Finance in Hospitality: Strategies for Financial Management and Growth

VerifiedAdded on 2019/12/03

|21

|6145

|161

Report

AI Summary

This report provides an in-depth analysis of financial planning within the hospitality sector. It covers various sources of funding, including bank loans, equity capital, retained earnings, and debentures. The report also examines methods of generating income, such as product development, market expansion, and franchising. Key elements of cost, gross profit percentages, and techniques for controlling stock and cash, including EOQ, JIT, and cash control methods, are discussed. Furthermore, it delves into budgetary control, including its process and purpose, with a variance analysis example. The report includes trial balance analysis, business accounts adjustments, and ratio analysis, offering recommendations for future management strategies. Finally, the report explores cost classifications and break-even analysis to provide a comprehensive overview of financial management in the hospitality industry.

Finance in hospitality

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction................................................................................................................................1

Task 1.........................................................................................................................................1

1.1 Sources of funding within business and service industry................................................1

1.2 Methods of generating income for a large chain of restaurants.......................................2

Task 2.........................................................................................................................................2

2.1 Elements of cost, gross profit percentages.......................................................................2

2.2 Methods of controlling stock and cash in a business and service environment...............3

Task 3.........................................................................................................................................4

3.3 Process and purpose of budgetary control.......................................................................4

3.4 Variance analysis of Yuri’s budget..................................................................................5

Task 4.........................................................................................................................................5

3.1 Source and structure of trial balance................................................................................5

3.2 Business accounts, adjustments and notes.......................................................................6

4.1 Ratio analysis...................................................................................................................8

4.2 Recommendations for future management strategies......................................................9

Task 5.........................................................................................................................................9

5.1 Classification of costs......................................................................................................9

5.2 & 5.3 Contribution per unit and break-even analysis....................................................10

Conclusion................................................................................................................................11

References................................................................................................................................12

Introduction................................................................................................................................1

Task 1.........................................................................................................................................1

1.1 Sources of funding within business and service industry................................................1

1.2 Methods of generating income for a large chain of restaurants.......................................2

Task 2.........................................................................................................................................2

2.1 Elements of cost, gross profit percentages.......................................................................2

2.2 Methods of controlling stock and cash in a business and service environment...............3

Task 3.........................................................................................................................................4

3.3 Process and purpose of budgetary control.......................................................................4

3.4 Variance analysis of Yuri’s budget..................................................................................5

Task 4.........................................................................................................................................5

3.1 Source and structure of trial balance................................................................................5

3.2 Business accounts, adjustments and notes.......................................................................6

4.1 Ratio analysis...................................................................................................................8

4.2 Recommendations for future management strategies......................................................9

Task 5.........................................................................................................................................9

5.1 Classification of costs......................................................................................................9

5.2 & 5.3 Contribution per unit and break-even analysis....................................................10

Conclusion................................................................................................................................11

References................................................................................................................................12

List of tables

Table 1: Trial balance’s performa..............................................................................................6

Table 2: Income statements - adjustments.................................................................................6

Table 3: Balance sheet - adjustments.........................................................................................7

Table 4: Ratio Analysis for R. Riggs.........................................................................................8

Table 5: Calculation of Variable Cost per Unit.......................................................................10

Table 6: Sensitivity analysis.....................................................................................................10

Table 1: Trial balance’s performa..............................................................................................6

Table 2: Income statements - adjustments.................................................................................6

Table 3: Balance sheet - adjustments.........................................................................................7

Table 4: Ratio Analysis for R. Riggs.........................................................................................8

Table 5: Calculation of Variable Cost per Unit.......................................................................10

Table 6: Sensitivity analysis.....................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

In present scenario, hospitality industry is growing at significant pace. The growth in

industry needs to be accompanied by its financial or monetary growth (Helfrit, 2001). It is

essential for businesses in hospitality sector to plan their financial resources in an effective

manner. The financial planning involves proper allocation of financial resources and efficient

forecasting future. The report proposed herewith emphasizes on providing an in-depth

overview of financial planning within hospitality sector. The research report presented

herewith helps in generating deep understanding of financial planning within hospitality

industry.

TASK 1

1.1 Sources of funding within business and service industry

The organization needs to acquire funds through suitable sources of finance so as to

meet its monetary requirements. The varied ranges of financial sources that are available to

businesses in hospitality sector are described underneath in detail.

Bank loans: The organization can acquire funds through bank loans so as to meet all

kind of financial requirements (Nikbakht, 2006). The banking units in present scenario tend

to provide varied range of loan facilities. This in turn helps in meeting short to long-term

financial requirement on part of the organization.

Equity capital: The businesses in hospitality sector can acquire funds through issuing

equity shares. The financing option helps in meeting business requirement for long-run. The

acquisition of funds through equity capital does not involve regular interest payments.

However, financing option results in dilution of ownership among shareholders. It can be

therefore claimed that the source of financing helps in meeting business requirement for long

run.

