Financial Analysis Report: Qantas and Emirates Performance Comparison

VerifiedAdded on 2020/06/06

|38

|11354

|75

Report

AI Summary

This financial analysis report compares the financial positions of Qantas and Emirates, two major airlines. It utilizes various financial tools, including profitability, efficiency, liquidity, and gearing ratios, to assess their performance. The report also conducts horizontal and vertical analyses to evaluate growth trends and uses comparative analysis to benchmark the two companies. Furthermore, it examines both financial and non-financial measures to evaluate Qantas's performance, identifying its strengths and weaknesses. The analysis reveals insights into each company's financial health, helping to identify areas for improvement and strategic decision-making in the aviation industry. The report concludes with recommendations based on the findings.

Financial Analysis Report

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

EXECUTIVE SUMMARY.............................................................................................................1

INTRODUCTION...........................................................................................................................2

TASK...............................................................................................................................................2

A. Profitability ratios...................................................................................................................2

B. Efficiency ratios......................................................................................................................6

C. Liquidity ratios.....................................................................................................................10

D. Gearing ratios.......................................................................................................................12

E. Horizontal common size analysis.........................................................................................14

F. Vertical common size analysis..............................................................................................19

G. Comparative analysis...........................................................................................................22

H. Evaluation of performance of business................................................................................25

CONCLUSION AND RECOMMENDATIONS..........................................................................26

REFERENCES..............................................................................................................................27

APPENDIX....................................................................................................................................28

EXECUTIVE SUMMARY.............................................................................................................1

INTRODUCTION...........................................................................................................................2

TASK...............................................................................................................................................2

A. Profitability ratios...................................................................................................................2

B. Efficiency ratios......................................................................................................................6

C. Liquidity ratios.....................................................................................................................10

D. Gearing ratios.......................................................................................................................12

E. Horizontal common size analysis.........................................................................................14

F. Vertical common size analysis..............................................................................................19

G. Comparative analysis...........................................................................................................22

H. Evaluation of performance of business................................................................................25

CONCLUSION AND RECOMMENDATIONS..........................................................................26

REFERENCES..............................................................................................................................27

APPENDIX....................................................................................................................................28

EXECUTIVE SUMMARY

In this report there is the analysis carried out in context of financial position of Qantas

and emirates. There will be various aspects which are present in business which are related to

finance and for them analysis will have to be carried out. Under this certain tools are there that

are used. They involve ratio analysis in which various sectors such as profitability, liquidity,

efficiency and gearing are measured. It is identified that whether company is able to meet all the

requirements and standards in proper manner. Another part of the report shows horizontal and

vertical analysis that is carried out. In that performance of various years is compared so that

growth level can be determined and it can be known that how much development has taken

place. In addition to them comparative analysis is also done where the working of both the

companies are compared with one another so that it can be known that which one is better among

them. There are various measures that are used for performance evaluation and it includes both

financial and non financial methods. In this report a evaluation segment is made in which

performance of Qantas is taken into consideration and various aspects such as its structure,

performance measures and other factors are taken into consideration. In the analysis it is

identified that performance of which is growing at faster speed and which is in loss. All of these

are very important to carry on the business in most successful manner as by this all shortcomings

are identified and then measures are taken to remove them. This way it will be possible to make

the development process even better and fast.

1

In this report there is the analysis carried out in context of financial position of Qantas

and emirates. There will be various aspects which are present in business which are related to

finance and for them analysis will have to be carried out. Under this certain tools are there that

are used. They involve ratio analysis in which various sectors such as profitability, liquidity,

efficiency and gearing are measured. It is identified that whether company is able to meet all the

requirements and standards in proper manner. Another part of the report shows horizontal and

vertical analysis that is carried out. In that performance of various years is compared so that

growth level can be determined and it can be known that how much development has taken

place. In addition to them comparative analysis is also done where the working of both the

companies are compared with one another so that it can be known that which one is better among

them. There are various measures that are used for performance evaluation and it includes both

financial and non financial methods. In this report a evaluation segment is made in which

performance of Qantas is taken into consideration and various aspects such as its structure,

performance measures and other factors are taken into consideration. In the analysis it is

identified that performance of which is growing at faster speed and which is in loss. All of these

are very important to carry on the business in most successful manner as by this all shortcomings

are identified and then measures are taken to remove them. This way it will be possible to make

the development process even better and fast.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

In the global economy, there are various sectors which are present and one of the most

important among them is aviation industry. By the help of airline services, people are able to

travel from one place to another in an easy and convenient manner. In order to survive in this

sector, it is needed that proper analysis shall be carried out so that all the shortcomings and faults

in system can be identified (Almazari, 2012). It is necessary that services shall be provided at the

lowest possible cost as then only, it will be able to deal with high level of competition that is

existing in market. There are various expenses which are to be incurred and in order to carry out

this business, license will have to be obtained from government so that it can travel to other

countries.

There are many airlines which are providing these services and in this report, two of them

are taken into consideration which are Qantas and Emirates. Qantas is one of the largest airlines

that is established in Australia which provides the best facilities by using advanced technologies.

Whereas, emirates is a Dubai based airline which is also providing such services. In this report,

analysis will be carried out in order to evaluate the position of both companies. For this purpose,

several ratios will be calculated and also, vertical and horizontal analysis will be performed

(David, 2011). This helps in knowing the working in respect of certain years that is done by both

of them. On the basis of them, comparison will be made among both the organisations. Financial

and non-financial measures will also be used to evaluate the performance of any one company.

TASK

A. Profitability ratios

In business, it is important that profitability shall be examined as by this, company's

performance will be reflected. All investors and analysts will be able to gain knowledge about its

position and on that basis, they can take required decisions for the making of investments. There

are various metrics which are used in finance and they are all classified with the help of these

ratios (Carfì and Musolino, 2011). By the help of them, ability of business in terms of making

good earnings will be evaluated and all the expenditures which are made during that particular

period will be compared. For the assessment of this, several tools are there which can be taken

into use. Some of the main ratios which are included in this are net profit margin, gross profit

margin, return on investment as well as return on assets and equity. They are to be calculated as

2

In the global economy, there are various sectors which are present and one of the most

important among them is aviation industry. By the help of airline services, people are able to

travel from one place to another in an easy and convenient manner. In order to survive in this

sector, it is needed that proper analysis shall be carried out so that all the shortcomings and faults

in system can be identified (Almazari, 2012). It is necessary that services shall be provided at the

lowest possible cost as then only, it will be able to deal with high level of competition that is

existing in market. There are various expenses which are to be incurred and in order to carry out

this business, license will have to be obtained from government so that it can travel to other

countries.

There are many airlines which are providing these services and in this report, two of them

are taken into consideration which are Qantas and Emirates. Qantas is one of the largest airlines

that is established in Australia which provides the best facilities by using advanced technologies.

Whereas, emirates is a Dubai based airline which is also providing such services. In this report,

analysis will be carried out in order to evaluate the position of both companies. For this purpose,

several ratios will be calculated and also, vertical and horizontal analysis will be performed

(David, 2011). This helps in knowing the working in respect of certain years that is done by both

of them. On the basis of them, comparison will be made among both the organisations. Financial

and non-financial measures will also be used to evaluate the performance of any one company.

