Impact of IFRS on Financial Reporting

VerifiedAdded on 2020/05/16

|15

|3074

|72

AI Summary

This assignment explores the influence of International Financial Reporting Standards (IFRS) on financial reporting practices. It examines specific areas such as goodwill accounting under IFRS, including impairment testing and compliance challenges, and the impact of operating lease capitalization on key financial ratios. Students are expected to analyze scholarly articles and resources to understand the complexities and implications of IFRS adoption in accounting.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: FINANCIAL IMPAIRMENT

FINANCIAL IMPAIRMENT

Name of the Student

Name of the University

Author Note

FINANCIAL IMPAIRMENT

Name of the Student

Name of the University

Author Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1FINANCIAL IMPAIRMENT

Table of Contents

Assessment task Part A....................................................................................................................2

(i) Assets tested for impairment................................................................................................2

(ii) Method of conducting the impairment test.......................................................................3

(iii) Impairment expenditures...................................................................................................4

(iv) Assumptions and estimates used by the company for conducting impairment test..........4

For the calculation of value-in use the assumptions are as follows:............................................5

(v) Subjectivity involved in the process of impairment testing..............................................5

(vi) Interesting, surprising, difficult or confusing part to understand impairment testing.......6

(vii) New insights regarding conducting the impairment.........................................................6

(viii) Fair value measurement....................................................................................................7

Assesstment task Part B...................................................................................................................8

(i) Reason why the former accounting standards does not reflect the economic reality...........8

(ii) Reasons why under the previous accounting standards the lease liabilities of the

reporting entities in the balance sheet were 66 times more than the reported debts under the

balance sheet................................................................................................................................8

(iii) Reasons why the Chairperson of IASB is in the view that under the previous accounting

standard no level playing field was there among some airline entities.......................................9

(iv) Reasons why the Chairperson is in the view that the new standard will not be popular

with everyone...............................................................................................................................9

Table of Contents

Assessment task Part A....................................................................................................................2

(i) Assets tested for impairment................................................................................................2

(ii) Method of conducting the impairment test.......................................................................3

(iii) Impairment expenditures...................................................................................................4

(iv) Assumptions and estimates used by the company for conducting impairment test..........4

For the calculation of value-in use the assumptions are as follows:............................................5

(v) Subjectivity involved in the process of impairment testing..............................................5

(vi) Interesting, surprising, difficult or confusing part to understand impairment testing.......6

(vii) New insights regarding conducting the impairment.........................................................6

(viii) Fair value measurement....................................................................................................7

Assesstment task Part B...................................................................................................................8

(i) Reason why the former accounting standards does not reflect the economic reality...........8

(ii) Reasons why under the previous accounting standards the lease liabilities of the

reporting entities in the balance sheet were 66 times more than the reported debts under the

balance sheet................................................................................................................................8

(iii) Reasons why the Chairperson of IASB is in the view that under the previous accounting

standard no level playing field was there among some airline entities.......................................9

(iv) Reasons why the Chairperson is in the view that the new standard will not be popular

with everyone...............................................................................................................................9

2FINANCIAL IMPAIRMENT

(v) Possibilities that the new visibility with regard to all the leases will result into better

informed decision for investment................................................................................................9

References......................................................................................................................................11

(v) Possibilities that the new visibility with regard to all the leases will result into better

informed decision for investment................................................................................................9

References......................................................................................................................................11

3FINANCIAL IMPAIRMENT

Assessment task Part A

The given report aims to throw light on the impairment component and the assumptions,

which have been used by AMP Limited to prepare their financial statements and conduct the

impairment tests on the given assets. The report shall also elaborate on the procedures of

impairment testing which are often used by the company and describes the subjectivity that will

be involved in the given procedure of conducting the given test (Amiraslani, Iatridis & Pope,

2013). The annual report of the chosen company has been taken for the year ended as on 31

December 2016. AML Limited is a bay area sales agency, which promotes various interior

decoration products. It has a large variety of flooring products for end users, architects and

various design clients. It has products like rugs, flooring equipments, furniture and other interior

item (Annualreports.com, 2018). The company is established in Australia and makes use of a

wide variety of experience to inculcate new ideas and experience for the given consumers.

An impaired asset of a company can be defined as an asset, which has a market value less

than that of the carrying value of the given asset. The assets that are most likely to get impaired

are the fixed tangible assets like property, plant and equipment. Intangible assets include

accounts receivable, goodwill and others (loans, retirement & education, 2018). When the asset

is impaired against its carrying value , the loss incurred is recorded in the income statement of

the given company. After this procedure is followed, the asset reflects a reduced carrying cost

and the given adjustments shall be recognized as a loss and this shall result in the reduction in the

value of an asset.