Retained earnings The businesses in hospitality sector can utilize funds that are saved

as a part of reserves and surplus. It is the source of funding that helps in meeting financial

requirement at free of cost. Henceforth, it is considered to be suitable to meet financial

requirements in short and very-short run.

Issue of debentures: The large-scale businesses within hospitality industry can issue

debentures so as to meet financial requirement (Grahl, 2009). It is the costlier source of

finance that helps in meeting business requirement for long-run.

The organization in present case needs to acquire £ 50000 for purchase of machinery.

The bank loans are considered to be suitable source of financing for acquisition of machinery.

1 | P a g e

In present scenario, hospitality industry is growing at significant pace. The growth in

industry needs to be accompanied by its financial or monetary growth (Helfrit, 2001). It is

essential for businesses in hospitality sector to plan their financial resources in an effective

manner. The financial planning involves proper allocation of financial resources and efficient

forecasting future. The report proposed herewith emphasizes on providing an in-depth

overview of financial planning within hospitality sector. The research report presented

herewith helps in generating deep understanding of financial planning within hospitality

industry.

TASK 1

1.1 Sources of funding within business and service industry

The organization needs to acquire funds through suitable sources of finance so as to

meet its monetary requirements. The varied ranges of financial sources that are available to

businesses in hospitality sector are described underneath in detail.

Bank loans: The organization can acquire funds through bank loans so as to meet all

kind of financial requirements (Nikbakht, 2006). The banking units in present scenario tend

to provide varied range of loan facilities. This in turn helps in meeting short to long-term

financial requirement on part of the organization.

Equity capital: The businesses in hospitality sector can acquire funds through issuing

equity shares. The financing option helps in meeting business requirement for long-run. The

acquisition of funds through equity capital does not involve regular interest payments.

However, financing option results in dilution of ownership among shareholders. It can be

therefore claimed that the source of financing helps in meeting business requirement for long

run.

Retained earnings The businesses in hospitality sector can utilize funds that are saved

as a part of reserves and surplus. It is the source of funding that helps in meeting financial

requirement at free of cost. Henceforth, it is considered to be suitable to meet financial

requirements in short and very-short run.

Issue of debentures: The large-scale businesses within hospitality industry can issue

debentures so as to meet financial requirement (Grahl, 2009). It is the costlier source of

finance that helps in meeting business requirement for long-run.

The organization in present case needs to acquire £ 50000 for purchase of machinery.

The bank loans are considered to be suitable source of financing for acquisition of machinery.

1 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It is through bank loans that the hotel unit is able to acquire funds so as to purchase

machinery.

1.2 Methods of generating income for a large chain of restaurants

It is essential for businesses to generate sufficient amount of income on continuous

basis. The large chain of restaurants helps can generate income through following ways:

Product development: The restaurant unit can offer wide range of eatables so as to

suit taste buds of customers. This in turn helps in attracting large number of customers and

increasing profitability on part of the organization.

Market expansion in foreign markets: The large-scale restaurant units can expand

their operations in foreign markets. In present scenario, Asian markets offer wide range of

growth opportunities (Deakins, Galloway and Morrison, 2002). It can be therefore claimed

that expansion in foreign markets helps in generating more amount of income on part of

restaurant unit.

Market expansion in domestic markets: Opening up more number of branches in

domestic country also helps in generating of additional income. Henceforth, opening up of

more branches in domestic country also leads to increasing profitability.

Franchising: The large chain of restaurants can offer franchisee to open up new

branches. This in turn helps in increasing revenue and income earned on part of the restaurant

unit. The restaurant units can therefore earn additional income by offering franchising to

different businesses.

TASK 2

2.1 Elements of cost, gross profit percentages

Elements of cost

The businesses tend to incur varied range of costs while carrying its manufacturing

and operations. The different elements of costs incurred on part of the organization includes

following elements:

Material costs: The costs incurred on part of the restaurant unit in acquiring raw

materials (Hirsch, 2000). The organization tends to incur sufficient amount of expenditure on

acquiring materials for supporting manufacturing process.

Labour costs: In order to support operations, the business unit needs to pay wages and

salaries to its employees. In case of hospitality sector, employees tend to represent the

2 | P a g e

machinery.

1.2 Methods of generating income for a large chain of restaurants

It is essential for businesses to generate sufficient amount of income on continuous

basis. The large chain of restaurants helps can generate income through following ways:

Product development: The restaurant unit can offer wide range of eatables so as to

suit taste buds of customers. This in turn helps in attracting large number of customers and

increasing profitability on part of the organization.

Market expansion in foreign markets: The large-scale restaurant units can expand

their operations in foreign markets. In present scenario, Asian markets offer wide range of

growth opportunities (Deakins, Galloway and Morrison, 2002). It can be therefore claimed

that expansion in foreign markets helps in generating more amount of income on part of

restaurant unit.