TASK

A. Profitability ratios

In business, it is important that profitability shall be examined as by this, company's

performance will be reflected. All investors and analysts will be able to gain knowledge about its

position and on that basis, they can take required decisions for the making of investments. There

are various metrics which are used in finance and they are all classified with the help of these

ratios (Carfì and Musolino, 2011). By the help of them, ability of business in terms of making

good earnings will be evaluated and all the expenditures which are made during that particular

period will be compared. For the assessment of this, several tools are there which can be taken

into use. Some of the main ratios which are included in this are net profit margin, gross profit

margin, return on investment as well as return on assets and equity. They are to be calculated as

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

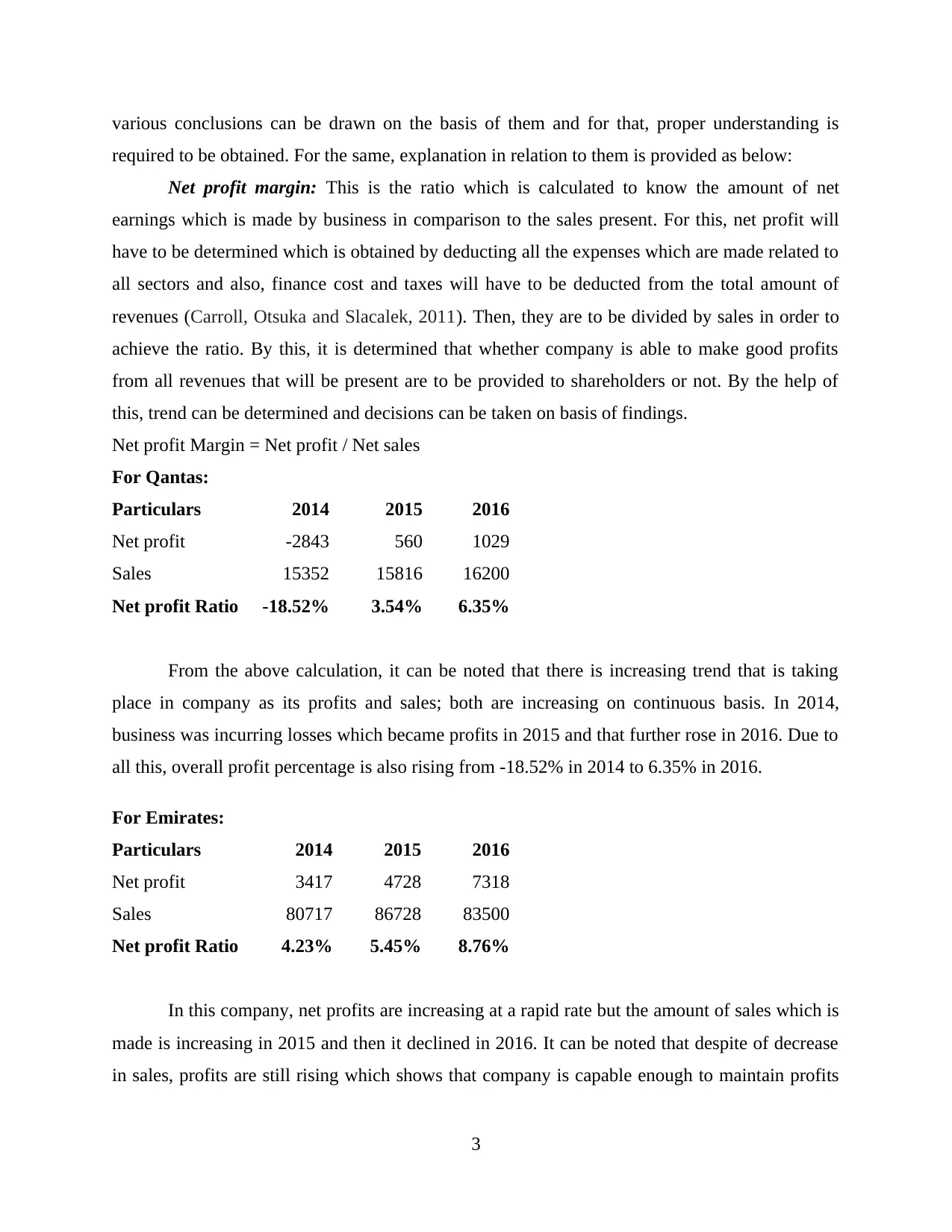

various conclusions can be drawn on the basis of them and for that, proper understanding is

required to be obtained. For the same, explanation in relation to them is provided as below:

Net profit margin: This is the ratio which is calculated to know the amount of net

earnings which is made by business in comparison to the sales present. For this, net profit will

have to be determined which is obtained by deducting all the expenses which are made related to

all sectors and also, finance cost and taxes will have to be deducted from the total amount of

revenues (Carroll, Otsuka and Slacalek, 2011). Then, they are to be divided by sales in order to

achieve the ratio. By this, it is determined that whether company is able to make good profits

from all revenues that will be present are to be provided to shareholders or not. By the help of

this, trend can be determined and decisions can be taken on basis of findings.

Net profit Margin = Net profit / Net sales

For Qantas:

Particulars 2014 2015 2016

Net profit -2843 560 1029

Sales 15352 15816 16200

Net profit Ratio -18.52% 3.54% 6.35%

From the above calculation, it can be noted that there is increasing trend that is taking

place in company as its profits and sales; both are increasing on continuous basis. In 2014,

business was incurring losses which became profits in 2015 and that further rose in 2016. Due to

all this, overall profit percentage is also rising from -18.52% in 2014 to 6.35% in 2016.

For Emirates:

Particulars 2014 2015 2016

Net profit 3417 4728 7318

Sales 80717 86728 83500

Net profit Ratio 4.23% 5.45% 8.76%

In this company, net profits are increasing at a rapid rate but the amount of sales which is

made is increasing in 2015 and then it declined in 2016. It can be noted that despite of decrease

in sales, profits are still rising which shows that company is capable enough to maintain profits

3

required to be obtained. For the same, explanation in relation to them is provided as below:

Net profit margin: This is the ratio which is calculated to know the amount of net

earnings which is made by business in comparison to the sales present. For this, net profit will

have to be determined which is obtained by deducting all the expenses which are made related to

all sectors and also, finance cost and taxes will have to be deducted from the total amount of

revenues (Carroll, Otsuka and Slacalek, 2011). Then, they are to be divided by sales in order to

achieve the ratio. By this, it is determined that whether company is able to make good profits

from all revenues that will be present are to be provided to shareholders or not. By the help of

this, trend can be determined and decisions can be taken on basis of findings.

Net profit Margin = Net profit / Net sales

For Qantas:

Particulars 2014 2015 2016

Net profit -2843 560 1029

Sales 15352 15816 16200

Net profit Ratio -18.52% 3.54% 6.35%

From the above calculation, it can be noted that there is increasing trend that is taking

place in company as its profits and sales; both are increasing on continuous basis. In 2014,

business was incurring losses which became profits in 2015 and that further rose in 2016. Due to

all this, overall profit percentage is also rising from -18.52% in 2014 to 6.35% in 2016.

For Emirates:

Particulars 2014 2015 2016

Net profit 3417 4728 7318

Sales 80717 86728 83500

Net profit Ratio 4.23% 5.45% 8.76%

In this company, net profits are increasing at a rapid rate but the amount of sales which is

made is increasing in 2015 and then it declined in 2016. It can be noted that despite of decrease

in sales, profits are still rising which shows that company is capable enough to maintain profits

3

even in the adverse situations. Profits are earned at the rate of 4.23% in 2014 and that increased

constantly as well as reached till 8.76% in 2016.

