Trial Balance, Adjusting & Closing Entries

VerifiedAdded on 2020/05/16

|15

|2888

|50

AI Summary

The assignment explores the concepts of Trial Balance, Adjusting Entries, and Closing Entries in accounting. It delves into the purpose of each entry type, highlighting how they contribute to accurate financial reporting. The document differentiates between adjusting entries, which rectify timing discrepancies and deferred expenses, and closing entries, which reset revenue and expense accounts to zero at the end of an accounting period. Additionally, it emphasizes the significance of Trial Balance as a foundational tool for preparing key financial statements.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: BUSINESS ACCOUNTING

Business accounting

Name of the student

Name of the university

Author note

Business accounting

Name of the student

Name of the university

Author note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1BUSINESS ACCOUNTING

Executive summary

The main objective of this report is to focus on the importance of trial balance and journal

entries for preparation of the balance sheet and income statement. It will present the journal

entries for the adjusted transactions. Further, the report will also present the preparation of

balance sheet, income statement and changes in equity through the adjusted trial balance.

Moreover, the report will focus on the purpose of preparing the trial balance and adjusting

journal entries.

Executive summary

The main objective of this report is to focus on the importance of trial balance and journal

entries for preparation of the balance sheet and income statement. It will present the journal

entries for the adjusted transactions. Further, the report will also present the preparation of

balance sheet, income statement and changes in equity through the adjusted trial balance.

Moreover, the report will focus on the purpose of preparing the trial balance and adjusting

journal entries.

2BUSINESS ACCOUNTING

Table of Contents

Introduction................................................................................................................................3

Step 2 – Journal entries for the adjustment transactions............................................................3

Step 3 – Completion of worksheet.............................................................................................4

Step 4 – Income statement from completed worksheet.............................................................5

Step 5 – Closing entries journals................................................................................................6

Step 6 – Changes in equity.........................................................................................................6

Step 7..........................................................................................................................................8

1) Trial balance and its purpose.......................................................................................8

2) Adjustment journal entries and purpose of recording adjustment journal entries.......9

3) Purpose of preparing the adjusted trial balance.........................................................10

4) Difference between adjusting journal entries and closing journal entries.................11

Conclusion................................................................................................................................12

Reference..................................................................................................................................13

Table of Contents

Introduction................................................................................................................................3

Step 2 – Journal entries for the adjustment transactions............................................................3

Step 3 – Completion of worksheet.............................................................................................4

Step 4 – Income statement from completed worksheet.............................................................5

Step 5 – Closing entries journals................................................................................................6

Step 6 – Changes in equity.........................................................................................................6

Step 7..........................................................................................................................................8

1) Trial balance and its purpose.......................................................................................8

2) Adjustment journal entries and purpose of recording adjustment journal entries.......9

3) Purpose of preparing the adjusted trial balance.........................................................10

4) Difference between adjusting journal entries and closing journal entries.................11

Conclusion................................................................................................................................12

Reference..................................................................................................................................13

3BUSINESS ACCOUNTING

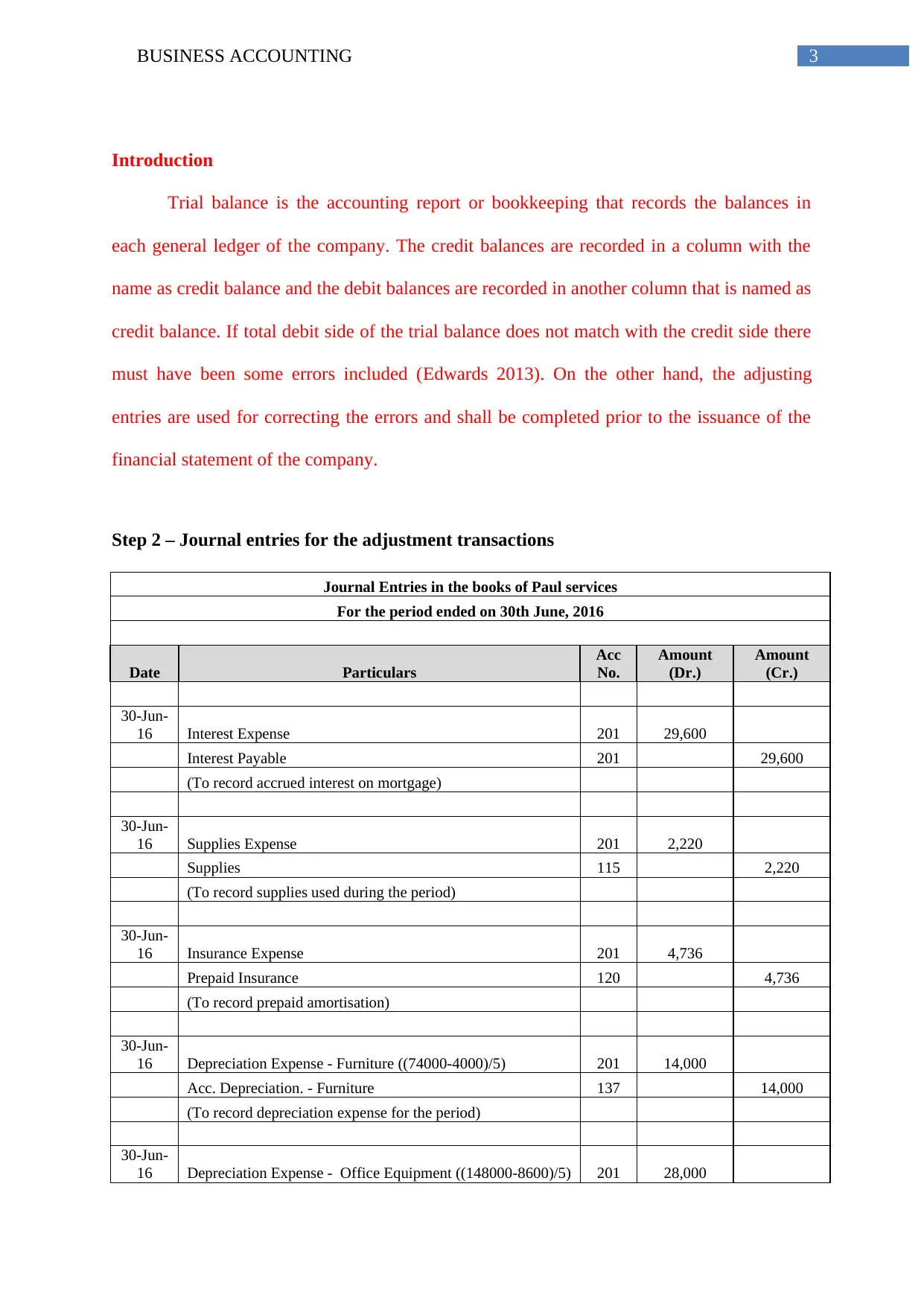

Introduction

Trial balance is the accounting report or bookkeeping that records the balances in

each general ledger of the company. The credit balances are recorded in a column with the

name as credit balance and the debit balances are recorded in another column that is named as

credit balance. If total debit side of the trial balance does not match with the credit side there

must have been some errors included (Edwards 2013). On the other hand, the adjusting

entries are used for correcting the errors and shall be completed prior to the issuance of the

financial statement of the company.

