Management Accounting Report: Cost, Budget, and Performance Analysis

VerifiedAdded on 2020/02/05

|21

|6890

|46

Report

AI Summary

This report on management accounting provides a comprehensive overview of cost classification, job costing, and absorption costing techniques. It delves into the calculation of job and unit costs, followed by an analysis of overhead absorption rates using direct labor hours. The report also includes a detailed cost sheet preparation and variance analysis, highlighting performance indicators for potential improvements and strategies for cost reduction. Furthermore, it covers the budgeting process, including material purchase, production, and cash budgets, along with variance analysis and the identification of responsibility centers. The report concludes with recommendations for corrective actions based on the variance analysis and provides a detailed analysis of the performance of the company.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

1.1 Classification of cost on the basis of various factors............................................................3

1.2 Calculation of job cost and unit cost.....................................................................................4

1.3 Calculation of the cost by using absorption costing technique.............................................4

1.4 Calculation of overhead absorption rate using direct labor hours.........................................6

TASK 2............................................................................................................................................7

2.1 Preparation of cost sheet and variance analysis...................................................................7

2.2 Various performance indicators used to identify the areas of potential improvements.......8

2.3 Ways to reduce cost, enhance value and quality..................................................................9

TASK 3 .........................................................................................................................................10

3.1 Nature and purpose of budgeting process...........................................................................10

3.2 Appropriate budgeting method for the organization and its need.......................................11

3.3 Material purchase budget and production requirement budget...........................................12

3.4 preparation of cash budget.................................................................................................13

TASK 4..........................................................................................................................................14

4.1, 4.2 Variance analysis and recommendation corrective actions.........................................14

4.3 Identifications of responsibility centers.............................................................................15

CONCLCUSION...........................................................................................................................15

REFERENCES..............................................................................................................................16

INDEX OF TABLES

Table 1: Calculation of total cost and per unit cost for a job...........................................................5

Table 2: Calculation of overhead absorption rate using direct labor hours.....................................7

Table 3: Preparation of budgeted and actual cost (In £)..................................................................8

Table 4: Variance analysis...............................................................................................................8

Table 5: Production budget for July, August and September (In Units).......................................13

Table 6: Material purchase budget (In Kg)....................................................................................14

Table 7: preparation of Cash budget..............................................................................................14

Table 8: Calculation of budgeted cost for 4000 units....................................................................15

Table 9: operating statement reconciling both budgeted and actual results..................................15

Table 10: Calculation of per unit variances...................................................................................15

INTRODUCTION...........................................................................................................................3

1.1 Classification of cost on the basis of various factors............................................................3

1.2 Calculation of job cost and unit cost.....................................................................................4

1.3 Calculation of the cost by using absorption costing technique.............................................4

1.4 Calculation of overhead absorption rate using direct labor hours.........................................6

TASK 2............................................................................................................................................7

2.1 Preparation of cost sheet and variance analysis...................................................................7

2.2 Various performance indicators used to identify the areas of potential improvements.......8

2.3 Ways to reduce cost, enhance value and quality..................................................................9

TASK 3 .........................................................................................................................................10

3.1 Nature and purpose of budgeting process...........................................................................10

3.2 Appropriate budgeting method for the organization and its need.......................................11

3.3 Material purchase budget and production requirement budget...........................................12

3.4 preparation of cash budget.................................................................................................13

TASK 4..........................................................................................................................................14

4.1, 4.2 Variance analysis and recommendation corrective actions.........................................14

4.3 Identifications of responsibility centers.............................................................................15

CONCLCUSION...........................................................................................................................15

REFERENCES..............................................................................................................................16

INDEX OF TABLES

Table 1: Calculation of total cost and per unit cost for a job...........................................................5

Table 2: Calculation of overhead absorption rate using direct labor hours.....................................7

Table 3: Preparation of budgeted and actual cost (In £)..................................................................8

Table 4: Variance analysis...............................................................................................................8

Table 5: Production budget for July, August and September (In Units).......................................13

Table 6: Material purchase budget (In Kg)....................................................................................14

Table 7: preparation of Cash budget..............................................................................................14

Table 8: Calculation of budgeted cost for 4000 units....................................................................15

Table 9: operating statement reconciling both budgeted and actual results..................................15

Table 10: Calculation of per unit variances...................................................................................15

INTRODUCTION

In the competitive business environment most of the firms are competing with each other

on the basis of price of the product. Due to this reason it become necessary for the firms to

reduce their cost of production and to keep control on the expenses that are incurred for

producing goods and services. In this report, classification of cost is done and the same is

explained in detail. Further, various performance indicators are explained in detail in the report.

Apart from this, steps that firms can take in order to reduce their cost of production is also

explained in the report. After that budget process and its main purpose is explained in detail. In

the report, cash, material and production budget are prepared and necessary comments regarding

same are made. At the end of the report, responsibility center is explained and managers are held

responsible for the mistakes they committed in compliance with the budget.

TASK 1

1.1 Classification of cost on the basis of various factors

Cost indicates the aggregate value that is incurred to produce the goods and while making

services available at the workplace. There are many types of costs and these are classified on the

basis of various parameters. Classification of costs is given as below:

Elements of cost- Costs are divided into three categories namely material, labor and

overhead cost. Labor cost refers to the wages that are paid to the labors for producing goods in

the manufacturing facility. On the other hand, material cost refers to the cost of purchase of raw

material that is used for the production of goods (Kaplan and Atkinson, 2015). At last, overhead

expenses come in which all expenses related to the production are included. All these costs are

added in order to compute the final cost of production.

Function – On the basis of functions, cost related to various departments is considered

by the firm. There are various departments like HR, marketing and finance, etc. Various

administrative expenses are incurred in these departments. By adding these expenses, final cost

of various departments are computed in the organization.

Nature- On the basis of nature, costs are classified into two categories like direct and

indirect costs. Direct cost is a cost that is incurred in the production process. On the contrary,

indirect cost refers to the cost that is incurred to support the entire production process (Zadek,

Evans and Pruzan, 2013). Cost incurred to purchase raw material is the example of direct cost.

In the competitive business environment most of the firms are competing with each other

on the basis of price of the product. Due to this reason it become necessary for the firms to

reduce their cost of production and to keep control on the expenses that are incurred for

producing goods and services. In this report, classification of cost is done and the same is

explained in detail. Further, various performance indicators are explained in detail in the report.

