Activity Based Costing vs Traditional/Absorption Costing

VerifiedAdded on 2022/11/24

|12

|2627

|267

AI Summary

This report compares Activity Based Costing and Traditional/Absorption Costing. It discusses the allocation of indirect costs and the impact on product cost. It also explores the advantages and disadvantages of Absorption Costing and its use for inventory valuation. Additionally, it highlights the benefits of Activity Based Costing for decision making and budgeting.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

REPORT ON ACTIVITY BASED COSTING VS

TRADITIONAL/ABSORPTION COSTING

TRADITIONAL/ABSORPTION COSTING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

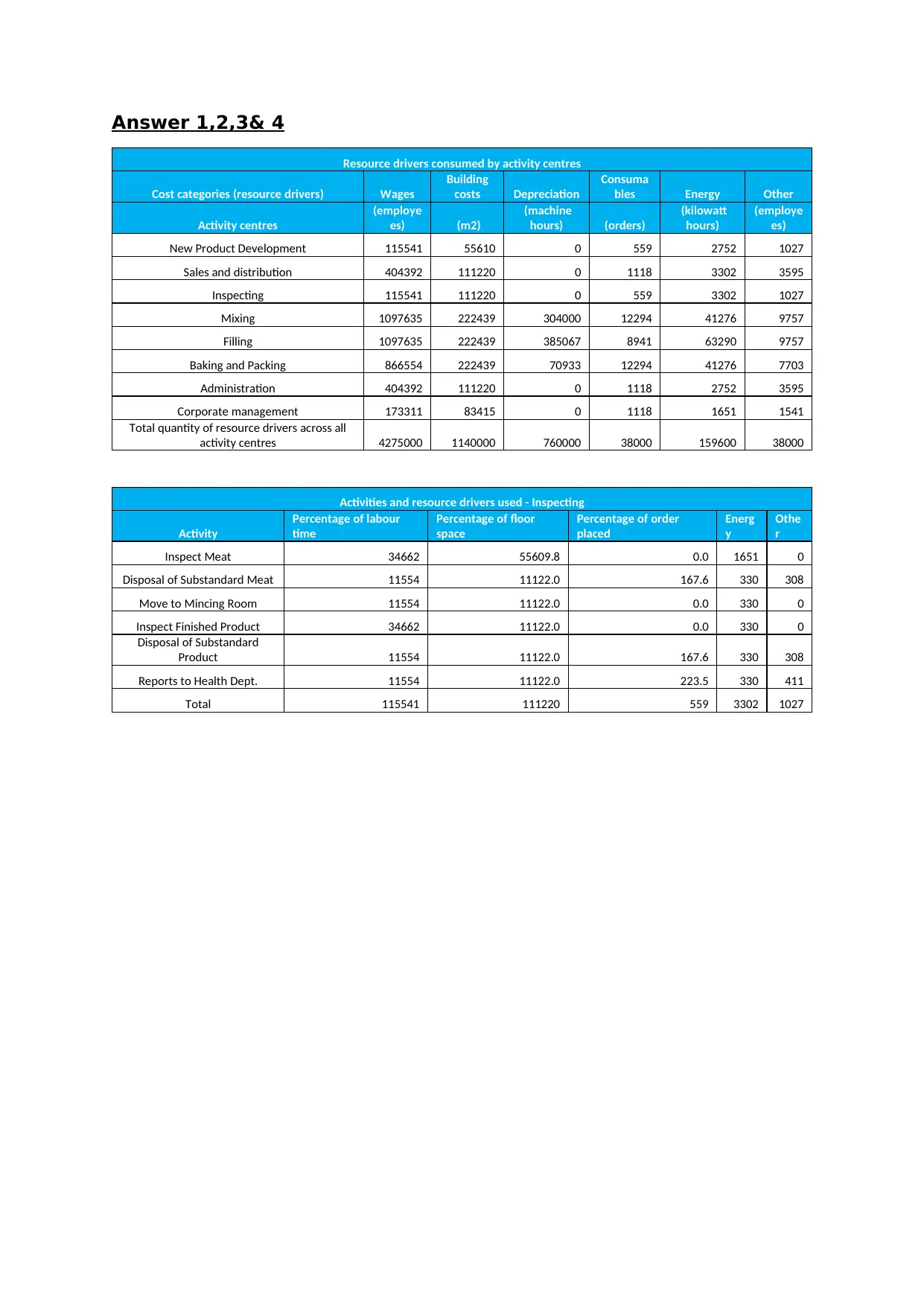

Answer 1,2,3& 4

Resource drivers consumed by activity centres

Cost categories (resource drivers) Wages

Building

costs Depreciation

Consuma

bles Energy Other

Activity centres

(employe

es) (m2)

(machine

hours) (orders)

(kilowatt

hours)

(employe

es)

New Product Development 115541 55610 0 559 2752 1027

Sales and distribution 404392 111220 0 1118 3302 3595

Inspecting 115541 111220 0 559 3302 1027

Mixing 1097635 222439 304000 12294 41276 9757

Filling 1097635 222439 385067 8941 63290 9757

Baking and Packing 866554 222439 70933 12294 41276 7703

Administration 404392 111220 0 1118 2752 3595

Corporate management 173311 83415 0 1118 1651 1541

Total quantity of resource drivers across all

activity centres 4275000 1140000 760000 38000 159600 38000

Activities and resource drivers used - Inspecting

Activity

Percentage of labour

time

Percentage of floor

space

Percentage of order

placed

Energ

y

Othe

r

Inspect Meat 34662 55609.8 0.0 1651 0

Disposal of Substandard Meat 11554 11122.0 167.6 330 308

Move to Mincing Room 11554 11122.0 0.0 330 0

Inspect Finished Product 34662 11122.0 0.0 330 0

Disposal of Substandard

Product 11554 11122.0 167.6 330 308

Reports to Health Dept. 11554 11122.0 223.5 330 411

Total 115541 111220 559 3302 1027

Resource drivers consumed by activity centres

Cost categories (resource drivers) Wages

Building

costs Depreciation

Consuma

bles Energy Other

Activity centres

(employe

es) (m2)

(machine

hours) (orders)

(kilowatt

hours)

(employe

es)