Assessment task Part A

The given report aims to throw light on the impairment component and the assumptions,

which have been used by AMP Limited to prepare their financial statements and conduct the

impairment tests on the given assets. The report shall also elaborate on the procedures of

impairment testing which are often used by the company and describes the subjectivity that will

be involved in the given procedure of conducting the given test (Amiraslani, Iatridis & Pope,

2013). The annual report of the chosen company has been taken for the year ended as on 31

December 2016. AML Limited is a bay area sales agency, which promotes various interior

decoration products. It has a large variety of flooring products for end users, architects and

various design clients. It has products like rugs, flooring equipments, furniture and other interior

item (Annualreports.com, 2018). The company is established in Australia and makes use of a

wide variety of experience to inculcate new ideas and experience for the given consumers.

An impaired asset of a company can be defined as an asset, which has a market value less

than that of the carrying value of the given asset. The assets that are most likely to get impaired

are the fixed tangible assets like property, plant and equipment. Intangible assets include

accounts receivable, goodwill and others (loans, retirement & education, 2018). When the asset

is impaired against its carrying value , the loss incurred is recorded in the income statement of

the given company. After this procedure is followed, the asset reflects a reduced carrying cost

and the given adjustments shall be recognized as a loss and this shall result in the reduction in the

value of an asset.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4FINANCIAL IMPAIRMENT

(i) Assets tested for impairment

As per the annual report of the given company, AML Limited for the year ended as on

December 2016, the company tested the given assets for impairment-

The Goodwill as well as the intangible assets have not been amortized and so it is tested

for the impairment criteria annually or even frequently which means for more than 1 time

in an year if there results any changes in a circumstance or if there occurs a particular

event which may indicate that the asset may be required to be impaired. This shall result

in the asset being carried on to the financial statement at a reduced cost in a method by

which the accumulated losses are taken on the account of impairment (Amiraslani,

Iatridis & Pope, 2013). Other assets, which are plant, property, investors and equipment,

may be tested for the impairment when there is an indication from sources that the

amount they have been carrying will not be recoverable.

(ii) Method of conducting the impairment test

Like stated earlier, the assets except the goodwill and the intangible assets might be

tested for impairment in cases where an indication is received that the carrying amount of the

given asset may not be able to be recovered. However, there may arise cases whereby the

intangible assets and other goodwill that are not amortized earlier may be tested for impairment

annually or may be tested for more than once in a year. This may happen when any circum

stance or an event indicates so (Andrews, 2012). For the assessment of impairment, the given

class of assets is grouped together at their lowest levels, which can be easily identified as a

separate cash inflow and are independent of cash inflows of the other classes of assets, which are

the cash generating units. The non-financial assets except the goodwill one on which the

(i) Assets tested for impairment

As per the annual report of the given company, AML Limited for the year ended as on

December 2016, the company tested the given assets for impairment-

The Goodwill as well as the intangible assets have not been amortized and so it is tested

for the impairment criteria annually or even frequently which means for more than 1 time

in an year if there results any changes in a circumstance or if there occurs a particular

event which may indicate that the asset may be required to be impaired. This shall result

in the asset being carried on to the financial statement at a reduced cost in a method by

which the accumulated losses are taken on the account of impairment (Amiraslani,

Iatridis & Pope, 2013). Other assets, which are plant, property, investors and equipment,

may be tested for the impairment when there is an indication from sources that the

amount they have been carrying will not be recoverable.

(ii) Method of conducting the impairment test

Like stated earlier, the assets except the goodwill and the intangible assets might be

tested for impairment in cases where an indication is received that the carrying amount of the

given asset may not be able to be recovered. However, there may arise cases whereby the

intangible assets and other goodwill that are not amortized earlier may be tested for impairment

annually or may be tested for more than once in a year. This may happen when any circum

stance or an event indicates so (Andrews, 2012). For the assessment of impairment, the given

class of assets is grouped together at their lowest levels, which can be easily identified as a

separate cash inflow and are independent of cash inflows of the other classes of assets, which are

the cash generating units. The non-financial assets except the goodwill one on which the

5FINANCIAL IMPAIRMENT

impairment has been analyzed because there are certain possibilities of the reversal o the same at

each date of reporting.

