Comprehensive Financial Analysis Report: Marshall Motor Holdings PLC

VerifiedAdded on 2020/04/29

|27

|8175

|33

Project

AI Summary

This project report conducts a comprehensive financial analysis of Marshall Motor Holdings PLC, utilizing the CORE approach (Context, Overview, Ratio Analysis, and Evaluation) to assess the company's financial health and performance. The report examines the internal and external contexts affecting the company, providing an overview of its operations, including its market position and key performance indicators such as sales and operating profit. Ratio analysis, encompassing liquidity, profitability, solvency, and efficiency ratios, is performed to evaluate the company's financial strengths and weaknesses over several years. The evaluation phase synthesizes the findings, offering insights into the company's competitive landscape, market position, and overall financial stability. The report concludes with an assessment of the company's current financial standing and future prospects, offering valuable information for investors and stakeholders. The analysis includes competitor analysis to find out the condition of the comapny in the market. For this report, MARSHAL MOTOR HOLDINGS PLC has been taken into the concern and the above evaluation method has been performed over this company.

Running Head: Accounting and financial management

1

Project Report: Accounting and financial management

1

Project Report: Accounting and financial management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting and financial management 2

Executive Summary:

This report has been prepared to analyze the financial performance of a company. In

this report, CORE approach (context performance, overview of the comapny, ratio analysis

and evaluation) has been done to evaluate the financial strength of the company. Further, the

financial statement of the comapny has been evaluated to analyze the changes and the

performance of the comapny in terms of the financial figures. More, the competition analysis

has also been done to find out the condition of the comapny in the market. For this report,

MARSHAL MOTOR HOLDINGS PLC has been taken into the concern and the above

evaluation method has been performed over this company.

Executive Summary:

This report has been prepared to analyze the financial performance of a company. In

this report, CORE approach (context performance, overview of the comapny, ratio analysis

and evaluation) has been done to evaluate the financial strength of the company. Further, the

financial statement of the comapny has been evaluated to analyze the changes and the

performance of the comapny in terms of the financial figures. More, the competition analysis

has also been done to find out the condition of the comapny in the market. For this report,

MARSHAL MOTOR HOLDINGS PLC has been taken into the concern and the above

evaluation method has been performed over this company.

Accounting and financial management 3

Contents

Part A................................................................................................................................4

Introduction.................................................................................................................4

CORE approach.........................................................................................................4

Financial performance...............................................................................................8

Market position...........................................................................................................9

Competitor analysis.................................................................................................10

Conclusion.................................................................................................................12

Part B1 Fido’s Frisbees...................................................................................................13

Case B1...........................................................................................................................13

Introduction...............................................................................................................13

Profit of the company...............................................................................................13

Breakeven perspective............................................................................................13

Cash flow forecast...................................................................................................14

Recommendation and conclusion.........................................................................14

References.......................................................................................................................15

Appendix.........................................................................................................................17

Contents

Part A................................................................................................................................4

Introduction.................................................................................................................4

CORE approach.........................................................................................................4

Financial performance...............................................................................................8

Market position...........................................................................................................9

Competitor analysis.................................................................................................10

Conclusion.................................................................................................................12

Part B1 Fido’s Frisbees...................................................................................................13

Case B1...........................................................................................................................13

Introduction...............................................................................................................13

Profit of the company...............................................................................................13

Breakeven perspective............................................................................................13

Cash flow forecast...................................................................................................14

Recommendation and conclusion.........................................................................14

References.......................................................................................................................15

Appendix.........................................................................................................................17

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting and financial management 4

Part A

Introduction:

This report has been prepared to analyze the performance of the Marshall Motor plc.

This report depicts the user about the various position of the company which could be used

by the user while making a decision about making the investment into the company. This

report has been prepared over the company through taking the concern of various tools and

techniques so that the performance could be measured in a perfect manner and a good

result could be offered to the top level management of the company to make a better

decisions about the performance of the company and make the strategies on the basis of

that (horngren, 2009).

In this report, CORE approach (context performance, overview of the comapny, ratio

analysis and evaluation) has been done to evaluate the financial strength of the company.

Further, the financial statement of the comapny has been evaluated to analyze the changes

and the performance of the comapny in terms of the financial figures. More, the competition

analysis has also been done to find out the condition of the comapny in the market.

For this report, various tools and techniques have been analyzed. The CORE

approach of the company describes that the financial perf0rmance of the company in terms

of the internal and external phases are quite attractive and helping the company to manage

the activities, operations, functions and the performance of the company.

CORE approach:

“CORE” is an approach which has been invented by the Moon and Bates to analyze

the financial performance of a company. CORE approach of a company depict about the

performance of an organization in context of the various financial terms. CORE approach

depict that it becomes mandatory for an organization to evaluate its business with context of

the many terms so that a best result could be got and it becomes easy for the company to

manage the performance and make a better decision about the performance and the

position of the company. This approach assists the users to identify and understand the

competitive environment, it also assist the comapny to manage the performance of the

comapny itself (Hopper, Northcott & Scapens, 2007). In core approach, context of a

comapny, overview of the comapny, ratio analysis and evaluation of the company has been

evaluated so that the best analysis could be done over the comapny. The CORE approach

study has been conducted over the MARSHAL MOTOR HOLDINGS PLC to analyze and

evaluate the performance of the company in terms of various financial matters so that a best

Part A

Introduction:

This report has been prepared to analyze the performance of the Marshall Motor plc.

