Report on Boral Limited: Advanced Financial Accounting Concepts

VerifiedAdded on 2023/03/30

|13

|2816

|430

Report

AI Summary

This report provides a detailed analysis of the accounting concepts and framework employed by Boral Limited, an Australian company involved in building and construction materials. It explains key accounting concepts such as the economic entity concept, matching concept, consistency concept, materiality concept, conservatism concept, accruals concept, and going concern concept, illustrating how Boral Limited applies these in its financial reporting. The report also discusses the conceptual framework used by the company, measurement issues, and fundamental qualitative characteristics that guide financial reporting. Furthermore, it highlights how Boral Limited adheres to the Australian Accounting Standards and the International Financial Reporting Standards (IFRS) issued by the IASB, ensuring transparency and reliability in its financial statements. This comprehensive analysis provides valuable insights into Boral Limited's financial practices and its commitment to maintaining a sound financial reporting framework.

Running head: REPORT 0

ADVANCED FINANCIAL ACCOUNTING

MAY 29, 2019

STUDENT DETAILS:

ADVANCED FINANCIAL ACCOUNTING

MAY 29, 2019

STUDENT DETAILS:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REPORT 1

Contents

Introduction................................................................................................................................2

Background of company............................................................................................................2

Explanation of accounting concepts...........................................................................................2

The conceptual framework and issues related to measurement.................................................2

Fundamental Qualitative Characteristics...................................................................................2

Conclusion..................................................................................................................................2

References..................................................................................................................................3

Contents

Introduction................................................................................................................................2

Background of company............................................................................................................2

Explanation of accounting concepts...........................................................................................2

The conceptual framework and issues related to measurement.................................................2

Fundamental Qualitative Characteristics...................................................................................2

Conclusion..................................................................................................................................2

References..................................................................................................................................3

REPORT 2

Introduction

The key objective of financial reporting is to render data, which is significant as well as

helpful. The accounting concept deals with laws, rules, and regulations required for fulfilling

the requirements of the worker, investor, as well as different shareholders.

This concept means that the businesses can identify the revenues, losses and profits in the

amount, which differ from what will be identified on the basis of cash accepted from the

customer and while payment is made to the workers as well as the dealers.

In financial reporting, the conceptual framework is the theory of accounting made through the

standards-setting bodies in opposition to that the practical issues may be tested quantitatively.

In addition, the conceptual framework is the systematic device with various frameworks as

well as differences. This is utilised to create the conceptual distinction and manage the

concepts. The solid conceptual framework captures something actual and does this in the

manner, which is simple to recall as well as implement. The conceptual framework for

presentation, as well as the preparation of the financial statement as changed, involves the

conceptual framework used for Financial Reporting as provided through the IASB. A main

motive for establishing conceptual framework is that it provides framework for setting

accounting standards, a base for resolving the accounting problems, the fundamental concepts

that do not require happening in the accounting standards. In the following parts, the

accounting concepts followed by Boral limited is discussed and assessed. This report also

states the conceptual framework of the company, measurement issues, and fundamental

qualitative characteristics (Costa and Torrecchia, 2018).

Introduction

The key objective of financial reporting is to render data, which is significant as well as

helpful. The accounting concept deals with laws, rules, and regulations required for fulfilling

the requirements of the worker, investor, as well as different shareholders.

This concept means that the businesses can identify the revenues, losses and profits in the

amount, which differ from what will be identified on the basis of cash accepted from the

customer and while payment is made to the workers as well as the dealers.

In financial reporting, the conceptual framework is the theory of accounting made through the

standards-setting bodies in opposition to that the practical issues may be tested quantitatively.

