Financial Impairment Report: Analysis of Accounting Standards

VerifiedAdded on 2020/05/16

|14

|2958

|59

Report

AI Summary

This report provides an in-depth analysis of financial impairment, focusing on the practices and procedures of Codan Limited. It examines the impairment test of asset value, the procedures involved, and the expenditures associated with impairment. The report delves into the necessary estimations and assumptions, highlighting the subjectivity inherent in the impairment testing process. It also addresses the insights derived from the impairment tests and the measurement of fair value. Furthermore, the report discusses the absence of former accounting standards in the economic reality, reasons for the discrepancies in lease liabilities, and the views of the IASB Chairperson regarding accounting standards. The analysis includes the ineffectiveness of new standards and possibilities for improvement in investment decisions, providing a comprehensive overview of financial impairment and its implications.

Running head: FINANCIAL IMPAIRMENT

Financial Impairment

Name of the Student:

Name of the University:

Author Note:

Financial Impairment

Name of the Student:

Name of the University:

Author Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

FINANCIAL IMPAIRMENT

Table of Contents

Assessment Task: Part A:................................................................................................................2

1. Impairment Test of the Asset value.............................................................................................3

2. Procedure of Impairment Test.....................................................................................................4

3. Expenditure of the Impairment....................................................................................................4

4. Necessary estimation and assumptions associated with the impairment test..............................6

5. Associated subjectivity in Impairment Testing Process..............................................................7

6. Surprises, difficulties, confusion, and interest associated with the impairment test...................8

7. Insights derived from the impairment test...................................................................................8

8. Measurement of the Fair Value...................................................................................................8

Assessment Task Part B:.................................................................................................................9

1. Absence of former accounting standards in the economic reality...............................................9

2. Reasons why under the previous accounting standards the lease liabilities of the reporting

entities in the balance sheet were 66 times more than the reported debts under the balance sheet.9

3. Views of IASB Chairperson regarding the accounting standards.............................................10

4. The view of Chairperson about the ineffectiveness of the new standards.................................10

5. Possibilities in providing better improvement in investment decisions....................................10

References......................................................................................................................................12

FINANCIAL IMPAIRMENT

Table of Contents

Assessment Task: Part A:................................................................................................................2

1. Impairment Test of the Asset value.............................................................................................3

2. Procedure of Impairment Test.....................................................................................................4

3. Expenditure of the Impairment....................................................................................................4

4. Necessary estimation and assumptions associated with the impairment test..............................6

5. Associated subjectivity in Impairment Testing Process..............................................................7

6. Surprises, difficulties, confusion, and interest associated with the impairment test...................8

7. Insights derived from the impairment test...................................................................................8

8. Measurement of the Fair Value...................................................................................................8

Assessment Task Part B:.................................................................................................................9

1. Absence of former accounting standards in the economic reality...............................................9

2. Reasons why under the previous accounting standards the lease liabilities of the reporting

entities in the balance sheet were 66 times more than the reported debts under the balance sheet.9

3. Views of IASB Chairperson regarding the accounting standards.............................................10

4. The view of Chairperson about the ineffectiveness of the new standards.................................10

5. Possibilities in providing better improvement in investment decisions....................................10

References......................................................................................................................................12

2

FINANCIAL IMPAIRMENT

Assessment Task: Part A:

The financial impairment depends on the costs that include exceeded amount of the book

value. This report would provide the insights of the financial impairment and the underlying

assumptions. Codan Limited, the financial corporation, would prepare the financial statements

and the annual report by conducting the impairment tests based on the measurements of existing

assets. Furthermore, the report would also focus on the associated practices and procedures

related to the impairment tests process developed by the organization. The study would also

provide the clear elaboration of the subjectivity associated with the developed tests of financial

impairment. Codan Limited has captured the leading position in manufacturing and supplying

the mining technology, communication, and metal detection technicalities. Headquarter of the

company is in South Australia from where the company generates the revenues of almost $132.3

million. The information obtained from the annual report of 2016 suggests that the company

utilizes the highly advanced technologies to overcome the issues emerge due to the security,

communication, safety parameter, and productivity. Currently, the company has secured the

position in the competitive business market by selling the products in 150 nations from which

almost 85% revenue is gathered.

According to Amiraslani, Iatridis and Pope (2013), asset impairment is conceptualized as

the measurement of the lower value of the existing asset than the actual value. It is necessary to

facilitate the impairment in the tangible fixed assets, such as plant, property, and equipment.