This report depicts the user about the various position of the company which could be used

by the user while making a decision about making the investment into the company. This

report has been prepared over the company through taking the concern of various tools and

techniques so that the performance could be measured in a perfect manner and a good

result could be offered to the top level management of the company to make a better

decisions about the performance of the company and make the strategies on the basis of

that (horngren, 2009).

In this report, CORE approach (context performance, overview of the comapny, ratio

analysis and evaluation) has been done to evaluate the financial strength of the company.

Further, the financial statement of the comapny has been evaluated to analyze the changes

and the performance of the comapny in terms of the financial figures. More, the competition

analysis has also been done to find out the condition of the comapny in the market.

For this report, various tools and techniques have been analyzed. The CORE

approach of the company describes that the financial perf0rmance of the company in terms

of the internal and external phases are quite attractive and helping the company to manage

the activities, operations, functions and the performance of the company.

CORE approach:

“CORE” is an approach which has been invented by the Moon and Bates to analyze

the financial performance of a company. CORE approach of a company depict about the

performance of an organization in context of the various financial terms. CORE approach

depict that it becomes mandatory for an organization to evaluate its business with context of

the many terms so that a best result could be got and it becomes easy for the company to

manage the performance and make a better decision about the performance and the

position of the company. This approach assists the users to identify and understand the

competitive environment, it also assist the comapny to manage the performance of the

comapny itself (Hopper, Northcott & Scapens, 2007). In core approach, context of a

comapny, overview of the comapny, ratio analysis and evaluation of the company has been

evaluated so that the best analysis could be done over the comapny. The CORE approach

study has been conducted over the MARSHAL MOTOR HOLDINGS PLC to analyze and

evaluate the performance of the company in terms of various financial matters so that a best

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting and financial management 5

decision could be taken and strategy could be prepared accordingly. Following is the study

of the CORE approach of MARSHAL MOTOR HOLDINGS PLC:

Context:

Context is the first phase of the CORE approach which depict about the various

phases of the company in terms of the finance. This study depict that how is the comapny

performing in the market. Further, various tools and techniques have been analyzed to

perform this study and reach over a conclusion so that the good decision could be made by

the management of the company and the investors.

Context is a study which is done over the internal and external phases of a comapny.

External context depicts about the commercial environment which surrounds over the

comapny whereas internal context depicts about the management and the organizational

level of a company (Hansen, Mowen and Guan, 2007).

The study over MARSHALL MOTOR PLC depict that the internal context of the

comapny is quite attractive, comapny is managing the business in a better way than other

companies in the industry. Further, it has been found that the company has changed the

various polices and strategies to manage the performance and the capital structure of the

company. From past trends, the current trends of the comapny are bit better and the current

investment in the comapny would offer the high return to the investing comapny.

At the same time, the external context of the comapny has been analyzed and it has

been found that the performance of the industry is quite attractive, economical condition of

the comapny has also become better right now (Hansen, Mowen & Madison, 2010). Further,

it has been found that the company has changed the various polices and strategies to

manage the performance and the capital structure according to the industry so that it could

attract the investors more.

Overview:

Overview is the second phase of the CORE approach which depict about the various

phases of the company in terms of the finance. This study depict that how is the comapny

performing in the market. Further, various tools and techniques have been analyzed to

perform this study and reach over a conclusion so that the good decision could be made by

the management of the company and the investors.

Marshall Motor Holdings plc has registered itself in the London stock exchange. The

main functions and the activities of the company are the repairing and selling the various

commercial vehicles and the passenger’s vehicles in the international market. This comapny

decision could be taken and strategy could be prepared accordingly. Following is the study

of the CORE approach of MARSHAL MOTOR HOLDINGS PLC:

Context:

Context is the first phase of the CORE approach which depict about the various

phases of the company in terms of the finance. This study depict that how is the comapny

performing in the market. Further, various tools and techniques have been analyzed to

perform this study and reach over a conclusion so that the good decision could be made by

the management of the company and the investors.

Context is a study which is done over the internal and external phases of a comapny.

External context depicts about the commercial environment which surrounds over the

comapny whereas internal context depicts about the management and the organizational

level of a company (Hansen, Mowen and Guan, 2007).

The study over MARSHALL MOTOR PLC depict that the internal context of the

comapny is quite attractive, comapny is managing the business in a better way than other

companies in the industry. Further, it has been found that the company has changed the

various polices and strategies to manage the performance and the capital structure of the

company. From past trends, the current trends of the comapny are bit better and the current

investment in the comapny would offer the high return to the investing comapny.

At the same time, the external context of the comapny has been analyzed and it has

been found that the performance of the industry is quite attractive, economical condition of

the comapny has also become better right now (Hansen, Mowen & Madison, 2010). Further,

it has been found that the company has changed the various polices and strategies to

manage the performance and the capital structure according to the industry so that it could

attract the investors more.

Overview:

Overview is the second phase of the CORE approach which depict about the various

phases of the company in terms of the finance. This study depict that how is the comapny

performing in the market. Further, various tools and techniques have been analyzed to

perform this study and reach over a conclusion so that the good decision could be made by

the management of the company and the investors.

Marshall Motor Holdings plc has registered itself in the London stock exchange. The

main functions and the activities of the company are the repairing and selling the various

commercial vehicles and the passenger’s vehicles in the international market. This comapny

Accounting and financial management 6

has 103 franchises which cover around 24 brands of the company and the business

operates its business across 25 countries and 28 sites (Home, 2017).