Apart from this, steps that firms can take in order to reduce their cost of production is also

explained in the report. After that budget process and its main purpose is explained in detail. In

the report, cash, material and production budget are prepared and necessary comments regarding

same are made. At the end of the report, responsibility center is explained and managers are held

responsible for the mistakes they committed in compliance with the budget.

TASK 1

1.1 Classification of cost on the basis of various factors

Cost indicates the aggregate value that is incurred to produce the goods and while making

services available at the workplace. There are many types of costs and these are classified on the

basis of various parameters. Classification of costs is given as below:

Elements of cost- Costs are divided into three categories namely material, labor and

overhead cost. Labor cost refers to the wages that are paid to the labors for producing goods in

the manufacturing facility. On the other hand, material cost refers to the cost of purchase of raw

material that is used for the production of goods (Kaplan and Atkinson, 2015). At last, overhead

expenses come in which all expenses related to the production are included. All these costs are

added in order to compute the final cost of production.

Function – On the basis of functions, cost related to various departments is considered

by the firm. There are various departments like HR, marketing and finance, etc. Various

administrative expenses are incurred in these departments. By adding these expenses, final cost

of various departments are computed in the organization.

Nature- On the basis of nature, costs are classified into two categories like direct and

indirect costs. Direct cost is a cost that is incurred in the production process. On the contrary,

indirect cost refers to the cost that is incurred to support the entire production process (Zadek,

Evans and Pruzan, 2013). Cost incurred to purchase raw material is the example of direct cost.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

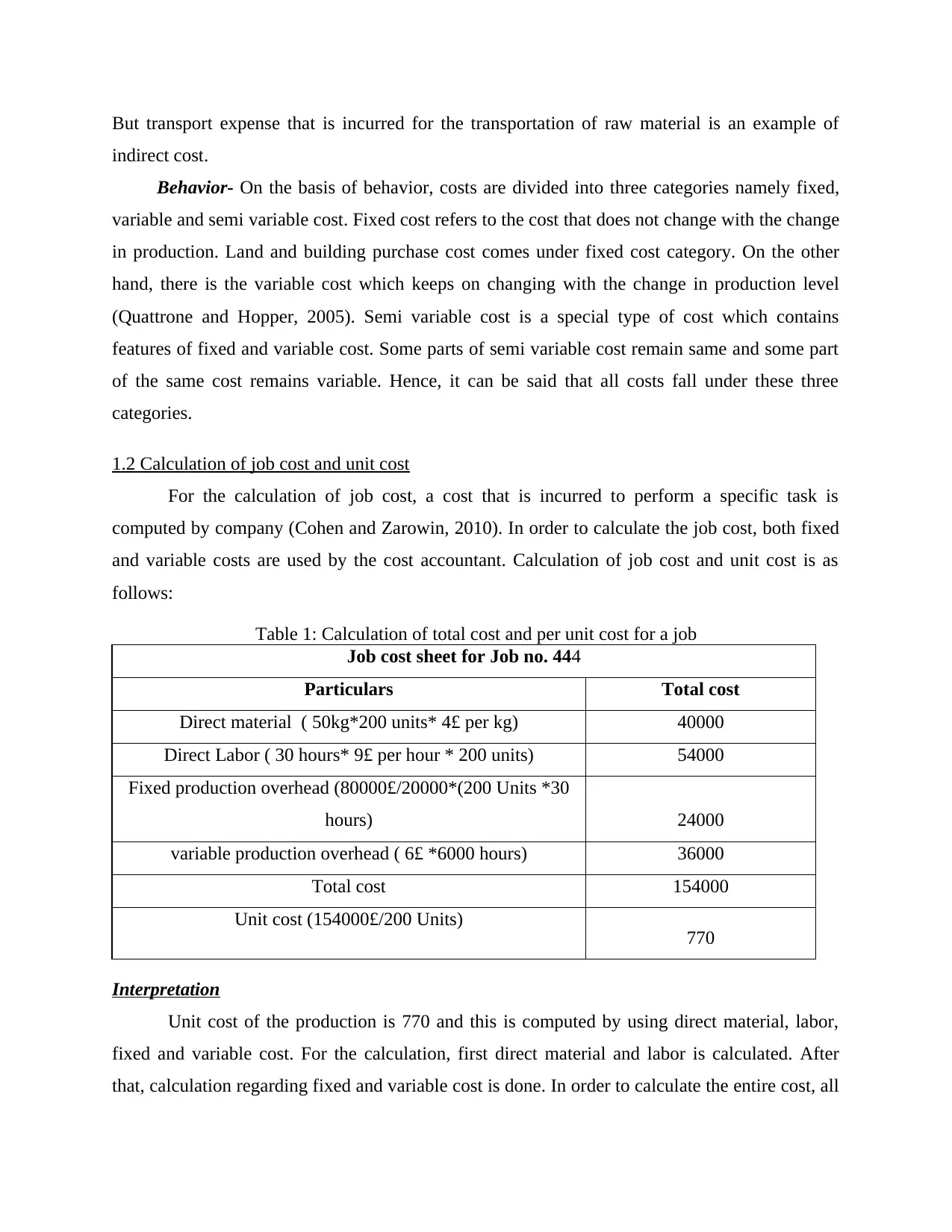

But transport expense that is incurred for the transportation of raw material is an example of

indirect cost.

Behavior- On the basis of behavior, costs are divided into three categories namely fixed,

variable and semi variable cost. Fixed cost refers to the cost that does not change with the change

in production. Land and building purchase cost comes under fixed cost category. On the other

hand, there is the variable cost which keeps on changing with the change in production level

(Quattrone and Hopper, 2005). Semi variable cost is a special type of cost which contains

features of fixed and variable cost. Some parts of semi variable cost remain same and some part

of the same cost remains variable. Hence, it can be said that all costs fall under these three

categories.

1.2 Calculation of job cost and unit cost

For the calculation of job cost, a cost that is incurred to perform a specific task is

computed by company (Cohen and Zarowin, 2010). In order to calculate the job cost, both fixed

and variable costs are used by the cost accountant. Calculation of job cost and unit cost is as

follows:

Table 1: Calculation of total cost and per unit cost for a job

Job cost sheet for Job no. 444

Particulars Total cost

Direct material ( 50kg*200 units* 4£ per kg) 40000

Direct Labor ( 30 hours* 9£ per hour * 200 units) 54000

Fixed production overhead (80000£/20000*(200 Units *30

hours) 24000

variable production overhead ( 6£ *6000 hours) 36000

Total cost 154000

Unit cost (154000£/200 Units) 770

Interpretation

Unit cost of the production is 770 and this is computed by using direct material, labor,

fixed and variable cost. For the calculation, first direct material and labor is calculated. After

that, calculation regarding fixed and variable cost is done. In order to calculate the entire cost, all

indirect cost.

