Management Accounting Report: HLW Case Study Analysis and Projections

VerifiedAdded on 2020/05/16

|15

|2908

|310

Report

AI Summary

This management accounting report analyzes a case study, focusing on cost accounting and management accounting principles, with an emphasis on cash flow projections and activity-based costing. The report is divided into two parts. Part A involves calculating overhead costs using activity-based co...

Running head: MANAGEMENT ACCOUNTING

Management Accounting

Name of the Student

Name of the University

Authors Note

Course ID

Management Accounting

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGEMENT ACCOUNTING

Executive Summary:

The main objective of the report is to provide the management with the necessary projection

of future profits to make the necessary decision. The case study is based on the explanation of

the two important methods namely the cost accounting and the management accounting with

better understanding of the cash flow. The initial stages of the case study is based on the

determination of the overhead cost involved in the calculating the cost of product. The second

part of the study is associated with the determination of the cash flow from the application of

the new plans. The report would demonstrate the effectiveness of the activity based costing

techniques in the process of business decision making.

Executive Summary:

The main objective of the report is to provide the management with the necessary projection

of future profits to make the necessary decision. The case study is based on the explanation of

the two important methods namely the cost accounting and the management accounting with

better understanding of the cash flow. The initial stages of the case study is based on the

determination of the overhead cost involved in the calculating the cost of product. The second

part of the study is associated with the determination of the cash flow from the application of

the new plans. The report would demonstrate the effectiveness of the activity based costing

techniques in the process of business decision making.

2MANAGEMENT ACCOUNTING

Table of Contents

Answer to task Part A:...............................................................................................................3

Answer to requirement A:..........................................................................................................3

Answer to requirement B:..........................................................................................................3

Answer to requirement C:..........................................................................................................4

Answer to part B:.......................................................................................................................5

Answer to requirement A:..........................................................................................................5

Answer to requirement B:..........................................................................................................7

Sales revenue under the new scheme of membership:...............................................................8

Effect on sales revenue and cash inflow:...................................................................................9

Answer to Requirement 3:.......................................................................................................10

Conclusion:..............................................................................................................................11

Reference List:.........................................................................................................................12

Table of Contents

Answer to task Part A:...............................................................................................................3

Answer to requirement A:..........................................................................................................3

Answer to requirement B:..........................................................................................................3

Answer to requirement C:..........................................................................................................4

Answer to part B:.......................................................................................................................5

Answer to requirement A:..........................................................................................................5

Answer to requirement B:..........................................................................................................7

Sales revenue under the new scheme of membership:...............................................................8

Effect on sales revenue and cash inflow:...................................................................................9

Answer to Requirement 3:.......................................................................................................10

Conclusion:..............................................................................................................................11

Reference List:.........................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGEMENT ACCOUNTING

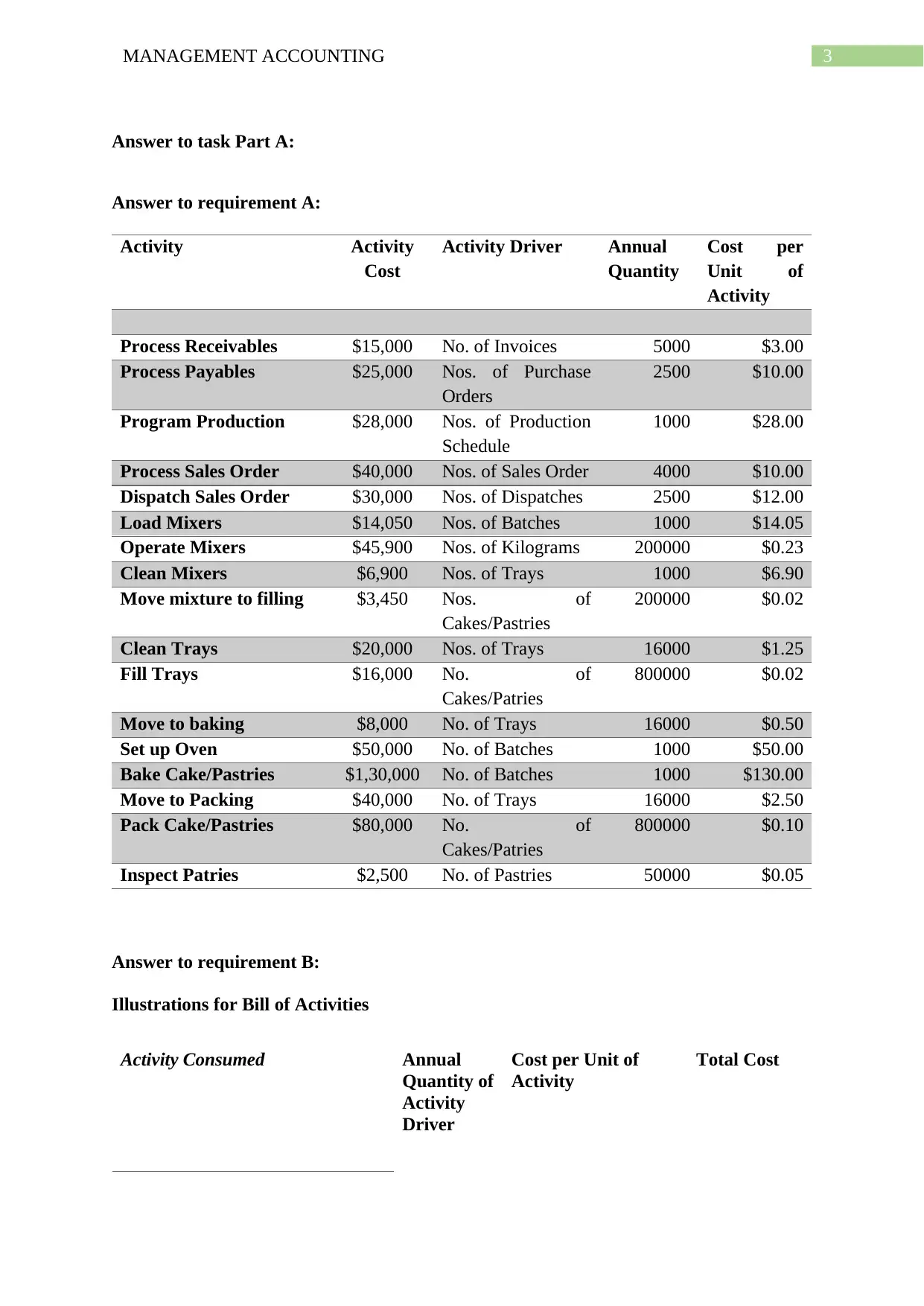

Answer to task Part A:

Answer to requirement A:

Activity Activity

Cost

Activity Driver Annual

Quantity

Cost per

Unit of

Activity

Process Receivables $15,000 No. of Invoices 5000 $3.00

Process Payables $25,000 Nos. of Purchase

Orders

2500 $10.00

Program Production $28,000 Nos. of Production

Schedule

1000 $28.00

Process Sales Order $40,000 Nos. of Sales Order 4000 $10.00

Dispatch Sales Order $30,000 Nos. of Dispatches 2500 $12.00

Load Mixers $14,050 Nos. of Batches 1000 $14.05

Operate Mixers $45,900 Nos. of Kilograms 200000 $0.23

Clean Mixers $6,900 Nos. of Trays 1000 $6.90

Move mixture to filling $3,450 Nos. of

Cakes/Pastries

200000 $0.02

Clean Trays $20,000 Nos. of Trays 16000 $1.25

Fill Trays $16,000 No. of

Cakes/Patries

800000 $0.02

Move to baking $8,000 No. of Trays 16000 $0.50

Set up Oven $50,000 No. of Batches 1000 $50.00

Bake Cake/Pastries $1,30,000 No. of Batches 1000 $130.00

Move to Packing $40,000 No. of Trays 16000 $2.50

Pack Cake/Pastries $80,000 No. of

Cakes/Patries

800000 $0.10

Inspect Patries $2,500 No. of Pastries 50000 $0.05

Answer to requirement B:

Illustrations for Bill of Activities

Activity Consumed Annual

Quantity of

Activity

Driver

Cost per Unit of

Activity

Total Cost

Answer to task Part A:

Answer to requirement A:

Activity Activity

Cost

Activity Driver Annual

Quantity

Cost per

Unit of

Activity

Process Receivables $15,000 No. of Invoices 5000 $3.00

Process Payables $25,000 Nos. of Purchase

Orders

2500 $10.00

Program Production $28,000 Nos. of Production

Schedule

1000 $28.00

Process Sales Order $40,000 Nos. of Sales Order 4000 $10.00

Dispatch Sales Order $30,000 Nos. of Dispatches 2500 $12.00

Load Mixers $14,050 Nos. of Batches 1000 $14.05

Operate Mixers $45,900 Nos. of Kilograms 200000 $0.23

Clean Mixers $6,900 Nos. of Trays 1000 $6.90

Move mixture to filling $3,450 Nos. of

Cakes/Pastries

200000 $0.02

Clean Trays $20,000 Nos. of Trays 16000 $1.25

Fill Trays $16,000 No. of

Cakes/Patries

800000 $0.02

Move to baking $8,000 No. of Trays 16000 $0.50

Set up Oven $50,000 No. of Batches 1000 $50.00

Bake Cake/Pastries $1,30,000 No. of Batches 1000 $130.00

Move to Packing $40,000 No. of Trays 16000 $2.50

Pack Cake/Pastries $80,000 No. of

Cakes/Patries

800000 $0.10

Inspect Patries $2,500 No. of Pastries 50000 $0.05

Answer to requirement B:

Illustrations for Bill of Activities

Activity Consumed Annual

Quantity of

Activity

Driver

Cost per Unit of

Activity

Total Cost

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGEMENT ACCOUNTING

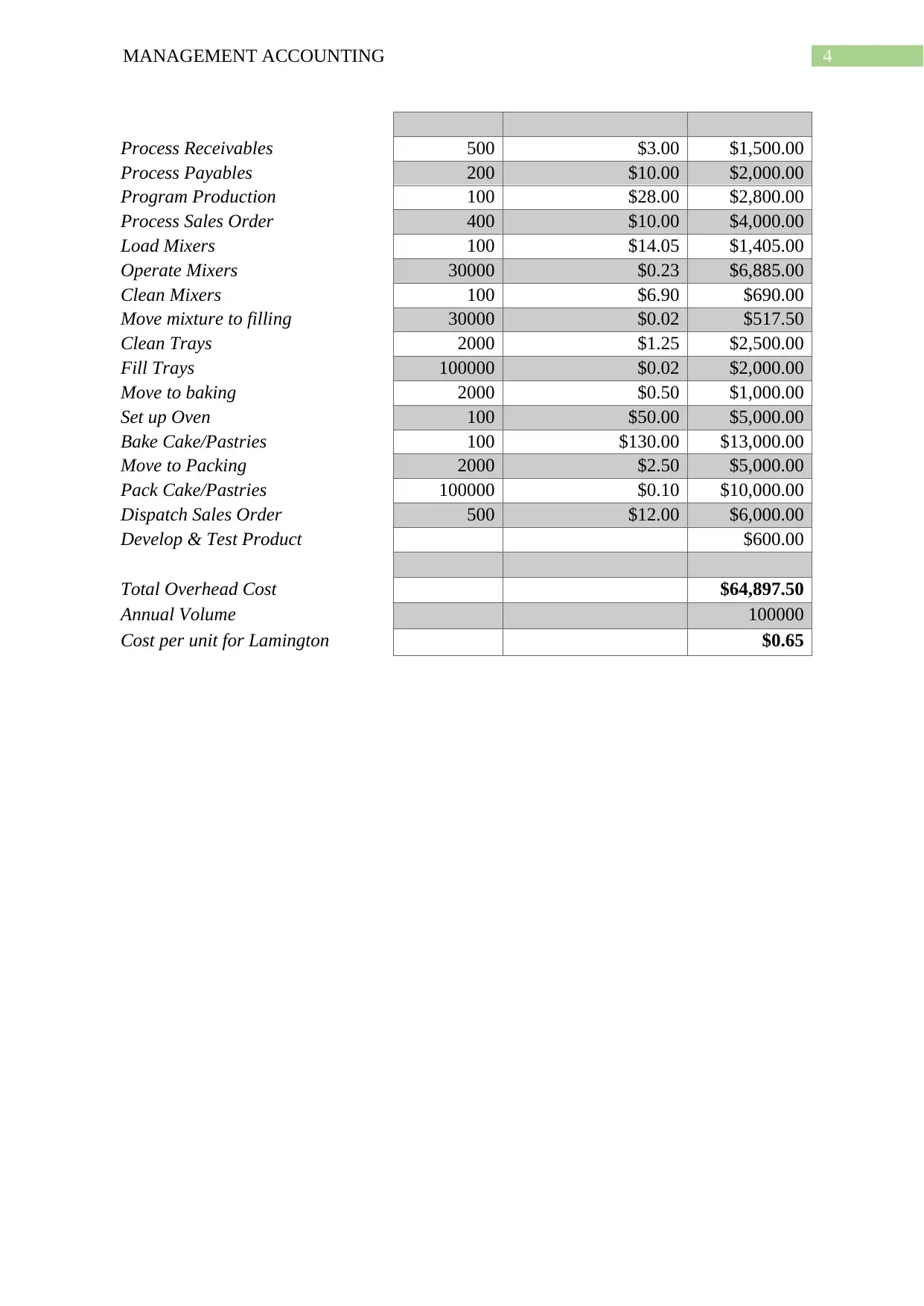

Process Receivables 500 $3.00 $1,500.00

Process Payables 200 $10.00 $2,000.00

Program Production 100 $28.00 $2,800.00

Process Sales Order 400 $10.00 $4,000.00

Load Mixers 100 $14.05 $1,405.00

Operate Mixers 30000 $0.23 $6,885.00

Clean Mixers 100 $6.90 $690.00

Move mixture to filling 30000 $0.02 $517.50

Clean Trays 2000 $1.25 $2,500.00

Fill Trays 100000 $0.02 $2,000.00

Move to baking 2000 $0.50 $1,000.00

Set up Oven 100 $50.00 $5,000.00

Bake Cake/Pastries 100 $130.00 $13,000.00

Move to Packing 2000 $2.50 $5,000.00

Pack Cake/Pastries 100000 $0.10 $10,000.00

Dispatch Sales Order 500 $12.00 $6,000.00

Develop & Test Product $600.00

Total Overhead Cost $64,897.50

Annual Volume 100000

Cost per unit for Lamington $0.65

Process Receivables 500 $3.00 $1,500.00

Process Payables 200 $10.00 $2,000.00

Program Production 100 $28.00 $2,800.00

Process Sales Order 400 $10.00 $4,000.00

Load Mixers 100 $14.05 $1,405.00

Operate Mixers 30000 $0.23 $6,885.00

Clean Mixers 100 $6.90 $690.00

Move mixture to filling 30000 $0.02 $517.50

Clean Trays 2000 $1.25 $2,500.00

Fill Trays 100000 $0.02 $2,000.00

Move to baking 2000 $0.50 $1,000.00

Set up Oven 100 $50.00 $5,000.00

Bake Cake/Pastries 100 $130.00 $13,000.00

Move to Packing 2000 $2.50 $5,000.00

Pack Cake/Pastries 100000 $0.10 $10,000.00

Dispatch Sales Order 500 $12.00 $6,000.00

Develop & Test Product $600.00

Total Overhead Cost $64,897.50

Annual Volume 100000

Cost per unit for Lamington $0.65

5MANAGEMENT ACCOUNTING

Answer to requirement C:

As evident from the illustration of the computations that has been performed above an

important consideration in this regard is that the overhead cost is quantified. Evidences from

the calculations have stated that there are indirect costs that offers their support to the process

of producing or alternatively in the procedure of allocation (Renz, 2016). Additionally the

indications from the calculations have represented that there are large sum of indirect cost

that are considered as the part of the cost however the indirect costs that are occurred have

not yet been incorporated. Direct cost are regarded as those costs, which can be assigned to

the product cost of the specific goods and services (Zeff, 2016). There are certain costs that

are regarded as the part of the direct cost namely the depreciation costs and the administrative

expenditure. These costs are regarded as the difficult to distribute and therefore there are

considered as the indirect costs.

Direct costs are treated as those costs that primarily originates from the production of

goods and services in which the firms is dealing (Clinton & England, 2016). They are

regarded as the important element of the production process however there are some are some

situations where manufacturing of goods and services cannot be done with incurring any

direct cost. In order to arrive at the cost of production of the lamington, it is necessary to take

account of the indirect costs and these costs are stated below in the tabular format

a. Costs originating from the freight inward

b. Direct cost associated with labour

c. Direct costs associated with materials

Answer to requirement C:

As evident from the illustration of the computations that has been performed above an

important consideration in this regard is that the overhead cost is quantified. Evidences from

the calculations have stated that there are indirect costs that offers their support to the process

of producing or alternatively in the procedure of allocation (Renz, 2016). Additionally the

indications from the calculations have represented that there are large sum of indirect cost

that are considered as the part of the cost however the indirect costs that are occurred have

not yet been incorporated. Direct cost are regarded as those costs, which can be assigned to

the product cost of the specific goods and services (Zeff, 2016). There are certain costs that

are regarded as the part of the direct cost namely the depreciation costs and the administrative

expenditure. These costs are regarded as the difficult to distribute and therefore there are

considered as the indirect costs.

Direct costs are treated as those costs that primarily originates from the production of

goods and services in which the firms is dealing (Clinton & England, 2016). They are

regarded as the important element of the production process however there are some are some

situations where manufacturing of goods and services cannot be done with incurring any

direct cost. In order to arrive at the cost of production of the lamington, it is necessary to take

account of the indirect costs and these costs are stated below in the tabular format

a. Costs originating from the freight inward

b. Direct cost associated with labour

c. Direct costs associated with materials

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGEMENT ACCOUNTING

Answer to part B:

Answer to requirement A:

On viewing the circumstances from the case study, it is understood that the amount of

revenue that is derived by the HLW are largely from two different bases. The sales revenue

that is generated by HLW is particularly from the yearly subscription of membership and the

revenue that is derived from the court fees (Morden, 2017). Accordingly, there are greater

than 40% of the total amount of sales revenue that is generated from the yearly membership

fees for the period of two months. On considering the remaining part, it can be inferred from

the case study that revenue generated from the court fees is based on yearly basis.

To be very specific the cash flow that is generated from the court fees generally

remains uneven in every month. An important assertion in this regard is that whenever the

business is experiencing the peak time the revenue that is derived from the court fees

multiplies double fold and significantly increases by 45% of the total sales (Schuster, 2015).

Furthermore, commencing from the period of May to September the instances obtained from

the case study has suggested that the amount of court fees has fell down significantly and

yields as low as 15% of the total sum of sales revenue.