This company is performing very well in the market, the sales turnover of the

company has been analyzed and it has been found that the company’s turnover has been

enhanced by 54.08%. Further, it has also been found that the operating profit of the

comapny has been rose by the 59.23%. The other evaluation and calculations of the

comapny is as follows:

Calculation of the increment

2016 2015

Sales 1899405000 1232761000 54.08%

Operating profit 29054000 18246000 59.23%

Earnings 17762000 11721000 51.54%

Dividend payment 3251000 15448000 -78.96%

Market

capitalization 145638000 129884000 12.13%

Operating cash flow 80309000 25493000 215.02%

Capital expenditure 40754000 -2169000

-

1978.93%

Debt increment 85444000 28642000 198.32%

(Garrison, Noreen, Brewer and McGowan, 2010)

This table depicts that the performance of the comapny has became way better than

the last year.

Ratio:

Ratio is the third phase of the CORE approach which depict about the various

phases of the company in terms of the finance. This study depict that how is the comapny

performing in the market. Further, various tools and techniques have been analyzed to

perform this study and reach over a conclusion so that the good decision could be made by

the management of the company and the investors

Further, the study over the ratio analysis has been done to analyze the financial

strength position and the condition of the company. In this study, the analysis has been done

over the various position of the company such as liquidity ratios, profitability ratios, solvency

ratios and the efficiency ratios (Bhimani et al, 2008).

The evaluation of the ratio depicts that the profitability position of the comapny has

became better than the last year. In 2016, the comapny has earned more return on equity.

Further, the liquidity ratios of the comapny depict that the position of the comapny to pay the

debt has became lower in 2016 rather than the last year. This depict that the company is

has 103 franchises which cover around 24 brands of the company and the business

operates its business across 25 countries and 28 sites (Home, 2017).

This company is performing very well in the market, the sales turnover of the

company has been analyzed and it has been found that the company’s turnover has been

enhanced by 54.08%. Further, it has also been found that the operating profit of the

comapny has been rose by the 59.23%. The other evaluation and calculations of the

comapny is as follows:

Calculation of the increment

2016 2015

Sales 1899405000 1232761000 54.08%

Operating profit 29054000 18246000 59.23%

Earnings 17762000 11721000 51.54%

Dividend payment 3251000 15448000 -78.96%

Market

capitalization 145638000 129884000 12.13%

Operating cash flow 80309000 25493000 215.02%

Capital expenditure 40754000 -2169000

-

1978.93%

Debt increment 85444000 28642000 198.32%

(Garrison, Noreen, Brewer and McGowan, 2010)

This table depicts that the performance of the comapny has became way better than

the last year.

Ratio:

Ratio is the third phase of the CORE approach which depict about the various

phases of the company in terms of the finance. This study depict that how is the comapny

performing in the market. Further, various tools and techniques have been analyzed to

perform this study and reach over a conclusion so that the good decision could be made by

the management of the company and the investors

Further, the study over the ratio analysis has been done to analyze the financial

strength position and the condition of the company. In this study, the analysis has been done

over the various position of the company such as liquidity ratios, profitability ratios, solvency

ratios and the efficiency ratios (Bhimani et al, 2008).

The evaluation of the ratio depicts that the profitability position of the comapny has

became better than the last year. In 2016, the comapny has earned more return on equity.

Further, the liquidity ratios of the comapny depict that the position of the comapny to pay the

debt has became lower in 2016 rather than the last year. This depict that the company is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

