Accounting for Managers: TDABC Implementation at West Farmers Ltd.

VerifiedAdded on 2020/05/16

|11

|2757

|182

Report

AI Summary

This report examines Time-Driven Activity Based Costing (TDABC) and its application, particularly in the context of West Farmers Ltd. It begins by introducing the importance of cost management for businesses of all sizes and provides a depiction of the client firm, West Farmers Ltd. The report then delves into the specifics of TDABC, outlining its key characteristics and how it differs from traditional and Activity-Based Costing (ABC) methods. A detailed comparison between ABC, TDABC, and traditional costing systems is provided. The report assesses the appropriateness of TDABC for West Farmers Ltd., highlighting its benefits in terms of resource allocation, cost prediction, and efficiency. The analysis suggests that TDABC can offer significant advantages over traditional ABC methods, particularly in terms of simplicity and accuracy, and concludes with a summary of the findings and recommendations for implementation.

Running head: ACCOUNTING FOR MANAGERS

Accounting for Managers

Name of the Student

Name of the University

Authors Note

Accounting for Managers

Name of the Student

Name of the University

Authors Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING FOR MANAGERS

Table of Contents

Introduction......................................................................................................................................2

Depiction of the Clients firm...........................................................................................................2

Elaboration of the Time-Driven Activity Based Costing and its essentials....................................3

Differences between ABC, TDABC and Traditional costing system.............................................5

Whether the TDABC is appropriate for the Client company..........................................................7

Conclusion.......................................................................................................................................9

Table of Contents

Introduction......................................................................................................................................2

Depiction of the Clients firm...........................................................................................................2

Elaboration of the Time-Driven Activity Based Costing and its essentials....................................3

Differences between ABC, TDABC and Traditional costing system.............................................5

Whether the TDABC is appropriate for the Client company..........................................................7

Conclusion.......................................................................................................................................9

2ACCOUNTING FOR MANAGERS

Introduction

The size of the firm whether big or small is not the concern in the modern world of

business. What matters is that there should be clear comprehension among the managers

regarding the cost. It is essential to have and maintain a healthy understanding of the various

methods of costing since it will be helpful and better to locate the challenges that take place in

the trade (Hemmer and Labro 2016). This study that into consideration the TDABC and the

understanding of the special characteristics. The report further aims at the ways that will

ascertain the methods under which the TDABC will be different from the ABC model costing

and the Traditional methods of ABC costing. This study will further assess the costing system

that is associated with the implementation of the model in West farmers Ltd.

Depiction of the Clients firm

The West farmers Ltd. is known as one of the leading companies of Australia that is

associated with the construction of materials and in the areas of lime manufacturing. Adelaide

Brighton Ltd. is engaged with the process of manufacturing and supplying wide range of goods

concerned with constructing the infrastructure, processing of building materials throughout the

territories of Australia. The activities of the firm consisted of manufacturing, importation and

delivering cement, concrete, lime goods and premixed concrete. West farmers Ltd. has a wide

base of operational facilities that prompted the supply of materials to the customers. This

company organized a good production capacity in order to meet the demands of the customers

throughout the country (Campbell 2017). It allowed the organization to offer the supply of

packaged materials and the supply of the logistics in all the regions of Australia and Asia.

Introduction

The size of the firm whether big or small is not the concern in the modern world of

business. What matters is that there should be clear comprehension among the managers

regarding the cost. It is essential to have and maintain a healthy understanding of the various

methods of costing since it will be helpful and better to locate the challenges that take place in

the trade (Hemmer and Labro 2016). This study that into consideration the TDABC and the

understanding of the special characteristics. The report further aims at the ways that will

ascertain the methods under which the TDABC will be different from the ABC model costing

and the Traditional methods of ABC costing. This study will further assess the costing system

that is associated with the implementation of the model in West farmers Ltd.

