Report on Accounting Standard and Regulations: Myer Holdings Limited

VerifiedAdded on 2020/02/24

|11

|1904

|49

Report

AI Summary

This report provides an analysis of Myer Holdings Limited's approach to accounting standards and regulations, with a specific focus on asset impairment in accordance with AASB 136. The report examines the evidence of impairment testing, outlining the process for determining asset impairment, and detailing the information required for this determination. It also discusses management's flexibility in determining impairment of assets. The analysis covers the calculation of recoverable amounts and value in use, the recognition of impairment losses, and the application of relevant accounting standards. The report concludes that Myer Holdings Limited adheres to AASB 136 in its asset impairment tests. The company measures value in use and recoverable value when asset impairment is indicated. Management demonstrates flexibility in determining impairment loss and conducting asset impairment tests.

Running head: ACCOUNTING STANDARD AND REGULATIONS

Accounting standard and regulations

Name of the University

Name of the student

Authors note

Accounting standard and regulations

Name of the University

Name of the student

Authors note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING STANDARD AND REGULATIONS

Executive summary:

The report discusses about media release of ASIC that would assist readers in providing clear

idea about concepts of impairment of assets and treatment of it by Myer holdings limited.

Moreover, report also demonstrate test of impairment in according with AASB 136.

Information required for determining impairment of assets, impairment evidence and

management flexibility in determining impairment of assets are also demonstrated in report.

Executive summary:

The report discusses about media release of ASIC that would assist readers in providing clear

idea about concepts of impairment of assets and treatment of it by Myer holdings limited.

Moreover, report also demonstrate test of impairment in according with AASB 136.

Information required for determining impairment of assets, impairment evidence and

management flexibility in determining impairment of assets are also demonstrated in report.

2ACCOUNTING STANDARD AND REGULATIONS

Table of Contents

Introduction:...............................................................................................................................3

Discussion:.................................................................................................................................4

a)Evidence of Impairment testing of assets of Myer Holdings limited.....................................4

b)Outlining process for determining asset impairment..............................................................5

c) Information is required in determining asset impairment......................................................6

d)Management flexibility in determining impairment of assets................................................7

Conclusion:................................................................................................................................8

Reference:..................................................................................................................................8

Table of Contents

Introduction:...............................................................................................................................3

Discussion:.................................................................................................................................4

a)Evidence of Impairment testing of assets of Myer Holdings limited.....................................4

b)Outlining process for determining asset impairment..............................................................5

c) Information is required in determining asset impairment......................................................6

d)Management flexibility in determining impairment of assets................................................7

Conclusion:................................................................................................................................8

Reference:..................................................................................................................................8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING STANDARD AND REGULATIONS

Introduction:

Australian securities and investment commission has asked companies to focus on

providing relevant information that are meaningful and useful to their users of financial

reports. It is required by auditor and directors to focus in accounting policy choice and assets

value. ASIC is of the view that most of companies make use of unrealistic assumptions for

testing values of assets and application of inappropriate approaches in areas of revenue

recognition. Risk criteria forms the basis of reviewing financial reports that helps in

determining compliance with accounting standards and Corporation act. For addressing

issues, ASIC features some of zones by declaring range of concentrations of public

organization and listed organizations. It is stated by commissioner of ASIC that chiefs and

evaluator as per past announcing periods should concentrate on decisions of bookkeeping

strategies and estimating benefits (Albu et al. 2014).

AASB 136 states that it is required by entity to conduct impairment test for assets that

will ensure that assets are not overvalued. Value of assets that can be compared to

recoverable sum and associated benefits are no involved in financial reports. Recoverable

value of assets for disposal and value in use is more than assets fair value less costs. Such

assets might involve goodwill and intangible assets. Any organization showing signs of

repairing assets should undertake impairment test (Oulasvirta 2014). Moreover, test can also

be undertaken for assets where they do not make any income such as cash generating unit.

There are internal and external sources of indication for carrying out assets impairment.

Introduction:

Australian securities and investment commission has asked companies to focus on

providing relevant information that are meaningful and useful to their users of financial

reports. It is required by auditor and directors to focus in accounting policy choice and assets

value. ASIC is of the view that most of companies make use of unrealistic assumptions for

testing values of assets and application of inappropriate approaches in areas of revenue

recognition. Risk criteria forms the basis of reviewing financial reports that helps in

determining compliance with accounting standards and Corporation act. For addressing

issues, ASIC features some of zones by declaring range of concentrations of public

organization and listed organizations. It is stated by commissioner of ASIC that chiefs and

evaluator as per past announcing periods should concentrate on decisions of bookkeeping

strategies and estimating benefits (Albu et al. 2014).