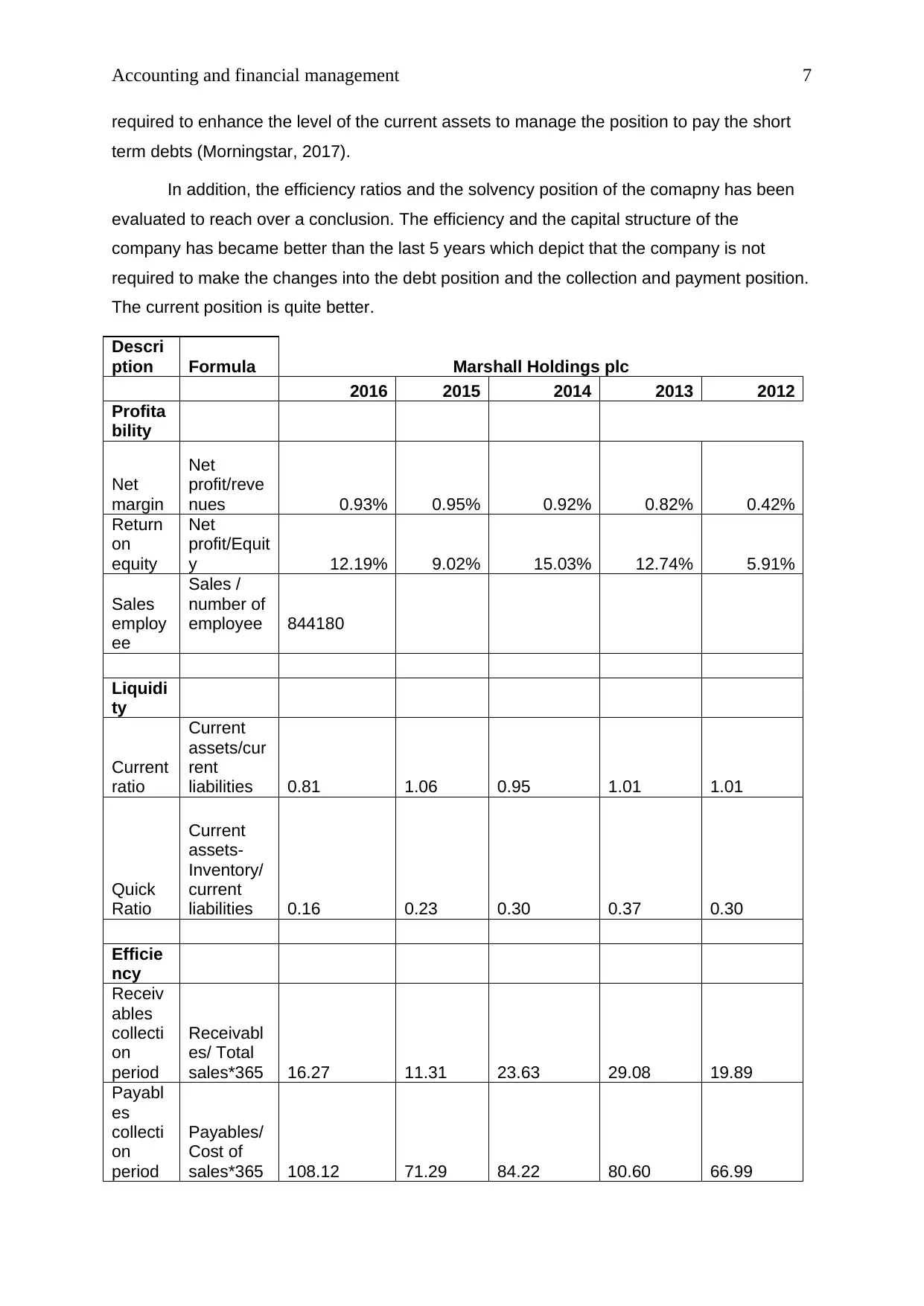

Accounting and financial management 7

required to enhance the level of the current assets to manage the position to pay the short

term debts (Morningstar, 2017).

In addition, the efficiency ratios and the solvency position of the comapny has been

evaluated to reach over a conclusion. The efficiency and the capital structure of the

company has became better than the last 5 years which depict that the company is not

required to make the changes into the debt position and the collection and payment position.

The current position is quite better.

Descri

ption Formula Marshall Holdings plc

2016 2015 2014 2013 2012

Profita

bility

Net

margin

Net

profit/reve

nues 0.93% 0.95% 0.92% 0.82% 0.42%

Return

on

equity

Net

profit/Equit

y 12.19% 9.02% 15.03% 12.74% 5.91%

Sales

employ

ee

Sales /

number of

employee 844180

Liquidi

ty

Current

ratio

Current

assets/cur

rent

liabilities 0.81 1.06 0.95 1.01 1.01

Quick

Ratio

Current

assets-

Inventory/

current

liabilities 0.16 0.23 0.30 0.37 0.30

Efficie

ncy

Receiv

ables

collecti

on

period

Receivabl

es/ Total

sales*365 16.27 11.31 23.63 29.08 19.89

Payabl

es

collecti

on

period

Payables/

Cost of

sales*365 108.12 71.29 84.22 80.60 66.99

required to enhance the level of the current assets to manage the position to pay the short

term debts (Morningstar, 2017).

In addition, the efficiency ratios and the solvency position of the comapny has been

evaluated to reach over a conclusion. The efficiency and the capital structure of the

company has became better than the last 5 years which depict that the company is not

required to make the changes into the debt position and the collection and payment position.

The current position is quite better.

Descri

ption Formula Marshall Holdings plc

2016 2015 2014 2013 2012

Profita

bility

Net

margin

Net

profit/reve

nues 0.93% 0.95% 0.92% 0.82% 0.42%

Return

on

equity

Net

profit/Equit

y 12.19% 9.02% 15.03% 12.74% 5.91%

Sales

employ

ee

Sales /

number of

employee 844180

Liquidi

ty

Current

ratio

Current

assets/cur

rent

liabilities 0.81 1.06 0.95 1.01 1.01

Quick

Ratio

Current

assets-

Inventory/

current

liabilities 0.16 0.23 0.30 0.37 0.30

Efficie

ncy

Receiv

ables

collecti

on

period

Receivabl

es/ Total

sales*365 16.27 11.31 23.63 29.08 19.89

Payabl

es

collecti

on

period

Payables/

Cost of

sales*365 108.12 71.29 84.22 80.60 66.99

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting and financial management 8