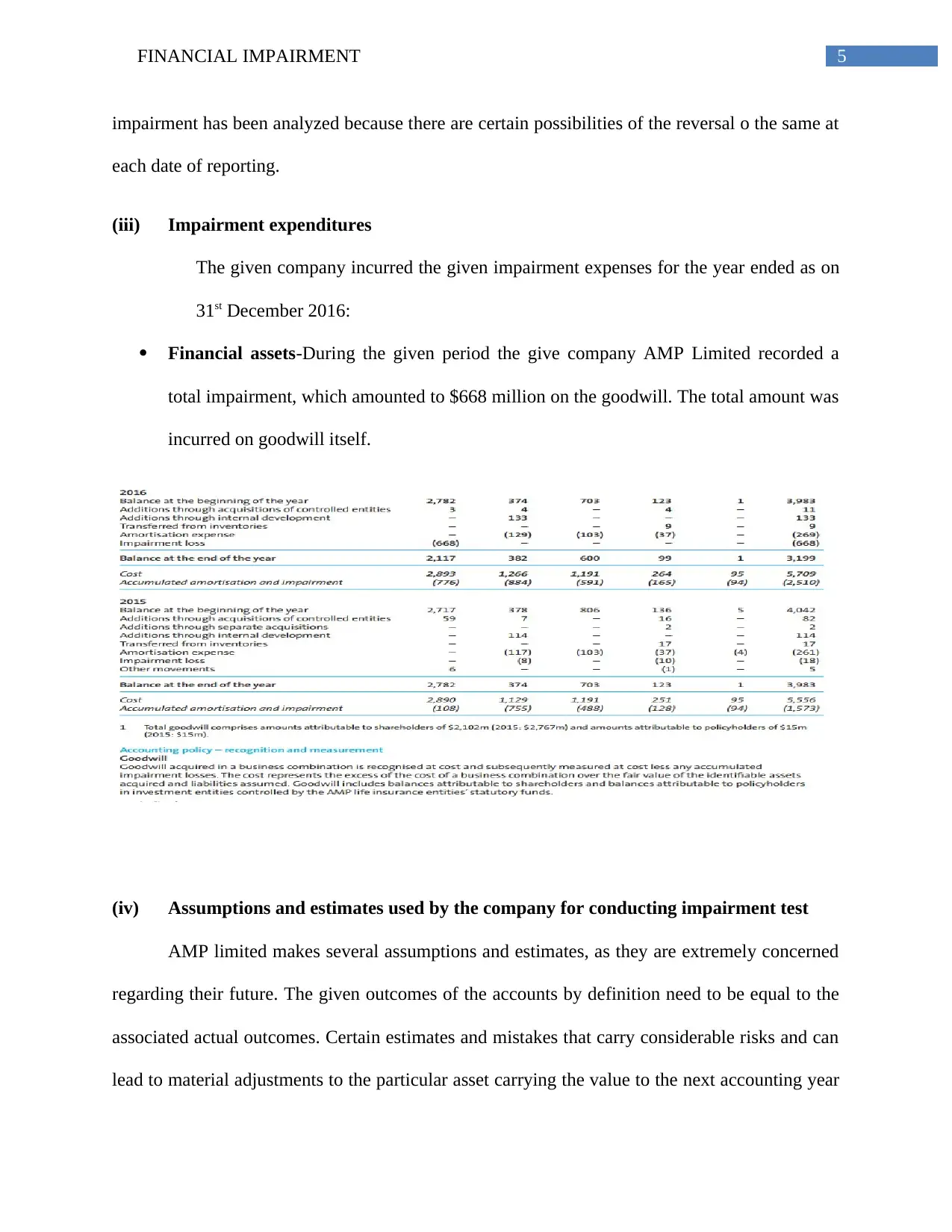

(iii) Impairment expenditures

The given company incurred the given impairment expenses for the year ended as on

31st December 2016:

Financial assets-During the given period the give company AMP Limited recorded a

total impairment, which amounted to $668 million on the goodwill. The total amount was

incurred on goodwill itself.

