University Statistics Report: Stock Market Analysis, Risk, and CAPM

VerifiedAdded on 2020/03/16

|13

|1932

|52

Report

AI Summary

This report provides a statistical analysis of four different stocks, aiming to compare their volatility and risk. The analysis utilizes data from Yahoo Finance spanning from December 2010 to May 2016. The methodology includes descriptive statistics (mean, median, standard deviation), time series plots, and hypothesis testing. The report tests hypotheses related to average returns, risk comparisons (using F-statistics), and CAPM estimation through linear regression. Normality tests are performed using Jarque-Bera and Shapiro-Wilk tests. The report concludes with the estimation of CAPM, confidence interval to test neutrality of stock, and testing the normality of the error term. The analysis provides insights into the performance, risk profiles, and relationships of the stocks, contributing to a better understanding of financial analysis and stock market dynamics.

Statistics

Name

University

6th October 2017

Name

University

6th October 2017

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction......................................................................................................................................3

Methodology....................................................................................................................................3

Descriptive statistics........................................................................................................................4

Summary statistics.......................................................................................................................4

Time series plots..........................................................................................................................4

Hypothesis Test...............................................................................................................................7

Testing whether the average return on Boeing stock is at least 3%.............................................7

Comparison of risk associated with stocks..................................................................................8

Comparison of average returns....................................................................................................9

Estimating the CAPM using linear regression...........................................................................10

Confidence interval to test neutrality of stock...........................................................................11

Testing normality of error term..................................................................................................12

References......................................................................................................................................14

Introduction......................................................................................................................................3

Methodology....................................................................................................................................3

Descriptive statistics........................................................................................................................4

Summary statistics.......................................................................................................................4

Time series plots..........................................................................................................................4

Hypothesis Test...............................................................................................................................7

Testing whether the average return on Boeing stock is at least 3%.............................................7

Comparison of risk associated with stocks..................................................................................8

Comparison of average returns....................................................................................................9

Estimating the CAPM using linear regression...........................................................................10

Confidence interval to test neutrality of stock...........................................................................11

Testing normality of error term..................................................................................................12

References......................................................................................................................................14

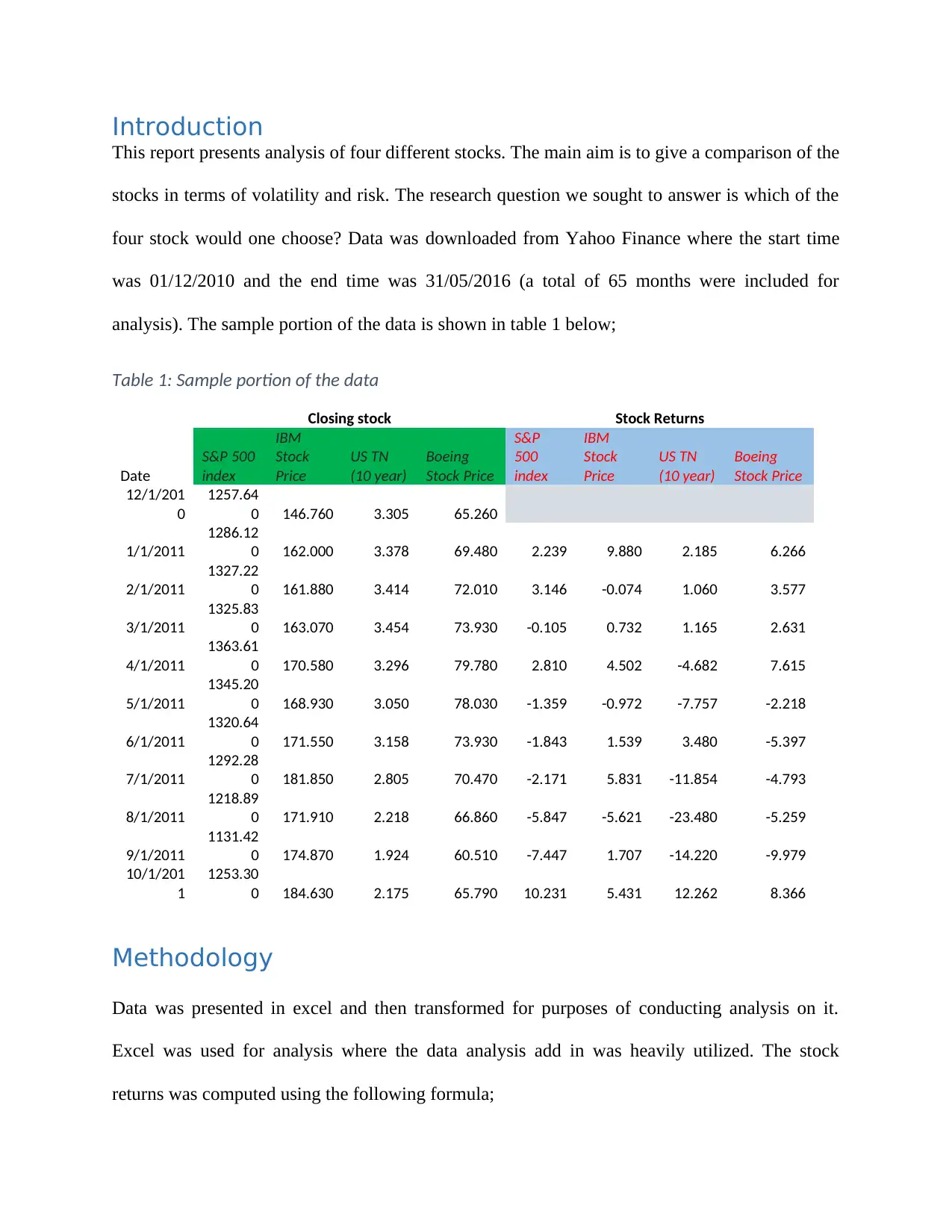

Introduction

This report presents analysis of four different stocks. The main aim is to give a comparison of the

stocks in terms of volatility and risk. The research question we sought to answer is which of the

four stock would one choose? Data was downloaded from Yahoo Finance where the start time

was 01/12/2010 and the end time was 31/05/2016 (a total of 65 months were included for

analysis). The sample portion of the data is shown in table 1 below;

Table 1: Sample portion of the data

Closing stock Stock Returns

Date

S&P 500

index

IBM

Stock

Price

US TN

(10 year)

Boeing

Stock Price

S&P

500

index

IBM

Stock

Price

US TN

(10 year)

Boeing

Stock Price

12/1/201

0

1257.64

0 146.760 3.305 65.260

1/1/2011

1286.12

0 162.000 3.378 69.480 2.239 9.880 2.185 6.266

2/1/2011

1327.22

0 161.880 3.414 72.010 3.146 -0.074 1.060 3.577

3/1/2011

1325.83

0 163.070 3.454 73.930 -0.105 0.732 1.165 2.631

4/1/2011

1363.61

0 170.580 3.296 79.780 2.810 4.502 -4.682 7.615

5/1/2011

1345.20

0 168.930 3.050 78.030 -1.359 -0.972 -7.757 -2.218

6/1/2011

1320.64

0 171.550 3.158 73.930 -1.843 1.539 3.480 -5.397

7/1/2011

1292.28

0 181.850 2.805 70.470 -2.171 5.831 -11.854 -4.793

8/1/2011

1218.89

0 171.910 2.218 66.860 -5.847 -5.621 -23.480 -5.259

9/1/2011

1131.42

0 174.870 1.924 60.510 -7.447 1.707 -14.220 -9.979

10/1/201

1

1253.30

0 184.630 2.175 65.790 10.231 5.431 12.262 8.366

Methodology

Data was presented in excel and then transformed for purposes of conducting analysis on it.