Behavior- On the basis of behavior, costs are divided into three categories namely fixed,

variable and semi variable cost. Fixed cost refers to the cost that does not change with the change

in production. Land and building purchase cost comes under fixed cost category. On the other

hand, there is the variable cost which keeps on changing with the change in production level

(Quattrone and Hopper, 2005). Semi variable cost is a special type of cost which contains

features of fixed and variable cost. Some parts of semi variable cost remain same and some part

of the same cost remains variable. Hence, it can be said that all costs fall under these three

categories.

1.2 Calculation of job cost and unit cost

For the calculation of job cost, a cost that is incurred to perform a specific task is

computed by company (Cohen and Zarowin, 2010). In order to calculate the job cost, both fixed

and variable costs are used by the cost accountant. Calculation of job cost and unit cost is as

follows:

Table 1: Calculation of total cost and per unit cost for a job

Job cost sheet for Job no. 444

Particulars Total cost

Direct material ( 50kg*200 units* 4£ per kg) 40000

Direct Labor ( 30 hours* 9£ per hour * 200 units) 54000

Fixed production overhead (80000£/20000*(200 Units *30

hours) 24000

variable production overhead ( 6£ *6000 hours) 36000

Total cost 154000

Unit cost (154000£/200 Units) 770

Interpretation

Unit cost of the production is 770 and this is computed by using direct material, labor,

fixed and variable cost. For the calculation, first direct material and labor is calculated. After

that, calculation regarding fixed and variable cost is done. In order to calculate the entire cost, all

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

these expenses or costs are added and then divided by the total number of units that firm

produces. Finally, by doing this, per unit cost is calculated.

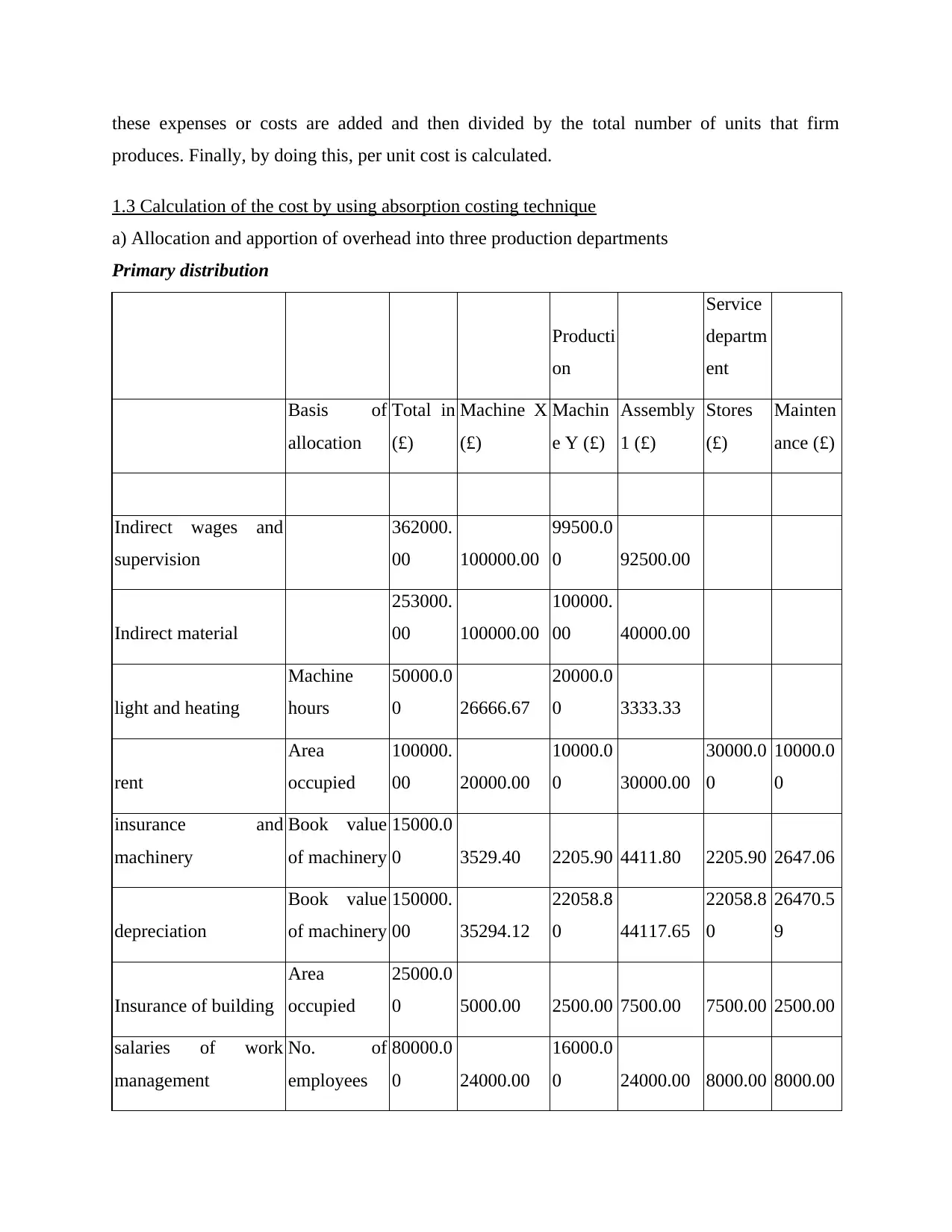

1.3 Calculation of the cost by using absorption costing technique

a) Allocation and apportion of overhead into three production departments

Primary distribution

Producti

on

Service

departm

ent

Basis of

allocation

Total in

(£)

Machine X

(£)

Machin

e Y (£)

Assembly

1 (£)

Stores

(£)

Mainten

ance (£)

Indirect wages and

supervision

362000.

00 100000.00

99500.0

0 92500.00

Indirect material

253000.

00 100000.00

100000.

00 40000.00

light and heating

Machine

hours

50000.0

0 26666.67

20000.0

0 3333.33

rent

Area

occupied

100000.

