Australian Accounting Practices: A Report on Current Trends

VerifiedAdded on 2019/10/30

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

EXECUTIVE SUMMARY

This report analyses how there is a shift in focus of accounting systems in Australian companies

from creation of value for shareholders and customers to sustainability reports, creation of value

for stakeholders and effective risk management. A literature review is done and practical

examples from annual reports of existing companies of Australia are provided.

Contents

1. INTRODUCTION.......................................................................................................................2

2. LITERATURE REVIEW............................................................................................................2

3. CHANGES IN FOCUS OF MANAGEMENT ACCOUNTING FUNCTION...........................4

4. PRACTICAL EXAMPLES FROM ANNUAL REPORTS OF COMPANIES CURRENTLY

OPERATING IN AUSTRALI.........................................................................................................5

CONCLUSION................................................................................................................................6

5. APPENDICES.............................................................................................................................7

6. REFERENCE LISTS...................................................................................................................8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1. INTRODUCTION

In the 21st century, management accounting practices in Australia shifted from creating

value for customers and shareholders and organizational innovation to creation of value for

stakeholder, management of risks and sustainability reporting. There are multiple risks which are

involved in the business processes of a company. Risk can pose serious threats to the resources

of practices. Unlike early 1980s and 1990s management accounting practices in Australia

focused on risk management by either minimizing the risk or eliminating risks. Management

accounting practices in Australia aim to create value for stakeholders by shifting focus from

profitability during a shorter span of time to aiming to accomplish prosperity in the long run.

Management accounting practices in Australia do not focus only on creating profit for

shareholders but also focuses on corporate governance and corporate social responsibility so that

firms can return value to stakeholders of business and thus can achieve long term sustainability.

Management accounting practices have introduced models like Stakeholder Value Model (STV)

and Corporate Social Responsibility (CSR) models in Australia. Organizations and firms are no

more viewed as microscopic organizations in Australia with the advent of globalization and

management accounting practices have changed from 1990s and 2000 and have adopted a

contemporary approach (Birt et al., 2014).

Discussion

2. LITERATURE REVIEW

In early 1980s and 1990s management accounting practices ignored the consequences

that business have on society and environment. Social accounting practices have emerged in

Paraphrase This Document

Australia and firms no longer focus on only economic performance (Cantrell, Kyriazis & Noble,

2015). Management accountants must provide information on development of stakeholders. Thus

in Australia, management accounting practices has incorporated Stakeholder Value Model where

appropriate management practices and strategies are followed and there is core commitment to

humanistic values in organization. A flexible and supportive organization structure and an open

model of communication help management accounting practices to create value for stakeholders

in AustraliaThe economic approach of corporate governance focuses on enhancing the

competitive position of the firm which helps manager to achieve short term success. However

the implementation of the STV model in management accounting practices focuses on both

performance which is good financially and enhances the commitment of an enterprise towards

fair accounting practices and equity (Tucker & Schaltegger, 2016). The firms in Australia

incorporates STV model in accounting practices by identifying its primary stakeholders and

addressing their issues and concerns immediately, secondary stakeholders are addressed

ethically. In modern days management accounting practices in firms in Australia focuses on

allocating resources efficiently and achieves better control by providing information about

society and environment (Kang & Gray, 2013). .

The accounting system in Australia focuses on Sustainability accounting practices in

modern days. Sustainability reporting comprises of multiple arenas like non-financial reporting,

corporate social responsibility, environmental and social accounting practices. Sustainability

report provides information about integrated report which reveals how value is created by a firm

on short, medium and long term. The information about sustainability is disclosed to public by

Australian firms. Thus analysts and investors in Australia focus on long-term performance of a

firm and addresses sustainability issues like greenhouse gas emission and corporate

responsibility (Higgins, Milne & Van Gramberg, 2015). Reports of sustainability are jointly

formed by members of Boards of Australian firms and investment analysts. Earlier only public

companies in Australia focused on sustainability reporting but in modern days sustainability

reports are also prepared and disclosed by private enterprises in Australia. Global Reporting