Excel was used for analysis where the data analysis add in was heavily utilized. The stock

returns was computed using the following formula;

This report presents analysis of four different stocks. The main aim is to give a comparison of the

stocks in terms of volatility and risk. The research question we sought to answer is which of the

four stock would one choose? Data was downloaded from Yahoo Finance where the start time

was 01/12/2010 and the end time was 31/05/2016 (a total of 65 months were included for

analysis). The sample portion of the data is shown in table 1 below;

Table 1: Sample portion of the data

Closing stock Stock Returns

Date

S&P 500

index

IBM

Stock

Price

US TN

(10 year)

Boeing

Stock Price

S&P

500

index

IBM

Stock

Price

US TN

(10 year)

Boeing

Stock Price

12/1/201

0

1257.64

0 146.760 3.305 65.260

1/1/2011

1286.12

0 162.000 3.378 69.480 2.239 9.880 2.185 6.266

2/1/2011

1327.22

0 161.880 3.414 72.010 3.146 -0.074 1.060 3.577

3/1/2011

1325.83

0 163.070 3.454 73.930 -0.105 0.732 1.165 2.631

4/1/2011

1363.61

0 170.580 3.296 79.780 2.810 4.502 -4.682 7.615

5/1/2011

1345.20

0 168.930 3.050 78.030 -1.359 -0.972 -7.757 -2.218

6/1/2011

1320.64

0 171.550 3.158 73.930 -1.843 1.539 3.480 -5.397

7/1/2011

1292.28

0 181.850 2.805 70.470 -2.171 5.831 -11.854 -4.793

8/1/2011

1218.89

0 171.910 2.218 66.860 -5.847 -5.621 -23.480 -5.259

9/1/2011

1131.42

0 174.870 1.924 60.510 -7.447 1.707 -14.220 -9.979

10/1/201

1

1253.30

0 184.630 2.175 65.790 10.231 5.431 12.262 8.366

Methodology

Data was presented in excel and then transformed for purposes of conducting analysis on it.

Excel was used for analysis where the data analysis add in was heavily utilized. The stock

returns was computed using the following formula;

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

rt =100 ln [ Pt

Pt−1 ]

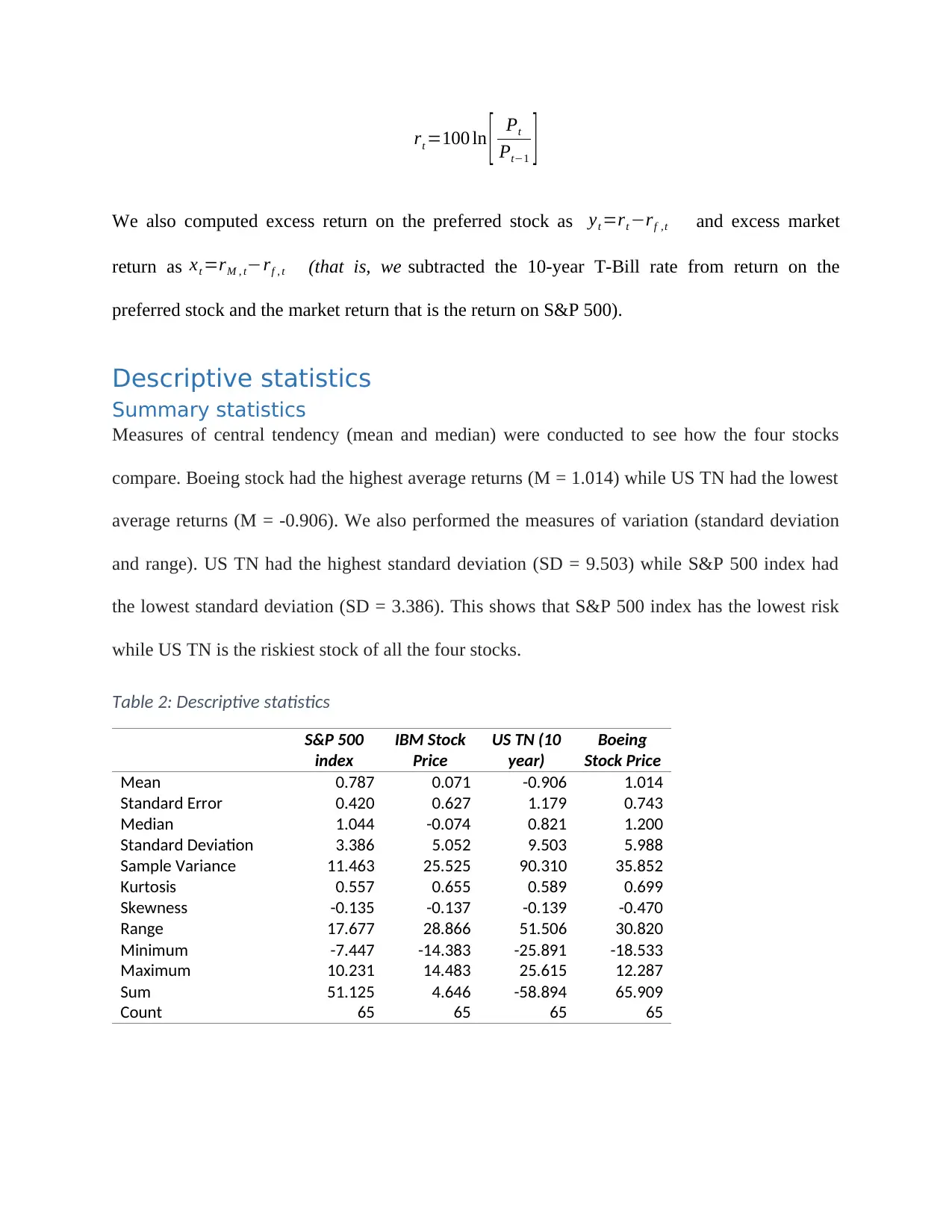

We also computed excess return on the preferred stock as yt =rt −rf ,t and excess market

return as xt =rM , t−rf , t (that is, we subtracted the 10-year T-Bill rate from return on the

preferred stock and the market return that is the return on S&P 500).

Descriptive statistics

Summary statistics

Measures of central tendency (mean and median) were conducted to see how the four stocks

compare. Boeing stock had the highest average returns (M = 1.014) while US TN had the lowest

average returns (M = -0.906). We also performed the measures of variation (standard deviation

and range). US TN had the highest standard deviation (SD = 9.503) while S&P 500 index had

the lowest standard deviation (SD = 3.386). This shows that S&P 500 index has the lowest risk

while US TN is the riskiest stock of all the four stocks.

