Comprehensive Portfolio Analysis: Barclays & Vodafone Investment Risk

VerifiedAdded on 2023/04/22

|16

|3626

|448

Report

AI Summary

This report provides a comprehensive portfolio analysis focusing on Barclays and Vodafone Group, evaluating their investment potential through risk and return assessments. The analysis includes calculations of annual returns, variance, standard deviation, and correlation to determine the optimal ...

Running head:REPORT FOR PORTFOLIO ANALYSIS

Report for Portfolio Analysis

Name of the Student:

Name of the University:

Authors Note:

Report for Portfolio Analysis

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REPORT FOR PORTFOLIO ANALYSIS

1

Table of Contents

Company Background:...............................................................................................................2

Section A: Two asset portfolio...................................................................................................2

Section B: Optimal portfolio......................................................................................................5

Section C: Cost of capital...........................................................................................................8

Conclusion:..............................................................................................................................10

Reference and Bibliography:....................................................................................................12

Appendices:..............................................................................................................................14

1

Table of Contents

Company Background:...............................................................................................................2

Section A: Two asset portfolio...................................................................................................2

Section B: Optimal portfolio......................................................................................................5

Section C: Cost of capital...........................................................................................................8

Conclusion:..............................................................................................................................10

Reference and Bibliography:....................................................................................................12

Appendices:..............................................................................................................................14

REPORT FOR PORTFOLIO ANALYSIS

2

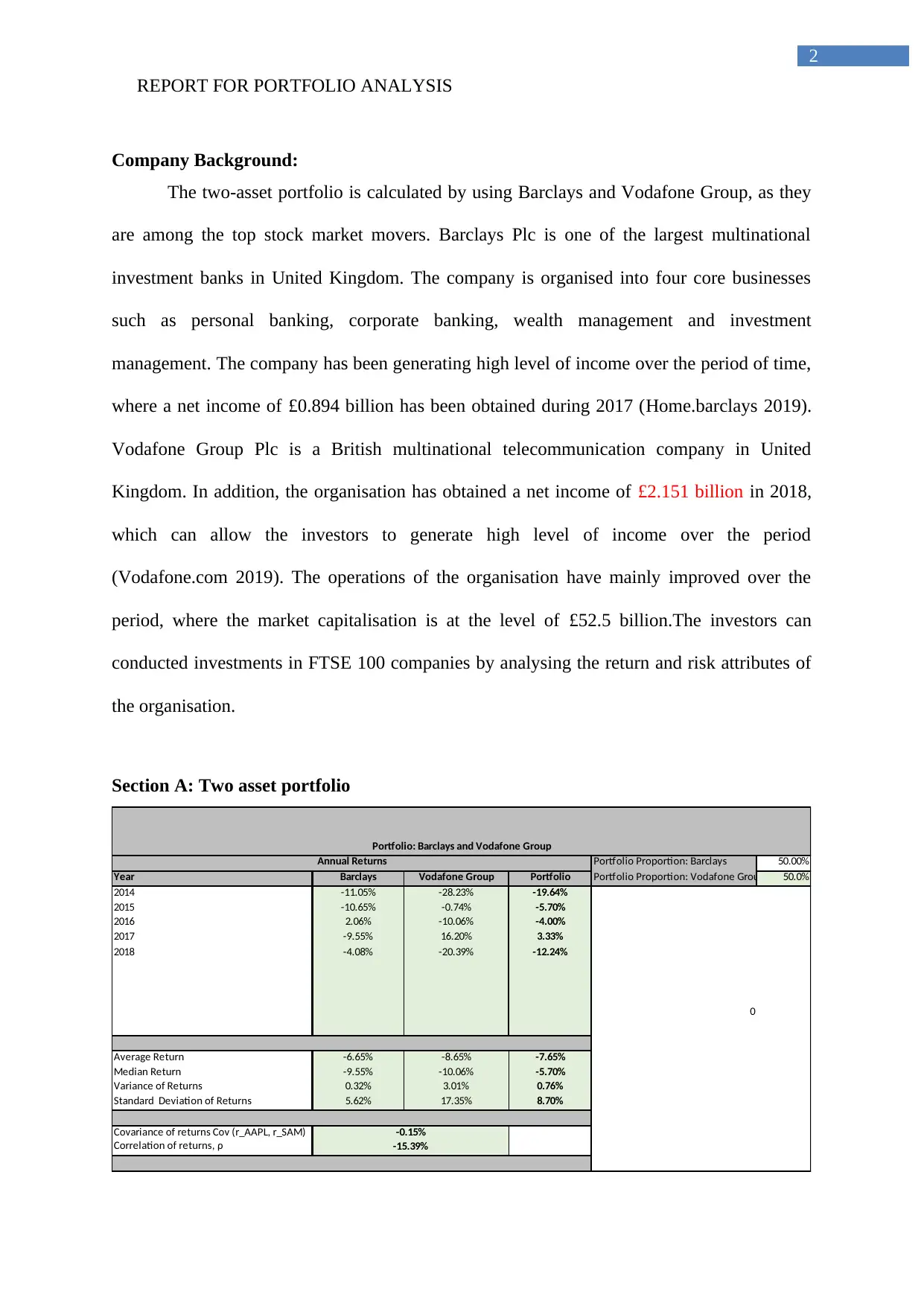

Company Background:

The two-asset portfolio is calculated by using Barclays and Vodafone Group, as they

are among the top stock market movers. Barclays Plc is one of the largest multinational

investment banks in United Kingdom. The company is organised into four core businesses

such as personal banking, corporate banking, wealth management and investment

management. The company has been generating high level of income over the period of time,

where a net income of £0.894 billion has been obtained during 2017 (Home.barclays 2019).

Vodafone Group Plc is a British multinational telecommunication company in United

Kingdom. In addition, the organisation has obtained a net income of £2.151 billion in 2018,

which can allow the investors to generate high level of income over the period

(Vodafone.com 2019). The operations of the organisation have mainly improved over the

period, where the market capitalisation is at the level of £52.5 billion.The investors can

conducted investments in FTSE 100 companies by analysing the return and risk attributes of

the organisation.

Section A: Two asset portfolio

Portfolio Proportion: Barclays 50.00%

Year Barclays Vodafone Group Portfolio Portfolio Proportion: Vodafone Group 50.0%

2014 -11.05% -28.23% -19.64%

2015 -10.65% -0.74% -5.70%

2016 2.06% -10.06% -4.00%

2017 -9.55% 16.20% 3.33%

2018 -4.08% -20.39% -12.24%

0

Average Return -6.65% -8.65% -7.65%

Median Return -9.55% -10.06% -5.70%

Variance of Returns 0.32% 3.01% 0.76%

Standard Deviation of Returns 5.62% 17.35% 8.70%

Covariance of returns Cov (r_AAPL, r_SAM)

Correlation of returns, ρ

Portfolio: Barclays and Vodafone Group

Annual Returns

-0.15%

-15.39%

2

Company Background:

The two-asset portfolio is calculated by using Barclays and Vodafone Group, as they

are among the top stock market movers. Barclays Plc is one of the largest multinational

investment banks in United Kingdom. The company is organised into four core businesses

such as personal banking, corporate banking, wealth management and investment

management. The company has been generating high level of income over the period of time,

where a net income of £0.894 billion has been obtained during 2017 (Home.barclays 2019).

Vodafone Group Plc is a British multinational telecommunication company in United

Kingdom. In addition, the organisation has obtained a net income of £2.151 billion in 2018,

which can allow the investors to generate high level of income over the period

(Vodafone.com 2019). The operations of the organisation have mainly improved over the

period, where the market capitalisation is at the level of £52.5 billion.The investors can

conducted investments in FTSE 100 companies by analysing the return and risk attributes of

the organisation.