AASB 136 states that it is required by entity to conduct impairment test for assets that

will ensure that assets are not overvalued. Value of assets that can be compared to

recoverable sum and associated benefits are no involved in financial reports. Recoverable

value of assets for disposal and value in use is more than assets fair value less costs. Such

assets might involve goodwill and intangible assets. Any organization showing signs of

repairing assets should undertake impairment test (Oulasvirta 2014). Moreover, test can also

be undertaken for assets where they do not make any income such as cash generating unit.

There are internal and external sources of indication for carrying out assets impairment.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING STANDARD AND REGULATIONS

Discussion:

a)Evidence of Impairment testing of assets of Myer Holdings limited

Considering the case of Myer Holdings limited, it is not possible to recognize

goodwill from acquisition of business by separating cash generating unit. Therefore, it is

required for business to allocate goodwill.

Asset flow- It can be identified from the given data relating to flow of assets that they

are consistent or have increased by little amount. There is no evidence of impairment test and

it is not required to conduct test of impairment as evident by decreasing trend of stores.

Establishment of indication of impairment is difficult from the given data.

Asset base- There has not been much change in assets base of Myer holdings limited

and for the past few years, they have remained more or less same in value. Considering the

asset base for undertraining impairment, there is clear indication that assets are not required

to be impaired (Bond et al. 2016).

Turnover of assets- It can be ascertained from Myer holding ltd financial statements

that asset turnover ratio has ranged from 1.40 to 1.80. During the period under consideration,

there is no significant movement of asset turnover ratio. Therefore, impairment of test is not

indicated using this particular test.

Therefore, considering the above strategies, it is certainly not possible for undertaking

impairment. However, looking at the departmental store of company in Frankston, there are

some indications for impairment. Myer has planned for altering the colours of their

departmental stores for competing with Amazon. Changing system of storing products would

also be altered that will result in more free space (Preiato et al. 2014). All the aspects

Discussion:

a)Evidence of Impairment testing of assets of Myer Holdings limited

Considering the case of Myer Holdings limited, it is not possible to recognize

goodwill from acquisition of business by separating cash generating unit. Therefore, it is

required for business to allocate goodwill.

Asset flow- It can be identified from the given data relating to flow of assets that they

are consistent or have increased by little amount. There is no evidence of impairment test and

it is not required to conduct test of impairment as evident by decreasing trend of stores.

Establishment of indication of impairment is difficult from the given data.

Asset base- There has not been much change in assets base of Myer holdings limited

and for the past few years, they have remained more or less same in value. Considering the

asset base for undertraining impairment, there is clear indication that assets are not required

to be impaired (Bond et al. 2016).

Turnover of assets- It can be ascertained from Myer holding ltd financial statements

that asset turnover ratio has ranged from 1.40 to 1.80. During the period under consideration,

there is no significant movement of asset turnover ratio. Therefore, impairment of test is not

indicated using this particular test.

Therefore, considering the above strategies, it is certainly not possible for undertaking

impairment. However, looking at the departmental store of company in Frankston, there are

some indications for impairment. Myer has planned for altering the colours of their

departmental stores for competing with Amazon. Changing system of storing products would

also be altered that will result in more free space (Preiato et al. 2014). All the aspects

5ACCOUNTING STANDARD AND REGULATIONS

discussed above are considered as partial construction that qualifies determination of

impairment of assets according to AASB 136.

b)Outlining process for determining asset impairment

Calculation of recoverable amount of assets and value in use is done by Myer

holdings ltd for determining assets impairment test. Forecasting cash flow is done based on

model that is approved by management of organization. Extrapolation of cash flow for more

than five years is done using the terminal growth rate. Some of the assumptions for

calculation are given below:

Terminal growth rate is assumed at 2.5%

Gross profit operating margin is assumed to be at 39.5%.

Pre-tax discount rate is assumed to be at 14.4%.

Management of organization decides future flow of cash resulting from cash

generating unit of assets and their carrying value. Future cash flow is estimated based on

budget and value can be considerably lower than budget. In order to determine existence of

impairment of assets, separate examination of each stores of company is done. If any

indication of impairment of stores are indicated using the test, then the management of

organization measures recoverable value of unit and make comparison with value in use

(Lawson et al. 2013).

discussed above are considered as partial construction that qualifies determination of

impairment of assets according to AASB 136.

b)Outlining process for determining asset impairment

Calculation of recoverable amount of assets and value in use is done by Myer

holdings ltd for determining assets impairment test. Forecasting cash flow is done based on

model that is approved by management of organization. Extrapolation of cash flow for more

than five years is done using the terminal growth rate. Some of the assumptions for

calculation are given below:

Terminal growth rate is assumed at 2.5%

Gross profit operating margin is assumed to be at 39.5%.