New Product Development 115541 55610 0 559 2752 1027

Sales and distribution 404392 111220 0 1118 3302 3595

Inspecting 115541 111220 0 559 3302 1027

Mixing 1097635 222439 304000 12294 41276 9757

Filling 1097635 222439 385067 8941 63290 9757

Baking and Packing 866554 222439 70933 12294 41276 7703

Administration 404392 111220 0 1118 2752 3595

Corporate management 173311 83415 0 1118 1651 1541

Total quantity of resource drivers across all

activity centres 4275000 1140000 760000 38000 159600 38000

Activities and resource drivers used - Inspecting

Activity

Percentage of labour

time

Percentage of floor

space

Percentage of order

placed

Energ

y

Othe

r

Inspect Meat 34662 55609.8 0.0 1651 0

Disposal of Substandard Meat 11554 11122.0 167.6 330 308

Move to Mincing Room 11554 11122.0 0.0 330 0

Inspect Finished Product 34662 11122.0 0.0 330 0

Disposal of Substandard

Product 11554 11122.0 167.6 330 308

Reports to Health Dept. 11554 11122.0 223.5 330 411

Total 115541 111220 559 3302 1027

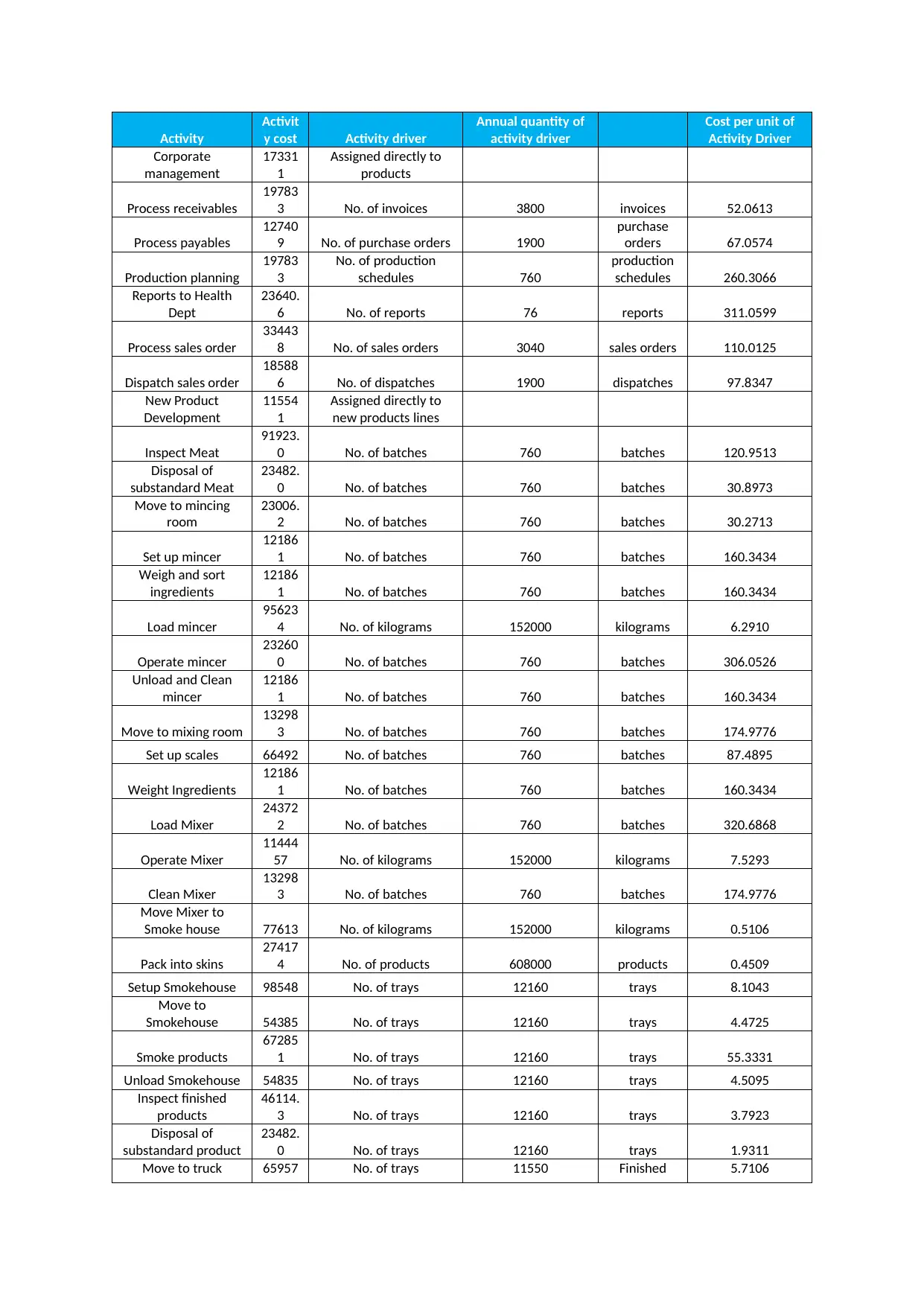

Activity

Activit

y cost Activity driver

Annual quantity of

activity driver

Cost per unit of

Activity Driver

Corporate

management

17331

1

Assigned directly to

products

Process receivables

19783

3 No. of invoices 3800 invoices 52.0613

Process payables

12740

9 No. of purchase orders 1900

purchase

orders 67.0574

Production planning

19783

3

No. of production

schedules 760

production

schedules 260.3066

Reports to Health

Dept

23640.

6 No. of reports 76 reports 311.0599

Process sales order

33443

8 No. of sales orders 3040 sales orders 110.0125

Dispatch sales order

18588

6 No. of dispatches 1900 dispatches 97.8347

New Product

Development

11554

1

Assigned directly to

new products lines

Inspect Meat

91923.

0 No. of batches 760 batches 120.9513

Disposal of

substandard Meat

23482.

0 No. of batches 760 batches 30.8973

Move to mincing

room

23006.

