Harvest Kitchen: Research Report on Sales and Profitability Analysis

VerifiedAdded on 2020/03/16

|17

|3075

|35

Report

AI Summary

This research report analyzes the sales performance of Harvest Kitchen, a company dealing in green groceries, addressing challenges such as competition and low sales volume. The study investigates key research questions, including top and worst-performing products, differences in payment methods (visa vs. credit), the impact of product location in the shop on sales, the relationship between sales and gross profits across different months, and the correlation between sales and rainfall. The report utilizes statistical methods like paired sample t-tests and ANOVA to analyze data and identify significant differences. Findings reveal insights into product performance, payment method effectiveness, the influence of product placement, and seasonal sales trends, providing recommendations for improving sales and profitability. The report also includes graphical representations of sales data and detailed statistical tables.

Research report 1

Business report

Student Name:

Student number:

Lecturer:

Business report

Student Name:

Student number:

Lecturer:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Research report 2

Table of contents

Content Page

1.0 Introduction ……………………………………………………….3

2.0 Problem statement…………………………………………………….3

3.0 Research questions……………………………………………………4

3.1 Top and worst performers…………………………………………….4

3.2 Difference in payment methods ……………………… …………….5

3.3 Difference in sales performance …………………………………….6

3.4 Difference in sales and gross profit………………………………….8

3.5 Test for correlation-sales and rain …………………………….…...13

3.6 Test for correlation-sales and gross profit ………………………….13

3.7 Product category…………………………………………………….14

4.0 Discussion and recommendation …………………………………...15

5.0 Reference……………………… …………………………………...16

Table of contents

Content Page

1.0 Introduction ……………………………………………………….3

2.0 Problem statement…………………………………………………….3

3.0 Research questions……………………………………………………4

3.1 Top and worst performers…………………………………………….4

3.2 Difference in payment methods ……………………… …………….5

3.3 Difference in sales performance …………………………………….6

3.4 Difference in sales and gross profit………………………………….8

3.5 Test for correlation-sales and rain …………………………….…...13

3.6 Test for correlation-sales and gross profit ………………………….13

3.7 Product category…………………………………………………….14

4.0 Discussion and recommendation …………………………………...15

5.0 Reference……………………… …………………………………...16

Research report 3

1.0 Introduction

New enterprises in the market face a lot of challenges in the market especially if the industry is

dominated by organizations which have been in the business for long (Kotler , 2012) and

(Romano, 2009). Start up business face various problems from competition to low sales volume

due to unpopular company name or products that they sell. Harvest kitchen, a company that deals

in green groceries has also not been spared. It has been facing challenges from competition from

other established businesses to low sales.

2.0 Problem statement

The main challenge to harvest kitchen organization has been inability to close in on leads hence

leading to low sales across the year. Other factors that contributed to the staggering sales levels

were assumed to be rainfall and location of the produced products in their shops. In order to

increase sales, harvest kitchen has decided to conduct an research survey to understand the

various factors that are perceived to be influencing sales and hence gross profit.

3.0 Research questions

The main research questions for this report are;

What are the top and worst performing products in terms of sales?

Are there differences in payment methods?

Are the differences in sales performance based on where the product is located in the

shop? How does this affect both profits and revenue?

Is there a difference in sales and gross profits between different months of the year?

1.0 Introduction

New enterprises in the market face a lot of challenges in the market especially if the industry is

dominated by organizations which have been in the business for long (Kotler , 2012) and

(Romano, 2009). Start up business face various problems from competition to low sales volume

due to unpopular company name or products that they sell. Harvest kitchen, a company that deals

in green groceries has also not been spared. It has been facing challenges from competition from

other established businesses to low sales.

2.0 Problem statement

The main challenge to harvest kitchen organization has been inability to close in on leads hence

leading to low sales across the year. Other factors that contributed to the staggering sales levels

were assumed to be rainfall and location of the produced products in their shops. In order to

increase sales, harvest kitchen has decided to conduct an research survey to understand the

various factors that are perceived to be influencing sales and hence gross profit.

3.0 Research questions

The main research questions for this report are;

What are the top and worst performing products in terms of sales?

Are there differences in payment methods?

Are the differences in sales performance based on where the product is located in the

shop? How does this affect both profits and revenue?

Is there a difference in sales and gross profits between different months of the year?

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Research report 4

Are their differences in sales performance between different seasons?

How does this relate to rainfall and profits?

