Corporate and Financial Accounting Australia Report 2022

VerifiedAdded on 2022/10/15

|16

|3122

|19

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running Head: CORPORATE AND FINANCIAL ACCOUNTING

CORPORATE AND FINANCIAL ACCOUNTING

Name of the Student

Name of the University

Author Note

CORPORATE AND FINANCIAL ACCOUNTING

Name of the Student

Name of the University

Author Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1ReferencesReferences

Abstract

The main objective of the report is to understand the different owner’s equity elements and

the liabilities elements, recorded in the annual report balance sheet of the two companies.

The two companies chosen for the study is Bega Cheese Limited Company and Bellamy's

Australia Limited. This paper helps to develop the understanding of different sources of

funds that these companies are raising from. It is found that the main source for raising

funds is equity and borrowings for the two companies taken. This report also aims at

developing the concepts of implications in terms of compliance and reporting requirements

among different classifications of entities. A small proprietary company is chosen for

understanding this concept. It was found that the company needs to follow the

requirements and accounting standards before doing any reporting or auditing process.

Abstract

The main objective of the report is to understand the different owner’s equity elements and

the liabilities elements, recorded in the annual report balance sheet of the two companies.

The two companies chosen for the study is Bega Cheese Limited Company and Bellamy's

Australia Limited. This paper helps to develop the understanding of different sources of

funds that these companies are raising from. It is found that the main source for raising

funds is equity and borrowings for the two companies taken. This report also aims at

developing the concepts of implications in terms of compliance and reporting requirements

among different classifications of entities. A small proprietary company is chosen for

understanding this concept. It was found that the company needs to follow the

requirements and accounting standards before doing any reporting or auditing process.

2ReferencesReferences

Table of Contents

Table of Contents..............................................................................................................................2

Introduction........................................................................................................................................3

Part A..................................................................................................................................................4

Part B................................................................................................................................................10

Conclusion........................................................................................................................................13

References.......................................................................................................................................14

Table of Contents

Table of Contents..............................................................................................................................2

Introduction........................................................................................................................................3

Part A..................................................................................................................................................4

Part B................................................................................................................................................10

Conclusion........................................................................................................................................13

References.......................................................................................................................................14

3ReferencesReferences

Introduction

The companies need to raise their funds for expanding their market of the

business. Companies want to earn profits from the undergoing operations of the

organization. Companies seek to various external investors or lenders for raising funds.

Companies, generally raise their funds in the form of debt capital, where they borrow the

money from the lenders in the form of loans. They need to pay a fixed amount of interests

to the lender within a specific period of time. They also raise their funds from equity by

selling a percentage of their shares to the stockholders and raising funds. Other sources

of funds are the retained earnings. The first part of this paper will discuss the various

movements in the items recorded in the owners’ equity section and liabilities section of

Bega Cheese Limited and Bellamy’s Australia limited company. This also discusses the

advantages and disadvantages of the sources of these two companies are raising from.

The second part of this paper discusses understanding the concepts of the three

classifications of entities, and the implications for a small proprietary company in terms of

reporting is explained. The intense of this paper is to understand the different sources of

funds companies are raising and analysis of these sources used by Bega Cheese Limited

and Bellamy’s Australia limited Company. To develop an understanding of the three types

of entities in terms of reporting.

Part A

(i) Owners’ equity section

Items recorded in the owners’ equity section are explained in the following:-

1. Retained Earnings- Retained earnings is the amount of net revenue that any

business has generated after the organization has paid out its dividends to the

Introduction

The companies need to raise their funds for expanding their market of the

business. Companies want to earn profits from the undergoing operations of the

organization. Companies seek to various external investors or lenders for raising funds.

Companies, generally raise their funds in the form of debt capital, where they borrow the

money from the lenders in the form of loans. They need to pay a fixed amount of interests

to the lender within a specific period of time. They also raise their funds from equity by

selling a percentage of their shares to the stockholders and raising funds. Other sources

of funds are the retained earnings. The first part of this paper will discuss the various

movements in the items recorded in the owners’ equity section and liabilities section of

Bega Cheese Limited and Bellamy’s Australia limited company. This also discusses the

advantages and disadvantages of the sources of these two companies are raising from.

The second part of this paper discusses understanding the concepts of the three

classifications of entities, and the implications for a small proprietary company in terms of

reporting is explained. The intense of this paper is to understand the different sources of

funds companies are raising and analysis of these sources used by Bega Cheese Limited

and Bellamy’s Australia limited Company. To develop an understanding of the three types

of entities in terms of reporting.

Part A

(i) Owners’ equity section

Items recorded in the owners’ equity section are explained in the following:-

1. Retained Earnings- Retained earnings is the amount of net revenue that any

business has generated after the organization has paid out its dividends to the

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4ReferencesReferences

shareholders1. This indicates that whenever any company has earned any surplus

income than the portion of income is distributed among the company’s

shareholders.

2. Reserves- Reserves are part of shareholders’ equity, liabilities, or assets. Reserves

are the profits that are incurred by a company and has a credit balance which can

help a business during their legislations2.

3. Share capital- Share capital is the number of funds that any company raises for

issuing the shares; the total amount that is paid initially by the shareholders. They

are of two types: common stock and preferred stocks. Common stock may vary in

amount and have the chance of missing out the shares, depending upon the

certainty of the company's shares. Preferred stocks provide a fixed dividend to the

shareholders, and priorities are given to the ordinary stockholder dividends.

4. Issued capital- This refers to the number of shares that a part of a company’s

certified share is issued the shareholders. Issued shares are the shares that are

agreed by the company’s board of members3.

