International Property Finance Report 2022

VerifiedAdded on 2022/10/14

|13

|2797

|20

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: INTERNATIONAL PROPERTY FINANCE

International Property Finance

Name of Student:

Name of the University:

Authors’ note

International Property Finance

Name of Student:

Name of the University:

Authors’ note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1INTERNATIONAL PROPERTY FINANCE

EXECUTIVE SUMMARY:

This report is providing the brief idea about the real estate investment trust or REIT. Here, in

this report for evaluating the overall performance of a REIT, selecting the Scentre Group. In

the first part of this report providing a basic overview of Scentre Group. The details about the

group’s performance, profit evaluation method, amount of profitability etc. Next to such a

basic overview, this report is providing a brief idea about the using of AASB. After such

individual AASB details, this report is offered the general accounting policies. Next to such

accounting policies, this report is providing the relevant idea about group’s investment

policies, Derivative financial instruments, taxation policies, generally followed depreciation

method etc. As a final presentation, this report is providing the complete details of the

group’s capital structure.

EXECUTIVE SUMMARY:

This report is providing the brief idea about the real estate investment trust or REIT. Here, in

this report for evaluating the overall performance of a REIT, selecting the Scentre Group. In

the first part of this report providing a basic overview of Scentre Group. The details about the

group’s performance, profit evaluation method, amount of profitability etc. Next to such a

basic overview, this report is providing a brief idea about the using of AASB. After such

individual AASB details, this report is offered the general accounting policies. Next to such

accounting policies, this report is providing the relevant idea about group’s investment

policies, Derivative financial instruments, taxation policies, generally followed depreciation

method etc. As a final presentation, this report is providing the complete details of the

group’s capital structure.

2INTERNATIONAL PROPERTY FINANCE

Table of Contents

Introduction................................................................................................................................3

Discussions.................................................................................................................................4

Followed AASB:....................................................................................................................5

Accounting policies:...............................................................................................................5

Investments:...........................................................................................................................6

Taxation:................................................................................................................................6

Depreciation:..........................................................................................................................7

Capital Structure:...................................................................................................................7

Conclusion:................................................................................................................................9

References:...............................................................................................................................11

Table of Contents

Introduction................................................................................................................................3

Discussions.................................................................................................................................4

Followed AASB:....................................................................................................................5

Accounting policies:...............................................................................................................5

Investments:...........................................................................................................................6

Taxation:................................................................................................................................6

Depreciation:..........................................................................................................................7

Capital Structure:...................................................................................................................7

Conclusion:................................................................................................................................9

References:...............................................................................................................................11

3INTERNATIONAL PROPERTY FINANCE

Introduction

In general, the term real estate investment trust or REIT is implying to a closed to end

investment organization. Such REIT usually owns assets related to real estate, and those are

like the buildings, real estate securities, buildings etc. Such organization is generally earned

its revenues from the collection of investor’s amount and through providing them the access

of such real estate assets. Publically such real estate is built their cash for their portfolios

through selling shares on an exchange. Generally, the REIT’s are required to distribute

according to the legal point of views at least 90% of their taxable income to the investors.

Such revenues are generated through the rent, fees for proper managing or leasing of usable

properties (Andreasen, Schindler and Valenzuela 2017).

A real estate investment trust is normally required to funding their capital just like any

other corporation. Normally the way a publically traded REIT does is called initial public

offering. Such investment is generally followed the same way just like selling any other

stocks to the public. Such publics have implied those peoples who are usually making their

investment in the corporations’ income. Generally, the way a real estate investment trust’s

profits are generally evaluated is called fund from operation or FFO (Bradley, Pantzalis and

Yuan 2016). As per the statement made by National Association of real estate investment

trusts or NAREIT, the fund from operation is normally stated as the calculation of net income

through the rent or sales of real estate properties after the deduction of the cost of

administration or financing. Such estimation is normally based on the concept that is

provided by the GAAP. In this assignment using one of the Real estate investment

companies, which is Scentre group.

Introduction

In general, the term real estate investment trust or REIT is implying to a closed to end

investment organization. Such REIT usually owns assets related to real estate, and those are

like the buildings, real estate securities, buildings etc. Such organization is generally earned

its revenues from the collection of investor’s amount and through providing them the access

of such real estate assets. Publically such real estate is built their cash for their portfolios

through selling shares on an exchange. Generally, the REIT’s are required to distribute

according to the legal point of views at least 90% of their taxable income to the investors.