Section A: Two asset portfolio

Portfolio Proportion: Barclays 50.00%

Year Barclays Vodafone Group Portfolio Portfolio Proportion: Vodafone Group 50.0%

2014 -11.05% -28.23% -19.64%

2015 -10.65% -0.74% -5.70%

2016 2.06% -10.06% -4.00%

2017 -9.55% 16.20% 3.33%

2018 -4.08% -20.39% -12.24%

0

Average Return -6.65% -8.65% -7.65%

Median Return -9.55% -10.06% -5.70%

Variance of Returns 0.32% 3.01% 0.76%

Standard Deviation of Returns 5.62% 17.35% 8.70%

Covariance of returns Cov (r_AAPL, r_SAM)

Correlation of returns, ρ

Portfolio: Barclays and Vodafone Group

Annual Returns

-0.15%

-15.39%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REPORT FOR PORTFOLIO ANALYSIS

3

The calculation indicates the valuation of two-portfolio asset, which depicts the

income that will be generated from investment. Adequate measure is used by the investors for

detecting the risk and return capabilities of the portfolio. In addition, different calculations

are mainly conducted to identify the level of income, which can be generated from the

portfolio over the investment period. Fagereng, Gottlieb and Guiso (2017) mentioned that

with the help of adequatecalculation investors are able to formulate a portfolio, which has

low risk and high returns from investment.

The data highlighted in the calculation highlights the returns and risk associated with

each organisation. In addition, from the evaluation, it is noticed that the annualized returns of

both Barclays and Vodafone Group has been used from 2014 to 2018 in the calculation. The

values of average returns, median returns, variance returns and standard deviation returns is

used by investors to formulate the two-stock portfolio, which can reduce risk and increase

returns. He, Kelly and Manela (2017) mentioned that with the help of returns calculation, the

volatility and average expected returns of the stock is determined by the investors, which help

them to make appropriateinvestment decisions.

The composition of the portfolio used in the calculation is 50:50, which has allowed

the portfolio to mitigate the risk from investment. The relevant calculation of the portfolio

spots the level of returns, which is generated from the formulated portfolio. Moreover, from

the evaluation it can be noticed that the average return of the portfolio is calculated at the

levels of -7.65%. The variance is at 0.76% and standard deviation of the return is at 8.70%.

The correlation and covariance of the stock returns are also calculated for identifying the

impact it might have on the portfolio return and discover the minimum variance portfolio

(Pagliari 2017).The risk attributes of Barclay is lower than portfolio, which is 5.62%, while

Vodafone Group has high level of risk amounting to 17.35%.

3

The calculation indicates the valuation of two-portfolio asset, which depicts the

income that will be generated from investment. Adequate measure is used by the investors for

detecting the risk and return capabilities of the portfolio. In addition, different calculations

are mainly conducted to identify the level of income, which can be generated from the

portfolio over the investment period. Fagereng, Gottlieb and Guiso (2017) mentioned that

with the help of adequatecalculation investors are able to formulate a portfolio, which has

low risk and high returns from investment.

The data highlighted in the calculation highlights the returns and risk associated with

each organisation. In addition, from the evaluation, it is noticed that the annualized returns of

both Barclays and Vodafone Group has been used from 2014 to 2018 in the calculation. The

values of average returns, median returns, variance returns and standard deviation returns is

used by investors to formulate the two-stock portfolio, which can reduce risk and increase

returns. He, Kelly and Manela (2017) mentioned that with the help of returns calculation, the

volatility and average expected returns of the stock is determined by the investors, which help

them to make appropriateinvestment decisions.

The composition of the portfolio used in the calculation is 50:50, which has allowed

the portfolio to mitigate the risk from investment. The relevant calculation of the portfolio

spots the level of returns, which is generated from the formulated portfolio. Moreover, from

the evaluation it can be noticed that the average return of the portfolio is calculated at the

levels of -7.65%. The variance is at 0.76% and standard deviation of the return is at 8.70%.

The correlation and covariance of the stock returns are also calculated for identifying the

impact it might have on the portfolio return and discover the minimum variance portfolio

(Pagliari 2017).The risk attributes of Barclay is lower than portfolio, which is 5.62%, while

Vodafone Group has high level of risk amounting to 17.35%.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REPORT FOR PORTFOLIO ANALYSIS

4

There is specific portfolio theory that helps in understanding the risk and return

attributes of the stock. The modern portfolio theory evaluates the risk and return attributes of

the stock by using different standard deviation and average returns of the stock. The portfolio

specifies the mathematical model used for perceiving the level of returns and risk generated

from an investment. The portfolio also helps in detecting the expected return, variance and

standard deviation of the stock, which is used for formulating the portfolio. In addition, from

the evaluation it is noticed that with adequate portfolio theory investors are able to sense the

viable investment options, which can understand the investment opportunity in a stock.

Arthur (2018) stated that investors use the CAPM model and portfolio weights to devise

adequate investment optionsthat generate high level of income from investment. The

portfolio diversification reduces the risk factors of investment that maximises the level of

income generated from the portfolio.

4

There is specific portfolio theory that helps in understanding the risk and return

attributes of the stock. The modern portfolio theory evaluates the risk and return attributes of

the stock by using different standard deviation and average returns of the stock. The portfolio

specifies the mathematical model used for perceiving the level of returns and risk generated

from an investment. The portfolio also helps in detecting the expected return, variance and

standard deviation of the stock, which is used for formulating the portfolio. In addition, from

the evaluation it is noticed that with adequate portfolio theory investors are able to sense the

viable investment options, which can understand the investment opportunity in a stock.

Arthur (2018) stated that investors use the CAPM model and portfolio weights to devise

adequate investment optionsthat generate high level of income from investment. The

portfolio diversification reduces the risk factors of investment that maximises the level of

income generated from the portfolio.