00 20000.00

10000.0

0 30000.00

30000.0

0

10000.0

0

insurance and

machinery

Book value

of machinery

15000.0

0 3529.40 2205.90 4411.80 2205.90 2647.06

depreciation

Book value

of machinery

150000.

00 35294.12

22058.8

0 44117.65

22058.8

0

26470.5

9

Insurance of building

Area

occupied

25000.0

0 5000.00 2500.00 7500.00 7500.00 2500.00

salaries of work

management

No. of

employees

80000.0

0 24000.00

16000.0

0 24000.00 8000.00 8000.00

produces. Finally, by doing this, per unit cost is calculated.

1.3 Calculation of the cost by using absorption costing technique

a) Allocation and apportion of overhead into three production departments

Primary distribution

Producti

on

Service

departm

ent

Basis of

allocation

Total in

(£)

Machine X

(£)

Machin

e Y (£)

Assembly

1 (£)

Stores

(£)

Mainten

ance (£)

Indirect wages and

supervision

362000.

00 100000.00

99500.0

0 92500.00

Indirect material

253000.

00 100000.00

100000.

00 40000.00

light and heating

Machine

hours

50000.0

0 26666.67

20000.0

0 3333.33

rent

Area

occupied

100000.

00 20000.00

10000.0

0 30000.00

30000.0

0

10000.0

0

insurance and

machinery

Book value

of machinery

15000.0

0 3529.40 2205.90 4411.80 2205.90 2647.06

depreciation

Book value

of machinery

150000.

00 35294.12

22058.8

0 44117.65

22058.8

0

26470.5

9

Insurance of building

Area

occupied

25000.0

0 5000.00 2500.00 7500.00 7500.00 2500.00

salaries of work

management

No. of

employees

80000.0

0 24000.00

16000.0

0 24000.00 8000.00 8000.00

103500

0.00 314490.19

272264.

70 245862.78

69764.7

0

49617.6

5

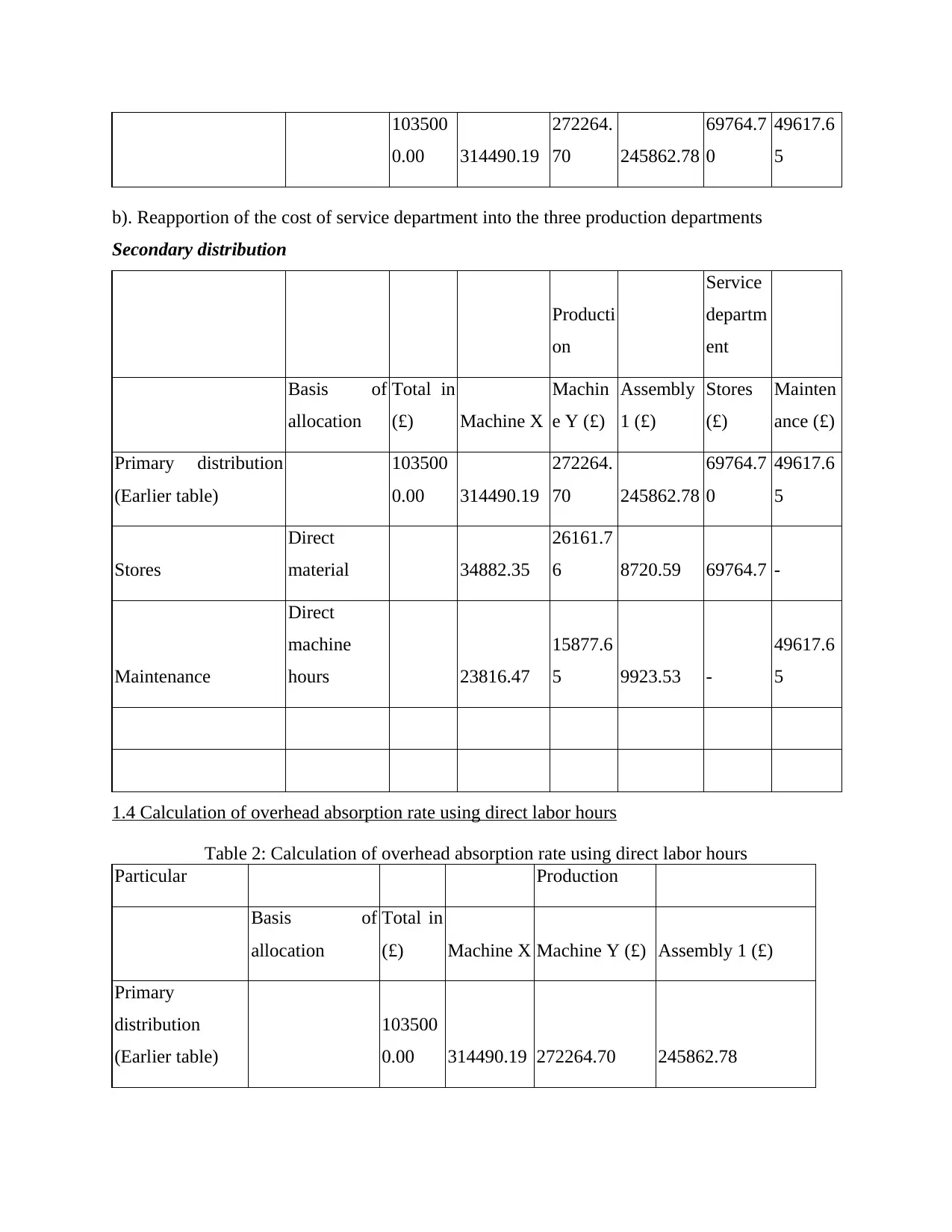

b). Reapportion of the cost of service department into the three production departments

Secondary distribution

Producti

on

Service

departm

ent

Basis of

allocation

Total in

(£) Machine X

Machin

e Y (£)

Assembly

1 (£)

Stores

(£)

Mainten

ance (£)

Primary distribution

(Earlier table)

103500

0.00 314490.19

272264.

70 245862.78

69764.7

0

49617.6

5

Stores

Direct

material 34882.35

26161.7

6 8720.59 69764.7 -

Maintenance

Direct

machine

hours 23816.47

15877.6

5 9923.53 -

49617.6

5

1.4 Calculation of overhead absorption rate using direct labor hours

Table 2: Calculation of overhead absorption rate using direct labor hours

Particular Production

Basis of

allocation

Total in

(£) Machine X Machine Y (£) Assembly 1 (£)

Primary

distribution

(Earlier table)

103500

0.00 314490.19 272264.70 245862.78

0.00 314490.19

272264.