Table 2: Descriptive statistics

S&P 500

index

IBM Stock

Price

US TN (10

year)

Boeing

Stock Price

Mean 0.787 0.071 -0.906 1.014

Standard Error 0.420 0.627 1.179 0.743

Median 1.044 -0.074 0.821 1.200

Standard Deviation 3.386 5.052 9.503 5.988

Sample Variance 11.463 25.525 90.310 35.852

Kurtosis 0.557 0.655 0.589 0.699

Skewness -0.135 -0.137 -0.139 -0.470

Range 17.677 28.866 51.506 30.820

Minimum -7.447 -14.383 -25.891 -18.533

Maximum 10.231 14.483 25.615 12.287

Sum 51.125 4.646 -58.894 65.909

Count 65 65 65 65

Pt−1 ]

We also computed excess return on the preferred stock as yt =rt −rf ,t and excess market

return as xt =rM , t−rf , t (that is, we subtracted the 10-year T-Bill rate from return on the

preferred stock and the market return that is the return on S&P 500).

Descriptive statistics

Summary statistics

Measures of central tendency (mean and median) were conducted to see how the four stocks

compare. Boeing stock had the highest average returns (M = 1.014) while US TN had the lowest

average returns (M = -0.906). We also performed the measures of variation (standard deviation

and range). US TN had the highest standard deviation (SD = 9.503) while S&P 500 index had

the lowest standard deviation (SD = 3.386). This shows that S&P 500 index has the lowest risk

while US TN is the riskiest stock of all the four stocks.

Table 2: Descriptive statistics

S&P 500

index

IBM Stock

Price

US TN (10

year)