REPORT FOR PORTFOLIO ANALYSIS

5

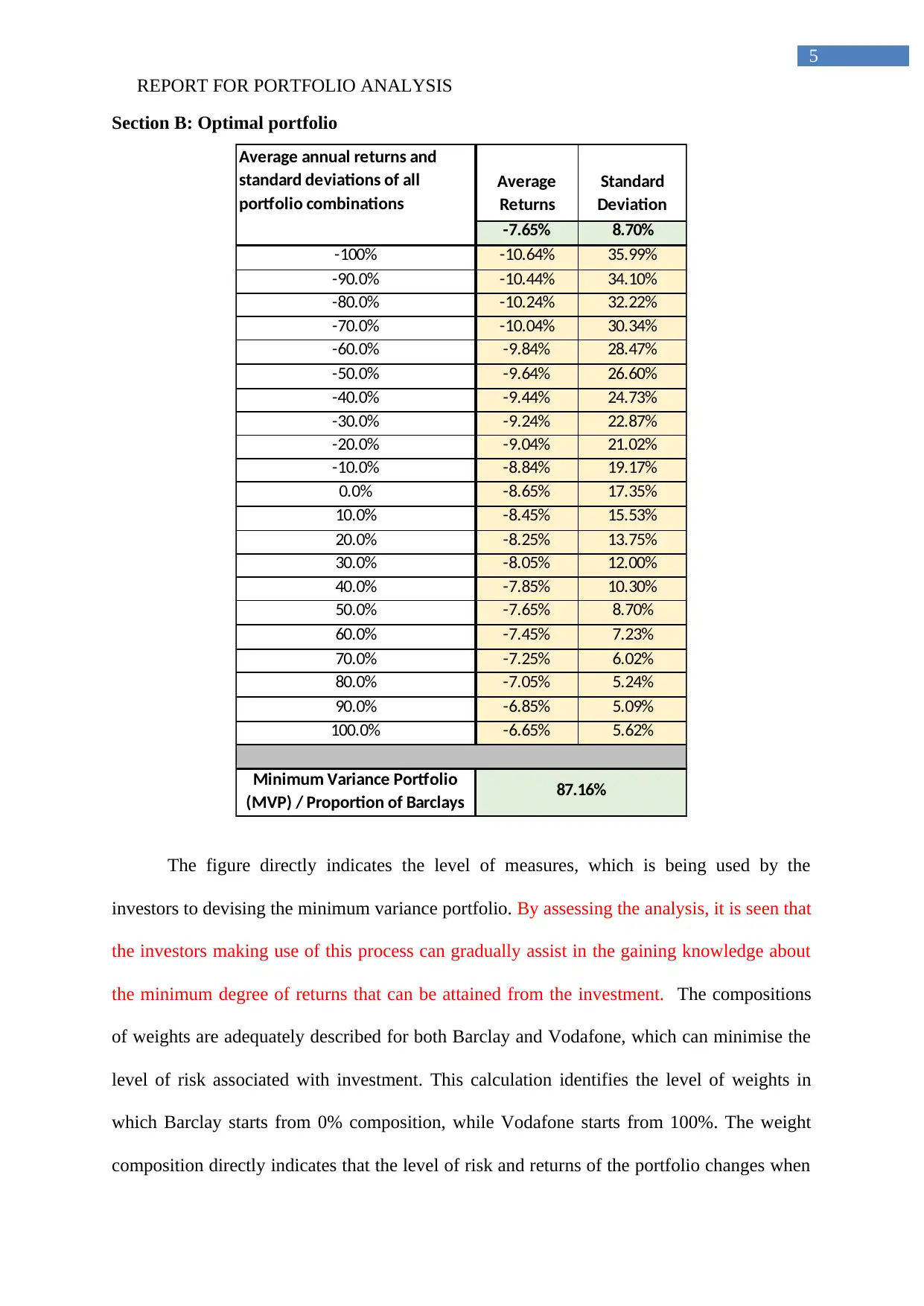

Section B: Optimal portfolio

Average annual returns and

standard deviations of all

portfolio combinations

Average

Returns

Standard

Deviation

-7.65% 8.70%

-100% -10.64% 35.99%

-90.0% -10.44% 34.10%

-80.0% -10.24% 32.22%

-70.0% -10.04% 30.34%

-60.0% -9.84% 28.47%

-50.0% -9.64% 26.60%

-40.0% -9.44% 24.73%

-30.0% -9.24% 22.87%

-20.0% -9.04% 21.02%

-10.0% -8.84% 19.17%

0.0% -8.65% 17.35%

10.0% -8.45% 15.53%

20.0% -8.25% 13.75%

30.0% -8.05% 12.00%

40.0% -7.85% 10.30%

50.0% -7.65% 8.70%

60.0% -7.45% 7.23%

70.0% -7.25% 6.02%

80.0% -7.05% 5.24%

90.0% -6.85% 5.09%

100.0% -6.65% 5.62%

87.16%

Minimum Variance Portfolio

(MVP) / Proportion of Barclays

The figure directly indicates the level of measures, which is being used by the

investors to devising the minimum variance portfolio. By assessing the analysis, it is seen that

the investors making use of this process can gradually assist in the gaining knowledge about

the minimum degree of returns that can be attained from the investment. The compositions

of weights are adequately described for both Barclay and Vodafone, which can minimise the

level of risk associated with investment. This calculation identifies the level of weights in

which Barclay starts from 0% composition, while Vodafone starts from 100%. The weight

composition directly indicates that the level of risk and returns of the portfolio changes when

5

Section B: Optimal portfolio

Average annual returns and

standard deviations of all

portfolio combinations

Average

Returns

Standard

Deviation

-7.65% 8.70%

-100% -10.64% 35.99%

-90.0% -10.44% 34.10%

-80.0% -10.24% 32.22%

-70.0% -10.04% 30.34%

-60.0% -9.84% 28.47%

-50.0% -9.64% 26.60%

-40.0% -9.44% 24.73%

-30.0% -9.24% 22.87%

-20.0% -9.04% 21.02%

-10.0% -8.84% 19.17%

0.0% -8.65% 17.35%

10.0% -8.45% 15.53%

20.0% -8.25% 13.75%

30.0% -8.05% 12.00%

40.0% -7.85% 10.30%

50.0% -7.65% 8.70%

60.0% -7.45% 7.23%

70.0% -7.25% 6.02%

80.0% -7.05% 5.24%

90.0% -6.85% 5.09%

100.0% -6.65% 5.62%

87.16%

Minimum Variance Portfolio

(MVP) / Proportion of Barclays

The figure directly indicates the level of measures, which is being used by the

investors to devising the minimum variance portfolio. By assessing the analysis, it is seen that

the investors making use of this process can gradually assist in the gaining knowledge about

the minimum degree of returns that can be attained from the investment. The compositions

of weights are adequately described for both Barclay and Vodafone, which can minimise the

level of risk associated with investment. This calculation identifies the level of weights in

which Barclay starts from 0% composition, while Vodafone starts from 100%. The weight

composition directly indicates that the level of risk and returns of the portfolio changes when

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REPORT FOR PORTFOLIO ANALYSIS

6

the composition of the portfolio changes. The rising composition of Barclay in the portfolio,

while declining investment of Vodafone has relevantly illustratesthe reduction in overall risk

and improvements in returns. Pettenuzzo and Ravazzolo (2016) mentioned that minimum

variance portfolio only provides details regarding the lowest risk that is generated by the

combination of the stock. Thus, minimum variance portfolio only provides details regarding

the level of risk and does not focus on the returns that be generated from the investment. The

risk trade-off of the portfolios depicted in the figure, whichindicates that reduction in weights

of Vodafone Group, will reduce the risk engulfed in the investment.

Hence, it could be understood that the investments in Barclay needs to be conducted

in higher values for reducing the level of risk and generatingthe level of returns from

investment.Therefore,from the evaluation, it is perceived that investments in the overall

portfolio have allowed the organisation to generate income from operations. Hua et al. (2015)

stated the investorsby calculating the overall minimum variance portfolio are able to spot the

weights, which can reduce risk from the investment. Consequently, investors by analysing the

different level of risk and return from investment are able to make decisions regarding the

investment parameters. Thus, from the calculation, it is discovered that the minimum

variance portfolio comprises of 87.16% Barclay and 12.84% in Vodafone. This is mainly

calculated with the help of correlation and covariance values. The above weights are

depicting the optimal portfolio, which minimises the risk from investment and secures their

investment capital. The non-risk taking investor will use the efficient portfolio to detect and

identify the optimal weights for reducing the risk involved in investment.

6

the composition of the portfolio changes. The rising composition of Barclay in the portfolio,

while declining investment of Vodafone has relevantly illustratesthe reduction in overall risk

and improvements in returns. Pettenuzzo and Ravazzolo (2016) mentioned that minimum

variance portfolio only provides details regarding the lowest risk that is generated by the

combination of the stock. Thus, minimum variance portfolio only provides details regarding

the level of risk and does not focus on the returns that be generated from the investment. The

risk trade-off of the portfolios depicted in the figure, whichindicates that reduction in weights

of Vodafone Group, will reduce the risk engulfed in the investment.