In addition, the conceptual framework is the systematic device with various frameworks as

well as differences. This is utilised to create the conceptual distinction and manage the

concepts. The solid conceptual framework captures something actual and does this in the

manner, which is simple to recall as well as implement. The conceptual framework for

presentation, as well as the preparation of the financial statement as changed, involves the

conceptual framework used for Financial Reporting as provided through the IASB. A main

motive for establishing conceptual framework is that it provides framework for setting

accounting standards, a base for resolving the accounting problems, the fundamental concepts

that do not require happening in the accounting standards. In the following parts, the

accounting concepts followed by Boral limited is discussed and assessed. This report also

states the conceptual framework of the company, measurement issues, and fundamental

qualitative characteristics (Costa and Torrecchia, 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REPORT 3

Background of the company

Boral Limited was founded in the year 1946. This company is established in North Sydney

(Australia). Boral Limited produces as well as delivers the materials related to building &

construction in American countries, Asian countries and Australian countries. This company

also makes an offer of block, brick; asphalt materials related to cement, concrete and

retaining walls, pavers, materials related to roof, board of plaster, light materials related to

window and building, timber product, quarry material, fly ashes, stone, materials for roofing

as well as masonry. Boral Limited also renders spray sealing or asphalt lying, services related

to material techniques, placing of materials, installation of roof tiles, as well as assortment

services related to empty pallets. Additionally, this involves in the activities related to

properties, transport, and landfill-services. This organisation serves the non-residential

construction as well as residential construction. It also provides services in the marketplace of

engineering as well as infrastructure (Lyle, 2018).

The financial year 2018 represented as the remarkable year in the transformation of Boral

Limited, with positive incorporation of a headwater business in Northern America, along with

more profits in Australia and alliance of important development of previous periods in Boral

USG. In the financial year 2018, Boral Limited delivered fundamental PAT (exclusive of

important items) of 473 million dollars, the substantial increment of 38% over the last years

(Panteli and Mancarella, 2015). The company also attained the acquirement net synergy of 39

million American dollars, ahead of the preliminary30–35 million American dollars target,

and the company has enhanced the 4-year synergy targets to 115 million American dollars.

The main approach of a company is to deliver advanced performances and maintainable

development is continuing well and delivering the value for the shareholders of the company

(Kelley and Knowles, 2016).

Background of the company

Boral Limited was founded in the year 1946. This company is established in North Sydney

(Australia). Boral Limited produces as well as delivers the materials related to building &

construction in American countries, Asian countries and Australian countries. This company

also makes an offer of block, brick; asphalt materials related to cement, concrete and

retaining walls, pavers, materials related to roof, board of plaster, light materials related to

window and building, timber product, quarry material, fly ashes, stone, materials for roofing

as well as masonry. Boral Limited also renders spray sealing or asphalt lying, services related

to material techniques, placing of materials, installation of roof tiles, as well as assortment

services related to empty pallets. Additionally, this involves in the activities related to

properties, transport, and landfill-services. This organisation serves the non-residential

construction as well as residential construction. It also provides services in the marketplace of

engineering as well as infrastructure (Lyle, 2018).

The financial year 2018 represented as the remarkable year in the transformation of Boral

Limited, with positive incorporation of a headwater business in Northern America, along with

more profits in Australia and alliance of important development of previous periods in Boral

USG. In the financial year 2018, Boral Limited delivered fundamental PAT (exclusive of

important items) of 473 million dollars, the substantial increment of 38% over the last years

(Panteli and Mancarella, 2015). The company also attained the acquirement net synergy of 39

million American dollars, ahead of the preliminary30–35 million American dollars target,

and the company has enhanced the 4-year synergy targets to 115 million American dollars.

The main approach of a company is to deliver advanced performances and maintainable

development is continuing well and delivering the value for the shareholders of the company

(Kelley and Knowles, 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REPORT 4

Explanation of accounting concepts

The accounting concept means the fundamental rules, assumptions, and principles that use as

a foundation to record the transactions related to business and preparing the accounts. It is

also assumed by the accounting concept a business entity as well as the owner of the entity,

are considered as two separate independent personalities for the accounting purpose. The

accounting concepts have a significant role in conducting business affairs. The mechanism is

required to know the credit and debit of the functions of a corporation (Bridgett, et. al, 2015).