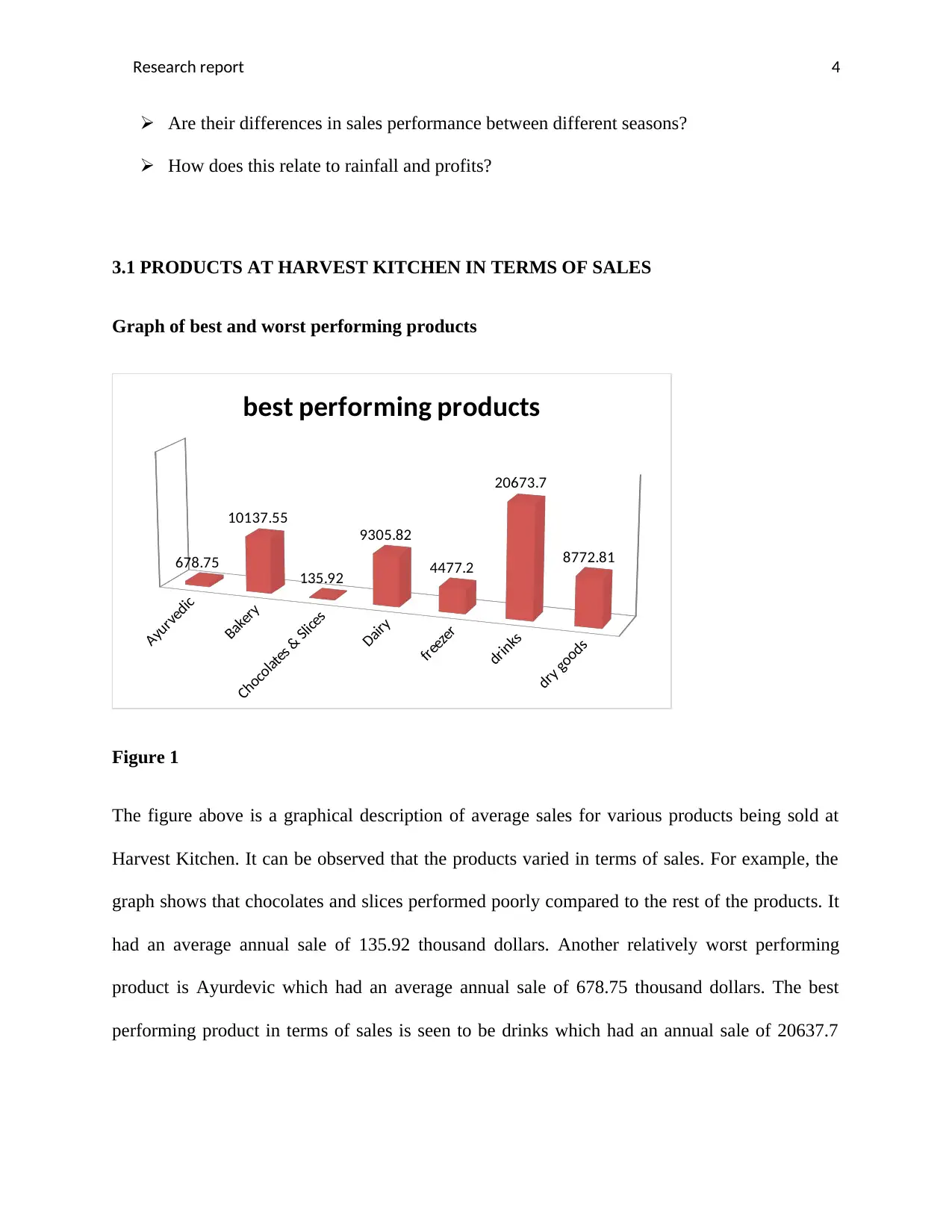

3.1 PRODUCTS AT HARVEST KITCHEN IN TERMS OF SALES

Graph of best and worst performing products

Ayurvedic

Bakery

Chocolates & Slices

Dairy

freezer

drinks

dry goods

678.75

10137.55

135.92

9305.82

4477.2

20673.7

8772.81

best performing products

Figure 1

The figure above is a graphical description of average sales for various products being sold at

Harvest Kitchen. It can be observed that the products varied in terms of sales. For example, the

graph shows that chocolates and slices performed poorly compared to the rest of the products. It

had an average annual sale of 135.92 thousand dollars. Another relatively worst performing

product is Ayurdevic which had an average annual sale of 678.75 thousand dollars. The best

performing product in terms of sales is seen to be drinks which had an annual sale of 20637.7

Are their differences in sales performance between different seasons?

How does this relate to rainfall and profits?

3.1 PRODUCTS AT HARVEST KITCHEN IN TERMS OF SALES

Graph of best and worst performing products

Ayurvedic

Bakery

Chocolates & Slices

Dairy

freezer

drinks

dry goods

678.75

10137.55

135.92

9305.82

4477.2

20673.7

8772.81

best performing products

Figure 1

The figure above is a graphical description of average sales for various products being sold at

Harvest Kitchen. It can be observed that the products varied in terms of sales. For example, the

graph shows that chocolates and slices performed poorly compared to the rest of the products. It

had an average annual sale of 135.92 thousand dollars. Another relatively worst performing

product is Ayurdevic which had an average annual sale of 678.75 thousand dollars. The best

performing product in terms of sales is seen to be drinks which had an annual sale of 20637.7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Research report 5

thousand dollars. Other better performing products were bakery products which had a sale of

10137.55 thousand dollars.

3.2 ESTABLISHING THE EXISTENCE DIFFERENCES IN PAYMENT METHODS

Since Harvest Kitchen is a bigger company serving customers from various regions, they have

diversified their modes of payments such that they accept visa and credits. To establish whether

there was any difference in the two payment methods, a paired sample t-test was run to

determine whether there was any significant difference in the two methods of payment. The

report arrived at the decision of using a paired sample t-test because there were only two main

methods of payments hence only two variables (Robert, 2008) and (Rubin, 2002). This

parametric test was also chosen on the assumption that there is normal distribution in these data

otherwise a non-parametric approach would have been employed.

The hypothesis to be tested is therefore as below;

Hypothesis

At 95% confidence level,

H0: There is no significant difference in the two payment methods

Versus

H1: There is a significant difference in the two payment methods

The paired sample t-test results are as seen in the results table below;

thousand dollars. Other better performing products were bakery products which had a sale of

10137.55 thousand dollars.

3.2 ESTABLISHING THE EXISTENCE DIFFERENCES IN PAYMENT METHODS

Since Harvest Kitchen is a bigger company serving customers from various regions, they have

diversified their modes of payments such that they accept visa and credits. To establish whether

there was any difference in the two payment methods, a paired sample t-test was run to

determine whether there was any significant difference in the two methods of payment. The

report arrived at the decision of using a paired sample t-test because there were only two main

methods of payments hence only two variables (Robert, 2008) and (Rubin, 2002). This

parametric test was also chosen on the assumption that there is normal distribution in these data

otherwise a non-parametric approach would have been employed.