Hence, it could be understood that the investments in Barclay needs to be conducted

in higher values for reducing the level of risk and generatingthe level of returns from

investment.Therefore,from the evaluation, it is perceived that investments in the overall

portfolio have allowed the organisation to generate income from operations. Hua et al. (2015)

stated the investorsby calculating the overall minimum variance portfolio are able to spot the

weights, which can reduce risk from the investment. Consequently, investors by analysing the

different level of risk and return from investment are able to make decisions regarding the

investment parameters. Thus, from the calculation, it is discovered that the minimum

variance portfolio comprises of 87.16% Barclay and 12.84% in Vodafone. This is mainly

calculated with the help of correlation and covariance values. The above weights are

depicting the optimal portfolio, which minimises the risk from investment and secures their

investment capital. The non-risk taking investor will use the efficient portfolio to detect and

identify the optimal weights for reducing the risk involved in investment.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REPORT FOR PORTFOLIO ANALYSIS

7

4.00%

9.00%

14.00%

19.00%

24.00%

29.00%

34.00%

39.00%

-11.00%

-10.00%

-9.00%

-8.00%

-7.00%

-6.00%

-5.00%

-4.00%

-6.85%

Average Annual Returns and Standard Deviations of the

Portfolio Combinations

Standard Deviation of Portfolio

Average Return of Portfolio

The above graph represents the level of average return and standard deviation of the

portfolio under different weight combinations. The graph also represents that risk from

investment which will decline, as the losses are reduced from investment. The calculation

actually helps in perceiving the level of returns that can be generated from the investment

under different risk standards, which can support in the investment decisions. The analysis

shown in the above figure, the optimal portfolio return is calculated at -6.85%,as it

contributes the lowest risk from investment.The minimum variance portfolio theory is

provided by Harry Markowitz, which directly utilises the expected return, and standard

deviation formulate the efficient frontier that ascertains the level of returns and risk projected

by the portfolio.The minimum variance portfolio theory directly allows the investors to

recognize the level of minimum portfolio weights, which can be used for investment

purposes. Dang and Forsyth (2014) indicated that minimum variance portfolio is only used by

conservative investors, as they want to minimise the level of risk involved in investment

without considering the returns. Thus, by looking at the analysis it is revealed that minimum

7

4.00%

9.00%

14.00%

19.00%

24.00%

29.00%

34.00%

39.00%

-11.00%

-10.00%

-9.00%

-8.00%

-7.00%

-6.00%

-5.00%

-4.00%

-6.85%

Average Annual Returns and Standard Deviations of the

Portfolio Combinations

Standard Deviation of Portfolio

Average Return of Portfolio

The above graph represents the level of average return and standard deviation of the

portfolio under different weight combinations. The graph also represents that risk from

investment which will decline, as the losses are reduced from investment. The calculation

actually helps in perceiving the level of returns that can be generated from the investment

under different risk standards, which can support in the investment decisions. The analysis

shown in the above figure, the optimal portfolio return is calculated at -6.85%,as it

contributes the lowest risk from investment.The minimum variance portfolio theory is

provided by Harry Markowitz, which directly utilises the expected return, and standard

deviation formulate the efficient frontier that ascertains the level of returns and risk projected

by the portfolio.The minimum variance portfolio theory directly allows the investors to

recognize the level of minimum portfolio weights, which can be used for investment

purposes. Dang and Forsyth (2014) indicated that minimum variance portfolio is only used by

conservative investors, as they want to minimise the level of risk involved in investment

without considering the returns. Thus, by looking at the analysis it is revealed that minimum

REPORT FOR PORTFOLIO ANALYSIS

8

variance portfolio will permit the investors to lower the extent of risk attained from

investment.

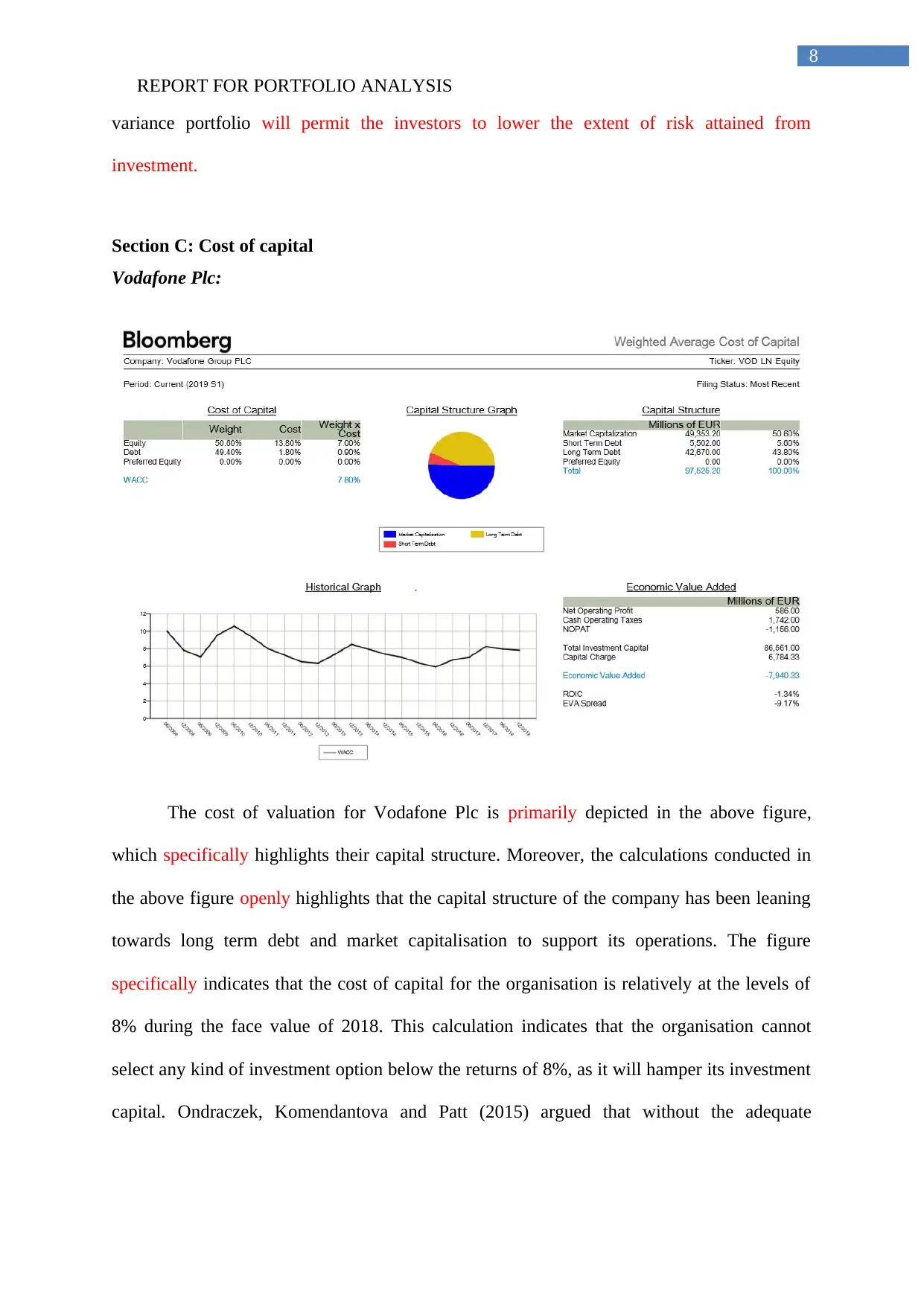

Section C: Cost of capital

Vodafone Plc:

The cost of valuation for Vodafone Plc is primarily depicted in the above figure,

which specifically highlights their capital structure. Moreover, the calculations conducted in

the above figure openly highlights that the capital structure of the company has been leaning

towards long term debt and market capitalisation to support its operations. The figure

specifically indicates that the cost of capital for the organisation is relatively at the levels of

8% during the face value of 2018. This calculation indicates that the organisation cannot

select any kind of investment option below the returns of 8%, as it will hamper its investment

capital. Ondraczek, Komendantova and Patt (2015) argued that without the adequate

8

variance portfolio will permit the investors to lower the extent of risk attained from

investment.