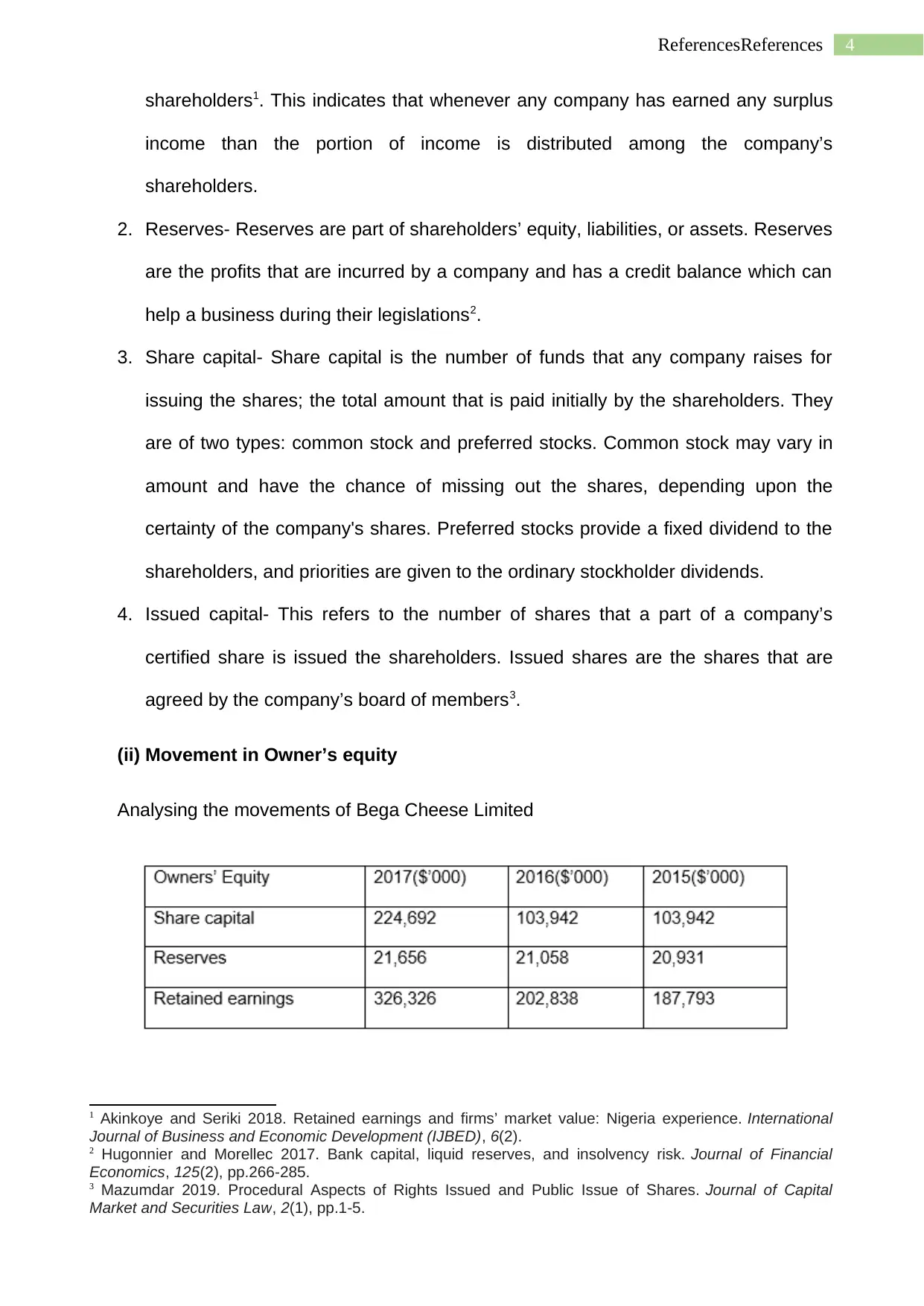

(ii) Movement in Owner’s equity

Analysing the movements of Bega Cheese Limited

1 Akinkoye and Seriki 2018. Retained earnings and firms’ market value: Nigeria experience. International

Journal of Business and Economic Development (IJBED), 6(2).

2 Hugonnier and Morellec 2017. Bank capital, liquid reserves, and insolvency risk. Journal of Financial

Economics, 125(2), pp.266-285.

3 Mazumdar 2019. Procedural Aspects of Rights Issued and Public Issue of Shares. Journal of Capital

Market and Securities Law, 2(1), pp.1-5.

shareholders1. This indicates that whenever any company has earned any surplus

income than the portion of income is distributed among the company’s

shareholders.

2. Reserves- Reserves are part of shareholders’ equity, liabilities, or assets. Reserves

are the profits that are incurred by a company and has a credit balance which can

help a business during their legislations2.

3. Share capital- Share capital is the number of funds that any company raises for

issuing the shares; the total amount that is paid initially by the shareholders. They

are of two types: common stock and preferred stocks. Common stock may vary in

amount and have the chance of missing out the shares, depending upon the

certainty of the company's shares. Preferred stocks provide a fixed dividend to the

shareholders, and priorities are given to the ordinary stockholder dividends.

4. Issued capital- This refers to the number of shares that a part of a company’s

certified share is issued the shareholders. Issued shares are the shares that are

agreed by the company’s board of members3.

(ii) Movement in Owner’s equity

Analysing the movements of Bega Cheese Limited

1 Akinkoye and Seriki 2018. Retained earnings and firms’ market value: Nigeria experience. International

Journal of Business and Economic Development (IJBED), 6(2).

2 Hugonnier and Morellec 2017. Bank capital, liquid reserves, and insolvency risk. Journal of Financial

Economics, 125(2), pp.266-285.

3 Mazumdar 2019. Procedural Aspects of Rights Issued and Public Issue of Shares. Journal of Capital

Market and Securities Law, 2(1), pp.1-5.

5ReferencesReferences

The share investment of the company was 103,942 in both the financial year 2015 and

2016. But the share capital of the company increases to 224,692 during the financial year

2017. This shows that the company has generated more funds for issuing the shares to

the shareholders4. But it may be not good for the shareholders because the increase of

shares may result in a decrease in value to the shareholders. Retained Earnings was

found to be 187,793 in the year 2015 and to 202,838 in the year 2016 and raised to

326.326 in the financial year 2017. This shows, the company has generated more profit in

the past two years. Reserves were found to be 20,931 in the year 2015 and 21,058 in the

year 2016 and increases to 21,656 in the year 2017. This indicates that the company has

generated enough surplus for meeting its obligations.