Step 2 – Journal entries for the adjustment transactions

Journal Entries in the books of Paul services

For the period ended on 30th June, 2016

Date Particulars

Acc

No.

Amount

(Dr.)

Amount

(Cr.)

30-Jun-

16 Interest Expense 201 29,600

Interest Payable 201 29,600

(To record accrued interest on mortgage)

30-Jun-

16 Supplies Expense 201 2,220

Supplies 115 2,220

(To record supplies used during the period)

30-Jun-

16 Insurance Expense 201 4,736

Prepaid Insurance 120 4,736

(To record prepaid amortisation)

30-Jun-

16 Depreciation Expense - Furniture ((74000-4000)/5) 201 14,000

Acc. Depreciation. - Furniture 137 14,000

(To record depreciation expense for the period)

30-Jun-

16 Depreciation Expense - Office Equipment ((148000-8600)/5) 201 28,000

Introduction

Trial balance is the accounting report or bookkeeping that records the balances in

each general ledger of the company. The credit balances are recorded in a column with the

name as credit balance and the debit balances are recorded in another column that is named as

credit balance. If total debit side of the trial balance does not match with the credit side there

must have been some errors included (Edwards 2013). On the other hand, the adjusting

entries are used for correcting the errors and shall be completed prior to the issuance of the

financial statement of the company.

Step 2 – Journal entries for the adjustment transactions

Journal Entries in the books of Paul services

For the period ended on 30th June, 2016

Date Particulars

Acc

No.

Amount

(Dr.)

Amount

(Cr.)

30-Jun-

16 Interest Expense 201 29,600

Interest Payable 201 29,600

(To record accrued interest on mortgage)

30-Jun-

16 Supplies Expense 201 2,220

Supplies 115 2,220

(To record supplies used during the period)

30-Jun-

16 Insurance Expense 201 4,736

Prepaid Insurance 120 4,736

(To record prepaid amortisation)

30-Jun-

16 Depreciation Expense - Furniture ((74000-4000)/5) 201 14,000

Acc. Depreciation. - Furniture 137 14,000

(To record depreciation expense for the period)

30-Jun-

16 Depreciation Expense - Office Equipment ((148000-8600)/5) 201 28,000

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4BUSINESS ACCOUNTING

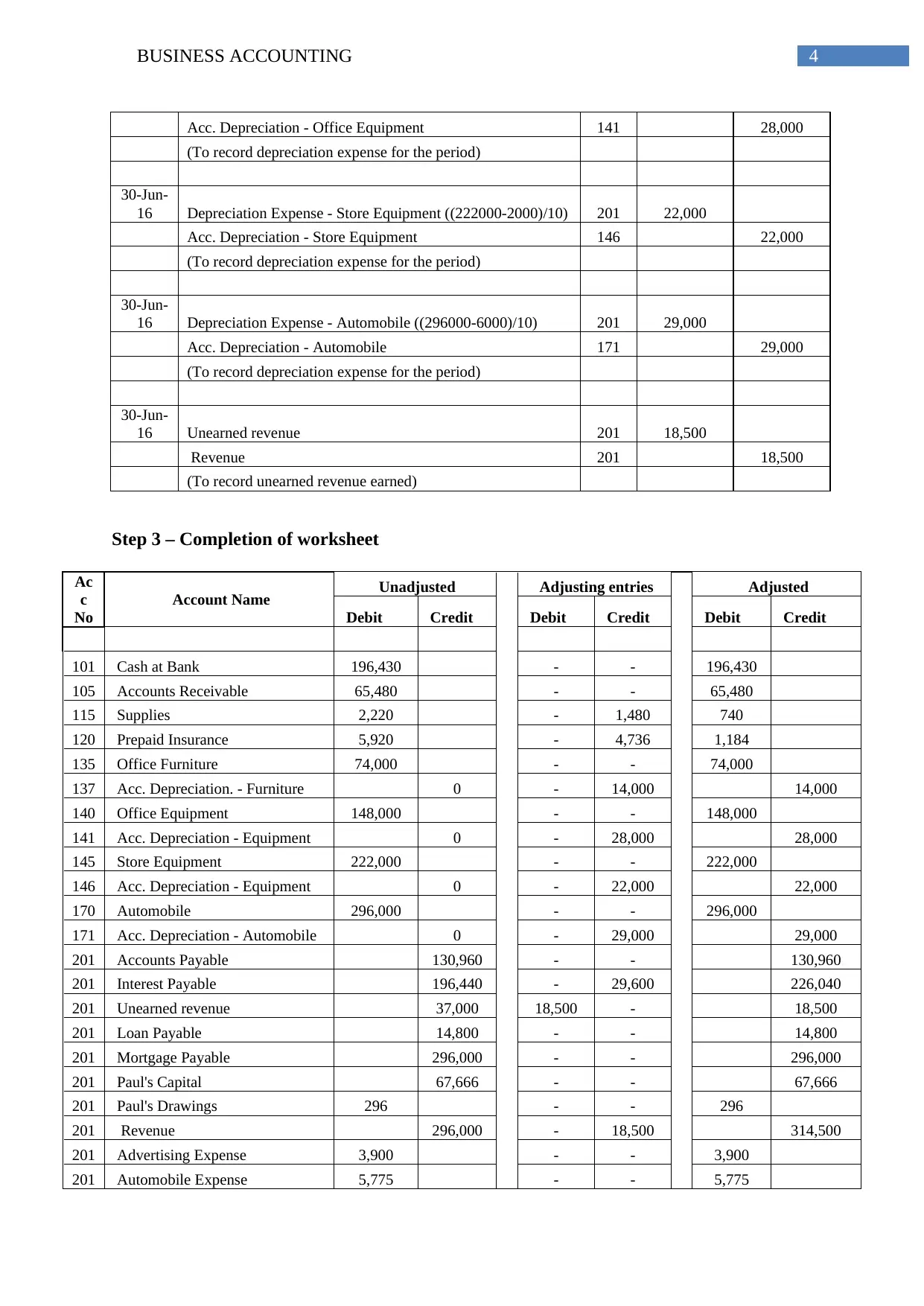

Acc. Depreciation - Office Equipment 141 28,000

(To record depreciation expense for the period)