Boeing

Stock Price

Mean 0.787 0.071 -0.906 1.014

Standard Error 0.420 0.627 1.179 0.743

Median 1.044 -0.074 0.821 1.200

Standard Deviation 3.386 5.052 9.503 5.988

Sample Variance 11.463 25.525 90.310 35.852

Kurtosis 0.557 0.655 0.589 0.699

Skewness -0.135 -0.137 -0.139 -0.470

Range 17.677 28.866 51.506 30.820

Minimum -7.447 -14.383 -25.891 -18.533

Maximum 10.231 14.483 25.615 12.287

Sum 51.125 4.646 -58.894 65.909

Count 65 65 65 65

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

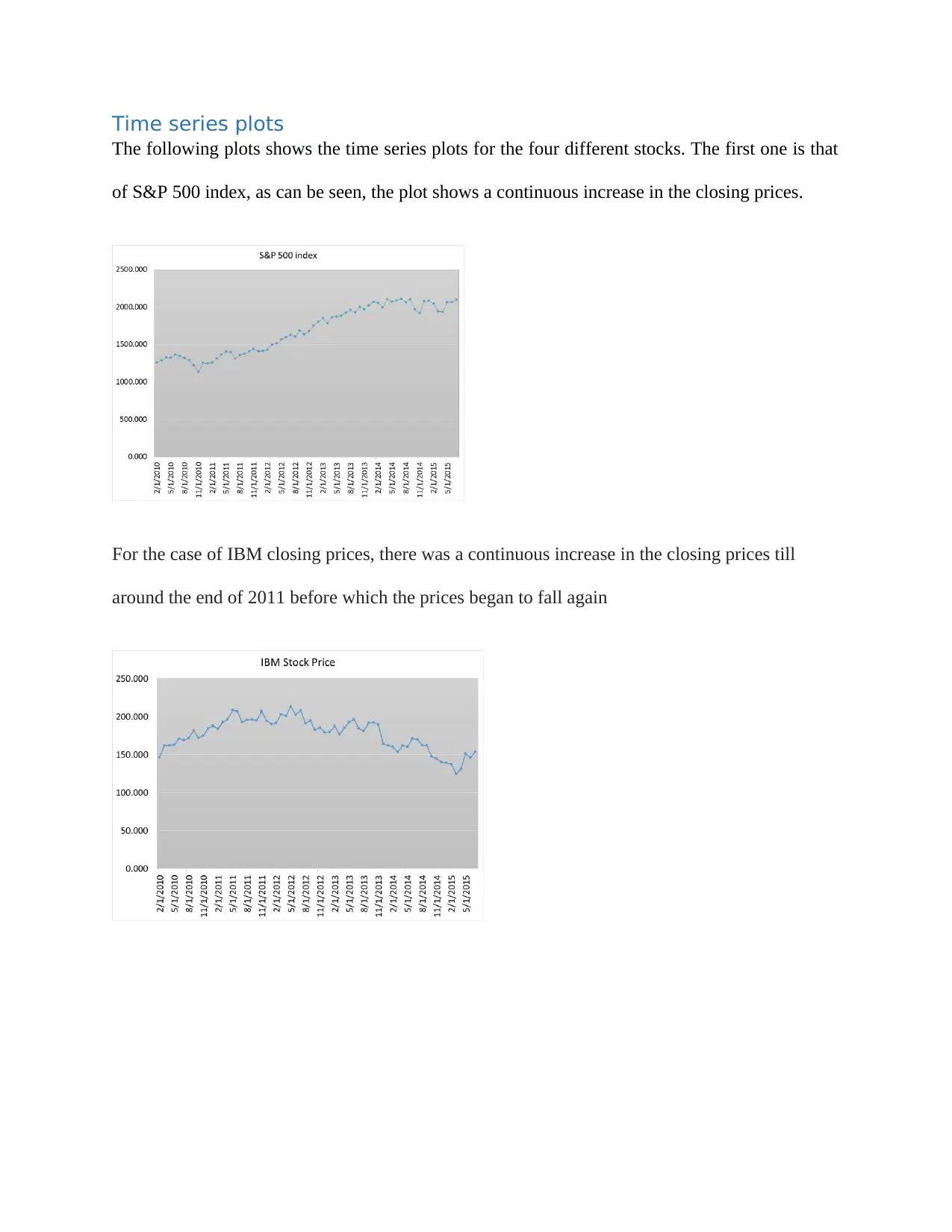

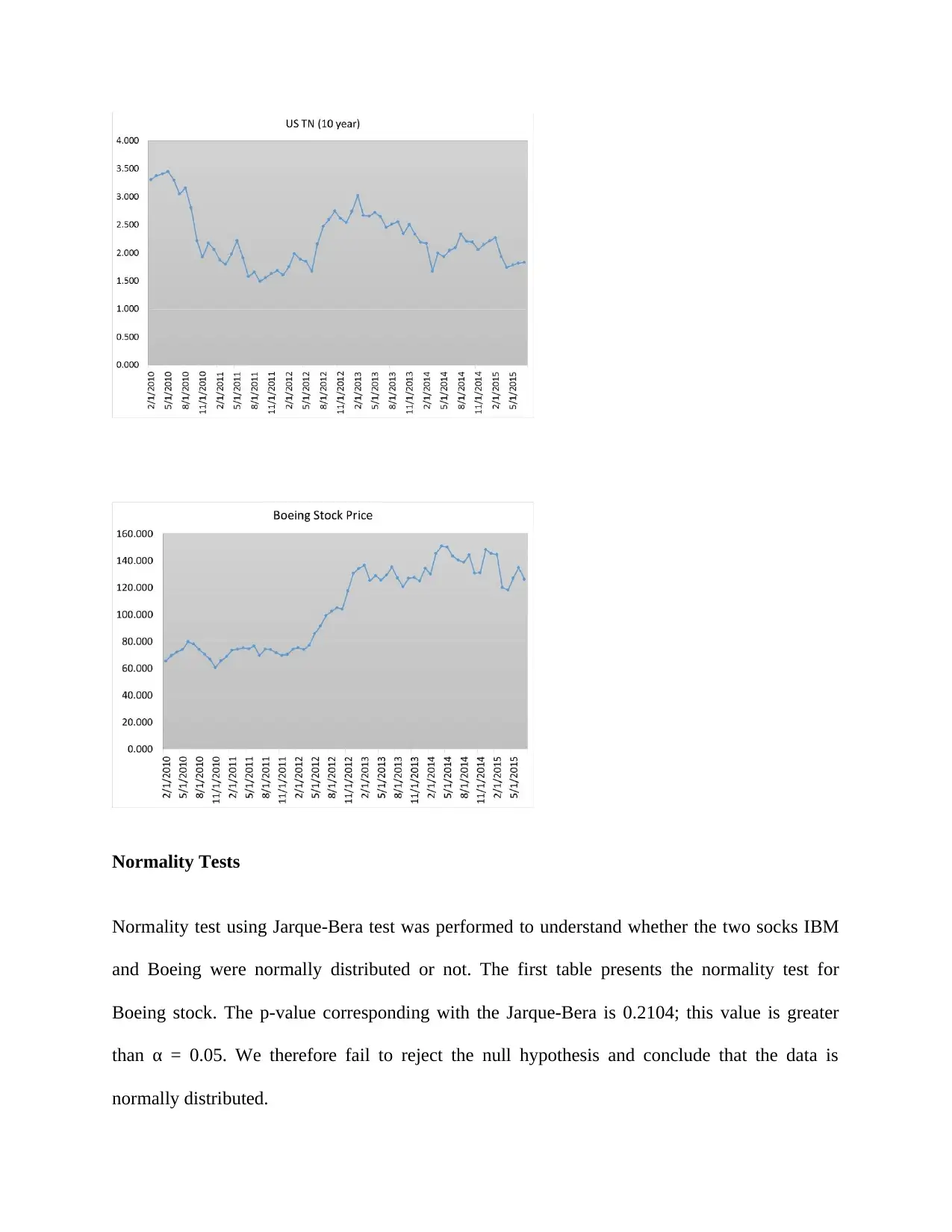

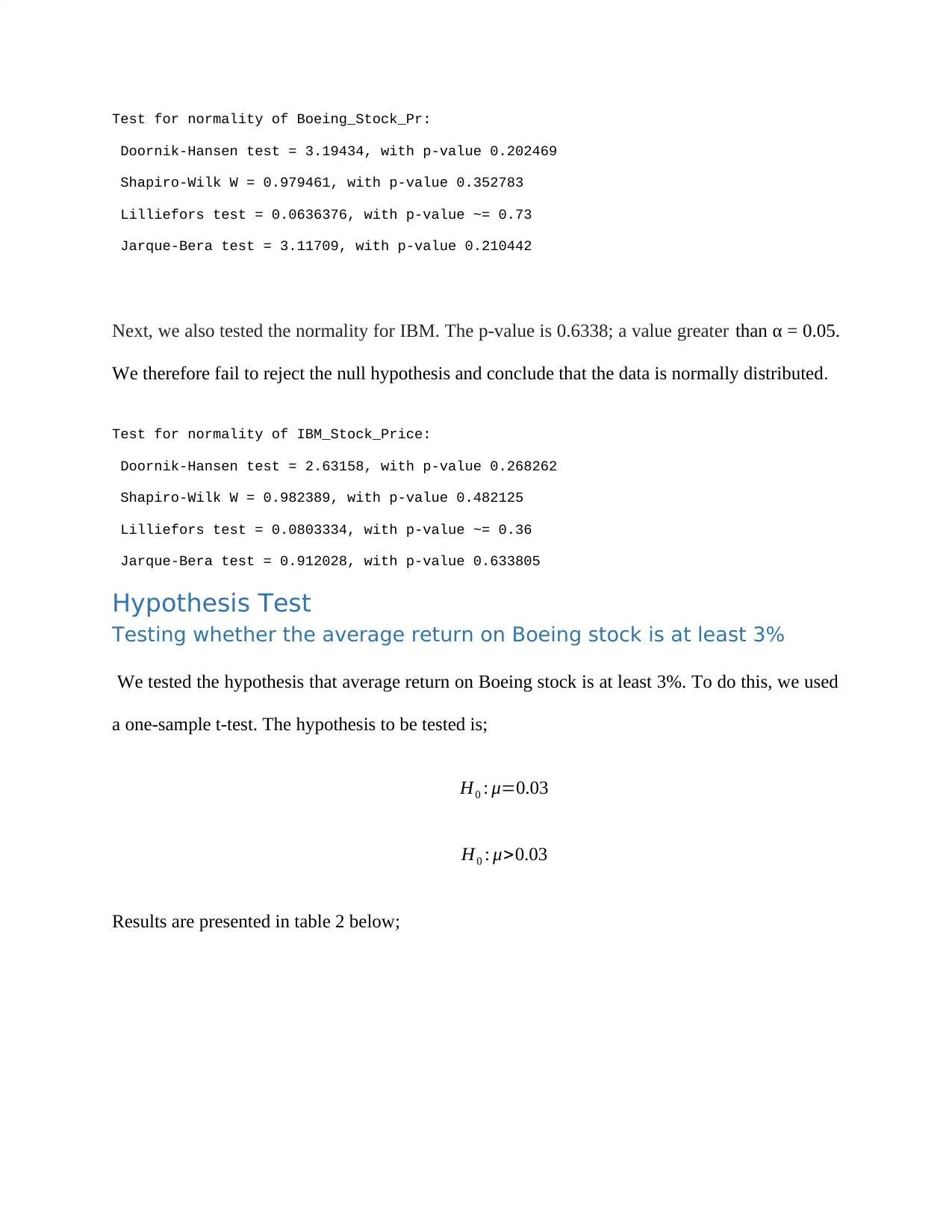

Time series plots

The following plots shows the time series plots for the four different stocks. The first one is that

of S&P 500 index, as can be seen, the plot shows a continuous increase in the closing prices.

For the case of IBM closing prices, there was a continuous increase in the closing prices till

around the end of 2011 before which the prices began to fall again

The following plots shows the time series plots for the four different stocks. The first one is that

of S&P 500 index, as can be seen, the plot shows a continuous increase in the closing prices.

For the case of IBM closing prices, there was a continuous increase in the closing prices till

around the end of 2011 before which the prices began to fall again

Normality Tests

Normality test using Jarque-Bera test was performed to understand whether the two socks IBM

and Boeing were normally distributed or not. The first table presents the normality test for

Boeing stock. The p-value corresponding with the Jarque-Bera is 0.2104; this value is greater

than α = 0.05. We therefore fail to reject the null hypothesis and conclude that the data is

normally distributed.