Market expansion in domestic markets: Opening up more number of branches in

domestic country also helps in generating of additional income. Henceforth, opening up of

more branches in domestic country also leads to increasing profitability.

Franchising: The large chain of restaurants can offer franchisee to open up new

branches. This in turn helps in increasing revenue and income earned on part of the restaurant

unit. The restaurant units can therefore earn additional income by offering franchising to

different businesses.

TASK 2

2.1 Elements of cost, gross profit percentages

Elements of cost

The businesses tend to incur varied range of costs while carrying its manufacturing

and operations. The different elements of costs incurred on part of the organization includes

following elements:

Material costs: The costs incurred on part of the restaurant unit in acquiring raw

materials (Hirsch, 2000). The organization tends to incur sufficient amount of expenditure on

acquiring materials for supporting manufacturing process.

Labour costs: In order to support operations, the business unit needs to pay wages and

salaries to its employees. In case of hospitality sector, employees tend to represent the

2 | P a g e

business unit. Henceforth, the organization needs to incur high amount of labour costs for

management of business operations.

Administrative and other expenses: The business unit needs to incur administrative

and other expenses apart from labour and material costs (Hildreth, 2004). The businesses in

hospitality sector needs to incur sufficient amount of administrative expenses for the purpose

of managing operations.

Gross profit percentage

The organization can judge its profitability by estimating gross profit ratio which

indicates percentage of profit earned after meeting all direct expenses (Friedlob and Schleifer,

2003). The formulas mentioned below helps in estimating gross and operating profit ratio as

mentioned underneath.

Gross profit ratio=Gross Profit

Net Sales ∗100

Operating profit ratio=Operating Profit

Net sales ∗100

Operating profit Ratio for marks and Spencer for 2013:

Operating profit ratio= 838.22

9382.37∗100

Operating profit ratio=8.93 %

As per the estimations, marks and Spencer has earned operating profit ratio of 8.93%.

It can be claimed that the organization is able to earn sufficient profitability after meeting all

direct expenses. However, the organization is able to increase profitability by reducing

operating and other business expenses.

2.2 Methods of controlling stock and cash in a business and service environment

In order to achieve operational excellence, the organization needs to adopt strict

control mechanism. The business unit needs to adopt appropriate strategies for controlling

stock and cash flow. The lists of techniques through which stock can be controlled within

business unit are described underneath in detail.

Economic order quantity: The organization needs to determine economic order

quantity that helps in determining level at which inventory needs to be re-ordered (Theeke

and Mitchell, 2008). It is through estimation of economic order quantity that the organization

is able to order appropriate quantity of inventory at adequate intervals.

3 | P a g e

management of business operations.

Administrative and other expenses: The business unit needs to incur administrative

and other expenses apart from labour and material costs (Hildreth, 2004). The businesses in

hospitality sector needs to incur sufficient amount of administrative expenses for the purpose

of managing operations.

Gross profit percentage

The organization can judge its profitability by estimating gross profit ratio which

indicates percentage of profit earned after meeting all direct expenses (Friedlob and Schleifer,

2003). The formulas mentioned below helps in estimating gross and operating profit ratio as

mentioned underneath.

Gross profit ratio=Gross Profit

Net Sales ∗100

Operating profit ratio=Operating Profit

Net sales ∗100

Operating profit Ratio for marks and Spencer for 2013:

Operating profit ratio= 838.22

9382.37∗100

Operating profit ratio=8.93 %

As per the estimations, marks and Spencer has earned operating profit ratio of 8.93%.

It can be claimed that the organization is able to earn sufficient profitability after meeting all

direct expenses. However, the organization is able to increase profitability by reducing

operating and other business expenses.

2.2 Methods of controlling stock and cash in a business and service environment

In order to achieve operational excellence, the organization needs to adopt strict

control mechanism. The business unit needs to adopt appropriate strategies for controlling

stock and cash flow. The lists of techniques through which stock can be controlled within

business unit are described underneath in detail.

Economic order quantity: The organization needs to determine economic order

quantity that helps in determining level at which inventory needs to be re-ordered (Theeke

and Mitchell, 2008). It is through estimation of economic order quantity that the organization

is able to order appropriate quantity of inventory at adequate intervals.

3 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Just-in-time approach: The technique of just-in-time emphasizes on adopting real

time monitoring and controlling of cost. The approach emphasizes on fact that the

organization needs to continuous monitor all activities so as to identify variances. This in turn

helps in reducing costs to the maximum level. Just-in-time approach helps in monitoring and

controlling costs involved in business operations.

Re-order quantity: The methodology emphasizes on estimating the quantity that

should be ordered on regular intervals. It is through estimation of re-order quantity that the

organization is able to re-order appropriate levels of quantity (Deakins, Galloway and

Morrison, 2002). The acquisition of raw materials in adequate quantity helps in proper

inventory management within the organization.