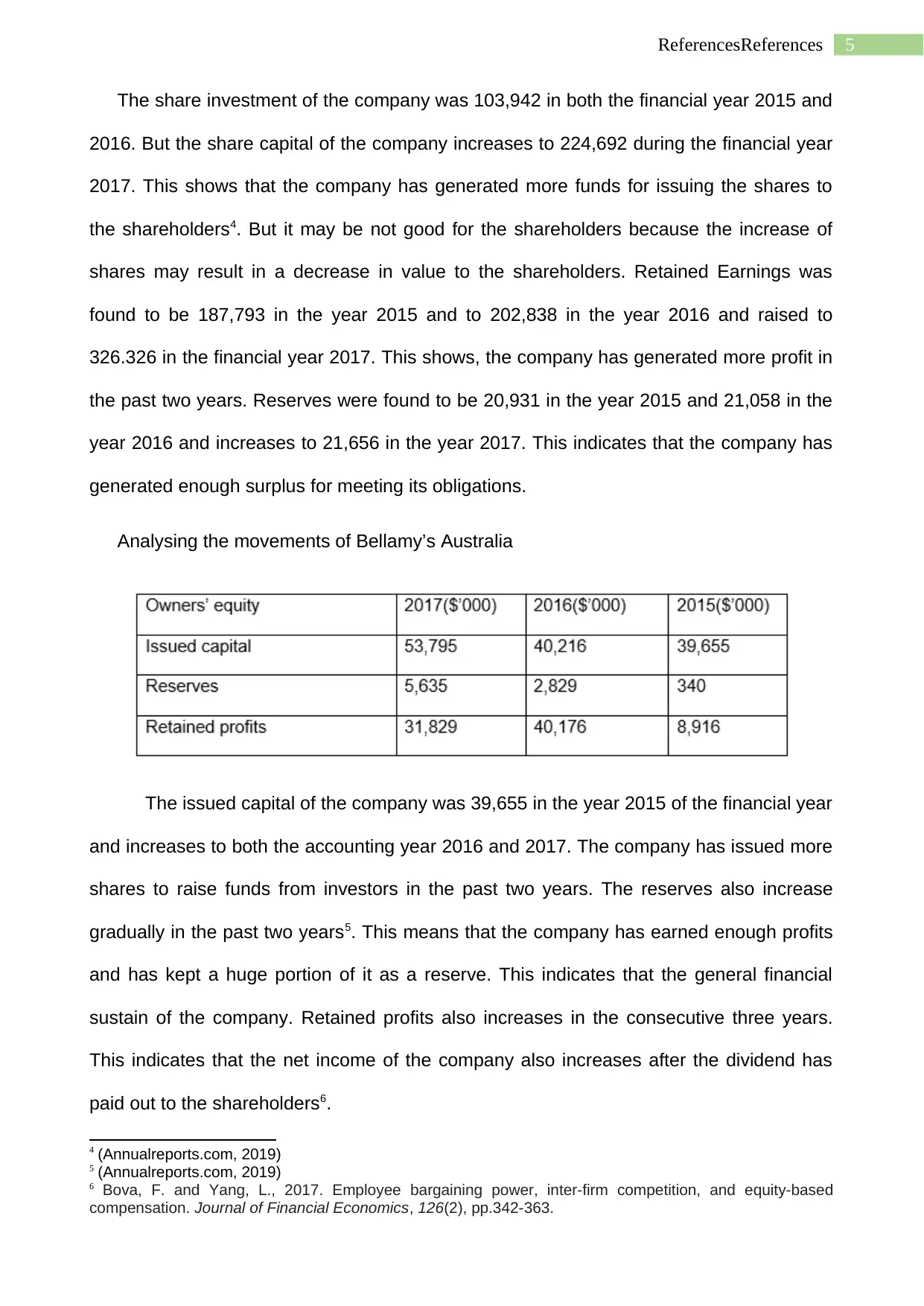

Analysing the movements of Bellamy’s Australia

The issued capital of the company was 39,655 in the year 2015 of the financial year

and increases to both the accounting year 2016 and 2017. The company has issued more

shares to raise funds from investors in the past two years. The reserves also increase

gradually in the past two years5. This means that the company has earned enough profits

and has kept a huge portion of it as a reserve. This indicates that the general financial

sustain of the company. Retained profits also increases in the consecutive three years.

This indicates that the net income of the company also increases after the dividend has

paid out to the shareholders6.

4 (Annualreports.com, 2019)

5 (Annualreports.com, 2019)

6 Bova, F. and Yang, L., 2017. Employee bargaining power, inter-firm competition, and equity-based

compensation. Journal of Financial Economics, 126(2), pp.342-363.

The share investment of the company was 103,942 in both the financial year 2015 and

2016. But the share capital of the company increases to 224,692 during the financial year

2017. This shows that the company has generated more funds for issuing the shares to

the shareholders4. But it may be not good for the shareholders because the increase of

shares may result in a decrease in value to the shareholders. Retained Earnings was

found to be 187,793 in the year 2015 and to 202,838 in the year 2016 and raised to

326.326 in the financial year 2017. This shows, the company has generated more profit in

the past two years. Reserves were found to be 20,931 in the year 2015 and 21,058 in the

year 2016 and increases to 21,656 in the year 2017. This indicates that the company has

generated enough surplus for meeting its obligations.

Analysing the movements of Bellamy’s Australia

The issued capital of the company was 39,655 in the year 2015 of the financial year

and increases to both the accounting year 2016 and 2017. The company has issued more

shares to raise funds from investors in the past two years. The reserves also increase

gradually in the past two years5. This means that the company has earned enough profits

and has kept a huge portion of it as a reserve. This indicates that the general financial

sustain of the company. Retained profits also increases in the consecutive three years.

This indicates that the net income of the company also increases after the dividend has

paid out to the shareholders6.

4 (Annualreports.com, 2019)

5 (Annualreports.com, 2019)

6 Bova, F. and Yang, L., 2017. Employee bargaining power, inter-firm competition, and equity-based

compensation. Journal of Financial Economics, 126(2), pp.342-363.

6ReferencesReferences

(iii)Liabilities section

The two types of liabilities are recorded in the liabilities section of a balance sheet

are current assets and current liabilities:

Current liabilities

1. Trade and other payables- These includes the total amount paid by a business for

purchasing any type of business-related goods or business materials from the

vendors7. The other payables may include short-term debt, expenses, accrued

expenses, wages payable, dividend payables that are recorded in the balance

sheets to identify the expenses related to the company.

2. Borrowings- These are the short term liabilities that a company needs to pay in the

form of loans in the next twelve months to the borrower.

3. Tax liabilities- These are the tax that is due, and the company will pay more income

in the future for the transactions took place at the current period8.

4. Provisions- Provisions are the amount that a company set aside to meet the current

liabilities of a business.

5. Derivative liabilities- These are the financial instruments which are under the

contract becomes due within the specific period than it is classified as a liability.

Non-current liabilities

1. Borrowings- These are the amount of due that a company cannot meet within one year.

These are also known as long term debt of a business.

2. Provisions- These are the amount of money that a company set aside for meeting

the long term employee benefits like gratuity and other termination benefits9.

7 Beck Hoseini and Uras 2018. Trade credit and access to finance of retailers in Ethiopia. DFID Working

Paper.