Pre-tax discount rate is assumed to be at 14.4%.

Management of organization decides future flow of cash resulting from cash

generating unit of assets and their carrying value. Future cash flow is estimated based on

budget and value can be considerably lower than budget. In order to determine existence of

impairment of assets, separate examination of each stores of company is done. If any

indication of impairment of stores are indicated using the test, then the management of

organization measures recoverable value of unit and make comparison with value in use

(Lawson et al. 2013).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING STANDARD AND REGULATIONS

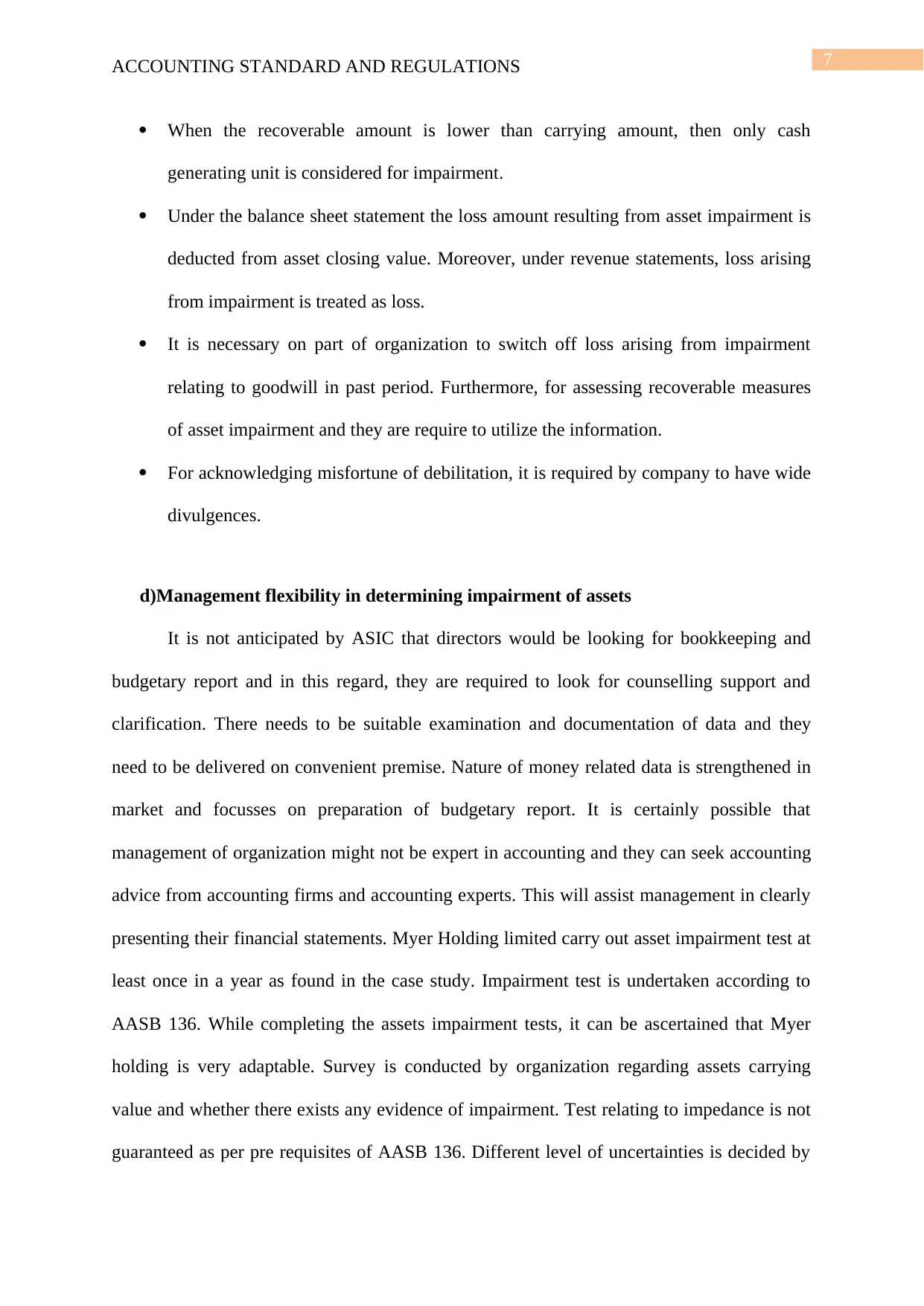

c) Information is required in determining asset impairment

Information required for determining impairment test of Myer Holdings ltd are as

follows:

Recoverable amount of assets within the intention of estimating is expressed as

percentage that is higher among the fair value of assets deducted by selling price and

fair value in use.