30-Jun-

16 Depreciation Expense - Store Equipment ((222000-2000)/10) 201 22,000

Acc. Depreciation - Store Equipment 146 22,000

(To record depreciation expense for the period)

30-Jun-

16 Depreciation Expense - Automobile ((296000-6000)/10) 201 29,000

Acc. Depreciation - Automobile 171 29,000

(To record depreciation expense for the period)

30-Jun-

16 Unearned revenue 201 18,500

Revenue 201 18,500

(To record unearned revenue earned)

Step 3 – Completion of worksheet

Ac

c

No

Account Name Unadjusted Adjusting entries Adjusted

Debit Credit Debit Credit Debit Credit

101 Cash at Bank 196,430 - - 196,430

105 Accounts Receivable 65,480 - - 65,480

115 Supplies 2,220 - 1,480 740

120 Prepaid Insurance 5,920 - 4,736 1,184

135 Office Furniture 74,000 - - 74,000

137 Acc. Depreciation. - Furniture 0 - 14,000 14,000

140 Office Equipment 148,000 - - 148,000

141 Acc. Depreciation - Equipment 0 - 28,000 28,000

145 Store Equipment 222,000 - - 222,000

146 Acc. Depreciation - Equipment 0 - 22,000 22,000

170 Automobile 296,000 - - 296,000

171 Acc. Depreciation - Automobile 0 - 29,000 29,000

201 Accounts Payable 130,960 - - 130,960

201 Interest Payable 196,440 - 29,600 226,040

201 Unearned revenue 37,000 18,500 - 18,500

201 Loan Payable 14,800 - - 14,800

201 Mortgage Payable 296,000 - - 296,000

201 Paul's Capital 67,666 - - 67,666

201 Paul's Drawings 296 - - 296

201 Revenue 296,000 - 18,500 314,500

201 Advertising Expense 3,900 - - 3,900

201 Automobile Expense 5,775 - - 5,775

Acc. Depreciation - Office Equipment 141 28,000

(To record depreciation expense for the period)

30-Jun-

16 Depreciation Expense - Store Equipment ((222000-2000)/10) 201 22,000

Acc. Depreciation - Store Equipment 146 22,000

(To record depreciation expense for the period)

30-Jun-

16 Depreciation Expense - Automobile ((296000-6000)/10) 201 29,000

Acc. Depreciation - Automobile 171 29,000

(To record depreciation expense for the period)

30-Jun-

16 Unearned revenue 201 18,500

Revenue 201 18,500

(To record unearned revenue earned)