Apart from these tangible assets, it is necessary to impair the intangible assets as well, such as

establishing the good will and developing the remarkable account receivable. The income

statement of the company highlights the subsequent loss, which is needed to be adjusted for

FINANCIAL IMPAIRMENT

Assessment Task: Part A:

The financial impairment depends on the costs that include exceeded amount of the book

value. This report would provide the insights of the financial impairment and the underlying

assumptions. Codan Limited, the financial corporation, would prepare the financial statements

and the annual report by conducting the impairment tests based on the measurements of existing

assets. Furthermore, the report would also focus on the associated practices and procedures

related to the impairment tests process developed by the organization. The study would also

provide the clear elaboration of the subjectivity associated with the developed tests of financial

impairment. Codan Limited has captured the leading position in manufacturing and supplying

the mining technology, communication, and metal detection technicalities. Headquarter of the

company is in South Australia from where the company generates the revenues of almost $132.3

million. The information obtained from the annual report of 2016 suggests that the company

utilizes the highly advanced technologies to overcome the issues emerge due to the security,

communication, safety parameter, and productivity. Currently, the company has secured the

position in the competitive business market by selling the products in 150 nations from which

almost 85% revenue is gathered.

According to Amiraslani, Iatridis and Pope (2013), asset impairment is conceptualized as

the measurement of the lower value of the existing asset than the actual value. It is necessary to

facilitate the impairment in the tangible fixed assets, such as plant, property, and equipment.

Apart from these tangible assets, it is necessary to impair the intangible assets as well, such as

establishing the good will and developing the remarkable account receivable. The income

statement of the company highlights the subsequent loss, which is needed to be adjusted for

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

FINANCIAL IMPAIRMENT

improving the values of the assets by undertaking impairment practices. The practices for writing

off impairment display the reduced level of the carrying cost. The asset value is decreased as

some of adjustments are made and the result further discloses the significant loss.

1. Impairment Test of the Asset value

Codan Ltd published the annual report on 30th June, 2016, in which the entire financial

impairment test result is systematically informed. It has been observed that the impairment tests

are conducted annually or more than once in a year. The report of these tests specifies that the

reputation of the company, which is considered as the major intangible asset, is not amortized n

the field of financial account. Andrews (2012) implied that the asset impairment is generally

required if the company makes any changes to the event or to any specific circumstance. The

further report indicates that the accumulated loss during the impairment affected the financial

aspects by decreasing the costs. The other assets in Codan Ltd. include property, equipment,

inventories and plants. These assets are also needed to be tested for the impairments, especially

when the irrecoverable amount becomes the major concern.

FINANCIAL IMPAIRMENT

improving the values of the assets by undertaking impairment practices. The practices for writing

off impairment display the reduced level of the carrying cost. The asset value is decreased as

some of adjustments are made and the result further discloses the significant loss.

1. Impairment Test of the Asset value

Codan Ltd published the annual report on 30th June, 2016, in which the entire financial

impairment test result is systematically informed. It has been observed that the impairment tests

are conducted annually or more than once in a year. The report of these tests specifies that the

reputation of the company, which is considered as the major intangible asset, is not amortized n

the field of financial account. Andrews (2012) implied that the asset impairment is generally

required if the company makes any changes to the event or to any specific circumstance. The

further report indicates that the accumulated loss during the impairment affected the financial

aspects by decreasing the costs. The other assets in Codan Ltd. include property, equipment,

inventories and plants. These assets are also needed to be tested for the impairments, especially

when the irrecoverable amount becomes the major concern.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