Initiative (GRI) helps in comparing the sustainability reports of companies belonging to a

specific industry in Australia. Climate change plays a vital role in sustainability reporting in

Australia. Companies ensure to be neutral to carbon and focus on development of products

which are less carbon intensive. The investment value of a firm is impacted by this sustainability

report. Top 100 public companies in Australia have 48 % sustainability reporting and 47%

sustainability reporting is provided by top 100 private companies in Australia. The trend on

publishing stand-alone sustainability reports is popular among companies in Australia which is

separate from the annual reports of the company (Bachoo, Tan & Wilson, 2013).

The regulations of accounting systems in Australia manage risk faced by organizations by

providing reliable and timely information. The accounting practices have become technical and

complicated. A risk management framework is adopted by Australian firms in modern days for

effective control and mitigation of risks faced by business processes of Australian enterprises.

Key organization risks can be risk of governance, risk of business continuity and risk in

succession planning, risks imposed by stakeholders and technology and other financial risks.

Risks can also be imposed to firms in Australia by regulatory changes and human resources and

the system of operation of firms. The accounting practices to handle risks hugely depend on the

size and the practices of operation followed by an Australian firm. It is of paramount importance

to monitor the policies and practices of risk management of an enterprise to align the risk

management process with the accounting practices of an enterprise in Australia

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The Risk Management Framework will have direct impact on the partners of a firm. The

system of leadership and clear communication of risk management process across all levels in an

organization helps firms in Australia to manage, eliminate and mitigate risks effectively (Chung

& Hensher, 2015). The Risk Management framework of a firm is reviewed regularly, at least

annually by business leaders in Australia. Proper documentation of the risk management process

is also important so that the policies and procedures of risk management can be clearly

communicated to the personnel of a firm (Wadeson & Ciccotosto, 2013). The effective

management of risks by accounting practices in Australia helps in maintaining the reputation of a

firm. Blind spots and deficiencies can be identified better by an organization if Risk

Management Framework is effectively implemented and integrated with the accounting practices

in Australia (Brown, Steen & Foreman, 2009).

3. CHANGES IN FOCUS OF MANAGEMENT ACCOUNTING FUNCTION

The management accounting function has changed focus. Organizational innovation,

economic profitability, creating value for shareholders and stakeholders were the prime focus of

management accounting firms in 1980 and 1990s.The principle of accounting practices by firms

in Australia was greatly influenced by Great Britain in earlier days and there was absence of a

single professional institution also desired results of accounting practices were not achieved by

firms of Australia because of absence of co-operation among accounting bodies in Australia that

existed in earlier days(Considine et al. , 2012).

In twentieth century, management accountants were involved in managerial decision

making, they were show the big picture of the firm and were involved in decision making

process of the organization. Management accountants also had a holistic approach towards an

Paraphrase This Document

organization, they demonstrated complete understanding of the requirements of an organization

and also helped managers to achieve competitive advantage. In the second part of twentieth

century there were two major professional bodies which handled accounting practices of

enterprises in Australia. These two professional bodies were Institute of Chartered Accountants

in Australia (ICAA) and CPA Australia. The Australian Accounting Research Foundation

(AARF) promoted research in accounting in Australia with the medium of Accounting Standard

Boards (AcSB). In earlier days there was implementation in promoting accounting practices as

each state in Australia had its own company law. The Accounting Standard Review Board

(ASRB) was formed in Australia in the year 1984 which was responsible to review accounting

standards. However this board did not continue for long and was replaced by Australian

Accounting Standards Board (AASB) in the year 1989. In the year 1990s, huge pressure was

imposed by boards like Australian Stock Exchange to align accounting practices in Australia to

the accounting practices followed internationally. This was a result of economic globalization. In

modern days accounting standards in Australia are determined by the International Accounting

Standards Board ( IASB). Thus it can be clearly stated that accounting has achieved a strong

position in the 21st century in economic framework of Australia. Urgent Issues Group was

created in Australia which provided a quick and prompt solution to difficulties of accounting

practices which was a result of difference in opinion of accounting standards (Henderson et al.,

2014).

