Kidman Resources: Capital Budgeting and Investment Decision Report

VerifiedAdded on 2023/01/16

|11

|1676

|44

Report

AI Summary

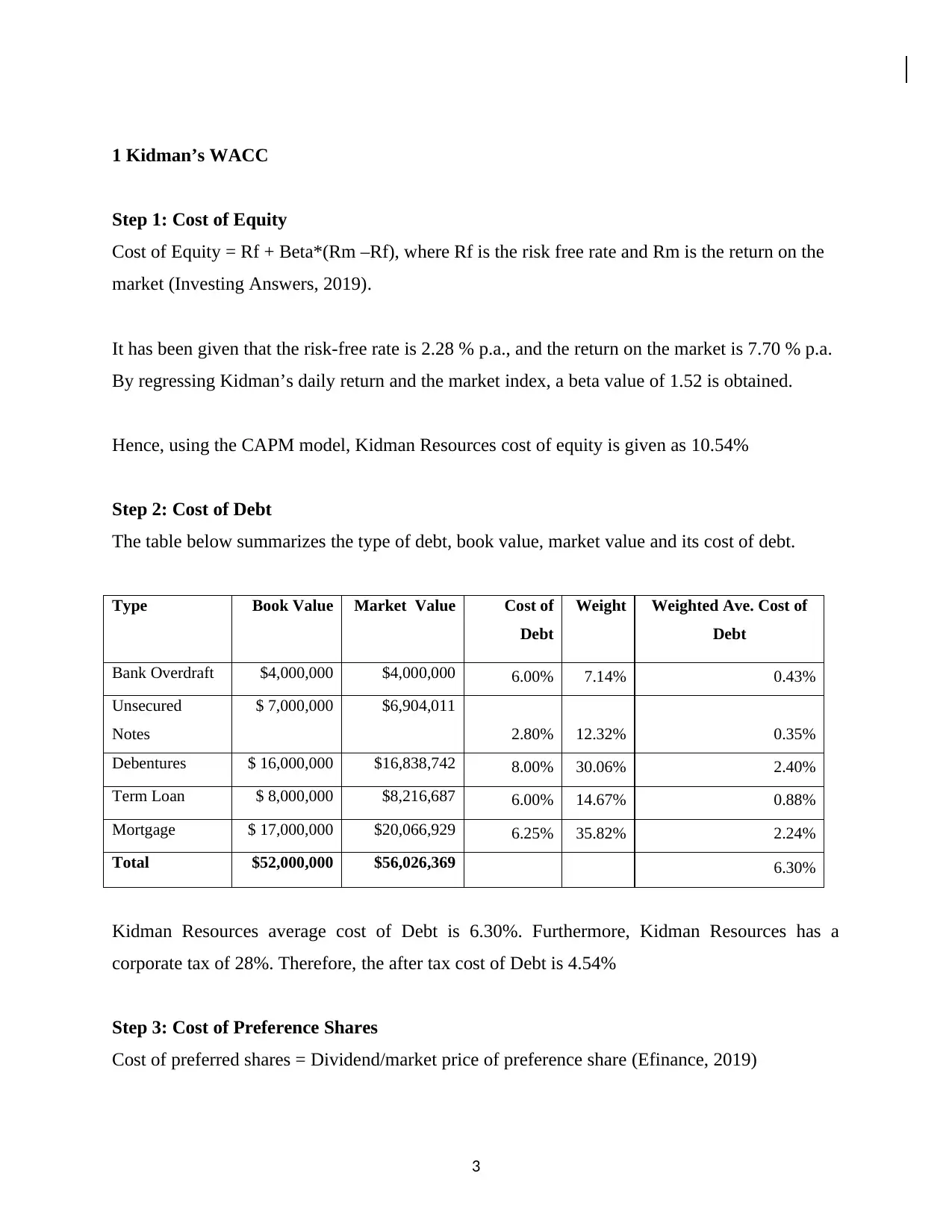

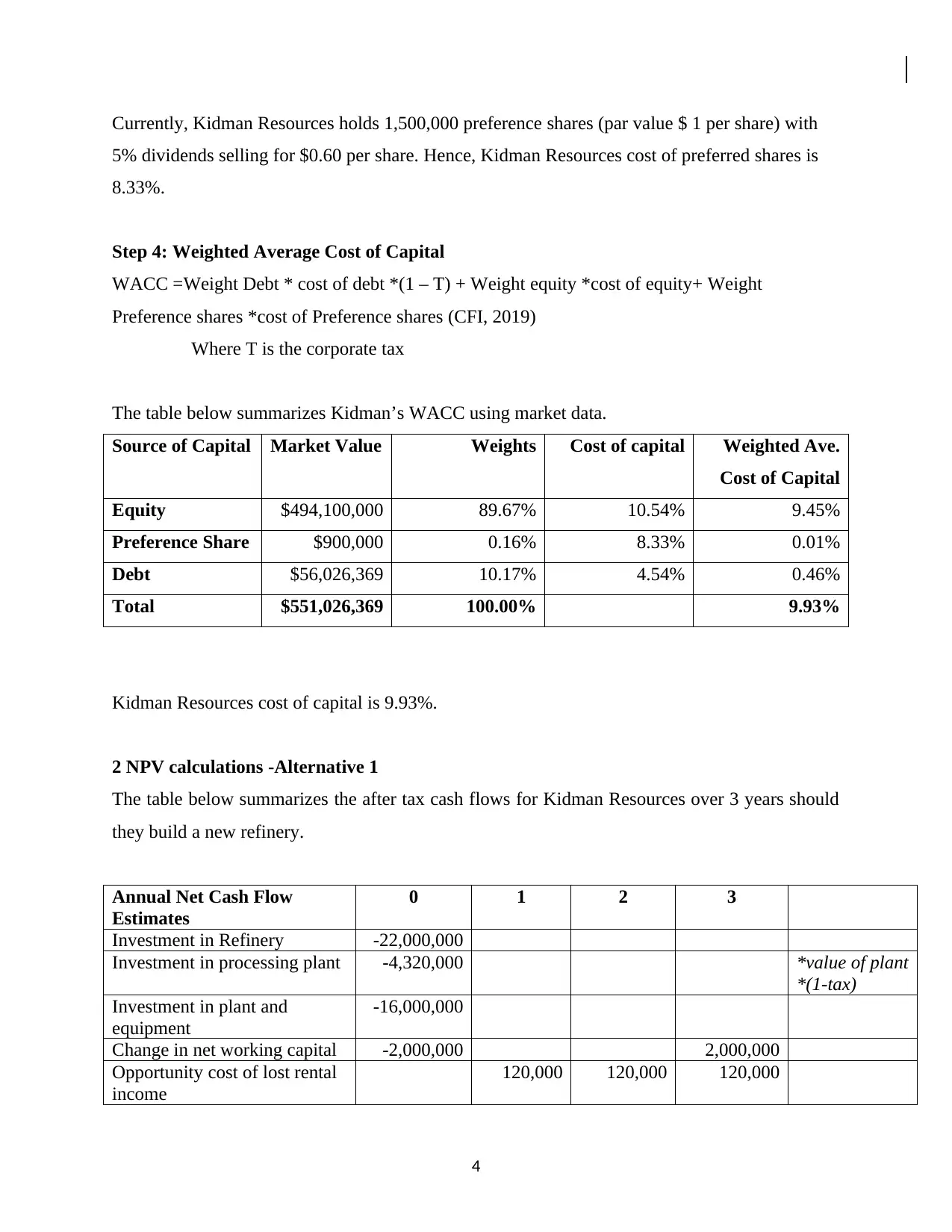