Step 3 – Completion of worksheet

Ac

c

No

Account Name Unadjusted Adjusting entries Adjusted

Debit Credit Debit Credit Debit Credit

101 Cash at Bank 196,430 - - 196,430

105 Accounts Receivable 65,480 - - 65,480

115 Supplies 2,220 - 1,480 740

120 Prepaid Insurance 5,920 - 4,736 1,184

135 Office Furniture 74,000 - - 74,000

137 Acc. Depreciation. - Furniture 0 - 14,000 14,000

140 Office Equipment 148,000 - - 148,000

141 Acc. Depreciation - Equipment 0 - 28,000 28,000

145 Store Equipment 222,000 - - 222,000

146 Acc. Depreciation - Equipment 0 - 22,000 22,000

170 Automobile 296,000 - - 296,000

171 Acc. Depreciation - Automobile 0 - 29,000 29,000

201 Accounts Payable 130,960 - - 130,960

201 Interest Payable 196,440 - 29,600 226,040

201 Unearned revenue 37,000 18,500 - 18,500

201 Loan Payable 14,800 - - 14,800

201 Mortgage Payable 296,000 - - 296,000

201 Paul's Capital 67,666 - - 67,666

201 Paul's Drawings 296 - - 296

201 Revenue 296,000 - 18,500 314,500

201 Advertising Expense 3,900 - - 3,900

201 Automobile Expense 5,775 - - 5,775

5BUSINESS ACCOUNTING

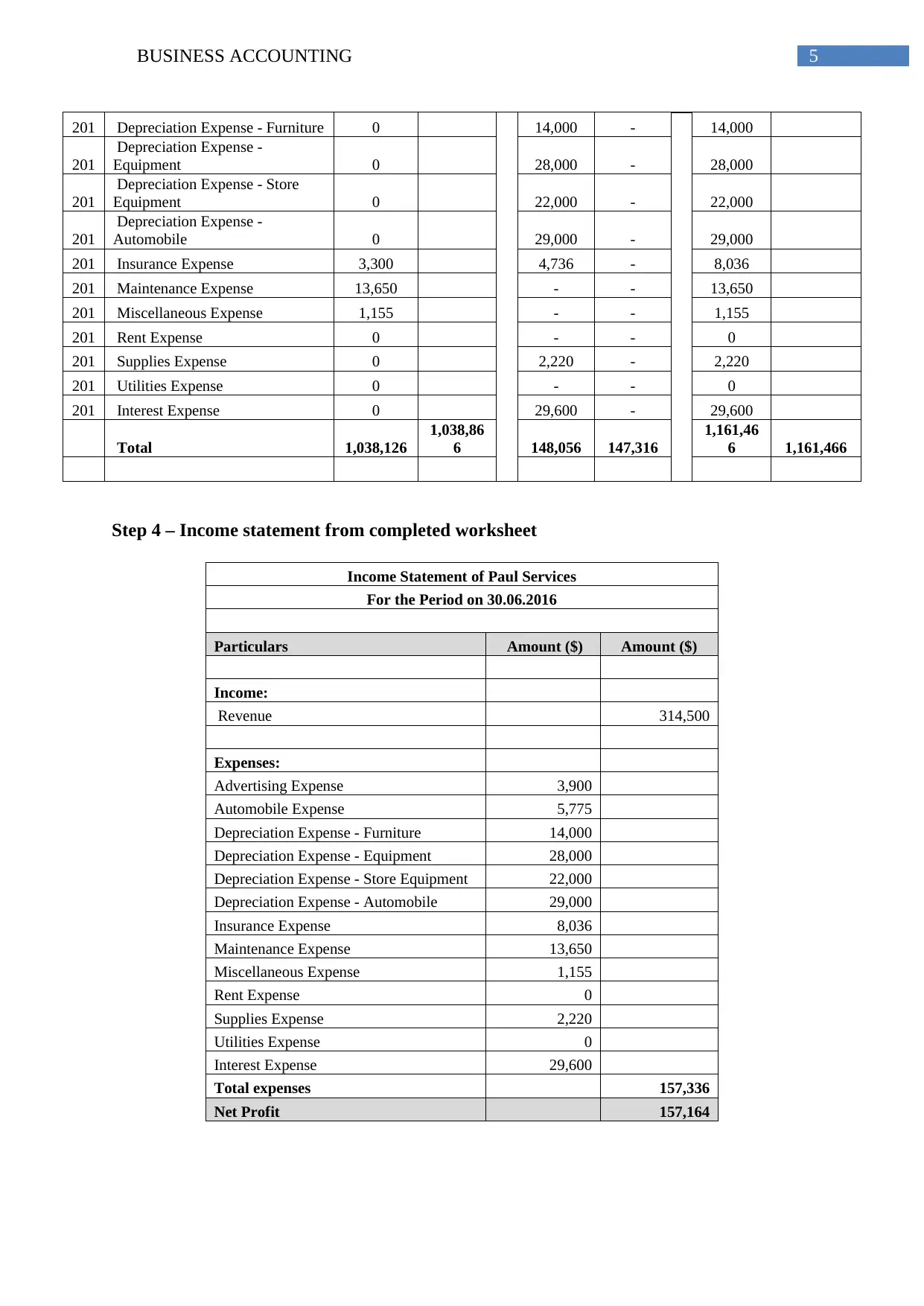

201 Depreciation Expense - Furniture 0 14,000 - 14,000

201

Depreciation Expense -

Equipment 0 28,000 - 28,000

201

Depreciation Expense - Store

Equipment 0 22,000 - 22,000

201

Depreciation Expense -

Automobile 0 29,000 - 29,000

201 Insurance Expense 3,300 4,736 - 8,036

201 Maintenance Expense 13,650 - - 13,650

201 Miscellaneous Expense 1,155 - - 1,155

201 Rent Expense 0 - - 0

201 Supplies Expense 0 2,220 - 2,220

201 Utilities Expense 0 - - 0

201 Interest Expense 0 29,600 - 29,600

Total 1,038,126

1,038,86

6 148,056 147,316

1,161,46

6 1,161,466

Step 4 – Income statement from completed worksheet

Income Statement of Paul Services

For the Period on 30.06.2016

Particulars Amount ($) Amount ($)

Income:

Revenue 314,500

Expenses:

Advertising Expense 3,900

Automobile Expense 5,775

Depreciation Expense - Furniture 14,000

Depreciation Expense - Equipment 28,000

Depreciation Expense - Store Equipment 22,000

Depreciation Expense - Automobile 29,000

Insurance Expense 8,036

Maintenance Expense 13,650

Miscellaneous Expense 1,155

Rent Expense 0

Supplies Expense 2,220

Utilities Expense 0

Interest Expense 29,600

Total expenses 157,336

Net Profit 157,164

201 Depreciation Expense - Furniture 0 14,000 - 14,000

201

Depreciation Expense -

Equipment 0 28,000 - 28,000

201

Depreciation Expense - Store

Equipment 0 22,000 - 22,000

201

Depreciation Expense -

Automobile 0 29,000 - 29,000

201 Insurance Expense 3,300 4,736 - 8,036

201 Maintenance Expense 13,650 - - 13,650

201 Miscellaneous Expense 1,155 - - 1,155

201 Rent Expense 0 - - 0

201 Supplies Expense 0 2,220 - 2,220

201 Utilities Expense 0 - - 0

201 Interest Expense 0 29,600 - 29,600

Total 1,038,126

1,038,86

6 148,056 147,316

1,161,46

6 1,161,466

Step 4 – Income statement from completed worksheet

Income Statement of Paul Services

For the Period on 30.06.2016

Particulars Amount ($) Amount ($)

Income:

Revenue 314,500

Expenses:

Advertising Expense 3,900

Automobile Expense 5,775

Depreciation Expense - Furniture 14,000

Depreciation Expense - Equipment 28,000

Depreciation Expense - Store Equipment 22,000

Depreciation Expense - Automobile 29,000

Insurance Expense 8,036

Maintenance Expense 13,650

Miscellaneous Expense 1,155

Rent Expense 0

Supplies Expense 2,220

Utilities Expense 0

Interest Expense 29,600

Total expenses 157,336

Net Profit 157,164

6BUSINESS ACCOUNTING

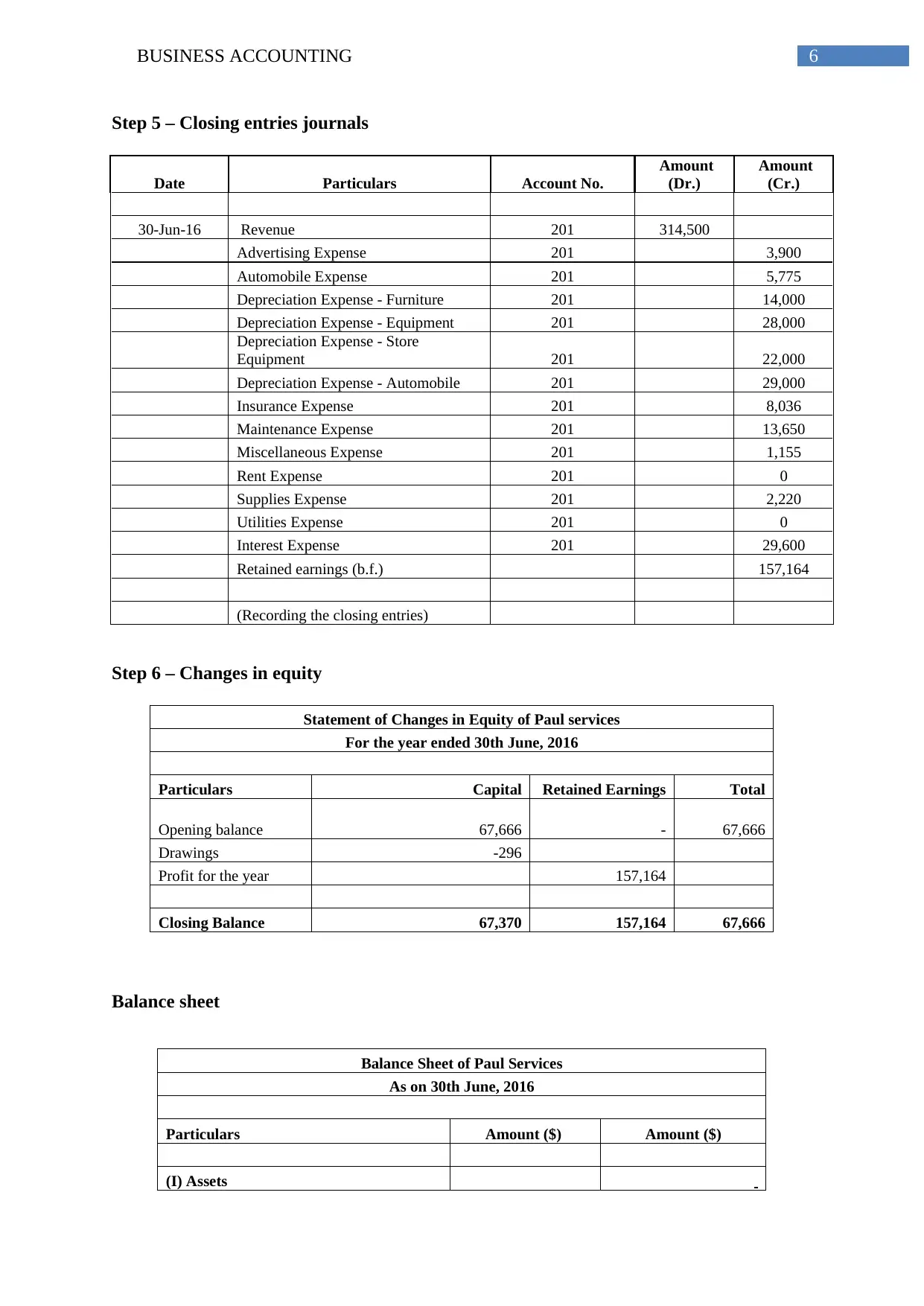

Step 5 – Closing entries journals

Date Particulars Account No.

Amount

(Dr.)

Amount

(Cr.)

30-Jun-16 Revenue 201 314,500

Advertising Expense 201 3,900

Automobile Expense 201 5,775

Depreciation Expense - Furniture 201 14,000

Depreciation Expense - Equipment 201 28,000

Depreciation Expense - Store

Equipment 201 22,000

Depreciation Expense - Automobile 201 29,000

Insurance Expense 201 8,036

Maintenance Expense 201 13,650

Miscellaneous Expense 201 1,155

Rent Expense 201 0

Supplies Expense 201 2,220

Utilities Expense 201 0

Interest Expense 201 29,600

Retained earnings (b.f.) 157,164

(Recording the closing entries)

Step 6 – Changes in equity

Statement of Changes in Equity of Paul services

For the year ended 30th June, 2016

Particulars Capital Retained Earnings Total

Opening balance 67,666 - 67,666

Drawings -296

Profit for the year 157,164

Closing Balance 67,370 157,164 67,666

Balance sheet

Balance Sheet of Paul Services

As on 30th June, 2016

Particulars Amount ($) Amount ($)

(I) Assets

Step 5 – Closing entries journals

Date Particulars Account No.

Amount

(Dr.)

Amount

(Cr.)

30-Jun-16 Revenue 201 314,500

Advertising Expense 201 3,900

Automobile Expense 201 5,775

Depreciation Expense - Furniture 201 14,000

Depreciation Expense - Equipment 201 28,000

Depreciation Expense - Store

Equipment 201 22,000

Depreciation Expense - Automobile 201 29,000

Insurance Expense 201 8,036

Maintenance Expense 201 13,650

Miscellaneous Expense 201 1,155

Rent Expense 201 0

Supplies Expense 201 2,220

Utilities Expense 201 0

Interest Expense 201 29,600

Retained earnings (b.f.) 157,164

(Recording the closing entries)

Step 6 – Changes in equity

Statement of Changes in Equity of Paul services

For the year ended 30th June, 2016

Particulars Capital Retained Earnings Total

Opening balance 67,666 - 67,666

Drawings -296

Profit for the year 157,164

Closing Balance 67,370 157,164 67,666

Balance sheet

Balance Sheet of Paul Services

As on 30th June, 2016

Particulars Amount ($) Amount ($)