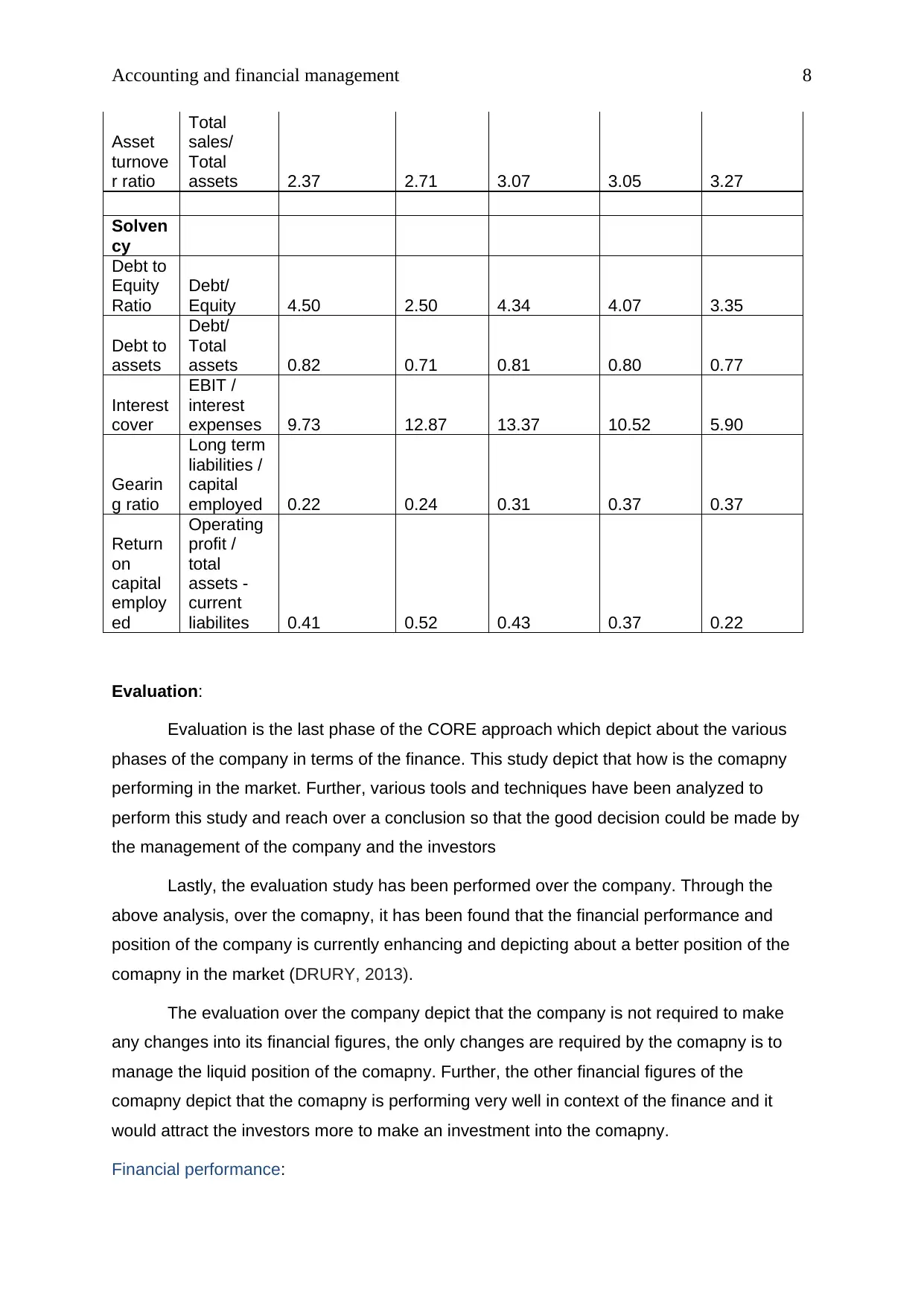

Asset

turnove

r ratio

Total

sales/

Total

assets 2.37 2.71 3.07 3.05 3.27

Solven

cy

Debt to

Equity

Ratio

Debt/

Equity 4.50 2.50 4.34 4.07 3.35

Debt to

assets

Debt/

Total

assets 0.82 0.71 0.81 0.80 0.77

Interest

cover

EBIT /

interest

expenses 9.73 12.87 13.37 10.52 5.90

Gearin

g ratio

Long term

liabilities /

capital

employed 0.22 0.24 0.31 0.37 0.37

Return

on

capital

employ

ed

Operating

profit /

total

assets -

current

liabilites 0.41 0.52 0.43 0.37 0.22

Evaluation:

Evaluation is the last phase of the CORE approach which depict about the various

phases of the company in terms of the finance. This study depict that how is the comapny

performing in the market. Further, various tools and techniques have been analyzed to

perform this study and reach over a conclusion so that the good decision could be made by

the management of the company and the investors

Lastly, the evaluation study has been performed over the company. Through the

above analysis, over the comapny, it has been found that the financial performance and

position of the company is currently enhancing and depicting about a better position of the

comapny in the market (DRURY, 2013).

The evaluation over the company depict that the company is not required to make

any changes into its financial figures, the only changes are required by the comapny is to

manage the liquid position of the comapny. Further, the other financial figures of the

comapny depict that the comapny is performing very well in context of the finance and it

would attract the investors more to make an investment into the comapny.

Financial performance:

Asset

turnove

r ratio

Total

sales/

Total

assets 2.37 2.71 3.07 3.05 3.27

Solven

cy

Debt to

Equity

Ratio

Debt/

Equity 4.50 2.50 4.34 4.07 3.35

Debt to

assets

Debt/

Total

assets 0.82 0.71 0.81 0.80 0.77

Interest

cover

EBIT /

interest

expenses 9.73 12.87 13.37 10.52 5.90

Gearin

g ratio

Long term

liabilities /

capital

employed 0.22 0.24 0.31 0.37 0.37

Return

on

capital

employ

ed

Operating

profit /

total

assets -

current

liabilites 0.41 0.52 0.43 0.37 0.22

Evaluation:

Evaluation is the last phase of the CORE approach which depict about the various

phases of the company in terms of the finance. This study depict that how is the comapny

performing in the market. Further, various tools and techniques have been analyzed to

perform this study and reach over a conclusion so that the good decision could be made by

the management of the company and the investors

Lastly, the evaluation study has been performed over the company. Through the

above analysis, over the comapny, it has been found that the financial performance and

position of the company is currently enhancing and depicting about a better position of the

comapny in the market (DRURY, 2013).

