Contemporary Issues in Accounting

VerifiedAdded on 2023/01/20

|11

|1350

|61

AI Summary

This report explores the contemporary issues in accounting and focuses on compliance with measurement requirements, fundamental and enhancing qualitative characteristics, and the use of financial statements for users.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: REPORT 1

CONTEMPORARY ISSUES IN ACCOUNTING

Student details:

4/19/2019

CONTEMPORARY ISSUES IN ACCOUNTING

Student details:

4/19/2019

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REPORT 2

Executive summary

The major objective of the conceptual framework is to assist the Board to make International

Financial Reporting Standards on the basis of constant concepts, resulting in financial data,

which is helpful for the users including investors, potential investors, lenders and creditors. This

report discovers the contemporary issues in accounting in critically manner.

Executive summary

The major objective of the conceptual framework is to assist the Board to make International

Financial Reporting Standards on the basis of constant concepts, resulting in financial data,

which is helpful for the users including investors, potential investors, lenders and creditors. This

report discovers the contemporary issues in accounting in critically manner.

REPORT 3

Contents

Executive summary.....................................................................................................................................2

Introduction.................................................................................................................................................4

Company overview......................................................................................................................................4

Compliance with measurement requirements of conceptual framework......................................................4

Compliance with fundamental qualitative characteristics............................................................................5

Compliance with enhancing qualitative characteristics...............................................................................6

Use of financial statements for the users.....................................................................................................7

Deep analyses of financial statements for the users.....................................................................................7

Compliance with general purpose financial reporting.................................................................................7

Conclusion...................................................................................................................................................8

References...................................................................................................................................................8

Contents

Executive summary.....................................................................................................................................2

Introduction.................................................................................................................................................4

Company overview......................................................................................................................................4

Compliance with measurement requirements of conceptual framework......................................................4

Compliance with fundamental qualitative characteristics............................................................................5

Compliance with enhancing qualitative characteristics...............................................................................6

Use of financial statements for the users.....................................................................................................7

Deep analyses of financial statements for the users.....................................................................................7

Compliance with general purpose financial reporting.................................................................................7

Conclusion...................................................................................................................................................8

References...................................................................................................................................................8

REPORT 4

Introduction

The contemporary issues are related to the issues which are faced by the professional in

accounting. In the following parts, the contemporary issues in accounting in G8 Education

Limited is discussed and critically examined. This report focuses on existing and new issues,

which influence the contemporary practices related to accounting.

Company overview

In Australia, G8 Education Limited is a biggest ASX listed operator related to child care centre.

G8 Education Limited has very easy mission. The main target of this company is to become the

leading provider of high quality, developmental and learning child care service in Australia. G8

Education Limited looks for getting this throughout the 4 pillars for the development and

expansion. This company was established in year 2006 and taken together the dedicated experts

as team driven, to provide highest quality developmental and educational child care service

through Australia. It was in response to improving administrative regulations creating this harder

for single-centre operator to live.

Compliance with measurement requirements of conceptual framework

The IASB issued amended Conceptual Framework for Financial Reporting, the comprehensive

set of theories regarding the financial reporting (Gummer and Mandinach, 2015). The

conceptual framework defines-

1. the objective of financial reporting

2. fundamental qualitative characteristics in respect of relevant financial data

3. Enhancing qualitative characteristics in respect of relevant financial data

Introduction

The contemporary issues are related to the issues which are faced by the professional in

accounting. In the following parts, the contemporary issues in accounting in G8 Education

Limited is discussed and critically examined. This report focuses on existing and new issues,

which influence the contemporary practices related to accounting.

Company overview

In Australia, G8 Education Limited is a biggest ASX listed operator related to child care centre.

G8 Education Limited has very easy mission. The main target of this company is to become the

leading provider of high quality, developmental and learning child care service in Australia. G8

Education Limited looks for getting this throughout the 4 pillars for the development and

expansion. This company was established in year 2006 and taken together the dedicated experts

as team driven, to provide highest quality developmental and educational child care service

through Australia. It was in response to improving administrative regulations creating this harder

for single-centre operator to live.