2 No. of batches 760 batches 30.2713

Set up mincer

12186

1 No. of batches 760 batches 160.3434

Weigh and sort

ingredients

12186

1 No. of batches 760 batches 160.3434

Load mincer

95623

4 No. of kilograms 152000 kilograms 6.2910

Operate mincer

23260

0 No. of batches 760 batches 306.0526

Unload and Clean

mincer

12186

1 No. of batches 760 batches 160.3434

Move to mixing room

13298

3 No. of batches 760 batches 174.9776

Set up scales 66492 No. of batches 760 batches 87.4895

Weight Ingredients

12186

1 No. of batches 760 batches 160.3434

Load Mixer

24372

2 No. of batches 760 batches 320.6868

Operate Mixer

11444

57 No. of kilograms 152000 kilograms 7.5293

Clean Mixer

13298

3 No. of batches 760 batches 174.9776

Move Mixer to

Smoke house 77613 No. of kilograms 152000 kilograms 0.5106

Pack into skins

27417

4 No. of products 608000 products 0.4509

Setup Smokehouse 98548 No. of trays 12160 trays 8.1043

Move to

Smokehouse 54385 No. of trays 12160 trays 4.4725

Smoke products

67285

1 No. of trays 12160 trays 55.3331

Unload Smokehouse 54835 No. of trays 12160 trays 4.5095

Inspect finished

products

46114.

3 No. of trays 12160 trays 3.7923

Disposal of

substandard product

23482.

0 No. of trays 12160 trays 1.9311

Move to truck 65957 No. of trays 11550 Finished 5.7106

Activit

y cost Activity driver

Annual quantity of

activity driver

Cost per unit of

Activity Driver

Corporate

management

17331

1

Assigned directly to

products

Process receivables

19783

3 No. of invoices 3800 invoices 52.0613

Process payables

12740

9 No. of purchase orders 1900

purchase

orders 67.0574

Production planning

19783

3

No. of production

schedules 760

production

schedules 260.3066

Reports to Health

Dept

23640.

6 No. of reports 76 reports 311.0599

Process sales order

33443

8 No. of sales orders 3040 sales orders 110.0125

Dispatch sales order

18588

6 No. of dispatches 1900 dispatches 97.8347

New Product

Development

11554

1

Assigned directly to

new products lines

Inspect Meat

91923.

0 No. of batches 760 batches 120.9513

Disposal of

substandard Meat

23482.

0 No. of batches 760 batches 30.8973

Move to mincing

room

23006.

2 No. of batches 760 batches 30.2713

Set up mincer

12186

1 No. of batches 760 batches 160.3434

Weigh and sort

ingredients

12186

1 No. of batches 760 batches 160.3434

Load mincer

95623

4 No. of kilograms 152000 kilograms 6.2910

Operate mincer

23260

0 No. of batches 760 batches 306.0526

Unload and Clean

mincer

12186

1 No. of batches 760 batches 160.3434

Move to mixing room

13298

3 No. of batches 760 batches 174.9776

Set up scales 66492 No. of batches 760 batches 87.4895

Weight Ingredients

12186

1 No. of batches 760 batches 160.3434

Load Mixer

24372

2 No. of batches 760 batches 320.6868

Operate Mixer

11444

57 No. of kilograms 152000 kilograms 7.5293

Clean Mixer

13298

3 No. of batches 760 batches 174.9776

Move Mixer to

Smoke house 77613 No. of kilograms 152000 kilograms 0.5106

Pack into skins

27417

4 No. of products 608000 products 0.4509

Setup Smokehouse 98548 No. of trays 12160 trays 8.1043

Move to

Smokehouse 54385 No. of trays 12160 trays 4.4725

Smoke products

67285

1 No. of trays 12160 trays 55.3331

Unload Smokehouse 54835 No. of trays 12160 trays 4.5095

Inspect finished

products

46114.

3 No. of trays 12160 trays 3.7923

Disposal of

substandard product

23482.