LIFO (Last-in-first-out): The inventory management technique focuses on accounting

of inventory in a manner that the stock purchased at last is accounted for the first. The

methodology assumes that inventory that is arrived at last will be sold first. Henceforth, the

technique emphasizes on accounting in the manner whereby inventory that has been recently

purchased in accounted for first.

First-in-first out (FIFO): Another inventory management technique that is First-in-

first-out (FIFO) method emphasizes on accounting for inventories in a manner that the

inventory that is purchased first should be accounted for the first. The methodology takes into

consideration an assumption that the inventory is sold in order of its purchase. The

methodology helps in effective control of inventory within the organization.

In order to efficiently control inventory, the business unit can adopt response-based

supply chain instead of anticipation-based. In case of anticipation based supply chain, the

organization tends to predict or forecast its inventory requirements. It is on the basis of future

forecast that the stock is produced. Thereafter, the business unit waits for demand to arise in

the market. On other hand, response based supply chain emphasizes on taking orders in

advance. The inventory in case of response based supply chain is managed as per the orders

received by the organization. In recent times, the businesses majorly adopt response based

supply chain. It is through adoption of response based supply chain that the businesses are

able to minimize cost by maintaining adequate level of inventory.

It is seen that the organization can manage and control its inventory in an effective

manner. Moreover, the business unit needs to adopt strict control mechanism for its cash

collection and payment systems. The adequate level of liquidity helps the organization in

achievement of business objectives. Cash control mechanism and its different methods for the

organization are detailed underneath.

4 | P a g e

time monitoring and controlling of cost. The approach emphasizes on fact that the

organization needs to continuous monitor all activities so as to identify variances. This in turn

helps in reducing costs to the maximum level. Just-in-time approach helps in monitoring and

controlling costs involved in business operations.

Re-order quantity: The methodology emphasizes on estimating the quantity that

should be ordered on regular intervals. It is through estimation of re-order quantity that the

organization is able to re-order appropriate levels of quantity (Deakins, Galloway and

Morrison, 2002). The acquisition of raw materials in adequate quantity helps in proper

inventory management within the organization.

LIFO (Last-in-first-out): The inventory management technique focuses on accounting

of inventory in a manner that the stock purchased at last is accounted for the first. The

methodology assumes that inventory that is arrived at last will be sold first. Henceforth, the

technique emphasizes on accounting in the manner whereby inventory that has been recently

purchased in accounted for first.

First-in-first out (FIFO): Another inventory management technique that is First-in-

first-out (FIFO) method emphasizes on accounting for inventories in a manner that the

inventory that is purchased first should be accounted for the first. The methodology takes into

consideration an assumption that the inventory is sold in order of its purchase. The

methodology helps in effective control of inventory within the organization.

In order to efficiently control inventory, the business unit can adopt response-based

supply chain instead of anticipation-based. In case of anticipation based supply chain, the

organization tends to predict or forecast its inventory requirements. It is on the basis of future

forecast that the stock is produced. Thereafter, the business unit waits for demand to arise in

the market. On other hand, response based supply chain emphasizes on taking orders in

advance. The inventory in case of response based supply chain is managed as per the orders

received by the organization. In recent times, the businesses majorly adopt response based

supply chain. It is through adoption of response based supply chain that the businesses are

able to minimize cost by maintaining adequate level of inventory.

It is seen that the organization can manage and control its inventory in an effective

manner. Moreover, the business unit needs to adopt strict control mechanism for its cash

collection and payment systems. The adequate level of liquidity helps the organization in

achievement of business objectives. Cash control mechanism and its different methods for the

organization are detailed underneath.

4 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cash controlling methods: The business unit needs to control all kind of direct and

indirect expenses so as to meet long-term objectives. It is through adoption of strict control

mechanism that the organization is able to minimize costs and take appropriate measures

(Objectives of Financial Statement Analysis, 2015). This in turn helps in achieving

operational excellence and long-term business objectives. The organization needs to

continuously monitor all business activities. The continuous monitoring of operations and

cash inflow/outflow helps in adopting strict cash control mechanism. The business unit can

adopt following cash controlling mechanism so as to maintain liquidity.

Dual control: As per the dual control system, the organization needs to employ

multiple employees for managing cash. It can be said that the business unit can

involve two employees for cash counting, generating receipts and checking deposits.

It is through involvement of more than one employee at cash department that the

organization is able to control and manage liquidity or cash balance within business

unit.

Reconciliation: The business unit should adopt electronic system of recording

receipts and payments. It is through reconciliation of all records that the business unit

is able to monitor cash inflow and outflow. This in turn results in adopting strict cash

controlling mechanism within the organization.

The organization needs to also adopt cash controlling mechanisms so as to ensure

sufficient liquidity. In order to ensure sufficient inflow of cash, the organisation needs to

monitor all business activities and take appropriate measures to control cash expenditure.

The effective cash control mechanism is considered to improve liquidity of the business into

consideration.