70 245862.78

69764.7

0

49617.6

5

b). Reapportion of the cost of service department into the three production departments

Secondary distribution

Producti

on

Service

departm

ent

Basis of

allocation

Total in

(£) Machine X

Machin

e Y (£)

Assembly

1 (£)

Stores

(£)

Mainten

ance (£)

Primary distribution

(Earlier table)

103500

0.00 314490.19

272264.

70 245862.78

69764.7

0

49617.6

5

Stores

Direct

material 34882.35

26161.7

6 8720.59 69764.7 -

Maintenance

Direct

machine

hours 23816.47

15877.6

5 9923.53 -

49617.6

5

1.4 Calculation of overhead absorption rate using direct labor hours

Table 2: Calculation of overhead absorption rate using direct labor hours

Particular Production

Basis of

allocation

Total in

(£) Machine X Machine Y (£) Assembly 1 (£)

Primary

distribution

(Earlier table)

103500

0.00 314490.19 272264.70 245862.78

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Stores Direct material 34882.35 26161.76 8720.59

Maintenance Labor hours 2:1.5:1 22052.29 16539.22 11026.14

Total Cost 371424.83 314965.68 265609.51

Calculation of overhead absorption rates

Machine Y = 314965.68/150000 labor hours = £ 2.10

Assembly = 265609.51/100000 labor hours = £ 2.66

Machine X = 371424.83/200000 Labor hours = £1.86

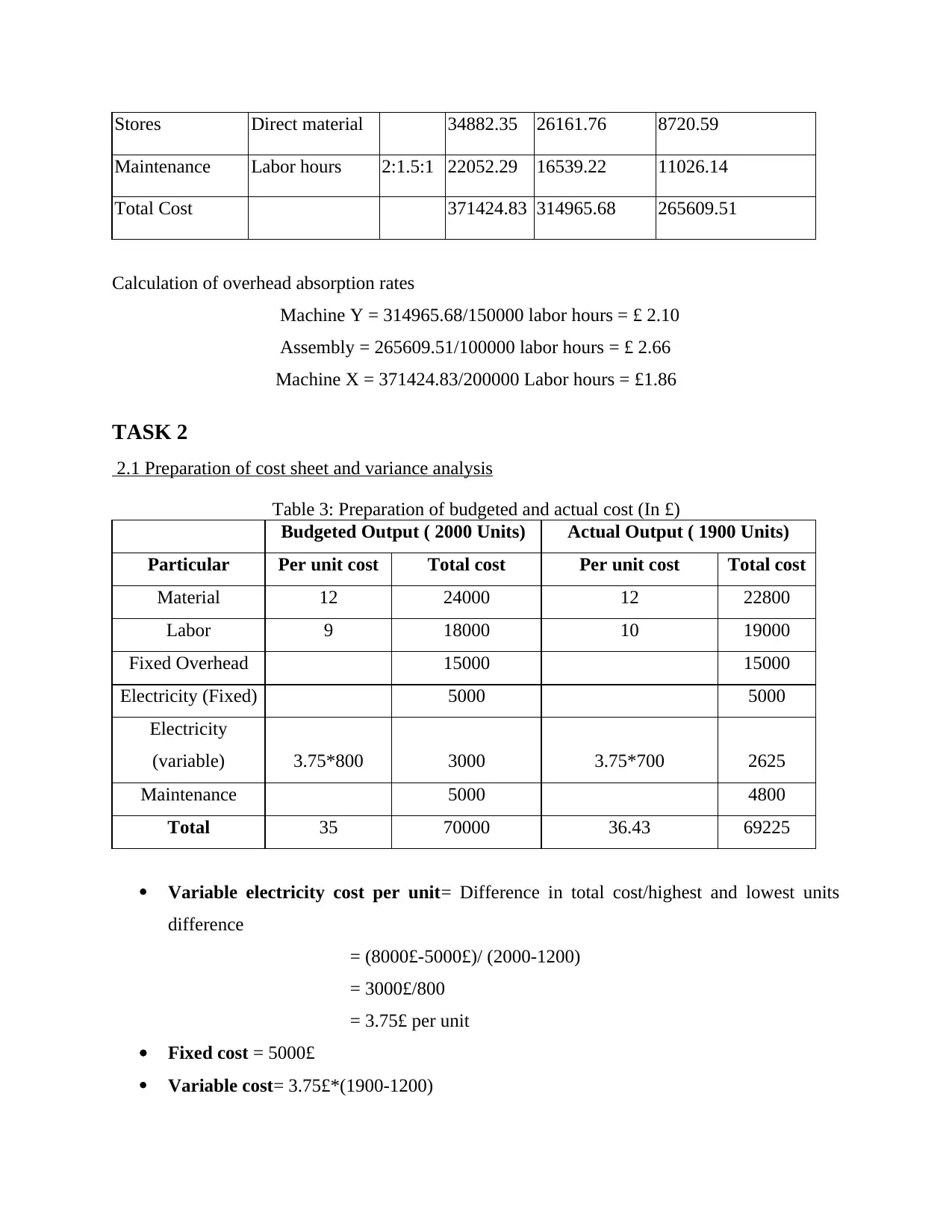

TASK 2

2.1 Preparation of cost sheet and variance analysis

Table 3: Preparation of budgeted and actual cost (In £)

Budgeted Output ( 2000 Units) Actual Output ( 1900 Units)

Particular Per unit cost Total cost Per unit cost Total cost

Material 12 24000 12 22800

Labor 9 18000 10 19000

Fixed Overhead 15000 15000

Electricity (Fixed) 5000 5000

Electricity

(variable) 3.75*800 3000 3.75*700 2625

Maintenance 5000 4800

Total 35 70000 36.43 69225

Variable electricity cost per unit= Difference in total cost/highest and lowest units

difference

= (8000£-5000£)/ (2000-1200)

= 3000£/800

= 3.75£ per unit

Fixed cost = 5000£

Variable cost= 3.75£*(1900-1200)

Maintenance Labor hours 2:1.5:1 22052.29 16539.22 11026.14

Total Cost 371424.83 314965.68 265609.51

Calculation of overhead absorption rates

Machine Y = 314965.68/150000 labor hours = £ 2.10

Assembly = 265609.51/100000 labor hours = £ 2.66

Machine X = 371424.83/200000 Labor hours = £1.86

TASK 2

2.1 Preparation of cost sheet and variance analysis

Table 3: Preparation of budgeted and actual cost (In £)