0 No. of trays 12160 trays 1.9311

Move to truck 65957 No. of trays 11550 Finished 5.7106

Activity

Activit

y cost Activity driver

Annual quantity of

activity driver

Cost per unit of

Activity Driver

trays

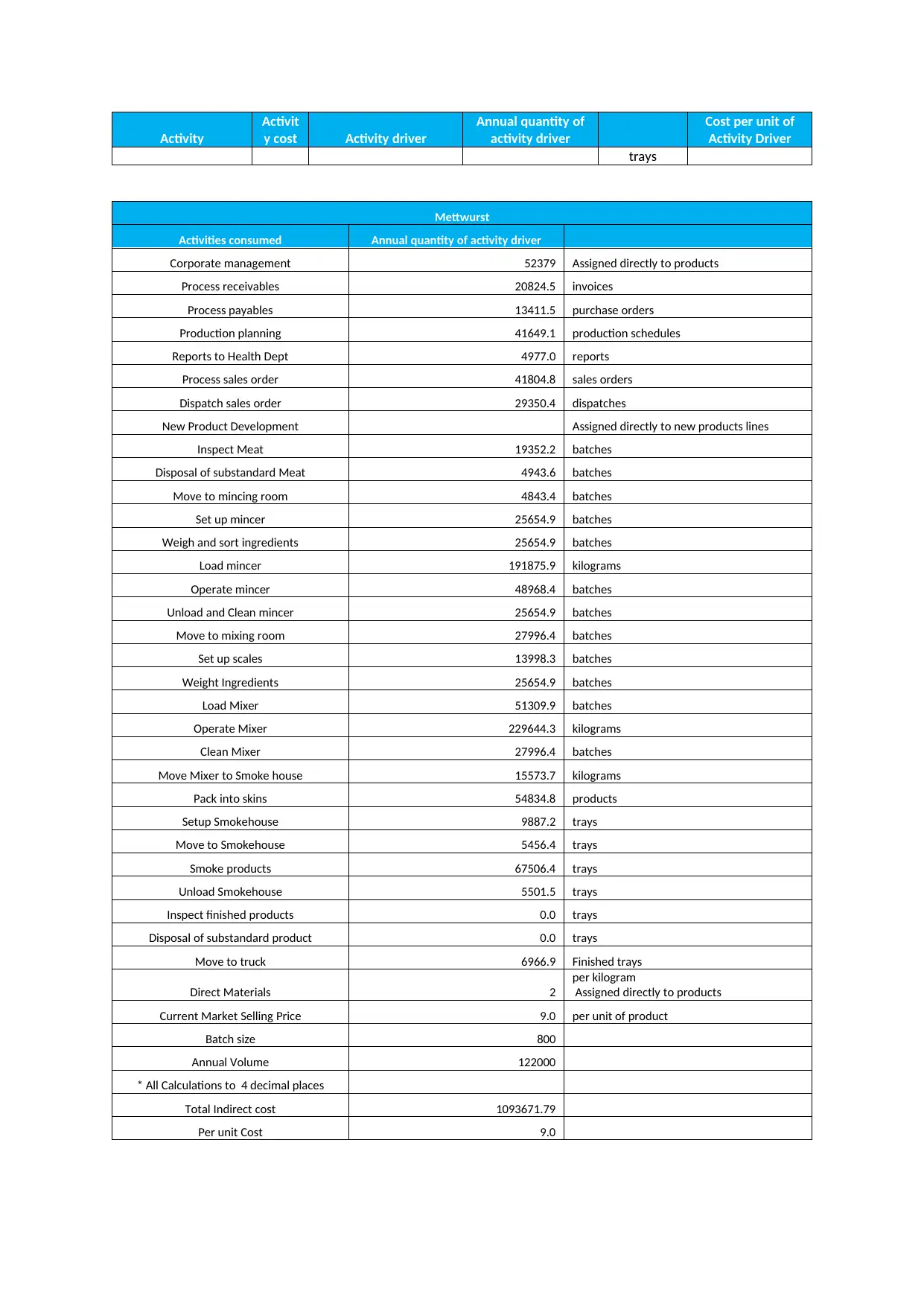

Mettwurst

Activities consumed Annual quantity of activity driver

Corporate management 52379 Assigned directly to products

Process receivables 20824.5 invoices

Process payables 13411.5 purchase orders

Production planning 41649.1 production schedules

Reports to Health Dept 4977.0 reports

Process sales order 41804.8 sales orders

Dispatch sales order 29350.4 dispatches

New Product Development Assigned directly to new products lines

Inspect Meat 19352.2 batches

Disposal of substandard Meat 4943.6 batches

Move to mincing room 4843.4 batches

Set up mincer 25654.9 batches

Weigh and sort ingredients 25654.9 batches

Load mincer 191875.9 kilograms

Operate mincer 48968.4 batches

Unload and Clean mincer 25654.9 batches

Move to mixing room 27996.4 batches

Set up scales 13998.3 batches

Weight Ingredients 25654.9 batches

Load Mixer 51309.9 batches

Operate Mixer 229644.3 kilograms

Clean Mixer 27996.4 batches

Move Mixer to Smoke house 15573.7 kilograms

Pack into skins 54834.8 products

Setup Smokehouse 9887.2 trays

Move to Smokehouse 5456.4 trays

Smoke products 67506.4 trays

Unload Smokehouse 5501.5 trays

Inspect finished products 0.0 trays

Disposal of substandard product 0.0 trays

Move to truck 6966.9 Finished trays

Direct Materials 2

per kilogram

Assigned directly to products

Current Market Selling Price 9.0 per unit of product

Batch size 800

Annual Volume 122000

* All Calculations to 4 decimal places

Total Indirect cost 1093671.79

Per unit Cost 9.0

Activit

y cost Activity driver

Annual quantity of

activity driver

Cost per unit of

Activity Driver

trays

Mettwurst

Activities consumed Annual quantity of activity driver

Corporate management 52379 Assigned directly to products

Process receivables 20824.5 invoices

Process payables 13411.5 purchase orders

Production planning 41649.1 production schedules

Reports to Health Dept 4977.0 reports

Process sales order 41804.8 sales orders

Dispatch sales order 29350.4 dispatches

New Product Development Assigned directly to new products lines

Inspect Meat 19352.2 batches

Disposal of substandard Meat 4943.6 batches

Move to mincing room 4843.4 batches

Set up mincer 25654.9 batches

Weigh and sort ingredients 25654.9 batches

Load mincer 191875.9 kilograms

Operate mincer 48968.4 batches

Unload and Clean mincer 25654.9 batches

Move to mixing room 27996.4 batches

Set up scales 13998.3 batches

Weight Ingredients 25654.9 batches

Load Mixer 51309.9 batches

Operate Mixer 229644.3 kilograms

Clean Mixer 27996.4 batches

Move Mixer to Smoke house 15573.7 kilograms

Pack into skins 54834.8 products

Setup Smokehouse 9887.2 trays

Move to Smokehouse 5456.4 trays

Smoke products 67506.4 trays

Unload Smokehouse 5501.5 trays

Inspect finished products 0.0 trays

Disposal of substandard product 0.0 trays

Move to truck 6966.9 Finished trays

Direct Materials 2

per kilogram

Assigned directly to products

Current Market Selling Price 9.0 per unit of product