8 Hamilton, R., 2018. New Evidence on Investors’ Valuation of Deferred Tax Liabilities. Available at SSRN

3304846.

9 Nayak, S., Balakrishnan, V., Ponappa, L.K., Gadiyar, V., Krishnakanth, G.V. and Kanakia, P., 2018.

EQUITY AND LIABILITIES.

(iii)Liabilities section

The two types of liabilities are recorded in the liabilities section of a balance sheet

are current assets and current liabilities:

Current liabilities

1. Trade and other payables- These includes the total amount paid by a business for

purchasing any type of business-related goods or business materials from the

vendors7. The other payables may include short-term debt, expenses, accrued

expenses, wages payable, dividend payables that are recorded in the balance

sheets to identify the expenses related to the company.

2. Borrowings- These are the short term liabilities that a company needs to pay in the

form of loans in the next twelve months to the borrower.

3. Tax liabilities- These are the tax that is due, and the company will pay more income

in the future for the transactions took place at the current period8.

4. Provisions- Provisions are the amount that a company set aside to meet the current

liabilities of a business.

5. Derivative liabilities- These are the financial instruments which are under the

contract becomes due within the specific period than it is classified as a liability.

Non-current liabilities

1. Borrowings- These are the amount of due that a company cannot meet within one year.

These are also known as long term debt of a business.

2. Provisions- These are the amount of money that a company set aside for meeting

the long term employee benefits like gratuity and other termination benefits9.

7 Beck Hoseini and Uras 2018. Trade credit and access to finance of retailers in Ethiopia. DFID Working

Paper.

8 Hamilton, R., 2018. New Evidence on Investors’ Valuation of Deferred Tax Liabilities. Available at SSRN

3304846.

9 Nayak, S., Balakrishnan, V., Ponappa, L.K., Gadiyar, V., Krishnakanth, G.V. and Kanakia, P., 2018.

EQUITY AND LIABILITIES.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ReferencesReferences

(iv) Movement in the liabilities section

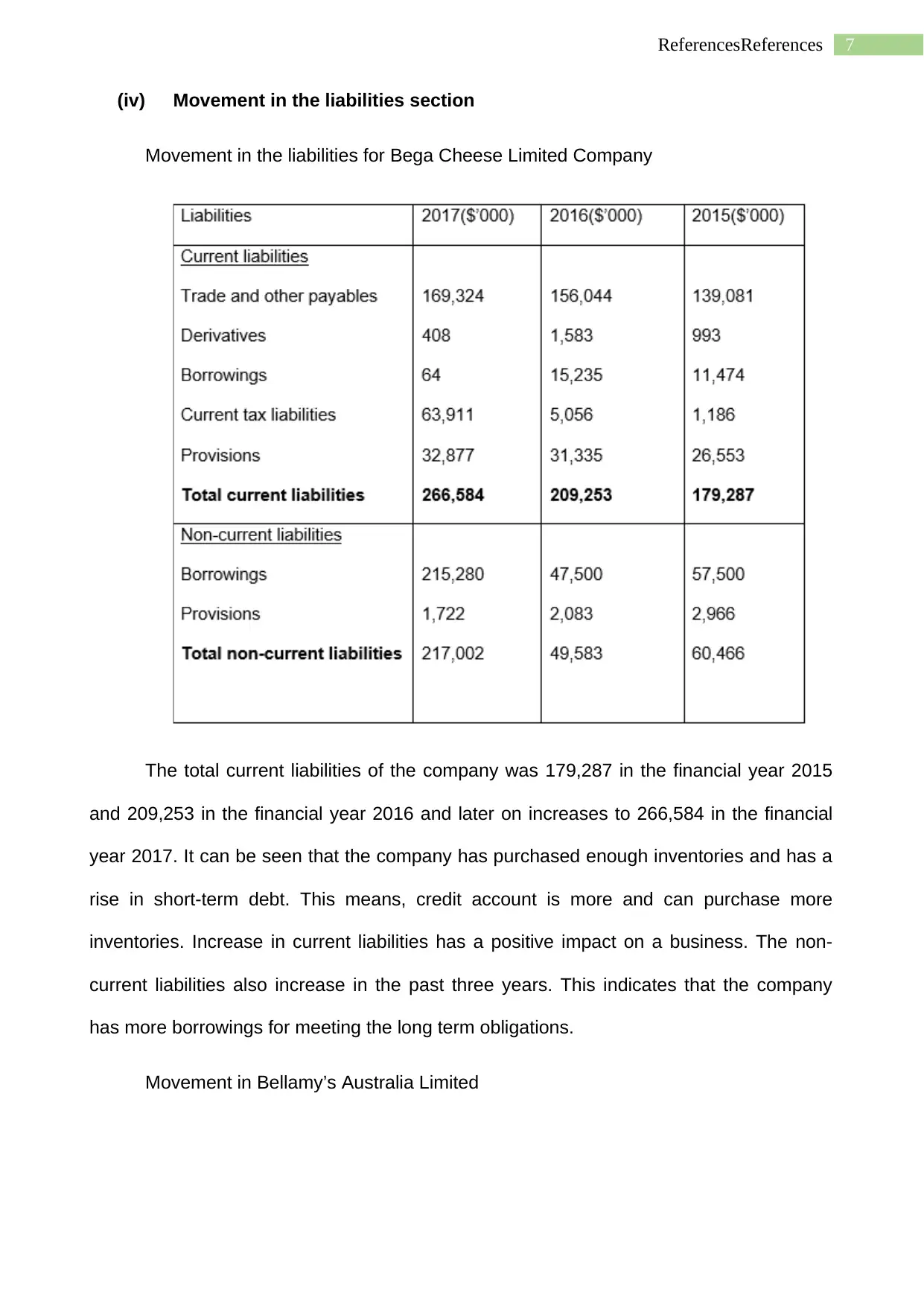

Movement in the liabilities for Bega Cheese Limited Company

The total current liabilities of the company was 179,287 in the financial year 2015

and 209,253 in the financial year 2016 and later on increases to 266,584 in the financial

year 2017. It can be seen that the company has purchased enough inventories and has a

rise in short-term debt. This means, credit account is more and can purchase more

inventories. Increase in current liabilities has a positive impact on a business. The non-

current liabilities also increase in the past three years. This indicates that the company

has more borrowings for meeting the long term obligations.