FINANCIAL IMPAIRMENT

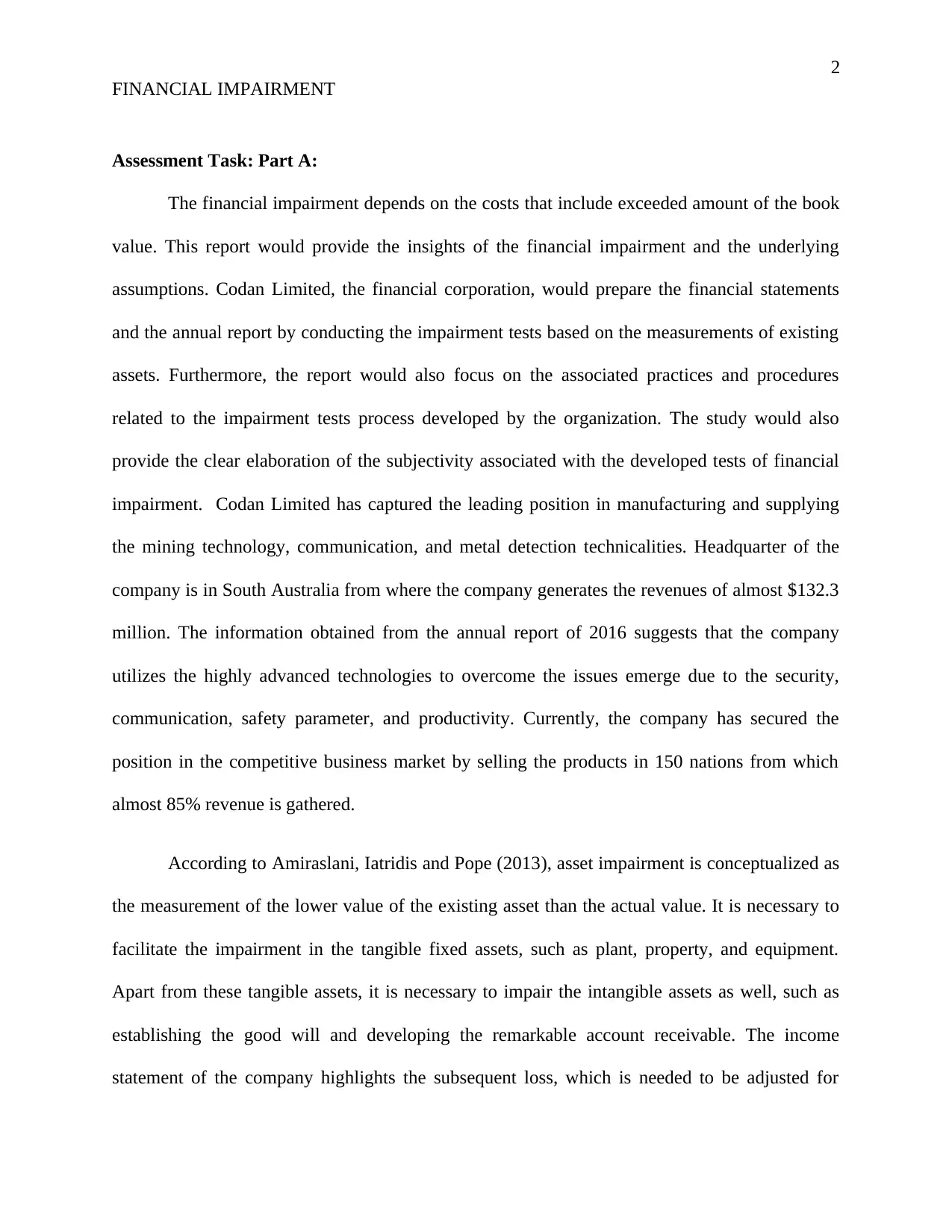

2. Procedure of Impairment Test

The carrying amount of the asset is sometimes unrecovered due to which the impairment

tests become essential to be conducted. The intangible assets and the company reputation are

also needed to be tested for impairment (Jennings and Marques 2013). This test is needed to be

conducted for more than once in a year. The particular set of assets is needed to be combined

together for the impairment assessment since the separated cash inflow indicates the reduced

level. The cash generating units depends on the independent cash inflows received from the

group of assets. On the other hand, the non-financial assets also require the impairment analysis

(Filip, Jeanjean and Paugam 2015). In fact, it is noticed that each of the reporting date of the

impairment in the organization can be reversed at times.

3. Expenditure of the Impairment

The report presented in the annual report published on 30th June, 2016 highlights the

expenditure amount, which is as follows:

Expenditure of the Tangible Asset Impairment

FINANCIAL IMPAIRMENT

2. Procedure of Impairment Test

The carrying amount of the asset is sometimes unrecovered due to which the impairment

tests become essential to be conducted. The intangible assets and the company reputation are

also needed to be tested for impairment (Jennings and Marques 2013). This test is needed to be

conducted for more than once in a year. The particular set of assets is needed to be combined

together for the impairment assessment since the separated cash inflow indicates the reduced

level. The cash generating units depends on the independent cash inflows received from the

group of assets. On the other hand, the non-financial assets also require the impairment analysis

(Filip, Jeanjean and Paugam 2015). In fact, it is noticed that each of the reporting date of the

impairment in the organization can be reversed at times.