TASK 3

3.3 Process and purpose of budgetary control

The organization needs to adopt budgetary control mechanism so as to achieve

benchmarks set. Budgetary control is a method in which budgets are prepared so as to

allocate financial resources. Moreover, it provides guidance to allocation of financial

resources and generation of sufficient level of profits. The purpose and process of budgetary

control is described underneath in detail.

Purpose of budgetary control

The budgets are prepared on part of the organization so as to achieve short-term and

long-term objectives. It is through budgetary control that the business unit is able to achieve

5 | P a g e

indirect expenses so as to meet long-term objectives. It is through adoption of strict control

mechanism that the organization is able to minimize costs and take appropriate measures

(Objectives of Financial Statement Analysis, 2015). This in turn helps in achieving

operational excellence and long-term business objectives. The organization needs to

continuously monitor all business activities. The continuous monitoring of operations and

cash inflow/outflow helps in adopting strict cash control mechanism. The business unit can

adopt following cash controlling mechanism so as to maintain liquidity.

Dual control: As per the dual control system, the organization needs to employ

multiple employees for managing cash. It can be said that the business unit can

involve two employees for cash counting, generating receipts and checking deposits.

It is through involvement of more than one employee at cash department that the

organization is able to control and manage liquidity or cash balance within business

unit.

Reconciliation: The business unit should adopt electronic system of recording

receipts and payments. It is through reconciliation of all records that the business unit

is able to monitor cash inflow and outflow. This in turn results in adopting strict cash

controlling mechanism within the organization.

The organization needs to also adopt cash controlling mechanisms so as to ensure

sufficient liquidity. In order to ensure sufficient inflow of cash, the organisation needs to

monitor all business activities and take appropriate measures to control cash expenditure.

The effective cash control mechanism is considered to improve liquidity of the business into

consideration.

TASK 3

3.3 Process and purpose of budgetary control

The organization needs to adopt budgetary control mechanism so as to achieve

benchmarks set. Budgetary control is a method in which budgets are prepared so as to

allocate financial resources. Moreover, it provides guidance to allocation of financial

resources and generation of sufficient level of profits. The purpose and process of budgetary

control is described underneath in detail.

Purpose of budgetary control

The budgets are prepared on part of the organization so as to achieve short-term and

long-term objectives. It is through budgetary control that the business unit is able to achieve

5 | P a g e

pre-defined targets and benchmarks. The main purpose of budgetary control is to

appropriately allocate financial resources. It is through budgetary control that the

organization is able to earn sufficient profitability. The technique helps in increasing

efficiency and imbibing operational excellence within the organization. It can be said that

adoption of budgetary control mechanism results in optimum utilization of financial

resources within organization. The purpose of budgeting and budgetary control mechanism

is discussed underneath in detail.

Formal process of communication: It is through preparation of budgets that the top

management is able to communicate its objectives to middle and lower level. It can be

therefore said that preparation of budgets is an efficient way to communicate management’s

expectations to employees.

Bridging gap between short-term and long-term plans: The organization is able to

bridge gap that exists between long-term and short-term business objectives. It is through

preparation of budgets that the organization is able to bridge gap that exists between short-

term and long-term plans.

Continuous improvements in business operations: The budgetary control serves

purpose of continuous improvements in business operations. It is through continuous

improvements in business activities that the organization is able to achieve success in long-

run. The budgetary control mechanism helps in improving business performance on

continuous basis.

Achieving financial objectives: It is through preparation of budgets that financial

objectives of the organization are achieved. The organization is able to allocate financial

resources in an effective manner. It can be therefore said that the business unit is able to

achieve all its financial objectives through preparation of budgets.

It can be said that the budgetary control serves varied range of purpose for the

organization. The business unit is able to meet its objectives in an efficient manner through

preparation of budgets.

Process of budgetary control

The budgetary control technique needs to be implemented in a sequential procedure.

The complete step-by-step process of budgetary control mechanism is described underneath

in detail.

6 | P a g e

appropriately allocate financial resources. It is through budgetary control that the

organization is able to earn sufficient profitability. The technique helps in increasing

efficiency and imbibing operational excellence within the organization. It can be said that

adoption of budgetary control mechanism results in optimum utilization of financial

resources within organization. The purpose of budgeting and budgetary control mechanism

is discussed underneath in detail.

Formal process of communication: It is through preparation of budgets that the top

management is able to communicate its objectives to middle and lower level. It can be

therefore said that preparation of budgets is an efficient way to communicate management’s

expectations to employees.

Bridging gap between short-term and long-term plans: The organization is able to

bridge gap that exists between long-term and short-term business objectives. It is through

preparation of budgets that the organization is able to bridge gap that exists between short-

term and long-term plans.

Continuous improvements in business operations: The budgetary control serves

purpose of continuous improvements in business operations. It is through continuous

improvements in business activities that the organization is able to achieve success in long-

run. The budgetary control mechanism helps in improving business performance on

continuous basis.