Loss from impairment of assets is recognized as cost under misfortune and benefit

account. Against the perceived revaluation, affected resources are revalued under

immaterial resource (IAS 38) and IAS 16 PPE (IAS 16) (Guthrie and Pang 2013).

It is essential to determine recoverable values and value in use relating to impairment

of assets.

c) Information is required in determining asset impairment

Information required for determining impairment test of Myer Holdings ltd are as

follows:

Recoverable amount of assets within the intention of estimating is expressed as

percentage that is higher among the fair value of assets deducted by selling price and

fair value in use.

Loss from impairment of assets is recognized as cost under misfortune and benefit

account. Against the perceived revaluation, affected resources are revalued under

immaterial resource (IAS 38) and IAS 16 PPE (IAS 16) (Guthrie and Pang 2013).

It is essential to determine recoverable values and value in use relating to impairment

of assets.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING STANDARD AND REGULATIONS

When the recoverable amount is lower than carrying amount, then only cash

generating unit is considered for impairment.

Under the balance sheet statement the loss amount resulting from asset impairment is

deducted from asset closing value. Moreover, under revenue statements, loss arising

from impairment is treated as loss.

It is necessary on part of organization to switch off loss arising from impairment

relating to goodwill in past period. Furthermore, for assessing recoverable measures

of asset impairment and they are require to utilize the information.

For acknowledging misfortune of debilitation, it is required by company to have wide

divulgences.

d)Management flexibility in determining impairment of assets

It is not anticipated by ASIC that directors would be looking for bookkeeping and

budgetary report and in this regard, they are required to look for counselling support and

clarification. There needs to be suitable examination and documentation of data and they

need to be delivered on convenient premise. Nature of money related data is strengthened in

market and focusses on preparation of budgetary report. It is certainly possible that

management of organization might not be expert in accounting and they can seek accounting

advice from accounting firms and accounting experts. This will assist management in clearly

presenting their financial statements. Myer Holding limited carry out asset impairment test at

least once in a year as found in the case study. Impairment test is undertaken according to

AASB 136. While completing the assets impairment tests, it can be ascertained that Myer

holding is very adaptable. Survey is conducted by organization regarding assets carrying

value and whether there exists any evidence of impairment. Test relating to impedance is not

guaranteed as per pre requisites of AASB 136. Different level of uncertainties is decided by

When the recoverable amount is lower than carrying amount, then only cash

generating unit is considered for impairment.

Under the balance sheet statement the loss amount resulting from asset impairment is

deducted from asset closing value. Moreover, under revenue statements, loss arising

from impairment is treated as loss.

It is necessary on part of organization to switch off loss arising from impairment

relating to goodwill in past period. Furthermore, for assessing recoverable measures

of asset impairment and they are require to utilize the information.

For acknowledging misfortune of debilitation, it is required by company to have wide

divulgences.

d)Management flexibility in determining impairment of assets

It is not anticipated by ASIC that directors would be looking for bookkeeping and

budgetary report and in this regard, they are required to look for counselling support and

clarification. There needs to be suitable examination and documentation of data and they

need to be delivered on convenient premise. Nature of money related data is strengthened in

market and focusses on preparation of budgetary report. It is certainly possible that

management of organization might not be expert in accounting and they can seek accounting

advice from accounting firms and accounting experts. This will assist management in clearly

presenting their financial statements. Myer Holding limited carry out asset impairment test at

least once in a year as found in the case study. Impairment test is undertaken according to

AASB 136. While completing the assets impairment tests, it can be ascertained that Myer

holding is very adaptable. Survey is conducted by organization regarding assets carrying

value and whether there exists any evidence of impairment. Test relating to impedance is not

guaranteed as per pre requisites of AASB 136. Different level of uncertainties is decided by

8ACCOUNTING STANDARD AND REGULATIONS

level of management that help in giving assurance of the fact that cash generating unit of

Myer holdings would be advantageous without money bound streams. Therefore, it can be

identified from the evidence depicted by case study and discussing the relevant facts deduce

that there is active engagement on part of company for determining impairment test annually

that are in compliance with AASB 136.

Conclusion:

From the above analysis, it can be concluded that Myer holdings limited determine

the asset impairment tests by complying with the requirement of AASB 136. For measuring

the loss arising from impairment, it is required by company to measure the value in use and

recoverable value in the event of indication of asset impairment. Therefore, it can be

concluded that management of Myer holdings limited is flexible when it comes to determine

the loss arising from impairment and carrying out asset impairment test.

level of management that help in giving assurance of the fact that cash generating unit of

Myer holdings would be advantageous without money bound streams. Therefore, it can be

identified from the evidence depicted by case study and discussing the relevant facts deduce

that there is active engagement on part of company for determining impairment test annually

that are in compliance with AASB 136.