Depiction of the Clients firm

The West farmers Ltd. is known as one of the leading companies of Australia that is

associated with the construction of materials and in the areas of lime manufacturing. Adelaide

Brighton Ltd. is engaged with the process of manufacturing and supplying wide range of goods

concerned with constructing the infrastructure, processing of building materials throughout the

territories of Australia. The activities of the firm consisted of manufacturing, importation and

delivering cement, concrete, lime goods and premixed concrete. West farmers Ltd. has a wide

base of operational facilities that prompted the supply of materials to the customers. This

company organized a good production capacity in order to meet the demands of the customers

throughout the country (Campbell 2017). It allowed the organization to offer the supply of

packaged materials and the supply of the logistics in all the regions of Australia and Asia.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING FOR MANAGERS

Elaboration of the Time-Driven Activity Based Costing and its essentials

The Activity based methodology of costing is presently viewed and treated as a complete

method of costing (Kalpan et al. 2014). Therefore, the model suffers from an amount of criticism

for the approach that is being undertaken with several such of the ABC costing have stopped

using this method. The original procedure of ABC costing provides a greater system of costing.

The variety of products and services under the new model of Time Driven Activity based costing

method will have the capacity to incorporate a large amount of variations and complications by

offering an improved quality of information ignoring the restrictions linked with the scheme of

ABC costing. Modern day customers focus on the business inventions by generating and

providing a wide range of products that will offer their support to the large order and channels of

tracking the orders at various levels of technical support. As stated by Velasquez, Suomala and

Järvenpää, there is an increase in the maximum number of consumers (Mörtl and Schmied 2016).

These consumers need an appropriate management of customer data along with the

administration of the profit generated by them.

The method of ABC costing has attracted the concentration of different costing

methodology among the products that varies from the upper limit, custom and standard products.

TDABC system helped in offering better information regarding the earnings and the frequency

of profits by demonstrating the differences in the cost method among the customers that has

lower demand and ease of service than the ones that has greater demand with the preferences of

complex customer (Armitage, Webb and Glynn 2016).

Based on the time required in performing the activity of the method of TDABC is able to

recognize the sum of every unit or procedure together along with the allocation of cost to the

resource group. It has been noted, that the demand for TDABC can guess the amount of

Elaboration of the Time-Driven Activity Based Costing and its essentials

The Activity based methodology of costing is presently viewed and treated as a complete

method of costing (Kalpan et al. 2014). Therefore, the model suffers from an amount of criticism

for the approach that is being undertaken with several such of the ABC costing have stopped

using this method. The original procedure of ABC costing provides a greater system of costing.

The variety of products and services under the new model of Time Driven Activity based costing

method will have the capacity to incorporate a large amount of variations and complications by

offering an improved quality of information ignoring the restrictions linked with the scheme of

ABC costing. Modern day customers focus on the business inventions by generating and

providing a wide range of products that will offer their support to the large order and channels of

tracking the orders at various levels of technical support. As stated by Velasquez, Suomala and

Järvenpää, there is an increase in the maximum number of consumers (Mörtl and Schmied 2016).

These consumers need an appropriate management of customer data along with the

administration of the profit generated by them.

The method of ABC costing has attracted the concentration of different costing

methodology among the products that varies from the upper limit, custom and standard products.

TDABC system helped in offering better information regarding the earnings and the frequency

of profits by demonstrating the differences in the cost method among the customers that has

lower demand and ease of service than the ones that has greater demand with the preferences of

complex customer (Armitage, Webb and Glynn 2016).

Based on the time required in performing the activity of the method of TDABC is able to

recognize the sum of every unit or procedure together along with the allocation of cost to the

resource group. It has been noted, that the demand for TDABC can guess the amount of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING FOR MANAGERS

resources that have been released (Phan, Baird and Su 2017). TDABC method of costing has

been successful in capturing the various characteristics of activity through the time equation that

usually takes time as per the activity. The TDABC method of costing is therefore observed as the

function of diverse features. Following are the characteristics of the Time Driven Activity Based

Costing:

The initial characteristic of TDABC costing is easily comprehendible and makes the

model accurate.

The model of TDABC assists in offering visibility during the process of utilization

capacity.

Time Driven Activity Based Costing method drives the cost into the operation, orders and

thorough processing of customers, materials and orders (Cooper 2017).

TDABC runs on a monthly basis to trace the economies of the present business functions.

The model of TDABC combines an effective way with the information that is available

from the ERP and the customer relationship management that makes the system of

TDABC vibrant.