(I) Assets

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7BUSINESS ACCOUNTING

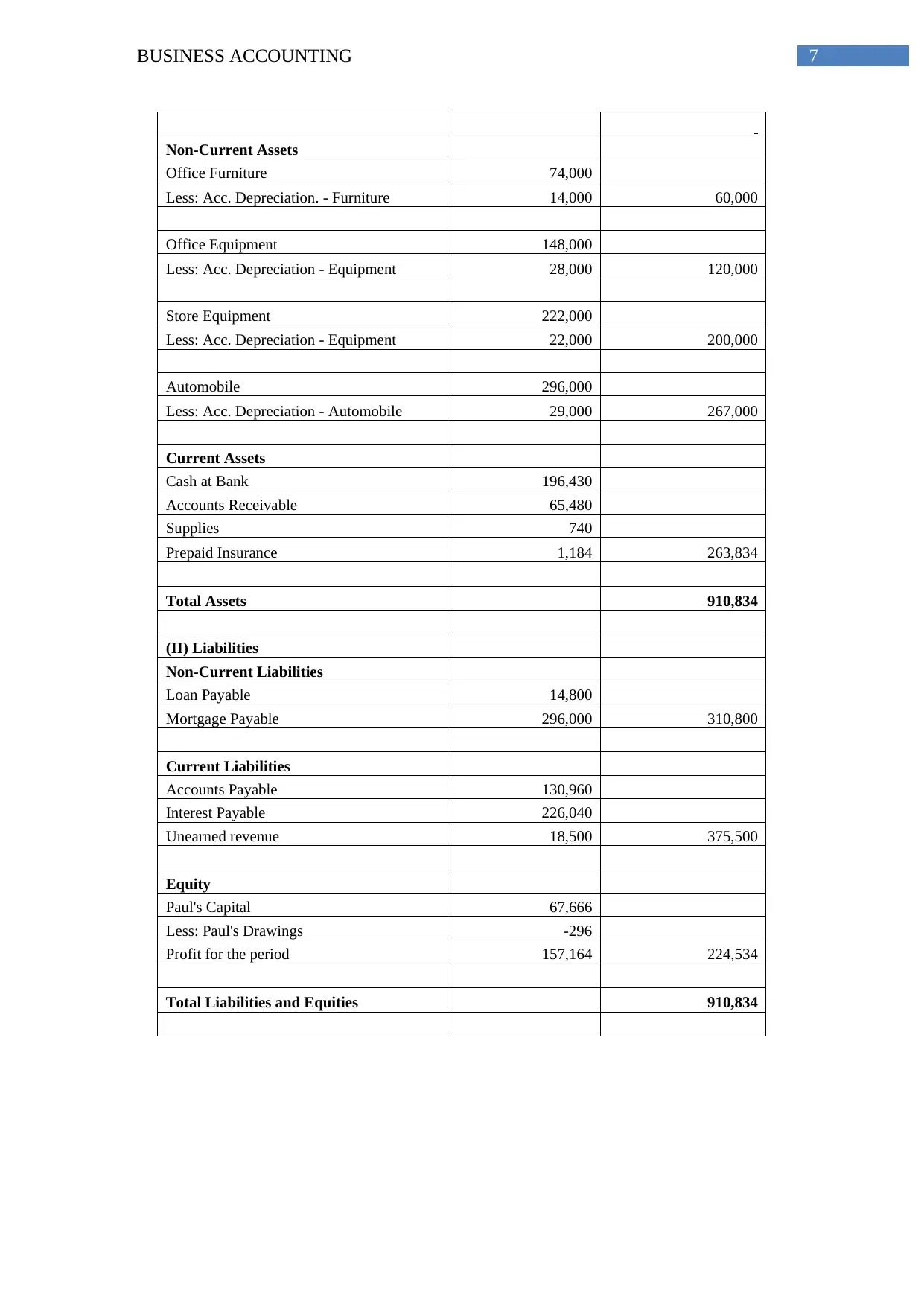

Non-Current Assets

Office Furniture 74,000

Less: Acc. Depreciation. - Furniture 14,000 60,000

Office Equipment 148,000

Less: Acc. Depreciation - Equipment 28,000 120,000

Store Equipment 222,000

Less: Acc. Depreciation - Equipment 22,000 200,000

Automobile 296,000

Less: Acc. Depreciation - Automobile 29,000 267,000

Current Assets

Cash at Bank 196,430

Accounts Receivable 65,480

Supplies 740

Prepaid Insurance 1,184 263,834

Total Assets 910,834

(II) Liabilities

Non-Current Liabilities

Loan Payable 14,800

Mortgage Payable 296,000 310,800

Current Liabilities

Accounts Payable 130,960

Interest Payable 226,040

Unearned revenue 18,500 375,500

Equity

Paul's Capital 67,666

Less: Paul's Drawings -296

Profit for the period 157,164 224,534

Total Liabilities and Equities 910,834

Non-Current Assets

Office Furniture 74,000

Less: Acc. Depreciation. - Furniture 14,000 60,000

Office Equipment 148,000

Less: Acc. Depreciation - Equipment 28,000 120,000

Store Equipment 222,000

Less: Acc. Depreciation - Equipment 22,000 200,000

Automobile 296,000

Less: Acc. Depreciation - Automobile 29,000 267,000

Current Assets

Cash at Bank 196,430

Accounts Receivable 65,480

Supplies 740

Prepaid Insurance 1,184 263,834

Total Assets 910,834

(II) Liabilities

Non-Current Liabilities

Loan Payable 14,800

Mortgage Payable 296,000 310,800

Current Liabilities

Accounts Payable 130,960

Interest Payable 226,040

Unearned revenue 18,500 375,500

Equity

Paul's Capital 67,666

Less: Paul's Drawings -296

Profit for the period 157,164 224,534

Total Liabilities and Equities 910,834

8BUSINESS ACCOUNTING

Step 7

1) Trial balance and its purpose

Trial balance can be defined as the statement of the balances that is extracted from

various accounts of ledger for testing the arithmetical exactness of the account books. The

trial balance has 2 sides – debit side and credit sides. It is the accounting report or

bookkeeping that records the balances in each general ledger of the company (Lee 2014). The

credit balances are recorded in a column with the name as credit balance and the debit

balances are recorded in another column that is named as credit balance. However, the

summation of each of this column shall be same as other. Within the accounting period the

trial balance can be prepared at anytime. However, it is not the part of double entry method of

accounting but is prepared to check the posting accuracy.

Under the manual process the trial balance is generally prepared by the accountant for

discovering whether any error exists there on account of clerical mistake or calculation

mistake (Year 2017). Trial balance is very crucial for the purpose of accounting and auditing.

It is used to reveal the following –

The account balance of the general ledger prior to the adjustments

All the balances after adjustments

Details adjustments

Preparation of trial balance for the company helps to detect the calculation errors that

may have taken place under the double entry system of accounting. If total debit side of the

trial balance does not match with the credit side there must have been some errors included.

The reason may be the transactions have been wrongly classified or material errors related to

Step 7

1) Trial balance and its purpose

Trial balance can be defined as the statement of the balances that is extracted from

various accounts of ledger for testing the arithmetical exactness of the account books. The

trial balance has 2 sides – debit side and credit sides. It is the accounting report or

bookkeeping that records the balances in each general ledger of the company (Lee 2014). The

credit balances are recorded in a column with the name as credit balance and the debit

balances are recorded in another column that is named as credit balance. However, the

summation of each of this column shall be same as other. Within the accounting period the

trial balance can be prepared at anytime. However, it is not the part of double entry method of

accounting but is prepared to check the posting accuracy.

Under the manual process the trial balance is generally prepared by the accountant for

discovering whether any error exists there on account of clerical mistake or calculation

mistake (Year 2017). Trial balance is very crucial for the purpose of accounting and auditing.