Section C: Cost of capital

Vodafone Plc:

The cost of valuation for Vodafone Plc is primarily depicted in the above figure,

which specifically highlights their capital structure. Moreover, the calculations conducted in

the above figure openly highlights that the capital structure of the company has been leaning

towards long term debt and market capitalisation to support its operations. The figure

specifically indicates that the cost of capital for the organisation is relatively at the levels of

8% during the face value of 2018. This calculation indicates that the organisation cannot

select any kind of investment option below the returns of 8%, as it will hamper its investment

capital. Ondraczek, Komendantova and Patt (2015) argued that without the adequate

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REPORT FOR PORTFOLIO ANALYSIS

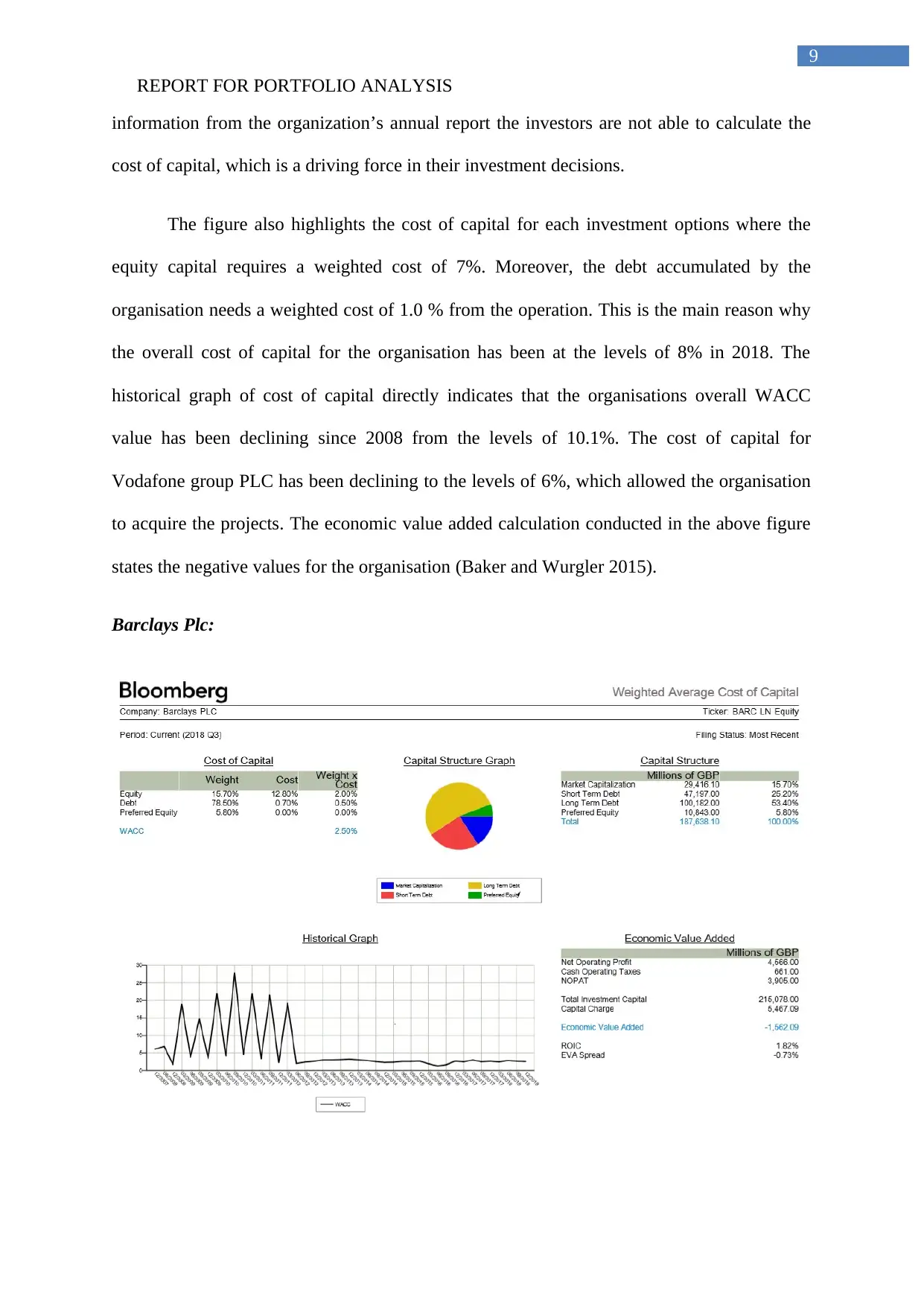

9

information from the organization’s annual report the investors are not able to calculate the

cost of capital, which is a driving force in their investment decisions.

The figure also highlights the cost of capital for each investment options where the

equity capital requires a weighted cost of 7%. Moreover, the debt accumulated by the

organisation needs a weighted cost of 1.0 % from the operation. This is the main reason why

the overall cost of capital for the organisation has been at the levels of 8% in 2018. The

historical graph of cost of capital directly indicates that the organisations overall WACC

value has been declining since 2008 from the levels of 10.1%. The cost of capital for

Vodafone group PLC has been declining to the levels of 6%, which allowed the organisation

to acquire the projects. The economic value added calculation conducted in the above figure

states the negative values for the organisation (Baker and Wurgler 2015).

Barclays Plc:

9

information from the organization’s annual report the investors are not able to calculate the

cost of capital, which is a driving force in their investment decisions.

The figure also highlights the cost of capital for each investment options where the

equity capital requires a weighted cost of 7%. Moreover, the debt accumulated by the

organisation needs a weighted cost of 1.0 % from the operation. This is the main reason why

the overall cost of capital for the organisation has been at the levels of 8% in 2018. The

historical graph of cost of capital directly indicates that the organisations overall WACC

value has been declining since 2008 from the levels of 10.1%. The cost of capital for

Vodafone group PLC has been declining to the levels of 6%, which allowed the organisation

to acquire the projects. The economic value added calculation conducted in the above figure

states the negative values for the organisation (Baker and Wurgler 2015).

Barclays Plc:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REPORT FOR PORTFOLIO ANALYSIS