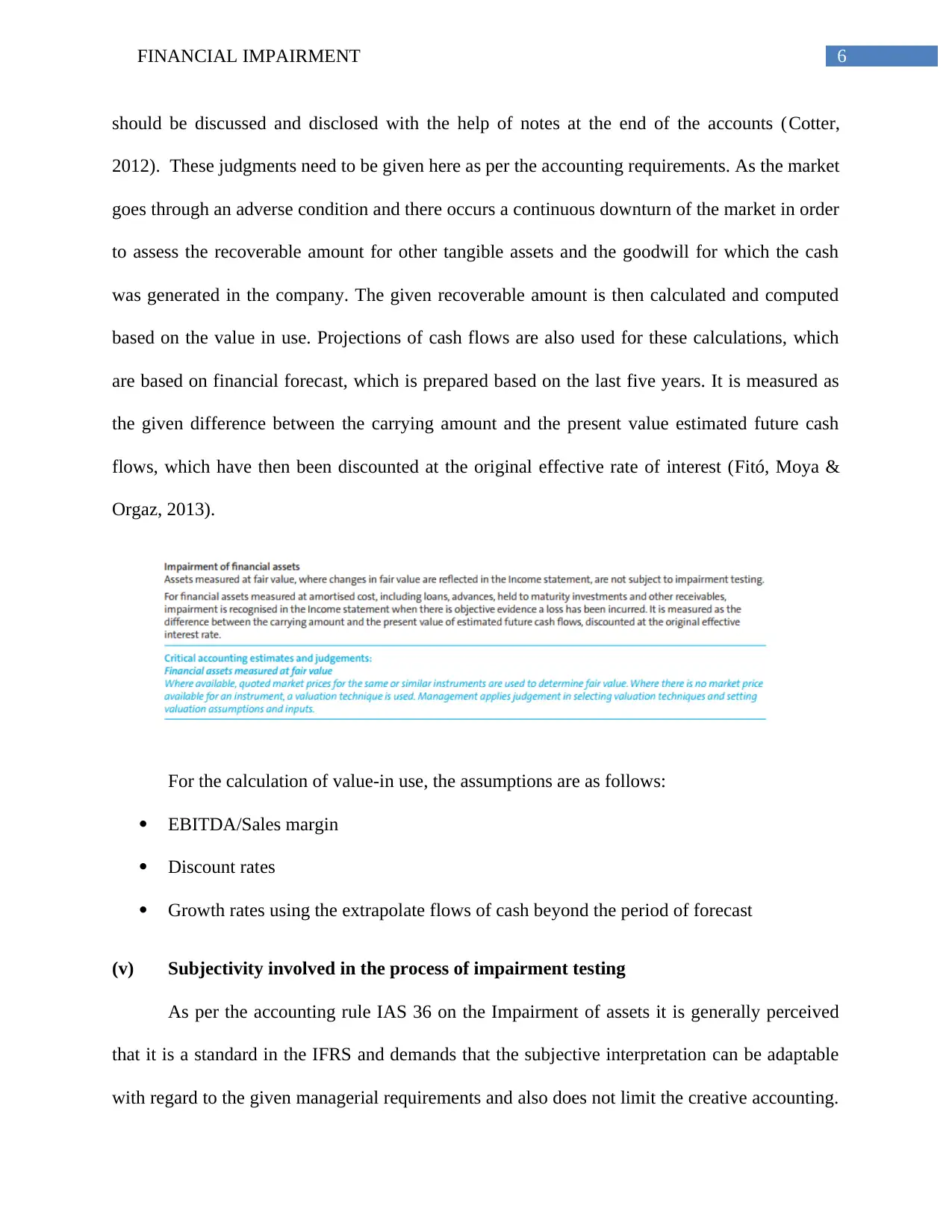

(iv) Assumptions and estimates used by the company for conducting impairment test

AMP limited makes several assumptions and estimates, as they are extremely concerned

regarding their future. The given outcomes of the accounts by definition need to be equal to the

associated actual outcomes. Certain estimates and mistakes that carry considerable risks and can

lead to material adjustments to the particular asset carrying the value to the next accounting year

impairment has been analyzed because there are certain possibilities of the reversal o the same at

each date of reporting.

(iii) Impairment expenditures

The given company incurred the given impairment expenses for the year ended as on

31st December 2016:

Financial assets-During the given period the give company AMP Limited recorded a

total impairment, which amounted to $668 million on the goodwill. The total amount was

incurred on goodwill itself.

(iv) Assumptions and estimates used by the company for conducting impairment test

AMP limited makes several assumptions and estimates, as they are extremely concerned

regarding their future. The given outcomes of the accounts by definition need to be equal to the

associated actual outcomes. Certain estimates and mistakes that carry considerable risks and can

lead to material adjustments to the particular asset carrying the value to the next accounting year

6FINANCIAL IMPAIRMENT

should be discussed and disclosed with the help of notes at the end of the accounts (Cotter,

2012). These judgments need to be given here as per the accounting requirements. As the market

goes through an adverse condition and there occurs a continuous downturn of the market in order

to assess the recoverable amount for other tangible assets and the goodwill for which the cash

was generated in the company. The given recoverable amount is then calculated and computed

based on the value in use. Projections of cash flows are also used for these calculations, which

are based on financial forecast, which is prepared based on the last five years. It is measured as

the given difference between the carrying amount and the present value estimated future cash

flows, which have then been discounted at the original effective rate of interest (Fitó, Moya &

Orgaz, 2013).