In the current state of affairs of HLW on applying the newly proposed plans of

membership, it is understood that the scheme has yielded approximately 80% of the total sum

of sales income inside the first month of the financial year (Mohanty, 2014). In addition to

this, HLW would be able to gain benefit of the increased revenue and these benefits are stated

below;

a. With the application of the new plans, HLW is in the position of gaining the

advantage of the greater increases in the cash flow that would be generated for the

Answer to part B:

Answer to requirement A:

On viewing the circumstances from the case study, it is understood that the amount of

revenue that is derived by the HLW are largely from two different bases. The sales revenue

that is generated by HLW is particularly from the yearly subscription of membership and the

revenue that is derived from the court fees (Morden, 2017). Accordingly, there are greater

than 40% of the total amount of sales revenue that is generated from the yearly membership

fees for the period of two months. On considering the remaining part, it can be inferred from

the case study that revenue generated from the court fees is based on yearly basis.

To be very specific the cash flow that is generated from the court fees generally

remains uneven in every month. An important assertion in this regard is that whenever the

business is experiencing the peak time the revenue that is derived from the court fees

multiplies double fold and significantly increases by 45% of the total sales (Schuster, 2015).

Furthermore, commencing from the period of May to September the instances obtained from

the case study has suggested that the amount of court fees has fell down significantly and

yields as low as 15% of the total sum of sales revenue.

In the current state of affairs of HLW on applying the newly proposed plans of

membership, it is understood that the scheme has yielded approximately 80% of the total sum

of sales income inside the first month of the financial year (Mohanty, 2014). In addition to

this, HLW would be able to gain benefit of the increased revenue and these benefits are stated

below;

a. With the application of the new plans, HLW is in the position of gaining the

advantage of the greater increases in the cash flow that would be generated for the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGEMENT ACCOUNTING

operational sources and yearly subscriptions to the memberships (Klychova et al.,

2014).

b. On the considering the current stated plan, the club is under obligation of remaining

reliant on the single schemes of generating fees such as the hourly fees that is

generated from the court would ultimately increase by 50% of the total amount of

anticipated revenue from the application of new plans.

c. With the application of the new improved plan, the HLW would be able to generate

revenue that would enable the club in generating greater volume of cash in every

month (Otley, 2016).

d. The application of the new plan would be considered to be beneficial for the club as

the managers of the club would be able to gain more than 80% of the total revenue

during beginning phases of the implementation rather than waiting for the completion

of six months (Cooper, 2017). Because of this benefit would enable management of

the club in making an appropriate use of the accumulated funds by taking account of

the several accounting decisions as and when required.

Answer to requirement B:

The evidences that has been obtained from the case study evidently provides that

there are several number of issues and because of this there are some specific number of

assumptions that is needed to be made (Malmi, 2016). These assumptions would enable in

gauging into the effect that is created by the new plans of membership. The necessary

assumptions are listed below;

a. Full use of the court should be made by the management of the club during the high

business hours

b. Sixty percent of the utilization capacity must be made when the business is not

running in in the peak time.

operational sources and yearly subscriptions to the memberships (Klychova et al.,

2014).

b. On the considering the current stated plan, the club is under obligation of remaining

reliant on the single schemes of generating fees such as the hourly fees that is

generated from the court would ultimately increase by 50% of the total amount of

anticipated revenue from the application of new plans.

c. With the application of the new improved plan, the HLW would be able to generate

revenue that would enable the club in generating greater volume of cash in every

month (Otley, 2016).

d. The application of the new plan would be considered to be beneficial for the club as

the managers of the club would be able to gain more than 80% of the total revenue

during beginning phases of the implementation rather than waiting for the completion

of six months (Cooper, 2017). Because of this benefit would enable management of

the club in making an appropriate use of the accumulated funds by taking account of

the several accounting decisions as and when required.

Answer to requirement B:

The evidences that has been obtained from the case study evidently provides that

there are several number of issues and because of this there are some specific number of

assumptions that is needed to be made (Malmi, 2016). These assumptions would enable in

gauging into the effect that is created by the new plans of membership. The necessary

assumptions are listed below;

a. Full use of the court should be made by the management of the club during the high

business hours

b. Sixty percent of the utilization capacity must be made when the business is not

running in in the peak time.

8MANAGEMENT ACCOUNTING

c. It is assumed that that the management to resolve the issue must make around forty

per cent of the overall usage of court during the lean business hours (Lanen, 2016).