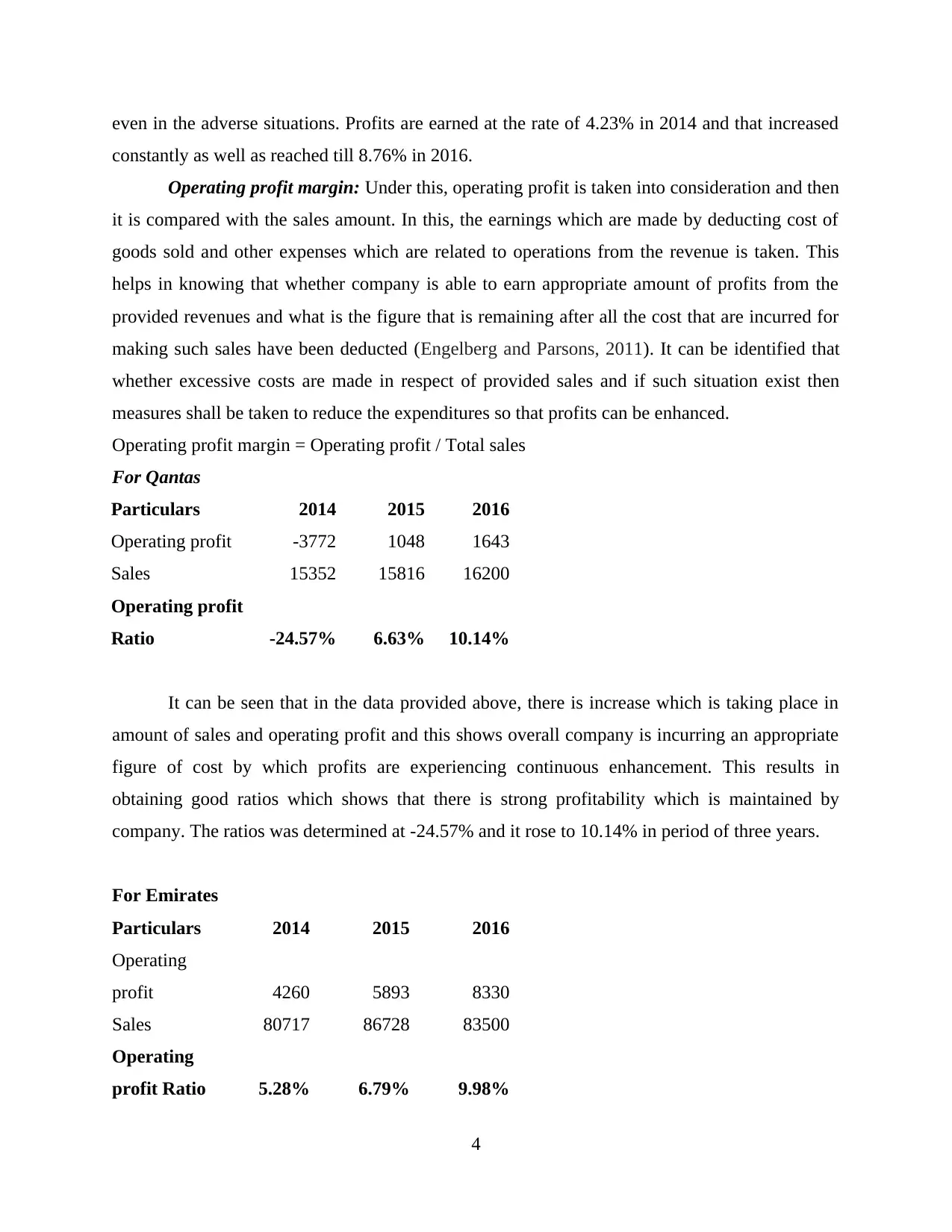

Operating profit margin: Under this, operating profit is taken into consideration and then

it is compared with the sales amount. In this, the earnings which are made by deducting cost of

goods sold and other expenses which are related to operations from the revenue is taken. This

helps in knowing that whether company is able to earn appropriate amount of profits from the

provided revenues and what is the figure that is remaining after all the cost that are incurred for

making such sales have been deducted (Engelberg and Parsons, 2011). It can be identified that

whether excessive costs are made in respect of provided sales and if such situation exist then

measures shall be taken to reduce the expenditures so that profits can be enhanced.

Operating profit margin = Operating profit / Total sales

For Qantas

Particulars 2014 2015 2016

Operating profit -3772 1048 1643

Sales 15352 15816 16200

Operating profit

Ratio -24.57% 6.63% 10.14%

It can be seen that in the data provided above, there is increase which is taking place in

amount of sales and operating profit and this shows overall company is incurring an appropriate

figure of cost by which profits are experiencing continuous enhancement. This results in

obtaining good ratios which shows that there is strong profitability which is maintained by

company. The ratios was determined at -24.57% and it rose to 10.14% in period of three years.

For Emirates

Particulars 2014 2015 2016

Operating

profit 4260 5893 8330

Sales 80717 86728 83500

Operating

profit Ratio 5.28% 6.79% 9.98%

4

constantly as well as reached till 8.76% in 2016.

Operating profit margin: Under this, operating profit is taken into consideration and then

it is compared with the sales amount. In this, the earnings which are made by deducting cost of

goods sold and other expenses which are related to operations from the revenue is taken. This

helps in knowing that whether company is able to earn appropriate amount of profits from the

provided revenues and what is the figure that is remaining after all the cost that are incurred for

making such sales have been deducted (Engelberg and Parsons, 2011). It can be identified that

whether excessive costs are made in respect of provided sales and if such situation exist then

measures shall be taken to reduce the expenditures so that profits can be enhanced.

Operating profit margin = Operating profit / Total sales

For Qantas

Particulars 2014 2015 2016

Operating profit -3772 1048 1643

Sales 15352 15816 16200

Operating profit

Ratio -24.57% 6.63% 10.14%

It can be seen that in the data provided above, there is increase which is taking place in

amount of sales and operating profit and this shows overall company is incurring an appropriate

figure of cost by which profits are experiencing continuous enhancement. This results in

obtaining good ratios which shows that there is strong profitability which is maintained by

company. The ratios was determined at -24.57% and it rose to 10.14% in period of three years.

For Emirates

Particulars 2014 2015 2016

Operating

profit 4260 5893 8330

Sales 80717 86728 83500

Operating

profit Ratio 5.28% 6.79% 9.98%

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

In this also it can be noted that there are changes which can be seen and they show that

operating profit is rising and sales is increasing and then decreasing. Company is efficiency

using its resources as then only profit can be maintained at lower level of revenue also which is

taking place in current situation. Rate of operating profits are 5.28%, 6.79% and 9.98% in 2014,

2015 and 2016.