The evaluation over the company depict that the company is not required to make

any changes into its financial figures, the only changes are required by the comapny is to

manage the liquid position of the comapny. Further, the other financial figures of the

comapny depict that the comapny is performing very well in context of the finance and it

would attract the investors more to make an investment into the comapny.

Financial performance:

Accounting and financial management 9

In addition, the study has been performed over the financial performance of the

comapny, through this analysis, it has been found that the position of the comapny has

became very well in the market in 2016 in comparison of its last years, through the study

over the financial statements of the comapny of last 5 years, it has been evaluated that the

company has performed way better in the last 5 years (Schlichting, 2013). The turnover of

the comapny has been enhanced from last 5 years by 181%. Further, the details of the

company depict that the changes which have been faced by the comapny express about the

positive changes and the performance of the company.

The additional study over the income statement of the company expresses that the

net income of the company has been enhanced on a great level from 2012 in 2016. The

changes expresses that it is a good option for the investing companies to make an

investment into this comapny for a long term to manage and enhance the worth of the

invested amount (London stock exchange, 2017).

The further study over the statement of the financial position of the company

expresses that the total assets and the total liabilities of the company has been enhanced on

a great level from 2012 in 2016 (Phillips and Stawarski, 2016). The changes expresses that

it is a good option for the investing companies to make an investment into this comapny for a

long term to manage and enhance the worth of the invested amount. The company has

managed the position in a great manner.

The additional study over the statement of the cash flow of the company expresses

that the cash flow position of the company has been better from 2012 in 2016. The changes

expresses that it is a good option for the investing companies to make an investment into

this comapny for a long term to manage and enhance the worth of the invested amount

(Madhura, 2014).

Market position:

Further, the market position of the company has been investigated to find out the

performance and the position of the company in the market. For this analysis, PESTLE has

been analyzed (Palicka, 2011). The PESTLE study of the company is as follows:

Political factor:

Political stability and significance in

material and construction sector in

the economy

Military invasion risk

Economical factor:

Interest rate

Inflation rate

Discretionary rate

In addition, the study has been performed over the financial performance of the

comapny, through this analysis, it has been found that the position of the comapny has

became very well in the market in 2016 in comparison of its last years, through the study

over the financial statements of the comapny of last 5 years, it has been evaluated that the

company has performed way better in the last 5 years (Schlichting, 2013). The turnover of

the comapny has been enhanced from last 5 years by 181%. Further, the details of the

company depict that the changes which have been faced by the comapny express about the

positive changes and the performance of the company.

The additional study over the income statement of the company expresses that the

net income of the company has been enhanced on a great level from 2012 in 2016. The

changes expresses that it is a good option for the investing companies to make an

investment into this comapny for a long term to manage and enhance the worth of the

invested amount (London stock exchange, 2017).

The further study over the statement of the financial position of the company

expresses that the total assets and the total liabilities of the company has been enhanced on

a great level from 2012 in 2016 (Phillips and Stawarski, 2016). The changes expresses that

it is a good option for the investing companies to make an investment into this comapny for a

long term to manage and enhance the worth of the invested amount. The company has

managed the position in a great manner.

The additional study over the statement of the cash flow of the company expresses

that the cash flow position of the company has been better from 2012 in 2016. The changes

expresses that it is a good option for the investing companies to make an investment into

this comapny for a long term to manage and enhance the worth of the invested amount

(Madhura, 2014).

Market position:

Further, the market position of the company has been investigated to find out the

performance and the position of the company in the market. For this analysis, PESTLE has

been analyzed (Palicka, 2011). The PESTLE study of the company is as follows:

Political factor:

Political stability and significance in

material and construction sector in

the economy

Military invasion risk

Economical factor:

Interest rate

Inflation rate

Discretionary rate

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting and financial management 10

Corruption level

Property protection

Favoured trading partners

Mandatory employee benefits

Industry safety regulations

Intellectual property protection

Legal framework

Week regulations in material and

construction

Business cycle stage

Labour cost and productivity

Educational level

Financial market efficiency

Infrastructure quality in the company

and in the industry

Comparative advantages

Stability in the market

Exchange rate fluctuations

Social Factor:

Skill level of the pubic

Demographics

Leisure interest

Culture

Attitudes

Class structure

Hierarchy and power structure

Broader nature of society and

entrepreneurial spirit

Technological factor:

Various changes in the technology

New development

Technological diffusion

Value chain structure impact

Cost structure impact

Impact over the product offering

Service offering impact

From the above analysis, it has been found that various changes have taken place

into the position and the performance of the industry. The above factors impact over the

entire industry as whole and thus the company is required to look over these changes and

make a better decision accordingly.