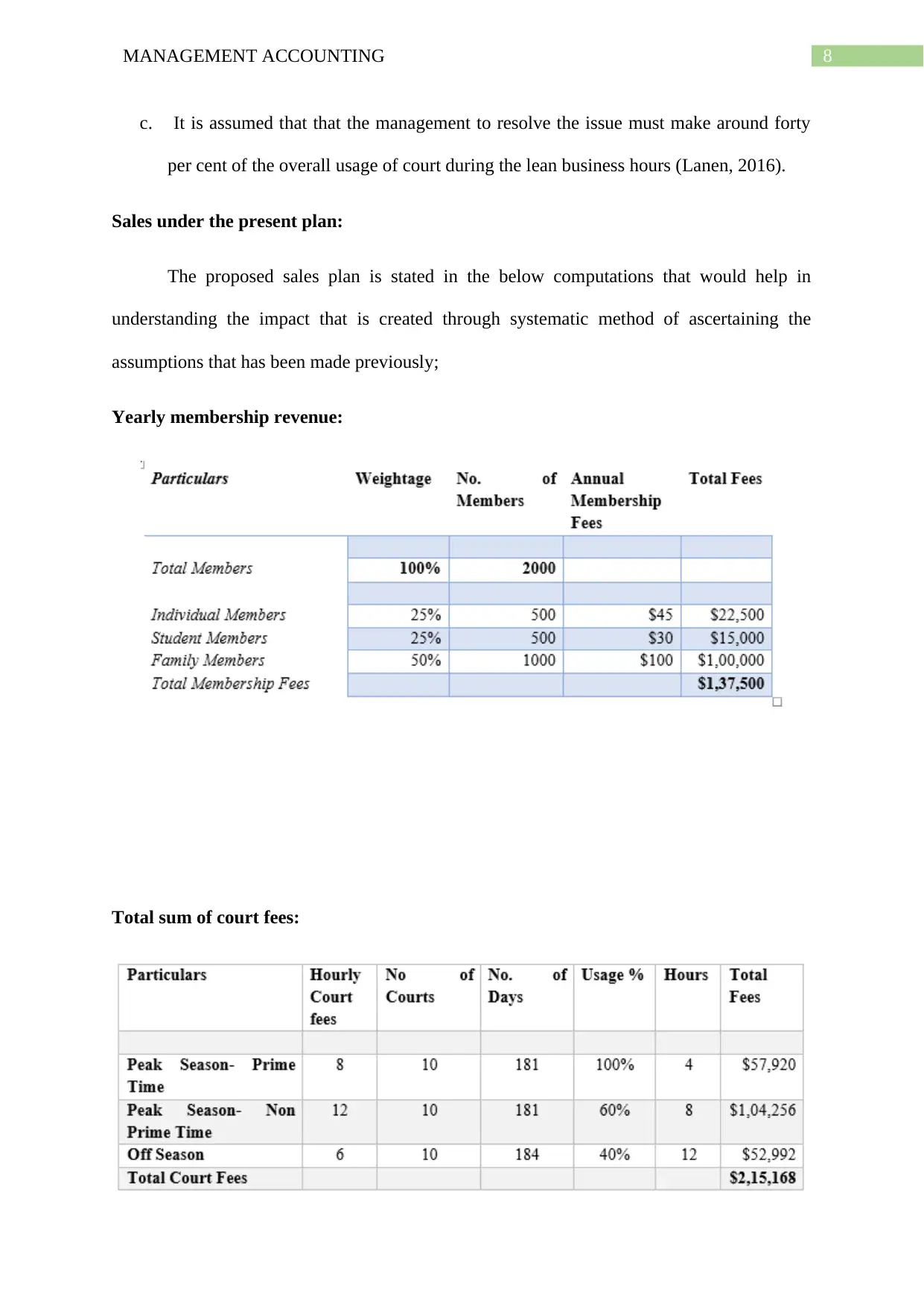

Sales under the present plan:

The proposed sales plan is stated in the below computations that would help in

understanding the impact that is created through systematic method of ascertaining the

assumptions that has been made previously;

Yearly membership revenue:

Total sum of court fees:

c. It is assumed that that the management to resolve the issue must make around forty

per cent of the overall usage of court during the lean business hours (Lanen, 2016).

Sales under the present plan:

The proposed sales plan is stated in the below computations that would help in

understanding the impact that is created through systematic method of ascertaining the

assumptions that has been made previously;

Yearly membership revenue:

Total sum of court fees:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGEMENT ACCOUNTING

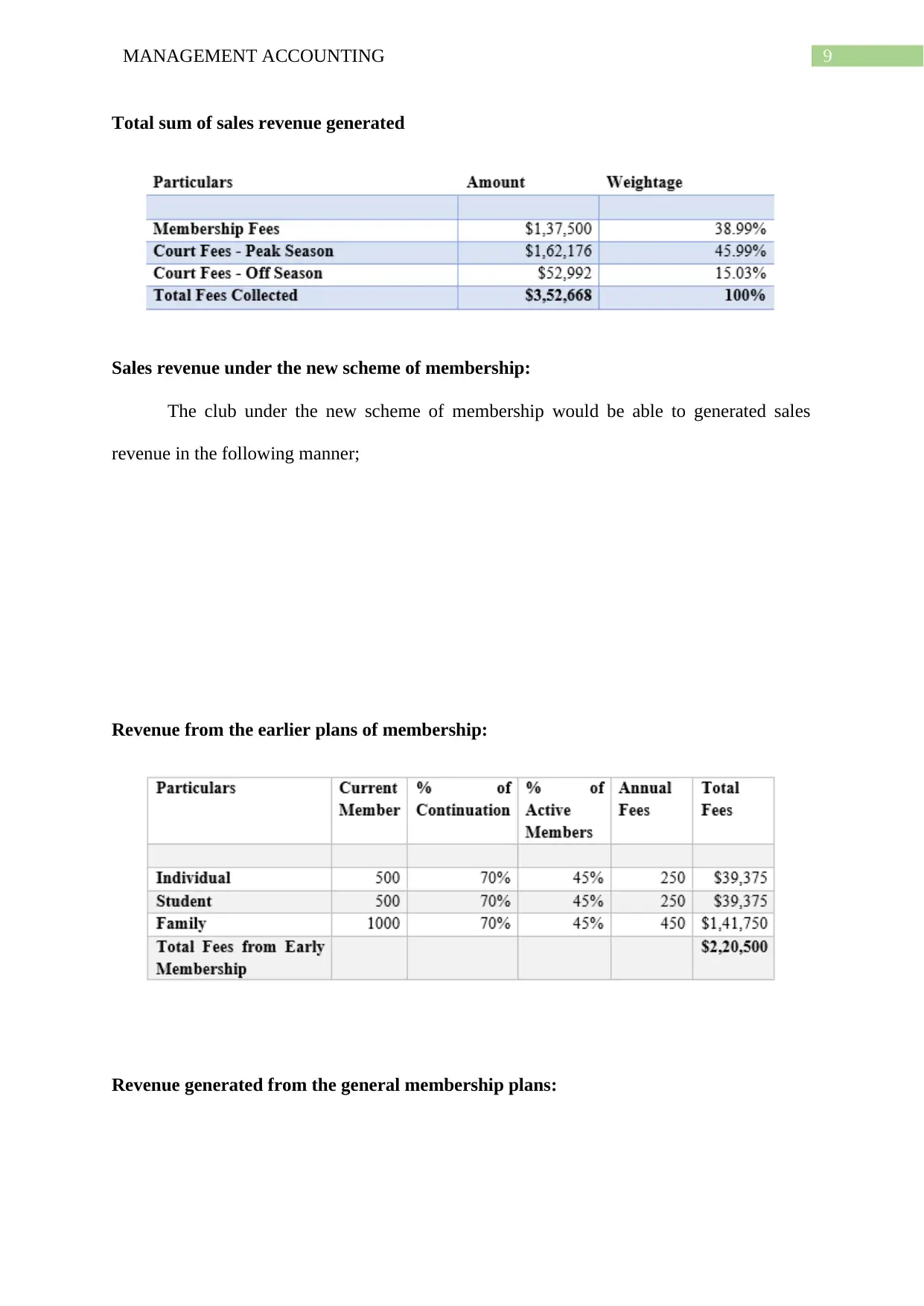

Total sum of sales revenue generated

Sales revenue under the new scheme of membership:

The club under the new scheme of membership would be able to generated sales

revenue in the following manner;

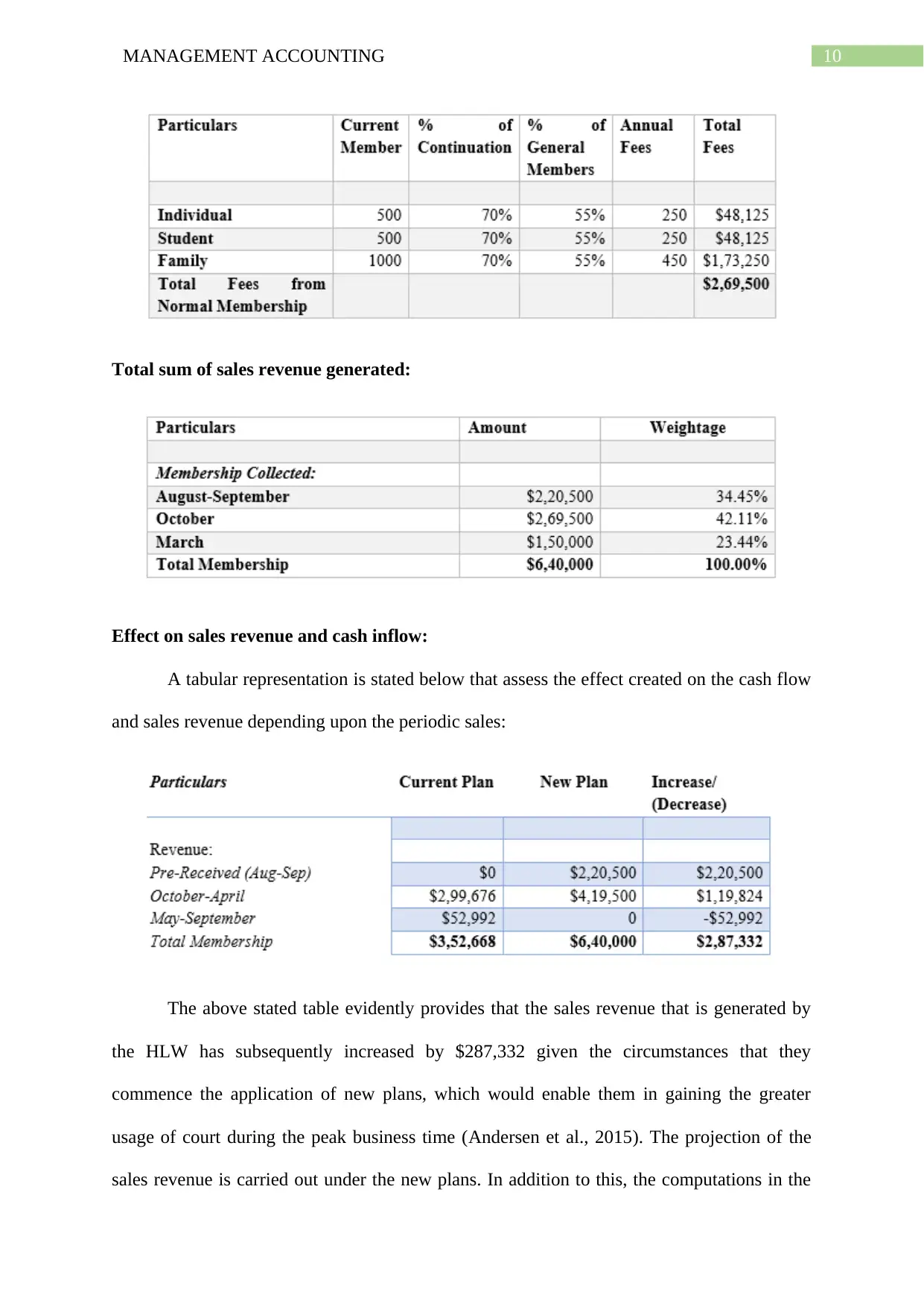

Revenue from the earlier plans of membership:

Revenue generated from the general membership plans:

Total sum of sales revenue generated

Sales revenue under the new scheme of membership:

The club under the new scheme of membership would be able to generated sales

revenue in the following manner;

Revenue from the earlier plans of membership:

Revenue generated from the general membership plans:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGEMENT ACCOUNTING

Total sum of sales revenue generated:

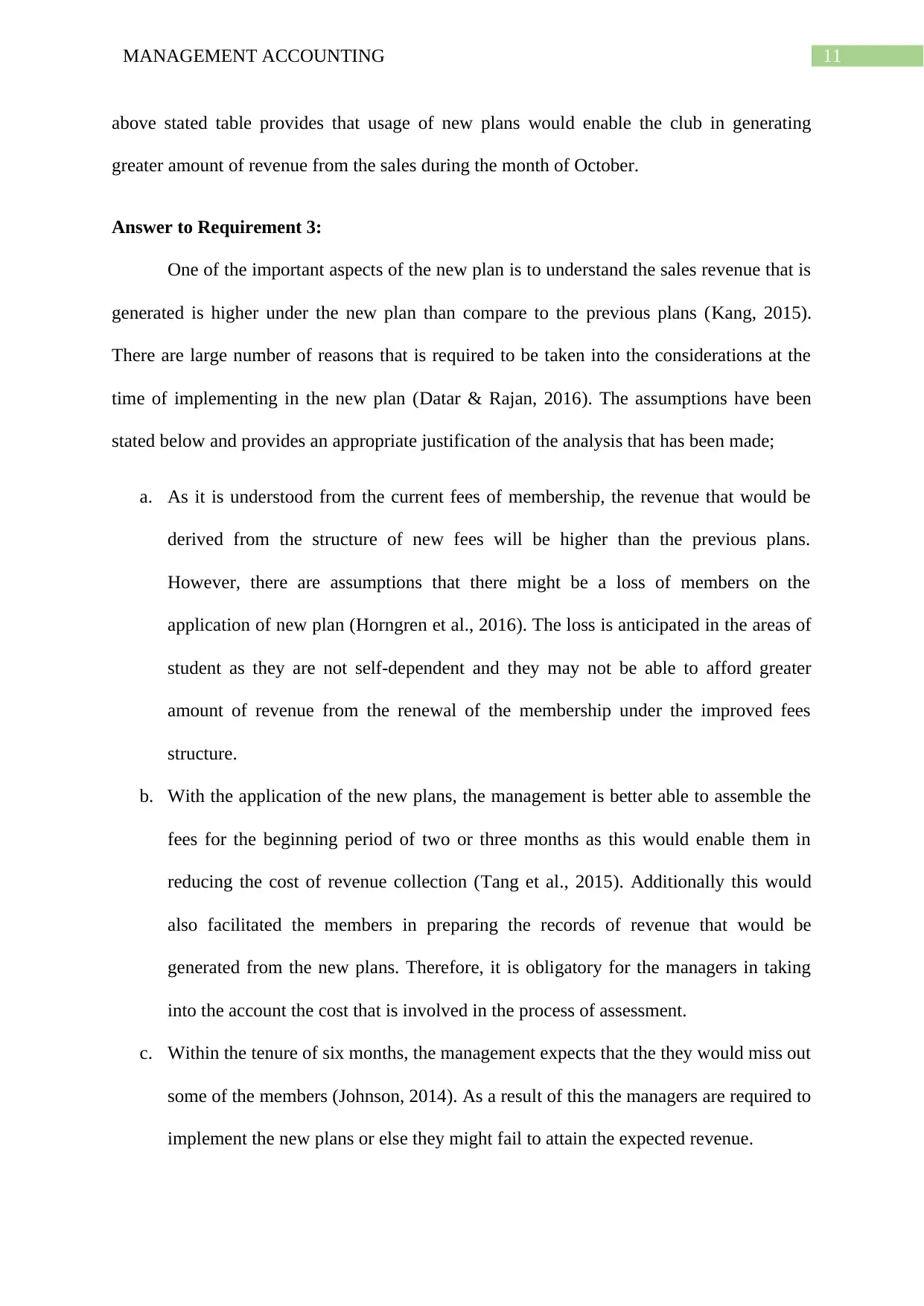

Effect on sales revenue and cash inflow:

A tabular representation is stated below that assess the effect created on the cash flow

and sales revenue depending upon the periodic sales:

The above stated table evidently provides that the sales revenue that is generated by

the HLW has subsequently increased by $287,332 given the circumstances that they

commence the application of new plans, which would enable them in gaining the greater

usage of court during the peak business time (Andersen et al., 2015). The projection of the

sales revenue is carried out under the new plans. In addition to this, the computations in the

Total sum of sales revenue generated:

Effect on sales revenue and cash inflow:

A tabular representation is stated below that assess the effect created on the cash flow

and sales revenue depending upon the periodic sales:

The above stated table evidently provides that the sales revenue that is generated by

the HLW has subsequently increased by $287,332 given the circumstances that they

commence the application of new plans, which would enable them in gaining the greater

usage of court during the peak business time (Andersen et al., 2015). The projection of the

sales revenue is carried out under the new plans. In addition to this, the computations in the

11MANAGEMENT ACCOUNTING

above stated table provides that usage of new plans would enable the club in generating

greater amount of revenue from the sales during the month of October.

Answer to Requirement 3:

One of the important aspects of the new plan is to understand the sales revenue that is

generated is higher under the new plan than compare to the previous plans (Kang, 2015).

There are large number of reasons that is required to be taken into the considerations at the

time of implementing in the new plan (Datar & Rajan, 2016). The assumptions have been

stated below and provides an appropriate justification of the analysis that has been made;

a. As it is understood from the current fees of membership, the revenue that would be

derived from the structure of new fees will be higher than the previous plans.

However, there are assumptions that there might be a loss of members on the

application of new plan (Horngren et al., 2016). The loss is anticipated in the areas of

student as they are not self-dependent and they may not be able to afford greater

amount of revenue from the renewal of the membership under the improved fees

structure.

b. With the application of the new plans, the management is better able to assemble the

fees for the beginning period of two or three months as this would enable them in

reducing the cost of revenue collection (Tang et al., 2015). Additionally this would

also facilitated the members in preparing the records of revenue that would be

generated from the new plans. Therefore, it is obligatory for the managers in taking

into the account the cost that is involved in the process of assessment.

c. Within the tenure of six months, the management expects that the they would miss out

some of the members (Johnson, 2014). As a result of this the managers are required to

implement the new plans or else they might fail to attain the expected revenue.

above stated table provides that usage of new plans would enable the club in generating

greater amount of revenue from the sales during the month of October.

Answer to Requirement 3:

One of the important aspects of the new plan is to understand the sales revenue that is

generated is higher under the new plan than compare to the previous plans (Kang, 2015).

There are large number of reasons that is required to be taken into the considerations at the

time of implementing in the new plan (Datar & Rajan, 2016). The assumptions have been

stated below and provides an appropriate justification of the analysis that has been made;

a. As it is understood from the current fees of membership, the revenue that would be

derived from the structure of new fees will be higher than the previous plans.

However, there are assumptions that there might be a loss of members on the

application of new plan (Horngren et al., 2016). The loss is anticipated in the areas of

student as they are not self-dependent and they may not be able to afford greater

amount of revenue from the renewal of the membership under the improved fees

structure.

b. With the application of the new plans, the management is better able to assemble the

fees for the beginning period of two or three months as this would enable them in

reducing the cost of revenue collection (Tang et al., 2015). Additionally this would

also facilitated the members in preparing the records of revenue that would be

generated from the new plans. Therefore, it is obligatory for the managers in taking

into the account the cost that is involved in the process of assessment.

c. Within the tenure of six months, the management expects that the they would miss out

some of the members (Johnson, 2014). As a result of this the managers are required to

implement the new plans or else they might fail to attain the expected revenue.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

12MANAGEMENT ACCOUNTING

d. The club is also required to perform the special campaign for promoting the new

plans. The cost that is incurred in the promotional strategies must be included in the

determination of the net income together with the cash flow that is generated on

applying the new plans (Gopalakrishnan et al., 2015).

Conclusion:

On arriving at the conclusion, it is noteworthy to denote that the activity method of

costing is regarded as the beneficial method of determination of cost. There are several

noteworthy assumptions has been considered in this report and the same has been duly

complied with the necessary information. The report has provided sufficient understanding

that the activity method of costing is an important step forward in determining the actual cost

of product and decision-making. Therefore, the report has immensely contributed by stating

that the activity based costing is helpful for the business owners in better understating of the

business situations and taking necessary corrective actions for improving the operational

functions.

d. The club is also required to perform the special campaign for promoting the new

plans. The cost that is incurred in the promotional strategies must be included in the

determination of the net income together with the cash flow that is generated on

applying the new plans (Gopalakrishnan et al., 2015).