Thus it can be clearly understood how the accounting practices in Australia has changed

from 1980s to 2000 to the 21st century. The accounting firms in Australia focus towards creating

value for both primary and secondary stakeholders, both public and private organizations in

Australia publish sustainability reports which addresses issues like climate change and other

environmental issues and management accounting practices also focus on management of risks.

It can be clearly understood that focus of Australian accounting practices shifted from just a

good economic performance of the firm and firms introduced on non-financial performance by

adopting approaches like Stakeholder Value Model and focusing on corporate governance and

corporate social responsibility. In order to gain prosperity for business on a long term

perspective, management accountants have shifted focus from creating value for shareholders

and customers to create value for all stakeholders of business. In Australia, both public and

private enterprises focus on accounting practices on environmental accounting and have shifted

focus to sustainability and corporate social responsibility (Horngren, 2013). Disclosure reports

are published by company on opportunities for equal employment, safety of work environment,

product and industry and aim to provide better working conditions for employees. Accounting

systems of public and private enterprises in Australia provide data related to these topics so that

reports of disclosure can be published by companies. Contemporary accounting practices in

Australia focuses on four major arenas which include growth and learning, internal business

process, performance related to finance and customers. On modern days companies perform

Strategic audits which are quite different from audits which are financial in nature. In strategic

audits, all strategic functions of a firm are reviewed. Value based reporting are adopted by many

public enterprises in Australia which focuses on social governance, issues related to

environment, framework of empowerment and economics. Thus there is sustainable change in

focus of management accounting functions in Australia (Hoggett, 2012).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4. PRACTICAL EXAMPLES FROM ANNUAL REPORTS OF COMPANIES

CURRENTLY OPERATING IN AUSTRALI

The change in focus of management accounting functions can be clearly seen from the

annual report of National Australia Bank Limited. The primary stakeholders of the bank are

customers, community, suppliers, employees and shareholders. The firm has adopted an ESG

framework while publishing its annual report in the year 2016. The ESG framework comprises

of themes related to environment, society and governance. Surveys from primary stakeholders of

the bank are conducted every year and feedback from stakeholders like employees and

community members are taken. The bank also creates a supporting work environment for his

stakeholders (National Australian Bank, 2017)

From the annual report of Wesfarmers it is clearly evident that the company focuses on

creating value for stakeholder and publishes sustainability report. The company focuses on risk

management which includes operational risks, risks related to strategy, financial risks and

regulatory risks. Though the company focuses on creating value for shareholders but issues

related to people and sourcing networks of the company, issues related to environment and

governance are also addressed by the firm as evident from its annual report published in the year

2016( WESFARMERS, 2017)

It is also evident from the annual report of Coles that the company focuses on risk

management. The focus is on mitigation of risks on supply chain of fuel, risks related to retention

of employees. The leading supermarket in Australia focuses on creating value for all its primary

stakeholders which include customers who can avail fresh stocks from Coles at lower prices.

Coles also focuses on environmental issues and creates value for all its suppliers. Sustainability

Paraphrase This Document

reports are published by the company and all management accounting practices have shifted

from just mere profitability and financial performance (Coles, 2017)

CONCLUSION

It can be concluded that, in the global world, the accounting system of Australia has

demonstrated major changes. Companies focus on long term profit and thus focus of

management accountants have shifted from creating value for shareholders and customers to

sustainability reports, creation of value for stakeholders which include both primary and

secondary stakeholders and risk management. It is evident from the annual reports of existing

companies of Australia published in the year 2016 like National Australia Bank, Wesfarmers and

Coles that the companies mange risks effectively and publishes sustainability reports, addresses

concern for environment, CSR and creates vale for stakeholders.