Such revenues are generated through the rent, fees for proper managing or leasing of usable

properties (Andreasen, Schindler and Valenzuela 2017).

A real estate investment trust is normally required to funding their capital just like any

other corporation. Normally the way a publically traded REIT does is called initial public

offering. Such investment is generally followed the same way just like selling any other

stocks to the public. Such publics have implied those peoples who are usually making their

investment in the corporations’ income. Generally, the way a real estate investment trust’s

profits are generally evaluated is called fund from operation or FFO (Bradley, Pantzalis and

Yuan 2016). As per the statement made by National Association of real estate investment

trusts or NAREIT, the fund from operation is normally stated as the calculation of net income

through the rent or sales of real estate properties after the deduction of the cost of

administration or financing. Such estimation is normally based on the concept that is

provided by the GAAP. In this assignment using one of the Real estate investment

companies, which is Scentre group.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4INTERNATIONAL PROPERTY FINANCE

Discussions

Scentre Group is one of the real estate investment trusts, which is mainly owned and

conducts the pre-eminent shopping centre in Australia. Such group is having with real estate

assets under the management that was valued to $47.4 billion. This organization has 41

Westfield shopping centres, and it is considered as 15th largest entity as per the market

capitalization on the ASX list. Such group is having a reasonable strategy to achieve interests

as the highest quality regional shopping centre in the global markets and also to provide

investments in these assets through the procedure of redevelopment opportunities. Scentre

Group was normally created in the year 2014 using the process of demerger with the

Westfield group. Many individual shopping centres are generally owned in partnership with

other leading retails investment institutions (Brusovet al. 2018)

Westfield shopping centres is considered as one of the essential parts of the

community, and in the year 2016 more than 520 customers were visited in such centres.

Scentre group generally works with the world’s leading and luxury brands in the case to

create an unidentifiable leisure and shopping experience. This group is engaged in manage

every aspect of its portfolio, which is starting from the design, construction and development

to the leasing of an asset, management and marketing (El Ghoul et al. 2018). It is generally

used in the case to ensure the individual customer’s experiences and retailer’s feedback

regarding the opportunities provided by such group or organization. Scentre Group was

normally created in the year 2014 using the process of demerger with the Westfield group.

As per the annual report 2018 of Scentre Group, this group was strong with Funds

From Operations (FFO) of $1.30 billion that generally representing the 25.66 per cent per

security. Such a group has total assets of $39.1 billion and up to $54.00 billion of assets under

the control of management. Such a group was completed more than $1.10 billion of

Discussions

Scentre Group is one of the real estate investment trusts, which is mainly owned and

conducts the pre-eminent shopping centre in Australia. Such group is having with real estate

assets under the management that was valued to $47.4 billion. This organization has 41

Westfield shopping centres, and it is considered as 15th largest entity as per the market

capitalization on the ASX list. Such group is having a reasonable strategy to achieve interests

as the highest quality regional shopping centre in the global markets and also to provide

investments in these assets through the procedure of redevelopment opportunities. Scentre

Group was normally created in the year 2014 using the process of demerger with the

Westfield group. Many individual shopping centres are generally owned in partnership with

other leading retails investment institutions (Brusovet al. 2018)

Westfield shopping centres is considered as one of the essential parts of the

community, and in the year 2016 more than 520 customers were visited in such centres.

Scentre group generally works with the world’s leading and luxury brands in the case to

create an unidentifiable leisure and shopping experience. This group is engaged in manage

every aspect of its portfolio, which is starting from the design, construction and development

to the leasing of an asset, management and marketing (El Ghoul et al. 2018). It is generally

used in the case to ensure the individual customer’s experiences and retailer’s feedback

regarding the opportunities provided by such group or organization. Scentre Group was

normally created in the year 2014 using the process of demerger with the Westfield group.

As per the annual report 2018 of Scentre Group, this group was strong with Funds

From Operations (FFO) of $1.30 billion that generally representing the 25.66 per cent per

security. Such a group has total assets of $39.1 billion and up to $54.00 billion of assets under

the control of management. Such a group was completed more than $1.10 billion of

5INTERNATIONAL PROPERTY FINANCE

developments, and such developments have used to enhance the customer experience and

also to contribute to high levels of customer advocacy (Annual report 2018).