The hypothesis to be tested is therefore as below;

Hypothesis

At 95% confidence level,

H0: There is no significant difference in the two payment methods

Versus

H1: There is a significant difference in the two payment methods

The paired sample t-test results are as seen in the results table below;

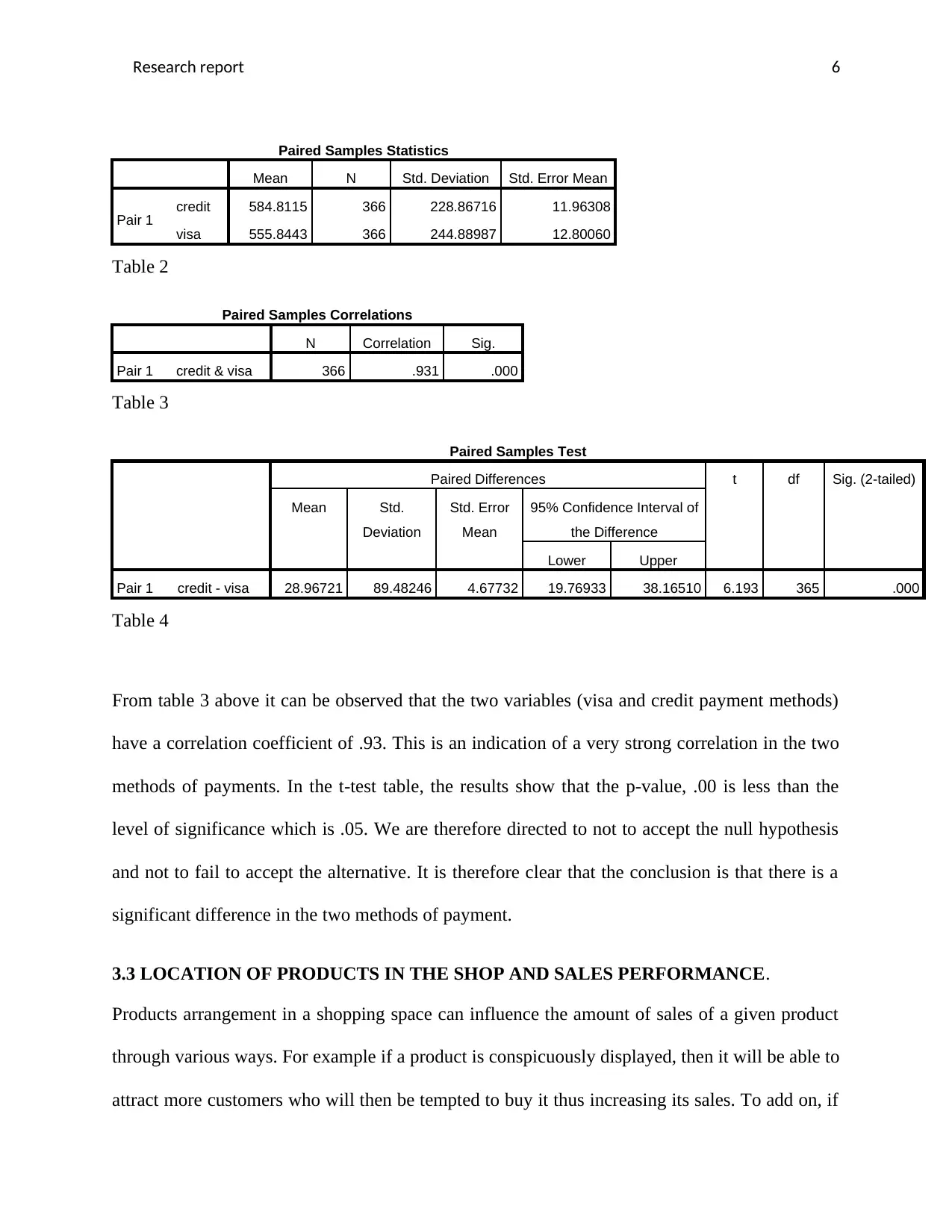

Research report 6

Paired Samples Statistics

Mean N Std. Deviation Std. Error Mean

Pair 1 credit 584.8115 366 228.86716 11.96308

visa 555.8443 366 244.88987 12.80060

Table 2

Paired Samples Correlations

N Correlation Sig.

Pair 1 credit & visa 366 .931 .000

Table 3

Paired Samples Test

Paired Differences t df Sig. (2-tailed)

Mean Std.

Deviation

Std. Error

Mean

95% Confidence Interval of

the Difference

Lower Upper

Pair 1 credit - visa 28.96721 89.48246 4.67732 19.76933 38.16510 6.193 365 .000

Table 4

From table 3 above it can be observed that the two variables (visa and credit payment methods)

have a correlation coefficient of .93. This is an indication of a very strong correlation in the two

methods of payments. In the t-test table, the results show that the p-value, .00 is less than the

level of significance which is .05. We are therefore directed to not to accept the null hypothesis

and not to fail to accept the alternative. It is therefore clear that the conclusion is that there is a

significant difference in the two methods of payment.

3.3 LOCATION OF PRODUCTS IN THE SHOP AND SALES PERFORMANCE.

Products arrangement in a shopping space can influence the amount of sales of a given product

through various ways. For example if a product is conspicuously displayed, then it will be able to

attract more customers who will then be tempted to buy it thus increasing its sales. To add on, if

Paired Samples Statistics

Mean N Std. Deviation Std. Error Mean

Pair 1 credit 584.8115 366 228.86716 11.96308

visa 555.8443 366 244.88987 12.80060

Table 2

Paired Samples Correlations

N Correlation Sig.

Pair 1 credit & visa 366 .931 .000

Table 3

Paired Samples Test

Paired Differences t df Sig. (2-tailed)

Mean Std.

Deviation

Std. Error

Mean

95% Confidence Interval of

the Difference

Lower Upper

Pair 1 credit - visa 28.96721 89.48246 4.67732 19.76933 38.16510 6.193 365 .000

Table 4

From table 3 above it can be observed that the two variables (visa and credit payment methods)

have a correlation coefficient of .93. This is an indication of a very strong correlation in the two

methods of payments. In the t-test table, the results show that the p-value, .00 is less than the

level of significance which is .05. We are therefore directed to not to accept the null hypothesis

and not to fail to accept the alternative. It is therefore clear that the conclusion is that there is a

significant difference in the two methods of payment.