The model of TDABC is helpful in guessing the resources of demand. It will enable the

organization in making the budget for resource capacity in respect of the anticipated

ability to order and complication.

Differences between ABC, TDABC and Traditional costing system

In the current situation, the system of TDABC helping in offering variations of the ABC

model due to the ability of easy execution of the purposes that is needed to manufacture goods

and services that are sold in the market. Traditional system of costing assigns the product

resources that have been released (Phan, Baird and Su 2017). TDABC method of costing has

been successful in capturing the various characteristics of activity through the time equation that

usually takes time as per the activity. The TDABC method of costing is therefore observed as the

function of diverse features. Following are the characteristics of the Time Driven Activity Based

Costing:

The initial characteristic of TDABC costing is easily comprehendible and makes the

model accurate.

The model of TDABC assists in offering visibility during the process of utilization

capacity.

Time Driven Activity Based Costing method drives the cost into the operation, orders and

thorough processing of customers, materials and orders (Cooper 2017).

TDABC runs on a monthly basis to trace the economies of the present business functions.

The model of TDABC combines an effective way with the information that is available

from the ERP and the customer relationship management that makes the system of

TDABC vibrant.

The model of TDABC is helpful in guessing the resources of demand. It will enable the

organization in making the budget for resource capacity in respect of the anticipated

ability to order and complication.

Differences between ABC, TDABC and Traditional costing system

In the current situation, the system of TDABC helping in offering variations of the ABC

model due to the ability of easy execution of the purposes that is needed to manufacture goods

and services that are sold in the market. Traditional system of costing assigns the product

5ACCOUNTING FOR MANAGERS

overhead associated with the capacity of the cost driver, mainly the direct labour hours that are

needed to manufacture the product (Otley 2016).

An important element that origins the cost to take place is cost driver. For instance, direct

labour hours, machine hours and direct material hours that are included in manufacturing the

products. In the ABC method of costing, the cost occurred in manufacturing the products are

distributed for the activities that is essential to manufacture the item. On the contrary, the model

of TDABC helped in easy measurement of the efficiency of the products occupied in

manufacturing the product at a given level of capacity against the consumption (Cooper,

Ezzamel and Qu 2017). However, the cost equation helped in providing less costly system than

the traditional method of ABC costing.

The Time Driven Based Costing system is known as economical and reasonable than the

ABC method of costing (Mahal and Hossain 2015). The chief reason for this is that the methods

makes the method of costing easy and diminishes the instances of surveys that are used in the

method of ABC costing. The TDABC allocates the cost directly to the units of cost. The model

of transitional absorption costing helps in dividing the costs generated from the resources by

using the capacity cost to predict the requirement of resources for each unit of cost.

According to the words of Onat, Anitsal and Anitsal, the Time Driven Activity model

based on costing system needs time projections to route the orders of the consumers and it is not

compulsory that the cost should be equal. This is because of the fact that the TDABC projects in

innumerable times varying on the features of application by using the reproduction of variables

and equations. On the other hand, in ABC costing method the amount of cost drivers that were

used in distributing the cost activities is not considered and it is not considered or obligatory to

allocate he cost.

overhead associated with the capacity of the cost driver, mainly the direct labour hours that are

needed to manufacture the product (Otley 2016).

An important element that origins the cost to take place is cost driver. For instance, direct

labour hours, machine hours and direct material hours that are included in manufacturing the

products. In the ABC method of costing, the cost occurred in manufacturing the products are

distributed for the activities that is essential to manufacture the item. On the contrary, the model

of TDABC helped in easy measurement of the efficiency of the products occupied in

manufacturing the product at a given level of capacity against the consumption (Cooper,

Ezzamel and Qu 2017). However, the cost equation helped in providing less costly system than

the traditional method of ABC costing.

The Time Driven Based Costing system is known as economical and reasonable than the

ABC method of costing (Mahal and Hossain 2015). The chief reason for this is that the methods

makes the method of costing easy and diminishes the instances of surveys that are used in the

method of ABC costing. The TDABC allocates the cost directly to the units of cost. The model

of transitional absorption costing helps in dividing the costs generated from the resources by

using the capacity cost to predict the requirement of resources for each unit of cost.