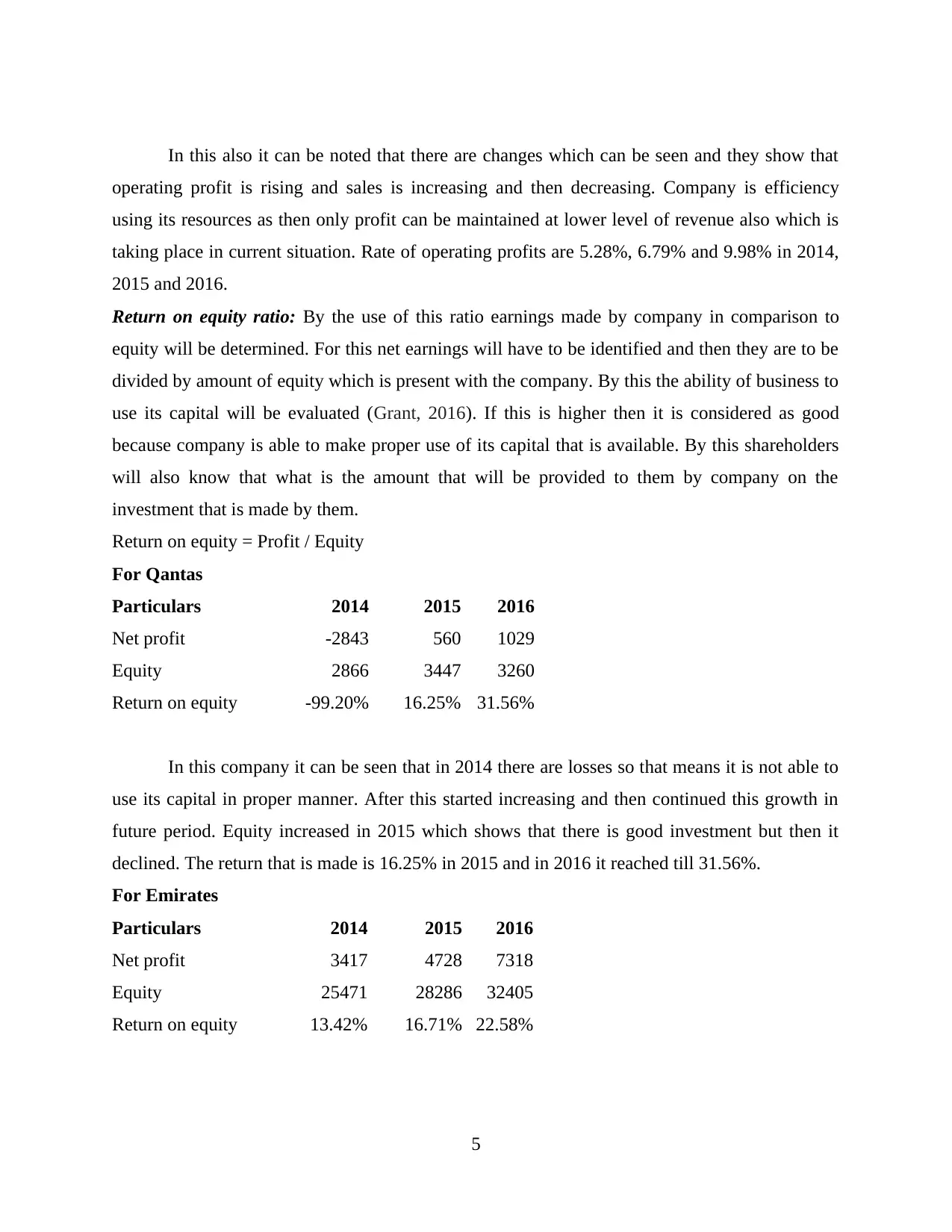

Return on equity ratio: By the use of this ratio earnings made by company in comparison to

equity will be determined. For this net earnings will have to be identified and then they are to be

divided by amount of equity which is present with the company. By this the ability of business to

use its capital will be evaluated (Grant, 2016). If this is higher then it is considered as good

because company is able to make proper use of its capital that is available. By this shareholders

will also know that what is the amount that will be provided to them by company on the

investment that is made by them.

Return on equity = Profit / Equity

For Qantas

Particulars 2014 2015 2016

Net profit -2843 560 1029

Equity 2866 3447 3260

Return on equity -99.20% 16.25% 31.56%

In this company it can be seen that in 2014 there are losses so that means it is not able to

use its capital in proper manner. After this started increasing and then continued this growth in

future period. Equity increased in 2015 which shows that there is good investment but then it

declined. The return that is made is 16.25% in 2015 and in 2016 it reached till 31.56%.

For Emirates

Particulars 2014 2015 2016

Net profit 3417 4728 7318

Equity 25471 28286 32405

Return on equity 13.42% 16.71% 22.58%

5

operating profit is rising and sales is increasing and then decreasing. Company is efficiency

using its resources as then only profit can be maintained at lower level of revenue also which is

taking place in current situation. Rate of operating profits are 5.28%, 6.79% and 9.98% in 2014,

2015 and 2016.

Return on equity ratio: By the use of this ratio earnings made by company in comparison to

equity will be determined. For this net earnings will have to be identified and then they are to be

divided by amount of equity which is present with the company. By this the ability of business to

use its capital will be evaluated (Grant, 2016). If this is higher then it is considered as good

because company is able to make proper use of its capital that is available. By this shareholders

will also know that what is the amount that will be provided to them by company on the

investment that is made by them.

Return on equity = Profit / Equity

For Qantas

Particulars 2014 2015 2016

Net profit -2843 560 1029

Equity 2866 3447 3260

Return on equity -99.20% 16.25% 31.56%

In this company it can be seen that in 2014 there are losses so that means it is not able to

use its capital in proper manner. After this started increasing and then continued this growth in

future period. Equity increased in 2015 which shows that there is good investment but then it

declined. The return that is made is 16.25% in 2015 and in 2016 it reached till 31.56%.

For Emirates

Particulars 2014 2015 2016

Net profit 3417 4728 7318

Equity 25471 28286 32405

Return on equity 13.42% 16.71% 22.58%

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

There is an increase which is noted in both the aspects which are profit and equity and

due to this rate is also rising. There is constant increment which is noted in the rates of earnings

which are derived in terms of equity. They were at 13.42% in 2014 and in 2016 it is found at

22.58%.