3.3 LOCATION OF PRODUCTS IN THE SHOP AND SALES PERFORMANCE.

Products arrangement in a shopping space can influence the amount of sales of a given product

through various ways. For example if a product is conspicuously displayed, then it will be able to

attract more customers who will then be tempted to buy it thus increasing its sales. To add on, if

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Research report 7

a low moving product is placed next to a fast moving product, there is likelihood that this could

influence the buyer to also consider buying the low moving good out of impulse (Mowlana &

Smith, 2003). In this way, the sales levels of the product whose turnover is low will have been

boosted. The other approach in terms of location that can influence sales of a given product is

whether the product is located near the entrance or in the back end shelves. Products at the

entrance can be spotted very first by the customers thus get stuck into their minds and this can

also prompt impulse buying. Products that are shelved at the back end of a shop can be very

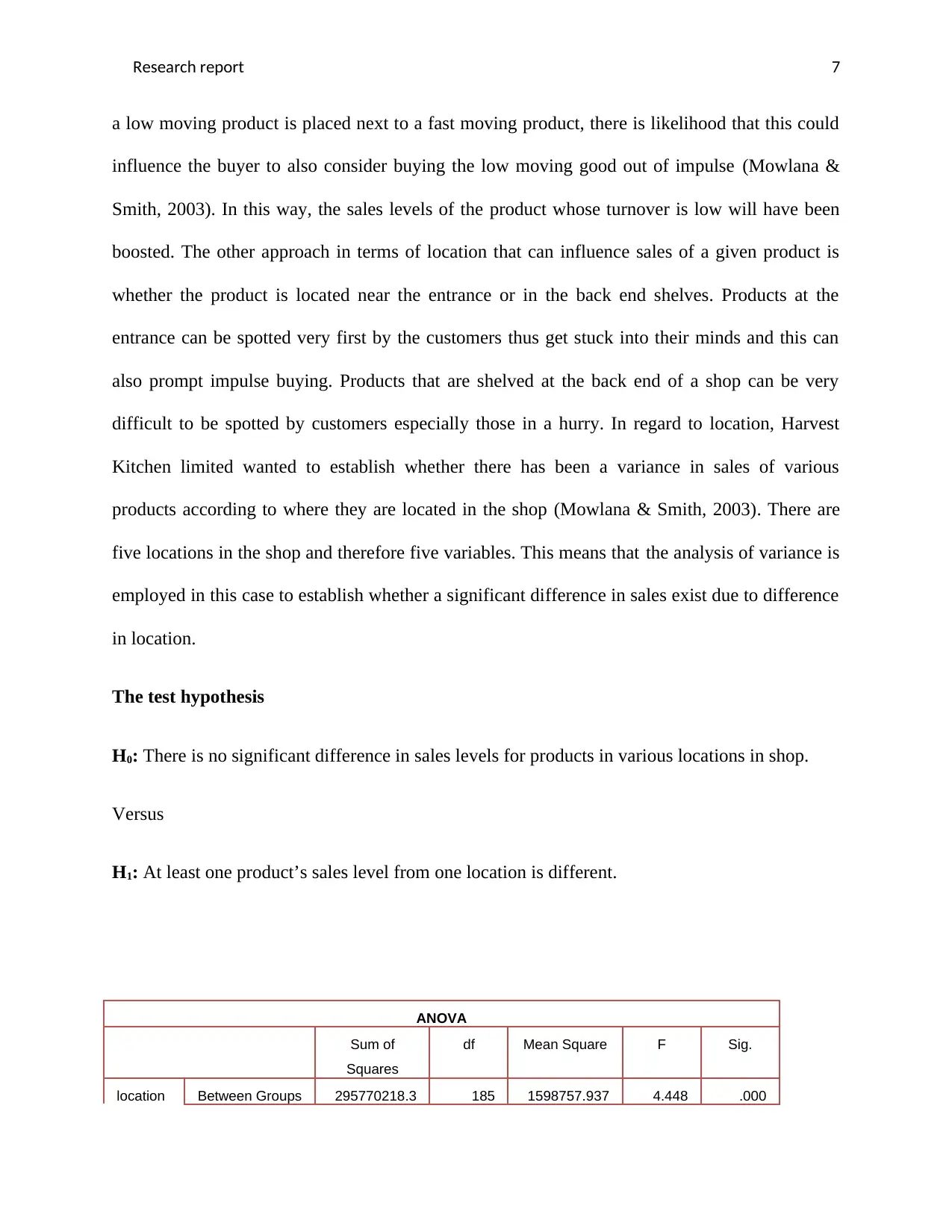

difficult to be spotted by customers especially those in a hurry. In regard to location, Harvest

Kitchen limited wanted to establish whether there has been a variance in sales of various

products according to where they are located in the shop (Mowlana & Smith, 2003). There are

five locations in the shop and therefore five variables. This means that the analysis of variance is

employed in this case to establish whether a significant difference in sales exist due to difference

in location.

The test hypothesis

H0: There is no significant difference in sales levels for products in various locations in shop.

Versus

H1: At least one product’s sales level from one location is different.

ANOVA

Sum of

Squares

df Mean Square F Sig.

location Between Groups 295770218.3 185 1598757.937 4.448 .000

a low moving product is placed next to a fast moving product, there is likelihood that this could

influence the buyer to also consider buying the low moving good out of impulse (Mowlana &

Smith, 2003). In this way, the sales levels of the product whose turnover is low will have been

boosted. The other approach in terms of location that can influence sales of a given product is

whether the product is located near the entrance or in the back end shelves. Products at the

entrance can be spotted very first by the customers thus get stuck into their minds and this can

also prompt impulse buying. Products that are shelved at the back end of a shop can be very

difficult to be spotted by customers especially those in a hurry. In regard to location, Harvest

Kitchen limited wanted to establish whether there has been a variance in sales of various

products according to where they are located in the shop (Mowlana & Smith, 2003). There are

five locations in the shop and therefore five variables. This means that the analysis of variance is

employed in this case to establish whether a significant difference in sales exist due to difference

in location.