According to the words of Onat, Anitsal and Anitsal, the Time Driven Activity model

based on costing system needs time projections to route the orders of the consumers and it is not

compulsory that the cost should be equal. This is because of the fact that the TDABC projects in

innumerable times varying on the features of application by using the reproduction of variables

and equations. On the other hand, in ABC costing method the amount of cost drivers that were

used in distributing the cost activities is not considered and it is not considered or obligatory to

allocate he cost.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING FOR MANAGERS

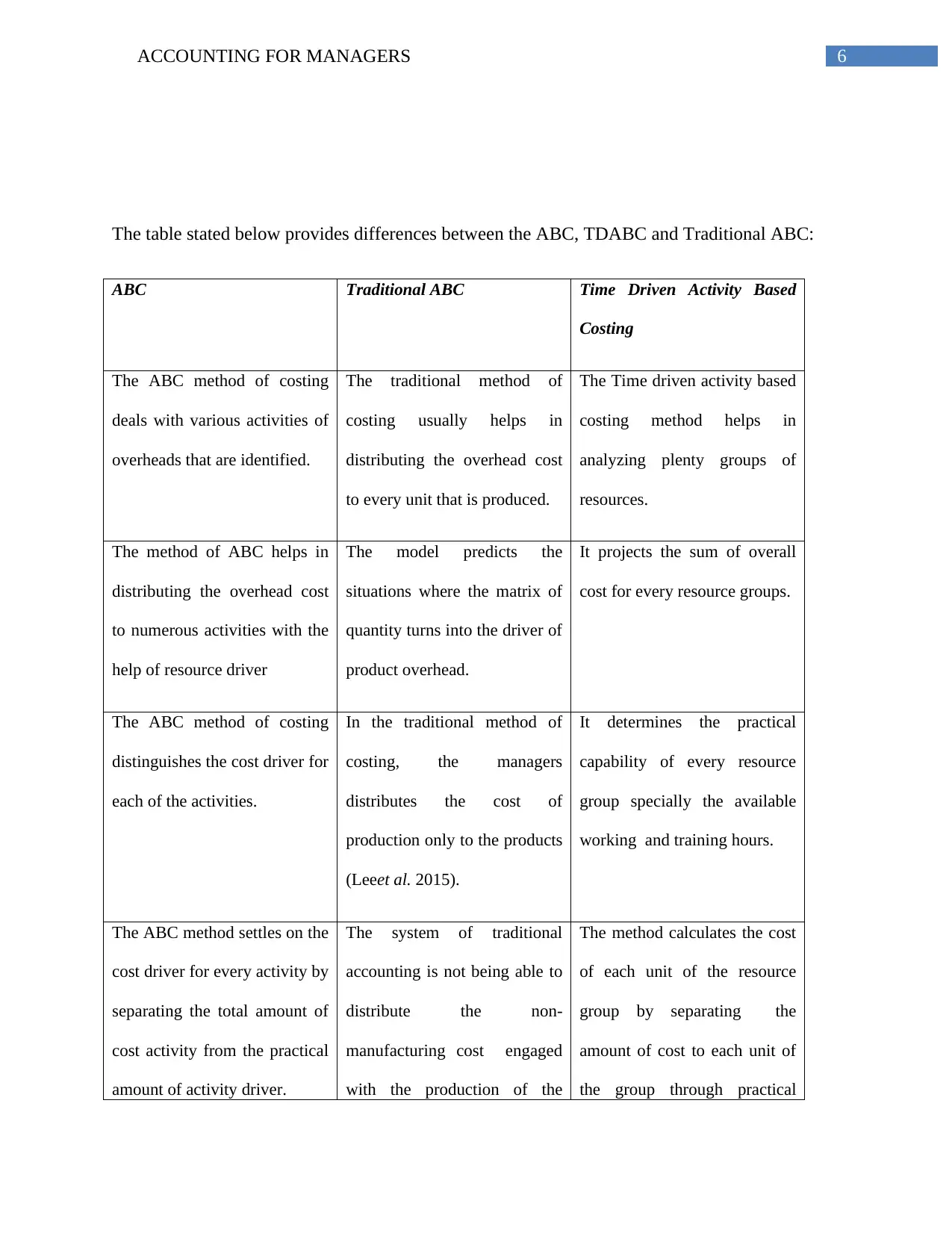

The table stated below provides differences between the ABC, TDABC and Traditional ABC:

ABC Traditional ABC Time Driven Activity Based

Costing

The ABC method of costing

deals with various activities of

overheads that are identified.