Normality test using Jarque-Bera test was performed to understand whether the two socks IBM

and Boeing were normally distributed or not. The first table presents the normality test for

Boeing stock. The p-value corresponding with the Jarque-Bera is 0.2104; this value is greater

than α = 0.05. We therefore fail to reject the null hypothesis and conclude that the data is

normally distributed.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Test for normality of Boeing_Stock_Pr:

Doornik-Hansen test = 3.19434, with p-value 0.202469

Shapiro-Wilk W = 0.979461, with p-value 0.352783

Lilliefors test = 0.0636376, with p-value ~= 0.73

Jarque-Bera test = 3.11709, with p-value 0.210442

Next, we also tested the normality for IBM. The p-value is 0.6338; a value greater than α = 0.05.

We therefore fail to reject the null hypothesis and conclude that the data is normally distributed.

Test for normality of IBM_Stock_Price:

Doornik-Hansen test = 2.63158, with p-value 0.268262

Shapiro-Wilk W = 0.982389, with p-value 0.482125

Lilliefors test = 0.0803334, with p-value ~= 0.36

Jarque-Bera test = 0.912028, with p-value 0.633805

Hypothesis Test

Testing whether the average return on Boeing stock is at least 3%

We tested the hypothesis that average return on Boeing stock is at least 3%. To do this, we used

a one-sample t-test. The hypothesis to be tested is;

H0 : μ=0.03

H0 : μ>0.03

Results are presented in table 2 below;

Doornik-Hansen test = 3.19434, with p-value 0.202469

Shapiro-Wilk W = 0.979461, with p-value 0.352783

Lilliefors test = 0.0636376, with p-value ~= 0.73

Jarque-Bera test = 3.11709, with p-value 0.210442

Next, we also tested the normality for IBM. The p-value is 0.6338; a value greater than α = 0.05.

We therefore fail to reject the null hypothesis and conclude that the data is normally distributed.

Test for normality of IBM_Stock_Price:

Doornik-Hansen test = 2.63158, with p-value 0.268262

Shapiro-Wilk W = 0.982389, with p-value 0.482125

Lilliefors test = 0.0803334, with p-value ~= 0.36

Jarque-Bera test = 0.912028, with p-value 0.633805

Hypothesis Test

Testing whether the average return on Boeing stock is at least 3%

We tested the hypothesis that average return on Boeing stock is at least 3%. To do this, we used

a one-sample t-test. The hypothesis to be tested is;

H0 : μ=0.03

H0 : μ>0.03

Results are presented in table 2 below;

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table 3: T-test of Boeing Stock price

Pr(T < t) = 0.9050 Pr(|T| > |t|) = 0.1899 Pr(T > t) = 0.0950

Ha: mean < 0.03 Ha: mean != 0.03 Ha: mean > 0.03

Ho: mean = 0.03 degrees of freedom = 64

mean = mean(x) t = 1.3249

x 65 1.013988 .7426766 5.98765 -.4696789 2.497655

Obs Mean Std. Err. Std. Dev. [95% Conf. Interval]

One-sample t test

. ttesti 65 1.0139882602 5.98765037 0.03

Table 4 above gives the one-sample t-test where we sought to test whether the average return on

Boeing stock is at least 3% , we observe the p-value to be 0.0950 (a value greater than 5% level

of significance), hence we fail to reject the null hypothesis and conclude that the average return

on Boeing is not significantly greater than 3%.

Comparison of risk associated with stocks

To compare the risk associated with the two stocks (Boeing and IBM). To compare them, we

used F-statistics as follows;

25.525493 90.309611 35.851957

25.525 90.310 35.85195694

n1=65 , s1

2 =35.85195694 , n2=65 , s2

2=25.525493

H0 :s1

2 /s2

2=1

Ha :s1

2 /s2

2 ≠ 1

Pr(T < t) = 0.9050 Pr(|T| > |t|) = 0.1899 Pr(T > t) = 0.0950

Ha: mean < 0.03 Ha: mean != 0.03 Ha: mean > 0.03

Ho: mean = 0.03 degrees of freedom = 64

mean = mean(x) t = 1.3249

x 65 1.013988 .7426766 5.98765 -.4696789 2.497655

Obs Mean Std. Err. Std. Dev. [95% Conf. Interval]

One-sample t test

. ttesti 65 1.0139882602 5.98765037 0.03

Table 4 above gives the one-sample t-test where we sought to test whether the average return on

Boeing stock is at least 3% , we observe the p-value to be 0.0950 (a value greater than 5% level

of significance), hence we fail to reject the null hypothesis and conclude that the average return

on Boeing is not significantly greater than 3%.

Comparison of risk associated with stocks

To compare the risk associated with the two stocks (Boeing and IBM). To compare them, we

used F-statistics as follows;

25.525493 90.309611 35.851957

25.525 90.310 35.85195694

n1=65 , s1

2 =35.85195694 , n2=65 , s2

2=25.525493

H0 :s1

2 /s2

2=1

Ha :s1

2 /s2

2 ≠ 1

Test statistic: F= s1

2

s2

2 = 35.85195694

25.525493 =1.40455

The P value equals to 0.0885

We observe the p-value to be 0.0885 (this value is greater than α = 0.05), we therefore fail to

reject the null hypothesis of equal variances and conclude that the risks associated with the two

stocks (Boeing and IBM) are not significantly different at the 5% level.

Comparison of average returns

To test for the comparison of the average returns for the two stocks (Boeing and IBM), we

developed the hypothesis which we then tested at 5% level of significance;

H0 : μBO =μIBM

Ha : μBO ≠ μIBM

Tested at α=0.05

Table 4: t-Test: Two-Sample Assuming Equal Variances

IBM Stock

Price

Boeing Stock

Price

Mean 0.071484 1.013988

Variance 25.52549 35.85196

Observations 65 65

Pooled Variance 30.68872

Hypothesized Mean

Difference 0

df 128

t Stat -0.96992

P(T<=t) one-tail 0.166958

t Critical one-tail 1.656845

P(T<=t) two-tail 0.333916

t Critical two-tail 1.978671

2

s2

2 = 35.85195694

25.525493 =1.40455

The P value equals to 0.0885

We observe the p-value to be 0.0885 (this value is greater than α = 0.05), we therefore fail to

reject the null hypothesis of equal variances and conclude that the risks associated with the two

stocks (Boeing and IBM) are not significantly different at the 5% level.