The test hypothesis

H0: There is no significant difference in sales levels for products in various locations in shop.

Versus

H1: At least one product’s sales level from one location is different.

ANOVA

Sum of

Squares

df Mean Square F Sig.

location Between Groups 295770218.3 185 1598757.937 4.448 .000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Research report 8

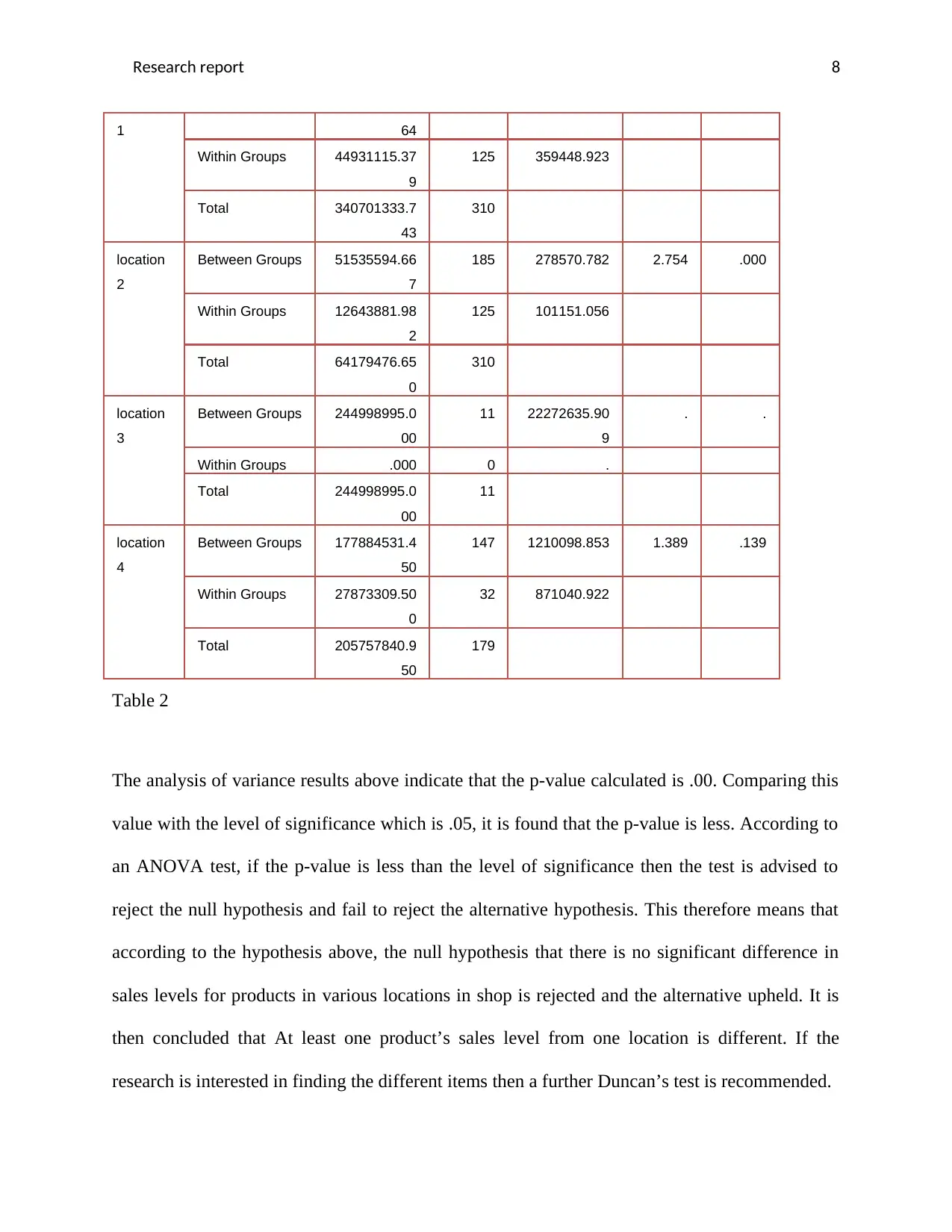

1 64

Within Groups 44931115.37

9

125 359448.923

Total 340701333.7

43

310

location

2

Between Groups 51535594.66

7

185 278570.782 2.754 .000

Within Groups 12643881.98

2

125 101151.056

Total 64179476.65

0

310

location

3

Between Groups 244998995.0

00

11 22272635.90

9

. .

Within Groups .000 0 .

Total 244998995.0

00

11

location

4

Between Groups 177884531.4

50

147 1210098.853 1.389 .139

Within Groups 27873309.50

0

32 871040.922

Total 205757840.9

50

179

Table 2

The analysis of variance results above indicate that the p-value calculated is .00. Comparing this

value with the level of significance which is .05, it is found that the p-value is less. According to

an ANOVA test, if the p-value is less than the level of significance then the test is advised to

reject the null hypothesis and fail to reject the alternative hypothesis. This therefore means that

according to the hypothesis above, the null hypothesis that there is no significant difference in

sales levels for products in various locations in shop is rejected and the alternative upheld. It is

then concluded that At least one product’s sales level from one location is different. If the

research is interested in finding the different items then a further Duncan’s test is recommended.

1 64

Within Groups 44931115.37

9

125 359448.923

Total 340701333.7

43

310

location

2

Between Groups 51535594.66

7

185 278570.782 2.754 .000

Within Groups 12643881.98

2

125 101151.056

Total 64179476.65

0

310

location

3

Between Groups 244998995.0

00

11 22272635.90

9

. .

Within Groups .000 0 .

