Financial Resources and Decisions: A Comprehensive Business Report

VerifiedAdded on 2020/01/15

|16

|5051

|392

Report

AI Summary

This report comprehensively analyzes financial resource management and decision-making within a business context. It begins with the preparation of a cash budget for Perry Barr Window Product, including surplus/deficit analysis, and extends to profit determination through selling price calculations for Fine Food Ltd. The report then applies investment appraisal techniques like Net Present Value (NPV) and payback period to evaluate investment projects, followed by a critical evaluation and a report to the Managing Director. It also explains the purpose and formats of financial statements, assesses information needs of various users, and includes a comparative financial ratio analysis of a Hotel and a Beauty Salon. Finally, the report explores finance sources, their implications, costs, and impact on financial statements, culminating in financial planning considerations. The report uses tables to present financial data and calculations, and provides recommendations based on the financial analysis.

MANAGING

FINANCIAL

RESOURCES AND

DECISIONS

FINANCIAL

RESOURCES AND

DECISIONS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION......................................................................................................................1

TASK 1......................................................................................................................................1

a) Preparation of cash budget................................................................................................1

b) Surplus or Deficit of cash budget .....................................................................................1

TASK 2......................................................................................................................................2

a) Calculation of selling prices and determining business profits ........................................2

1) Selling price per unit.........................................................................................................2

2) Profits at sales of 800 units...............................................................................................2

b) Selling price and profit determination...............................................................................3

1) Selling price per unit.........................................................................................................3

2) Profit at additional production of 400 units......................................................................3

TASK 3......................................................................................................................................3

a) Application of investment appraisal techniques................................................................3

b) Critical evaluation of financial appraisal methods and report to MD...............................5

TASK 4......................................................................................................................................6

a) Explain the purpose of main financial statements and their formats in different..............6

organizations .........................................................................................................................6

b) Assessing the information need of different users of the financial statements.................6

c) Calculation, comparison and analysing the financial ratio of Hotel and Beauty Salon...7

TASK 5......................................................................................................................................8

a) Finance sources, implication, cost and impact on financial statements............................8

1) Sources of finance.............................................................................................................8

2) Implication of financial sources........................................................................................8

3) Cost of financial sources...................................................................................................9

4) Impact on financial statements..........................................................................................9

5) Financial planning...........................................................................................................10

CONCLUSION .......................................................................................................................10

REFERENCES.........................................................................................................................11

Books and Journals .............................................................................................................11

INTRODUCTION......................................................................................................................1

TASK 1......................................................................................................................................1

a) Preparation of cash budget................................................................................................1

b) Surplus or Deficit of cash budget .....................................................................................1

TASK 2......................................................................................................................................2

a) Calculation of selling prices and determining business profits ........................................2

1) Selling price per unit.........................................................................................................2

2) Profits at sales of 800 units...............................................................................................2

b) Selling price and profit determination...............................................................................3

1) Selling price per unit.........................................................................................................3

2) Profit at additional production of 400 units......................................................................3

TASK 3......................................................................................................................................3

a) Application of investment appraisal techniques................................................................3

b) Critical evaluation of financial appraisal methods and report to MD...............................5

TASK 4......................................................................................................................................6

a) Explain the purpose of main financial statements and their formats in different..............6

organizations .........................................................................................................................6

b) Assessing the information need of different users of the financial statements.................6

c) Calculation, comparison and analysing the financial ratio of Hotel and Beauty Salon...7

TASK 5......................................................................................................................................8

a) Finance sources, implication, cost and impact on financial statements............................8

1) Sources of finance.............................................................................................................8

2) Implication of financial sources........................................................................................8

3) Cost of financial sources...................................................................................................9

4) Impact on financial statements..........................................................................................9

5) Financial planning...........................................................................................................10

CONCLUSION .......................................................................................................................10

REFERENCES.........................................................................................................................11

Books and Journals .............................................................................................................11

Index of Tables

Table 1: Cash budget of Perry bar Window Product..................................................................1

Table 2: Total cost of the product..............................................................................................2

Table 3: Calculation of Profits at sales of 800 units...................................................................3

Table 4: Calculation of selling price per unit at additional production .....................................3

Table 5: Calculation of Profits at sales of 1200 units.................................................................3

Table 6: NPV of project A.........................................................................................................4

Table 7: NPV of project B..........................................................................................................4

Table 8: payback period of Project A.........................................................................................5

Table 9: payback period of Project B.........................................................................................5

Table 10: Computation of ratios for Hotel and Beauty Salon....................................................7

Table 1: Cash budget of Perry bar Window Product..................................................................1

Table 2: Total cost of the product..............................................................................................2

Table 3: Calculation of Profits at sales of 800 units...................................................................3

Table 4: Calculation of selling price per unit at additional production .....................................3

Table 5: Calculation of Profits at sales of 1200 units.................................................................3

Table 6: NPV of project A.........................................................................................................4

Table 7: NPV of project B..........................................................................................................4

Table 8: payback period of Project A.........................................................................................5

Table 9: payback period of Project B.........................................................................................5

Table 10: Computation of ratios for Hotel and Beauty Salon....................................................7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