Compliance with measurement requirements of conceptual framework

The IASB issued amended Conceptual Framework for Financial Reporting, the comprehensive

set of theories regarding the financial reporting (Gummer and Mandinach, 2015). The

conceptual framework defines-

1. the objective of financial reporting

2. fundamental qualitative characteristics in respect of relevant financial data

3. Enhancing qualitative characteristics in respect of relevant financial data

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REPORT 5

4. explanation of reporting entity and the limit

5. meaning of an asset, expenses, equity, income and asset

6. methods to include assets and liabilities in financial statements

7. recognition and derecognition of assets and liabilities

8. basis for measurement and direction to use them

9. Concepts and direction on item’s disclosure and presentation.

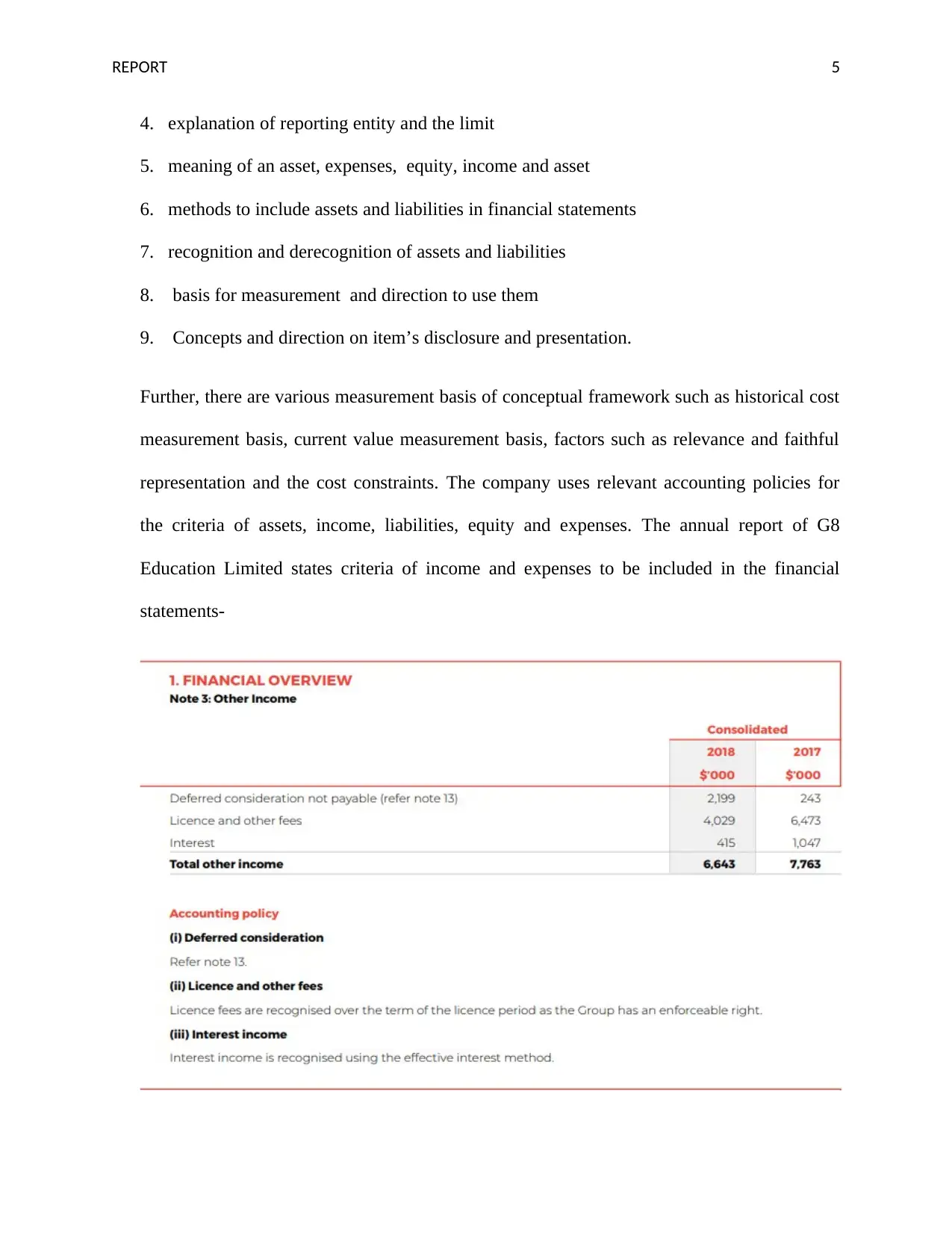

Further, there are various measurement basis of conceptual framework such as historical cost