Budgeted Output ( 2000 Units) Actual Output ( 1900 Units)

Particular Per unit cost Total cost Per unit cost Total cost

Material 12 24000 12 22800

Labor 9 18000 10 19000

Fixed Overhead 15000 15000

Electricity (Fixed) 5000 5000

Electricity

(variable) 3.75*800 3000 3.75*700 2625

Maintenance 5000 4800

Total 35 70000 36.43 69225

Variable electricity cost per unit= Difference in total cost/highest and lowest units

difference

= (8000£-5000£)/ (2000-1200)

= 3000£/800

= 3.75£ per unit

Fixed cost = 5000£

Variable cost= 3.75£*(1900-1200)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

= 3.75£ * 700

= 2625£

Maintenance cost = 5000£ – (1000£/500*100)

= 5000£ – 200£ = 4800£

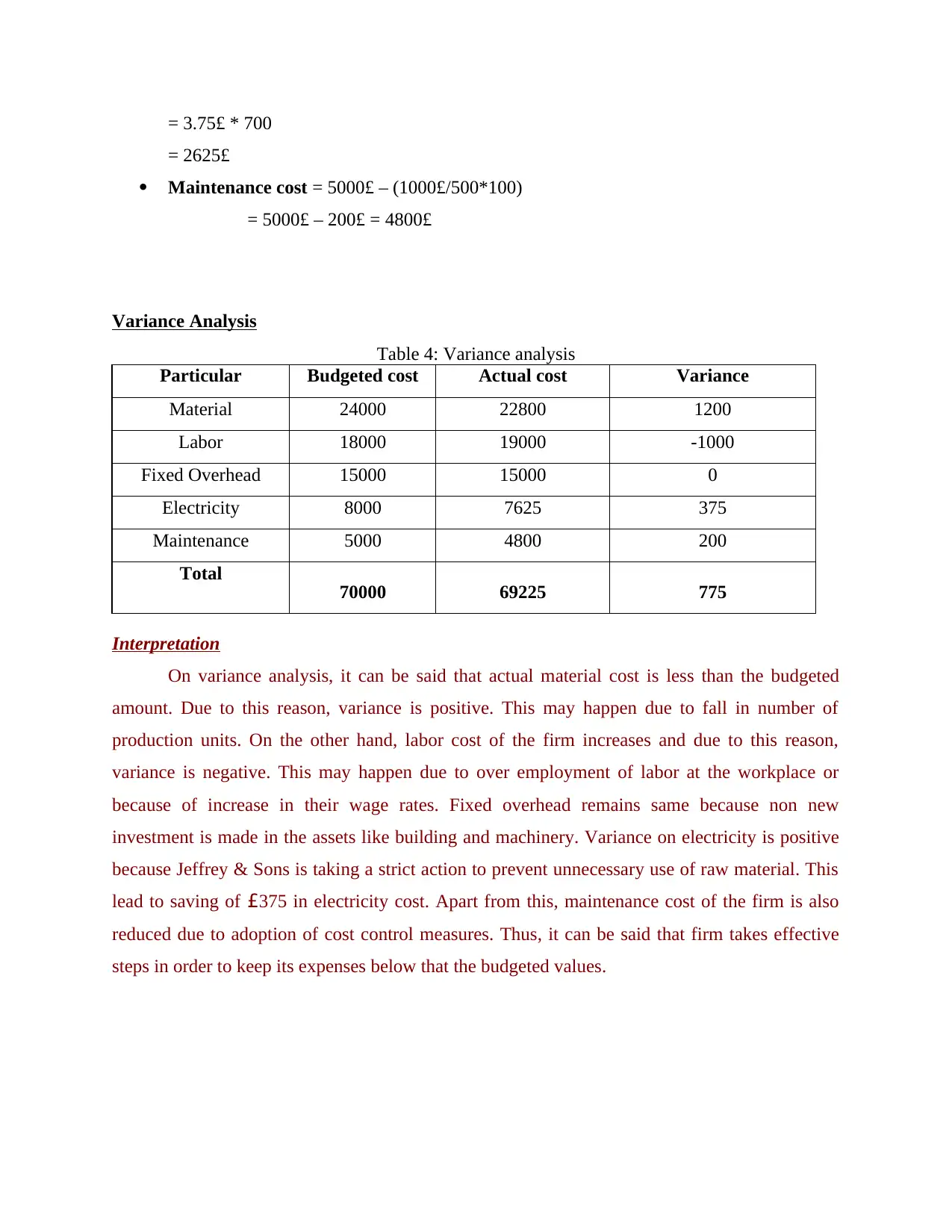

Variance Analysis

Table 4: Variance analysis

Particular Budgeted cost Actual cost Variance

Material 24000 22800 1200

Labor 18000 19000 -1000

Fixed Overhead 15000 15000 0

Electricity 8000 7625 375

Maintenance 5000 4800 200

Total 70000 69225 775

Interpretation

On variance analysis, it can be said that actual material cost is less than the budgeted

amount. Due to this reason, variance is positive. This may happen due to fall in number of

production units. On the other hand, labor cost of the firm increases and due to this reason,

variance is negative. This may happen due to over employment of labor at the workplace or

because of increase in their wage rates. Fixed overhead remains same because non new

investment is made in the assets like building and machinery. Variance on electricity is positive

because Jeffrey & Sons is taking a strict action to prevent unnecessary use of raw material. This

lead to saving of £375 in electricity cost. Apart from this, maintenance cost of the firm is also

reduced due to adoption of cost control measures. Thus, it can be said that firm takes effective

steps in order to keep its expenses below that the budgeted values.

= 2625£

Maintenance cost = 5000£ – (1000£/500*100)

= 5000£ – 200£ = 4800£

Variance Analysis

Table 4: Variance analysis

Particular Budgeted cost Actual cost Variance

Material 24000 22800 1200

Labor 18000 19000 -1000

Fixed Overhead 15000 15000 0

Electricity 8000 7625 375

Maintenance 5000 4800 200

Total 70000 69225 775

Interpretation

On variance analysis, it can be said that actual material cost is less than the budgeted

amount. Due to this reason, variance is positive. This may happen due to fall in number of

production units. On the other hand, labor cost of the firm increases and due to this reason,

variance is negative. This may happen due to over employment of labor at the workplace or

because of increase in their wage rates. Fixed overhead remains same because non new

investment is made in the assets like building and machinery. Variance on electricity is positive

because Jeffrey & Sons is taking a strict action to prevent unnecessary use of raw material. This

lead to saving of £375 in electricity cost. Apart from this, maintenance cost of the firm is also

reduced due to adoption of cost control measures. Thus, it can be said that firm takes effective

steps in order to keep its expenses below that the budgeted values.