Batch size 800

Annual Volume 122000

* All Calculations to 4 decimal places

Total Indirect cost 1093671.79

Per unit Cost 9.0

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

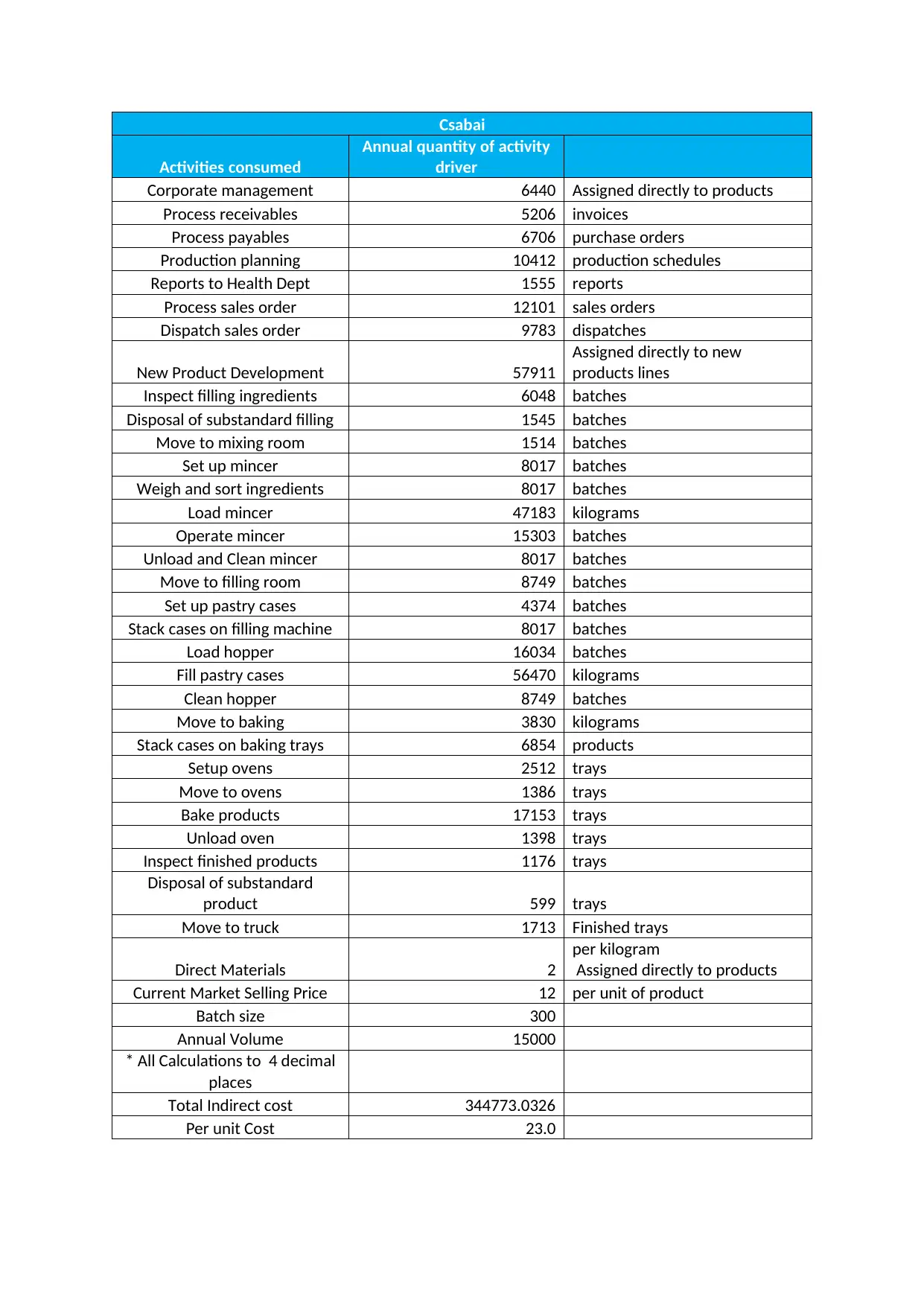

Csabai

Activities consumed

Annual quantity of activity

driver

Corporate management 6440 Assigned directly to products

Process receivables 5206 invoices

Process payables 6706 purchase orders

Production planning 10412 production schedules

Reports to Health Dept 1555 reports

Process sales order 12101 sales orders

Dispatch sales order 9783 dispatches

New Product Development 57911

Assigned directly to new

products lines

Inspect filling ingredients 6048 batches

Disposal of substandard filling 1545 batches

Move to mixing room 1514 batches

Set up mincer 8017 batches

Weigh and sort ingredients 8017 batches

Load mincer 47183 kilograms

Operate mincer 15303 batches

Unload and Clean mincer 8017 batches

Move to filling room 8749 batches

Set up pastry cases 4374 batches

Stack cases on filling machine 8017 batches

Load hopper 16034 batches

Fill pastry cases 56470 kilograms

Clean hopper 8749 batches

Move to baking 3830 kilograms

Stack cases on baking trays 6854 products

Setup ovens 2512 trays

Move to ovens 1386 trays

Bake products 17153 trays

Unload oven 1398 trays

Inspect finished products 1176 trays

Disposal of substandard

product 599 trays

Move to truck 1713 Finished trays

Direct Materials 2

per kilogram

Assigned directly to products

Current Market Selling Price 12 per unit of product

Batch size 300

Annual Volume 15000

* All Calculations to 4 decimal

places

Total Indirect cost 344773.0326

Per unit Cost 23.0

Activities consumed

Annual quantity of activity

driver

Corporate management 6440 Assigned directly to products

Process receivables 5206 invoices

Process payables 6706 purchase orders

Production planning 10412 production schedules

Reports to Health Dept 1555 reports

Process sales order 12101 sales orders

Dispatch sales order 9783 dispatches

New Product Development 57911

Assigned directly to new

products lines

Inspect filling ingredients 6048 batches

Disposal of substandard filling 1545 batches

Move to mixing room 1514 batches

Set up mincer 8017 batches

Weigh and sort ingredients 8017 batches

Load mincer 47183 kilograms

Operate mincer 15303 batches

Unload and Clean mincer 8017 batches

Move to filling room 8749 batches

Set up pastry cases 4374 batches

Stack cases on filling machine 8017 batches

Load hopper 16034 batches

Fill pastry cases 56470 kilograms

Clean hopper 8749 batches

Move to baking 3830 kilograms

Stack cases on baking trays 6854 products

Setup ovens 2512 trays

Move to ovens 1386 trays

Bake products 17153 trays

Unload oven 1398 trays

Inspect finished products 1176 trays

Disposal of substandard

product 599 trays

Move to truck 1713 Finished trays

Direct Materials 2

per kilogram

Assigned directly to products

Current Market Selling Price 12 per unit of product

Batch size 300

Annual Volume 15000

* All Calculations to 4 decimal

places

Total Indirect cost 344773.0326

Per unit Cost 23.0

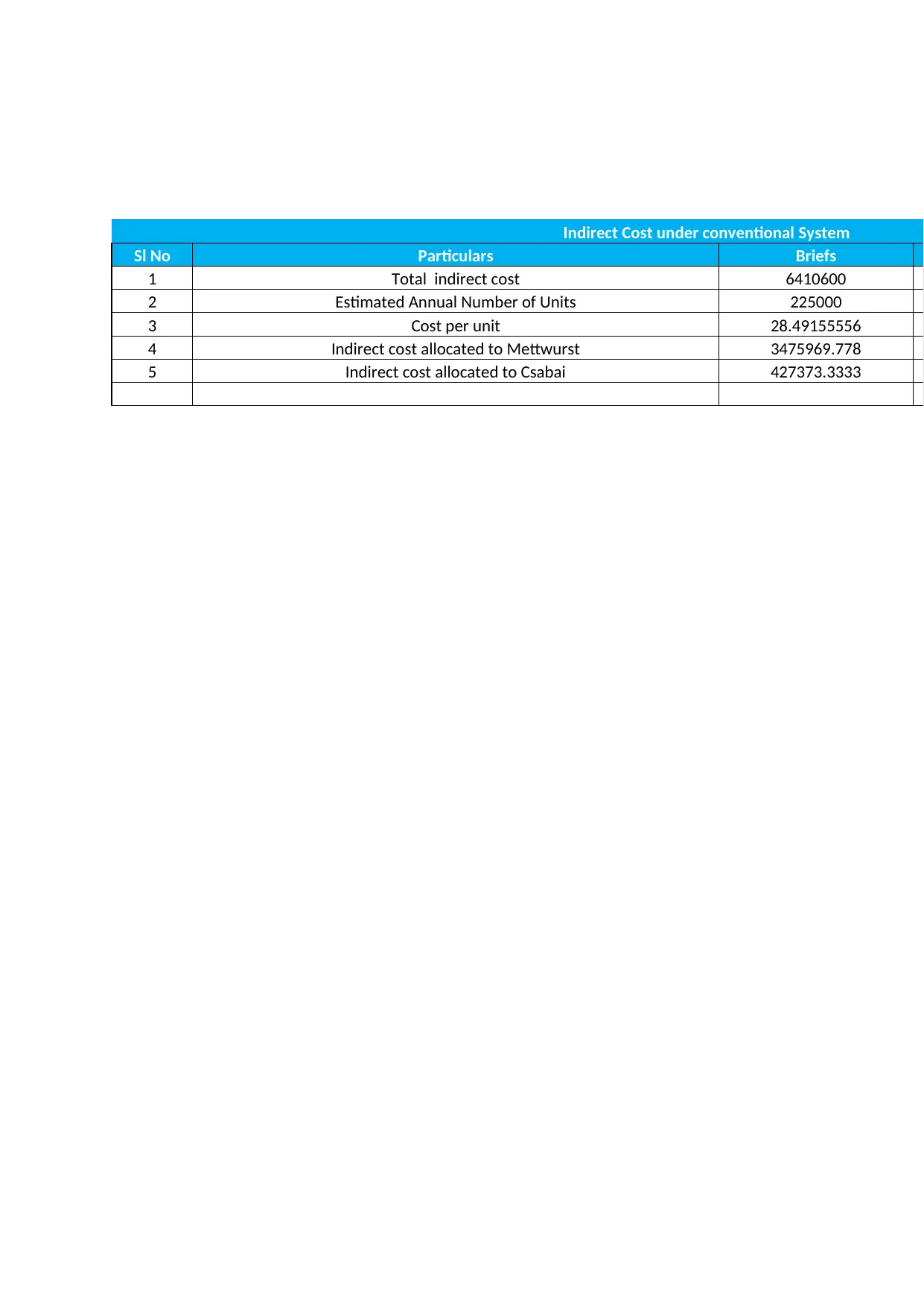

Indirect Cost under conventional System