10

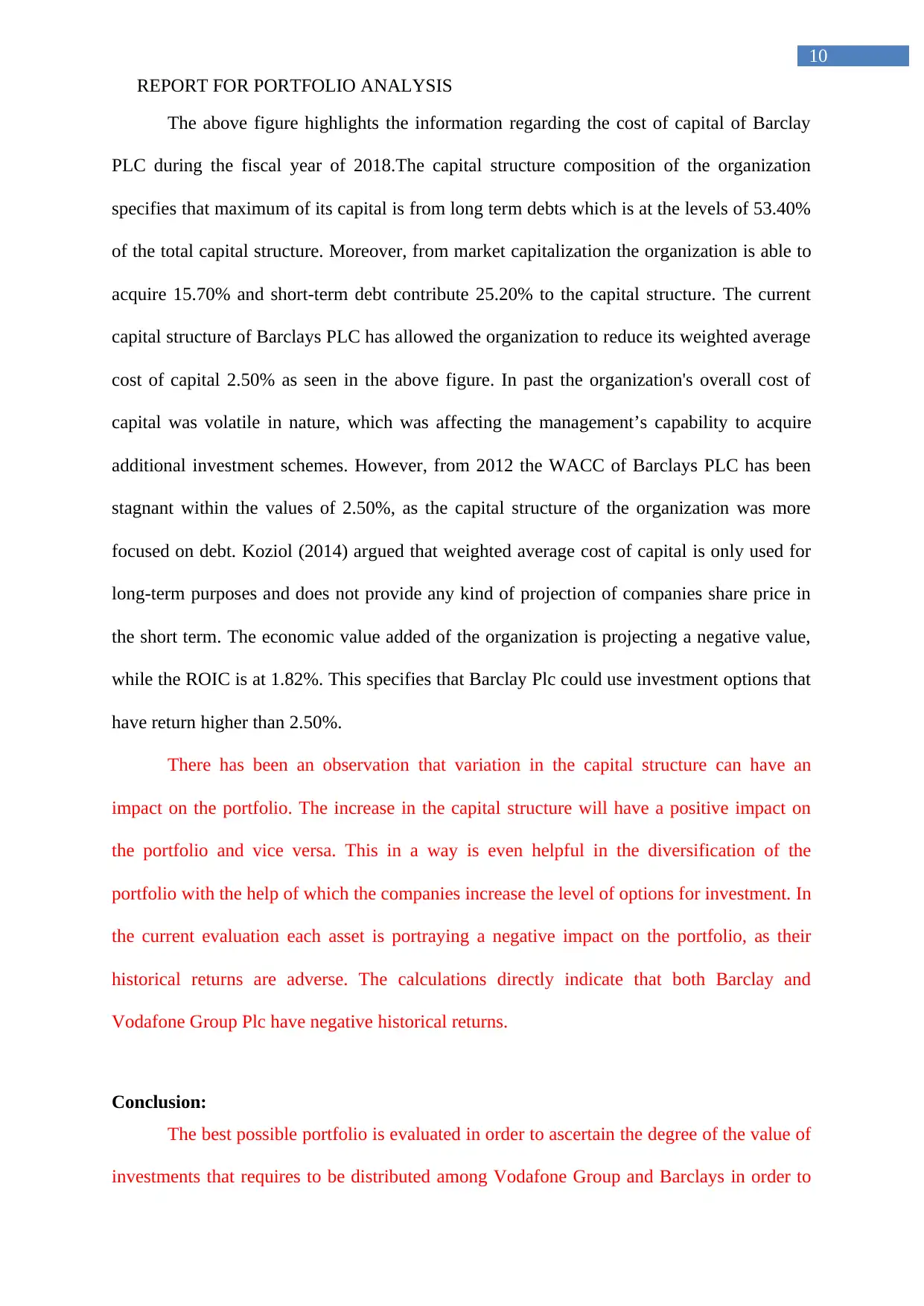

The above figure highlights the information regarding the cost of capital of Barclay

PLC during the fiscal year of 2018.The capital structure composition of the organization

specifies that maximum of its capital is from long term debts which is at the levels of 53.40%

of the total capital structure. Moreover, from market capitalization the organization is able to

acquire 15.70% and short-term debt contribute 25.20% to the capital structure. The current

capital structure of Barclays PLC has allowed the organization to reduce its weighted average

cost of capital 2.50% as seen in the above figure. In past the organization's overall cost of

capital was volatile in nature, which was affecting the management’s capability to acquire

additional investment schemes. However, from 2012 the WACC of Barclays PLC has been

stagnant within the values of 2.50%, as the capital structure of the organization was more

focused on debt. Koziol (2014) argued that weighted average cost of capital is only used for

long-term purposes and does not provide any kind of projection of companies share price in

the short term. The economic value added of the organization is projecting a negative value,

while the ROIC is at 1.82%. This specifies that Barclay Plc could use investment options that

have return higher than 2.50%.

There has been an observation that variation in the capital structure can have an

impact on the portfolio. The increase in the capital structure will have a positive impact on

the portfolio and vice versa. This in a way is even helpful in the diversification of the

portfolio with the help of which the companies increase the level of options for investment. In

the current evaluation each asset is portraying a negative impact on the portfolio, as their

historical returns are adverse. The calculations directly indicate that both Barclay and

Vodafone Group Plc have negative historical returns.

Conclusion:

The best possible portfolio is evaluated in order to ascertain the degree of the value of

investments that requires to be distributed among Vodafone Group and Barclays in order to

10

The above figure highlights the information regarding the cost of capital of Barclay

PLC during the fiscal year of 2018.The capital structure composition of the organization

specifies that maximum of its capital is from long term debts which is at the levels of 53.40%

of the total capital structure. Moreover, from market capitalization the organization is able to

acquire 15.70% and short-term debt contribute 25.20% to the capital structure. The current

capital structure of Barclays PLC has allowed the organization to reduce its weighted average

cost of capital 2.50% as seen in the above figure. In past the organization's overall cost of

capital was volatile in nature, which was affecting the management’s capability to acquire

additional investment schemes. However, from 2012 the WACC of Barclays PLC has been

stagnant within the values of 2.50%, as the capital structure of the organization was more

focused on debt. Koziol (2014) argued that weighted average cost of capital is only used for

long-term purposes and does not provide any kind of projection of companies share price in

the short term. The economic value added of the organization is projecting a negative value,

while the ROIC is at 1.82%. This specifies that Barclay Plc could use investment options that

have return higher than 2.50%.

There has been an observation that variation in the capital structure can have an

impact on the portfolio. The increase in the capital structure will have a positive impact on

the portfolio and vice versa. This in a way is even helpful in the diversification of the

portfolio with the help of which the companies increase the level of options for investment. In

the current evaluation each asset is portraying a negative impact on the portfolio, as their

historical returns are adverse. The calculations directly indicate that both Barclay and

Vodafone Group Plc have negative historical returns.

Conclusion:

The best possible portfolio is evaluated in order to ascertain the degree of the value of

investments that requires to be distributed among Vodafone Group and Barclays in order to

REPORT FOR PORTFOLIO ANALYSIS

11

have the least amount of risk and attain maximum returns from the investment. The

calculations states that optimal portfolio weights for Barclay is at 87.16% and

VodafoneGroup is at 12.84%. The relevant cost of capital calculation is also evaluated by the

investors, as it provides additional information while formulating the portfolio. The current

WACC of Vodafone Group is higher than Barclay Plc and therefore the extent of investment

options are higher as well, as evaluated in the information provided from Bloomberg. Hence,

the minimum variance portfolio can be used by the investor to lessen the risk from volatile

capital market on their investments. Therefore, the investors can invest in both Barclay and

Vodafone Group with the identified portfolio weights for minimizing the risk attributes

involved in the investment. In addition, the methods used for deriving the calculations on

covariance of the returns and correlation of the returns can be used for formulating other

portfolio with low risk and high returns. The investors can use the calculation for improving

their investment strategy and reduce the negative impact on their investment capital. The

analysis that has been undertaken in this report shows that the standard deviation of returns

will stimulate the investor to plan and construct various portfolios that may enhance their

level of returns.

11

have the least amount of risk and attain maximum returns from the investment. The

calculations states that optimal portfolio weights for Barclay is at 87.16% and

VodafoneGroup is at 12.84%. The relevant cost of capital calculation is also evaluated by the

investors, as it provides additional information while formulating the portfolio. The current

WACC of Vodafone Group is higher than Barclay Plc and therefore the extent of investment

options are higher as well, as evaluated in the information provided from Bloomberg. Hence,

the minimum variance portfolio can be used by the investor to lessen the risk from volatile

capital market on their investments. Therefore, the investors can invest in both Barclay and

Vodafone Group with the identified portfolio weights for minimizing the risk attributes

involved in the investment. In addition, the methods used for deriving the calculations on

covariance of the returns and correlation of the returns can be used for formulating other

portfolio with low risk and high returns. The investors can use the calculation for improving

their investment strategy and reduce the negative impact on their investment capital. The

analysis that has been undertaken in this report shows that the standard deviation of returns

will stimulate the investor to plan and construct various portfolios that may enhance their

level of returns.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REPORT FOR PORTFOLIO ANALYSIS

12

Reference and Bibliography:

Arthur, W.B., 2018. Asset pricing under endogenous expectations in an artificial stock

market.In The economy as an evolving complex system II (pp. 31-60).CRC Press.

Baker, M. and Wurgler, J., 2015. Do strict capital requirements raise the cost of capital? Bank

regulation, capital structure, and the low-risk anomaly. American Economic Review, 105(5),

pp.315-20.

Caldera, U., Bogdanov, D. and Breyer, C., 2016. Local cost of seawater RO desalination

based on solar PV and wind energy: A global estimate. Desalination, 385, pp.207-216.

Dang, D.M. and Forsyth, P.A., 2014. Continuous time mean‐variance optimal portfolio

allocation under jump diffusion: An numerical impulse control approach. Numerical Methods

for Partial Differential Equations, 30(2), pp.664-698.

Fagereng, A., Gottlieb, C. and Guiso, L., 2017. Asset market participation and portfolio

choice over the life‐cycle. The Journal of Finance, 72(2), pp.705-750.