2.2 Various performance indicators used to identify the areas of potential improvements

In order to measure the company’s performance on various platforms, performance

indicators are prepared by the managers. Some of the performance indicators that Jeffrey & Sons

can use are given as below: Profit- Profit is a point in company’s performance which gets changed with the change in

the firm’s way of management of activities. It means that in an organization, many

operations are performed like logistics, administration and cash management, etc. With

the change in all these things, firm’s turnover gets changed. Jeffery & Sons is in a

manufacturing sector and it is producing as well as selling goods in the market. For this,

it needs to transport the goods for which it pays a particular cost (Gunny, 2010). If it uses

transportation technique then it can identify a short route through which it can transport

its goods. The result of this effort will be that transportation cost will be reduced by some

percentage. Hence, it can be said that reduction in transportation cost will increase the

firm’s turnover to some extent. Due to this reason, turnover is taken as performance

indicator by most of the firms. Turnover- Turnover is another parameter that is used by the firms as a performance

indicator. In a year, firm makes many efforts that lead to increase in sales of the

organization (Greenwood and Suddaby, 2006). Jeffery & Sons can use social media in

order to increase the sale of its product. Along with this, it can also increase its sales

force size and can increase contact with the end users. This may also elevate the sales of

firm’s product. Hence, if these efforts will be made in a proper manner then it can be said

that sales of the firm will increase. Hence, it can be said that turnover is an important

performance indicator that can be used by the firm in order to measure its performance.

Customer satisfaction- This is another parameter that is commonly used by the firm

specially those who sale products to the general public. Many times, firms use some

different promotional techniques or introduce some features on the product (Francis and

Yu, 2009). In order to measure the effectiveness of newly made efforts, customer

satisfaction is used as an important parameter by the firm. Due to this reason, customer

satisfaction is commonly used by the firms in order to measure the effectiveness of

improvements that are newly made in the product.

In order to measure the company’s performance on various platforms, performance

indicators are prepared by the managers. Some of the performance indicators that Jeffrey & Sons

can use are given as below: Profit- Profit is a point in company’s performance which gets changed with the change in

the firm’s way of management of activities. It means that in an organization, many

operations are performed like logistics, administration and cash management, etc. With

the change in all these things, firm’s turnover gets changed. Jeffery & Sons is in a

manufacturing sector and it is producing as well as selling goods in the market. For this,

it needs to transport the goods for which it pays a particular cost (Gunny, 2010). If it uses

transportation technique then it can identify a short route through which it can transport

its goods. The result of this effort will be that transportation cost will be reduced by some

percentage. Hence, it can be said that reduction in transportation cost will increase the

firm’s turnover to some extent. Due to this reason, turnover is taken as performance

indicator by most of the firms. Turnover- Turnover is another parameter that is used by the firms as a performance

indicator. In a year, firm makes many efforts that lead to increase in sales of the

organization (Greenwood and Suddaby, 2006). Jeffery & Sons can use social media in

order to increase the sale of its product. Along with this, it can also increase its sales

force size and can increase contact with the end users. This may also elevate the sales of

firm’s product. Hence, if these efforts will be made in a proper manner then it can be said

that sales of the firm will increase. Hence, it can be said that turnover is an important

performance indicator that can be used by the firm in order to measure its performance.

Customer satisfaction- This is another parameter that is commonly used by the firm

specially those who sale products to the general public. Many times, firms use some

different promotional techniques or introduce some features on the product (Francis and

Yu, 2009). In order to measure the effectiveness of newly made efforts, customer

satisfaction is used as an important parameter by the firm. Due to this reason, customer

satisfaction is commonly used by the firms in order to measure the effectiveness of

improvements that are newly made in the product.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2.3 Ways to reduce cost, enhance value and quality

In order to reduce the cost, Jefferey & Sons can take many steps. It can make an effort

that will lead to generation of economies of scale. In respect to this, it can analyze its production

operations. On analysis of these operations, lots of unnecessary activities will be identified that

are increasing the cost of the firm and also elevating the completion time of task. After

identification of these unproductive tasks, firm will be in position to speed up its production cost

at a reduced production cost (Hillier, Grinblatt and Titman, 2011). This will lead to the

generation of economies of scale for the firm. In order to enhance the value of product, firm

needs to compare itself with other company’s products. By doing comparison, firm will be in

position to identify the areas where it can make improvement in its product. Thus, by making

necessary changes in the product, value can be improved Jeffery & sons. Quality is another area

where firm needs to give special attention and to improve the quality of product. It can carry out

research and development program (Francis, Reichelt and Wang, 2005). Under such kind of

activity, heavy investment will be made. But by organizing such kind of programs in the

organization, innovative changes can be made in the product. This will differentiate company’s

product from the same of competitor and will boost the sale of it as well.

In order to reduce the cost, Jefferey & Sons can take many steps. It can make an effort

that will lead to generation of economies of scale. In respect to this, it can analyze its production

operations. On analysis of these operations, lots of unnecessary activities will be identified that

are increasing the cost of the firm and also elevating the completion time of task. After

identification of these unproductive tasks, firm will be in position to speed up its production cost

at a reduced production cost (Hillier, Grinblatt and Titman, 2011). This will lead to the

generation of economies of scale for the firm. In order to enhance the value of product, firm

needs to compare itself with other company’s products. By doing comparison, firm will be in

position to identify the areas where it can make improvement in its product. Thus, by making

necessary changes in the product, value can be improved Jeffery & sons. Quality is another area

where firm needs to give special attention and to improve the quality of product. It can carry out

research and development program (Francis, Reichelt and Wang, 2005). Under such kind of

activity, heavy investment will be made. But by organizing such kind of programs in the

organization, innovative changes can be made in the product. This will differentiate company’s

product from the same of competitor and will boost the sale of it as well.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 3

3.1 Nature and purpose of budgeting process

Budget is a statement that covers targets or predictions done by the management.

Management makes an attempt to keep its performance nearby to the budgeted figures.