3. Expenditure of the Impairment

The report presented in the annual report published on 30th June, 2016 highlights the

expenditure amount, which is as follows:

Expenditure of the Tangible Asset Impairment

5

FINANCIAL IMPAIRMENT

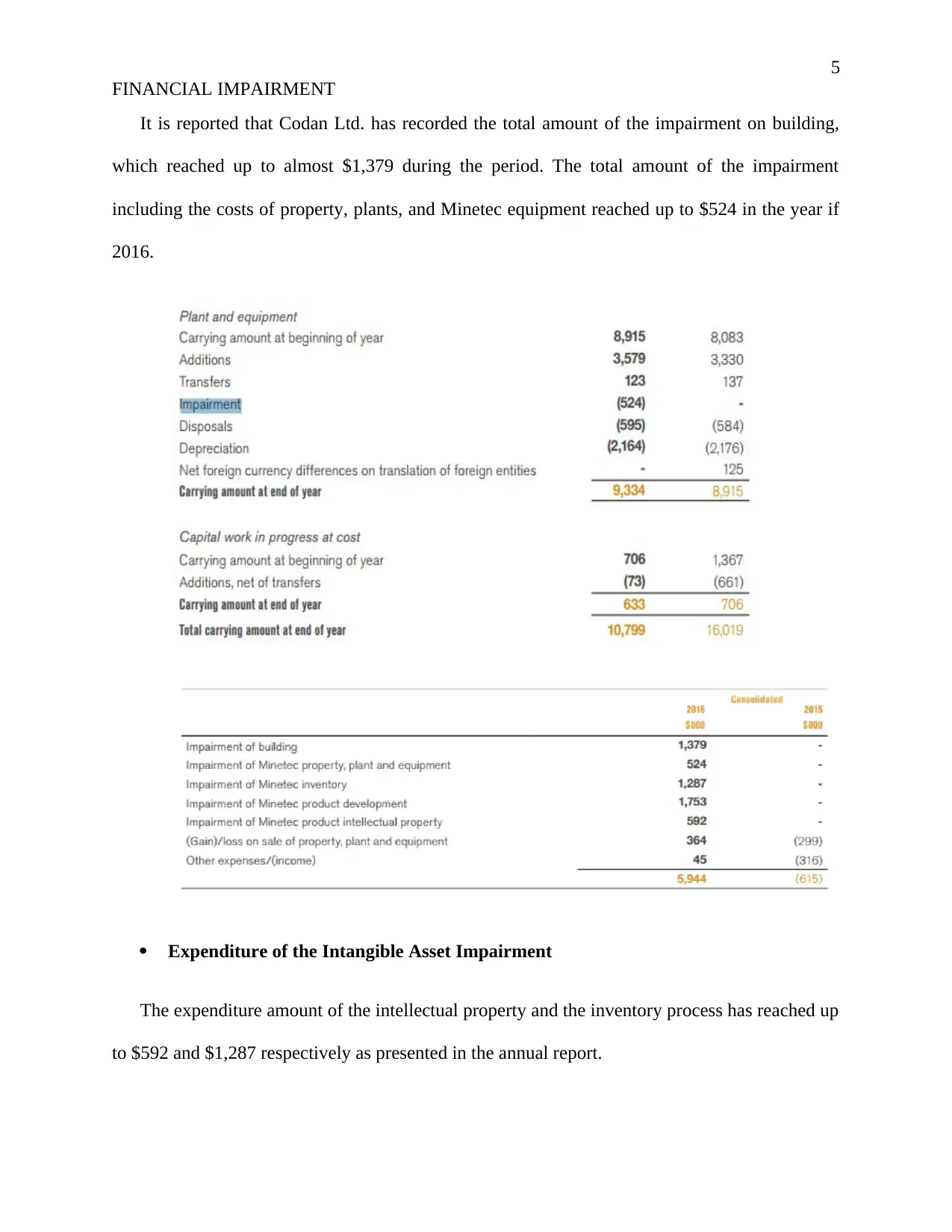

It is reported that Codan Ltd. has recorded the total amount of the impairment on building,

which reached up to almost $1,379 during the period. The total amount of the impairment

including the costs of property, plants, and Minetec equipment reached up to $524 in the year if

2016.