In case of analysing the financial results of such group, in the year 2018 the

organization having fund from operation with an amount of $1,339.5 million, which is

representing almost 3.8% growth of overall financial conditions. Followed the same manner

the group achieved 25.24 % FFO per security, which is nearly 3.9% growth of the financial

condition. During the year 2018, the group was achieved almost $2,295.9 million of profit

after the deduction of tax liability (Annual report 2018).In case to analyse the overall

financial report of the company using Scentre Group’s annual report for the year ended 2018.

Such report is provided the using of different accounting standards and principles in case to

evaluate and presentation of overall organizations’ financial performance.

Followed AASB:

This group is mainly engaged in property development, construction, through which it

is primarily earned reasonable revenues. For such revenue recognition purpose, the

organization is used the AASB 15 revenues from customer’s contracts. Next to this AASB,

such group has followed the provisions of AASB 9 in the case to a classification,

measurement, hedge and impairment accounting of financial elements for accounting

recognition and analysis (Graham, Leary and Roberts 2015). This group has also followed the

provisions of AASB 16 in the case to leases of accounting properties.

Accounting policies:

For the purpose of accounting policies such group is mainly provided the concepts

relating to revenue recognition, in such concept the revenue is considered up to the extent that

it is able to provide some economic benefits to such group. In case of Lease, normally the

rental incomes from those investment properties are evaluated through the straight line basis

developments, and such developments have used to enhance the customer experience and

also to contribute to high levels of customer advocacy (Annual report 2018).

In case of analysing the financial results of such group, in the year 2018 the

organization having fund from operation with an amount of $1,339.5 million, which is

representing almost 3.8% growth of overall financial conditions. Followed the same manner

the group achieved 25.24 % FFO per security, which is nearly 3.9% growth of the financial

condition. During the year 2018, the group was achieved almost $2,295.9 million of profit

after the deduction of tax liability (Annual report 2018).In case to analyse the overall

financial report of the company using Scentre Group’s annual report for the year ended 2018.

Such report is provided the using of different accounting standards and principles in case to

evaluate and presentation of overall organizations’ financial performance.

Followed AASB:

This group is mainly engaged in property development, construction, through which it

is primarily earned reasonable revenues. For such revenue recognition purpose, the

organization is used the AASB 15 revenues from customer’s contracts. Next to this AASB,

such group has followed the provisions of AASB 9 in the case to a classification,

measurement, hedge and impairment accounting of financial elements for accounting

recognition and analysis (Graham, Leary and Roberts 2015). This group has also followed the

provisions of AASB 16 in the case to leases of accounting properties.

Accounting policies:

For the purpose of accounting policies such group is mainly provided the concepts

relating to revenue recognition, in such concept the revenue is considered up to the extent that

it is able to provide some economic benefits to such group. In case of Lease, normally the

rental incomes from those investment properties are evaluated through the straight line basis

6INTERNATIONAL PROPERTY FINANCE

that depends on the terms of lease. However the contingent incomes are normally recognised

as income for the period in which it was earned. Along with such, this group is also provide

some concepts relating to revenues from contracts with individual customers, some policies

relating to the property management revenues, some relevant investment properties policies,

also development projects and constructions in progress policies, taxation policies, per

security earning policies etc. (Hasan, Hossain and Habib 2015).

Investments:

This group is engaged in investment properties relating with the shopping centre

investment and development projects & work-in-progress. In case of shopping centre

investment properties are generally relating with land and buildings that normally used as

freehold or leasehold purposes and also for the purpose of leasehold improvements. Those

leasehold land and buildings are treated as a composite asset and the value of such assets is

influenced through many individual factors. However in case of shopping centre investments

are normally evaluated at cost including the transaction value. Subsequently the group’s

shopping centres are stated at fair value and any income or losses from such changes in fair

value in shopping centres are reported in the income statements (Osinskiet al. 2017)

Taxation:

In case of taxable purpose, such group is comprises taxable and non-taxable

organizations and the income tax expenses is only recognised in respect of taxable

organizations. Here for the purpose of taxation the residential status of the parent company is

normally measured. Such holding company has commenced the tax funding agreement with

the Australian tax authorities in case to provide tax liabilities.

that depends on the terms of lease. However the contingent incomes are normally recognised

as income for the period in which it was earned. Along with such, this group is also provide

some concepts relating to revenues from contracts with individual customers, some policies

relating to the property management revenues, some relevant investment properties policies,

also development projects and constructions in progress policies, taxation policies, per

security earning policies etc. (Hasan, Hossain and Habib 2015).