Budgeting process that most of the firms are following is given below. Determination of standard- In this stage a standard is determined against which actual

values of the budget is compared. These standards are determined by considering lots of

factors like past budget and performance regarding same as well as economic data. In

case of past budget firm evaluate figures that were determined in the budget and after that

it check the extent to which firm gives better performance. Performance on that budget

gives lot of inputs to the firm that can be used to prepare a budget (Hennes, Leone and

Miller, 2008). Firm must also evaluate economic conditions of the time period with

which budget is related. By doing all this work manager will come to know that in

specific economic condition to what level of performance it delivered in earlier stage.

Thus, on the basis of evaluation of current economic environment managers will be able

to predict changes that can take place in the components of the budget. Hence, entire

result of this effort will be that management will be able to prepare budget targets that are

possible to achieve in the specific economic environment. Measurement of the company performance- In this stage performance of the firm is

measured in terms of units or specific value (Henri, 2006). For example, performance of

Jefferey & sons can be measured in terms of sales in form of units that are sold in the

market. With due care managers must measure company performance because it is very

important stage of the budget control process. Comparison with standard- In this stage actual performance figures are compared with

the budgeted figures. By making comparison variance is identified which may be positive

of negative in nature. If variance is positive then there is no problem. But if variance is

negative then there is a matter of concern (Ogneva, Subramanyam and Raghunandan,

2007). In such kind of case, managers operating at middle level of management need to

identify possible causes of variance. By identifying variance managers further go in next

stage which is a final stage of budget process.

3.1 Nature and purpose of budgeting process

Budget is a statement that covers targets or predictions done by the management.

Management makes an attempt to keep its performance nearby to the budgeted figures.

Budgeting process that most of the firms are following is given below. Determination of standard- In this stage a standard is determined against which actual

values of the budget is compared. These standards are determined by considering lots of

factors like past budget and performance regarding same as well as economic data. In

case of past budget firm evaluate figures that were determined in the budget and after that

it check the extent to which firm gives better performance. Performance on that budget

gives lot of inputs to the firm that can be used to prepare a budget (Hennes, Leone and

Miller, 2008). Firm must also evaluate economic conditions of the time period with

which budget is related. By doing all this work manager will come to know that in

specific economic condition to what level of performance it delivered in earlier stage.

Thus, on the basis of evaluation of current economic environment managers will be able

to predict changes that can take place in the components of the budget. Hence, entire

result of this effort will be that management will be able to prepare budget targets that are

possible to achieve in the specific economic environment. Measurement of the company performance- In this stage performance of the firm is

measured in terms of units or specific value (Henri, 2006). For example, performance of

Jefferey & sons can be measured in terms of sales in form of units that are sold in the

market. With due care managers must measure company performance because it is very

important stage of the budget control process. Comparison with standard- In this stage actual performance figures are compared with

the budgeted figures. By making comparison variance is identified which may be positive

of negative in nature. If variance is positive then there is no problem. But if variance is

negative then there is a matter of concern (Ogneva, Subramanyam and Raghunandan,

2007). In such kind of case, managers operating at middle level of management need to

identify possible causes of variance. By identifying variance managers further go in next

stage which is a final stage of budget process.

Taking corrective action- In this stage corrective actions are taken against that variance

which is negative in nature. These actions are taken in order to make sure that such kind

of mistakes due to which negative variance come in existence will not be committed

again at the workplace.

Process for preparing a budget Gather information- This is the first step in preparing a budget under which all relevant

information's are gathered related to income and expenditures that a firm may earn and

incur in upcoming time period. This information's can be gathered from company internal

sources like past income statements etc. Recording all sources of income- After collection of data all sources of income are

determined from which firm can earn revenue. These sources may be sales and income

from investments. Creating a list of monthly income- In this stage a list of monthly income is prepared

which can be earned in upcoming months. This estimate is made on the basis of past data

and growth rate of sales. By taking average growth rate projections for upcoming months

are prepared. Estimating expenses- In this stage all expenses are estimated on the basis of past growth

rate of expenses. Like income in case of expenses also projections are made. Hence, it

can be said that, method of projection is same in case of income and expenses. Preparing a final budget- In this last stage a budget is prepared in which all incomes and

expenses are placed in a budget in proper manner. In this regard firstly, all incomes are

shown in the budget and after that all expenses are shown in the budget. Hence, in this

way budget is prepared by the managers.

Purpose of budget

The main purpose of the budget is to ensure that expenses of the firm will remain in

control of the management. In other words, it can be said that the main objective of the budget is

to manage activities in a proper manner within predetermined standard. This budget is also used

to motivate employees to work hard for welfare of an organization (Easterby-Smith, Thorpe, and

Jackson, 2012). These standards acts as target for the employees and due to this reason they get

motivated to make efforts that helps an organization to achieve its objective. Hence, it can be

said that budget helps organization in achieving its objective.

which is negative in nature. These actions are taken in order to make sure that such kind

of mistakes due to which negative variance come in existence will not be committed

again at the workplace.

Process for preparing a budget Gather information- This is the first step in preparing a budget under which all relevant

information's are gathered related to income and expenditures that a firm may earn and

incur in upcoming time period. This information's can be gathered from company internal

sources like past income statements etc. Recording all sources of income- After collection of data all sources of income are

determined from which firm can earn revenue. These sources may be sales and income

from investments. Creating a list of monthly income- In this stage a list of monthly income is prepared

which can be earned in upcoming months. This estimate is made on the basis of past data

and growth rate of sales. By taking average growth rate projections for upcoming months

are prepared. Estimating expenses- In this stage all expenses are estimated on the basis of past growth

rate of expenses. Like income in case of expenses also projections are made. Hence, it

can be said that, method of projection is same in case of income and expenses. Preparing a final budget- In this last stage a budget is prepared in which all incomes and

expenses are placed in a budget in proper manner. In this regard firstly, all incomes are

shown in the budget and after that all expenses are shown in the budget. Hence, in this

way budget is prepared by the managers.

Purpose of budget

The main purpose of the budget is to ensure that expenses of the firm will remain in

control of the management. In other words, it can be said that the main objective of the budget is

to manage activities in a proper manner within predetermined standard. This budget is also used

to motivate employees to work hard for welfare of an organization (Easterby-Smith, Thorpe, and

Jackson, 2012). These standards acts as target for the employees and due to this reason they get

motivated to make efforts that helps an organization to achieve its objective. Hence, it can be

said that budget helps organization in achieving its objective.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.