For the calculation of value-in use, the assumptions are as follows:

EBITDA/Sales margin

Discount rates

Growth rates using the extrapolate flows of cash beyond the period of forecast

(v) Subjectivity involved in the process of impairment testing

As per the accounting rule IAS 36 on the Impairment of assets it is generally perceived

that it is a standard in the IFRS and demands that the subjective interpretation can be adaptable

with regard to the given managerial requirements and also does not limit the creative accounting.

should be discussed and disclosed with the help of notes at the end of the accounts (Cotter,

2012). These judgments need to be given here as per the accounting requirements. As the market

goes through an adverse condition and there occurs a continuous downturn of the market in order

to assess the recoverable amount for other tangible assets and the goodwill for which the cash

was generated in the company. The given recoverable amount is then calculated and computed

based on the value in use. Projections of cash flows are also used for these calculations, which

are based on financial forecast, which is prepared based on the last five years. It is measured as

the given difference between the carrying amount and the present value estimated future cash

flows, which have then been discounted at the original effective rate of interest (Fitó, Moya &

Orgaz, 2013).

For the calculation of value-in use, the assumptions are as follows:

EBITDA/Sales margin

Discount rates

Growth rates using the extrapolate flows of cash beyond the period of forecast

(v) Subjectivity involved in the process of impairment testing

As per the accounting rule IAS 36 on the Impairment of assets it is generally perceived

that it is a standard in the IFRS and demands that the subjective interpretation can be adaptable

with regard to the given managerial requirements and also does not limit the creative accounting.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL IMPAIRMENT

It can be reflected from the annual report of AMP Limited that there is a lot of involvement of

subjectivity in the given statement while the management was under the process of carrying out

the impairment test (Ifrs.org, 2018). This could be done because the management had the given

opportunity to exploit their discretion and they carried out the goodwill impairment test in an

opportunistic manner. This is further proved by the fact that the allocation of goodwill and the

computation of the recoverable amount when there does not exist any availability of the active

prices, as the given goodwill is a subject of discretion.

(vi) Interesting, surprising, difficult or confusing part to understand impairment testing

After analysing the assessment, which was undertaken it could be, recognized that, the

most difficult part of the given assessment was the indication of the impairment. As it is as a

stated fact that the indication depends on a wide variety of internal as well as external factors

(Carlin & Finch, 2011). The frequency at which the impairment test may be conducted may

depend on the discretion of the management (Jennings & Marques, 2013). Hence, it is believed

that there are chances that the management will carry out the test by analysing the opportunity in

a case where there is a value downturn.

(vii) New insights regarding conducting the impairment

Impairment loss is often calculated as the difference between the carrying amount of the

given asset and the recoverable amount of the given asset. The recoverable amount, which is

present, is higher among the value in use and the fair value of the required asset is reduced by the

given disposable cost (Carlin, Finch & Laili, 2009). The determination of the fait value is done

using a sales agreement or the provided value of the asset in the given active market in which the

asset is traded on the information about the availability of the asset is received (Md

It can be reflected from the annual report of AMP Limited that there is a lot of involvement of

subjectivity in the given statement while the management was under the process of carrying out

the impairment test (Ifrs.org, 2018). This could be done because the management had the given

opportunity to exploit their discretion and they carried out the goodwill impairment test in an

opportunistic manner. This is further proved by the fact that the allocation of goodwill and the

computation of the recoverable amount when there does not exist any availability of the active

prices, as the given goodwill is a subject of discretion.

(vi) Interesting, surprising, difficult or confusing part to understand impairment testing

After analysing the assessment, which was undertaken it could be, recognized that, the

most difficult part of the given assessment was the indication of the impairment. As it is as a

stated fact that the indication depends on a wide variety of internal as well as external factors

(Carlin & Finch, 2011). The frequency at which the impairment test may be conducted may

depend on the discretion of the management (Jennings & Marques, 2013). Hence, it is believed

that there are chances that the management will carry out the test by analysing the opportunity in

a case where there is a value downturn.

(vii) New insights regarding conducting the impairment

Impairment loss is often calculated as the difference between the carrying amount of the

given asset and the recoverable amount of the given asset. The recoverable amount, which is

present, is higher among the value in use and the fair value of the required asset is reduced by the

given disposable cost (Carlin, Finch & Laili, 2009). The determination of the fait value is done

using a sales agreement or the provided value of the asset in the given active market in which the

asset is traded on the information about the availability of the asset is received (Md

8FINANCIAL IMPAIRMENT

Khokan ,Sheikh & Mollik, 2014). The value in use as per IAS 36 is the present value of cash

glows, which can be received from the asset.