measurement basis, current value measurement basis, factors such as relevance and faithful

representation and the cost constraints. The company uses relevant accounting policies for

the criteria of assets, income, liabilities, equity and expenses. The annual report of G8

Education Limited states criteria of income and expenses to be included in the financial

statements-

4. explanation of reporting entity and the limit

5. meaning of an asset, expenses, equity, income and asset

6. methods to include assets and liabilities in financial statements

7. recognition and derecognition of assets and liabilities

8. basis for measurement and direction to use them

9. Concepts and direction on item’s disclosure and presentation.

Further, there are various measurement basis of conceptual framework such as historical cost

measurement basis, current value measurement basis, factors such as relevance and faithful

representation and the cost constraints. The company uses relevant accounting policies for

the criteria of assets, income, liabilities, equity and expenses. The annual report of G8

Education Limited states criteria of income and expenses to be included in the financial

statements-

REPORT 6

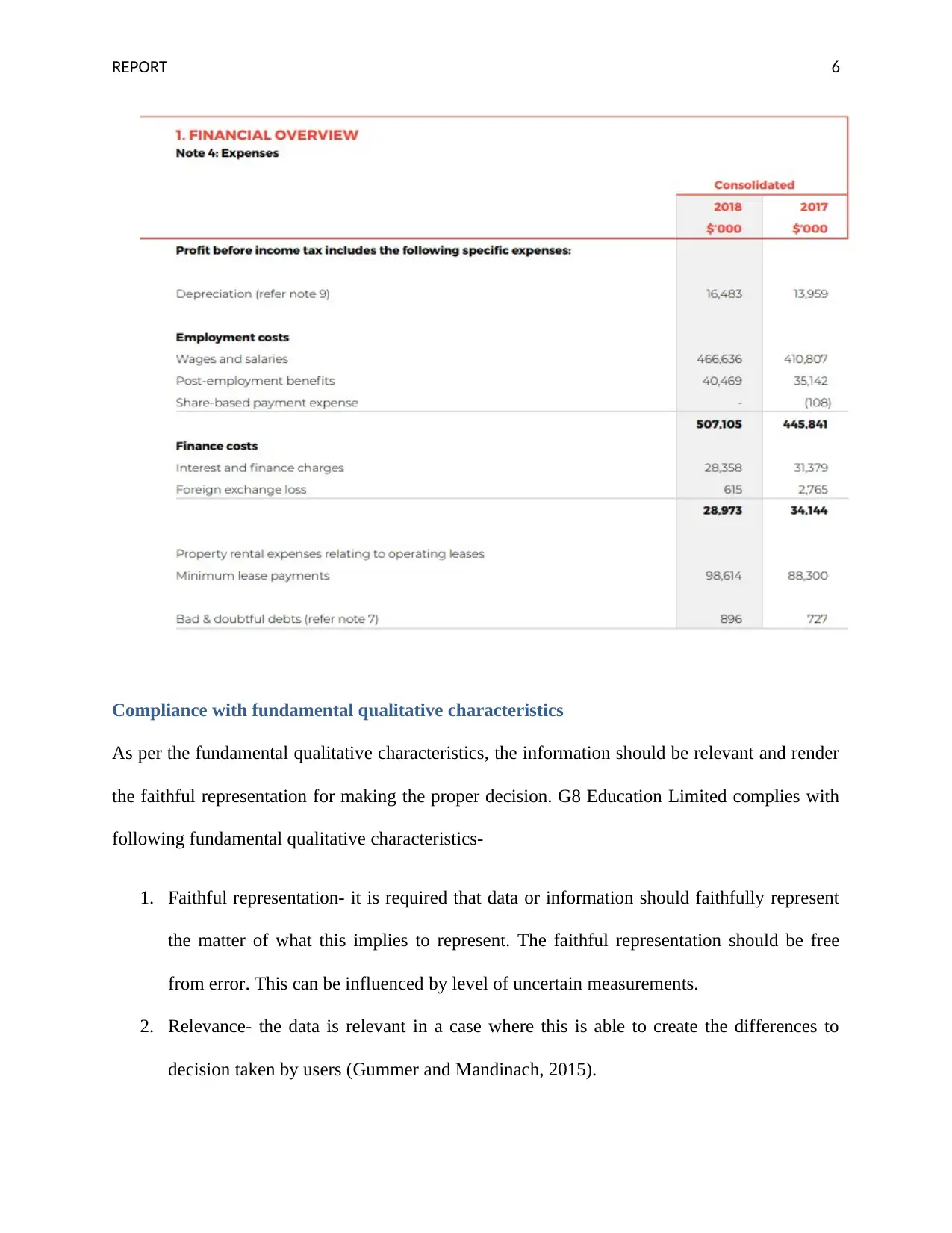

Compliance with fundamental qualitative characteristics

As per the fundamental qualitative characteristics, the information should be relevant and render

the faithful representation for making the proper decision. G8 Education Limited complies with

following fundamental qualitative characteristics-

1. Faithful representation- it is required that data or information should faithfully represent

the matter of what this implies to represent. The faithful representation should be free

from error. This can be influenced by level of uncertain measurements.

2. Relevance- the data is relevant in a case where this is able to create the differences to

decision taken by users (Gummer and Mandinach, 2015).

Compliance with fundamental qualitative characteristics

As per the fundamental qualitative characteristics, the information should be relevant and render

the faithful representation for making the proper decision. G8 Education Limited complies with

following fundamental qualitative characteristics-

1. Faithful representation- it is required that data or information should faithfully represent

the matter of what this implies to represent. The faithful representation should be free

from error. This can be influenced by level of uncertain measurements.

2. Relevance- the data is relevant in a case where this is able to create the differences to

decision taken by users (Gummer and Mandinach, 2015).