Sl No Particulars Briefs

1 Total indirect cost 6410600

2 Estimated Annual Number of Units 225000

3 Cost per unit 28.49155556

4 Indirect cost allocated to Mettwurst 3475969.778

5 Indirect cost allocated to Csabai 427373.3333

Sl No Particulars Briefs

1 Total indirect cost 6410600

2 Estimated Annual Number of Units 225000

3 Cost per unit 28.49155556

4 Indirect cost allocated to Mettwurst 3475969.778

5 Indirect cost allocated to Csabai 427373.3333

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Answer 5

On perusal of the above tables, there has been significant difference in

indirect cost allocation under the two methods.

Answer 6

It overstates the cost of both the products based on computation

presented above.

Answer 7

The changes that have occurred in cost majorly be due to the following:

(a) Wages on account of increased production, new employees would

have been recruited;

(b) Building Cost: Additional floor space must have been required to meet

with the increased demand and production capacity;

(c) Energy: Due to increased production increased electricity

consumption;

(d) Others: Must have increased;

(e) Direct cost.

Answer 8 & 9

Absorption Costing is a costing technique that is used for the valuation for

inventory. This technique includes all the cost of material and labour and

also consider the fixed and variable overhead inventory cost. This is also

known as full costing technique for computing the cost of product. The

components which are included in the absorption costing method are

direct material cost, direct labour cost, variable manufacturing overhead

and fixed manufacturing overhead of the product. Under this technique

the variable and fixed selling and administrative expenses are considered

to be the period cost and are included in the same period in which they

are incurred. (CFI Education Inc., 2019).This method is mainly used for the

purpose of external reporting and income tax filing purpose. For Example

if laptop company HP used full absorption costing method to value the

inventory of their HP, the stock valuation would consider the materials

used to manufacture the HP laptop, the wages which are paid to the

worker to manufacture the laptop, the manufacturing overhead as the

other fixed overhead which are to be included for the manufacture of

laptop. (MyAccountingCourse.com , 2019)

Few Advantages of Absorption Costing

1) Absorption Costing takes into account fixed overhead cost also in

the computation of product cost and form part of the unit cost of

On perusal of the above tables, there has been significant difference in

indirect cost allocation under the two methods.

Answer 6

It overstates the cost of both the products based on computation

presented above.

Answer 7

The changes that have occurred in cost majorly be due to the following:

(a) Wages on account of increased production, new employees would

have been recruited;

(b) Building Cost: Additional floor space must have been required to meet

with the increased demand and production capacity;

(c) Energy: Due to increased production increased electricity

consumption;

(d) Others: Must have increased;

(e) Direct cost.