(viii) Fair value measurement

As per the IFRS 13, fair value is determined with the help of-

Sales agreement

The availability of the best information to reveal the given amount at which the

company is going to sell the highlighted asset

The market value of the asset.

Khokan ,Sheikh & Mollik, 2014). The value in use as per IAS 36 is the present value of cash

glows, which can be received from the asset.

(viii) Fair value measurement

As per the IFRS 13, fair value is determined with the help of-

Sales agreement

The availability of the best information to reveal the given amount at which the

company is going to sell the highlighted asset

The market value of the asset.

9FINANCIAL IMPAIRMENT

Assessment task Part B

(i) Reason why the former accounting standards does not reflect the economic

reality

Nearly 50% of the companies who make the use of the GAAP or the IFRS have been

affected by the changes in accounting rules. The status currently states that the companies who

tend to follow the US GAAP or the IFRS have certain commitments and their given leased assets

come up to around 3.3 trillion (Carlin & Finch, 2010). Out of these figures, there are 85% of

companies who have stated that they do not report in their balance sheet as they treat these

figures as operating leases. In order to compensate this, the investors in hand generally take care

of the estimates, which are inconsistent and incomparable (Lee & Hooy, 2013). Hence, the

statement has been given that the former accounting standards do not reflect the reality.

(ii) Reasons why under the previous accounting standards the lease liabilities of the

reporting entities in the balance sheet were 66 times more than the reported

debts under the balance sheet

According to the previous accounting standards, the companies only tend to report

around 85% of their lease agreements, which was classified under the operating lease segment.

They do not reflect this on the balance sheet as they created actual liabilities. This resulted in a

number of companies going bankrupt during the financial crises period because they were unable

to adjust to the economic reality on time (Rennekamp, Rupar & Seybert, 2014). They had certain

commitments to the long-term operating leases, as their balance sheets were quite lean. Hence,

the given lease liabilities in the balance sheets were 66 times more when compared to the debt of

the balance sheet.

Assessment task Part B

(i) Reason why the former accounting standards does not reflect the economic

reality

Nearly 50% of the companies who make the use of the GAAP or the IFRS have been

affected by the changes in accounting rules. The status currently states that the companies who

tend to follow the US GAAP or the IFRS have certain commitments and their given leased assets

come up to around 3.3 trillion (Carlin & Finch, 2010). Out of these figures, there are 85% of

companies who have stated that they do not report in their balance sheet as they treat these

figures as operating leases. In order to compensate this, the investors in hand generally take care

of the estimates, which are inconsistent and incomparable (Lee & Hooy, 2013). Hence, the

statement has been given that the former accounting standards do not reflect the reality.

(ii) Reasons why under the previous accounting standards the lease liabilities of the

reporting entities in the balance sheet were 66 times more than the reported

debts under the balance sheet

According to the previous accounting standards, the companies only tend to report

around 85% of their lease agreements, which was classified under the operating lease segment.

They do not reflect this on the balance sheet as they created actual liabilities. This resulted in a

number of companies going bankrupt during the financial crises period because they were unable

to adjust to the economic reality on time (Rennekamp, Rupar & Seybert, 2014). They had certain

commitments to the long-term operating leases, as their balance sheets were quite lean. Hence,

the given lease liabilities in the balance sheets were 66 times more when compared to the debt of

the balance sheet.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10FINANCIAL IMPAIRMENT

(iii) Reasons why the Chairperson of IASB is in the view that under the previous

accounting standard no level playing field was there among some airline entities

Comparability cannot be done using the former accounting systems. The airline

industries tend to use the leases under operating leases and tend to not record it under the

balance sheet. Due to this reason, an airline company whose whole fleet is under rent

accounts will differ from the one who purchase their fleets even though the financial

obligations of the airline companies are almost the same (Ramanna & Watts, 2012).For

this reason, there will be no level playing field among the given airline companies . As

the new standard will be introduced, all these leases will be taken as assets and the

lessees will account as a liability. With this, the problem is expected to be resolved.

(iv) Reasons why the Chairperson is in the view that the new standard will not be

popular with everyone

As the new standard will be introduced, it is expected that it will almost every

company will be affected by the new standard. The changes that will occur are always

controversial and hence, they might not be popular among all. The given changes will be

brought about in the income statement as well as the balance sheet. Hence, it is believed

that these changes will have bigger impacts (Marshall, 2016). Due to these statements, all

departments of a business will be affected and they need to change their process to abide

by the new accounting standard.