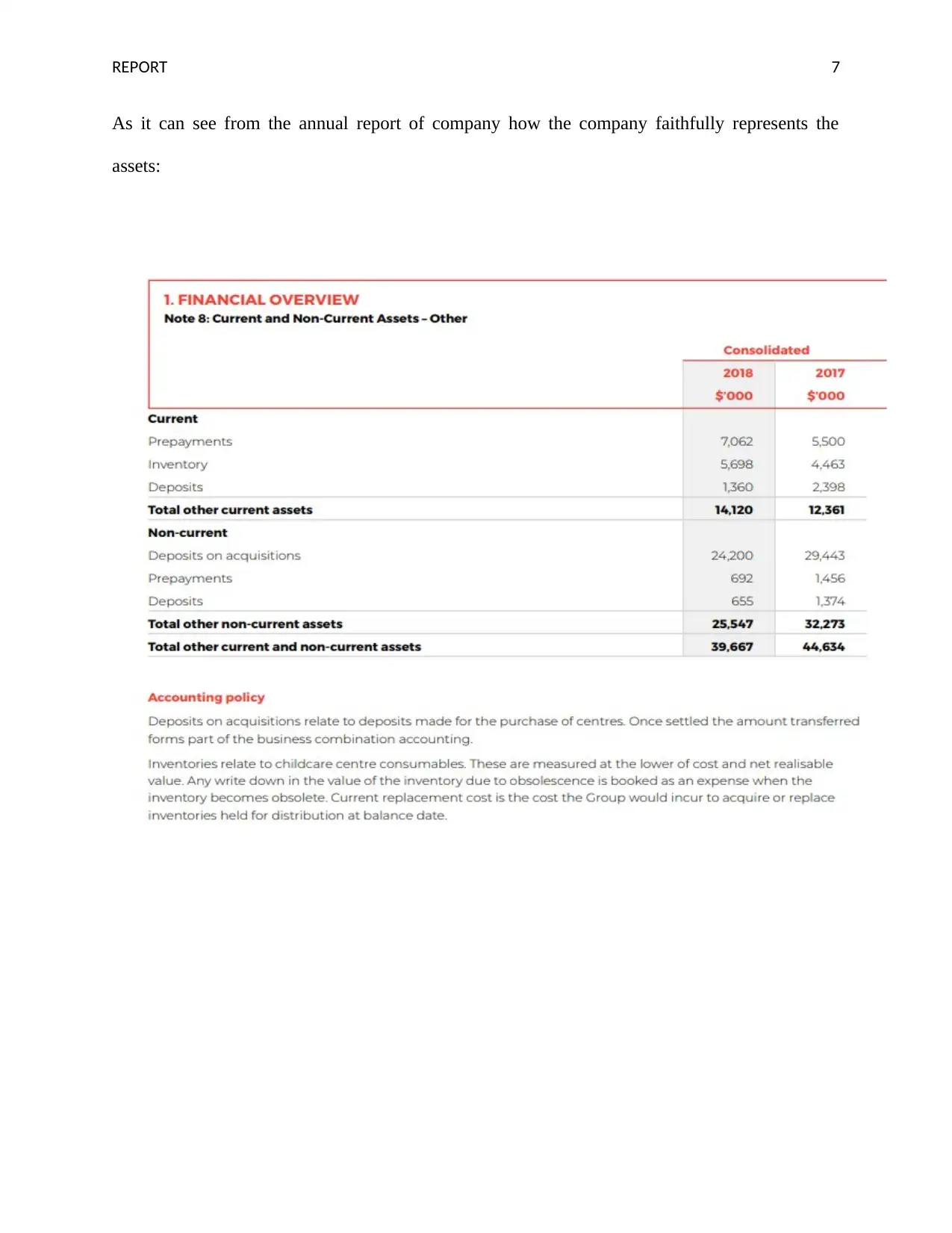

REPORT 7

As it can see from the annual report of company how the company faithfully represents the

assets:

As it can see from the annual report of company how the company faithfully represents the

assets:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REPORT 8

Compliance with enhancing qualitative characteristics

There are four enhancing qualitative characteristics such as verifiability, timeliness,

comparability and understandability. However, these enhancing qualitative characteristics may

not create non-useful data useful. G8 Education Limited complies with following enhancing

qualitative characteristics-

1. Verifiability- The verifiability is very helpful in stating the information faithfully for the

better results.

2. Timeliness- timeliness of accounting information means that the requirements of data to

use rapidly to take relevant actions.

3. Understandability- the information must be understood to take proper decisions.

4. Comparability- the data should be equivalent to financial information stated for various

accounting period to recognise the trend.

Use of financial statements for the users

The main purpose of the financial reporting is to give the financial information, which is helpful

to various users in taking proper decisions in relation to rendering resources to the company. The

financial reporting is very useful for the investors such as creditors, investors, potential investors

and lenders. These users use the financial statements in making decisions. The decisions of users

Compliance with enhancing qualitative characteristics

There are four enhancing qualitative characteristics such as verifiability, timeliness,

comparability and understandability. However, these enhancing qualitative characteristics may

not create non-useful data useful. G8 Education Limited complies with following enhancing

qualitative characteristics-

1. Verifiability- The verifiability is very helpful in stating the information faithfully for the

better results.

2. Timeliness- timeliness of accounting information means that the requirements of data to

use rapidly to take relevant actions.

3. Understandability- the information must be understood to take proper decisions.

4. Comparability- the data should be equivalent to financial information stated for various

accounting period to recognise the trend.

Use of financial statements for the users

The main purpose of the financial reporting is to give the financial information, which is helpful

to various users in taking proper decisions in relation to rendering resources to the company. The

financial reporting is very useful for the investors such as creditors, investors, potential investors

and lenders. These users use the financial statements in making decisions. The decisions of users

REPORT 9

include the decision in respect of rendering the loans and other credit, purchasing or holding or

selling instrument related to debt and equity, and in relation to vote, or else affecting the actions

or performances of management. For making these decisions, it is required by the users to

evaluate the prospect future net cash flow to a company and to assess the stewardship of

administration of financial resources of company (Annual Report, 2018).