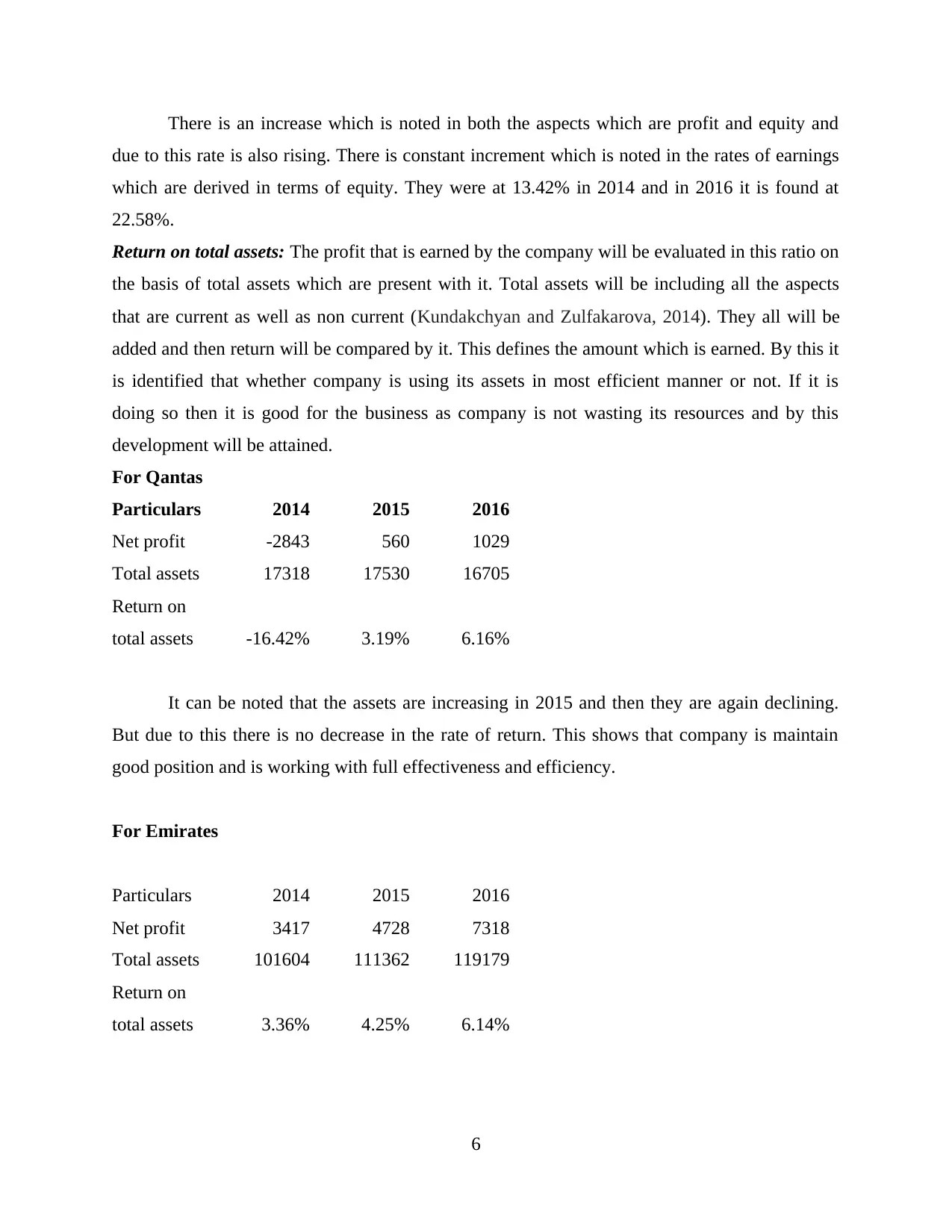

Return on total assets: The profit that is earned by the company will be evaluated in this ratio on

the basis of total assets which are present with it. Total assets will be including all the aspects

that are current as well as non current (Kundakchyan and Zulfakarova, 2014). They all will be

added and then return will be compared by it. This defines the amount which is earned. By this it

is identified that whether company is using its assets in most efficient manner or not. If it is

doing so then it is good for the business as company is not wasting its resources and by this

development will be attained.

For Qantas

Particulars 2014 2015 2016

Net profit -2843 560 1029

Total assets 17318 17530 16705

Return on

total assets -16.42% 3.19% 6.16%

It can be noted that the assets are increasing in 2015 and then they are again declining.

But due to this there is no decrease in the rate of return. This shows that company is maintain

good position and is working with full effectiveness and efficiency.

For Emirates

Particulars 2014 2015 2016

Net profit 3417 4728 7318

Total assets 101604 111362 119179

Return on

total assets 3.36% 4.25% 6.14%

6

due to this rate is also rising. There is constant increment which is noted in the rates of earnings

which are derived in terms of equity. They were at 13.42% in 2014 and in 2016 it is found at

22.58%.

Return on total assets: The profit that is earned by the company will be evaluated in this ratio on

the basis of total assets which are present with it. Total assets will be including all the aspects

that are current as well as non current (Kundakchyan and Zulfakarova, 2014). They all will be

added and then return will be compared by it. This defines the amount which is earned. By this it

is identified that whether company is using its assets in most efficient manner or not. If it is

doing so then it is good for the business as company is not wasting its resources and by this

development will be attained.

For Qantas

Particulars 2014 2015 2016

Net profit -2843 560 1029

Total assets 17318 17530 16705

Return on

total assets -16.42% 3.19% 6.16%

It can be noted that the assets are increasing in 2015 and then they are again declining.

But due to this there is no decrease in the rate of return. This shows that company is maintain

good position and is working with full effectiveness and efficiency.

For Emirates

Particulars 2014 2015 2016

Net profit 3417 4728 7318

Total assets 101604 111362 119179

Return on

total assets 3.36% 4.25% 6.14%

6

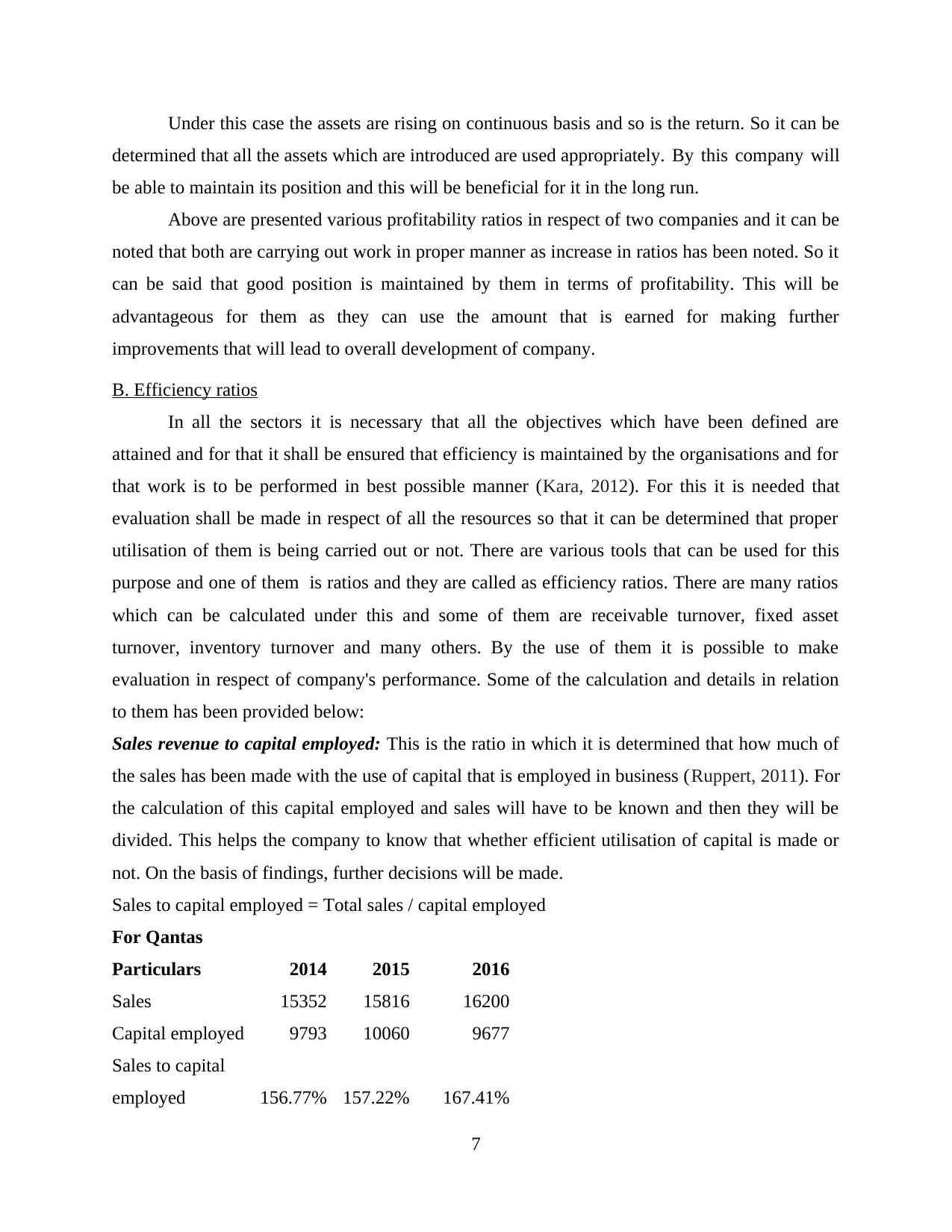

Under this case the assets are rising on continuous basis and so is the return. So it can be

determined that all the assets which are introduced are used appropriately. By this company will

be able to maintain its position and this will be beneficial for it in the long run.