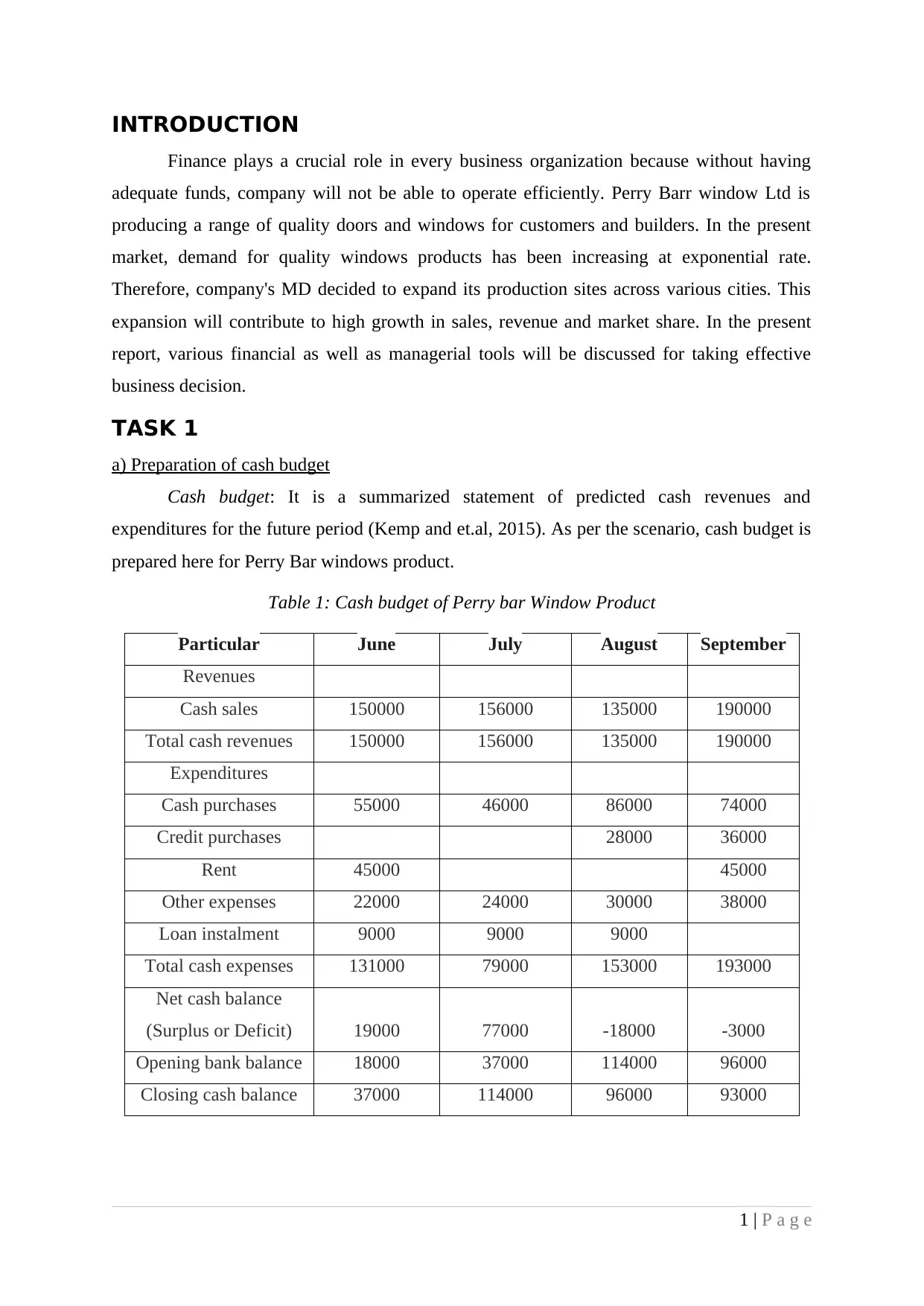

INTRODUCTION

Finance plays a crucial role in every business organization because without having

adequate funds, company will not be able to operate efficiently. Perry Barr window Ltd is

producing a range of quality doors and windows for customers and builders. In the present

market, demand for quality windows products has been increasing at exponential rate.

Therefore, company's MD decided to expand its production sites across various cities. This

expansion will contribute to high growth in sales, revenue and market share. In the present

report, various financial as well as managerial tools will be discussed for taking effective

business decision.

TASK 1

a) Preparation of cash budget

Cash budget: It is a summarized statement of predicted cash revenues and

expenditures for the future period (Kemp and et.al, 2015). As per the scenario, cash budget is

prepared here for Perry Bar windows product.

Table 1: Cash budget of Perry bar Window Product

Particular June July August September

Revenues

Cash sales 150000 156000 135000 190000

Total cash revenues 150000 156000 135000 190000

Expenditures

Cash purchases 55000 46000 86000 74000

Credit purchases 28000 36000

Rent 45000 45000

Other expenses 22000 24000 30000 38000

Loan instalment 9000 9000 9000

Total cash expenses 131000 79000 153000 193000

Net cash balance

(Surplus or Deficit) 19000 77000 -18000 -3000

Opening bank balance 18000 37000 114000 96000

Closing cash balance 37000 114000 96000 93000

1 | P a g e

Finance plays a crucial role in every business organization because without having

adequate funds, company will not be able to operate efficiently. Perry Barr window Ltd is

producing a range of quality doors and windows for customers and builders. In the present

market, demand for quality windows products has been increasing at exponential rate.

Therefore, company's MD decided to expand its production sites across various cities. This

expansion will contribute to high growth in sales, revenue and market share. In the present

report, various financial as well as managerial tools will be discussed for taking effective

business decision.

TASK 1

a) Preparation of cash budget

Cash budget: It is a summarized statement of predicted cash revenues and

expenditures for the future period (Kemp and et.al, 2015). As per the scenario, cash budget is

prepared here for Perry Bar windows product.

Table 1: Cash budget of Perry bar Window Product

Particular June July August September

Revenues

Cash sales 150000 156000 135000 190000

Total cash revenues 150000 156000 135000 190000

Expenditures

Cash purchases 55000 46000 86000 74000

Credit purchases 28000 36000

Rent 45000 45000

Other expenses 22000 24000 30000 38000

Loan instalment 9000 9000 9000

Total cash expenses 131000 79000 153000 193000

Net cash balance

(Surplus or Deficit) 19000 77000 -18000 -3000

Opening bank balance 18000 37000 114000 96000

Closing cash balance 37000 114000 96000 93000

1 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

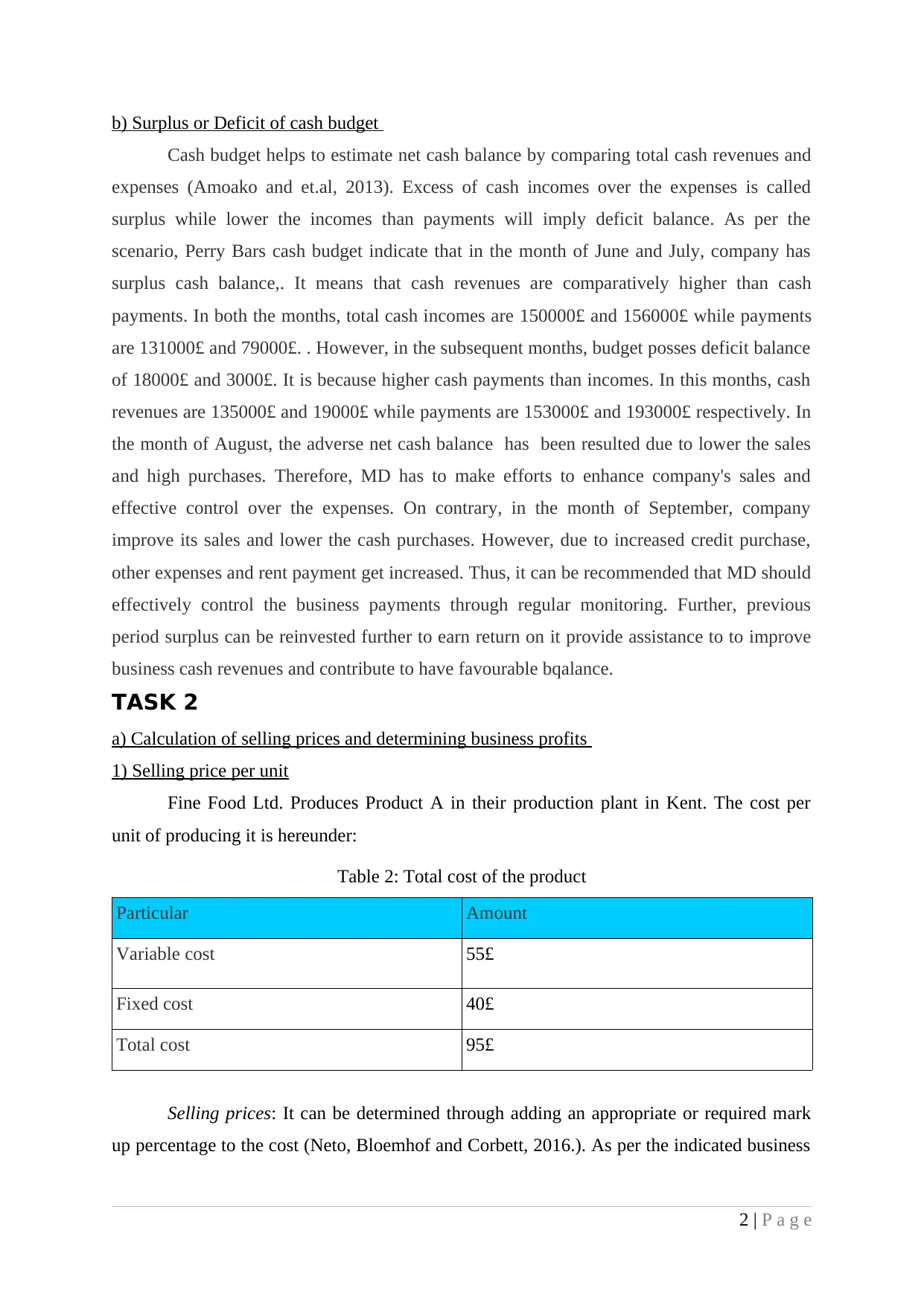

b) Surplus or Deficit of cash budget

Cash budget helps to estimate net cash balance by comparing total cash revenues and