Achieving financial objectives: It is through preparation of budgets that financial

objectives of the organization are achieved. The organization is able to allocate financial

resources in an effective manner. It can be therefore said that the business unit is able to

achieve all its financial objectives through preparation of budgets.

It can be said that the budgetary control serves varied range of purpose for the

organization. The business unit is able to meet its objectives in an efficient manner through

preparation of budgets.

Process of budgetary control

The budgetary control technique needs to be implemented in a sequential procedure.

The complete step-by-step process of budgetary control mechanism is described underneath

in detail.

6 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

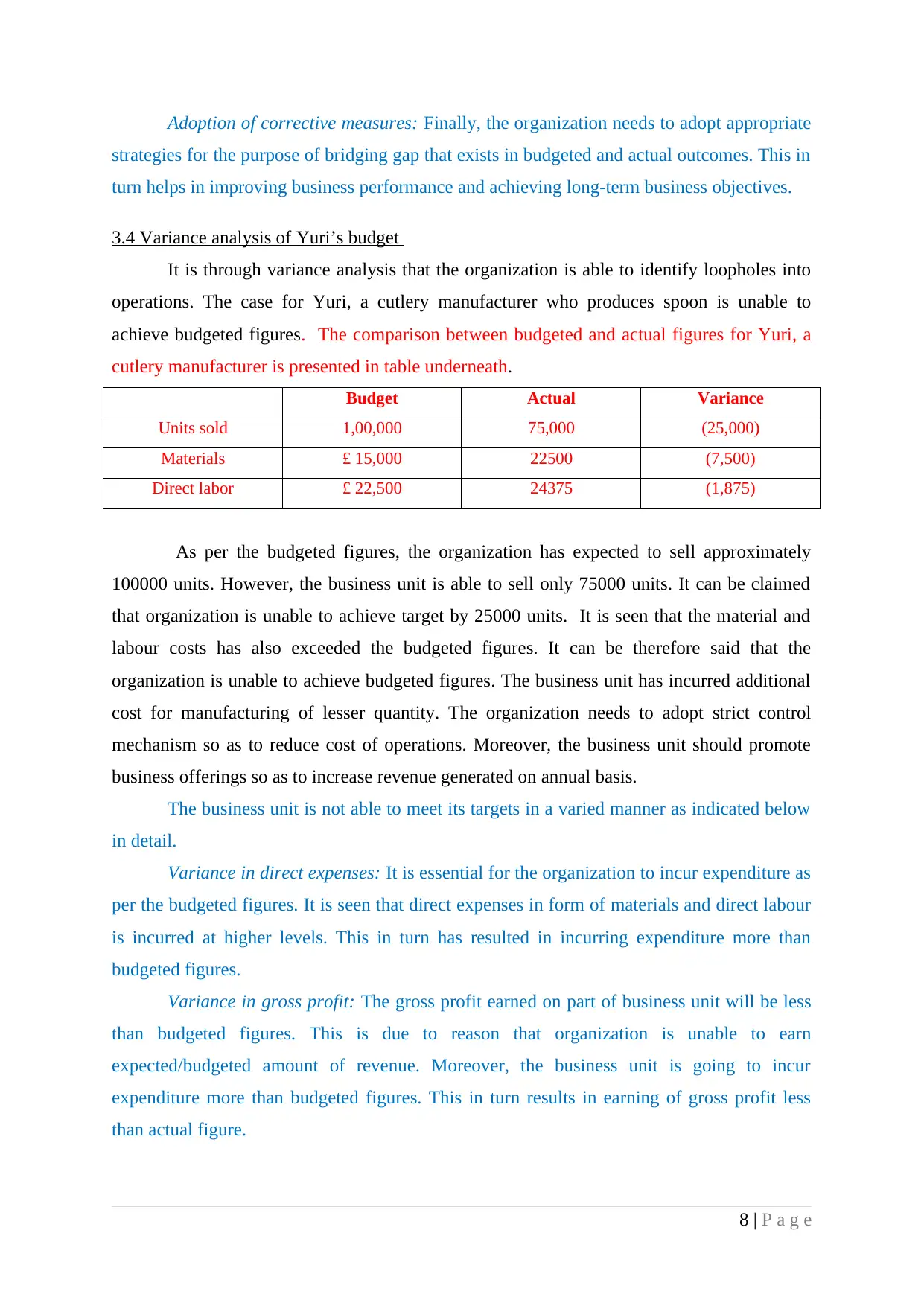

Figure 1: Budgetary control process

The diagram presented above indicates the budgetary control process that is to be

adopted by the organization. The sequential procedure for formulation and control of budgets

is detailed underneath.

Evaluating past trend and forecasting future performance: The organization needs to

conduct an in-depth evaluation of past performance. It is through identification of past trend

that the future performance can be forecasted.