Frank, M.Z. and Shen, T., 2016. Investment and the weighted average cost of capital. Journal

of Financial Economics, 119(2), pp.300-315.

He, Z., Kelly, B. and Manela, A., 2017. Intermediary asset pricing: New evidence from many

asset classes. Journal of Financial Economics, 126(1), pp.1-35.

Home.barclays. 2019. Home | Barclays. [online] Available at: https://home.barclays/

[Accessed 15 Jan. 2019].

Hua, S., Liang, J., Zeng, G., Xu, M., Zhang, C., Yuan, Y., Li, X., Li, P., Liu, J. and Huang,

L., 2015. How to manage future groundwater resource of China under climate change and

12

Reference and Bibliography:

Arthur, W.B., 2018. Asset pricing under endogenous expectations in an artificial stock

market.In The economy as an evolving complex system II (pp. 31-60).CRC Press.

Baker, M. and Wurgler, J., 2015. Do strict capital requirements raise the cost of capital? Bank

regulation, capital structure, and the low-risk anomaly. American Economic Review, 105(5),

pp.315-20.

Caldera, U., Bogdanov, D. and Breyer, C., 2016. Local cost of seawater RO desalination

based on solar PV and wind energy: A global estimate. Desalination, 385, pp.207-216.

Dang, D.M. and Forsyth, P.A., 2014. Continuous time mean‐variance optimal portfolio

allocation under jump diffusion: An numerical impulse control approach. Numerical Methods

for Partial Differential Equations, 30(2), pp.664-698.

Fagereng, A., Gottlieb, C. and Guiso, L., 2017. Asset market participation and portfolio

choice over the life‐cycle. The Journal of Finance, 72(2), pp.705-750.

Frank, M.Z. and Shen, T., 2016. Investment and the weighted average cost of capital. Journal

of Financial Economics, 119(2), pp.300-315.

He, Z., Kelly, B. and Manela, A., 2017. Intermediary asset pricing: New evidence from many

asset classes. Journal of Financial Economics, 126(1), pp.1-35.

Home.barclays. 2019. Home | Barclays. [online] Available at: https://home.barclays/

[Accessed 15 Jan. 2019].

Hua, S., Liang, J., Zeng, G., Xu, M., Zhang, C., Yuan, Y., Li, X., Li, P., Liu, J. and Huang,

L., 2015. How to manage future groundwater resource of China under climate change and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REPORT FOR PORTFOLIO ANALYSIS

13

urbanization: An optimal stage investment design from modern portfolio theory. Water

research, 85, pp.31-37.

Johannes, M., Korteweg, A. and Polson, N., 2014. Sequential learning, predictability, and

optimal portfolio returns. The Journal of Finance, 69(2), pp.611-644.

Koziol, C., 2014. A simple correction of the WACC discount rate for default risk and

bankruptcy costs. Review of Quantitative Finance and Accounting, 42(4), pp.653-666.

Krüger, P., Landier, A. and Thesmar, D., 2015. The WACC fallacy: The real effects of using

a unique discount rate. The Journal of Finance, 70(3), pp.1253-1285.

Ondraczek, J., Komendantova, N. and Patt, A., 2015. WACC the dog: The effect of financing

costs on the levelized cost of solar PV power. Renewable Energy, 75, pp.888-898.

Pagliari Jr, J.L., 2017. Another Take on Real Estate's Role in Mixed‐Asset Portfolio

Allocations. Real Estate Economics, 45(1), pp.75-132.

Pettenuzzo, D. and Ravazzolo, F., 2016. Optimal Portfolio Choice Under Decision‐Based

Model Combinations. Journal of applied econometrics, 31(7), pp.1312-1332.

Vodafone.com. 2019. Visit the Vodafone corporate website. [online] Available at:

https://www.vodafone.com/content/index.html [Accessed 15 Jan. 2019].

13

urbanization: An optimal stage investment design from modern portfolio theory. Water

research, 85, pp.31-37.

Johannes, M., Korteweg, A. and Polson, N., 2014. Sequential learning, predictability, and

optimal portfolio returns. The Journal of Finance, 69(2), pp.611-644.

Koziol, C., 2014. A simple correction of the WACC discount rate for default risk and

bankruptcy costs. Review of Quantitative Finance and Accounting, 42(4), pp.653-666.

Krüger, P., Landier, A. and Thesmar, D., 2015. The WACC fallacy: The real effects of using

a unique discount rate. The Journal of Finance, 70(3), pp.1253-1285.

Ondraczek, J., Komendantova, N. and Patt, A., 2015. WACC the dog: The effect of financing

costs on the levelized cost of solar PV power. Renewable Energy, 75, pp.888-898.

Pagliari Jr, J.L., 2017. Another Take on Real Estate's Role in Mixed‐Asset Portfolio

Allocations. Real Estate Economics, 45(1), pp.75-132.

Pettenuzzo, D. and Ravazzolo, F., 2016. Optimal Portfolio Choice Under Decision‐Based

Model Combinations. Journal of applied econometrics, 31(7), pp.1312-1332.

Vodafone.com. 2019. Visit the Vodafone corporate website. [online] Available at:

https://www.vodafone.com/content/index.html [Accessed 15 Jan. 2019].