expenses (Amoako and et.al, 2013). Excess of cash incomes over the expenses is called

surplus while lower the incomes than payments will imply deficit balance. As per the

scenario, Perry Bars cash budget indicate that in the month of June and July, company has

surplus cash balance,. It means that cash revenues are comparatively higher than cash

payments. In both the months, total cash incomes are 150000£ and 156000£ while payments

are 131000£ and 79000£. . However, in the subsequent months, budget posses deficit balance

of 18000£ and 3000£. It is because higher cash payments than incomes. In this months, cash

revenues are 135000£ and 19000£ while payments are 153000£ and 193000£ respectively. In

the month of August, the adverse net cash balance has been resulted due to lower the sales

and high purchases. Therefore, MD has to make efforts to enhance company's sales and

effective control over the expenses. On contrary, in the month of September, company

improve its sales and lower the cash purchases. However, due to increased credit purchase,

other expenses and rent payment get increased. Thus, it can be recommended that MD should

effectively control the business payments through regular monitoring. Further, previous

period surplus can be reinvested further to earn return on it provide assistance to to improve

business cash revenues and contribute to have favourable bqalance.

TASK 2

a) Calculation of selling prices and determining business profits

1) Selling price per unit

Fine Food Ltd. Produces Product A in their production plant in Kent. The cost per

unit of producing it is hereunder:

Table 2: Total cost of the product

Particular Amount

Variable cost 55£

Fixed cost 40£

Total cost 95£

Selling prices: It can be determined through adding an appropriate or required mark

up percentage to the cost (Neto, Bloemhof and Corbett, 2016.). As per the indicated business

2 | P a g e

Cash budget helps to estimate net cash balance by comparing total cash revenues and

expenses (Amoako and et.al, 2013). Excess of cash incomes over the expenses is called

surplus while lower the incomes than payments will imply deficit balance. As per the

scenario, Perry Bars cash budget indicate that in the month of June and July, company has

surplus cash balance,. It means that cash revenues are comparatively higher than cash

payments. In both the months, total cash incomes are 150000£ and 156000£ while payments

are 131000£ and 79000£. . However, in the subsequent months, budget posses deficit balance

of 18000£ and 3000£. It is because higher cash payments than incomes. In this months, cash

revenues are 135000£ and 19000£ while payments are 153000£ and 193000£ respectively. In

the month of August, the adverse net cash balance has been resulted due to lower the sales

and high purchases. Therefore, MD has to make efforts to enhance company's sales and

effective control over the expenses. On contrary, in the month of September, company

improve its sales and lower the cash purchases. However, due to increased credit purchase,

other expenses and rent payment get increased. Thus, it can be recommended that MD should

effectively control the business payments through regular monitoring. Further, previous

period surplus can be reinvested further to earn return on it provide assistance to to improve

business cash revenues and contribute to have favourable bqalance.

TASK 2

a) Calculation of selling prices and determining business profits

1) Selling price per unit

Fine Food Ltd. Produces Product A in their production plant in Kent. The cost per

unit of producing it is hereunder:

Table 2: Total cost of the product

Particular Amount

Variable cost 55£

Fixed cost 40£

Total cost 95£

Selling prices: It can be determined through adding an appropriate or required mark

up percentage to the cost (Neto, Bloemhof and Corbett, 2016.). As per the indicated business

2 | P a g e

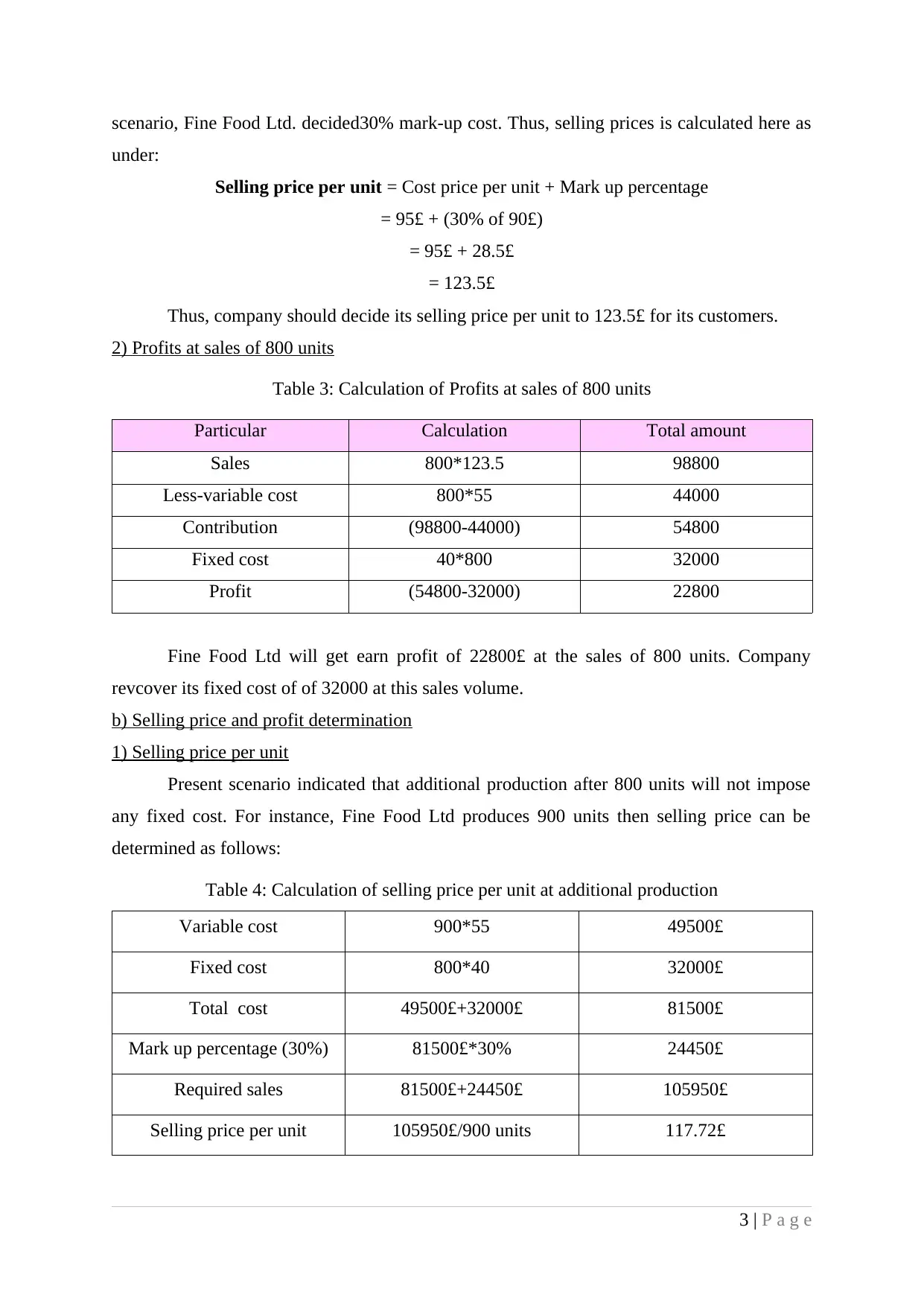

scenario, Fine Food Ltd. decided30% mark-up cost. Thus, selling prices is calculated here as

under:

Selling price per unit = Cost price per unit + Mark up percentage

= 95£ + (30% of 90£)

= 95£ + 28.5£

= 123.5£

Thus, company should decide its selling price per unit to 123.5£ for its customers.

2) Profits at sales of 800 units

Table 3: Calculation of Profits at sales of 800 units

Particular Calculation Total amount

Sales 800*123.5 98800

Less-variable cost 800*55 44000

Contribution (98800-44000) 54800

Fixed cost 40*800 32000

Profit (54800-32000) 22800

Fine Food Ltd will get earn profit of 22800£ at the sales of 800 units. Company

revcover its fixed cost of of 32000 at this sales volume.

b) Selling price and profit determination

1) Selling price per unit

Present scenario indicated that additional production after 800 units will not impose

any fixed cost. For instance, Fine Food Ltd produces 900 units then selling price can be

determined as follows:

Table 4: Calculation of selling price per unit at additional production

Variable cost 900*55 49500£

Fixed cost 800*40 32000£

Total cost 49500£+32000£ 81500£

Mark up percentage (30%) 81500£*30% 24450£

Required sales 81500£+24450£ 105950£

Selling price per unit 105950£/900 units 117.72£

3 | P a g e

under:

Selling price per unit = Cost price per unit + Mark up percentage

= 95£ + (30% of 90£)

= 95£ + 28.5£

= 123.5£

Thus, company should decide its selling price per unit to 123.5£ for its customers.

2) Profits at sales of 800 units

Table 3: Calculation of Profits at sales of 800 units

Particular Calculation Total amount

Sales 800*123.5 98800

Less-variable cost 800*55 44000

Contribution (98800-44000) 54800

Fixed cost 40*800 32000

Profit (54800-32000) 22800

Fine Food Ltd will get earn profit of 22800£ at the sales of 800 units. Company

revcover its fixed cost of of 32000 at this sales volume.

b) Selling price and profit determination

1) Selling price per unit

Present scenario indicated that additional production after 800 units will not impose

any fixed cost. For instance, Fine Food Ltd produces 900 units then selling price can be

determined as follows:

Table 4: Calculation of selling price per unit at additional production

Variable cost 900*55 49500£

Fixed cost 800*40 32000£

Total cost 49500£+32000£ 81500£

Mark up percentage (30%) 81500£*30% 24450£

Required sales 81500£+24450£ 105950£

Selling price per unit 105950£/900 units 117.72£

3 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

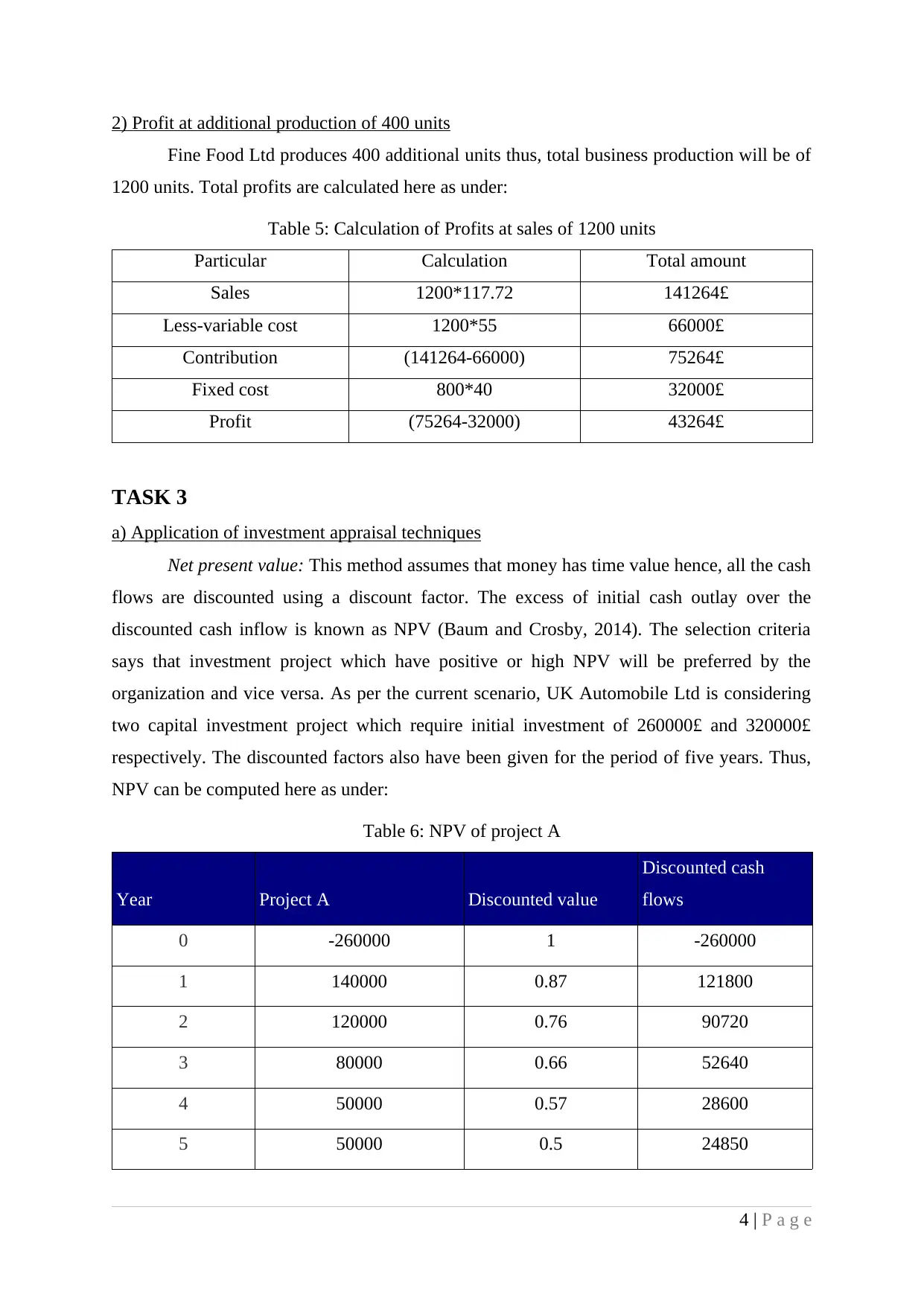

2) Profit at additional production of 400 units

Fine Food Ltd produces 400 additional units thus, total business production will be of