Above are presented various profitability ratios in respect of two companies and it can be

noted that both are carrying out work in proper manner as increase in ratios has been noted. So it

can be said that good position is maintained by them in terms of profitability. This will be

advantageous for them as they can use the amount that is earned for making further

improvements that will lead to overall development of company.

B. Efficiency ratios

In all the sectors it is necessary that all the objectives which have been defined are

attained and for that it shall be ensured that efficiency is maintained by the organisations and for

that work is to be performed in best possible manner (Kara, 2012). For this it is needed that

evaluation shall be made in respect of all the resources so that it can be determined that proper

utilisation of them is being carried out or not. There are various tools that can be used for this

purpose and one of them is ratios and they are called as efficiency ratios. There are many ratios

which can be calculated under this and some of them are receivable turnover, fixed asset

turnover, inventory turnover and many others. By the use of them it is possible to make

evaluation in respect of company's performance. Some of the calculation and details in relation

to them has been provided below:

Sales revenue to capital employed: This is the ratio in which it is determined that how much of

the sales has been made with the use of capital that is employed in business (Ruppert, 2011). For

the calculation of this capital employed and sales will have to be known and then they will be

divided. This helps the company to know that whether efficient utilisation of capital is made or

not. On the basis of findings, further decisions will be made.

Sales to capital employed = Total sales / capital employed

For Qantas

Particulars 2014 2015 2016

Sales 15352 15816 16200

Capital employed 9793 10060 9677

Sales to capital

employed 156.77% 157.22% 167.41%

7

determined that all the assets which are introduced are used appropriately. By this company will

be able to maintain its position and this will be beneficial for it in the long run.

Above are presented various profitability ratios in respect of two companies and it can be

noted that both are carrying out work in proper manner as increase in ratios has been noted. So it

can be said that good position is maintained by them in terms of profitability. This will be

advantageous for them as they can use the amount that is earned for making further

improvements that will lead to overall development of company.

B. Efficiency ratios

In all the sectors it is necessary that all the objectives which have been defined are

attained and for that it shall be ensured that efficiency is maintained by the organisations and for

that work is to be performed in best possible manner (Kara, 2012). For this it is needed that

evaluation shall be made in respect of all the resources so that it can be determined that proper

utilisation of them is being carried out or not. There are various tools that can be used for this

purpose and one of them is ratios and they are called as efficiency ratios. There are many ratios

which can be calculated under this and some of them are receivable turnover, fixed asset

turnover, inventory turnover and many others. By the use of them it is possible to make

evaluation in respect of company's performance. Some of the calculation and details in relation

to them has been provided below:

Sales revenue to capital employed: This is the ratio in which it is determined that how much of

the sales has been made with the use of capital that is employed in business (Ruppert, 2011). For

the calculation of this capital employed and sales will have to be known and then they will be

divided. This helps the company to know that whether efficient utilisation of capital is made or

not. On the basis of findings, further decisions will be made.

Sales to capital employed = Total sales / capital employed

For Qantas

Particulars 2014 2015 2016

Sales 15352 15816 16200

Capital employed 9793 10060 9677

Sales to capital

employed 156.77% 157.22% 167.41%

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

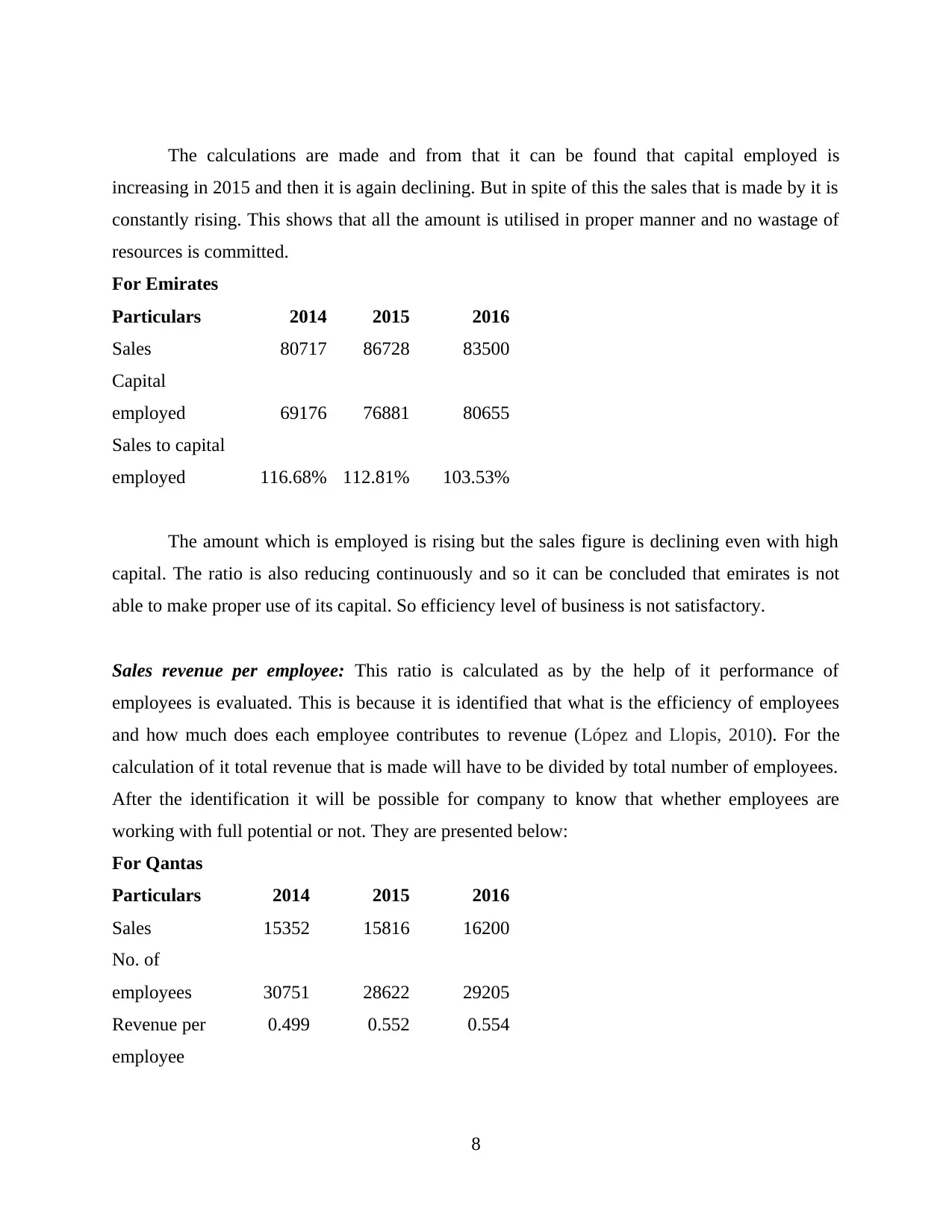

The calculations are made and from that it can be found that capital employed is

increasing in 2015 and then it is again declining. But in spite of this the sales that is made by it is

constantly rising. This shows that all the amount is utilised in proper manner and no wastage of

resources is committed.