Investments:

This group is engaged in investment properties relating with the shopping centre

investment and development projects & work-in-progress. In case of shopping centre

investment properties are generally relating with land and buildings that normally used as

freehold or leasehold purposes and also for the purpose of leasehold improvements. Those

leasehold land and buildings are treated as a composite asset and the value of such assets is

influenced through many individual factors. However in case of shopping centre investments

are normally evaluated at cost including the transaction value. Subsequently the group’s

shopping centres are stated at fair value and any income or losses from such changes in fair

value in shopping centres are reported in the income statements (Osinskiet al. 2017)

Taxation:

In case of taxable purpose, such group is comprises taxable and non-taxable

organizations and the income tax expenses is only recognised in respect of taxable

organizations. Here for the purpose of taxation the residential status of the parent company is

normally measured. Such holding company has commenced the tax funding agreement with

the Australian tax authorities in case to provide tax liabilities.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7INTERNATIONAL PROPERTY FINANCE

Depreciation:

Such group is mainly engaged in providing construction and leasing property

business. All the tangible assets including the plant, property and equipment is normally

evaluated at cost method, which is representing the historical cost. Such cost is deducted from

the impairment charges and also the amount of accumulated depreciation amount. In case of

depreciation, normally such group is followed the method of straight line to evaluate the

actual price of such assets during the particular period (Ratcliffe, Dimovski and

Keneley2017).

Capital Structure:

Scentre group generally divided their capital structure into two different financial

resources. One is the equity capital, and the other one is retained earnings. The equity capital

is divided between the member of Scentre group and external stakeholders (Serfling 2016).

Next financial resources of the company are debt or borrowings from the outside financial

institutions along with such the Scentre group having another resource of finance that is the

amount of retained earnings (Sotelo and McGreal 2016). In case of computation the

percentage of each capital sources in capital structure, generally the amount of retained

earnings are excluded (as it does not represent in capital structure, however such amount of

retained earnings are considered while preparing the weighted average cost of capital). The

percentages of individual capital in capital structure are given below;

Depreciation:

Such group is mainly engaged in providing construction and leasing property

business. All the tangible assets including the plant, property and equipment is normally

evaluated at cost method, which is representing the historical cost. Such cost is deducted from

the impairment charges and also the amount of accumulated depreciation amount. In case of

depreciation, normally such group is followed the method of straight line to evaluate the

actual price of such assets during the particular period (Ratcliffe, Dimovski and

Keneley2017).

Capital Structure:

Scentre group generally divided their capital structure into two different financial

resources. One is the equity capital, and the other one is retained earnings. The equity capital

is divided between the member of Scentre group and external stakeholders (Serfling 2016).

Next financial resources of the company are debt or borrowings from the outside financial

institutions along with such the Scentre group having another resource of finance that is the

amount of retained earnings (Sotelo and McGreal 2016). In case of computation the

percentage of each capital sources in capital structure, generally the amount of retained

earnings are excluded (as it does not represent in capital structure, however such amount of

retained earnings are considered while preparing the weighted average cost of capital). The

percentages of individual capital in capital structure are given below;