5. APPENDICES

Bachoo, K., Tan, R., & Wilson, M. (2013). Firm value and the quality of sustainability reporting

in australia. Australian Accounting Review, 23(1), 67-87. doi:10.1111/j.1835-2561.2012.00187.x

Brown, I., Steen, A., & Foreman, J. (2009). Risk management in corporate governance: A review

and proposal. Corporate Governance: An International Review, 17(5), 546-558.

doi:10.1111/j.1467-8683.2009.00763.x

Cantrell, J., Kyriazis, E., & Noble, G. (2015). Developing cSR giving as a dynamic capability for

salient stakeholder management. Journal of Business Ethics, 130(2), 403-421.

doi:10.1007/s10551-014-2229-1

Chung, D., & Hensher, D. (2015). Risk management in public-Private partnerships. Australian

Accounting Review, 25(1), 13-27. doi:10.1111/auar.12062

Higgins, C., Milne, M., & Van Gramberg, B. (2015). The uptake of sustainability reporting in

australia. Journal of Business Ethics, 129(2), 445-468. doi:10.1007/s10551-014-2171-2

Kang, H., & Gray, S. J. (2013). Segment reporting practices in australia: Has ifrs 8 made a

difference? Australian Accounting Review, 23(3), 232-243. doi:10.1111/j.1835-

2561.2012.00173.x

Tucker, B. P., & Schaltegger, S. (2016).Comparing the research-practice gap in management

accounting: A view from professional accounting bodies in australia and

germany. Accounting, Auditing and Accountability Journal, 29(3), 362-400.

doi:10.1108/AAAJ-02-2014-1601

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Wadeson, D., & Ciccotosto, S. (2013). Succession planning in small accounting practices in

regional far north queensland. Australian Accounting Review, 23(2), 177-188.

doi:10.1111/j.1835-2561.2012.00189.x

6. REFERENCE LISTS

Birt, J., Chalmers, K., Moroney, S., Brooks, A., & Oliver, J. (2014). Accounting business

reporting for decision making (Fifth edition. ed.). Milton, Qld.: John Wiley and Sons

Australia.

coles. (2017). coles.com.au/. Retrieved 15 September 2017, from

https://www.coles.com.au/about-coles/annual-reports

Considine, B., Parkes, A., Olesen, K., Blount, Y., & Speer, D. (2012). Accounting information

systems : Understanding business processes(4th ed. ed.). Milton, Qld.: John Wiley &

Sons Australia.

Henderson, S., Peirson, G., Herbohn, K., Artiach, T., & Howieson, B. (2014). Issues in financial

accounting (15th edition. ed.). Frenchs Forest, N.S.W.: Pearson Australia

Hoggett, J. (2012). Accounting (8th ed. ed.). Milton, Qld.: John Wiley and Sons Australia.

Horngren, C. (2013). Accounting (7th adaptation ed. ed.). Frenchs Forest, N.S.W.: Pearson

Australia.

National Australian Bank. (2017). nab.com.au/. Retrieved 15 September 2017, from

https://www.nab.com.au/

Paraphrase This Document

WESFARMERS. (2017). wesfarmers.com.au/. Retrieved 15 September 2017, from

https://www.wesfarmers.com.au/

TASK 2

Cost allocation Methods:

Allocation of cost is a very important part for the determination of the various costs of

productions and their units produced in the various department of the company. However in

allocating of cost there are several type of method used these are the ABC costing, traditional

costing and many methods for the division of cost in the various department of the organization.

1. Direct Method: This is the technique in which all the costs are divided into various

department within the organization (Javid et al ,2016).

2. Step down Method: This method is associated with different department and they share

the expenses and also the overhead cost in the organization within the particular

department.

3. Reciprocal Method: In this method there is proper allocation of the expenses which is

different for various departments and it is based on recognition for corresponding

services in the service departments. However, the method is complicated and this would

result in a higher level of complexity and in determining the allocation of the indirect

expenses in the particular department.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Report

To

The Managing Director

………ltd.