(v) Possibilities that the new visibility with regard to all the leases will result into

better informed decision for investment

With the given changes in the former accounting standards, the companies shall

be treating the leases in a new manner. With the given change the investors shall be able

(iii) Reasons why the Chairperson of IASB is in the view that under the previous

accounting standard no level playing field was there among some airline entities

Comparability cannot be done using the former accounting systems. The airline

industries tend to use the leases under operating leases and tend to not record it under the

balance sheet. Due to this reason, an airline company whose whole fleet is under rent

accounts will differ from the one who purchase their fleets even though the financial

obligations of the airline companies are almost the same (Ramanna & Watts, 2012).For

this reason, there will be no level playing field among the given airline companies . As

the new standard will be introduced, all these leases will be taken as assets and the

lessees will account as a liability. With this, the problem is expected to be resolved.

(iv) Reasons why the Chairperson is in the view that the new standard will not be

popular with everyone

As the new standard will be introduced, it is expected that it will almost every

company will be affected by the new standard. The changes that will occur are always

controversial and hence, they might not be popular among all. The given changes will be

brought about in the income statement as well as the balance sheet. Hence, it is believed

that these changes will have bigger impacts (Marshall, 2016). Due to these statements, all

departments of a business will be affected and they need to change their process to abide

by the new accounting standard.

(v) Possibilities that the new visibility with regard to all the leases will result into

better informed decision for investment

With the given changes in the former accounting standards, the companies shall

be treating the leases in a new manner. With the given change the investors shall be able

11FINANCIAL IMPAIRMENT

to have an entire picture of the company`s financial position at once and this reflects

transparency. They can even compare between different companies and invest accurately.

The update of the IFRS 16 will outweigh the costs and result in better decisions.

to have an entire picture of the company`s financial position at once and this reflects

transparency. They can even compare between different companies and invest accurately.

The update of the IFRS 16 will outweigh the costs and result in better decisions.

12FINANCIAL IMPAIRMENT

References

Amiraslani, H., Iatridis, G.E. & Pope, P.F. (2013). Accounting for asset impairment. London:

Cass Business School.

Amiraslani, H., Iatridis, G.E. & Pope, P.F. (2013). Accounting for asset impairment: a test for

IFRS compliance across Europe. Centre for Financial Analysis and Reporting Research

(CeFARR).

Andrews, R. (2012). Fair Value, earnings management and asset impairment: The impact of a

change in the regulatory environment. Procedia Economics and Finance, 2, pp.16-25.

Annualreports.com. (2018). Annualreports.com. Retrieved 23 January 2018, from

http://www.annualreports.com/HostedData/AnnualReports/PDF/OTC_AMLTY_2016.pd

f

Carlin, T.M. & Finch, N. (2010), Resisting compliance with IFRS goodwill accounting and

reporting disclosures evidence from Australia, Journal of Accounting & Organizational

Change, Vol. 6 No. 2, pp. 260-280. [Google Scholar] [Link] [Infotrieve]

Carlin, T.M. & Finch, N. (2011), Goodwill impairment testing under IFRS: a false impossible

shore?, Pacific Accounting Review, Vol. 23 No. 3, pp. 368-392. [Google Scholar] [Link]

[Infotrieve]

Carlin, T.M., Finch, N. & Laili, N.H. (2009), Goodwill accounting in Malaysia and the

transition to IFRS – a compliance assessment of large first year adopters, Journal of

References

Amiraslani, H., Iatridis, G.E. & Pope, P.F. (2013). Accounting for asset impairment. London:

Cass Business School.

Amiraslani, H., Iatridis, G.E. & Pope, P.F. (2013). Accounting for asset impairment: a test for

IFRS compliance across Europe. Centre for Financial Analysis and Reporting Research

(CeFARR).

Andrews, R. (2012). Fair Value, earnings management and asset impairment: The impact of a

change in the regulatory environment. Procedia Economics and Finance, 2, pp.16-25.

