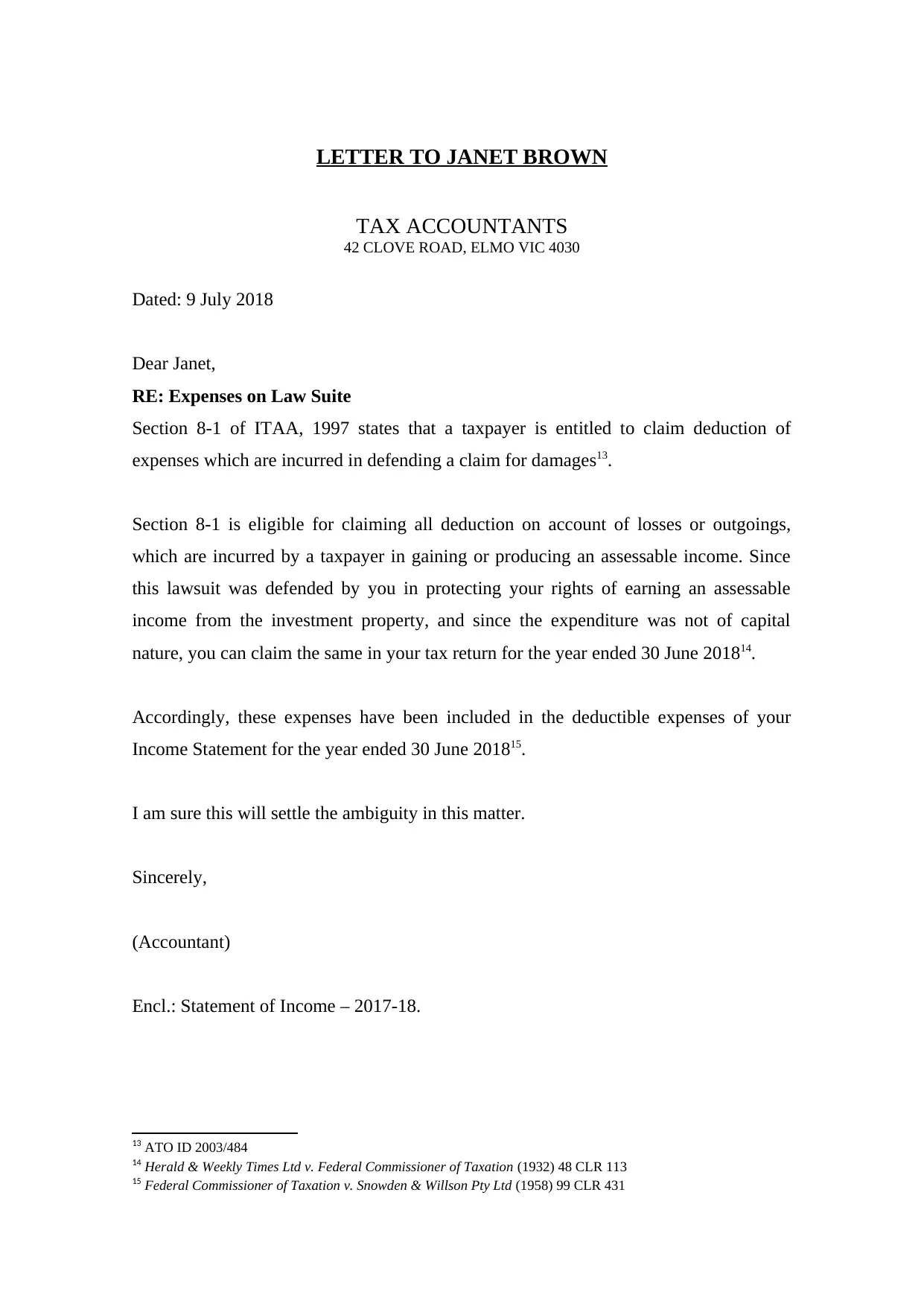

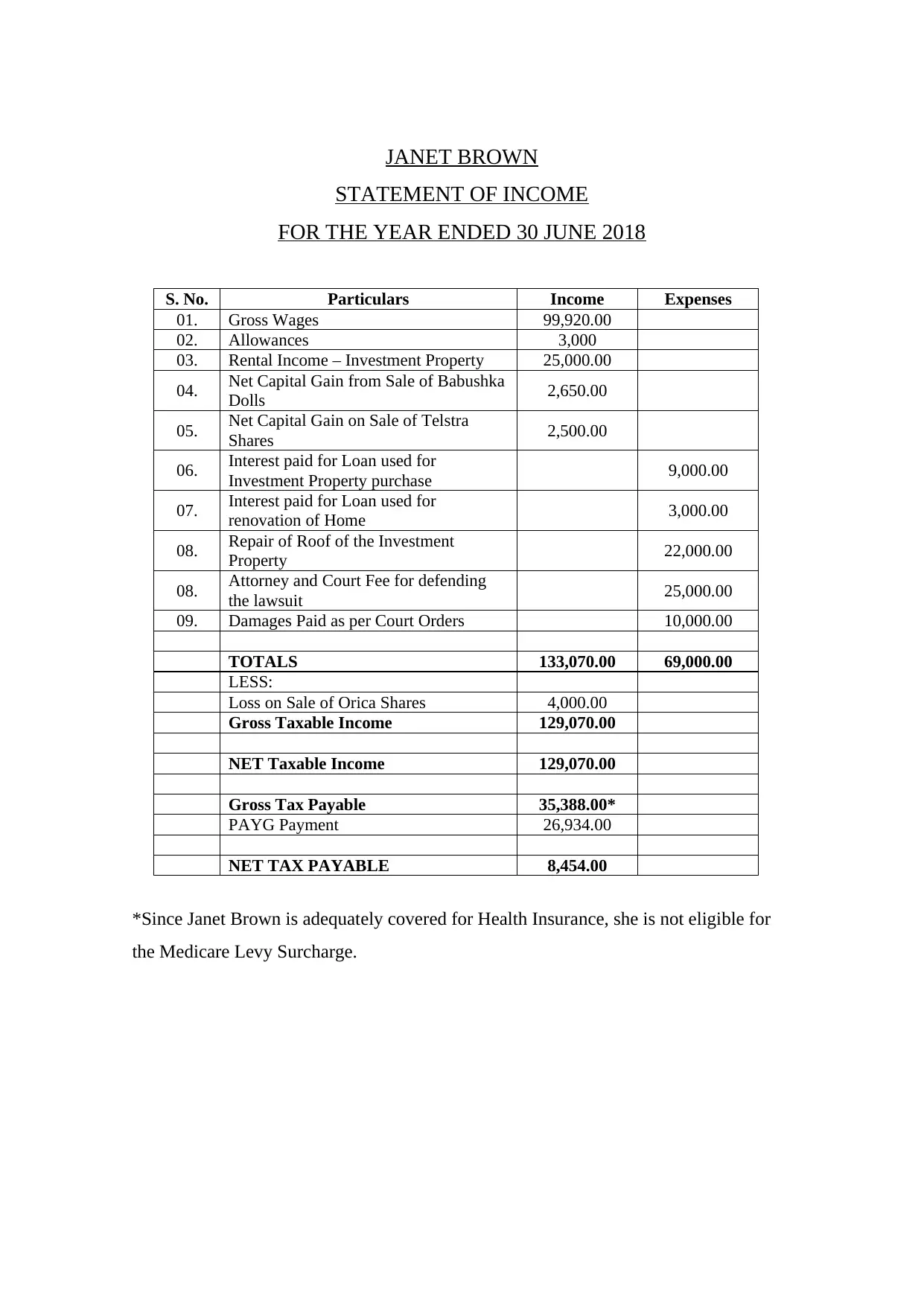

This assignment presents a comprehensive analysis of Janet Brown's tax return for the period of July 1, 2017, to June 30, 2018. It meticulously details various income sources, including salary from BMA Investments Ltd, rental income from a Newport VIC townhouse, and capital gains from the sale of Telstra and Babushka dolls shares. The assignment further examines deductible expenses such as interest payments on loans used for investment properties and renovations, repair costs for the rental property, and expenses related to a lawsuit. It calculates net capital gains, and taxable income, culminating in the determination of Janet's gross tax payable and net tax payable after accounting for PAYG payments. The analysis includes a letter to Janet Brown explaining the deductibility of lawsuit expenses, and concludes with a statement of income summarizing all financial aspects for the tax year.

1 out of 5

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.