Preparation of budgets: The business unit needs to prepare budgets so as to allocate

financial resources in an effective. Moreover, it is through preparation of budgets that the

organization is able to anticipate future performance.

Measuring actual performance: It is essential to measure actual performance on

continuous basis. The business unit is able to identify variances in budgeted and actual

figures by measuring actual performance.

Identification of variances: First of all, the organization needs to identify variances by

mapping budgeted figures to that of actual figures (The Importance of a Budget. 2015). It is

through identification of variances that the organization is able to take appropriate measures.

Evaluation of variances identified: The business unit needs to understand nature of

variances identified. It is through investigation of nature of variances that the organization is

able to plan appropriate strategies.

7 | P a g e

EvalautingpasttrendandforecastingfutureperformancePrepartionofbudgetsMeasuringactualperformanceIdentifyingvariancesEvaluatingvariancesidentifiedAdoptingcorrectivemeasures

The diagram presented above indicates the budgetary control process that is to be

adopted by the organization. The sequential procedure for formulation and control of budgets

is detailed underneath.

Evaluating past trend and forecasting future performance: The organization needs to

conduct an in-depth evaluation of past performance. It is through identification of past trend

that the future performance can be forecasted.

Preparation of budgets: The business unit needs to prepare budgets so as to allocate

financial resources in an effective. Moreover, it is through preparation of budgets that the

organization is able to anticipate future performance.

Measuring actual performance: It is essential to measure actual performance on

continuous basis. The business unit is able to identify variances in budgeted and actual

figures by measuring actual performance.

Identification of variances: First of all, the organization needs to identify variances by

mapping budgeted figures to that of actual figures (The Importance of a Budget. 2015). It is

through identification of variances that the organization is able to take appropriate measures.

Evaluation of variances identified: The business unit needs to understand nature of

variances identified. It is through investigation of nature of variances that the organization is

able to plan appropriate strategies.

7 | P a g e

EvalautingpasttrendandforecastingfutureperformancePrepartionofbudgetsMeasuringactualperformanceIdentifyingvariancesEvaluatingvariancesidentifiedAdoptingcorrectivemeasures

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Adoption of corrective measures: Finally, the organization needs to adopt appropriate

strategies for the purpose of bridging gap that exists in budgeted and actual outcomes. This in

turn helps in improving business performance and achieving long-term business objectives.

3.4 Variance analysis of Yuri’s budget

It is through variance analysis that the organization is able to identify loopholes into

operations. The case for Yuri, a cutlery manufacturer who produces spoon is unable to

achieve budgeted figures. The comparison between budgeted and actual figures for Yuri, a

cutlery manufacturer is presented in table underneath.

Budget Actual Variance

Units sold 1,00,000 75,000 (25,000)

Materials £ 15,000 22500 (7,500)

Direct labor £ 22,500 24375 (1,875)

As per the budgeted figures, the organization has expected to sell approximately

100000 units. However, the business unit is able to sell only 75000 units. It can be claimed

that organization is unable to achieve target by 25000 units. It is seen that the material and

labour costs has also exceeded the budgeted figures. It can be therefore said that the

organization is unable to achieve budgeted figures. The business unit has incurred additional

cost for manufacturing of lesser quantity. The organization needs to adopt strict control

mechanism so as to reduce cost of operations. Moreover, the business unit should promote

business offerings so as to increase revenue generated on annual basis.

The business unit is not able to meet its targets in a varied manner as indicated below

in detail.

Variance in direct expenses: It is essential for the organization to incur expenditure as

per the budgeted figures. It is seen that direct expenses in form of materials and direct labour

is incurred at higher levels. This in turn has resulted in incurring expenditure more than

budgeted figures.

Variance in gross profit: The gross profit earned on part of business unit will be less

than budgeted figures. This is due to reason that organization is unable to earn

expected/budgeted amount of revenue. Moreover, the business unit is going to incur

expenditure more than budgeted figures. This in turn results in earning of gross profit less

than actual figure.

8 | P a g e

strategies for the purpose of bridging gap that exists in budgeted and actual outcomes. This in

turn helps in improving business performance and achieving long-term business objectives.

3.4 Variance analysis of Yuri’s budget

It is through variance analysis that the organization is able to identify loopholes into

operations. The case for Yuri, a cutlery manufacturer who produces spoon is unable to

achieve budgeted figures. The comparison between budgeted and actual figures for Yuri, a

cutlery manufacturer is presented in table underneath.

Budget Actual Variance

Units sold 1,00,000 75,000 (25,000)

Materials £ 15,000 22500 (7,500)

Direct labor £ 22,500 24375 (1,875)

As per the budgeted figures, the organization has expected to sell approximately

100000 units. However, the business unit is able to sell only 75000 units. It can be claimed

that organization is unable to achieve target by 25000 units. It is seen that the material and

labour costs has also exceeded the budgeted figures. It can be therefore said that the

organization is unable to achieve budgeted figures. The business unit has incurred additional

cost for manufacturing of lesser quantity. The organization needs to adopt strict control

mechanism so as to reduce cost of operations. Moreover, the business unit should promote

business offerings so as to increase revenue generated on annual basis.