Movement in Bellamy’s Australia Limited

(iv) Movement in the liabilities section

Movement in the liabilities for Bega Cheese Limited Company

The total current liabilities of the company was 179,287 in the financial year 2015

and 209,253 in the financial year 2016 and later on increases to 266,584 in the financial

year 2017. It can be seen that the company has purchased enough inventories and has a

rise in short-term debt. This means, credit account is more and can purchase more

inventories. Increase in current liabilities has a positive impact on a business. The non-

current liabilities also increase in the past three years. This indicates that the company

has more borrowings for meeting the long term obligations.

Movement in Bellamy’s Australia Limited

8ReferencesReferences

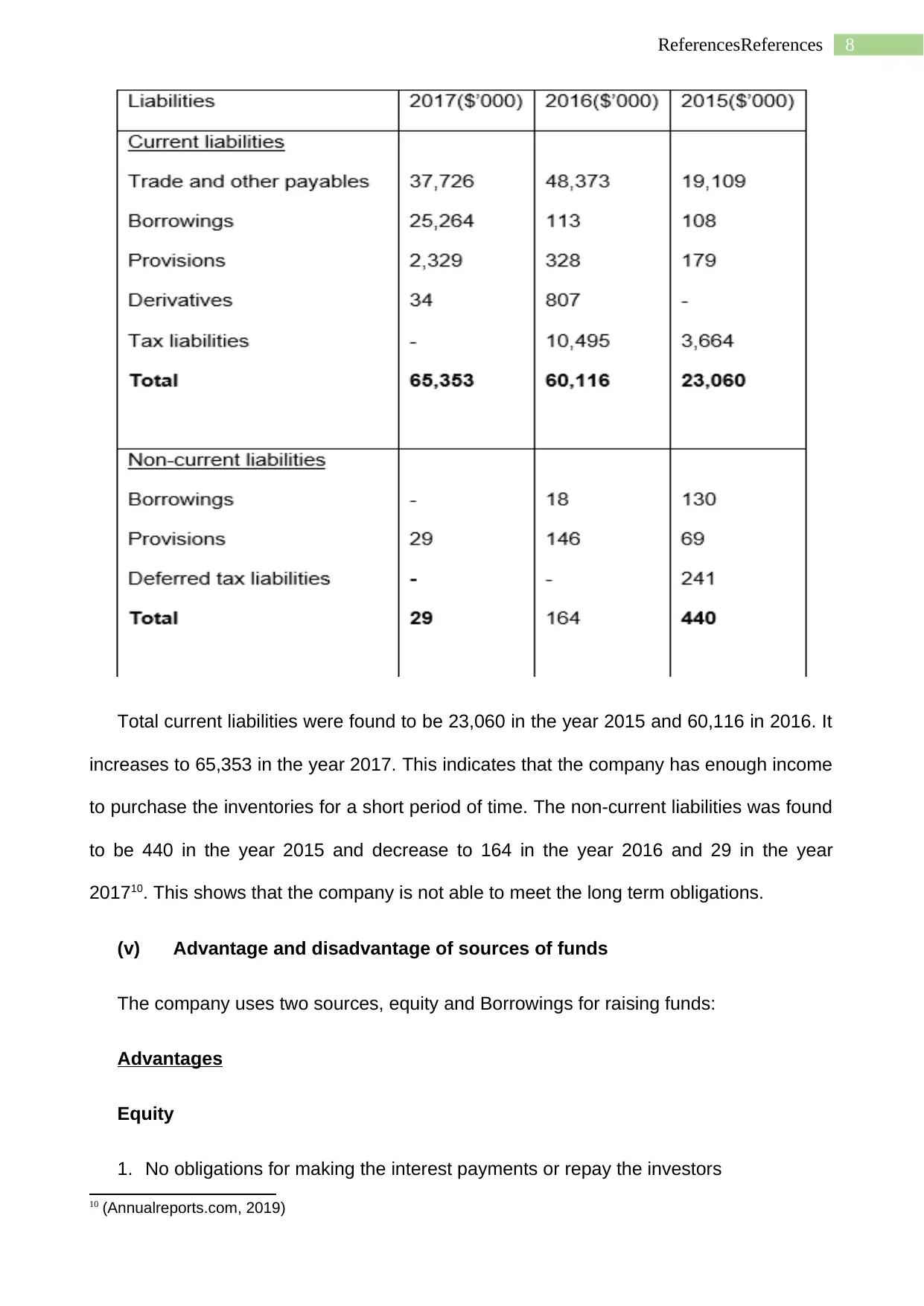

Total current liabilities were found to be 23,060 in the year 2015 and 60,116 in 2016. It

increases to 65,353 in the year 2017. This indicates that the company has enough income

to purchase the inventories for a short period of time. The non-current liabilities was found

to be 440 in the year 2015 and decrease to 164 in the year 2016 and 29 in the year

201710. This shows that the company is not able to meet the long term obligations.

(v) Advantage and disadvantage of sources of funds

The company uses two sources, equity and Borrowings for raising funds:

Advantages

Equity

1. No obligations for making the interest payments or repay the investors

10 (Annualreports.com, 2019)

Total current liabilities were found to be 23,060 in the year 2015 and 60,116 in 2016. It

increases to 65,353 in the year 2017. This indicates that the company has enough income

to purchase the inventories for a short period of time. The non-current liabilities was found

to be 440 in the year 2015 and decrease to 164 in the year 2016 and 29 in the year

201710. This shows that the company is not able to meet the long term obligations.

(v) Advantage and disadvantage of sources of funds

The company uses two sources, equity and Borrowings for raising funds:

Advantages

Equity

1. No obligations for making the interest payments or repay the investors

10 (Annualreports.com, 2019)

9ReferencesReferences

2. Lower risks of bankruptcy.

3. Can bring a new equity partner. They can secure more debt if required in the future.

4. No obligations for paying fixed dividends

Borrowings

1. It helps to meet the related cash obligations in a longer period of time.

2. The rate of interest on the capital borrowed is fixed.

3. Creditors cannot have control or interfere in the management of the company11.

Disadvantages

Equity

1. The investors demand a higher rate of return on their investments for acquiring

more risks towards investments12.

2. Process takes more time starting from the application process to securing equity.13

This takes more effort to get the required equity.

3. Equity share value depends on bidding and can cause the formation of groups or

any kind of proxy rights.

Borrowings

1. The company has to pay interest on the amount borrowed irrespective of profits or

loss.

2. The company can be bankrupt when the profit goes down14.

11 Dhanabhakyam, M., and Shobanageetha, K., 2017. Cost benefit analysis of State Bank of India and its

associates. IJAR, 3(5), pp.463-470.