1200 units. Total profits are calculated here as under:

Table 5: Calculation of Profits at sales of 1200 units

Particular Calculation Total amount

Sales 1200*117.72 141264£

Less-variable cost 1200*55 66000£

Contribution (141264-66000) 75264£

Fixed cost 800*40 32000£

Profit (75264-32000) 43264£

TASK 3

a) Application of investment appraisal techniques

Net present value: This method assumes that money has time value hence, all the cash

flows are discounted using a discount factor. The excess of initial cash outlay over the

discounted cash inflow is known as NPV (Baum and Crosby, 2014). The selection criteria

says that investment project which have positive or high NPV will be preferred by the

organization and vice versa. As per the current scenario, UK Automobile Ltd is considering

two capital investment project which require initial investment of 260000£ and 320000£

respectively. The discounted factors also have been given for the period of five years. Thus,

NPV can be computed here as under:

Table 6: NPV of project A

Year Project A Discounted value

Discounted cash

flows

0 -260000 1 -260000

1 140000 0.87 121800

2 120000 0.76 90720

3 80000 0.66 52640

4 50000 0.57 28600

5 50000 0.5 24850

4 | P a g e

Fine Food Ltd produces 400 additional units thus, total business production will be of

1200 units. Total profits are calculated here as under:

Table 5: Calculation of Profits at sales of 1200 units

Particular Calculation Total amount

Sales 1200*117.72 141264£

Less-variable cost 1200*55 66000£

Contribution (141264-66000) 75264£

Fixed cost 800*40 32000£

Profit (75264-32000) 43264£

TASK 3

a) Application of investment appraisal techniques

Net present value: This method assumes that money has time value hence, all the cash

flows are discounted using a discount factor. The excess of initial cash outlay over the

discounted cash inflow is known as NPV (Baum and Crosby, 2014). The selection criteria

says that investment project which have positive or high NPV will be preferred by the

organization and vice versa. As per the current scenario, UK Automobile Ltd is considering

two capital investment project which require initial investment of 260000£ and 320000£

respectively. The discounted factors also have been given for the period of five years. Thus,

NPV can be computed here as under:

Table 6: NPV of project A

Year Project A Discounted value

Discounted cash

flows

0 -260000 1 -260000

1 140000 0.87 121800

2 120000 0.76 90720

3 80000 0.66 52640

4 50000 0.57 28600

5 50000 0.5 24850

4 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

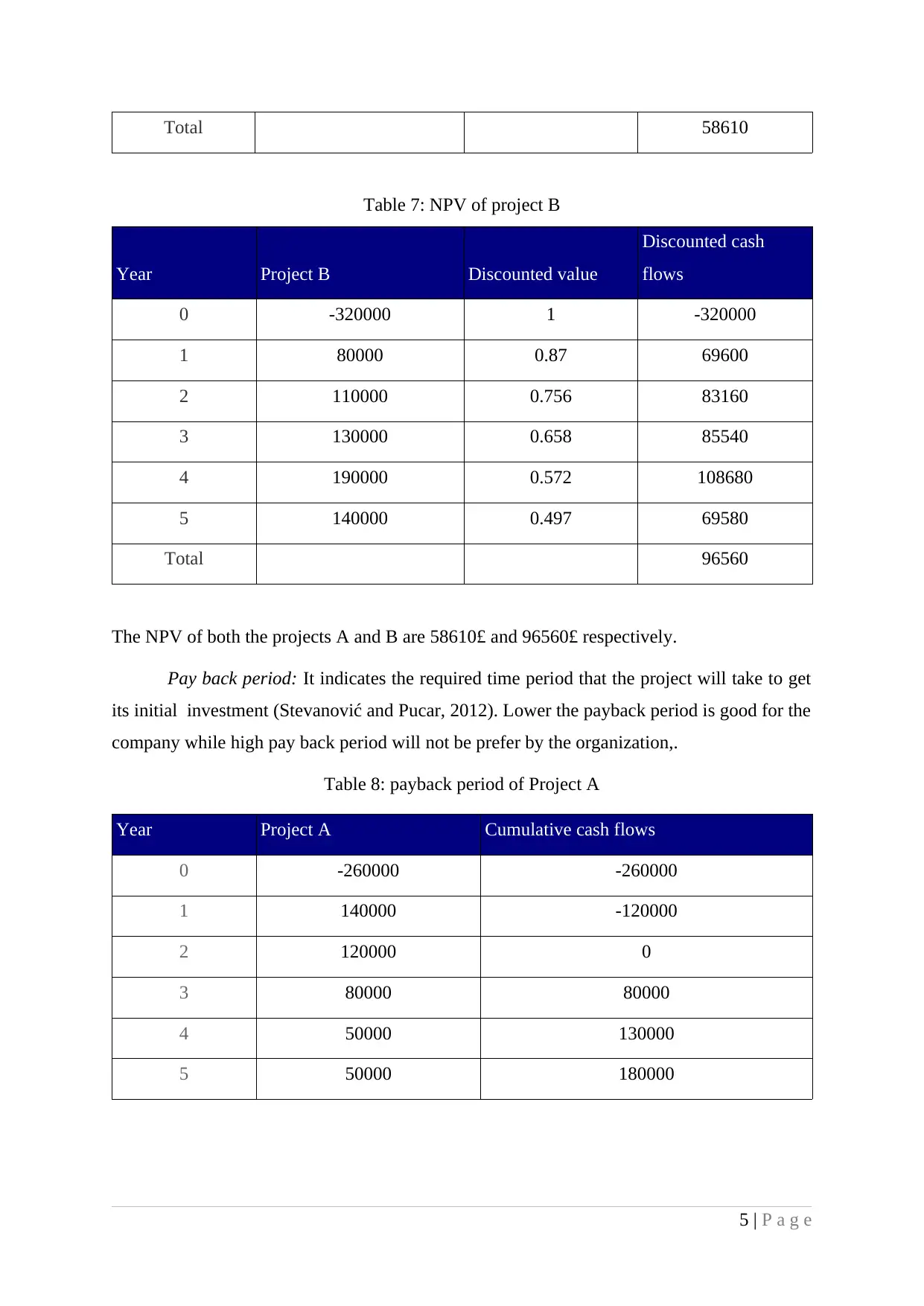

Total 58610

Table 7: NPV of project B

Year Project B Discounted value

Discounted cash

flows

0 -320000 1 -320000

1 80000 0.87 69600

2 110000 0.756 83160

3 130000 0.658 85540

4 190000 0.572 108680

5 140000 0.497 69580

Total 96560

The NPV of both the projects A and B are 58610£ and 96560£ respectively.

Pay back period: It indicates the required time period that the project will take to get

its initial investment (Stevanović and Pucar, 2012). Lower the payback period is good for the

company while high pay back period will not be prefer by the organization,.

Table 8: payback period of Project A

Year Project A Cumulative cash flows

0 -260000 -260000

1 140000 -120000

2 120000 0

3 80000 80000

4 50000 130000

5 50000 180000

5 | P a g e

Table 7: NPV of project B

Year Project B Discounted value

Discounted cash

flows

0 -320000 1 -320000

1 80000 0.87 69600

2 110000 0.756 83160

3 130000 0.658 85540

4 190000 0.572 108680

5 140000 0.497 69580

Total 96560

The NPV of both the projects A and B are 58610£ and 96560£ respectively.