Total 244998995.0

00

11

location

4

Between Groups 177884531.4

50

147 1210098.853 1.389 .139

Within Groups 27873309.50

0

32 871040.922

Total 205757840.9

50

179

Table 2

The analysis of variance results above indicate that the p-value calculated is .00. Comparing this

value with the level of significance which is .05, it is found that the p-value is less. According to

an ANOVA test, if the p-value is less than the level of significance then the test is advised to

reject the null hypothesis and fail to reject the alternative hypothesis. This therefore means that

according to the hypothesis above, the null hypothesis that there is no significant difference in

sales levels for products in various locations in shop is rejected and the alternative upheld. It is

then concluded that At least one product’s sales level from one location is different. If the

research is interested in finding the different items then a further Duncan’s test is recommended.

Research report 9

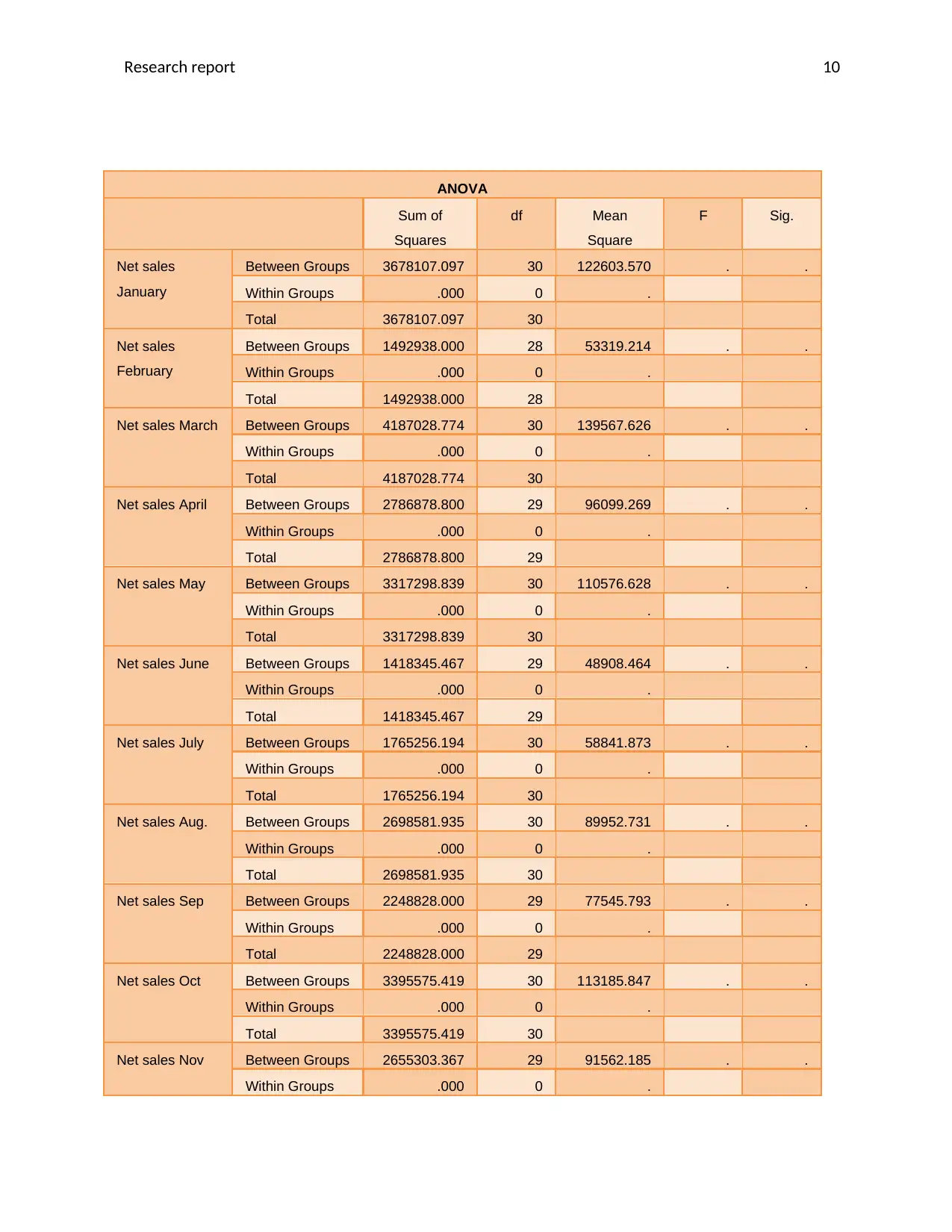

3.4 IS THERE A DIFFERENCE IN SALES AND GROSS PROFITS BETWEEN DIFFERENT MONTHS OF THE

YEAR?

Different seasons affect sales and hence the gross profits that are realized for the same periods. A

certain month may experience an upsurge of sales levels while another month might experience a

decline in sales levels. These variations are normally due to various factors due to weather. A

favorable weather encourages an increase for example in agricultural products and other products

that go with weather such as umbrellas and trench coats during rainy and cold seasons

respectively. On the other hand during dry seasons there is low production of agricultural

products. This may mean that the supply will go low and demand will rise hence raising sales

volume and hence gross profit. The converse also holds true. Harvest kitchen being a company

that deals with agricultural products is bound to experience lows and highs in terms of sales

volume and hence gross profit across the months. It is for this reason that it carried out an

analysis of variance to ascertain whether there were significant differences in gross profit and

sales across the months.

The test hypothesis is as below;

H0: The mean sales level is generally the same across all the months of the year.

Versus

H1: At least one month is different in terms of sales.

The test’s confidence level is 95%

3.4 IS THERE A DIFFERENCE IN SALES AND GROSS PROFITS BETWEEN DIFFERENT MONTHS OF THE

YEAR?

Different seasons affect sales and hence the gross profits that are realized for the same periods. A

certain month may experience an upsurge of sales levels while another month might experience a

decline in sales levels. These variations are normally due to various factors due to weather. A

favorable weather encourages an increase for example in agricultural products and other products

that go with weather such as umbrellas and trench coats during rainy and cold seasons

respectively. On the other hand during dry seasons there is low production of agricultural

products. This may mean that the supply will go low and demand will rise hence raising sales

volume and hence gross profit. The converse also holds true. Harvest kitchen being a company

that deals with agricultural products is bound to experience lows and highs in terms of sales

volume and hence gross profit across the months. It is for this reason that it carried out an

analysis of variance to ascertain whether there were significant differences in gross profit and

sales across the months.