12 Kim, Y.B., An, H.T. and Kim, J.D., 2015. The effect of carbon risk on the cost of equity capital. Journal of

Cleaner Production, 93, pp.279-287.

13 Nayak, S., Balakrishnan, V., Ponappa, L.K., Gadiyar, V., Krishnakanth, G.V. and Kanakia, P., 2018.

EQUITY AND LIABILITIES.

14 Amahalu, N., Abiahu, M.F.C., Nweze, C. and Chinyere, O., 2017. Effect of corporate governance on

borrowing the cost of quoted brewery firms in Nigeria (2010-2015). EPH-International Journal of Business &

Management Science, 2(3), pp.31-57.

2. Lower risks of bankruptcy.

3. Can bring a new equity partner. They can secure more debt if required in the future.

4. No obligations for paying fixed dividends

Borrowings

1. It helps to meet the related cash obligations in a longer period of time.

2. The rate of interest on the capital borrowed is fixed.

3. Creditors cannot have control or interfere in the management of the company11.

Disadvantages

Equity

1. The investors demand a higher rate of return on their investments for acquiring

more risks towards investments12.

2. Process takes more time starting from the application process to securing equity.13

This takes more effort to get the required equity.

3. Equity share value depends on bidding and can cause the formation of groups or

any kind of proxy rights.

Borrowings

1. The company has to pay interest on the amount borrowed irrespective of profits or

loss.

2. The company can be bankrupt when the profit goes down14.

11 Dhanabhakyam, M., and Shobanageetha, K., 2017. Cost benefit analysis of State Bank of India and its

associates. IJAR, 3(5), pp.463-470.

12 Kim, Y.B., An, H.T. and Kim, J.D., 2015. The effect of carbon risk on the cost of equity capital. Journal of

Cleaner Production, 93, pp.279-287.

13 Nayak, S., Balakrishnan, V., Ponappa, L.K., Gadiyar, V., Krishnakanth, G.V. and Kanakia, P., 2018.

EQUITY AND LIABILITIES.

14 Amahalu, N., Abiahu, M.F.C., Nweze, C. and Chinyere, O., 2017. Effect of corporate governance on

borrowing the cost of quoted brewery firms in Nigeria (2010-2015). EPH-International Journal of Business &

Management Science, 2(3), pp.31-57.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10ReferencesReferences

3. Sometimes the creditors may put conditions in use of funds. This may cause

problems for the owners for flexibility in using the funds.

Part B

Small proprietary companies

Small proprietary companies are the entities which are not controlled by any foreign

companies whose revenue is $25 million or greater than that in the counted financial year

and the company’s gross assets should be $12.5 million or greater than that. And the

number of employees in the organization must be less than 5015.

Large proprietary companies

A large proprietary enterprise is one whose profits for the financial year is more

than $50 million, and the value of gross assets is more than $25million. The company

needs to have at least 100 employees in the organization16. Large proprietary

organizations must have to formulate the annual financial reports and have to direct the

report for each and every financial year17. The accounts must be audited by the relief of

ASIC. If the following conditions are not satisfied, then the company will be known as a

small proprietary organization.

Reporting entities

Reporting entity is the entity where it is necessary for the users to prepare the

annual reports18.The annual reports will help the users to understand the financial situation

of the entity and make the business-related decisions on the base of the important

financial information.

15 Mittal, S., Khan, M.A., Romero, D. and Wuest, T., 2018. A critical review of smart manufacturing & Industry

4.0 maturity models: Implications for small and medium-sized enterprises (SMEs). Journal of manufacturing

systems, 49, pp.194-214.

16 och Dag, J.N., Regnell, B., Gervasi, V. and Brinkkemper, S., 2005. A linguistic-engineering approach to

large-scale requirements management. IEEE software, 22(1), pp.32-39.

17 Downes, S., 2015. Integrated Reporting. GAAP Consulting, pp.1-4.

18 Cohen, S., and Karatzimas, S., 2015. Tracing the future of reporting in the public sector: introducing

integrated popular reporting. International Journal of Public Sector Management, 28(6), pp.449-460.

3. Sometimes the creditors may put conditions in use of funds. This may cause

problems for the owners for flexibility in using the funds.

Part B

Small proprietary companies

Small proprietary companies are the entities which are not controlled by any foreign

companies whose revenue is $25 million or greater than that in the counted financial year

and the company’s gross assets should be $12.5 million or greater than that. And the

number of employees in the organization must be less than 5015.

Large proprietary companies

A large proprietary enterprise is one whose profits for the financial year is more

than $50 million, and the value of gross assets is more than $25million. The company

needs to have at least 100 employees in the organization16. Large proprietary

organizations must have to formulate the annual financial reports and have to direct the

report for each and every financial year17. The accounts must be audited by the relief of

ASIC. If the following conditions are not satisfied, then the company will be known as a

small proprietary organization.

Reporting entities

Reporting entity is the entity where it is necessary for the users to prepare the

annual reports18.The annual reports will help the users to understand the financial situation

of the entity and make the business-related decisions on the base of the important

financial information.

15 Mittal, S., Khan, M.A., Romero, D. and Wuest, T., 2018. A critical review of smart manufacturing & Industry

4.0 maturity models: Implications for small and medium-sized enterprises (SMEs). Journal of manufacturing

systems, 49, pp.194-214.

16 och Dag, J.N., Regnell, B., Gervasi, V. and Brinkkemper, S., 2005. A linguistic-engineering approach to

large-scale requirements management. IEEE software, 22(1), pp.32-39.

17 Downes, S., 2015. Integrated Reporting. GAAP Consulting, pp.1-4.

18 Cohen, S., and Karatzimas, S., 2015. Tracing the future of reporting in the public sector: introducing

integrated popular reporting. International Journal of Public Sector Management, 28(6), pp.449-460.

11ReferencesReferences

Implications for small proprietary companies:

In terms of compliance in accounting standards- The accounting standards for

preparing an annual report are made by Australian Accounting Standards (AASB). It is not

compulsory for a small proprietary company to prepare the annual reports of the company

as per section 292(2). The company is directed to do annual reporting if:

It is directed and mentioned to do under the sec 293 as per shareholders

direction19. That means the direction needs to be signed by the shareholders and

section 294 as per the ASIC(Australian Securities and Investments Commission)

The firm needs to be incorporated by a foreign company.