The traditional method of

costing usually helps in

distributing the overhead cost

to every unit that is produced.

The Time driven activity based

costing method helps in

analyzing plenty groups of

resources.

The method of ABC helps in

distributing the overhead cost

to numerous activities with the

help of resource driver

The model predicts the

situations where the matrix of

quantity turns into the driver of

product overhead.

It projects the sum of overall

cost for every resource groups.

The ABC method of costing

distinguishes the cost driver for

each of the activities.

In the traditional method of

costing, the managers

distributes the cost of

production only to the products

(Leeet al. 2015).

It determines the practical

capability of every resource

group specially the available

working and training hours.

The ABC method settles on the

cost driver for every activity by

separating the total amount of

cost activity from the practical

amount of activity driver.

The system of traditional

accounting is not being able to

distribute the non-

manufacturing cost engaged

with the production of the

The method calculates the cost

of each unit of the resource

group by separating the

amount of cost to each unit of

the group through practical

The table stated below provides differences between the ABC, TDABC and Traditional ABC:

ABC Traditional ABC Time Driven Activity Based

Costing

The ABC method of costing

deals with various activities of

overheads that are identified.

The traditional method of

costing usually helps in

distributing the overhead cost

to every unit that is produced.

The Time driven activity based

costing method helps in

analyzing plenty groups of

resources.

The method of ABC helps in

distributing the overhead cost

to numerous activities with the

help of resource driver

The model predicts the

situations where the matrix of

quantity turns into the driver of

product overhead.

It projects the sum of overall

cost for every resource groups.

The ABC method of costing

distinguishes the cost driver for

each of the activities.

In the traditional method of

costing, the managers

distributes the cost of

production only to the products

(Leeet al. 2015).

It determines the practical

capability of every resource

group specially the available

working and training hours.

The ABC method settles on the

cost driver for every activity by

separating the total amount of

cost activity from the practical

amount of activity driver.

The system of traditional

accounting is not being able to

distribute the non-

manufacturing cost engaged

with the production of the

The method calculates the cost

of each unit of the resource

group by separating the

amount of cost to each unit of

the group through practical

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING FOR MANAGERS

items particularly the

management expenditure.

capacity.

Whether the TDABC is appropriate for the Client company

When the model of Time Driven Activity Based costing is applied in the client’s firm of

West farmers Ltd. It can be observed that the model is simple and easy to comprehend. Further,

the model is effective and inexpensive compared to other models such as Traditional ABC and

ABC. The Time Driven Activity Based costing helped in making the costing system easy be

diminishing the need of survey and interview of all the employees.

The Traditional method of costing will help West farmer Ltd. in allocating the

cost resources to the activities that are related in driving them to the cost objects. A significant

consideration that can be drawn from the study is that the mechanism of TDABC will help West

farmer Ltd. in allocating the resources directly to the objects of cost by using a smart set of

framework in predicting the profit. The model will help in computing the cost that is required for

the supply of resource capacity (Santana and Afonso 2015). For instance, the department of

processing of the West farmer Ltd. on implementing the model of TDABC will be able to

determine the cost used in technology, supervision and resources.

The TDABC uses the rate of cost capacity in determining the departmental resource cost

in the cost unit by establishing the demand for the resource capacity needed by each cost objects

(Maiga, Nilsson and Jacobs 2014). Keeping in mind the example of customer order sub-division,

the model of Time Driven Activity based costing will be helpful for West farmer Ltd. in

estimating the time required for processing the orders of the customers.

items particularly the

management expenditure.

capacity.