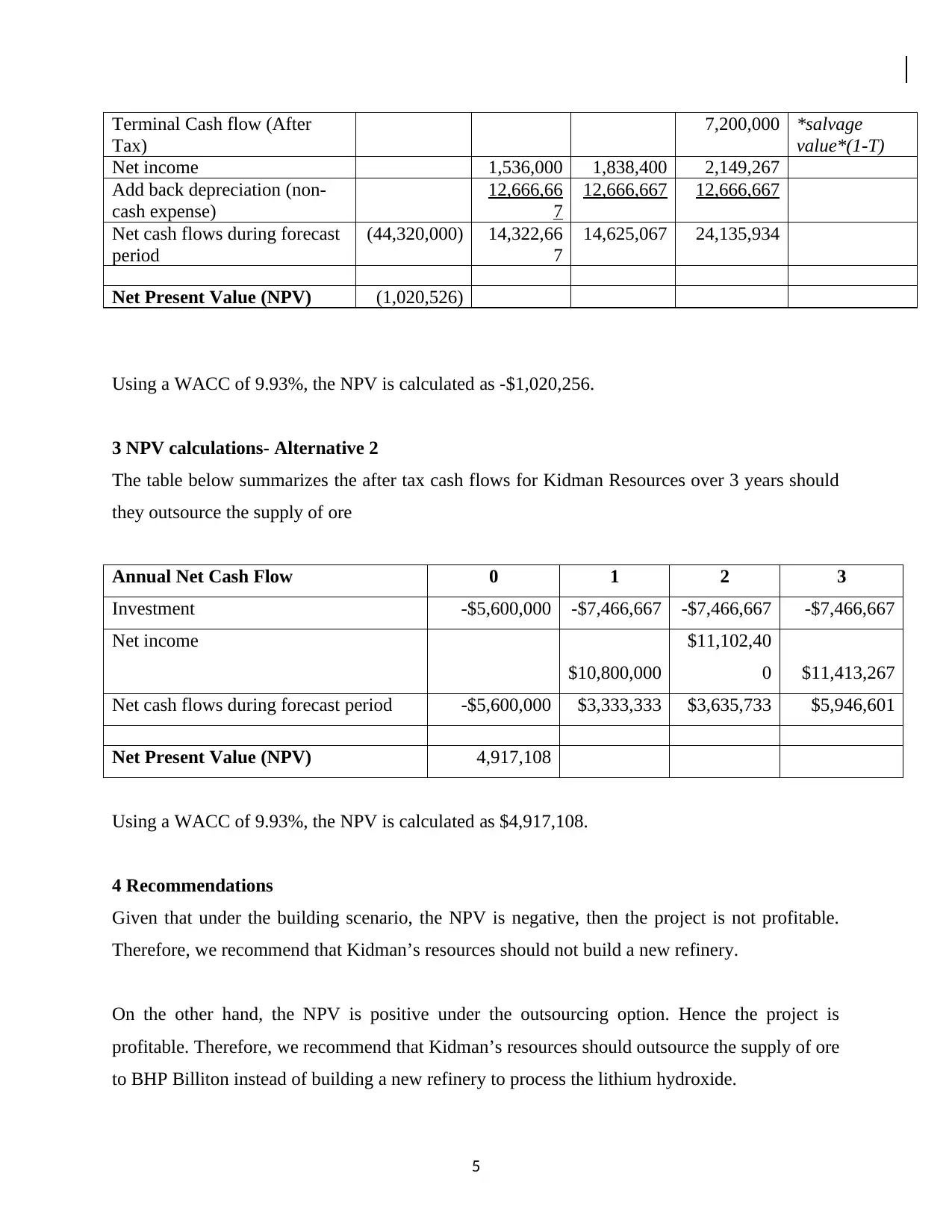

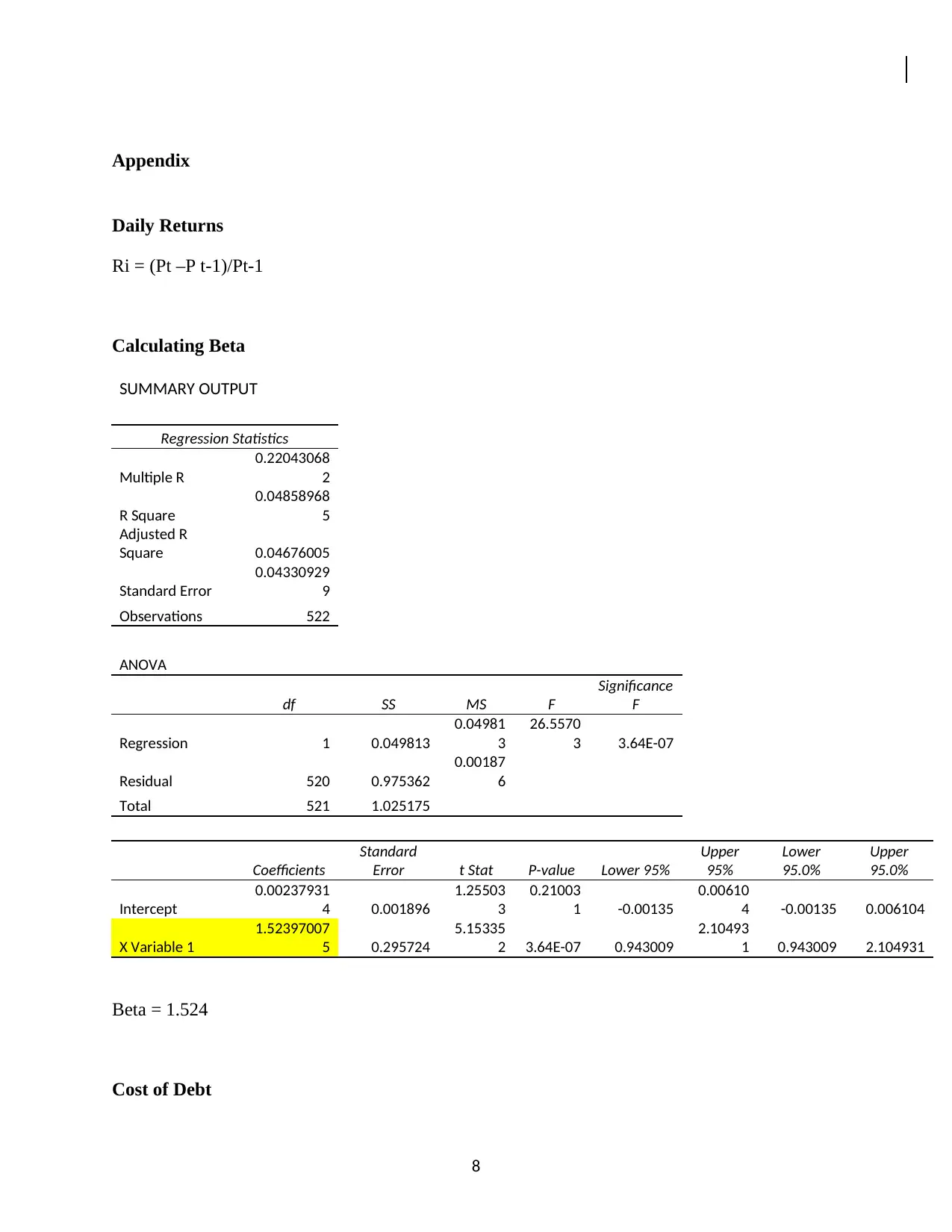

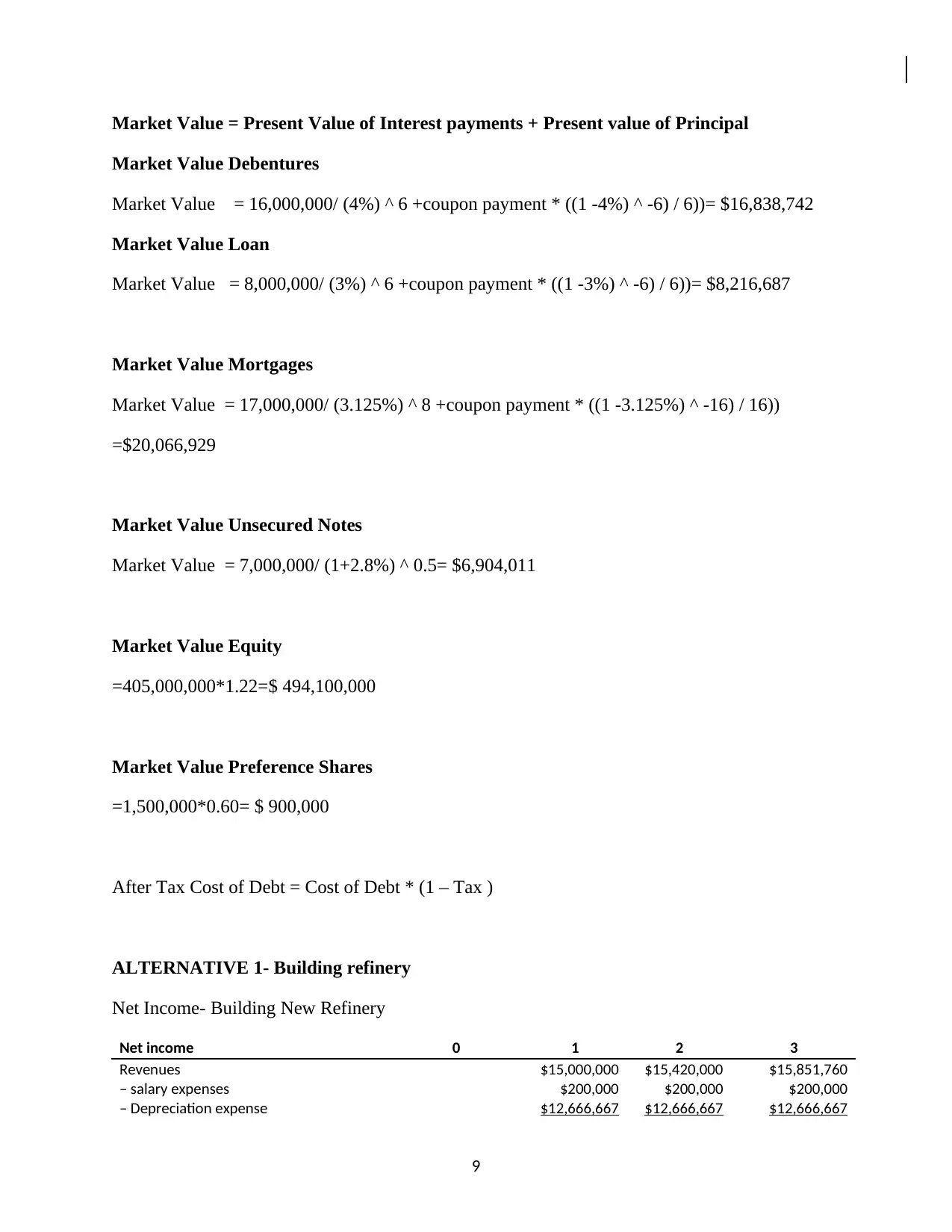

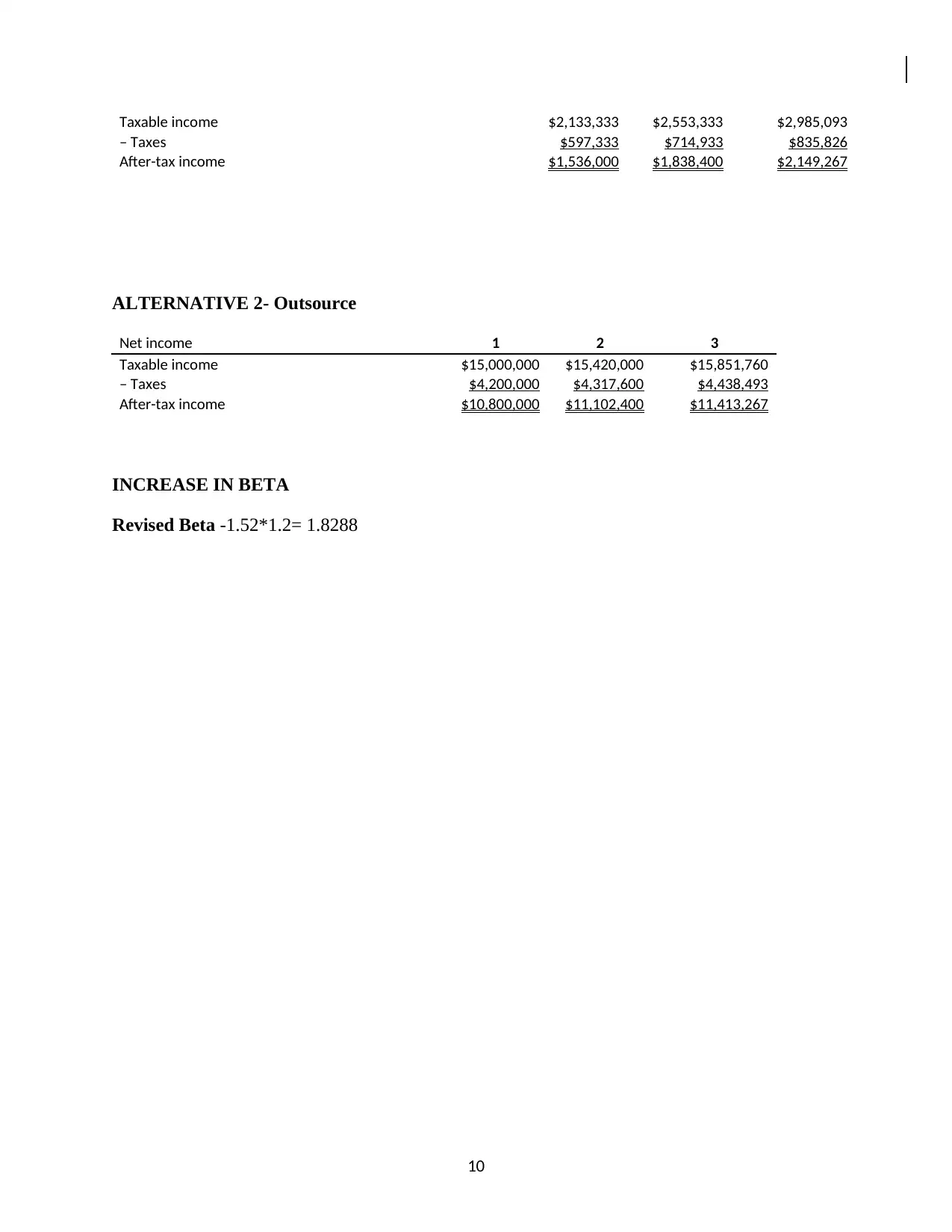

This report provides a comprehensive financial analysis of Kidman Resources, focusing on capital budgeting decisions related to a potential lithium hydroxide supply agreement with Tesla. The analysis begins with the calculation of Kidman Resources' Weighted Average Cost of Capital (WACC), considering the cost of equity, debt, and preference shares. The report then evaluates two investment alternatives: building a new refinery and outsourcing the supply of ore. Net Present Value (NPV) calculations are performed for each option, considering cash flows over a three-year period. The report recommends outsourcing the supply of ore, as the NPV is positive, while the NPV for building a new refinery is negative. The report also includes an analysis of beta risk, exploring how changes in beta would impact the WACC and NPV calculations, and provides references and appendices with supporting data.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.