Besides, it is essential to make sure by managers that they have proper knowledge of

accounting. The reason is that a simple mistake can spoil everything. The most significant

and easy problem, which is required to be understood by the managers, is different in nature,

going concern, disclosure, timeliness, true and fair representation, as well as relevance

(Kalisch, Müller and Tüscher, 2015). In the addition of this, the accounting practices entail

the documentation, extent and establishment of the financial-bound data that permits the

well-versed judgement as well as a foundation of the decisions taking by correct

shareholders. The company faces numerous conceptual problems. This is essential that one

must know the accounting concepts, to develop the firm’s foundation of how accounting does

work. The following are basic accounting concepts-

1. The economic entity concept- The business-related transactions are to be continued

separated from the owner’s transactions. By conducting this, there are no intermixing

of business transactions and private transaction in the financial statement of entity.

2. The matching concept- the expenses in relation to revenues are required to be

recognised in same time, where revenue was identified. With the help of this, there is

no any deferral of identification of expenses in upcoming reporting period, with a

Explanation of accounting concepts

The accounting concept means the fundamental rules, assumptions, and principles that use as

a foundation to record the transactions related to business and preparing the accounts. It is

also assumed by the accounting concept a business entity as well as the owner of the entity,

are considered as two separate independent personalities for the accounting purpose. The

accounting concepts have a significant role in conducting business affairs. The mechanism is

required to know the credit and debit of the functions of a corporation (Bridgett, et. al, 2015).

Besides, it is essential to make sure by managers that they have proper knowledge of

accounting. The reason is that a simple mistake can spoil everything. The most significant

and easy problem, which is required to be understood by the managers, is different in nature,

going concern, disclosure, timeliness, true and fair representation, as well as relevance

(Kalisch, Müller and Tüscher, 2015). In the addition of this, the accounting practices entail

the documentation, extent and establishment of the financial-bound data that permits the

well-versed judgement as well as a foundation of the decisions taking by correct

shareholders. The company faces numerous conceptual problems. This is essential that one

must know the accounting concepts, to develop the firm’s foundation of how accounting does

work. The following are basic accounting concepts-

1. The economic entity concept- The business-related transactions are to be continued

separated from the owner’s transactions. By conducting this, there are no intermixing

of business transactions and private transaction in the financial statement of entity.

2. The matching concept- the expenses in relation to revenues are required to be

recognised in same time, where revenue was identified. With the help of this, there is

no any deferral of identification of expenses in upcoming reporting period, with a

REPORT 5

purpose of someone seeing; the financial statements of the company can be assured

that each feature of dealing has recorded at the same time.

3. The consistency concept- while a company chooses to use the specific accounting

method, it should continue to use this over a go-forward basis. By doing this, financial

statements of corporation created in numerous times may be consistently compared.

4. The materiality concept- it is stated by materiality concept that an accounting standard

may be avoided, in a case where the net effect of conducting this so has this smaller

influence over the financial statements that user of financial statements will not be

misinformed. The materiality concept is known as the materiality constraint. It is

stated by this concept that the financial data is material to the company's financial

statements if this will modify the view and opinions of the rational individual. In

different terms, the significant financial data, which will sway the opinions of users of

financial statement, must be involved in financial statement of the company.

The materiality concept is comparative in significance as well as extent. Certain

financial data may be material to a corporation, however, may be irrelevant to others.

It is slightly obvious while a person thinks in relation to the smaller corporation

versus the larger corporation. The significant and larger expenditures to the smaller

corporation may be small the immaterial to the large corporation because of the

revenues as well as sizes.

5. The conservatism concept- The conservatism concept is a general concept of

identifying the liabilities and expenditures as soon as possible while there are

improbabilities in respect of results, however, to only identify the assets as well as

revenues when they are guaranteed of being accepted. The conservatism Principle is

the concept in accounting in GAAP that identifies and records expenditures and

purpose of someone seeing; the financial statements of the company can be assured

that each feature of dealing has recorded at the same time.

3. The consistency concept- while a company chooses to use the specific accounting

method, it should continue to use this over a go-forward basis. By doing this, financial

statements of corporation created in numerous times may be consistently compared.