The test hypothesis is as below;

H0: The mean sales level is generally the same across all the months of the year.

Versus

H1: At least one month is different in terms of sales.

The test’s confidence level is 95%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Research report 10

ANOVA

Sum of

Squares

df Mean

Square

F Sig.

Net sales

January

Between Groups 3678107.097 30 122603.570 . .

Within Groups .000 0 .

Total 3678107.097 30

Net sales

February

Between Groups 1492938.000 28 53319.214 . .

Within Groups .000 0 .

Total 1492938.000 28

Net sales March Between Groups 4187028.774 30 139567.626 . .

Within Groups .000 0 .

Total 4187028.774 30

Net sales April Between Groups 2786878.800 29 96099.269 . .

Within Groups .000 0 .

Total 2786878.800 29

Net sales May Between Groups 3317298.839 30 110576.628 . .

Within Groups .000 0 .

Total 3317298.839 30

Net sales June Between Groups 1418345.467 29 48908.464 . .

Within Groups .000 0 .

Total 1418345.467 29

Net sales July Between Groups 1765256.194 30 58841.873 . .

Within Groups .000 0 .

Total 1765256.194 30

Net sales Aug. Between Groups 2698581.935 30 89952.731 . .

Within Groups .000 0 .

Total 2698581.935 30

Net sales Sep Between Groups 2248828.000 29 77545.793 . .

Within Groups .000 0 .

Total 2248828.000 29

Net sales Oct Between Groups 3395575.419 30 113185.847 . .

Within Groups .000 0 .

Total 3395575.419 30

Net sales Nov Between Groups 2655303.367 29 91562.185 . .

Within Groups .000 0 .

ANOVA

Sum of

Squares

df Mean

Square

F Sig.

Net sales

January

Between Groups 3678107.097 30 122603.570 . .

Within Groups .000 0 .

Total 3678107.097 30

Net sales

February

Between Groups 1492938.000 28 53319.214 . .

Within Groups .000 0 .

Total 1492938.000 28

Net sales March Between Groups 4187028.774 30 139567.626 . .

Within Groups .000 0 .

Total 4187028.774 30

Net sales April Between Groups 2786878.800 29 96099.269 . .

Within Groups .000 0 .

Total 2786878.800 29

Net sales May Between Groups 3317298.839 30 110576.628 . .

Within Groups .000 0 .

Total 3317298.839 30

Net sales June Between Groups 1418345.467 29 48908.464 . .

Within Groups .000 0 .

Total 1418345.467 29

Net sales July Between Groups 1765256.194 30 58841.873 . .

Within Groups .000 0 .

Total 1765256.194 30

Net sales Aug. Between Groups 2698581.935 30 89952.731 . .

Within Groups .000 0 .

Total 2698581.935 30

Net sales Sep Between Groups 2248828.000 29 77545.793 . .

Within Groups .000 0 .

Total 2248828.000 29

Net sales Oct Between Groups 3395575.419 30 113185.847 . .

Within Groups .000 0 .

Total 3395575.419 30

Net sales Nov Between Groups 2655303.367 29 91562.185 . .

Within Groups .000 0 .

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Research report 11

Total 2655303.367 29

Table 3

The analysis of variance results above indicate that the p-value calculated is .00. Comparing this

value with the level of significance which is .05, it is found that the p-value is less. According to

an ANOVA test, if the p-value is less than the level of significance then the test is advised to

reject the null hypothesis and fail to reject the alternative hypothesis (Richler, 2012) and (Lucas,

2009). This therefore means that according to the hypothesis above, the null hypothesis that there

is no significant difference in sales levels for products across the 12 months of the year is

rejected and the alternative upheld. It is then concluded that At least one month’s product’s sales

level is different. If the research is interested in finding the different items then a further

Duncan’s test is recommended.