Conclusion:

From the above analysis, it can be concluded that Myer holdings limited determine

the asset impairment tests by complying with the requirement of AASB 136. For measuring

the loss arising from impairment, it is required by company to measure the value in use and

recoverable value in the event of indication of asset impairment. Therefore, it can be

concluded that management of Myer holdings limited is flexible when it comes to determine

the loss arising from impairment and carrying out asset impairment test.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING STANDARD AND REGULATIONS

Reference:

Adibah Wan Ismail, W., Anuar Kamarudin, K., van Zijl, T. and Dunstan, K., 2013. Earnings

quality and the adoption of IFRS-based accounting standards: Evidence from an emerging

market. Asian Review of Accounting, 21(1), pp.53-73.

Albu, C.N., Albu, N. and Alexander, D., 2014. When global accounting standards meet the

local context—Insights from an emerging economy. Critical Perspectives on

Accounting, 25(6), pp.489-510.

Bond, D., Govendir, B. and Wells, P., 2016. An evaluation of asset impairments by

Australian firms and whether they were impacted by AASB 136. Accounting &

Finance, 56(1), pp.259-288.

Guthrie, J. and Pang, T.T., 2013. Disclosure of Goodwill Impairment under AASB 136 from

2005–2010. Australian Accounting Review, 23(3), pp.216-231.

Lawson, R.A., Blocher, E.J., Brewer, P.C., Cokins, G., Sorensen, J.E., Stout, D.E., Sundem,

G.L., Wolcott, S.K. and Wouters, M.J., 2013. Focusing accounting curricula on students'

long-run careers: Recommendations for an integrated competency-based framework for

accounting education. Issues in Accounting Education, 29(2), pp.295-317.

Oulasvirta, L., 2014. The reluctance of a developed country to choose International Public

Sector Accounting Standards of the IFAC. A critical case study. Critical Perspectives on

Accounting, 25(3), pp.272-285.

Preiato, J., Brown, P. and Tarca, A., 2015. A comparison of between‐country measures of

legal setting and enforcement of accounting standards. Journal of Business Finance &

Accounting, 42(1-2), pp.1-50.

Reference:

Adibah Wan Ismail, W., Anuar Kamarudin, K., van Zijl, T. and Dunstan, K., 2013. Earnings

quality and the adoption of IFRS-based accounting standards: Evidence from an emerging

market. Asian Review of Accounting, 21(1), pp.53-73.

Albu, C.N., Albu, N. and Alexander, D., 2014. When global accounting standards meet the

local context—Insights from an emerging economy. Critical Perspectives on

Accounting, 25(6), pp.489-510.

Bond, D., Govendir, B. and Wells, P., 2016. An evaluation of asset impairments by

Australian firms and whether they were impacted by AASB 136. Accounting &

Finance, 56(1), pp.259-288.

Guthrie, J. and Pang, T.T., 2013. Disclosure of Goodwill Impairment under AASB 136 from

2005–2010. Australian Accounting Review, 23(3), pp.216-231.

Lawson, R.A., Blocher, E.J., Brewer, P.C., Cokins, G., Sorensen, J.E., Stout, D.E., Sundem,

G.L., Wolcott, S.K. and Wouters, M.J., 2013. Focusing accounting curricula on students'

long-run careers: Recommendations for an integrated competency-based framework for

accounting education. Issues in Accounting Education, 29(2), pp.295-317.

Oulasvirta, L., 2014. The reluctance of a developed country to choose International Public

Sector Accounting Standards of the IFAC. A critical case study. Critical Perspectives on

Accounting, 25(3), pp.272-285.

Preiato, J., Brown, P. and Tarca, A., 2015. A comparison of between‐country measures of

legal setting and enforcement of accounting standards. Journal of Business Finance &

Accounting, 42(1-2), pp.1-50.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING STANDARD AND REGULATIONS

Yongqing, L., Eddie, I. and Jinghui, L., 2013. The impact of carbon emissions on asset values

and operating cash flows: evidence from Australian listed companies. Journal of modern

Accounting and Auditing, 9(1), p.94.

Yongqing, L., Eddie, I. and Jinghui, L., 2013. The impact of carbon emissions on asset values

and operating cash flows: evidence from Australian listed companies. Journal of modern

Accounting and Auditing, 9(1), p.94.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.