Comparison of average returns

To test for the comparison of the average returns for the two stocks (Boeing and IBM), we

developed the hypothesis which we then tested at 5% level of significance;

H0 : μBO =μIBM

Ha : μBO ≠ μIBM

Tested at α=0.05

Table 4: t-Test: Two-Sample Assuming Equal Variances

IBM Stock

Price

Boeing Stock

Price

Mean 0.071484 1.013988

Variance 25.52549 35.85196

Observations 65 65

Pooled Variance 30.68872

Hypothesized Mean

Difference 0

df 128

t Stat -0.96992

P(T<=t) one-tail 0.166958

t Critical one-tail 1.656845

P(T<=t) two-tail 0.333916

t Critical two-tail 1.978671

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

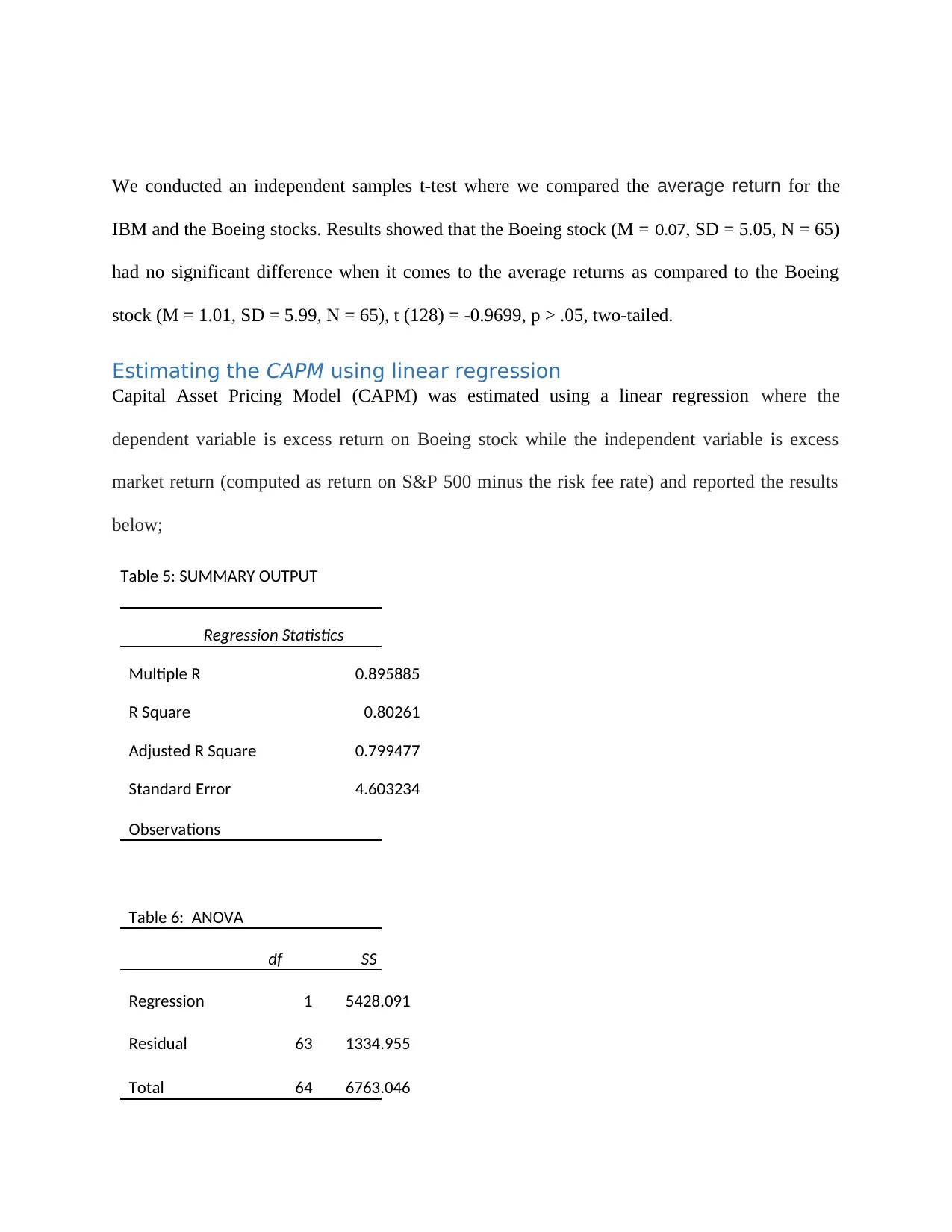

We conducted an independent samples t-test where we compared the average return for the

IBM and the Boeing stocks. Results showed that the Boeing stock (M = 0.07, SD = 5.05, N = 65)

had no significant difference when it comes to the average returns as compared to the Boeing

stock (M = 1.01, SD = 5.99, N = 65), t (128) = -0.9699, p > .05, two-tailed.

Estimating the CAPM using linear regression

Capital Asset Pricing Model (CAPM) was estimated using a linear regression where the

dependent variable is excess return on Boeing stock while the independent variable is excess

market return (computed as return on S&P 500 minus the risk fee rate) and reported the results

below;

Table 5: SUMMARY OUTPUT

Regression Statistics

Multiple R 0.895885

R Square 0.80261

Adjusted R Square 0.799477

Standard Error 4.603234

Observations

Table 6: ANOVA

df SS

Regression 1 5428.091

Residual 63 1334.955

Total 64 6763.046

IBM and the Boeing stocks. Results showed that the Boeing stock (M = 0.07, SD = 5.05, N = 65)

had no significant difference when it comes to the average returns as compared to the Boeing

stock (M = 1.01, SD = 5.99, N = 65), t (128) = -0.9699, p > .05, two-tailed.

Estimating the CAPM using linear regression

Capital Asset Pricing Model (CAPM) was estimated using a linear regression where the

dependent variable is excess return on Boeing stock while the independent variable is excess

market return (computed as return on S&P 500 minus the risk fee rate) and reported the results

below;