8INTERNATIONAL PROPERTY FINANCE

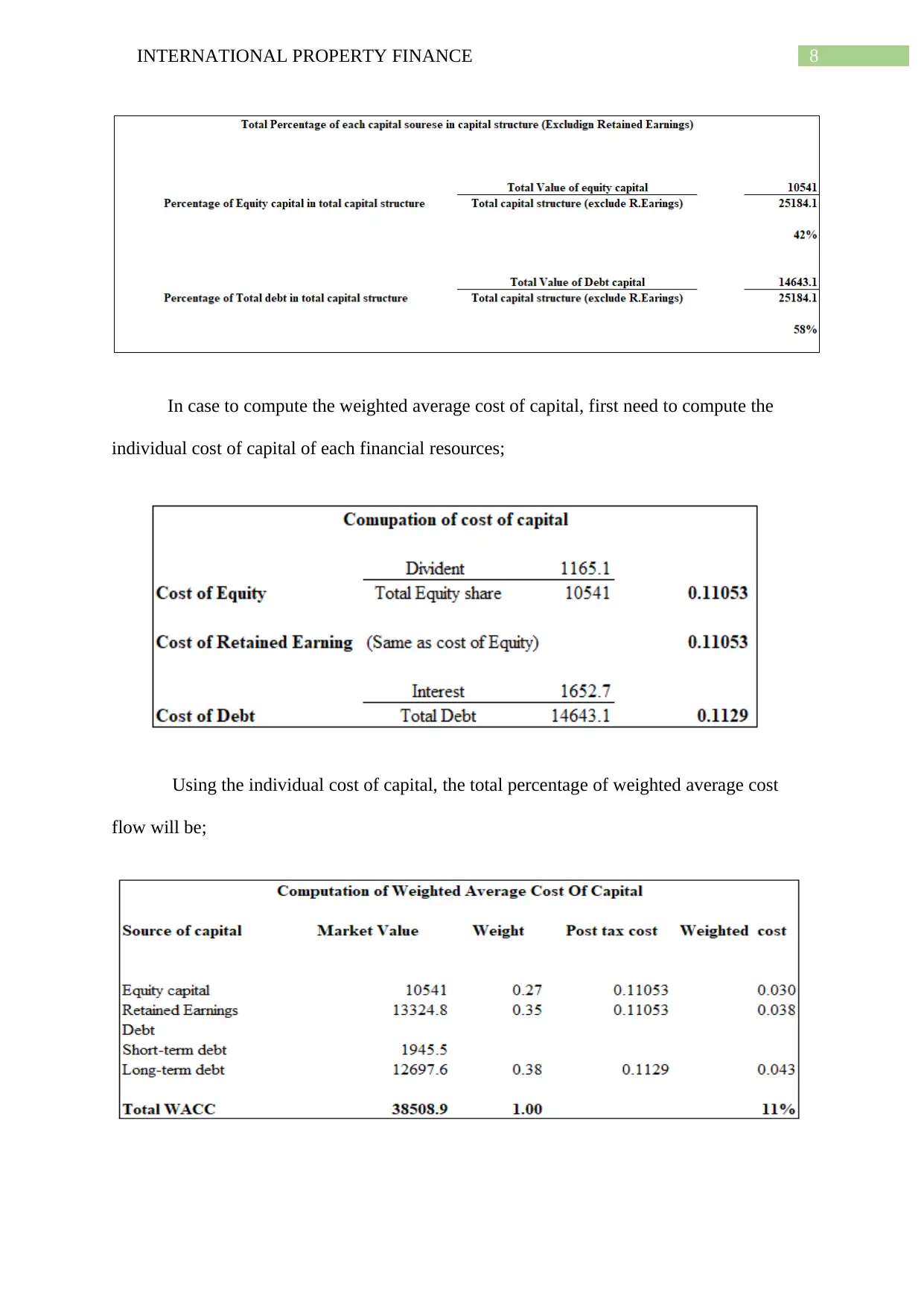

In case to compute the weighted average cost of capital, first need to compute the

individual cost of capital of each financial resources;

Using the individual cost of capital, the total percentage of weighted average cost

flow will be;

In case to compute the weighted average cost of capital, first need to compute the

individual cost of capital of each financial resources;

Using the individual cost of capital, the total percentage of weighted average cost

flow will be;

9INTERNATIONAL PROPERTY FINANCE

After analysing the calculation of the percentage of capital sources in capital

structure, it was found that the rate of equity capital is less than the percentage of total debt.

Such percentages structure is generally implies that the amount of debt or outside borrowing

capital amount is higher comparing with organizations own contributions. However, the

organization has a large amount of retained earnings, which is enough in the case to maintain

the overall capital structure of the organization (THANGAMANI 2018). Though in the case

to survive in the long run, an organization is required to increase the amount of capital,

through raised the amount of equity capital not with the using the external borrowings.

In the present scenario, such an organization is intended to invest in any capital assets

through the using of capital funds, like equity capital and debt capital. It will be better for the

company to use both the funds equally or increased the amount of equity capital more

comparing with the amount of total debt.