Deep analyses of financial statements for the users

It is said by the conceptual framework that the users only require basic knowledge of accounting.

However, for the better evaluation, it is required by users to get the information related to the

financial resources of a company, modifications in resources, and claims in against corporation.

The users are also required to have the knowledge regarding that how properly the administration

had discharged the duties to utilize the financial resources of an organization (Krsekova and

Paksiova, 2015).

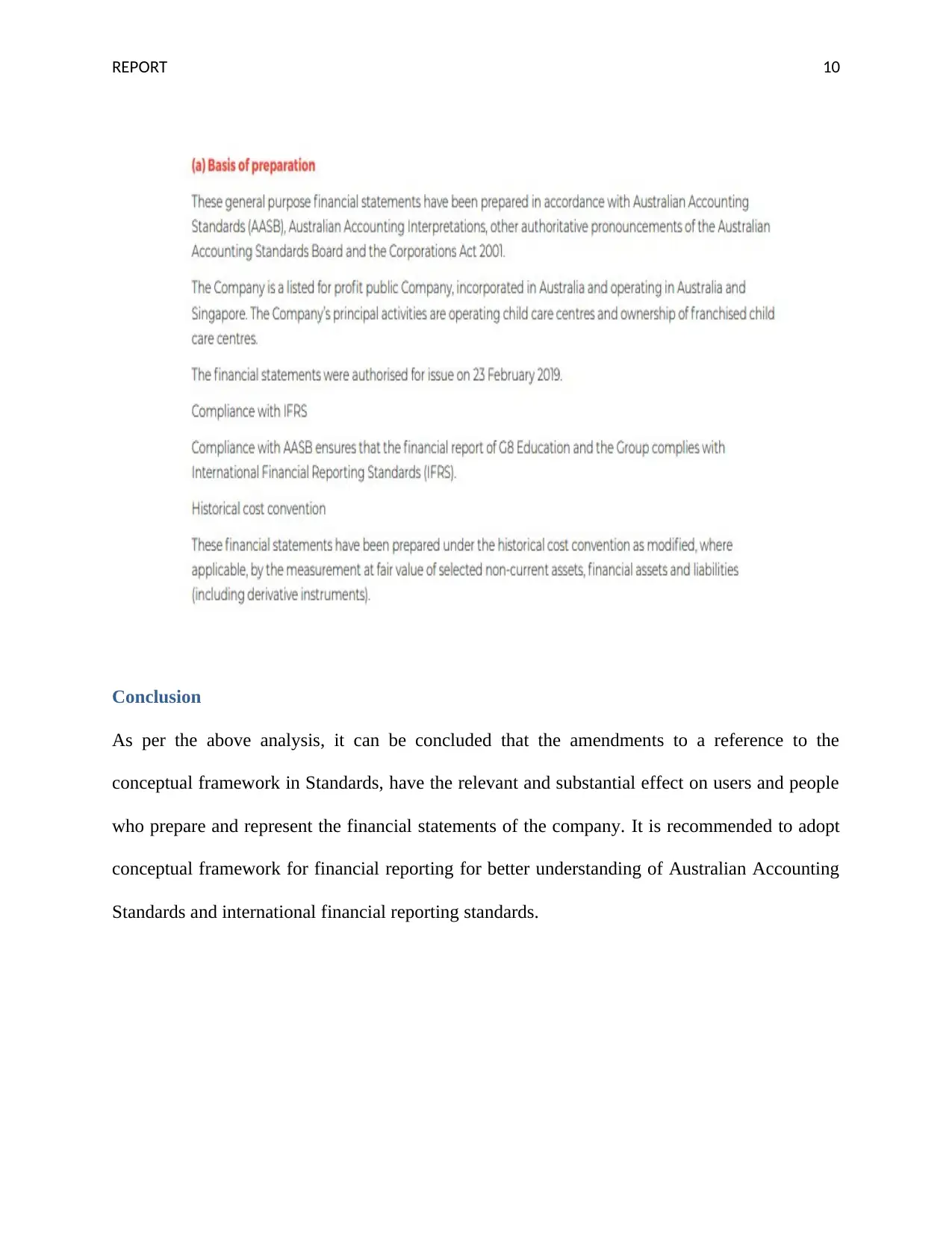

Compliance with general purpose financial reporting

The annual report of G8 Education Limited states that the conceptual framework for financial

reporting defines the concept and purpose for preparing the general purpose financial reporting.