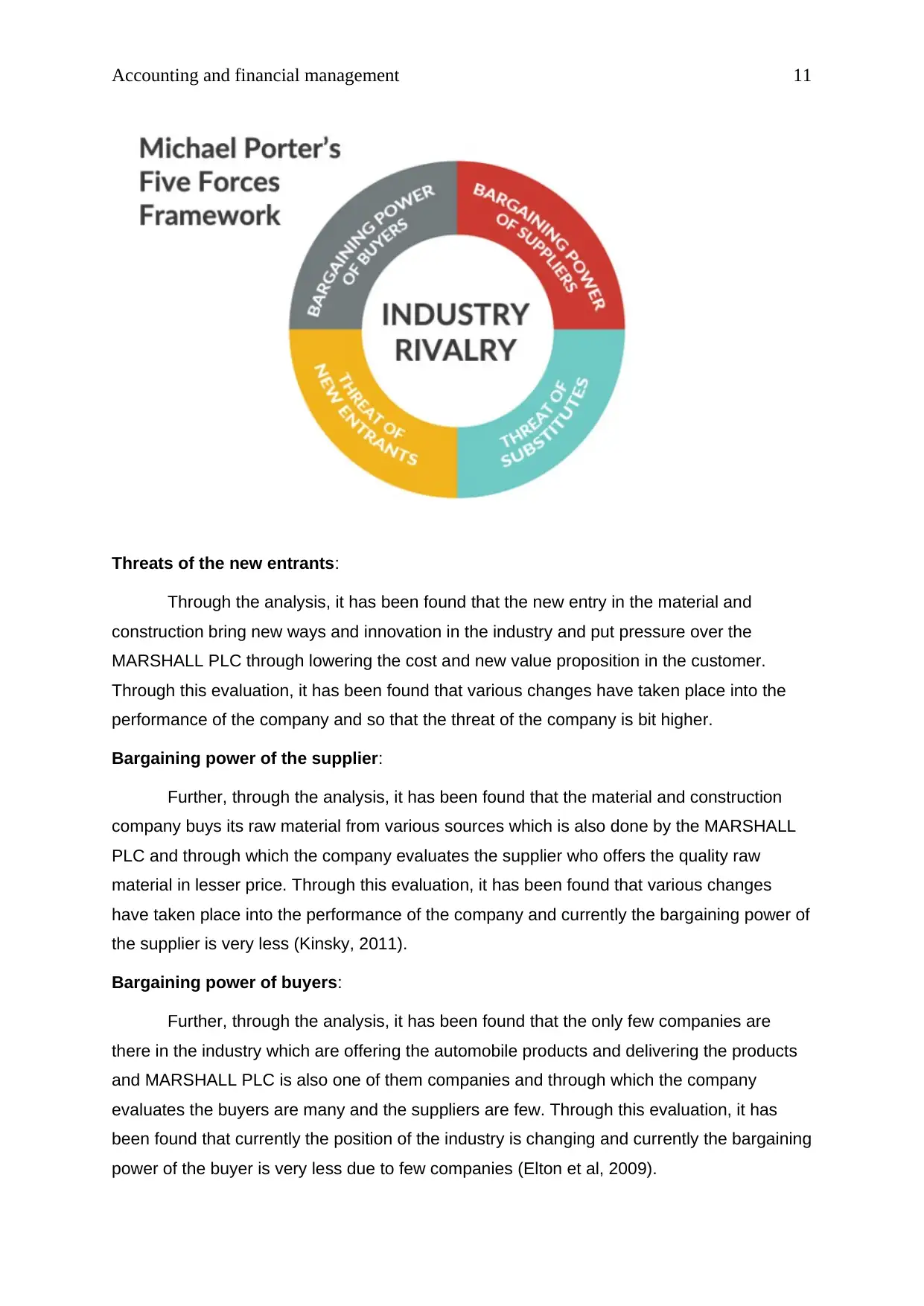

Competitor analysis:

Further the competitive analysis of the company expresses that the main competitors

of the comapny is the LOOKER’S PLC. For the competitive analysis, porter’s 5 forces model

study has been performed over the MASHALL MOTOR HOLDIGS PLC. Michael has

observed that the five forces make an impact over the profitability position of the company.

Corruption level

Property protection

Favoured trading partners

Mandatory employee benefits

Industry safety regulations

Intellectual property protection

Legal framework

Week regulations in material and

construction

Business cycle stage

Labour cost and productivity

Educational level

Financial market efficiency

Infrastructure quality in the company

and in the industry

Comparative advantages

Stability in the market

Exchange rate fluctuations

Social Factor:

Skill level of the pubic

Demographics

Leisure interest

Culture

Attitudes

Class structure

Hierarchy and power structure

Broader nature of society and

entrepreneurial spirit

Technological factor:

Various changes in the technology

New development

Technological diffusion

Value chain structure impact

Cost structure impact

Impact over the product offering

Service offering impact

From the above analysis, it has been found that various changes have taken place

into the position and the performance of the industry. The above factors impact over the

entire industry as whole and thus the company is required to look over these changes and

make a better decision accordingly.

Competitor analysis:

Further the competitive analysis of the company expresses that the main competitors

of the comapny is the LOOKER’S PLC. For the competitive analysis, porter’s 5 forces model

study has been performed over the MASHALL MOTOR HOLDIGS PLC. Michael has

observed that the five forces make an impact over the profitability position of the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting and financial management 11

Threats of the new entrants:

Through the analysis, it has been found that the new entry in the material and

construction bring new ways and innovation in the industry and put pressure over the

MARSHALL PLC through lowering the cost and new value proposition in the customer.