For Emirates

Particulars 2014 2015 2016

Sales 80717 86728 83500

Capital

employed 69176 76881 80655

Sales to capital

employed 116.68% 112.81% 103.53%

The amount which is employed is rising but the sales figure is declining even with high

capital. The ratio is also reducing continuously and so it can be concluded that emirates is not

able to make proper use of its capital. So efficiency level of business is not satisfactory.

Sales revenue per employee: This ratio is calculated as by the help of it performance of

employees is evaluated. This is because it is identified that what is the efficiency of employees

and how much does each employee contributes to revenue (López and Llopis, 2010). For the

calculation of it total revenue that is made will have to be divided by total number of employees.

After the identification it will be possible for company to know that whether employees are

working with full potential or not. They are presented below:

For Qantas

Particulars 2014 2015 2016

Sales 15352 15816 16200

No. of

employees 30751 28622 29205

Revenue per

employee

0.499 0.552 0.554

8

increasing in 2015 and then it is again declining. But in spite of this the sales that is made by it is

constantly rising. This shows that all the amount is utilised in proper manner and no wastage of

resources is committed.

For Emirates

Particulars 2014 2015 2016

Sales 80717 86728 83500

Capital

employed 69176 76881 80655

Sales to capital

employed 116.68% 112.81% 103.53%

The amount which is employed is rising but the sales figure is declining even with high

capital. The ratio is also reducing continuously and so it can be concluded that emirates is not

able to make proper use of its capital. So efficiency level of business is not satisfactory.

Sales revenue per employee: This ratio is calculated as by the help of it performance of

employees is evaluated. This is because it is identified that what is the efficiency of employees

and how much does each employee contributes to revenue (López and Llopis, 2010). For the

calculation of it total revenue that is made will have to be divided by total number of employees.

After the identification it will be possible for company to know that whether employees are

working with full potential or not. They are presented below:

For Qantas

Particulars 2014 2015 2016

Sales 15352 15816 16200

No. of

employees 30751 28622 29205

Revenue per

employee

0.499 0.552 0.554

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

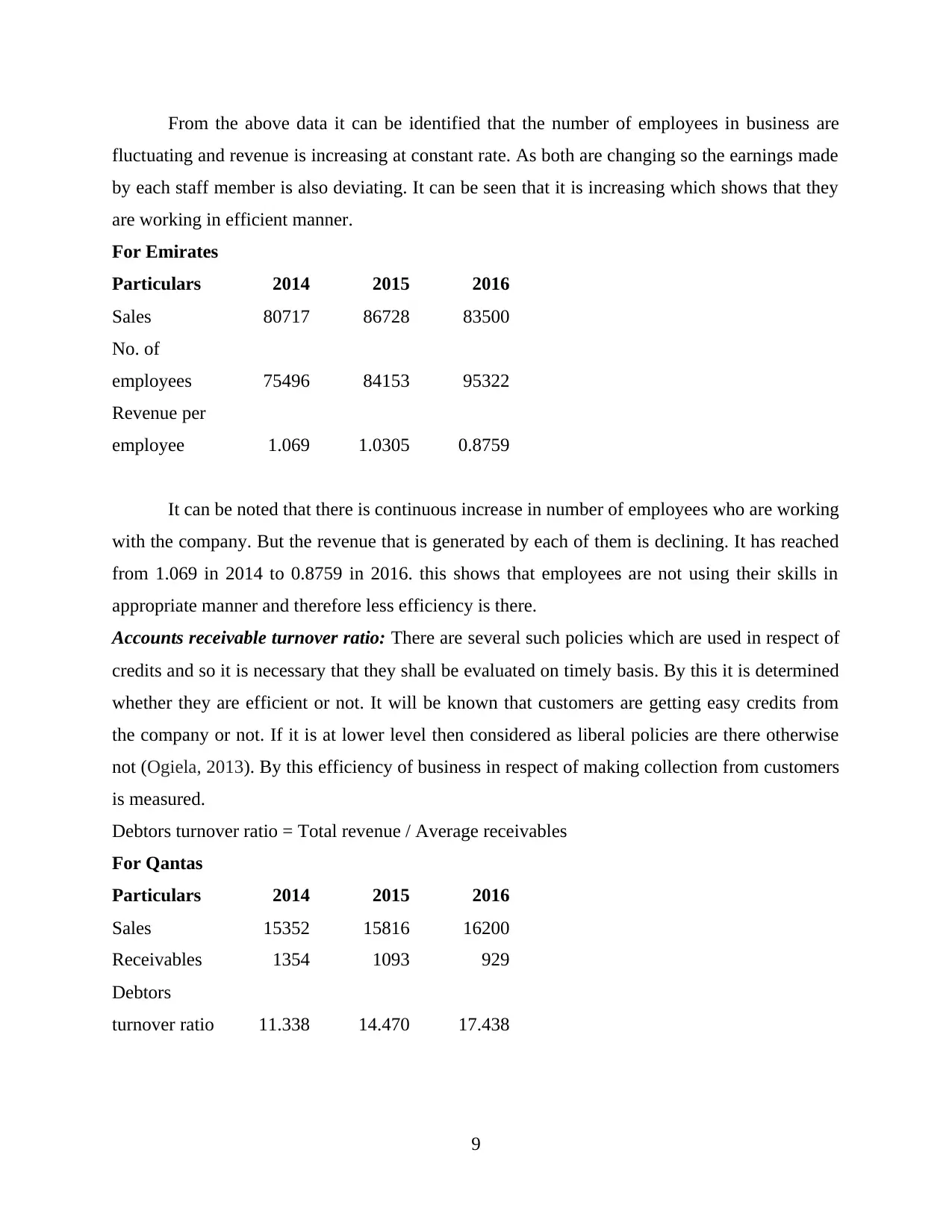

From the above data it can be identified that the number of employees in business are

fluctuating and revenue is increasing at constant rate. As both are changing so the earnings made

by each staff member is also deviating. It can be seen that it is increasing which shows that they

are working in efficient manner.

For Emirates

Particulars 2014 2015 2016

Sales 80717 86728 83500

No. of

employees 75496 84153 95322

Revenue per

employee 1.069 1.0305 0.8759

It can be noted that there is continuous increase in number of employees who are working

with the company. But the revenue that is generated by each of them is declining. It has reached

from 1.069 in 2014 to 0.8759 in 2016. this shows that employees are not using their skills in

appropriate manner and therefore less efficiency is there.

Accounts receivable turnover ratio: There are several such policies which are used in respect of

credits and so it is necessary that they shall be evaluated on timely basis. By this it is determined

whether they are efficient or not. It will be known that customers are getting easy credits from

the company or not. If it is at lower level then considered as liberal policies are there otherwise

not (Ogiela, 2013). By this efficiency of business in respect of making collection from customers

is measured.

Debtors turnover ratio = Total revenue / Average receivables

For Qantas

Particulars 2014 2015 2016

Sales 15352 15816 16200

Receivables 1354 1093 929

Debtors

turnover ratio 11.338 14.470 17.438

9

fluctuating and revenue is increasing at constant rate. As both are changing so the earnings made

by each staff member is also deviating. It can be seen that it is increasing which shows that they

are working in efficient manner.

For Emirates

Particulars 2014 2015 2016

Sales 80717 86728 83500

No. of

employees 75496 84153 95322

Revenue per

employee 1.069 1.0305 0.8759

It can be noted that there is continuous increase in number of employees who are working

with the company. But the revenue that is generated by each of them is declining. It has reached

from 1.069 in 2014 to 0.8759 in 2016. this shows that employees are not using their skills in

appropriate manner and therefore less efficiency is there.