Annualreports.com. (2018). Annualreports.com. Retrieved 23 January 2018, from

http://www.annualreports.com/HostedData/AnnualReports/PDF/OTC_AMLTY_2016.pd

f

Carlin, T.M. & Finch, N. (2010), Resisting compliance with IFRS goodwill accounting and

reporting disclosures evidence from Australia, Journal of Accounting & Organizational

Change, Vol. 6 No. 2, pp. 260-280. [Google Scholar] [Link] [Infotrieve]

Carlin, T.M. & Finch, N. (2011), Goodwill impairment testing under IFRS: a false impossible

shore?, Pacific Accounting Review, Vol. 23 No. 3, pp. 368-392. [Google Scholar] [Link]

[Infotrieve]

Carlin, T.M., Finch, N. & Laili, N.H. (2009), Goodwill accounting in Malaysia and the

transition to IFRS – a compliance assessment of large first year adopters, Journal of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13FINANCIAL IMPAIRMENT

Financial Reporting & Accounting, Vol. 7 No. 1, pp. 75-104. [Google Scholar] [Link]

[Infotrieve]

Cotter, D. (2012). Advanced financial reporting: A complete guide to IFRS. Financial

Times/Prentice Hall.

Fitó, M.À., Moya, S. & Orgaz, N. (2013). Considering the effects of operating lease

capitalization on key financial ratios. Spanish Journal of Finance and Accounting/Revista

Española de Financiación y Contabilidad, 42(159), pp.341-369.

Ifrs.org. (2018). IFRS. [online] Available at: http://www.ifrs.org/ [Accessed 23 Jan. 2018].

Jennings, R. & Marques, A. (2013). Amortized cost for operating lease assets. Accounting

Horizons, 27(1), pp.51-74.

Lee, C.H. & Hooy, C.W. (2013). Determinants of systematic financial risk exposures of airlines

in North America, Europe and Asia. Journal of Air Transport Management, 24, pp.31-35.

loans, H., retirement, S., & education, N. (2018). Bank Accounts, Super, Insurance & Home

Loans - AMP. Amp.com.au. Retrieved 23 January 2018, from https://www.amp.com.au/

Marshall, D. (2016). Accounting: What the numbers mean. McGraw-Hill Higher Education.

Md Khokan Bepari, Sheikh F. Rahman & Abu Taher Mollik. (2014) Firms' compliance with the

disclosure requirements of IFRS for goodwill impairment testing: Effect of the global

financial crisis and other firm characteristics, Journal of Accounting & Organizational

Change, Vol. 10 Issue: 1, pp.116149, https://doi.org/10.1108/JAOC-02-2011-0008

Financial Reporting & Accounting, Vol. 7 No. 1, pp. 75-104. [Google Scholar] [Link]

[Infotrieve]

Cotter, D. (2012). Advanced financial reporting: A complete guide to IFRS. Financial

Times/Prentice Hall.

Fitó, M.À., Moya, S. & Orgaz, N. (2013). Considering the effects of operating lease

capitalization on key financial ratios. Spanish Journal of Finance and Accounting/Revista

Española de Financiación y Contabilidad, 42(159), pp.341-369.

Ifrs.org. (2018). IFRS. [online] Available at: http://www.ifrs.org/ [Accessed 23 Jan. 2018].

Jennings, R. & Marques, A. (2013). Amortized cost for operating lease assets. Accounting

Horizons, 27(1), pp.51-74.

Lee, C.H. & Hooy, C.W. (2013). Determinants of systematic financial risk exposures of airlines

in North America, Europe and Asia. Journal of Air Transport Management, 24, pp.31-35.

loans, H., retirement, S., & education, N. (2018). Bank Accounts, Super, Insurance & Home

Loans - AMP. Amp.com.au. Retrieved 23 January 2018, from https://www.amp.com.au/

Marshall, D. (2016). Accounting: What the numbers mean. McGraw-Hill Higher Education.

Md Khokan Bepari, Sheikh F. Rahman & Abu Taher Mollik. (2014) Firms' compliance with the

disclosure requirements of IFRS for goodwill impairment testing: Effect of the global

financial crisis and other firm characteristics, Journal of Accounting & Organizational

Change, Vol. 10 Issue: 1, pp.116149, https://doi.org/10.1108/JAOC-02-2011-0008

14FINANCIAL IMPAIRMENT

Ramanna, K. & Watts, R.L. (2012). Evidence on the use of unverifiable estimates in required

goodwill impairment. Review of Accounting Studies, 17(4), pp.749-780.

Rennekamp, K., Rupar, K.K. & Seybert, N. (2014). Impaired judgment: The effects of asset

impairment reversibility and cognitive dissonance on future investment. The Accounting

Review, 90(2), pp.739-759.

Ramanna, K. & Watts, R.L. (2012). Evidence on the use of unverifiable estimates in required

goodwill impairment. Review of Accounting Studies, 17(4), pp.749-780.

Rennekamp, K., Rupar, K.K. & Seybert, N. (2014). Impaired judgment: The effects of asset

impairment reversibility and cognitive dissonance on future investment. The Accounting

Review, 90(2), pp.739-759.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.