Whether the TDABC is appropriate for the Client company

When the model of Time Driven Activity Based costing is applied in the client’s firm of

West farmers Ltd. It can be observed that the model is simple and easy to comprehend. Further,

the model is effective and inexpensive compared to other models such as Traditional ABC and

ABC. The Time Driven Activity Based costing helped in making the costing system easy be

diminishing the need of survey and interview of all the employees.

The Traditional method of costing will help West farmer Ltd. in allocating the

cost resources to the activities that are related in driving them to the cost objects. A significant

consideration that can be drawn from the study is that the mechanism of TDABC will help West

farmer Ltd. in allocating the resources directly to the objects of cost by using a smart set of

framework in predicting the profit. The model will help in computing the cost that is required for

the supply of resource capacity (Santana and Afonso 2015). For instance, the department of

processing of the West farmer Ltd. on implementing the model of TDABC will be able to

determine the cost used in technology, supervision and resources.

The TDABC uses the rate of cost capacity in determining the departmental resource cost

in the cost unit by establishing the demand for the resource capacity needed by each cost objects

(Maiga, Nilsson and Jacobs 2014). Keeping in mind the example of customer order sub-division,

the model of Time Driven Activity based costing will be helpful for West farmer Ltd. in

estimating the time required for processing the orders of the customers.

8ACCOUNTING FOR MANAGERS

The Time Driven Activity Based Costing support in stimulating the original process that

is used in carrying out the work for West farmer Ltd. The Time Driven Activity Based costing

will be beneficial for West farmer Ltd. in capturing a large number of variations than the

conventional model of ABC without forming any demand for data storage, projections and

processing of materials (Sigüenza Guzmán, Van den Abbeele and Cattrysse 2014). West farmer

Ltd. implemented the TDABC and it will be able to sustain the difficulties instead of using the

imprecise model of ABC for the business activities.

The model of TDABC will help West farmer Ltd. in projecting the cost object with the

ease and in terms for transactions of each unit that is processed in the department. There is proof

of various companies that uses the ERP system for storing the data. These data varies from

packaging and delivering method (Adeleke et al. 2017). In relation with the West farmer Ltd, it

implemented the model of TDABC, which will help the company in storing the complex

business information in an efficient way for transactions that has a fluctuating nature. In the case

of West farmer Ltd. the TDABC helps in improving the complexity of time equation. As a result

of this, the TDABC Model will help West farmer Ltd. in gaining more number of varieties

without forming the exploding demand for estimates of storage, data and processing capabilities.

Conclusion

In the conclusion, it can be stated that this report has been presented by using the

TDABC method based costing. An organization like West farmer Ltd. will be able to grasp the

complexity instead of being forced to use the effortless and accurate model of ABC. The model

will allow the company to avoid the time consuming, costly and subjective activity of the

conventional ABC. The TDABC model at the preliminary stages estimated the historical data.

The Time Driven Activity Based Costing support in stimulating the original process that

is used in carrying out the work for West farmer Ltd. The Time Driven Activity Based costing

will be beneficial for West farmer Ltd. in capturing a large number of variations than the

conventional model of ABC without forming any demand for data storage, projections and

processing of materials (Sigüenza Guzmán, Van den Abbeele and Cattrysse 2014). West farmer

Ltd. implemented the TDABC and it will be able to sustain the difficulties instead of using the

imprecise model of ABC for the business activities.

The model of TDABC will help West farmer Ltd. in projecting the cost object with the

ease and in terms for transactions of each unit that is processed in the department. There is proof

of various companies that uses the ERP system for storing the data. These data varies from

packaging and delivering method (Adeleke et al. 2017). In relation with the West farmer Ltd, it

implemented the model of TDABC, which will help the company in storing the complex

business information in an efficient way for transactions that has a fluctuating nature. In the case

of West farmer Ltd. the TDABC helps in improving the complexity of time equation. As a result

of this, the TDABC Model will help West farmer Ltd. in gaining more number of varieties

without forming the exploding demand for estimates of storage, data and processing capabilities.

Conclusion

In the conclusion, it can be stated that this report has been presented by using the

TDABC method based costing. An organization like West farmer Ltd. will be able to grasp the

complexity instead of being forced to use the effortless and accurate model of ABC. The model

will allow the company to avoid the time consuming, costly and subjective activity of the

conventional ABC. The TDABC model at the preliminary stages estimated the historical data.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING FOR MANAGERS

Subsequently, its fundamental power is to help in predicting the future. Hence, the TDABC will

assist the managers in overcoming the crisis of incorporating the data is ERP and CRM system.