Pay back period: It indicates the required time period that the project will take to get

its initial investment (Stevanović and Pucar, 2012). Lower the payback period is good for the

company while high pay back period will not be prefer by the organization,.

Table 8: payback period of Project A

Year Project A Cumulative cash flows

0 -260000 -260000

1 140000 -120000

2 120000 0

3 80000 80000

4 50000 130000

5 50000 180000

5 | P a g e

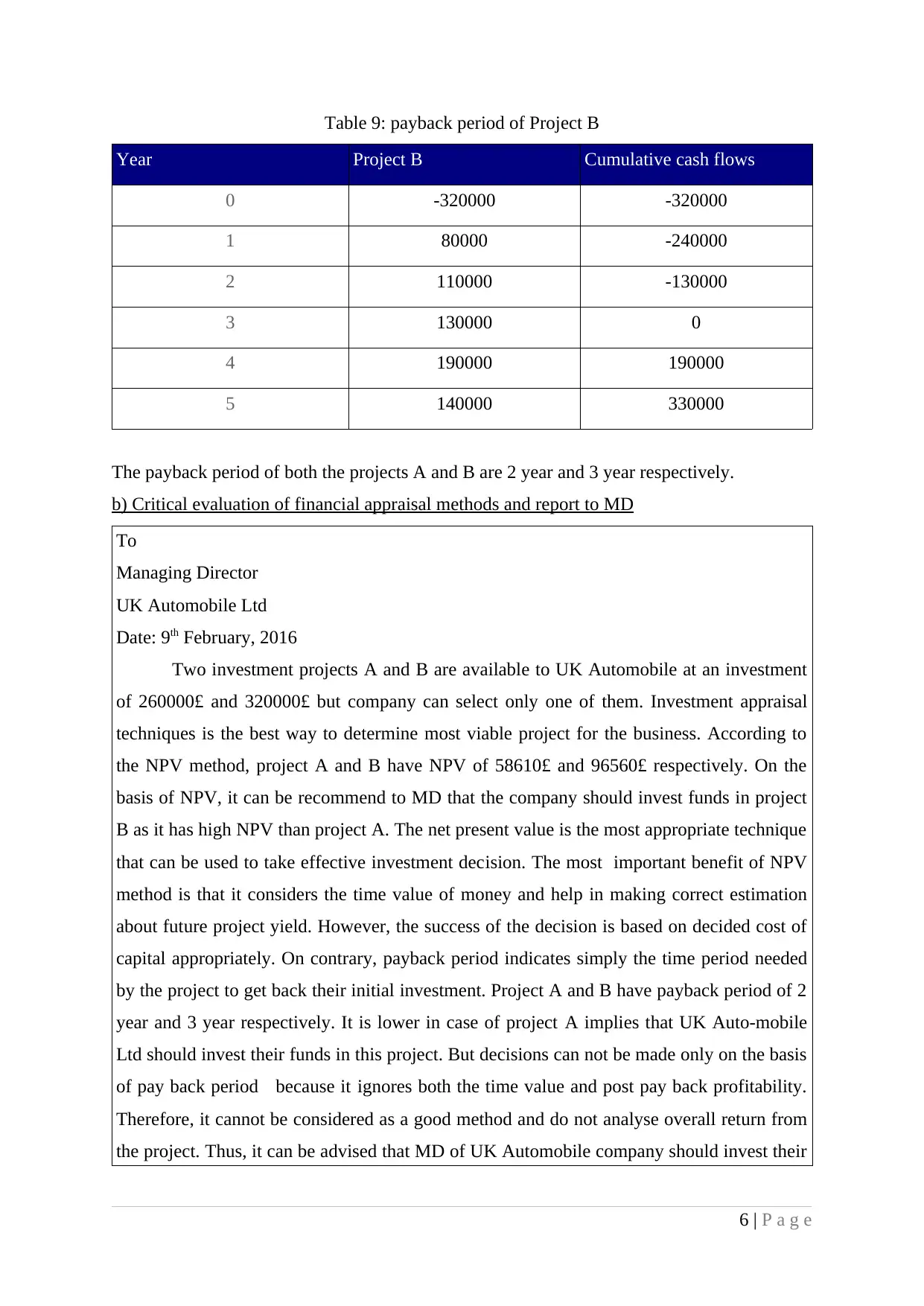

Table 9: payback period of Project B

Year Project B Cumulative cash flows

0 -320000 -320000

1 80000 -240000

2 110000 -130000

3 130000 0

4 190000 190000

5 140000 330000

The payback period of both the projects A and B are 2 year and 3 year respectively.

b) Critical evaluation of financial appraisal methods and report to MD

To

Managing Director

UK Automobile Ltd

Date: 9th February, 2016

Two investment projects A and B are available to UK Automobile at an investment

of 260000£ and 320000£ but company can select only one of them. Investment appraisal

techniques is the best way to determine most viable project for the business. According to

the NPV method, project A and B have NPV of 58610£ and 96560£ respectively. On the

basis of NPV, it can be recommend to MD that the company should invest funds in project

B as it has high NPV than project A. The net present value is the most appropriate technique

that can be used to take effective investment decision. The most important benefit of NPV

method is that it considers the time value of money and help in making correct estimation

about future project yield. However, the success of the decision is based on decided cost of

capital appropriately. On contrary, payback period indicates simply the time period needed

by the project to get back their initial investment. Project A and B have payback period of 2

year and 3 year respectively. It is lower in case of project A implies that UK Auto-mobile

Ltd should invest their funds in this project. But decisions can not be made only on the basis

of pay back period because it ignores both the time value and post pay back profitability.

Therefore, it cannot be considered as a good method and do not analyse overall return from

the project. Thus, it can be advised that MD of UK Automobile company should invest their

6 | P a g e

Year Project B Cumulative cash flows

0 -320000 -320000

1 80000 -240000

2 110000 -130000

3 130000 0

4 190000 190000

5 140000 330000

The payback period of both the projects A and B are 2 year and 3 year respectively.

b) Critical evaluation of financial appraisal methods and report to MD

To

Managing Director

UK Automobile Ltd

Date: 9th February, 2016

Two investment projects A and B are available to UK Automobile at an investment

of 260000£ and 320000£ but company can select only one of them. Investment appraisal

techniques is the best way to determine most viable project for the business. According to

the NPV method, project A and B have NPV of 58610£ and 96560£ respectively. On the

basis of NPV, it can be recommend to MD that the company should invest funds in project

B as it has high NPV than project A. The net present value is the most appropriate technique

that can be used to take effective investment decision. The most important benefit of NPV

method is that it considers the time value of money and help in making correct estimation

about future project yield. However, the success of the decision is based on decided cost of

capital appropriately. On contrary, payback period indicates simply the time period needed

by the project to get back their initial investment. Project A and B have payback period of 2

year and 3 year respectively. It is lower in case of project A implies that UK Auto-mobile

Ltd should invest their funds in this project. But decisions can not be made only on the basis

of pay back period because it ignores both the time value and post pay back profitability.

Therefore, it cannot be considered as a good method and do not analyse overall return from

the project. Thus, it can be advised that MD of UK Automobile company should invest their

6 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

funds in project B because it will be more profitable for the company.