Conclusion:

It can be concluded from the above discussion that this report is mainly providing a

brief idea about the real estate investment trust or REIT. Those organizations are primarily

raised its money from the collection of investors and through providing them with access to

real estate. Here, in this report for evaluating the overall performance of a REIT, select

Scentre Group, which is one of the real estate investment trusts, mainly owned and conducts

the pre-eminent shopping centre in Australia. In the first part of this report is providing a

basic overview of Scentre Group. The details about the group’s performance, profit

evaluation method, amount of profitability etc. Next to such a basic overview, this report is

providing a brief idea about the using of AASB, that generally followed by Scentre Group.

After such individual AASB details, this report is offered the general accounting policies.

Such policies were normally accompanied by such a group in the case to perform their

After analysing the calculation of the percentage of capital sources in capital

structure, it was found that the rate of equity capital is less than the percentage of total debt.

Such percentages structure is generally implies that the amount of debt or outside borrowing

capital amount is higher comparing with organizations own contributions. However, the

organization has a large amount of retained earnings, which is enough in the case to maintain

the overall capital structure of the organization (THANGAMANI 2018). Though in the case

to survive in the long run, an organization is required to increase the amount of capital,

through raised the amount of equity capital not with the using the external borrowings.

In the present scenario, such an organization is intended to invest in any capital assets

through the using of capital funds, like equity capital and debt capital. It will be better for the

company to use both the funds equally or increased the amount of equity capital more

comparing with the amount of total debt.

Conclusion:

It can be concluded from the above discussion that this report is mainly providing a

brief idea about the real estate investment trust or REIT. Those organizations are primarily

raised its money from the collection of investors and through providing them with access to

real estate. Here, in this report for evaluating the overall performance of a REIT, select

Scentre Group, which is one of the real estate investment trusts, mainly owned and conducts

the pre-eminent shopping centre in Australia. In the first part of this report is providing a

basic overview of Scentre Group. The details about the group’s performance, profit

evaluation method, amount of profitability etc. Next to such a basic overview, this report is

providing a brief idea about the using of AASB, that generally followed by Scentre Group.

After such individual AASB details, this report is offered the general accounting policies.

Such policies were normally accompanied by such a group in the case to perform their

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10INTERNATIONAL PROPERTY FINANCE

overall operations. Next to such accounting policies, this report is providing the relevant idea

about group’s investment policies, Derivative financial instruments, taxation policies,

generally followed depreciation method etc. As a final presentation, this report is providing

the complete details of the group’s capital structure. In this capital structure, generally, two

different financial sources are used. As a conclusion, this report is providing the basic

calculation of the weighted average cost of capital in the case to evaluate the overall

performance of the organization.

overall operations. Next to such accounting policies, this report is providing the relevant idea

about group’s investment policies, Derivative financial instruments, taxation policies,

generally followed depreciation method etc. As a final presentation, this report is providing

the complete details of the group’s capital structure. In this capital structure, generally, two

different financial sources are used. As a conclusion, this report is providing the basic

calculation of the weighted average cost of capital in the case to evaluate the overall

performance of the organization.

11INTERNATIONAL PROPERTY FINANCE

References:

Andreasen, E., Schindler, M.M. and Valenzuela, M.P.A., 2017. Capital controls and the cost

of debt. International Monetary Fund.

Annualreport,(2018).[ebook]pp.3472.Availableat:https://www.scentregroup.com/getmedia/

d563d065-7c64-4632-a67b-5d30884237aa/2018-Annual-Financial-Report_20-Feb-19.pdf

[Accessed 30 Sep. 2019].

Bradley, D., Pantzalis, C. and Yuan, X., 2016. Policy risk, corporate political strategies, and

the cost of debt. Journal of Corporate Finance, 40, pp.254-275.

Brusov, P., Filatova, T., Orekhova, N. and Eskindarov, M., 2018. Capital Structure:

Modigliani–Miller Theory. In Modern Corporate Finance, Investments, Taxation and Ratings

(pp. 9-27). Springer, Cham.

El Ghoul, S., Guedhami, O., Kim, H. and Park, K., 2018. Corporate environmental

responsibility and the cost of capital: International evidence. Journal of Business Ethics,

149(2), pp.335-361.

Graham, J.R., Leary, M.T. and Roberts, M.R., 2015. A century of capital structure: The

leveraging of corporate America. Journal of Financial Economics, 118(3), pp.658-683.

Hasan, M.M., Hossain, M. and Habib, A., 2015. Corporate life cycle and cost of equity

capital. Journal of Contemporary Accounting & Economics, 11(1), pp.46-60.