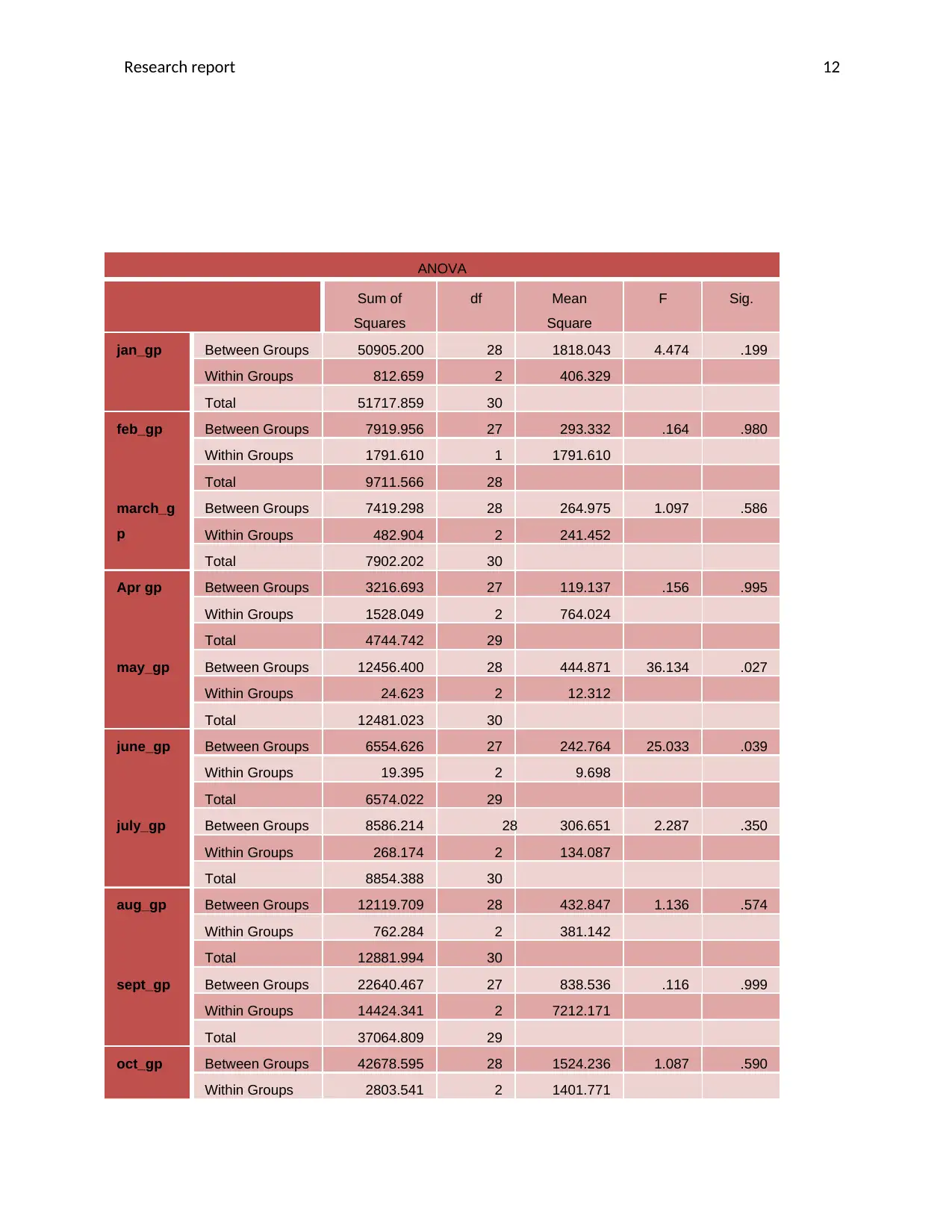

TEST FOR GROSS PROFIT DIFFERENCE BETWEEN THE MONTHS

Hypothesis

H0: The gross profit is almost the same across the 12 months of the year.

Versus

H1: At least one month is different in terms of gross profit.

In this hypothesis, 95% confidence level has been applied.

The ANOVA results are tabulated as below,

Total 2655303.367 29

Table 3

The analysis of variance results above indicate that the p-value calculated is .00. Comparing this

value with the level of significance which is .05, it is found that the p-value is less. According to

an ANOVA test, if the p-value is less than the level of significance then the test is advised to

reject the null hypothesis and fail to reject the alternative hypothesis (Richler, 2012) and (Lucas,

2009). This therefore means that according to the hypothesis above, the null hypothesis that there

is no significant difference in sales levels for products across the 12 months of the year is

rejected and the alternative upheld. It is then concluded that At least one month’s product’s sales

level is different. If the research is interested in finding the different items then a further

Duncan’s test is recommended.

TEST FOR GROSS PROFIT DIFFERENCE BETWEEN THE MONTHS

Hypothesis

H0: The gross profit is almost the same across the 12 months of the year.

Versus

H1: At least one month is different in terms of gross profit.

In this hypothesis, 95% confidence level has been applied.

The ANOVA results are tabulated as below,

Research report 12

ANOVA

Sum of

Squares

df Mean

Square

F Sig.

jan_gp Between Groups 50905.200 28 1818.043 4.474 .199

Within Groups 812.659 2 406.329

Total 51717.859 30

feb_gp Between Groups 7919.956 27 293.332 .164 .980

Within Groups 1791.610 1 1791.610

Total 9711.566 28

march_g

p

Between Groups 7419.298 28 264.975 1.097 .586

Within Groups 482.904 2 241.452

Total 7902.202 30

Apr gp Between Groups 3216.693 27 119.137 .156 .995

Within Groups 1528.049 2 764.024

Total 4744.742 29

may_gp Between Groups 12456.400 28 444.871 36.134 .027

Within Groups 24.623 2 12.312

Total 12481.023 30

june_gp Between Groups 6554.626 27 242.764 25.033 .039

Within Groups 19.395 2 9.698

Total 6574.022 29

july_gp Between Groups 8586.214 28 306.651 2.287 .350

Within Groups 268.174 2 134.087

Total 8854.388 30

aug_gp Between Groups 12119.709 28 432.847 1.136 .574

Within Groups 762.284 2 381.142

Total 12881.994 30

sept_gp Between Groups 22640.467 27 838.536 .116 .999

Within Groups 14424.341 2 7212.171

Total 37064.809 29

oct_gp Between Groups 42678.595 28 1524.236 1.087 .590

Within Groups 2803.541 2 1401.771

ANOVA

Sum of

Squares

df Mean

Square

F Sig.

jan_gp Between Groups 50905.200 28 1818.043 4.474 .199

Within Groups 812.659 2 406.329

Total 51717.859 30

feb_gp Between Groups 7919.956 27 293.332 .164 .980

Within Groups 1791.610 1 1791.610

Total 9711.566 28

march_g

p

Between Groups 7419.298 28 264.975 1.097 .586

Within Groups 482.904 2 241.452

Total 7902.202 30

Apr gp Between Groups 3216.693 27 119.137 .156 .995

Within Groups 1528.049 2 764.024

Total 4744.742 29

may_gp Between Groups 12456.400 28 444.871 36.134 .027

Within Groups 24.623 2 12.312

Total 12481.023 30

june_gp Between Groups 6554.626 27 242.764 25.033 .039

Within Groups 19.395 2 9.698

Total 6574.022 29

july_gp Between Groups 8586.214 28 306.651 2.287 .350

Within Groups 268.174 2 134.087

Total 8854.388 30

aug_gp Between Groups 12119.709 28 432.847 1.136 .574

Within Groups 762.284 2 381.142

Total 12881.994 30

sept_gp Between Groups 22640.467 27 838.536 .116 .999

Within Groups 14424.341 2 7212.171

Total 37064.809 29

oct_gp Between Groups 42678.595 28 1524.236 1.087 .590

Within Groups 2803.541 2 1401.771

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17