The business unit is not able to meet its targets in a varied manner as indicated below

in detail.

Variance in direct expenses: It is essential for the organization to incur expenditure as

per the budgeted figures. It is seen that direct expenses in form of materials and direct labour

is incurred at higher levels. This in turn has resulted in incurring expenditure more than

budgeted figures.

Variance in gross profit: The gross profit earned on part of business unit will be less

than budgeted figures. This is due to reason that organization is unable to earn

expected/budgeted amount of revenue. Moreover, the business unit is going to incur

expenditure more than budgeted figures. This in turn results in earning of gross profit less

than actual figure.

8 | P a g e

Variance in net profit: It is seen that reduced revenues and increased profits results in

reduction in gross profit. It can be therefore said that variances in gross profits leads to

variances in net profits. The business unit is therefore not able to earn expected or budgeted

profits.

It can be said that distinct set of variances occur in figures of revenue, direct

expenses, gross profit and net profit. In order to bridge the gap between actual and budgeted

figures, the organization should adopt strict control mechanism. The variances in budgeted

and actual figures indicate organization’s inefficiency in meeting its targets.

The variance can also be classified by distinguishing between usage and price

variance in the following manner.

Sales variance: The sales variance is a result of variance in number of units sold. The

organization has expected that it is going to sell approximately 100000 units. However, it is

able to sell 75000 units those results in variance of approximately 25000 units. The variance

in number of units sold in-turn results in variance in revenue. The organization is going to

earn revenue by selling adequate number of units. The reduction in number of units sold in

turn results in reducing overall sales revenue of the business unit. It can be therefore said that

the company is not able to achieve its target. The overall revenue is expected to decrease with

reduction in number of units sold. The sales variance is expected to incur due to reduction in

demand of the products into consideration. The business unit is unable to meet its expected

revenue due to decrease in demand or change in consumers’ preferences.

Material price variance: The business unit can incur material variance due to

reduction in material prices. It is with increase in prices of material that the organization ends

up with increase in actual expenditure. The material prices tend to increase with change in

rate of inflation. The rise in inflation results in increasing material price and expenditure on

part of the organization. Henceforth, the material price variance has been incurred on part of

the organization.

Material usage variance: The material usage variance refers to variance that arises as

a result of increase/decrease in usage of required materials. The business unit sometimes tend

to make additional utilization of quantity of materials. This in turn results in increasing

material variance. In present case, the business unit is incurring overall material variance of

7500 that includes material price and material usage variance. The business unit has utilized

additional materials in production of goods. Although demand has been reduced, material

usage has been increased on part of the organization. It is with increase in material usage and

price that overall expenditure on material has been increased.

9 | P a g e

reduction in gross profit. It can be therefore said that variances in gross profits leads to

variances in net profits. The business unit is therefore not able to earn expected or budgeted

profits.

It can be said that distinct set of variances occur in figures of revenue, direct

expenses, gross profit and net profit. In order to bridge the gap between actual and budgeted

figures, the organization should adopt strict control mechanism. The variances in budgeted

and actual figures indicate organization’s inefficiency in meeting its targets.

The variance can also be classified by distinguishing between usage and price

variance in the following manner.

Sales variance: The sales variance is a result of variance in number of units sold. The

organization has expected that it is going to sell approximately 100000 units. However, it is

able to sell 75000 units those results in variance of approximately 25000 units. The variance

in number of units sold in-turn results in variance in revenue. The organization is going to

earn revenue by selling adequate number of units. The reduction in number of units sold in

turn results in reducing overall sales revenue of the business unit. It can be therefore said that

the company is not able to achieve its target. The overall revenue is expected to decrease with

reduction in number of units sold. The sales variance is expected to incur due to reduction in

demand of the products into consideration. The business unit is unable to meet its expected

revenue due to decrease in demand or change in consumers’ preferences.

Material price variance: The business unit can incur material variance due to

reduction in material prices. It is with increase in prices of material that the organization ends

up with increase in actual expenditure. The material prices tend to increase with change in

rate of inflation. The rise in inflation results in increasing material price and expenditure on

part of the organization. Henceforth, the material price variance has been incurred on part of

the organization.

Material usage variance: The material usage variance refers to variance that arises as

a result of increase/decrease in usage of required materials. The business unit sometimes tend

to make additional utilization of quantity of materials. This in turn results in increasing

material variance. In present case, the business unit is incurring overall material variance of

7500 that includes material price and material usage variance. The business unit has utilized

additional materials in production of goods. Although demand has been reduced, material

usage has been increased on part of the organization. It is with increase in material usage and

price that overall expenditure on material has been increased.

9 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.