Answer 8 & 9

Absorption Costing is a costing technique that is used for the valuation for

inventory. This technique includes all the cost of material and labour and

also consider the fixed and variable overhead inventory cost. This is also

known as full costing technique for computing the cost of product. The

components which are included in the absorption costing method are

direct material cost, direct labour cost, variable manufacturing overhead

and fixed manufacturing overhead of the product. Under this technique

the variable and fixed selling and administrative expenses are considered

to be the period cost and are included in the same period in which they

are incurred. (CFI Education Inc., 2019).This method is mainly used for the

purpose of external reporting and income tax filing purpose. For Example

if laptop company HP used full absorption costing method to value the

inventory of their HP, the stock valuation would consider the materials

used to manufacture the HP laptop, the wages which are paid to the

worker to manufacture the laptop, the manufacturing overhead as the

other fixed overhead which are to be included for the manufacture of

laptop. (MyAccountingCourse.com , 2019)

Few Advantages of Absorption Costing

1) Absorption Costing takes into account fixed overhead cost also in

the computation of product cost and form part of the unit cost of

production ,which shows the more realistic and accurate cost of the

product per unit.

2) This cost is the most suitable and accurate form of costing for the

preparation of accounts. This is generally accepted under the

principles of Generally Accepted Accounting Principles (GAAP).The

main advantage point in this under absorption costing is that the

stocks are not under valued under this particular costing system as

this the costing technique under which the stock amount also

include the fixed manufacturing overhead which are incurred during

the production process. ( Accounting For Management, 2019)

3) Under this costing technique it shows a decreased value of the cost

of sales and the increase revenue for the organization .As the

formula involved for the computation purpose is “Opening

Stock+Purchase-Closing Stock”, the stock which has been remained

at the end of the year generally has a higher value as generally

reported under the marginal costing system. ( Accounting For

Management, 2019)

4) For smaller companies it is very much beneficial .As it makes the

calculation very much easy for the small companies .It becomes

very easy for the small business to compute the value of product

easily by taking into account fixed overhead too as part of the

product value and sell their products in a more realistic price and

earn profit. ( Accounting For Management, 2019)

5) It is also very helpful for the business who have a stagnant demand

for the product throughout the year.

Few Dis advantages Of Absorption Costing

1) This costing technique cannot be used as an efficient tool to

compute the profitability of the company, because this costing

technique includes the fixed cost of the overhead irrespective of the

volume of production. ( Accounting For Management, 2019)

2) As this costing technique includes both fixed and overhead cost of

product, so the management of the company cannot consider this

technique for the purpose of decision making purpose or for

budgeting or forecasting purpose.

3) Absorption costing technique makes the outlook of the company

look more good as the fixed cost form part of the product cost so

this procedure can be easily used to manipulate the profit of the

company and increase the practice of ‘creative accounting’.

( Accounting For Management, 2019)

product per unit.

2) This cost is the most suitable and accurate form of costing for the

preparation of accounts. This is generally accepted under the

principles of Generally Accepted Accounting Principles (GAAP).The

main advantage point in this under absorption costing is that the

stocks are not under valued under this particular costing system as

this the costing technique under which the stock amount also

include the fixed manufacturing overhead which are incurred during

the production process. ( Accounting For Management, 2019)

3) Under this costing technique it shows a decreased value of the cost

of sales and the increase revenue for the organization .As the

formula involved for the computation purpose is “Opening

Stock+Purchase-Closing Stock”, the stock which has been remained

at the end of the year generally has a higher value as generally

reported under the marginal costing system. ( Accounting For

Management, 2019)

4) For smaller companies it is very much beneficial .As it makes the

calculation very much easy for the small companies .It becomes

very easy for the small business to compute the value of product

easily by taking into account fixed overhead too as part of the

product value and sell their products in a more realistic price and

earn profit. ( Accounting For Management, 2019)

5) It is also very helpful for the business who have a stagnant demand

for the product throughout the year.

Few Dis advantages Of Absorption Costing

1) This costing technique cannot be used as an efficient tool to

compute the profitability of the company, because this costing

technique includes the fixed cost of the overhead irrespective of the

volume of production. ( Accounting For Management, 2019)

2) As this costing technique includes both fixed and overhead cost of

product, so the management of the company cannot consider this

technique for the purpose of decision making purpose or for

budgeting or forecasting purpose.

3) Absorption costing technique makes the outlook of the company

look more good as the fixed cost form part of the product cost so

this procedure can be easily used to manipulate the profit of the

company and increase the practice of ‘creative accounting’.

( Accounting For Management, 2019)

Activity based costing is a managerial based accounting that allocate all

the overhead cost incurred to the activities .In a simple definition it is a

way to allocate all the indirect cost to the products .

( MyAccountingCourse.com, 2019)

Few Advantages of Activity Based Costing (ABC)

The advantages of ABC are discussed here in below:

1) Accurate Product Cost: This ABC costing provides more accurate

and reliable method to determine the product cost .In the

manufacturing process where overhead constitute a large portion of

the total product cost, than this technique provides a more realistic

and more accurate product cost. In this costing technique the

product cost arrived at is more reliable and efficient as compare to

the traditional costing approach which brings more error in the

computation of the product cost per unit. (Agarwal, 2018)

2) Information about Cost Behaviour: ABC identifies the real

nature of the cost and particularly identify the cost which is not

adding any value to the product. Through this technique manager

will control the excess cost involved in any product. (Agarwal, 2018)

3) Tracing of Overhead Cost: ABC discover cost were it is assigned

in the areas of managerial responsibility, processes, customers and

various departments involved. (Agarwal, 2018)

4) Better decision making: Through this costing technique the

mangers can make more reliable and accurate decision. It is also

helpful in fixing the cost of the product more accurately and

properly as more proper and correct data is readily available.

5) Cost Management: Through the absorption costing technique cost

driver rates can be easily accessible which is very much useful for

the management for designing a new product or the existing

product. (Agarwal, 2018)

6) Benefits to Service industry: Many service organizations like

banking sector, hospital sector, government department sector

have totally different characteristics as compared to manufacturing

firm of the organization. In the service organization no, direct cost is

involved. All the cost which is incurred is generally indirect in nature

and the costs are overhead cost and any stock of service is also not

kept, as it is consumed immediately. This traditional costing

approach iOS considered to be inappropriate for these types of

organizations whereas the ABC costing approach offers varied types

of benefits and helpful for the management in the decision-making

purpose.

the overhead cost incurred to the activities .In a simple definition it is a

way to allocate all the indirect cost to the products .