4. The materiality concept- it is stated by materiality concept that an accounting standard

may be avoided, in a case where the net effect of conducting this so has this smaller

influence over the financial statements that user of financial statements will not be

misinformed. The materiality concept is known as the materiality constraint. It is

stated by this concept that the financial data is material to the company's financial

statements if this will modify the view and opinions of the rational individual. In

different terms, the significant financial data, which will sway the opinions of users of

financial statement, must be involved in financial statement of the company.

The materiality concept is comparative in significance as well as extent. Certain

financial data may be material to a corporation, however, may be irrelevant to others.

It is slightly obvious while a person thinks in relation to the smaller corporation

versus the larger corporation. The significant and larger expenditures to the smaller

corporation may be small the immaterial to the large corporation because of the

revenues as well as sizes.

5. The conservatism concept- The conservatism concept is a general concept of

identifying the liabilities and expenditures as soon as possible while there are

improbabilities in respect of results, however, to only identify the assets as well as

revenues when they are guaranteed of being accepted. The conservatism Principle is

the concept in accounting in GAAP that identifies and records expenditures and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REPORT 6

liabilities-uncertain or certain in nature, as soon as possible however identifies

revenue and asset, while they are guaranteed of being accepted. This provides the

easy direction to record the matters related to estimates as well as uncertainties (Crise,

et. al, 2018).

6. The accruals concept- as per an accruals concept, the revenue is identified at a period

when they generated. Additionally, the accruals concept states that the expense is

identified at a while asset is consumed. In this way, the accruals concept addresses

that the business may identify the revenues based on cash accepted by the customer or

while the payment is made to suppliers as well as employees. Therefore, the auditor of

the company will only approve the financial statements of the corporations, which

have conducted as according to a concept of accruals.

7. The going concern concept- The Corporation’s financial statements are made

according to an assumption that a business would stay in a function in a forthcoming

period. In addition, as per the going concern concept, recognition of expenditure and

the revenue recognition maybe deferred to forthcoming time, while an entity is still

working. Or else, the expenditure’s recording in specific will be accelerated in a

present time.

A capital structure of Boral Limited contains equity as well as debt. The directors

determine a company’s proper capital structure; particularly how much is raised from

equity shareholder and how much is advanced from the debt (the financial

instruments) to funding the upcoming and present functions of this company. In the

addition, the director of company reviews a capital structure of group and dividend

policy frequently and do so in reference of the capability of group to endure as the

liabilities-uncertain or certain in nature, as soon as possible however identifies

revenue and asset, while they are guaranteed of being accepted. This provides the

easy direction to record the matters related to estimates as well as uncertainties (Crise,

et. al, 2018).

6. The accruals concept- as per an accruals concept, the revenue is identified at a period

when they generated. Additionally, the accruals concept states that the expense is

identified at a while asset is consumed. In this way, the accruals concept addresses

that the business may identify the revenues based on cash accepted by the customer or

while the payment is made to suppliers as well as employees. Therefore, the auditor of

the company will only approve the financial statements of the corporations, which

have conducted as according to a concept of accruals.

7. The going concern concept- The Corporation’s financial statements are made

according to an assumption that a business would stay in a function in a forthcoming

period. In addition, as per the going concern concept, recognition of expenditure and

the revenue recognition maybe deferred to forthcoming time, while an entity is still

working. Or else, the expenditure’s recording in specific will be accelerated in a

present time.

A capital structure of Boral Limited contains equity as well as debt. The directors

determine a company’s proper capital structure; particularly how much is raised from

equity shareholder and how much is advanced from the debt (the financial

instruments) to funding the upcoming and present functions of this company. In the

addition, the director of company reviews a capital structure of group and dividend

policy frequently and do so in reference of the capability of group to endure as the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REPORT 7

going concern basis, for making investment in the chances, which develop the

business and increase the value of stakeholder (Crespo, Boschm and Balland, 2017).