Conclusion:

On arriving at the conclusion, it is noteworthy to denote that the activity method of

costing is regarded as the beneficial method of determination of cost. There are several

noteworthy assumptions has been considered in this report and the same has been duly

complied with the necessary information. The report has provided sufficient understanding

that the activity method of costing is an important step forward in determining the actual cost

of product and decision-making. Therefore, the report has immensely contributed by stating

that the activity based costing is helpful for the business owners in better understating of the

business situations and taking necessary corrective actions for improving the operational

functions.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13MANAGEMENT ACCOUNTING

Reference List:

Andersen, M. L., Zuber, J. M., & Hill, B. D. (2015). Moral foundations theory: An

exploratory study with accounting and other business students. Journal of Business

Ethics, 132(3), 525-538.

Clinton, B. D., & England, B. (2016). Principles of healthy managerial costing: a principles-

based approach to cost modeling would enhance the state of management accounting

and elevate its role in providing decision-support information. Strategic

Finance, 98(3), 40-46.

Cooper, R. (2017). Supply chain development for the lean enterprise: interorganizational cost

management. Routledge.

Datar, S. M., & Rajan, M. V. (2016). ACCT20053 Issues in Management Accounting:

ACCT20076 Foundations of Management Accounting. Pearson Education Limited.

Gopalakrishnan, M., Libby, T., Samuels, J. A., & Swenson, D. (2015). The effect of cost goal

specificity and new product development process on cost reduction

performance. Accounting, Organizations and Society, 42, 1-11.

Horngren, C. T., Datar, S. M., Rajan, M. V., Wynder, M. B., & Maguire, W. A. A.

(2016). Cost Management Systems ACCT2013, ACG25. Pearson Australia [for the]

University of South Australia.

Johnson, P. F. (2014). Purchasing and supply management. McGraw-Hill Higher Education.

Kang, M. (2015). Activity-based Costing Research on Enterprise Logistics Cost

Management. Business and Management Research, 4(2), 18.

Reference List:

Andersen, M. L., Zuber, J. M., & Hill, B. D. (2015). Moral foundations theory: An

exploratory study with accounting and other business students. Journal of Business

Ethics, 132(3), 525-538.

Clinton, B. D., & England, B. (2016). Principles of healthy managerial costing: a principles-

based approach to cost modeling would enhance the state of management accounting

and elevate its role in providing decision-support information. Strategic

Finance, 98(3), 40-46.

Cooper, R. (2017). Supply chain development for the lean enterprise: interorganizational cost

management. Routledge.

Datar, S. M., & Rajan, M. V. (2016). ACCT20053 Issues in Management Accounting:

ACCT20076 Foundations of Management Accounting. Pearson Education Limited.

Gopalakrishnan, M., Libby, T., Samuels, J. A., & Swenson, D. (2015). The effect of cost goal

specificity and new product development process on cost reduction

performance. Accounting, Organizations and Society, 42, 1-11.

Horngren, C. T., Datar, S. M., Rajan, M. V., Wynder, M. B., & Maguire, W. A. A.

(2016). Cost Management Systems ACCT2013, ACG25. Pearson Australia [for the]

University of South Australia.

Johnson, P. F. (2014). Purchasing and supply management. McGraw-Hill Higher Education.

Kang, M. (2015). Activity-based Costing Research on Enterprise Logistics Cost

Management. Business and Management Research, 4(2), 18.

14MANAGEMENT ACCOUNTING

Klychova, G. S., Faskhutdinova, М. S., & Sadrieva, E. R. (2014). Budget efficiency for cost

control purposes in management accounting system. Mediterranean journal of social

sciences, 5(24), 79.

Lanen, W. (2016). Fundamentals of cost accounting. McGraw-Hill Higher Education.

Malmi, T. (2016). Managerialist studies in management accounting: 1990–

2014. Management Accounting Research, 31, 31-44.

Mohanty, S.C., (2014). Relevance and Utility of Cost and Management Accounting in the

Present Socio-Economic Scenario. The MA Journal, 49(1), pp.12-17.

Morden, T. (2017). Principles of management. Routledge.

Otley, D. (2016). The contingency theory of management accounting and control: 1980–

2014. Management accounting research, 31, 45-62.

Renz, D. O. (2016). The Jossey-Bass handbook of nonprofit leadership and management.

John Wiley & Sons.

Schuster, P., (2015). Cost and Management Accounting. In Transfer Prices and Management

Accounting (pp. 1-4). Springer International Publishing.

Tang, J., Zhang, M., Tang, H., & Chen, Y. (2015, April). Research on Cost Management of

Construction Project Based on Activity-based Costing. In 2nd International

Conference on Civil, Materials and Environmental Sciences. Atlantis Press.

Zeff, S. A. (2016). Forging accounting principles in five countries: A history and an analysis

of trends. Routledge.

Klychova, G. S., Faskhutdinova, М. S., & Sadrieva, E. R. (2014). Budget efficiency for cost

control purposes in management accounting system. Mediterranean journal of social

sciences, 5(24), 79.

Lanen, W. (2016). Fundamentals of cost accounting. McGraw-Hill Higher Education.

Malmi, T. (2016). Managerialist studies in management accounting: 1990–

2014. Management Accounting Research, 31, 31-44.

Mohanty, S.C., (2014). Relevance and Utility of Cost and Management Accounting in the

Present Socio-Economic Scenario. The MA Journal, 49(1), pp.12-17.

Morden, T. (2017). Principles of management. Routledge.

Otley, D. (2016). The contingency theory of management accounting and control: 1980–

2014. Management accounting research, 31, 45-62.

Renz, D. O. (2016). The Jossey-Bass handbook of nonprofit leadership and management.

John Wiley & Sons.

Schuster, P., (2015). Cost and Management Accounting. In Transfer Prices and Management

Accounting (pp. 1-4). Springer International Publishing.

Tang, J., Zhang, M., Tang, H., & Chen, Y. (2015, April). Research on Cost Management of

Construction Project Based on Activity-based Costing. In 2nd International

Conference on Civil, Materials and Environmental Sciences. Atlantis Press.

Zeff, S. A. (2016). Forging accounting principles in five countries: A history and an analysis

of trends. Routledge.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.