In terms of reporting requirements- A small proprietary enterprise is not necessary to

formulate a financial report under the corporation act unless it is controlled by any foreign

company. The financial report is essential to be done, when the entity satisfies the

subsequent two conditions:

1. The total returns of the entity is more than the amount $25 million at the relevant

financial year

2. The gross assets value is more than $12.5 million in the commercial year

3. The total number of employees working in the organization is more than 50.

If the enterprise does not see the above principles, then the companies are referred to

as a small proprietorship and cannot prepare financial reports.

In terms of Auditing- Following are certain implications for a small proprietary

company to get an audit relief. The auditing relief for a small company is available

when the company is a foreign-controlled company and has a holding company. When

the shareholders direct that audit is not required in the company20. When the ASIC

19 Stubbs, W. and Higgins, C., 2018. Stakeholders’ perspectives on the role of regulatory reform in integrated

reporting. Journal of Business Ethics, 147(3), pp.489-508.

20 Glover, S.M., Taylor, M.H. and Wu, Y.J., 2016. Current practices and challenges in auditing fair value

measurements and complex estimates: Implications for auditing standards and the academy. Auditing: A

Implications for small proprietary companies:

In terms of compliance in accounting standards- The accounting standards for

preparing an annual report are made by Australian Accounting Standards (AASB). It is not

compulsory for a small proprietary company to prepare the annual reports of the company

as per section 292(2). The company is directed to do annual reporting if:

It is directed and mentioned to do under the sec 293 as per shareholders

direction19. That means the direction needs to be signed by the shareholders and

section 294 as per the ASIC(Australian Securities and Investments Commission)

The firm needs to be incorporated by a foreign company.

In terms of reporting requirements- A small proprietary enterprise is not necessary to

formulate a financial report under the corporation act unless it is controlled by any foreign

company. The financial report is essential to be done, when the entity satisfies the

subsequent two conditions:

1. The total returns of the entity is more than the amount $25 million at the relevant

financial year

2. The gross assets value is more than $12.5 million in the commercial year

3. The total number of employees working in the organization is more than 50.

If the enterprise does not see the above principles, then the companies are referred to

as a small proprietorship and cannot prepare financial reports.

In terms of Auditing- Following are certain implications for a small proprietary

company to get an audit relief. The auditing relief for a small company is available

when the company is a foreign-controlled company and has a holding company. When

the shareholders direct that audit is not required in the company20. When the ASIC

19 Stubbs, W. and Higgins, C., 2018. Stakeholders’ perspectives on the role of regulatory reform in integrated

reporting. Journal of Business Ethics, 147(3), pp.489-508.

20 Glover, S.M., Taylor, M.H. and Wu, Y.J., 2016. Current practices and challenges in auditing fair value

measurements and complex estimates: Implications for auditing standards and the academy. Auditing: A

12ReferencesReferences

state that the small proprietary company is properly managed and has a definite

financial condition. The company's financial report has been compiled by an

accountant and the company21.

Conclusion

Therefore, from the above report, it is found that the main sources of funds raised by a

company are equity capital, debt capital, and the retained earnings. It is found that the

companies chosen for the study mainly uses equity and borrowings as a source of funds

to raise their funds and help the business to increase its profitability and expand the

market. From the movement’s owners’ equity and liabilities of the two companies for the

three financial years 2015, 2016 and 2017, it is found that both the companies have

maintained a good use of money in investments and has generated profit. The company is

in a good financial position for the past three financial year period. From the later part, it is

also found that the small proprietary enterprise cannot prepare a yearly financial report

unless it is incorporated by a foreign company and is directed by the shareholders. A

small proprietary enterprise needs to monitor certain criteria of the annual report

mentioned by section 292(2). Large proprietary company is allowed to formulate the yearly

financial report because it follows the major criteria under section 292(2) and the reporting

entities must have to report the annual financial report for understanding the financial

position of the company.

Journal of Practice & Theory, 36(1), pp.63-84.

21 Sankara, J., Lindberg, D.L. and Razaki, K.A., 2015. Conflict minerals disclosures: reporting requirements

and implications for auditing. Current Issues in Auditing, 10(1), pp.A1-A23.

state that the small proprietary company is properly managed and has a definite

financial condition. The company's financial report has been compiled by an

accountant and the company21.

Conclusion

Therefore, from the above report, it is found that the main sources of funds raised by a

company are equity capital, debt capital, and the retained earnings. It is found that the

companies chosen for the study mainly uses equity and borrowings as a source of funds

to raise their funds and help the business to increase its profitability and expand the

market. From the movement’s owners’ equity and liabilities of the two companies for the

three financial years 2015, 2016 and 2017, it is found that both the companies have

maintained a good use of money in investments and has generated profit. The company is

in a good financial position for the past three financial year period. From the later part, it is

also found that the small proprietary enterprise cannot prepare a yearly financial report

unless it is incorporated by a foreign company and is directed by the shareholders. A

small proprietary enterprise needs to monitor certain criteria of the annual report

mentioned by section 292(2). Large proprietary company is allowed to formulate the yearly

financial report because it follows the major criteria under section 292(2) and the reporting

entities must have to report the annual financial report for understanding the financial

position of the company.

Journal of Practice & Theory, 36(1), pp.63-84.

21 Sankara, J., Lindberg, D.L. and Razaki, K.A., 2015. Conflict minerals disclosures: reporting requirements

and implications for auditing. Current Issues in Auditing, 10(1), pp.A1-A23.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13ReferencesReferences

References

Akinkoye E.Y. and Seriki, A.I., 2018. Retained earnings and firms’ market value: Nigeria

experience. International Journal of Business and Economic Development (IJBED), 6(2).

Annualreports.com (2019). Bega Cheese Ltd - AnnualReports.com. [online]

Annualreports.com. Available at: http://www.annualreports.com/Company/bega-cheese-

ltd [Accessed 25 Sep. 2019].

Annualreports.com (2019). Bellamy's Australia Ltd - AnnualReports.com. [online]

Annualreports.com. Available at: http://www.annualreports.com/Company/Bellamys-

AustraliaLtd [Accessed 25 Sep. 2019].

Beck, T., Hoseini, M. and Uras, B., 2018. Trade credit and access to finance of retailers

in Ethiopia. DFID Working Paper.

Bova, F. and Yang, L., 2017. Employee bargaining power, inter-firm competition, and

equity-based compensation. Journal of Financial Economics, 126(2), pp.342-363.

Cohen, S. and karatzimas, S., 2015. Tracing the future of reporting in the public sector:

introducing integrated popular reporting. International Journal of Public Sector

Management, 28(6), pp.449-460.

Dhanabakhyam M. and shobangeeta, K., 2017. Cost benefit analysis of State Bank of

India and its associates. IJAR, 3(5), pp.463-470.