Boral Limited also assesses the capability of a group to continue as the going concern, and

whether this going concern accounting concept is proper or relevant. It also includes the

disclosing, as applicable, cases associated with the going concern and utilising a going

concern accounting concept if they wish either to liquidate the Group or to end the functions

or have no accurate substitutes, however, to do so. Additionally, the company adopts the

matching concept at the time of recognising income and expenditure. Other incomes are

identified as per the systematic basis over a period essential to match it with the related costs

for that this is desired to reimburse. In a case when the cost already has incurred the amount

is recognised in the period, the claim is affirmed (Lewandowski, 2016).

The company also follows the consistency concept and materiality concept. Information is

only involved in a financial report to an extent this has regarded material and related to

proper knowledge of a company's financial statements. Besides, the accounting methods as

well as accounting methods of the calculation, in preparation of company’s financial

statements, are constant with the disclosed and followed in the annual report of Boral Limited

(Crandall, Deater-Deckard and Riley, 2015).

The conceptual framework and issues related to measurement

The sound conceptual framework serves as the foundation for standard setting and advances

the standards constancy over a period. The conceptual framework also renders the direction

in resolving the evolving practical issues. The major aim of conceptual Framework was to

help International Accounting Standard Board in establishment of future IFRS and within the

reviews of current IFRS. In the addition of this, the conceptual Framework can also help the

going concern basis, for making investment in the chances, which develop the

business and increase the value of stakeholder (Crespo, Boschm and Balland, 2017).

Boral Limited also assesses the capability of a group to continue as the going concern, and

whether this going concern accounting concept is proper or relevant. It also includes the

disclosing, as applicable, cases associated with the going concern and utilising a going

concern accounting concept if they wish either to liquidate the Group or to end the functions

or have no accurate substitutes, however, to do so. Additionally, the company adopts the

matching concept at the time of recognising income and expenditure. Other incomes are

identified as per the systematic basis over a period essential to match it with the related costs

for that this is desired to reimburse. In a case when the cost already has incurred the amount

is recognised in the period, the claim is affirmed (Lewandowski, 2016).

The company also follows the consistency concept and materiality concept. Information is

only involved in a financial report to an extent this has regarded material and related to

proper knowledge of a company's financial statements. Besides, the accounting methods as

well as accounting methods of the calculation, in preparation of company’s financial

statements, are constant with the disclosed and followed in the annual report of Boral Limited

(Crandall, Deater-Deckard and Riley, 2015).

The conceptual framework and issues related to measurement

The sound conceptual framework serves as the foundation for standard setting and advances

the standards constancy over a period. The conceptual framework also renders the direction

in resolving the evolving practical issues. The major aim of conceptual Framework was to

help International Accounting Standard Board in establishment of future IFRS and within the

reviews of current IFRS. In the addition of this, the conceptual Framework can also help the

REPORT 8

preparer of financial statements to develop the accounting policies for the event or transaction

not contained through the present standards. In this way, the conceptual framework handles

the problems related to the fundamental financial reporting like the readers and purposes of

the financial statement of an entity, a characteristic that creates accounting data relevant, and

the fundamental components of the financial statement of an entity. These fundamental

components of the financial statements include liability, asset equity, revenue, and expenses.

Moreover, this framework of the company also handles the concept to identify and measure

the components in financial statement of the company. In this way, fundamental elements of

conceptual framework involve qualitative characteristics of accounting data, the general

purpose of financial reporting, purpose of financial reports, measurement in addition to

identification in the financial statement of company, as well as other fundamental elements of

company’s financial statements (Bekçioglu, et. al, 2016).

According to annual report of Boral Limited, this is clear that the financial reports have

presented and made according to provisions of the Corporation Act Cth 2001, as well as the

authoritative declaration of the AASB and Australian Accounting Standards. Boral Limited

prepared the financial report as per the Australian IFRS issued by IASB and Accounting

Standards of Australia standards (Annual Report 2018). Financial statements of an entity

present fair as well as true view of performance of the company along with financial position.