Expenditure of the Intangible Asset Impairment

The expenditure amount of the intellectual property and the inventory process has reached up

to $592 and $1,287 respectively as presented in the annual report.

FINANCIAL IMPAIRMENT

It is reported that Codan Ltd. has recorded the total amount of the impairment on building,

which reached up to almost $1,379 during the period. The total amount of the impairment

including the costs of property, plants, and Minetec equipment reached up to $524 in the year if

2016.

Expenditure of the Intangible Asset Impairment

The expenditure amount of the intellectual property and the inventory process has reached up

to $592 and $1,287 respectively as presented in the annual report.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

FINANCIAL IMPAIRMENT

4. Necessary estimation and assumptions associated with the impairment test

It has been observed that Codan Ltd. is much concerned about the future opportunities due to

which the company has made few of the estimations and assumptions much significantly. It is

important to make the equal estimation outcome in accordance with the related actual outcomes.

In fact, if there will be any specific mistakes occurred in making proper estimation, it may affect

in leading the adjustments of the materials of any specific asset. This asset would carry the value

for the next financial year that will be disclosed through presenting the notes (Rennekamp, Rupar

and Seybert 2014). The judgments are generally based as per the necessary accounting necessity.

It has been observed that the business atmosphere of Codan Ltd. has been experiencing adverse

and negative conditions that developed and the continuous downturn in the market is also much

foreseen. The ash generating unit was conducted to ascertain the recoverable amount of both the

tangible and intangible assets. CGU (Cash Generating Unit) of the recoverable amount depends

on the value-in-use calculations, which can be utilized in projecting the cash flow based on the

financial forecast. The management has been working since last five years to develop this

forecast report. The impairment report is developed by comparing the values of the present and

the estimated cash flows for the future (Cotter 2014). The discount is estimated by depending on

the previous interest rate. The following assumptions are utilized for assessing the value-in-use:

Margin of Sales

Rate of the estimated discount

Use of the growth rate with the help of extrapolate cash flows beyond the forecast time

FINANCIAL IMPAIRMENT

4. Necessary estimation and assumptions associated with the impairment test

It has been observed that Codan Ltd. is much concerned about the future opportunities due to

which the company has made few of the estimations and assumptions much significantly. It is

important to make the equal estimation outcome in accordance with the related actual outcomes.

In fact, if there will be any specific mistakes occurred in making proper estimation, it may affect

in leading the adjustments of the materials of any specific asset. This asset would carry the value

for the next financial year that will be disclosed through presenting the notes (Rennekamp, Rupar

and Seybert 2014). The judgments are generally based as per the necessary accounting necessity.

It has been observed that the business atmosphere of Codan Ltd. has been experiencing adverse

and negative conditions that developed and the continuous downturn in the market is also much

foreseen. The ash generating unit was conducted to ascertain the recoverable amount of both the

tangible and intangible assets. CGU (Cash Generating Unit) of the recoverable amount depends

on the value-in-use calculations, which can be utilized in projecting the cash flow based on the

financial forecast. The management has been working since last five years to develop this

forecast report. The impairment report is developed by comparing the values of the present and

the estimated cash flows for the future (Cotter 2014). The discount is estimated by depending on

the previous interest rate. The following assumptions are utilized for assessing the value-in-use:

Margin of Sales

Rate of the estimated discount

Use of the growth rate with the help of extrapolate cash flows beyond the forecast time

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

FINANCIAL IMPAIRMENT

5. Associated subjectivity in Impairment Testing Process

The accounting regulations IAS 36 of asset impairments imply that the asset impairment

demands subjective interpretation and the appropriate IFRS standards. However, the estimation

can be adjusted as per the requirements presented by the managers in the company. It is notable

that the asset impairment does not depend on the limited portion of the creative accounting

(Ramanna and Watts, 2012). The report obtained from the 2016 annual report highlights that the

involvement of the subjective assumptions is huge. The organization has the considerable

opportunity of exploiting the discretion and conducting the impairment tests for the developing

the goodwill of the company. The cash generating units can also be utilized for allocating the

goodwill. The amount is quite recoverable and there is no possibility of the active prices since

the goodwill can become a subject of discretion (Bertomeu and Cheynel 2015).