Subsequently, its fundamental power is to help in predicting the future. Hence, the TDABC will

assist the managers in overcoming the crisis of incorporating the data is ERP and CRM system.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING FOR MANAGERS

References

Adeleke, S.O., Healy, G.N., Smith, C., Goode, A.D. and Clark, B.K., 2017. Effect of a

Workplace-Driven Sit–Stand Initiative on Sitting Time and Work Outcomes. Translational

Journal of the American College of Sports Medicine, 2(3), pp.20-26.

Armitage, H.M., Webb, A. and Glynn, J., 2016. The use of management accounting techniques

by small and medium‐sized enterprises: a field study of Canadian and Australian

practice. Accounting Perspectives, 15(1), pp.31-69.

Campbell, J., 2017. Insights from the company monitor: Wesfarmers. Equity, 31(8), p.16.

Kaplan, R.S., Witkowski, M., Abbott, M., Guzman, A.B., Higgins, L.D., Meara, J.G., Padden,

E., Shah, A.S., Waters, P., Weidemeier, M. and Wertheimer, S., 2014. Using time-driven

activity-based costing to identify value improvement opportunities in healthcare. Journal of

Healthcare Management, 59(6), pp.399-412.

Maiga, A.S., Nilsson, A. and Jacobs, F.A., 2014. Assessing the interaction effect of cost control

systems and information technology integration on manufacturing plant financial

performance. The British Accounting Review, 46(1), pp.77-90.

Mörtl, M. and Schmied, C., 2016. Design for Cost—A Review of Methods, Tools and Research

Directions. Journal of the Indian Institute of Science, 95(4), pp.379-404.

Öker, F. and Adıgüzel, H., 2016. Time‐driven activity‐based costing: An implementation in a

manufacturing company. Journal of Corporate Accounting & Finance, 27(3), pp.39-56.

Onat, O.K., Anitsal, I. and Anitsal, M.M., 2014. Activity based costing in services industry: A

conceptual framework for entrepreneurs. The Entrepreneurial Executive, 19, p.149.

References

Adeleke, S.O., Healy, G.N., Smith, C., Goode, A.D. and Clark, B.K., 2017. Effect of a

Workplace-Driven Sit–Stand Initiative on Sitting Time and Work Outcomes. Translational

Journal of the American College of Sports Medicine, 2(3), pp.20-26.

Armitage, H.M., Webb, A. and Glynn, J., 2016. The use of management accounting techniques

by small and medium‐sized enterprises: a field study of Canadian and Australian

practice. Accounting Perspectives, 15(1), pp.31-69.

Campbell, J., 2017. Insights from the company monitor: Wesfarmers. Equity, 31(8), p.16.

Kaplan, R.S., Witkowski, M., Abbott, M., Guzman, A.B., Higgins, L.D., Meara, J.G., Padden,

E., Shah, A.S., Waters, P., Weidemeier, M. and Wertheimer, S., 2014. Using time-driven

activity-based costing to identify value improvement opportunities in healthcare. Journal of

Healthcare Management, 59(6), pp.399-412.

Maiga, A.S., Nilsson, A. and Jacobs, F.A., 2014. Assessing the interaction effect of cost control

systems and information technology integration on manufacturing plant financial

performance. The British Accounting Review, 46(1), pp.77-90.

Mörtl, M. and Schmied, C., 2016. Design for Cost—A Review of Methods, Tools and Research

Directions. Journal of the Indian Institute of Science, 95(4), pp.379-404.

Öker, F. and Adıgüzel, H., 2016. Time‐driven activity‐based costing: An implementation in a

manufacturing company. Journal of Corporate Accounting & Finance, 27(3), pp.39-56.

Onat, O.K., Anitsal, I. and Anitsal, M.M., 2014. Activity based costing in services industry: A

conceptual framework for entrepreneurs. The Entrepreneurial Executive, 19, p.149.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.