The financial statements of the corporation conform to Corporations Regulations 2001 as

well as accounting. Boral Limited follows the important accounting policies to make the base

from the values of the asset, expenses, income, the value of liability as well as the value of

equity. In addition, the company is independent of a group as per the provisions related to

auditor’s independence according to the Corporations Act 2001. This organisation has also

fulfilled the other moral obligations as per the code of conduct.

preparer of financial statements to develop the accounting policies for the event or transaction

not contained through the present standards. In this way, the conceptual framework handles

the problems related to the fundamental financial reporting like the readers and purposes of

the financial statement of an entity, a characteristic that creates accounting data relevant, and

the fundamental components of the financial statement of an entity. These fundamental

components of the financial statements include liability, asset equity, revenue, and expenses.

Moreover, this framework of the company also handles the concept to identify and measure

the components in financial statement of the company. In this way, fundamental elements of

conceptual framework involve qualitative characteristics of accounting data, the general

purpose of financial reporting, purpose of financial reports, measurement in addition to

identification in the financial statement of company, as well as other fundamental elements of

company’s financial statements (Bekçioglu, et. al, 2016).

According to annual report of Boral Limited, this is clear that the financial reports have

presented and made according to provisions of the Corporation Act Cth 2001, as well as the

authoritative declaration of the AASB and Australian Accounting Standards. Boral Limited

prepared the financial report as per the Australian IFRS issued by IASB and Accounting

Standards of Australia standards (Annual Report 2018). Financial statements of an entity

present fair as well as true view of performance of the company along with financial position.

The financial statements of the corporation conform to Corporations Regulations 2001 as

well as accounting. Boral Limited follows the important accounting policies to make the base

from the values of the asset, expenses, income, the value of liability as well as the value of

equity. In addition, the company is independent of a group as per the provisions related to

auditor’s independence according to the Corporations Act 2001. This organisation has also

fulfilled the other moral obligations as per the code of conduct.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REPORT 9