FINANCIAL IMPAIRMENT

5. Associated subjectivity in Impairment Testing Process

The accounting regulations IAS 36 of asset impairments imply that the asset impairment

demands subjective interpretation and the appropriate IFRS standards. However, the estimation

can be adjusted as per the requirements presented by the managers in the company. It is notable

that the asset impairment does not depend on the limited portion of the creative accounting

(Ramanna and Watts, 2012). The report obtained from the 2016 annual report highlights that the

involvement of the subjective assumptions is huge. The organization has the considerable

opportunity of exploiting the discretion and conducting the impairment tests for the developing

the goodwill of the company. The cash generating units can also be utilized for allocating the

goodwill. The amount is quite recoverable and there is no possibility of the active prices since

the goodwill can become a subject of discretion (Bertomeu and Cheynel 2015).

8

FINANCIAL IMPAIRMENT

6. Surprises, difficulties, confusion, and interest associated with the impairment test

Presenting the indication of the impairments is highlighted as the most difficult and confusing

part as per the report derived from the above assessment. Both the internal and the external

signal of the asset impairment help in creating this indication as a whole. The management

discretion is responsible for delivering more frequency in the impairment test (Bertomeu and

Cheynel 2015). In fact, it has been observed that the management can even practice the test

opportunistically if there will be any value downturn is visible.

7. Insights derived from the impairment test

There are the considerable differences observed between the recoverable amount and the

carrying value of the assets. The higher fair value of the recoverable amount can be decreased

due to the deposal of the value-in-use cost (Costantini and Zanin 2015). The sales agreement and

the asset value determine the fair value of the organization in which the asset trade exists. The

fair value of the company discloses the exact amount of the existing asset, which can be sold by

the company (Bepari, Rahman and Mollik 2014). As mentioned in IAS 36, the business value-in-

use is characterized by the future cash flow that is to be gained from the cash generating units.

8. Measurement of the Fair Value

As highlighted in the IFRS 13 standard, the fair value of the company is determined by the

following aspects:

Sales agreement

Existing assets in the trade market

Availability of the adequate information in which the asset can be sold.

FINANCIAL IMPAIRMENT

6. Surprises, difficulties, confusion, and interest associated with the impairment test

Presenting the indication of the impairments is highlighted as the most difficult and confusing

part as per the report derived from the above assessment. Both the internal and the external

signal of the asset impairment help in creating this indication as a whole. The management

discretion is responsible for delivering more frequency in the impairment test (Bertomeu and

Cheynel 2015). In fact, it has been observed that the management can even practice the test

opportunistically if there will be any value downturn is visible.

7. Insights derived from the impairment test

There are the considerable differences observed between the recoverable amount and the

carrying value of the assets. The higher fair value of the recoverable amount can be decreased

due to the deposal of the value-in-use cost (Costantini and Zanin 2015). The sales agreement and

the asset value determine the fair value of the organization in which the asset trade exists. The

fair value of the company discloses the exact amount of the existing asset, which can be sold by

the company (Bepari, Rahman and Mollik 2014). As mentioned in IAS 36, the business value-in-

use is characterized by the future cash flow that is to be gained from the cash generating units.

8. Measurement of the Fair Value

As highlighted in the IFRS 13 standard, the fair value of the company is determined by the

following aspects:

Sales agreement

Existing assets in the trade market

Availability of the adequate information in which the asset can be sold.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

FINANCIAL IMPAIRMENT

Assessment Task Part B:

1. Absence of former accounting standards in the economic reality

In 1 out of 3 companies that are utilizing the US GAAP or IFRS standards are

recognizably affected by various forms of the accounting techniques. The current status is

reflecting that the organizations under these standards amount and commits for more than 3.3

trillion (Ifrs.org. 2018). It is noticed that almost 85% of the total asset are not shown in the

financial statement or balance sheet of the company as these are considered as the operational

leases. The real liability is created if these leases are not shown. Therefore, the company can face

bankruptcy if it does not maintain the standards with the latest economic reality during the

financial crisis (Fitó, Moya and Orgaz 2013). The company is committed towards the long-term

operating leases which were shown as lean in the balance sheet.

2. Reasons why under the previous accounting standards the lease liabilities of the

reporting entities in the balance sheet were 66 times more than the reported debts under

the balance sheet

The earlier accounting standards present the report, which determines 85% of the

operating lease and it even reflects on the balance sheet. It creates the real liability even though it

is not mentioned in the balance sheet (Fitó, Moya and Orgaz 2013). Therefore, during the time of

the financial crisis, the major companies need to make the amendments in the economic reality.