TASK 4

a) Explain the purpose of main financial statements and their formats in different

Organizations

Financial accounting is the process of recording all the business transaction in an

appropriate manner. It consists of preparing necessary statements to determine business

performance. Profitability account and balance sheet are two main statements which have

been prepared by every organization.

Profitability statement: Each and every enterprise do operating function with the aim

of getting maximum profits. Businesses earn incomes through selling its products into the

market and incurred necessary expenditures. Therefore, it became necessary for them to

determine their operational performance in terms of profits and losses as well. They prepare

profit and loss account to determine their operational results. According to the statement,

excess of incomes over the expenses will indicate profits and vice versa (Healy and Palepu,

2012). Small and medium sized enterprises such as sole trader prepare this statement

according to their convenience whereas large organization such as company prepares this

statement as per the legal requirement. They prepare the statement according to the

company’s act.

Financial position statement: Along with the profitability statement, organization also

prepare balance sheet. It is a summarized statement of companies’ assets and liabilities. The

main purpose of preparing this statement is to determine the financial position of the business

(Ormiston and Fraser, 2013). Fixed assets comprise of plant and machinery and land and

building while current assets include cash, inventory, debtors and accounts receivable. On

contrary, liability involves both the short term and long term liabilities such as overdraft,

debentures, bank loan and creditors. Moreover, the statement also helps to determine the

proportion of owners' share on total assets. Large scale organization such as companies

prepare balance sheet in the prescribed format by the company act (Fuchs and Colyvas,

2013). It is because of the legal obligations to publish their audited financial statements.

However, other SMEs do not require to follow any specific format they can prepare it as per

their convenience.

7 | P a g e

TASK 4

a) Explain the purpose of main financial statements and their formats in different

Organizations

Financial accounting is the process of recording all the business transaction in an

appropriate manner. It consists of preparing necessary statements to determine business

performance. Profitability account and balance sheet are two main statements which have

been prepared by every organization.

Profitability statement: Each and every enterprise do operating function with the aim

of getting maximum profits. Businesses earn incomes through selling its products into the

market and incurred necessary expenditures. Therefore, it became necessary for them to

determine their operational performance in terms of profits and losses as well. They prepare

profit and loss account to determine their operational results. According to the statement,

excess of incomes over the expenses will indicate profits and vice versa (Healy and Palepu,

2012). Small and medium sized enterprises such as sole trader prepare this statement

according to their convenience whereas large organization such as company prepares this

statement as per the legal requirement. They prepare the statement according to the

company’s act.

Financial position statement: Along with the profitability statement, organization also

prepare balance sheet. It is a summarized statement of companies’ assets and liabilities. The

main purpose of preparing this statement is to determine the financial position of the business

(Ormiston and Fraser, 2013). Fixed assets comprise of plant and machinery and land and

building while current assets include cash, inventory, debtors and accounts receivable. On

contrary, liability involves both the short term and long term liabilities such as overdraft,

debentures, bank loan and creditors. Moreover, the statement also helps to determine the

proportion of owners' share on total assets. Large scale organization such as companies

prepare balance sheet in the prescribed format by the company act (Fuchs and Colyvas,

2013). It is because of the legal obligations to publish their audited financial statements.

However, other SMEs do not require to follow any specific format they can prepare it as per

their convenience.

7 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

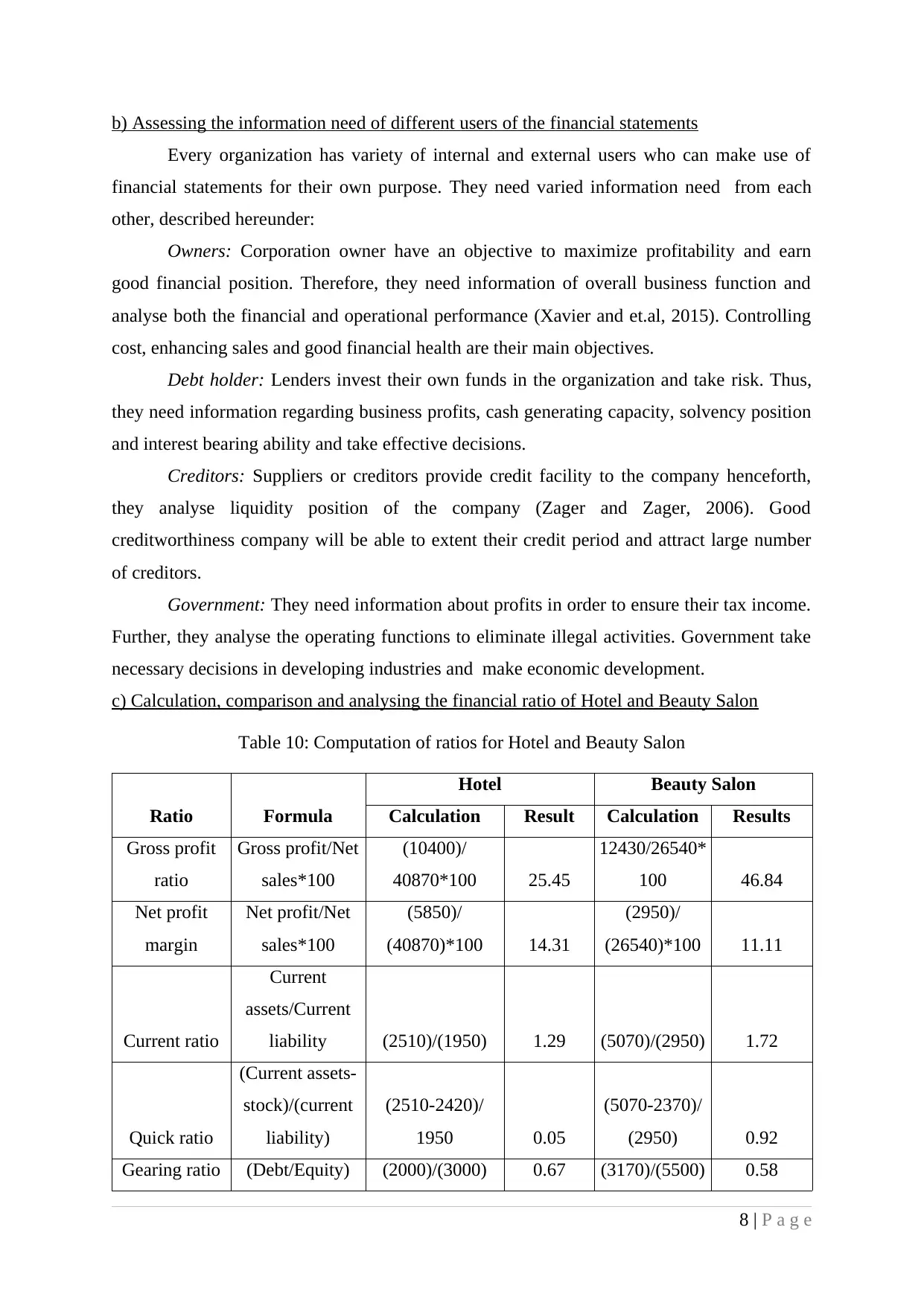

b) Assessing the information need of different users of the financial statements

Every organization has variety of internal and external users who can make use of

financial statements for their own purpose. They need varied information need from each

other, described hereunder:

Owners: Corporation owner have an objective to maximize profitability and earn

good financial position. Therefore, they need information of overall business function and

analyse both the financial and operational performance (Xavier and et.al, 2015). Controlling

cost, enhancing sales and good financial health are their main objectives.