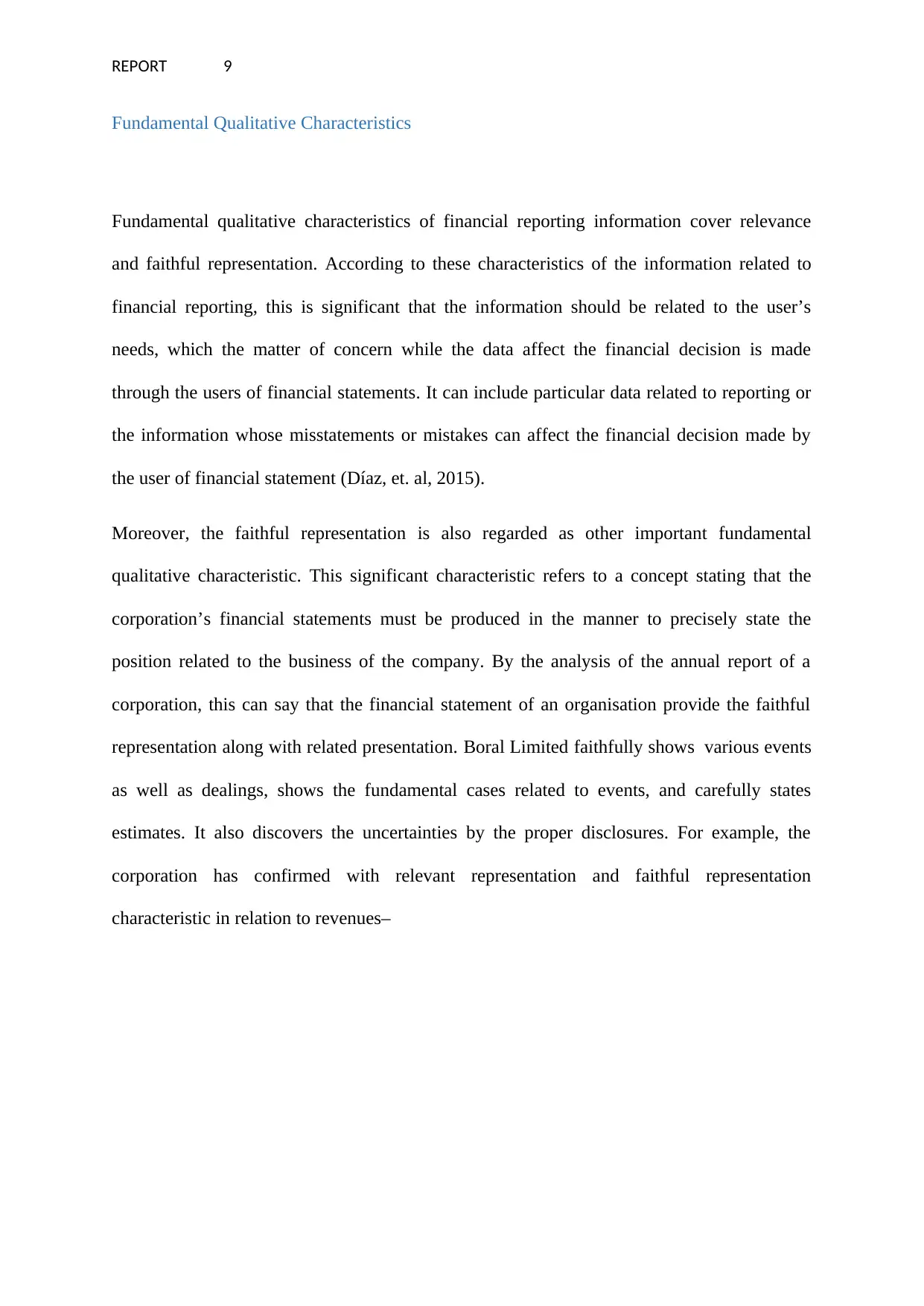

Fundamental Qualitative Characteristics

Fundamental qualitative characteristics of financial reporting information cover relevance

and faithful representation. According to these characteristics of the information related to

financial reporting, this is significant that the information should be related to the user’s

needs, which the matter of concern while the data affect the financial decision is made

through the users of financial statements. It can include particular data related to reporting or

the information whose misstatements or mistakes can affect the financial decision made by

the user of financial statement (Díaz, et. al, 2015).

Moreover, the faithful representation is also regarded as other important fundamental

qualitative characteristic. This significant characteristic refers to a concept stating that the

corporation’s financial statements must be produced in the manner to precisely state the

position related to the business of the company. By the analysis of the annual report of a

corporation, this can say that the financial statement of an organisation provide the faithful

representation along with related presentation. Boral Limited faithfully shows various events

as well as dealings, shows the fundamental cases related to events, and carefully states

estimates. It also discovers the uncertainties by the proper disclosures. For example, the

corporation has confirmed with relevant representation and faithful representation

characteristic in relation to revenues–

Fundamental Qualitative Characteristics

Fundamental qualitative characteristics of financial reporting information cover relevance

and faithful representation. According to these characteristics of the information related to

financial reporting, this is significant that the information should be related to the user’s

needs, which the matter of concern while the data affect the financial decision is made

through the users of financial statements. It can include particular data related to reporting or

the information whose misstatements or mistakes can affect the financial decision made by

the user of financial statement (Díaz, et. al, 2015).

Moreover, the faithful representation is also regarded as other important fundamental

qualitative characteristic. This significant characteristic refers to a concept stating that the

corporation’s financial statements must be produced in the manner to precisely state the

position related to the business of the company. By the analysis of the annual report of a

corporation, this can say that the financial statement of an organisation provide the faithful

representation along with related presentation. Boral Limited faithfully shows various events

as well as dealings, shows the fundamental cases related to events, and carefully states

estimates. It also discovers the uncertainties by the proper disclosures. For example, the

corporation has confirmed with relevant representation and faithful representation

characteristic in relation to revenues–

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REPORT 10

Conclusion

As per this discussion, it can say that the conceptual framework states nature of financial

reporting as well as accounting, the functions, and the drawbacks. This is regarded that the

Financial Accounting Standards Board’s contribution thus far and the presence to this day are

because of the conceptual framework’s quality and the utility. The major reason to establish

the agreed conceptual framework is that this renders the fundamental principles that improve

the setting of accounting standards. The accounting Concepts can be considered as the

fundamental accounting assumption, which acts as the foundation for making the financial

statement of the organisation. Additionally, the accounting concepts render the integrated

structure and rational strategy to the accounting procedure. The financial transactions that

occur are interpreted considering the accounting concepts that direct the accounting method.