Table 5: SUMMARY OUTPUT

Regression Statistics

Multiple R 0.895885

R Square 0.80261

Adjusted R Square 0.799477

Standard Error 4.603234

Observations

Table 6: ANOVA

df SS

Regression 1 5428.091

Residual 63 1334.955

Total 64 6763.046

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

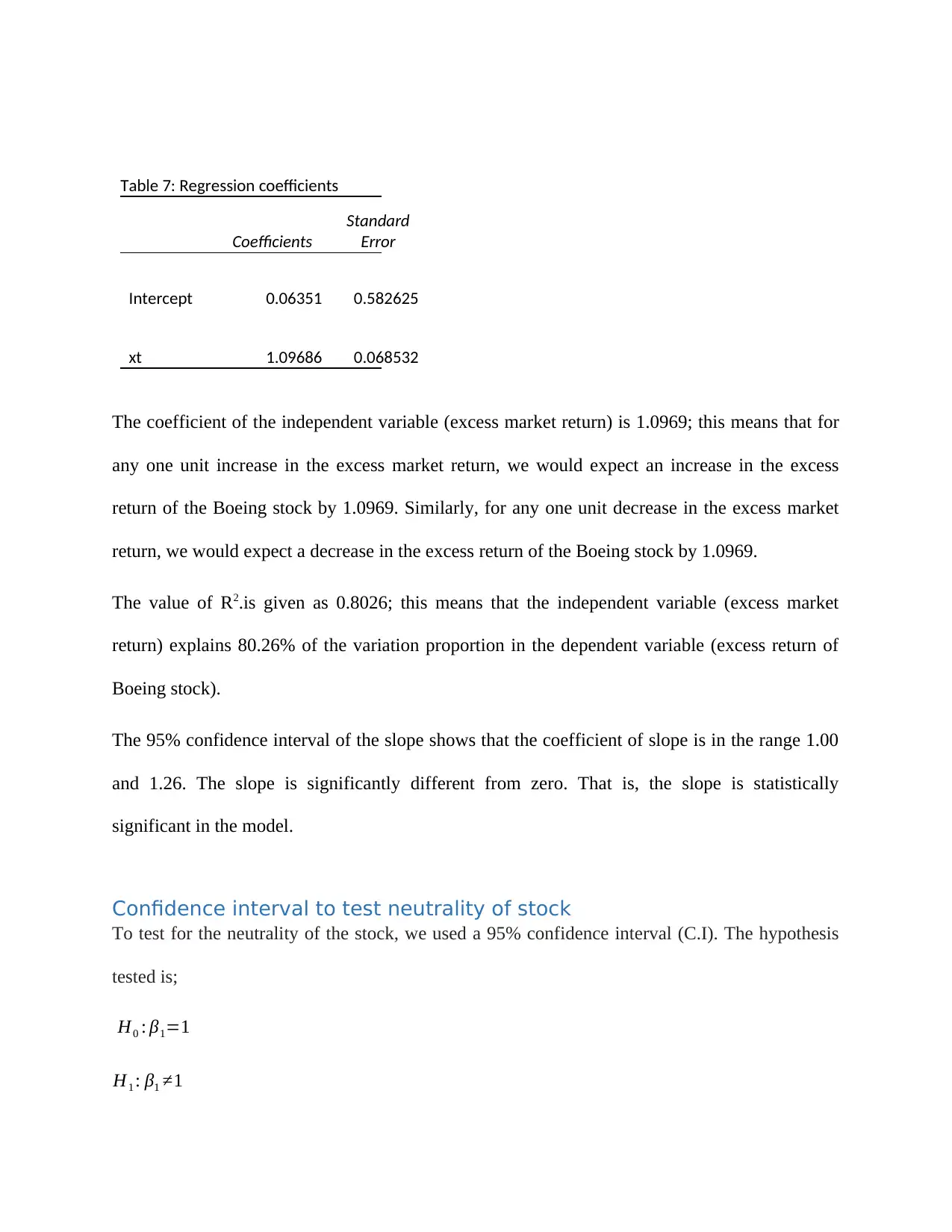

Table 7: Regression coefficients

Coefficients

Standard

Error

Intercept 0.06351 0.582625

xt 1.09686 0.068532

The coefficient of the independent variable (excess market return) is 1.0969; this means that for

any one unit increase in the excess market return, we would expect an increase in the excess

return of the Boeing stock by 1.0969. Similarly, for any one unit decrease in the excess market

return, we would expect a decrease in the excess return of the Boeing stock by 1.0969.

The value of R2.is given as 0.8026; this means that the independent variable (excess market

return) explains 80.26% of the variation proportion in the dependent variable (excess return of

Boeing stock).

The 95% confidence interval of the slope shows that the coefficient of slope is in the range 1.00

and 1.26. The slope is significantly different from zero. That is, the slope is statistically

significant in the model.

Confidence interval to test neutrality of stock

To test for the neutrality of the stock, we used a 95% confidence interval (C.I). The hypothesis

tested is;

H0 : β1=1

H1 : β1 ≠1

Coefficients

Standard

Error

Intercept 0.06351 0.582625

xt 1.09686 0.068532

The coefficient of the independent variable (excess market return) is 1.0969; this means that for

any one unit increase in the excess market return, we would expect an increase in the excess

return of the Boeing stock by 1.0969. Similarly, for any one unit decrease in the excess market

return, we would expect a decrease in the excess return of the Boeing stock by 1.0969.

The value of R2.is given as 0.8026; this means that the independent variable (excess market

return) explains 80.26% of the variation proportion in the dependent variable (excess return of

Boeing stock).

The 95% confidence interval of the slope shows that the coefficient of slope is in the range 1.00

and 1.26. The slope is significantly different from zero. That is, the slope is statistically

significant in the model.

Confidence interval to test neutrality of stock

To test for the neutrality of the stock, we used a 95% confidence interval (C.I). The hypothesis

tested is;

H0 : β1=1

H1 : β1 ≠1

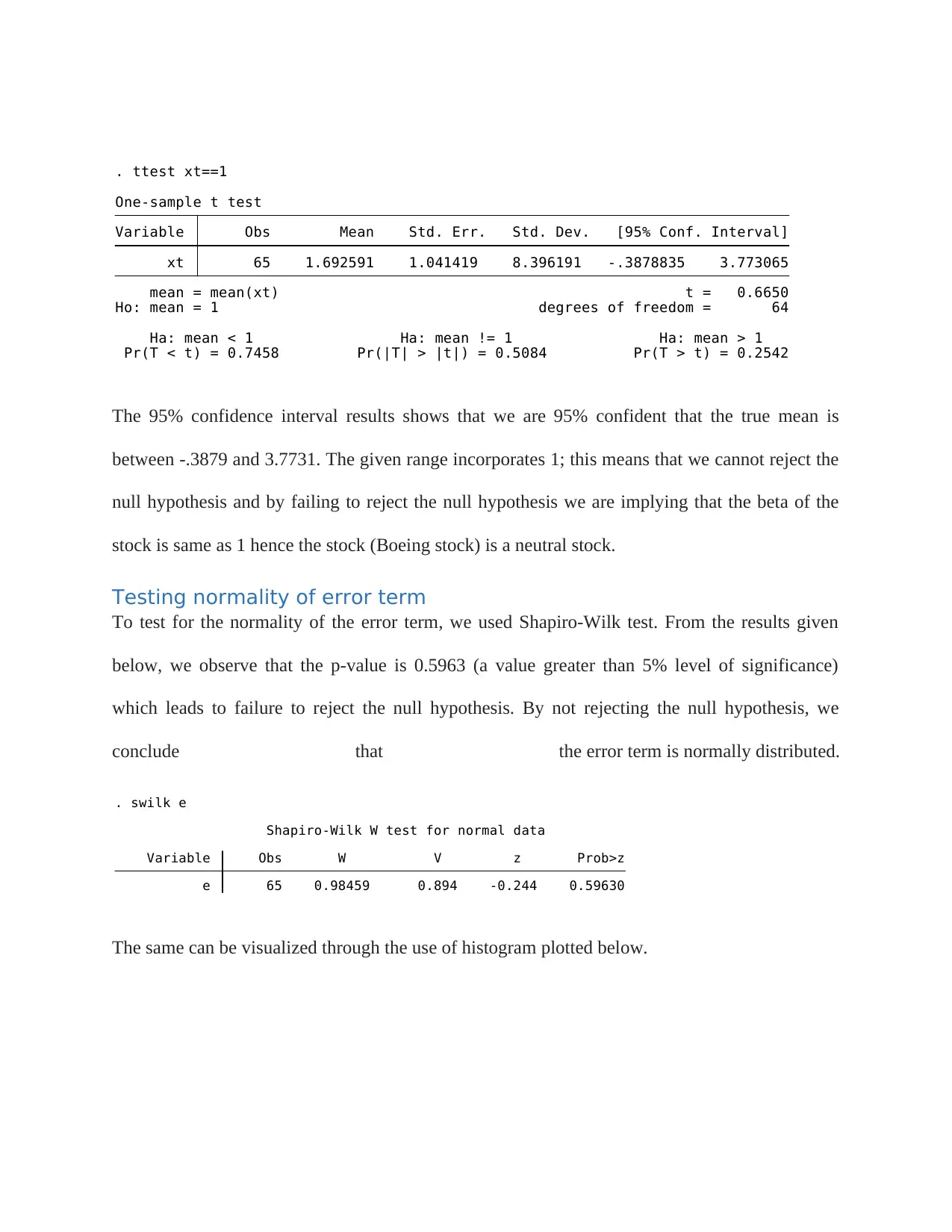

Pr(T < t) = 0.7458 Pr(|T| > |t|) = 0.5084 Pr(T > t) = 0.2542

Ha: mean < 1 Ha: mean != 1 Ha: mean > 1

Ho: mean = 1 degrees of freedom = 64

mean = mean(xt) t = 0.6650

xt 65 1.692591 1.041419 8.396191 -.3878835 3.773065

Variable Obs Mean Std. Err. Std. Dev. [95% Conf. Interval]