REPORT FOR PORTFOLIO ANALYSIS

14

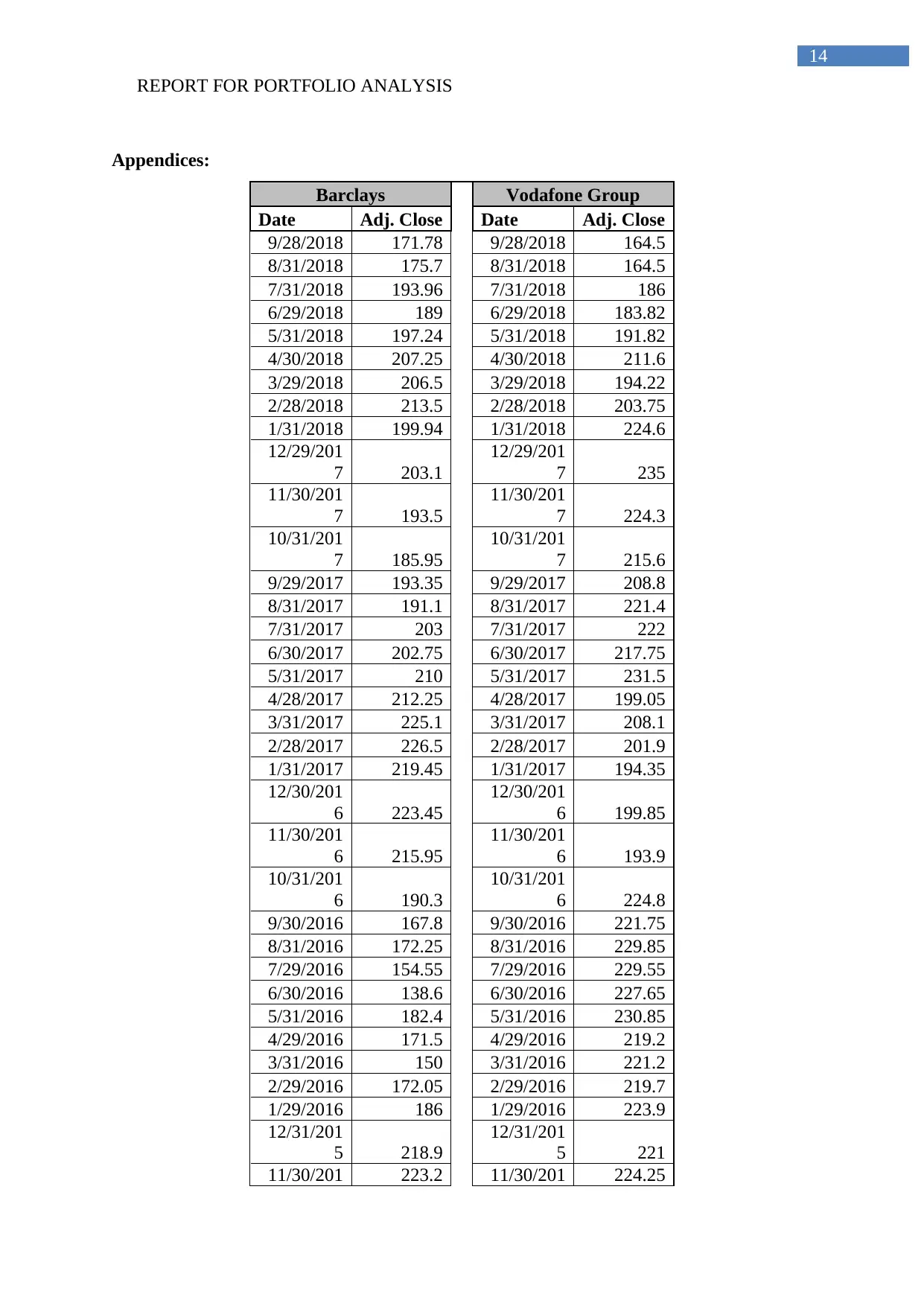

Appendices:

Barclays Vodafone Group

Date Adj. Close Date Adj. Close

9/28/2018 171.78 9/28/2018 164.5

8/31/2018 175.7 8/31/2018 164.5

7/31/2018 193.96 7/31/2018 186

6/29/2018 189 6/29/2018 183.82

5/31/2018 197.24 5/31/2018 191.82

4/30/2018 207.25 4/30/2018 211.6

3/29/2018 206.5 3/29/2018 194.22

2/28/2018 213.5 2/28/2018 203.75

1/31/2018 199.94 1/31/2018 224.6

12/29/201

7 203.1

12/29/201

7 235

11/30/201

7 193.5

11/30/201

7 224.3

10/31/201

7 185.95

10/31/201

7 215.6

9/29/2017 193.35 9/29/2017 208.8

8/31/2017 191.1 8/31/2017 221.4

7/31/2017 203 7/31/2017 222

6/30/2017 202.75 6/30/2017 217.75

5/31/2017 210 5/31/2017 231.5

4/28/2017 212.25 4/28/2017 199.05

3/31/2017 225.1 3/31/2017 208.1

2/28/2017 226.5 2/28/2017 201.9

1/31/2017 219.45 1/31/2017 194.35

12/30/201

6 223.45

12/30/201

6 199.85

11/30/201

6 215.95

11/30/201

6 193.9

10/31/201

6 190.3

10/31/201

6 224.8

9/30/2016 167.8 9/30/2016 221.75

8/31/2016 172.25 8/31/2016 229.85

7/29/2016 154.55 7/29/2016 229.55

6/30/2016 138.6 6/30/2016 227.65

5/31/2016 182.4 5/31/2016 230.85

4/29/2016 171.5 4/29/2016 219.2

3/31/2016 150 3/31/2016 221.2

2/29/2016 172.05 2/29/2016 219.7

1/29/2016 186 1/29/2016 223.9

12/31/201

5 218.9

12/31/201

5 221

11/30/201 223.2 11/30/201 224.25

14

Appendices:

Barclays Vodafone Group

Date Adj. Close Date Adj. Close

9/28/2018 171.78 9/28/2018 164.5

8/31/2018 175.7 8/31/2018 164.5

7/31/2018 193.96 7/31/2018 186

6/29/2018 189 6/29/2018 183.82

5/31/2018 197.24 5/31/2018 191.82

4/30/2018 207.25 4/30/2018 211.6

3/29/2018 206.5 3/29/2018 194.22

2/28/2018 213.5 2/28/2018 203.75

1/31/2018 199.94 1/31/2018 224.6

12/29/201

7 203.1

12/29/201

7 235

11/30/201

7 193.5

11/30/201

7 224.3

10/31/201

7 185.95

10/31/201

7 215.6

9/29/2017 193.35 9/29/2017 208.8

8/31/2017 191.1 8/31/2017 221.4

7/31/2017 203 7/31/2017 222

6/30/2017 202.75 6/30/2017 217.75

5/31/2017 210 5/31/2017 231.5

4/28/2017 212.25 4/28/2017 199.05

3/31/2017 225.1 3/31/2017 208.1

2/28/2017 226.5 2/28/2017 201.9

1/31/2017 219.45 1/31/2017 194.35

12/30/201

6 223.45

12/30/201

6 199.85

11/30/201

6 215.95

11/30/201

6 193.9

10/31/201

6 190.3

10/31/201

6 224.8

9/30/2016 167.8 9/30/2016 221.75

8/31/2016 172.25 8/31/2016 229.85

7/29/2016 154.55 7/29/2016 229.55

6/30/2016 138.6 6/30/2016 227.65

5/31/2016 182.4 5/31/2016 230.85

4/29/2016 171.5 4/29/2016 219.2

3/31/2016 150 3/31/2016 221.2

2/29/2016 172.05 2/29/2016 219.7

1/29/2016 186 1/29/2016 223.9

12/31/201

5 218.9

12/31/201

5 221

11/30/201 223.2 11/30/201 224.25

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REPORT FOR PORTFOLIO ANALYSIS

15

5 5

10/30/201

5 232

10/30/201

5 214.25

9/30/2015 244.15 9/30/2015 208.45

8/28/2015 261.45 8/28/2015 226.7

7/31/2015 288.95 7/31/2015 241.85

6/30/2015 260.5 6/30/2015 229.85

5/29/2015 270 5/29/2015 255.35

4/30/2015 255.3 4/30/2015 230.55

3/31/2015 242.6 3/31/2015 220.45

2/27/2015 256.9 2/27/2015 224.4

1/30/2015 234.15 1/30/2015 234.5

12/31/201

4 243.5

12/31/201

4 222.65

11/28/201

4 245.15

11/28/201

4 233.95

10/31/201

4 240.8

10/31/201

4 207.3

9/30/2014 227.45 9/30/2014 204.4

8/29/2014 224.45 8/29/2014 206.75

7/31/2014 225.7 7/31/2014 198.1

6/30/2014 212.8 6/30/2014 195

5/30/2014 247 5/30/2014 209.5

4/30/2014 252.2 4/30/2014 223.95

3/31/2014 233.4 3/31/2014 220.3

2/28/2014 252.1 2/28/2014 249

1/31/2014 272.5 1/31/2014 282.259

12/31/201

3 271.95

12/31/201

3 295.279

15

5 5

10/30/201

5 232

10/30/201

5 214.25

9/30/2015 244.15 9/30/2015 208.45

8/28/2015 261.45 8/28/2015 226.7

7/31/2015 288.95 7/31/2015 241.85

6/30/2015 260.5 6/30/2015 229.85

5/29/2015 270 5/29/2015 255.35

4/30/2015 255.3 4/30/2015 230.55

3/31/2015 242.6 3/31/2015 220.45

2/27/2015 256.9 2/27/2015 224.4

1/30/2015 234.15 1/30/2015 234.5

12/31/201

4 243.5

12/31/201

4 222.65

11/28/201

4 245.15

11/28/201

4 233.95

10/31/201

4 240.8

10/31/201

4 207.3

9/30/2014 227.45 9/30/2014 204.4

8/29/2014 224.45 8/29/2014 206.75

7/31/2014 225.7 7/31/2014 198.1

6/30/2014 212.8 6/30/2014 195

5/30/2014 247 5/30/2014 209.5

4/30/2014 252.2 4/30/2014 223.95

3/31/2014 233.4 3/31/2014 220.3

2/28/2014 252.1 2/28/2014 249

1/31/2014 272.5 1/31/2014 282.259

12/31/201

3 271.95

12/31/201

3 295.279

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.