( MyAccountingCourse.com, 2019)

Few Advantages of Activity Based Costing (ABC)

The advantages of ABC are discussed here in below:

1) Accurate Product Cost: This ABC costing provides more accurate

and reliable method to determine the product cost .In the

manufacturing process where overhead constitute a large portion of

the total product cost, than this technique provides a more realistic

and more accurate product cost. In this costing technique the

product cost arrived at is more reliable and efficient as compare to

the traditional costing approach which brings more error in the

computation of the product cost per unit. (Agarwal, 2018)

2) Information about Cost Behaviour: ABC identifies the real

nature of the cost and particularly identify the cost which is not

adding any value to the product. Through this technique manager

will control the excess cost involved in any product. (Agarwal, 2018)

3) Tracing of Overhead Cost: ABC discover cost were it is assigned

in the areas of managerial responsibility, processes, customers and

various departments involved. (Agarwal, 2018)

4) Better decision making: Through this costing technique the

mangers can make more reliable and accurate decision. It is also

helpful in fixing the cost of the product more accurately and

properly as more proper and correct data is readily available.

5) Cost Management: Through the absorption costing technique cost

driver rates can be easily accessible which is very much useful for

the management for designing a new product or the existing

product. (Agarwal, 2018)

6) Benefits to Service industry: Many service organizations like

banking sector, hospital sector, government department sector

have totally different characteristics as compared to manufacturing

firm of the organization. In the service organization no, direct cost is

involved. All the cost which is incurred is generally indirect in nature

and the costs are overhead cost and any stock of service is also not

kept, as it is consumed immediately. This traditional costing

approach iOS considered to be inappropriate for these types of

organizations whereas the ABC costing approach offers varied types

of benefits and helpful for the management in the decision-making

purpose.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Few Dis advantages Of Activity Based Costing

1) Expensive and Complex type of Costing Approach: This

costing technique has many cost pools and multiple cost driver and

is also more complex type of costing compared to other type of

costing. (Agarwal, 2018)

2) Drivers Selection: Sometimes difficulties also arise in the selection

of cost drivers, common cost assignment.

3) Disadvantage to smaller firms: ABC has a level of difficulty as

the larger manufacturing firm can use it more usefully compared to

the smaller firm. Activity Based Costing also has different level of

benefits for the different types of organizations such as benefit of

ABC is more useful for the larger organizations as compared to the

smaller firm .The smaller firm cannot go ABC approach as it is very

much complex process to get into and the cost involved is also very

huge ,making it costly for the smaller firm to sustain with ABC

costing approach. While the bigger manufacturing companies can

easily opt for it due to involvement of large manufacturing overhead

cost and large scale of operations which make it easier for the them

to use and allocate the indirect cost on the basis of various cost

driver.

4) Difficulties in Measurement: The main issue in the ABC system

are the necessary measurement which is useful in order to

implement it. (Agarwal, 2018).ABC costing system is very costly as

the management of the company need to determine a particular

cost of goods and services by going through many complicated

calculations .It is also very costly because the drivers cost need to

be updated regularly on a permanent basis.

References

Accounting For Management, 2019. Advantages and disadvantages of absorption costing. [Online]

Available at: https://www.accountingformanagement.org/advantages-and-disadvantages-of-absorpt

[Accessed 19 May 2019].

MyAccountingCourse.com, 2019. What is Activity Based Costing (ABC)?. [Online]

Available at: https://www.myaccountingcourse.com/accounting-dictionary/activity-based-costing

[Accessed 19 May 2019].

Agarwal, R., 2018. Advantages and Demerits of Activity Based Costing (ABC). [Online]

Available at: http://www.yourarticlelibrary.com/accounting/costing/advantages-and-demerits-of-

activity-based-co

[Accessed 19 May 2019].

1) Expensive and Complex type of Costing Approach: This

costing technique has many cost pools and multiple cost driver and

is also more complex type of costing compared to other type of

costing. (Agarwal, 2018)

2) Drivers Selection: Sometimes difficulties also arise in the selection

of cost drivers, common cost assignment.

3) Disadvantage to smaller firms: ABC has a level of difficulty as

the larger manufacturing firm can use it more usefully compared to

the smaller firm. Activity Based Costing also has different level of

benefits for the different types of organizations such as benefit of

ABC is more useful for the larger organizations as compared to the

smaller firm .The smaller firm cannot go ABC approach as it is very

much complex process to get into and the cost involved is also very

huge ,making it costly for the smaller firm to sustain with ABC

costing approach. While the bigger manufacturing companies can

easily opt for it due to involvement of large manufacturing overhead

cost and large scale of operations which make it easier for the them

to use and allocate the indirect cost on the basis of various cost

driver.

4) Difficulties in Measurement: The main issue in the ABC system

are the necessary measurement which is useful in order to

implement it. (Agarwal, 2018).ABC costing system is very costly as

the management of the company need to determine a particular

cost of goods and services by going through many complicated

calculations .It is also very costly because the drivers cost need to

be updated regularly on a permanent basis.

References

Accounting For Management, 2019. Advantages and disadvantages of absorption costing. [Online]

Available at: https://www.accountingformanagement.org/advantages-and-disadvantages-of-absorpt

[Accessed 19 May 2019].

MyAccountingCourse.com, 2019. What is Activity Based Costing (ABC)?. [Online]

Available at: https://www.myaccountingcourse.com/accounting-dictionary/activity-based-costing

[Accessed 19 May 2019].

Agarwal, R., 2018. Advantages and Demerits of Activity Based Costing (ABC). [Online]

Available at: http://www.yourarticlelibrary.com/accounting/costing/advantages-and-demerits-of-

activity-based-co

[Accessed 19 May 2019].

CFI Education Inc., 2019. Absorption Costing. [Online]

Available at: https://corporatefinanceinstitute.com/resources/knowledge/accounting/absorption-

costing-guide/

[Accessed 18 May 2019].

MyAccountingCourse.com , 2019. What is Absorption Costing?. [Online]

Available at: https://www.myaccountingcourse.com/accounting-dictionary/absorption-costing

[Accessed 19 May 2019].

Available at: https://corporatefinanceinstitute.com/resources/knowledge/accounting/absorption-

costing-guide/

[Accessed 18 May 2019].

MyAccountingCourse.com , 2019. What is Absorption Costing?. [Online]

Available at: https://www.myaccountingcourse.com/accounting-dictionary/absorption-costing

[Accessed 19 May 2019].

1 out of 12

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.