It is used to reveal the following –

The account balance of the general ledger prior to the adjustments

All the balances after adjustments

Details adjustments

Preparation of trial balance for the company helps to detect the calculation errors that

may have taken place under the double entry system of accounting. If total debit side of the

trial balance does not match with the credit side there must have been some errors included.

The reason may be the transactions have been wrongly classified or material errors related to

9BUSINESS ACCOUNTING

accounts that may not have been detected in the trial balance procedure. The trial balance

ensures –

That all transactions are recorded with same credit and debit balances

Through identification of errors in books of accounts it assists in correcting the errors

before preparing the final accounts (Wahlen, Baginski and Bradshaw 2014)

It makes preparation of balance sheet, profit and loss account and trading account

easy through making all the accounting balances available at single place.

2) Adjustment journal entries and purpose of recording adjustment journal entries

The adjustment journal entries are the accounting entries that are made under the

journal accounts of the company at the closing of financial period. These entries allocate the

expenses and income to actual period under which the expenses or incomes take place

(Henderson et al. 2015). It follows the principle of revenue recognition in the accrual method

of accounting as against the time of receiving the payment or under the cash method of

accounting. The adjusting journal entries are prepared for allocating –

Unearned revenue from the prepayment receipt to the period under which it is

actually earned.

Prepayment of the expense to period while the expenses are actually incurred

Accrued revenue that is earned but to be received later to period in which it is earned

Accrued expenses that will be paid later to period while the expenses are actually

incurred (Apostolou et al. 2013).

The adjusting entries are further used for correcting the errors and shall be completed

prior to the issuance of the financial statement of the company. Generally it includes the

scenarios when –

accounts that may not have been detected in the trial balance procedure. The trial balance

ensures –

That all transactions are recorded with same credit and debit balances

Through identification of errors in books of accounts it assists in correcting the errors

before preparing the final accounts (Wahlen, Baginski and Bradshaw 2014)

It makes preparation of balance sheet, profit and loss account and trading account

easy through making all the accounting balances available at single place.

2) Adjustment journal entries and purpose of recording adjustment journal entries

The adjustment journal entries are the accounting entries that are made under the

journal accounts of the company at the closing of financial period. These entries allocate the

expenses and income to actual period under which the expenses or incomes take place

(Henderson et al. 2015). It follows the principle of revenue recognition in the accrual method

of accounting as against the time of receiving the payment or under the cash method of

accounting. The adjusting journal entries are prepared for allocating –

Unearned revenue from the prepayment receipt to the period under which it is

actually earned.

Prepayment of the expense to period while the expenses are actually incurred

Accrued revenue that is earned but to be received later to period in which it is earned

Accrued expenses that will be paid later to period while the expenses are actually

incurred (Apostolou et al. 2013).

The adjusting entries are further used for correcting the errors and shall be completed

prior to the issuance of the financial statement of the company. Generally it includes the

scenarios when –

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10BUSINESS ACCOUNTING

When as per the company policy something like fixed asset is booked under the

capital account but it should have been booked under the expenses account like the

supplies expenses

Any entry that is made under the accounting records of the company, however, the

amount is required to move under the period in which the expenses actually incurred

or the revenue is actually earned or segregated among 2 or more than 2 accounting

periods.

No entries are recorded in the accounting records of the company for few revenues

and expenses however, the expenses or the revenues took place in that period and

shall be include in the balance sheet and income statement of that period (Weil,

Schipper and Francis 2013).

3) Purpose of preparing the adjusted trial balance

The extended trial balance or the adjusted trial balance is the working paper that is

used as the basis for the preparation of statement of financial position and income statement

at closing of financial period. It records the same as the name suggests. It is used to bring the

ledger balances together in trial balance form and adding the columns thereafter for recording

the corrections and adjustments. For the adjusting trial balance, the adjustment column,

statement of financial statement and profit and loss column is added. Before preparing the

financial statement the accounting balances shall be verified to ensure that the credit balance

and the debit balances are same (Edmonds et al. 2013). This is done through preparation of

trial balance, listing all the accounts that include revenue, liabilities, equity and expenses.

Thereafter each column is summed up and if 2 columns do not matched there must be some

errors.

In case of accrual accounting method, the revenues are recorded while it is earned and

not when it is paid. In the same way, the expenses are recorded at time when it is incurred

When as per the company policy something like fixed asset is booked under the

capital account but it should have been booked under the expenses account like the

supplies expenses

Any entry that is made under the accounting records of the company, however, the

amount is required to move under the period in which the expenses actually incurred

or the revenue is actually earned or segregated among 2 or more than 2 accounting

periods.

No entries are recorded in the accounting records of the company for few revenues

and expenses however, the expenses or the revenues took place in that period and

shall be include in the balance sheet and income statement of that period (Weil,

Schipper and Francis 2013).

3) Purpose of preparing the adjusted trial balance

The extended trial balance or the adjusted trial balance is the working paper that is

used as the basis for the preparation of statement of financial position and income statement

at closing of financial period. It records the same as the name suggests. It is used to bring the

ledger balances together in trial balance form and adding the columns thereafter for recording

the corrections and adjustments. For the adjusting trial balance, the adjustment column,

statement of financial statement and profit and loss column is added. Before preparing the

financial statement the accounting balances shall be verified to ensure that the credit balance

and the debit balances are same (Edmonds et al. 2013). This is done through preparation of

trial balance, listing all the accounts that include revenue, liabilities, equity and expenses.

Thereafter each column is summed up and if 2 columns do not matched there must be some

errors.

In case of accrual accounting method, the revenues are recorded while it is earned and

not when it is paid. In the same way, the expenses are recorded at time when it is incurred

11BUSINESS ACCOUNTING

and not when it is paid. Therefore, before closing of the accounting period the adjusting

entries are recorded to make the accounts up to date (Needles, Powers and Crosson 2013).

The reason behind preparing the adjusted trial balance is for assuring that adjusting entries

are recorded appropriately. Preparing the adjusted trial balance is the last step before the

preparation of financial statements that is used by the company, its creditors, investors,

shareholders and auditors for measuring the performance of the business. If wrong balances

are entered in the financial statement the statement will be inaccurate.

4) Difference between adjusting journal entries and closing journal entries

Adjusting entries are recorded at the closing of each accounting period and prior to

preparation of the financial statement for recording the accounting transactions and making

the financial statement up to date while the accrual method of accounting is followed

(Edwards 2013). For instance, every day the firm incurs the expenses related to salaries of

employees. However, the salaries under payroll for the last day of the month will not be

recorded till the end of the period. Other entries for adjustment involves amount that are paid

by the company prior to the amount actually turning into expenses. For instance, the company

made the payment towards insurance premiums for 3 months even before the start of these 3

months. Further, the expenses may be deferred through recording of the amount under the

asset account (Warren and Jones 2018).