One-sample t test

. ttest xt==1

The 95% confidence interval results shows that we are 95% confident that the true mean is

between -.3879 and 3.7731. The given range incorporates 1; this means that we cannot reject the

null hypothesis and by failing to reject the null hypothesis we are implying that the beta of the

stock is same as 1 hence the stock (Boeing stock) is a neutral stock.

Testing normality of error term

To test for the normality of the error term, we used Shapiro-Wilk test. From the results given

below, we observe that the p-value is 0.5963 (a value greater than 5% level of significance)

which leads to failure to reject the null hypothesis. By not rejecting the null hypothesis, we

conclude that the error term is normally distributed.

e 65 0.98459 0.894 -0.244 0.59630

Variable Obs W V z Prob>z

Shapiro-Wilk W test for normal data

. swilk e

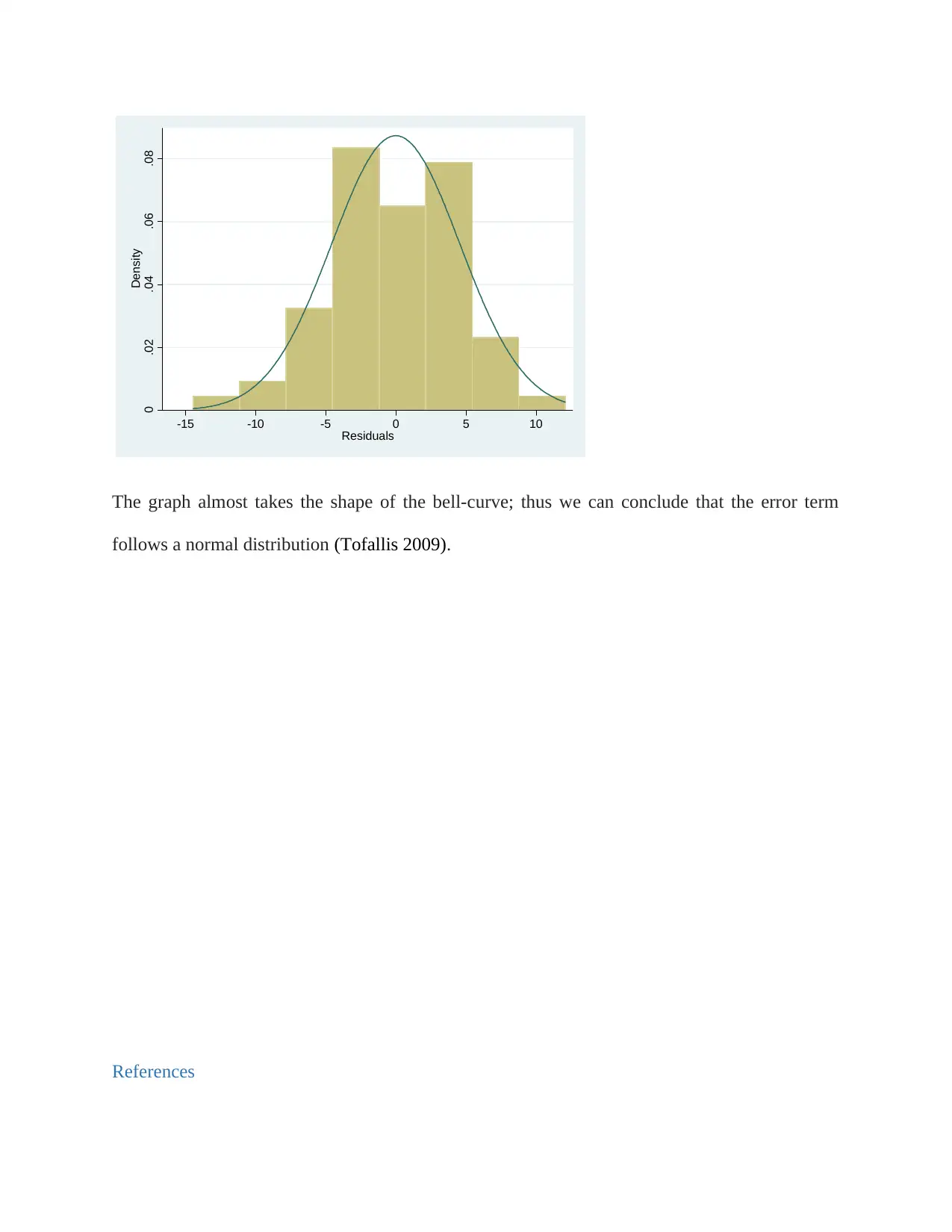

The same can be visualized through the use of histogram plotted below.

Ha: mean < 1 Ha: mean != 1 Ha: mean > 1

Ho: mean = 1 degrees of freedom = 64

mean = mean(xt) t = 0.6650

xt 65 1.692591 1.041419 8.396191 -.3878835 3.773065

Variable Obs Mean Std. Err. Std. Dev. [95% Conf. Interval]

One-sample t test

. ttest xt==1

The 95% confidence interval results shows that we are 95% confident that the true mean is

between -.3879 and 3.7731. The given range incorporates 1; this means that we cannot reject the

null hypothesis and by failing to reject the null hypothesis we are implying that the beta of the

stock is same as 1 hence the stock (Boeing stock) is a neutral stock.

Testing normality of error term

To test for the normality of the error term, we used Shapiro-Wilk test. From the results given

below, we observe that the p-value is 0.5963 (a value greater than 5% level of significance)

which leads to failure to reject the null hypothesis. By not rejecting the null hypothesis, we

conclude that the error term is normally distributed.

e 65 0.98459 0.894 -0.244 0.59630

Variable Obs W V z Prob>z

Shapiro-Wilk W test for normal data

. swilk e

The same can be visualized through the use of histogram plotted below.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

0 .02 .04 .06 .08

Density

-15 -10 -5 0 5 10

Residuals

The graph almost takes the shape of the bell-curve; thus we can conclude that the error term

follows a normal distribution (Tofallis 2009).

References

Density

-15 -10 -5 0 5 10

Residuals

The graph almost takes the shape of the bell-curve; thus we can conclude that the error term

follows a normal distribution (Tofallis 2009).

References

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.