Accounts receivable turnover ratio: There are several such policies which are used in respect of

credits and so it is necessary that they shall be evaluated on timely basis. By this it is determined

whether they are efficient or not. It will be known that customers are getting easy credits from

the company or not. If it is at lower level then considered as liberal policies are there otherwise

not (Ogiela, 2013). By this efficiency of business in respect of making collection from customers

is measured.

Debtors turnover ratio = Total revenue / Average receivables

For Qantas

Particulars 2014 2015 2016

Sales 15352 15816 16200

Receivables 1354 1093 929

Debtors

turnover ratio 11.338 14.470 17.438

9

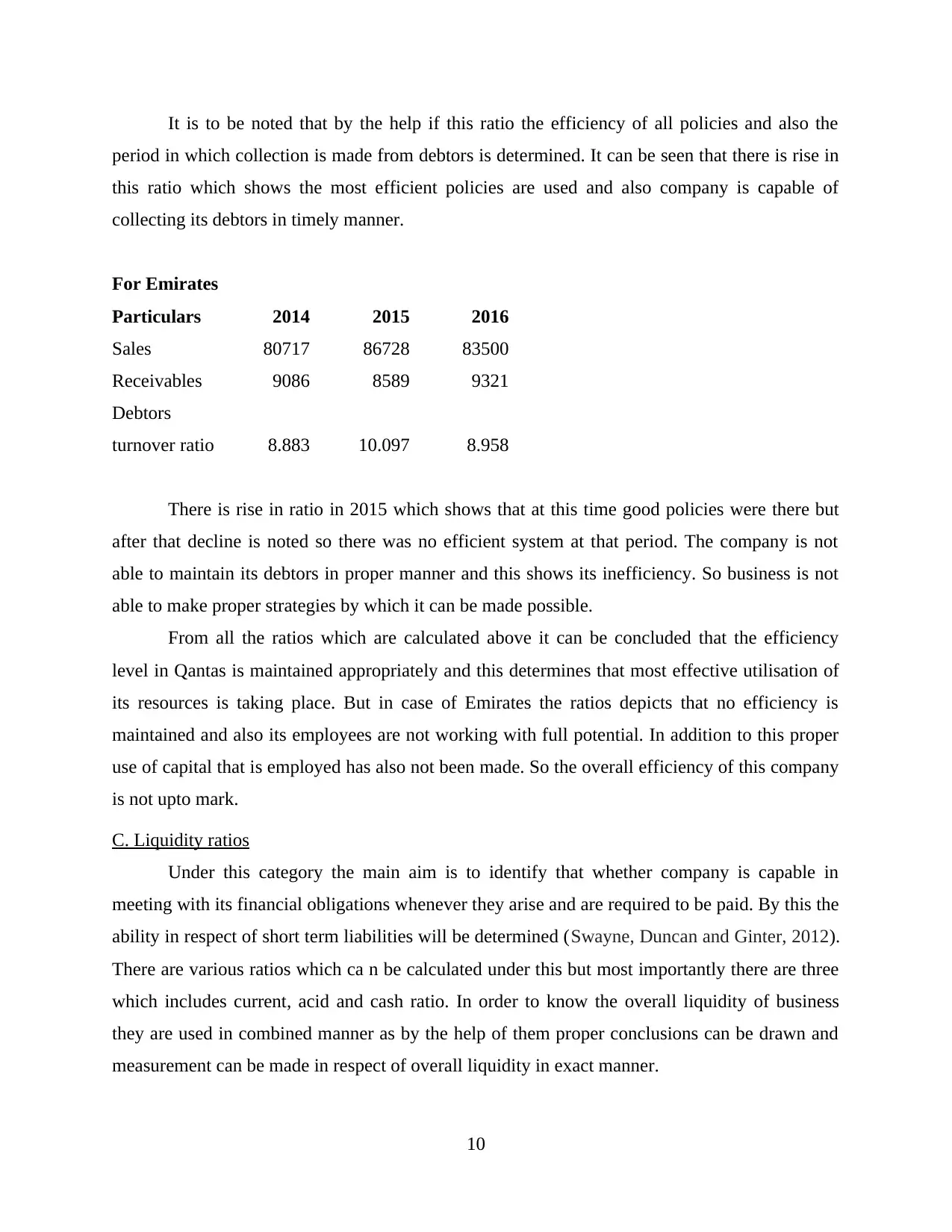

It is to be noted that by the help if this ratio the efficiency of all policies and also the

period in which collection is made from debtors is determined. It can be seen that there is rise in

this ratio which shows the most efficient policies are used and also company is capable of

collecting its debtors in timely manner.

For Emirates

Particulars 2014 2015 2016

Sales 80717 86728 83500

Receivables 9086 8589 9321

Debtors

turnover ratio 8.883 10.097 8.958

There is rise in ratio in 2015 which shows that at this time good policies were there but

after that decline is noted so there was no efficient system at that period. The company is not

able to maintain its debtors in proper manner and this shows its inefficiency. So business is not

able to make proper strategies by which it can be made possible.

From all the ratios which are calculated above it can be concluded that the efficiency

level in Qantas is maintained appropriately and this determines that most effective utilisation of

its resources is taking place. But in case of Emirates the ratios depicts that no efficiency is

maintained and also its employees are not working with full potential. In addition to this proper

use of capital that is employed has also not been made. So the overall efficiency of this company

is not upto mark.

C. Liquidity ratios

Under this category the main aim is to identify that whether company is capable in

meeting with its financial obligations whenever they arise and are required to be paid. By this the

ability in respect of short term liabilities will be determined (Swayne, Duncan and Ginter, 2012).

There are various ratios which ca n be calculated under this but most importantly there are three

which includes current, acid and cash ratio. In order to know the overall liquidity of business

they are used in combined manner as by the help of them proper conclusions can be drawn and

measurement can be made in respect of overall liquidity in exact manner.

10

period in which collection is made from debtors is determined. It can be seen that there is rise in

this ratio which shows the most efficient policies are used and also company is capable of

collecting its debtors in timely manner.

For Emirates

Particulars 2014 2015 2016

Sales 80717 86728 83500

Receivables 9086 8589 9321

Debtors

turnover ratio 8.883 10.097 8.958

There is rise in ratio in 2015 which shows that at this time good policies were there but

after that decline is noted so there was no efficient system at that period. The company is not

able to maintain its debtors in proper manner and this shows its inefficiency. So business is not

able to make proper strategies by which it can be made possible.

From all the ratios which are calculated above it can be concluded that the efficiency

level in Qantas is maintained appropriately and this determines that most effective utilisation of

its resources is taking place. But in case of Emirates the ratios depicts that no efficiency is

maintained and also its employees are not working with full potential. In addition to this proper

use of capital that is employed has also not been made. So the overall efficiency of this company

is not upto mark.

C. Liquidity ratios

Under this category the main aim is to identify that whether company is capable in

meeting with its financial obligations whenever they arise and are required to be paid. By this the

ability in respect of short term liabilities will be determined (Swayne, Duncan and Ginter, 2012).

There are various ratios which ca n be calculated under this but most importantly there are three

which includes current, acid and cash ratio. In order to know the overall liquidity of business

they are used in combined manner as by the help of them proper conclusions can be drawn and

measurement can be made in respect of overall liquidity in exact manner.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 38

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.