On the contrary, the closing entries are recorded on the last day of accounting period.

However, they are entered in accounts after preparation of financial statement. For most of

the part the closing entries includes the accounts related to income statement. The closing

entries record the balances from all the expense accounts and revenue accounts to zero

(Weygandt, Kimmel and Kieso 2015). This states that the expenses and revenues will start in

the New Year with no balance which in turn will allow the company to report the expenses

and revenues easily. Further, the net amount from all the balances from expenses and revenue

and not when it is paid. Therefore, before closing of the accounting period the adjusting

entries are recorded to make the accounts up to date (Needles, Powers and Crosson 2013).

The reason behind preparing the adjusted trial balance is for assuring that adjusting entries

are recorded appropriately. Preparing the adjusted trial balance is the last step before the

preparation of financial statements that is used by the company, its creditors, investors,

shareholders and auditors for measuring the performance of the business. If wrong balances

are entered in the financial statement the statement will be inaccurate.

4) Difference between adjusting journal entries and closing journal entries

Adjusting entries are recorded at the closing of each accounting period and prior to

preparation of the financial statement for recording the accounting transactions and making

the financial statement up to date while the accrual method of accounting is followed

(Edwards 2013). For instance, every day the firm incurs the expenses related to salaries of

employees. However, the salaries under payroll for the last day of the month will not be

recorded till the end of the period. Other entries for adjustment involves amount that are paid

by the company prior to the amount actually turning into expenses. For instance, the company

made the payment towards insurance premiums for 3 months even before the start of these 3

months. Further, the expenses may be deferred through recording of the amount under the

asset account (Warren and Jones 2018).

On the contrary, the closing entries are recorded on the last day of accounting period.

However, they are entered in accounts after preparation of financial statement. For most of

the part the closing entries includes the accounts related to income statement. The closing

entries record the balances from all the expense accounts and revenue accounts to zero

(Weygandt, Kimmel and Kieso 2015). This states that the expenses and revenues will start in

the New Year with no balance which in turn will allow the company to report the expenses

and revenues easily. Further, the net amount from all the balances from expenses and revenue

12BUSINESS ACCOUNTING

accounts at the closing of the period will recorded as retained earnings for the companies and

owner’s equity for the sole proprietorship.

Conclusion

From the above, it can be concluded that the Trial balance is very crucial for the

purpose of accounting and auditing. It helps in preparation of balance sheet, profit and loss

account and trading account easy through making all the accounting balances available at

single place. The adjusted trial balance is used to bring the ledger balances together in trial

balance form and adding the columns thereafter for recording the corrections and

adjustments. The main difference of adjusting journal entries with the closing balance is that

the closing entries record the balances from all the expense accounts and revenue accounts to

zero.

accounts at the closing of the period will recorded as retained earnings for the companies and

owner’s equity for the sole proprietorship.

Conclusion

From the above, it can be concluded that the Trial balance is very crucial for the

purpose of accounting and auditing. It helps in preparation of balance sheet, profit and loss

account and trading account easy through making all the accounting balances available at

single place. The adjusted trial balance is used to bring the ledger balances together in trial

balance form and adding the columns thereafter for recording the corrections and

adjustments. The main difference of adjusting journal entries with the closing balance is that

the closing entries record the balances from all the expense accounts and revenue accounts to

zero.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13BUSINESS ACCOUNTING

Reference

Apostolou, B., Dorminey, J.W., Hassell, J.M. and Watson, S.F., 2013. Accounting education

literature review (2010–2012). Journal of Accounting Education, 31(2), pp.107-161.

Edmonds, T.P., McNair, F.M., Olds, P.R. and Milam, E.E., 2013. Fundamental financial

accounting concepts. New York, NY: McGraw-Hill Irwin.

Edwards, J.R., 2013. A history of financial accounting (RLE Accounting) (Vol. 29).

Routledge.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial

accounting. Pearson Higher Education AU.

Lee, T.A., 2014. Evolution of Corporate Financial Reporting (RLE Accounting). Routledge.

Needles, B.E., Powers, M. and Crosson, S.V., 2013. Financial and managerial accounting.

Cengage Learning.

Wahlen, J., Baginski, S. and Bradshaw, M., 2014. Financial reporting, financial statement

analysis and valuation. Nelson Education.

Warren, C.S. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

Weil, R.L., Schipper, K. and Francis, J., 2013. Financial accounting: an introduction to

concepts, methods and uses. Cengage Learning.

Weygandt, J.J., Kimmel, P.D. and Kieso, D.E., 2015. Financial & managerial accounting.

John Wiley & Sons.

Year, B.C.S., 2017. Advanced accounting. Journal Entries in the books of Company, 12,

pp.12-750.

Reference

Apostolou, B., Dorminey, J.W., Hassell, J.M. and Watson, S.F., 2013. Accounting education

literature review (2010–2012). Journal of Accounting Education, 31(2), pp.107-161.

Edmonds, T.P., McNair, F.M., Olds, P.R. and Milam, E.E., 2013. Fundamental financial

accounting concepts. New York, NY: McGraw-Hill Irwin.

Edwards, J.R., 2013. A history of financial accounting (RLE Accounting) (Vol. 29).

Routledge.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial

accounting. Pearson Higher Education AU.

Lee, T.A., 2014. Evolution of Corporate Financial Reporting (RLE Accounting). Routledge.

Needles, B.E., Powers, M. and Crosson, S.V., 2013. Financial and managerial accounting.

Cengage Learning.

Wahlen, J., Baginski, S. and Bradshaw, M., 2014. Financial reporting, financial statement

analysis and valuation. Nelson Education.

Warren, C.S. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

Weil, R.L., Schipper, K. and Francis, J., 2013. Financial accounting: an introduction to

concepts, methods and uses. Cengage Learning.

Weygandt, J.J., Kimmel, P.D. and Kieso, D.E., 2015. Financial & managerial accounting.

John Wiley & Sons.

Year, B.C.S., 2017. Advanced accounting. Journal Entries in the books of Company, 12,

pp.12-750.

14BUSINESS ACCOUNTING

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.