The company even requires developing the commitments for the long-term operating leases due

FINANCIAL IMPAIRMENT

Assessment Task Part B:

1. Absence of former accounting standards in the economic reality

In 1 out of 3 companies that are utilizing the US GAAP or IFRS standards are

recognizably affected by various forms of the accounting techniques. The current status is

reflecting that the organizations under these standards amount and commits for more than 3.3

trillion (Ifrs.org. 2018). It is noticed that almost 85% of the total asset are not shown in the

financial statement or balance sheet of the company as these are considered as the operational

leases. The real liability is created if these leases are not shown. Therefore, the company can face

bankruptcy if it does not maintain the standards with the latest economic reality during the

financial crisis (Fitó, Moya and Orgaz 2013). The company is committed towards the long-term

operating leases which were shown as lean in the balance sheet.

2. Reasons why under the previous accounting standards the lease liabilities of the

reporting entities in the balance sheet were 66 times more than the reported debts under

the balance sheet

The earlier accounting standards present the report, which determines 85% of the

operating lease and it even reflects on the balance sheet. It creates the real liability even though it

is not mentioned in the balance sheet (Fitó, Moya and Orgaz 2013). Therefore, during the time of

the financial crisis, the major companies need to make the amendments in the economic reality.

The company even requires developing the commitments for the long-term operating leases due

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

FINANCIAL IMPAIRMENT

to which it is noticed that the lease liabilities are proved to be 66 times more than compared to

the existing debts under balance sheet.

3. Views of IASB Chairperson regarding the accounting standards

The former lease accounting technique lacks the compatibility. Airline industries usually

deal with the operating leases, which are not shown in the balance sheet or in the financial

statement. Therefore, the airline firm is proved to be quite dissimilar from the competitors that

are purchasing the overall fleets (Lee and Hooy 2012). There is no sign of the negligible level

playing field foreseen among the airline industry. Hence, these leases are considered as the

liabilities of the firm.

4. The view of Chairperson about the ineffectiveness of the new standards

The new standards is not considered to be popular among the companies but is expected

to have the long impacts in many of the listed companies. The changes are made in a very

controversial way (Banker, Basu and Byzalov 2016). It can even create negative impact on the

economic situations and the fair costs. It is necessary for the organization to accept the changes

readily and make amendments in the balance sheet and the income statements. For instance,

several contractual arrangements and banking covenants are associated with the financial

statement

5. Possibilities in providing better improvement in investment decisions

The operating lease for all the new documents are treated as off balance sheet items in the

former accounting standards. The complete picture about the financial business position is not

there with the financial statement users or the investors. Thus, it is not possible to compare the

FINANCIAL IMPAIRMENT

to which it is noticed that the lease liabilities are proved to be 66 times more than compared to

the existing debts under balance sheet.

3. Views of IASB Chairperson regarding the accounting standards

The former lease accounting technique lacks the compatibility. Airline industries usually

deal with the operating leases, which are not shown in the balance sheet or in the financial

statement. Therefore, the airline firm is proved to be quite dissimilar from the competitors that

are purchasing the overall fleets (Lee and Hooy 2012). There is no sign of the negligible level

playing field foreseen among the airline industry. Hence, these leases are considered as the

liabilities of the firm.

4. The view of Chairperson about the ineffectiveness of the new standards

The new standards is not considered to be popular among the companies but is expected

to have the long impacts in many of the listed companies. The changes are made in a very

controversial way (Banker, Basu and Byzalov 2016). It can even create negative impact on the

economic situations and the fair costs. It is necessary for the organization to accept the changes

readily and make amendments in the balance sheet and the income statements. For instance,

several contractual arrangements and banking covenants are associated with the financial

statement

5. Possibilities in providing better improvement in investment decisions

The operating lease for all the new documents are treated as off balance sheet items in the

former accounting standards. The complete picture about the financial business position is not

there with the financial statement users or the investors. Thus, it is not possible to compare the

11

FINANCIAL IMPAIRMENT

organization are buying assets and that are leasing assets. IFRS 16 consist of advanced updates

which can be used for outweighing costs and providing better decisions.

FINANCIAL IMPAIRMENT

organization are buying assets and that are leasing assets. IFRS 16 consist of advanced updates

which can be used for outweighing costs and providing better decisions.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.