Downes, S., 2015. Integrated Reporting. GAAP Consulting, pp.1-4.

Glover, S.M., Taylor, M.H. and Wu, Y.J., 2016. Current practices and challenges in

auditing fair value measurements and complex estimates: Implications for auditing

standards and the academy. Auditing: A Journal of Practice & Theory, 36(1), pp.63-84.

References

Akinkoye E.Y. and Seriki, A.I., 2018. Retained earnings and firms’ market value: Nigeria

experience. International Journal of Business and Economic Development (IJBED), 6(2).

Annualreports.com (2019). Bega Cheese Ltd - AnnualReports.com. [online]

Annualreports.com. Available at: http://www.annualreports.com/Company/bega-cheese-

ltd [Accessed 25 Sep. 2019].

Annualreports.com (2019). Bellamy's Australia Ltd - AnnualReports.com. [online]

Annualreports.com. Available at: http://www.annualreports.com/Company/Bellamys-

AustraliaLtd [Accessed 25 Sep. 2019].

Beck, T., Hoseini, M. and Uras, B., 2018. Trade credit and access to finance of retailers

in Ethiopia. DFID Working Paper.

Bova, F. and Yang, L., 2017. Employee bargaining power, inter-firm competition, and

equity-based compensation. Journal of Financial Economics, 126(2), pp.342-363.

Cohen, S. and karatzimas, S., 2015. Tracing the future of reporting in the public sector:

introducing integrated popular reporting. International Journal of Public Sector

Management, 28(6), pp.449-460.

Dhanabakhyam M. and shobangeeta, K., 2017. Cost benefit analysis of State Bank of

India and its associates. IJAR, 3(5), pp.463-470.

Downes, S., 2015. Integrated Reporting. GAAP Consulting, pp.1-4.

Glover, S.M., Taylor, M.H. and Wu, Y.J., 2016. Current practices and challenges in

auditing fair value measurements and complex estimates: Implications for auditing

standards and the academy. Auditing: A Journal of Practice & Theory, 36(1), pp.63-84.

14ReferencesReferences

Hamilton, R., 2018. New Evidence on Investors’ Valuation of Deferred Tax

Liabilities. Available at SSRN 3304846.

Hugonniew, J. and Morellac, E., 2017. Bank capital, liquid reserves, and insolvency

risk. Journal of Financial Economics, 125(2), pp.266-285.

Kim, Y.B., An, H.T. and Kim, J.D., 2015. The effect of carbon risk on the cost of equity

capital. Journal of Cleaner Production, 93, pp.279-287.

Mazumdar, S., 2019. Procedural Aspects of Rights Issued and Public Issue of

Shares. Journal of Capital Market and Securities Law, 2(1), pp.1-5.

Michael, N., Abiahu, M.F.C., Nweze, C. and Chinyere, O., 2017. Effect of corporate

governance on borrowing cost of quoted brewery firms in Nigeria (2010-2015). EPH-

International Journal of Business & Management Science, 2(3), pp.31-57.

Mittal, S., Khan, M.A., Romero, D. and Wuest, T., 2018. A critical review of smart

manufacturing & Industry 4.0 maturity models: Implications for small and medium-sized

enterprises (SMEs). Journal of manufacturing systems, 49, pp.194-214.

Nayak, S., Balakrishnan, V., Ponappa, L.K., Gadiyar, V., Krishnakanth, G.V. and

Kanakia, P., 2018. EQUITY AND LIABILITIES.

Nayak, S., Balakrishnan, V., Ponappa, L.K., Gadiyar, V., Krishnakanth, G.V. and

Kanakia, P., 2018. EQUITY AND LIABILITIES.

och Dag, J.N., Regnell, B., Gervasi, V. and Brinkkemper, S., 2005. A linguistic-

engineering approach to large-scale requirements management. IEEE software, 22(1),

pp.32-39.

Sankara, J., Lindberg, D.L. and Razaki, K.A., 2015. Conflict minerals disclosures:

reporting requirements and implications for auditing. Current Issues in Auditing, 10(1),

pp.A1-A23.

Hamilton, R., 2018. New Evidence on Investors’ Valuation of Deferred Tax

Liabilities. Available at SSRN 3304846.

Hugonniew, J. and Morellac, E., 2017. Bank capital, liquid reserves, and insolvency

risk. Journal of Financial Economics, 125(2), pp.266-285.

Kim, Y.B., An, H.T. and Kim, J.D., 2015. The effect of carbon risk on the cost of equity

capital. Journal of Cleaner Production, 93, pp.279-287.

Mazumdar, S., 2019. Procedural Aspects of Rights Issued and Public Issue of

Shares. Journal of Capital Market and Securities Law, 2(1), pp.1-5.

Michael, N., Abiahu, M.F.C., Nweze, C. and Chinyere, O., 2017. Effect of corporate

governance on borrowing cost of quoted brewery firms in Nigeria (2010-2015). EPH-

International Journal of Business & Management Science, 2(3), pp.31-57.

Mittal, S., Khan, M.A., Romero, D. and Wuest, T., 2018. A critical review of smart

manufacturing & Industry 4.0 maturity models: Implications for small and medium-sized

enterprises (SMEs). Journal of manufacturing systems, 49, pp.194-214.

Nayak, S., Balakrishnan, V., Ponappa, L.K., Gadiyar, V., Krishnakanth, G.V. and

Kanakia, P., 2018. EQUITY AND LIABILITIES.

Nayak, S., Balakrishnan, V., Ponappa, L.K., Gadiyar, V., Krishnakanth, G.V. and

Kanakia, P., 2018. EQUITY AND LIABILITIES.

och Dag, J.N., Regnell, B., Gervasi, V. and Brinkkemper, S., 2005. A linguistic-

engineering approach to large-scale requirements management. IEEE software, 22(1),

pp.32-39.

Sankara, J., Lindberg, D.L. and Razaki, K.A., 2015. Conflict minerals disclosures:

reporting requirements and implications for auditing. Current Issues in Auditing, 10(1),

pp.A1-A23.

15ReferencesReferences

Stubbs, W. and Higgins, C., 2018. Stakeholders’ perspectives on the role of regulatory

reform in integrated reporting. Journal of Business Ethics, 147(3), pp.489-508.

Stubbs, W. and Higgins, C., 2018. Stakeholders’ perspectives on the role of regulatory

reform in integrated reporting. Journal of Business Ethics, 147(3), pp.489-508.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.