Debt holder: Lenders invest their own funds in the organization and take risk. Thus,

they need information regarding business profits, cash generating capacity, solvency position

and interest bearing ability and take effective decisions.

Creditors: Suppliers or creditors provide credit facility to the company henceforth,

they analyse liquidity position of the company (Zager and Zager, 2006). Good

creditworthiness company will be able to extent their credit period and attract large number

of creditors.

Government: They need information about profits in order to ensure their tax income.

Further, they analyse the operating functions to eliminate illegal activities. Government take

necessary decisions in developing industries and make economic development.

c) Calculation, comparison and analysing the financial ratio of Hotel and Beauty Salon

Table 10: Computation of ratios for Hotel and Beauty Salon

Ratio Formula

Hotel Beauty Salon

Calculation Result Calculation Results

Gross profit

ratio

Gross profit/Net

sales*100

(10400)/

40870*100 25.45

12430/26540*

100 46.84

Net profit

margin

Net profit/Net

sales*100

(5850)/

(40870)*100 14.31

(2950)/

(26540)*100 11.11

Current ratio

Current

assets/Current

liability (2510)/(1950) 1.29 (5070)/(2950) 1.72

Quick ratio

(Current assets-

stock)/(current

liability)

(2510-2420)/

1950 0.05

(5070-2370)/

(2950) 0.92

Gearing ratio (Debt/Equity) (2000)/(3000) 0.67 (3170)/(5500) 0.58

8 | P a g e

Every organization has variety of internal and external users who can make use of

financial statements for their own purpose. They need varied information need from each

other, described hereunder:

Owners: Corporation owner have an objective to maximize profitability and earn

good financial position. Therefore, they need information of overall business function and

analyse both the financial and operational performance (Xavier and et.al, 2015). Controlling

cost, enhancing sales and good financial health are their main objectives.

Debt holder: Lenders invest their own funds in the organization and take risk. Thus,

they need information regarding business profits, cash generating capacity, solvency position

and interest bearing ability and take effective decisions.

Creditors: Suppliers or creditors provide credit facility to the company henceforth,

they analyse liquidity position of the company (Zager and Zager, 2006). Good

creditworthiness company will be able to extent their credit period and attract large number

of creditors.

Government: They need information about profits in order to ensure their tax income.

Further, they analyse the operating functions to eliminate illegal activities. Government take

necessary decisions in developing industries and make economic development.

c) Calculation, comparison and analysing the financial ratio of Hotel and Beauty Salon

Table 10: Computation of ratios for Hotel and Beauty Salon

Ratio Formula

Hotel Beauty Salon

Calculation Result Calculation Results

Gross profit

ratio

Gross profit/Net

sales*100

(10400)/

40870*100 25.45

12430/26540*

100 46.84

Net profit

margin

Net profit/Net

sales*100

(5850)/

(40870)*100 14.31

(2950)/

(26540)*100 11.11

Current ratio

Current

assets/Current

liability (2510)/(1950) 1.29 (5070)/(2950) 1.72

Quick ratio

(Current assets-

stock)/(current

liability)

(2510-2420)/

1950 0.05

(5070-2370)/

(2950) 0.92

Gearing ratio (Debt/Equity) (2000)/(3000) 0.67 (3170)/(5500) 0.58

8 | P a g e

1) Gross profit margin: Hotel's gross profit ratio is 25.45% while Beauty Salon is earning

gross profit of 46.84%. It is higher in case of Beauty Salon indicate that it is performing well

compare to Hotel.

2) Net profit margin: Hotel and Beauty Salon's net profit ratio are 14.31% and 11.11%

respectively. The ratio shows that Hotel's operational performance is quite good as compared

to Beauty Salon. It may be because of high operating expenses of Beauty Salon.

3) Current ratio: It indicates a relationship between current assets and current liabilities. It is

higher in case of Beauty salon to 1.72 shows that it havergood liquid availability in the

business. Thus, Salon is able to discharge their short term liabilities effectively.

4) Quick ratio: Inventory is a very liquid asset that can be converted into cash very quickly.

Beauty Salon has high quick ratio as 0.92 while hotel have only 0.05. Therefore, it can be

said that Beauty Salon is comparatively more able to pay off their short term obligations.

5) Gearing ratio: Hotel's debt equity ratio is 0.67 greater than Beauty Salon 0.58. It is

because hotel is using high debts of 2000£ which impose high financial risk to the company.

TASK 5

a) Finance sources, implication, cost and impact on financial statements

1) Sources of finance

An organization can collect funds from various sources for expanding its operations,

it has been described below:

Internal sources: This kind of sources is available inside the corporations. Retained

profits, disposing off the company assets and cash squeezing operations are the internal

sources. Organization can use their undistributed profits for expansion purpose, called

retained earnings (Peirson and et.al, 2014). Further, unused assets can be resale in the market

to collect required funds. In addition to it, cash squeezing operation means business should

negotiate their payments and receive promptly from the debtors. By doing this, companies

will be able to have more cash availability and fulfil their financial need.

External sources: Bank borrowings, issuing share capital and overdraft are the

external sources. Bank provides loans for different time duration helps to accomplish

organizational financial need to a great extent(Khan, 2015). Further, company can issue

equity and preference shares and gather funds in the form of share capital. On contrary,

9 | P a g e

gross profit of 46.84%. It is higher in case of Beauty Salon indicate that it is performing well

compare to Hotel.

2) Net profit margin: Hotel and Beauty Salon's net profit ratio are 14.31% and 11.11%

respectively. The ratio shows that Hotel's operational performance is quite good as compared

to Beauty Salon. It may be because of high operating expenses of Beauty Salon.

3) Current ratio: It indicates a relationship between current assets and current liabilities. It is

higher in case of Beauty salon to 1.72 shows that it havergood liquid availability in the

business. Thus, Salon is able to discharge their short term liabilities effectively.

4) Quick ratio: Inventory is a very liquid asset that can be converted into cash very quickly.

Beauty Salon has high quick ratio as 0.92 while hotel have only 0.05. Therefore, it can be

said that Beauty Salon is comparatively more able to pay off their short term obligations.

5) Gearing ratio: Hotel's debt equity ratio is 0.67 greater than Beauty Salon 0.58. It is

because hotel is using high debts of 2000£ which impose high financial risk to the company.

TASK 5

a) Finance sources, implication, cost and impact on financial statements

1) Sources of finance

An organization can collect funds from various sources for expanding its operations,

it has been described below:

Internal sources: This kind of sources is available inside the corporations. Retained

profits, disposing off the company assets and cash squeezing operations are the internal

sources. Organization can use their undistributed profits for expansion purpose, called

retained earnings (Peirson and et.al, 2014). Further, unused assets can be resale in the market

to collect required funds. In addition to it, cash squeezing operation means business should

negotiate their payments and receive promptly from the debtors. By doing this, companies

will be able to have more cash availability and fulfil their financial need.

External sources: Bank borrowings, issuing share capital and overdraft are the

external sources. Bank provides loans for different time duration helps to accomplish

organizational financial need to a great extent(Khan, 2015). Further, company can issue

equity and preference shares and gather funds in the form of share capital. On contrary,

9 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.