Practical analysis for the problem

Date: 23th September 2017

Sir,

These reports reflect the study for ABC costing and for traditional costing which could be used

by company.

Background

Since there is a change in the economic complexity of the business and the costing technique

used to determine the cost of production for the organization. Overheads are incurred by the

organization and it is done by using the costing technique and activity based costing.

However ABC costing technique is used to allocate the overhead and expenses for the

department which is made on the basis of several factors and the nature of business expenses

Paraphrase This Document

incurred for accounting of management practice for the organization (Kalpakjian and Schmid,

2014).

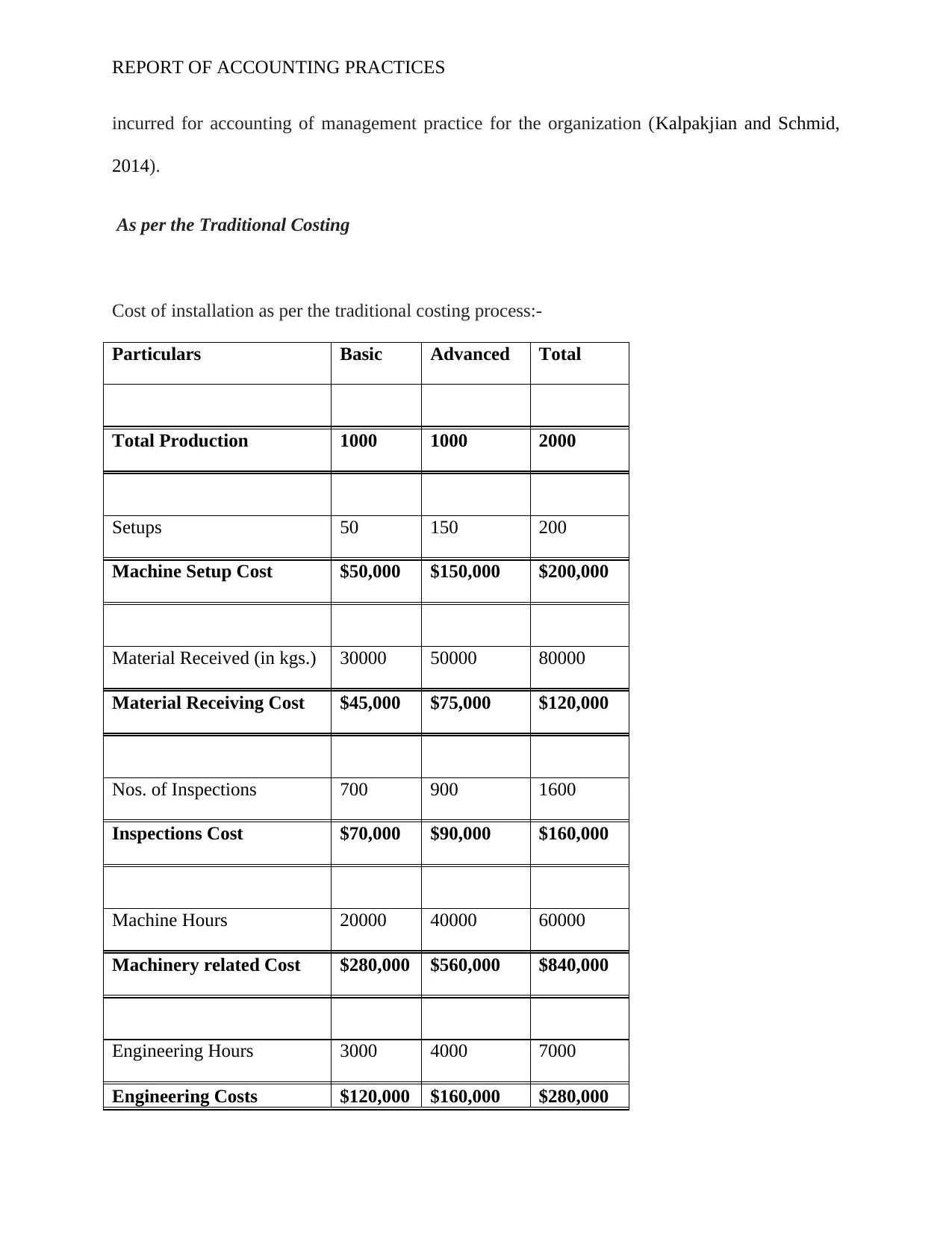

As per the Traditional Costing

Cost of installation as per the traditional costing process:-

Particulars Basic Advanced Total

Total Production 1000 1000 2000

Setups 50 150 200

Machine Setup Cost $50,000 $150,000 $200,000

Material Received (in kgs.) 30000 50000 80000

Material Receiving Cost $45,000 $75,000 $120,000

Nos. of Inspections 700 900 1600

Inspections Cost $70,000 $90,000 $160,000

Machine Hours 20000 40000 60000

Machinery related Cost $280,000 $560,000 $840,000

Engineering Hours 3000 4000 7000

Engineering Costs $120,000 $160,000 $280,000

Total Manufacturing

Overhead $565,000 $1,035,000

$1,600,00

0

Manufacturing Overhead

p.u. $565 $1,035

Assumption: Direct labour is consumed in both products. Therefore the fixed overheads will be

distributed in both the projects in the determined approach

As per ABC Costing

Particulars Basic Advanced

Direct Material p.u. $800 $1,600

Direct Labor Cost p.u. $600 $600

Manufacturing Overhead

p.u. $565 $1,035

Total Production Cost p.u. $1,965 $3,235

Cost Difference between two methods:

Particulars Basic Advanced

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

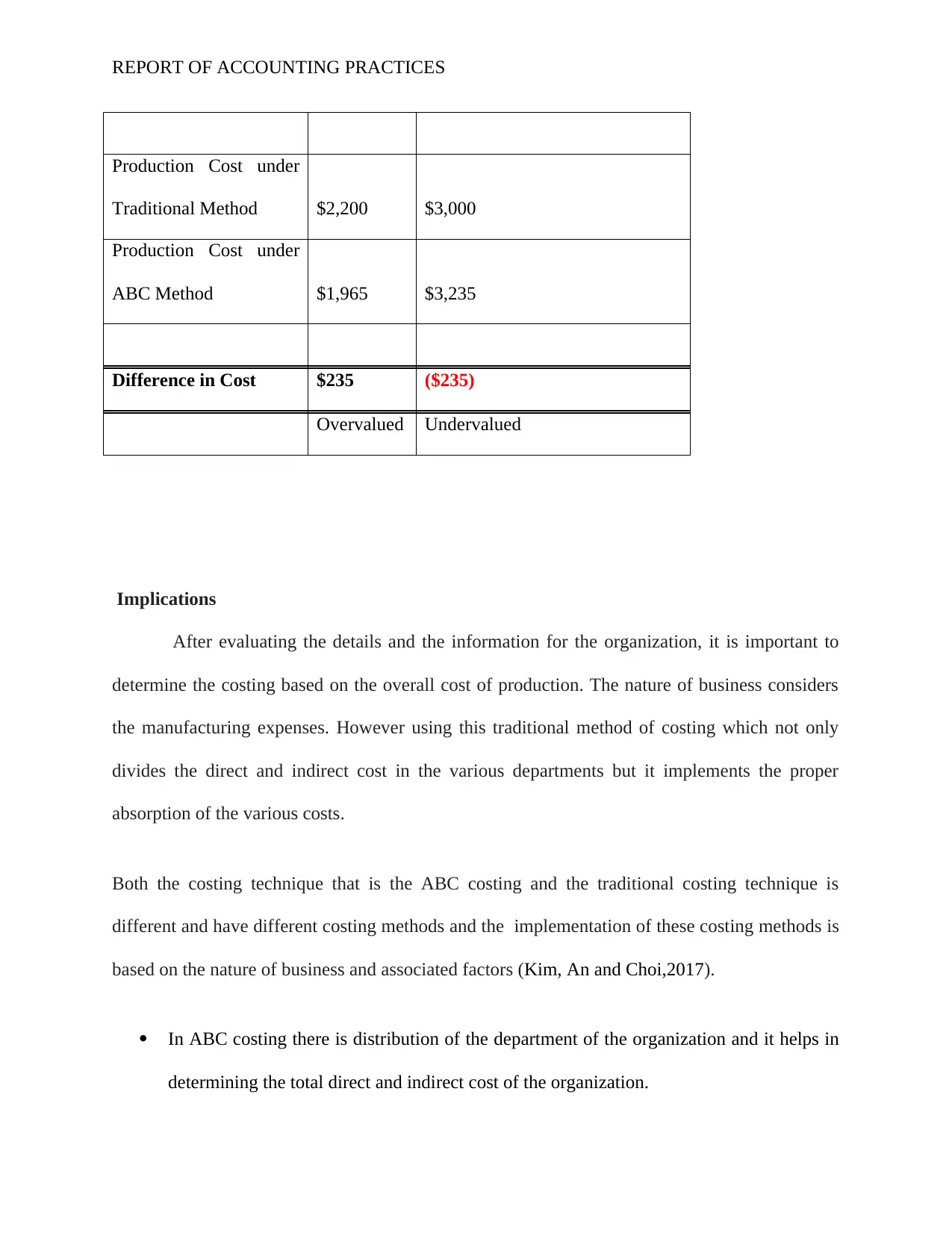

Production Cost under

Traditional Method $2,200 $3,000

Production Cost under

ABC Method $1,965 $3,235

Difference in Cost $235 ($235)

Overvalued Undervalued

Implications

After evaluating the details and the information for the organization, it is important to

determine the costing based on the overall cost of production. The nature of business considers

the manufacturing expenses. However using this traditional method of costing which not only

divides the direct and indirect cost in the various departments but it implements the proper

absorption of the various costs.

Both the costing technique that is the ABC costing and the traditional costing technique is

different and have different costing methods and the implementation of these costing methods is

based on the nature of business and associated factors (Kim, An and Choi,2017).

In ABC costing there is distribution of the department of the organization and it helps in

determining the total direct and indirect cost of the organization.

Paraphrase This Document

In using this method, the calculation for the cost that is associated for proper business

functioning and for factors on the cost of production.

Traditional costing method is the allocation of direct and indirect cost and this method is

mostly used by traditional companies. This method of evaluation of the cost of

production is based the distribution of the various cost (Mahal and Hossain, 2015).

Conclusion

In this report, there are various techniques used for costing such as ABC, revenue

management and other pricing techniques used to manage the costing and the pricing technique

of the organization. This technique helps the company so that there is increase in overall cost and

efficiency of this approach. It will be considered that the companies use this technique which

will increase the overall efficiency of business.

References

Javid, M., Hadian, M., Ghaderi, H., Ghaffari, S. and Salehi, M., 2016. Application of the

activity-based costing method for unit-cost calculation in a hospital. Global journal of health

science, 8(1), p.165.

Kalpakjian, S. and Schmid, S.R., 2014. Manufacturing engineering and technology (p. 913).

Upper Saddle River, NJ, USA: Pearson.

Kim, N.H., An, D. and Choi, J.H., 2017. Introduction. In Prognostics and Health Management of

Engineering Systems (pp. 1-24). Springer International Publishing.

Mahal, I. and Hossain, M.A., 2015. Activity-Based Costing (ABC)–An Effective Tool for Better

Management. Research Journal of Finance and Accounting, 6(4), pp.66-74.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.