Conclusion

As per this discussion, it can say that the conceptual framework states nature of financial

reporting as well as accounting, the functions, and the drawbacks. This is regarded that the

Financial Accounting Standards Board’s contribution thus far and the presence to this day are

because of the conceptual framework’s quality and the utility. The major reason to establish

the agreed conceptual framework is that this renders the fundamental principles that improve

the setting of accounting standards. The accounting Concepts can be considered as the

fundamental accounting assumption, which acts as the foundation for making the financial

statement of the organisation. Additionally, the accounting concepts render the integrated

structure and rational strategy to the accounting procedure. The financial transactions that

occur are interpreted considering the accounting concepts that direct the accounting method.

REPORT 11

References

Annual Report (2018) Boral Annual Report 2018. Available at:

http://acquia-stg.boral.com/sites/corporate/files/media/field_document/Boral-Annual-Report-

2018.pdf. Access on 30/05/2019

Bekçioğlu, S., Kaderli, Y., Köroğlu, Ç. and Sezer, D. (2016) A New Cost Accounting

Concept by the End of 20th Century: Strategic Cost Management. Muhasebe ve Finans

Tarihi Araştırmaları Dergisi, (10), pp.120-138.

Bloomberg (2018). Boral limited. Available at:

https://www.bloomberg.com/research/stocks/private/snapshot.asp?privcapId=392930. Access

on 29/05/2019

Bridgett, D.J., Burt, N.M., Edwards, E.S. and Deater-Deckard, K. (2015) Intergenerational

transmission of self-regulation: A multidisciplinary review and integrative conceptual

framework. Psychological Bulletin, 141(3), p.602.

Costa, M. and Torrecchia, P. (2018) The concept of value for CSR: A debate drawn from

Italian classical accounting. Corporate Social Responsibility and Environmental

Management, 25(2), pp.113-123.

Crandall, A., Deater-Deckard, K. and Riley, A.W. (2015) Maternal emotion and cognitive

control capacities and parenting: A conceptual framework. Developmental Review, 36,

pp.105-126.

Crespo, J., Boschma, R. and Balland, P.A. (2017) Resilience, networks and competitiveness:

a conceptual framework. In Handbook of Regions and Competitiveness. Edward Elgar

Publishing.

References

Annual Report (2018) Boral Annual Report 2018. Available at:

http://acquia-stg.boral.com/sites/corporate/files/media/field_document/Boral-Annual-Report-

2018.pdf. Access on 30/05/2019

Bekçioğlu, S., Kaderli, Y., Köroğlu, Ç. and Sezer, D. (2016) A New Cost Accounting

Concept by the End of 20th Century: Strategic Cost Management. Muhasebe ve Finans

Tarihi Araştırmaları Dergisi, (10), pp.120-138.

Bloomberg (2018). Boral limited. Available at:

https://www.bloomberg.com/research/stocks/private/snapshot.asp?privcapId=392930. Access

on 29/05/2019

Bridgett, D.J., Burt, N.M., Edwards, E.S. and Deater-Deckard, K. (2015) Intergenerational

transmission of self-regulation: A multidisciplinary review and integrative conceptual

framework. Psychological Bulletin, 141(3), p.602.

Costa, M. and Torrecchia, P. (2018) The concept of value for CSR: A debate drawn from

Italian classical accounting. Corporate Social Responsibility and Environmental

Management, 25(2), pp.113-123.

Crandall, A., Deater-Deckard, K. and Riley, A.W. (2015) Maternal emotion and cognitive

control capacities and parenting: A conceptual framework. Developmental Review, 36,

pp.105-126.

Crespo, J., Boschma, R. and Balland, P.A. (2017) Resilience, networks and competitiveness:

a conceptual framework. In Handbook of Regions and Competitiveness. Edward Elgar

Publishing.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.