The conceptual framework sets out the changes to standard, the associated document and the

statement of International financial reporting standards. The annual report of G8 Education

Limited states that it prepares cash flow statement, balance sheet, statement of owner’s equity,

income statement as per the Corporations Act 2001 (Lewandowski, 2016).

include the decision in respect of rendering the loans and other credit, purchasing or holding or

selling instrument related to debt and equity, and in relation to vote, or else affecting the actions

or performances of management. For making these decisions, it is required by the users to

evaluate the prospect future net cash flow to a company and to assess the stewardship of

administration of financial resources of company (Annual Report, 2018).

Deep analyses of financial statements for the users

It is said by the conceptual framework that the users only require basic knowledge of accounting.

However, for the better evaluation, it is required by users to get the information related to the

financial resources of a company, modifications in resources, and claims in against corporation.

The users are also required to have the knowledge regarding that how properly the administration

had discharged the duties to utilize the financial resources of an organization (Krsekova and

Paksiova, 2015).

Compliance with general purpose financial reporting

The annual report of G8 Education Limited states that the conceptual framework for financial

reporting defines the concept and purpose for preparing the general purpose financial reporting.

The conceptual framework sets out the changes to standard, the associated document and the

statement of International financial reporting standards. The annual report of G8 Education

Limited states that it prepares cash flow statement, balance sheet, statement of owner’s equity,

income statement as per the Corporations Act 2001 (Lewandowski, 2016).

REPORT 10

Conclusion

As per the above analysis, it can be concluded that the amendments to a reference to the

conceptual framework in Standards, have the relevant and substantial effect on users and people

who prepare and represent the financial statements of the company. It is recommended to adopt

conceptual framework for financial reporting for better understanding of Australian Accounting

Standards and international financial reporting standards.

Conclusion

As per the above analysis, it can be concluded that the amendments to a reference to the

conceptual framework in Standards, have the relevant and substantial effect on users and people

who prepare and represent the financial statements of the company. It is recommended to adopt

conceptual framework for financial reporting for better understanding of Australian Accounting

Standards and international financial reporting standards.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REPORT 11

References

Annual Report (2018) G8 Education Limited [Online] Available at:

<https://g8education.edu.au/wp-content/uploads/2019/02/Annual-Report-2018.pdf> [Accessed

19/04/2019]

Gummer, E. and Mandinach, E. (2015) Building a Conceptual Framework for Data

Literacy. Teachers College Record, 117(4), p.n4.

Kršeková, M. and Pakšiová, R. (2015) Financial reporting on information about the financial

position and financial performance in the financial statements of the public sector. Finance and

risk 2015, 14(1), pp.136-145.

Lewandowski, M. (2016) Designing the business models for circular economy—Towards the

conceptual framework. Sustainability, 8(1), p.43.

Panteli, M. and Mancarella, P. (2015) The grid: Stronger bigger smarter?: Presenting a

conceptual framework of power system resilience. IEEE Power Energy Mag, 13(3), pp.58-66.

References

Annual Report (2018) G8 Education Limited [Online] Available at:

<https://g8education.edu.au/wp-content/uploads/2019/02/Annual-Report-2018.pdf> [Accessed

19/04/2019]

Gummer, E. and Mandinach, E. (2015) Building a Conceptual Framework for Data

Literacy. Teachers College Record, 117(4), p.n4.

Kršeková, M. and Pakšiová, R. (2015) Financial reporting on information about the financial

position and financial performance in the financial statements of the public sector. Finance and

risk 2015, 14(1), pp.136-145.

Lewandowski, M. (2016) Designing the business models for circular economy—Towards the

conceptual framework. Sustainability, 8(1), p.43.

Panteli, M. and Mancarella, P. (2015) The grid: Stronger bigger smarter?: Presenting a

conceptual framework of power system resilience. IEEE Power Energy Mag, 13(3), pp.58-66.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.