Through this evaluation, it has been found that various changes have taken place into the

performance of the company and so that the threat of the company is bit higher.

Bargaining power of the supplier:

Further, through the analysis, it has been found that the material and construction

company buys its raw material from various sources which is also done by the MARSHALL

PLC and through which the company evaluates the supplier who offers the quality raw

material in lesser price. Through this evaluation, it has been found that various changes

have taken place into the performance of the company and currently the bargaining power of

the supplier is very less (Kinsky, 2011).

Bargaining power of buyers:

Further, through the analysis, it has been found that the only few companies are

there in the industry which are offering the automobile products and delivering the products

and MARSHALL PLC is also one of them companies and through which the company

evaluates the buyers are many and the suppliers are few. Through this evaluation, it has

been found that currently the position of the industry is changing and currently the bargaining

power of the buyer is very less due to few companies (Elton et al, 2009).

Threats of the new entrants:

Through the analysis, it has been found that the new entry in the material and

construction bring new ways and innovation in the industry and put pressure over the

MARSHALL PLC through lowering the cost and new value proposition in the customer.

Through this evaluation, it has been found that various changes have taken place into the

performance of the company and so that the threat of the company is bit higher.

Bargaining power of the supplier:

Further, through the analysis, it has been found that the material and construction

company buys its raw material from various sources which is also done by the MARSHALL

PLC and through which the company evaluates the supplier who offers the quality raw

material in lesser price. Through this evaluation, it has been found that various changes

have taken place into the performance of the company and currently the bargaining power of

the supplier is very less (Kinsky, 2011).

Bargaining power of buyers:

Further, through the analysis, it has been found that the only few companies are

there in the industry which are offering the automobile products and delivering the products

and MARSHALL PLC is also one of them companies and through which the company

evaluates the buyers are many and the suppliers are few. Through this evaluation, it has

been found that currently the position of the industry is changing and currently the bargaining

power of the buyer is very less due to few companies (Elton et al, 2009).

Accounting and financial management 12

Threat from substitute products:

Further, through the analysis, it has been found that the various subsidiary products

are there in the market which affects the product and services of the company such as direct

dealership from the manufacturing company. Through this evaluation, it has been found that

currently the position of the industry is changing and currently the threat from the substitute

products is quite higher.

Rivalry among the existing players:

Lastly, through the analysis, it has been found that various companies are there in

the industry such as Lookers’ plc which impact over the position of the MARSHALL PLC.

Through this evaluation, it has been found that the market share of the LOOKERS PLC is

better than the MARSHAL MOTOR HOLDINGS PLC limited. The financial statement and the

financial figures of the LOOKERS PLC depicts that it is the market leader in the comapny

(Morningstar, 2017). Currently the threat from the existing player to the company is also

higher.

Conclusion:

To conclude, CORE approach (context performance, overview of the comapny, ratio

analysis and evaluation) has been done to evaluate the financial strength of the company.

The context depict that the comapny is internally and externally quite string to manage all the

activities and functions of the company. The overview of the comapny in terms of finance

depict that the performance of this company has became very god than 012 in 2016. These

changes have helped the company to grab more opportunities.

In addition, ratio analysis study has also been performed over the comapny and it

has been found that comapny in enough strong in terms of profitability, capital structure and

solvency position. Further, the financial statement of the comapny has been evaluated to

analyze the changes and the performance of the comapny in terms of the financial figures.

More, the competition analysis has also been done to find out the condition of the comapny

in the market.

Through this report, it could be concluded that the contract with the MARSHAL

MOTOR HOLDING PLC would offer the high return to the comapny. Still, there are few

recommendations which must be followed by the company to manage the operations and

grab the opportunities from the market.

Threat from substitute products:

Further, through the analysis, it has been found that the various subsidiary products

are there in the market which affects the product and services of the company such as direct

dealership from the manufacturing company. Through this evaluation, it has been found that

currently the position of the industry is changing and currently the threat from the substitute

products is quite higher.

Rivalry among the existing players:

Lastly, through the analysis, it has been found that various companies are there in

the industry such as Lookers’ plc which impact over the position of the MARSHALL PLC.

Through this evaluation, it has been found that the market share of the LOOKERS PLC is

better than the MARSHAL MOTOR HOLDINGS PLC limited. The financial statement and the

financial figures of the LOOKERS PLC depicts that it is the market leader in the comapny

(Morningstar, 2017). Currently the threat from the existing player to the company is also

higher.

Conclusion:

To conclude, CORE approach (context performance, overview of the comapny, ratio

analysis and evaluation) has been done to evaluate the financial strength of the company.

The context depict that the comapny is internally and externally quite string to manage all the

activities and functions of the company. The overview of the comapny in terms of finance

depict that the performance of this company has became very god than 012 in 2016. These

changes have helped the company to grab more opportunities.

In addition, ratio analysis study has also been performed over the comapny and it

has been found that comapny in enough strong in terms of profitability, capital structure and

solvency position. Further, the financial statement of the comapny has been evaluated to

analyze the changes and the performance of the comapny in terms of the financial figures.

More, the competition analysis has also been done to find out the condition of the comapny

in the market.

Through this report, it could be concluded that the contract with the MARSHAL

MOTOR HOLDING PLC would offer the high return to the comapny. Still, there are few

recommendations which must be followed by the company to manage the operations and

grab the opportunities from the market.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 27

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.