Horváthová, J. and Mokrišová, M., 2017. Analysis of the impact of capital structure on

business performance. European Financial Systems 2017, p.243.

Osinski, M., Selig, P.M., Matos, F. and Roman, D.J., 2017. Methods of evaluation of

intangible assets and intellectual capital. Journal of Intellectual Capital, 18(3), pp.470-485.

Ratcliffe, C., Dimovski, B. and Keneley, M., 2017. Long‐Term post‐merger announcement

performance. A case study of Australian listed real estate. Accounting & Finance, 57(3),

pp.855-877.

References:

Andreasen, E., Schindler, M.M. and Valenzuela, M.P.A., 2017. Capital controls and the cost

of debt. International Monetary Fund.

Annualreport,(2018).[ebook]pp.3472.Availableat:https://www.scentregroup.com/getmedia/

d563d065-7c64-4632-a67b-5d30884237aa/2018-Annual-Financial-Report_20-Feb-19.pdf

[Accessed 30 Sep. 2019].

Bradley, D., Pantzalis, C. and Yuan, X., 2016. Policy risk, corporate political strategies, and

the cost of debt. Journal of Corporate Finance, 40, pp.254-275.

Brusov, P., Filatova, T., Orekhova, N. and Eskindarov, M., 2018. Capital Structure:

Modigliani–Miller Theory. In Modern Corporate Finance, Investments, Taxation and Ratings

(pp. 9-27). Springer, Cham.

El Ghoul, S., Guedhami, O., Kim, H. and Park, K., 2018. Corporate environmental

responsibility and the cost of capital: International evidence. Journal of Business Ethics,

149(2), pp.335-361.

Graham, J.R., Leary, M.T. and Roberts, M.R., 2015. A century of capital structure: The

leveraging of corporate America. Journal of Financial Economics, 118(3), pp.658-683.

Hasan, M.M., Hossain, M. and Habib, A., 2015. Corporate life cycle and cost of equity

capital. Journal of Contemporary Accounting & Economics, 11(1), pp.46-60.

Horváthová, J. and Mokrišová, M., 2017. Analysis of the impact of capital structure on

business performance. European Financial Systems 2017, p.243.

Osinski, M., Selig, P.M., Matos, F. and Roman, D.J., 2017. Methods of evaluation of

intangible assets and intellectual capital. Journal of Intellectual Capital, 18(3), pp.470-485.

Ratcliffe, C., Dimovski, B. and Keneley, M., 2017. Long‐Term post‐merger announcement

performance. A case study of Australian listed real estate. Accounting & Finance, 57(3),

pp.855-877.

12INTERNATIONAL PROPERTY FINANCE

Serfling, M., 2016. Firing costs and capital structure decisions. The Journal of Finance,

71(5), pp.2239-2286.

Sotelo, R. and McGreal, S., 2016. Real estate investment trusts in Europe. Springer-Verlag

Berlin An.

THANGAMANI, M., 2018. Capital structure analysis of software companies in India: A

structural equation modeling approach. International Journal of Pure and Applied

Mathematics, 119(10), pp.1369-1383.

Wahba, H., 2008. Does the market value corporate environmental responsibility? An

empirical examination. Corporate Social Responsibility and Environmental Management,

15(2), pp.89-99.

Xu, S., Liu, D. and Huang, J., 2015. Corporate social responsibility, the cost of equity capital

and ownership structure: An analysis of Chinese listed firms. Australian Journal of

Management, 40(2), pp.245-276.

Serfling, M., 2016. Firing costs and capital structure decisions. The Journal of Finance,

71(5), pp.2239-2286.

Sotelo, R. and McGreal, S., 2016. Real estate investment trusts in Europe. Springer-Verlag

Berlin An.

THANGAMANI, M., 2018. Capital structure analysis of software companies in India: A

structural equation modeling approach. International Journal of Pure and Applied

Mathematics, 119(10), pp.1369-1383.

Wahba, H., 2008. Does the market value corporate environmental responsibility? An

empirical examination. Corporate Social Responsibility and Environmental Management,

15(2), pp.89-99.

Xu, S., Liu, D. and Huang, J., 2015. Corporate social responsibility, the cost of equity capital

and ownership structure: An analysis of Chinese listed firms. Australian Journal of

Management, 40(2), pp.245-276.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.