Digital Dashboards and Impression Management in Accounting

VerifiedAdded on 2020/02/23

|19

|2252

|61

AI Summary

This assignment delves into two key concepts: digital dashboards and impression management in accounting. It examines how dashboards visualize data to aid decision-making across various business functions. Furthermore, it analyzes the impact of impression management on financial reporting quality and capital allocation decisions. The discussion encompasses different aspects of impression management, including psychological, economic, and sociological factors, highlighting its complexity and implications for organizational communication.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: BUSINESS AND ACCOUNTING FINANCE

Business and accounting finance

Name of the student

Name of the university

Author note

Business and accounting finance

Name of the student

Name of the university

Author note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1BUSINESS AND ACCOUNTING FINANCE

Table of Contents

Question 1..................................................................................................................................2

1.1 Accumulated depreciation is the sum of cash that is accumulated for replacing the fixed

asset........................................................................................................................................2

1.2 To capitalize the amount means the amount will not charged as expense.......................2

1.3 Inventory methods............................................................................................................2

Question 2..................................................................................................................................4

A. Balance sheet and income statement...............................................................................4

B. With changed data...........................................................................................................8

Question 3..................................................................................................................................9

Requirement 1........................................................................................................................9

Requirement 2......................................................................................................................10

Requirement 3......................................................................................................................10

Question 4................................................................................................................................11

1. Major financial reports and their purposes....................................................................11

2. Importance of profits and cash flow..............................................................................11

3. Ethical issues of ABC case study..................................................................................12

Question 5................................................................................................................................12

Comparisons made with the ratios.......................................................................................12

Question 6................................................................................................................................13

A. Financial ratios..............................................................................................................13

Table of Contents

Question 1..................................................................................................................................2

1.1 Accumulated depreciation is the sum of cash that is accumulated for replacing the fixed

asset........................................................................................................................................2

1.2 To capitalize the amount means the amount will not charged as expense.......................2

1.3 Inventory methods............................................................................................................2

Question 2..................................................................................................................................4

A. Balance sheet and income statement...............................................................................4

B. With changed data...........................................................................................................8

Question 3..................................................................................................................................9

Requirement 1........................................................................................................................9

Requirement 2......................................................................................................................10

Requirement 3......................................................................................................................10

Question 4................................................................................................................................11

1. Major financial reports and their purposes....................................................................11

2. Importance of profits and cash flow..............................................................................11

3. Ethical issues of ABC case study..................................................................................12

Question 5................................................................................................................................12

Comparisons made with the ratios.......................................................................................12

Question 6................................................................................................................................13

A. Financial ratios..............................................................................................................13

2BUSINESS AND ACCOUNTING FINANCE

B. Chart for rate of return on sales.....................................................................................13

C. Report on calculation and chart.....................................................................................15

Question 7................................................................................................................................15

Business report for decision making aspect.........................................................................15

Reference..................................................................................................................................18

B. Chart for rate of return on sales.....................................................................................13

C. Report on calculation and chart.....................................................................................15

Question 7................................................................................................................................15

Business report for decision making aspect.........................................................................15

Reference..................................................................................................................................18

3BUSINESS AND ACCOUNTING FINANCE

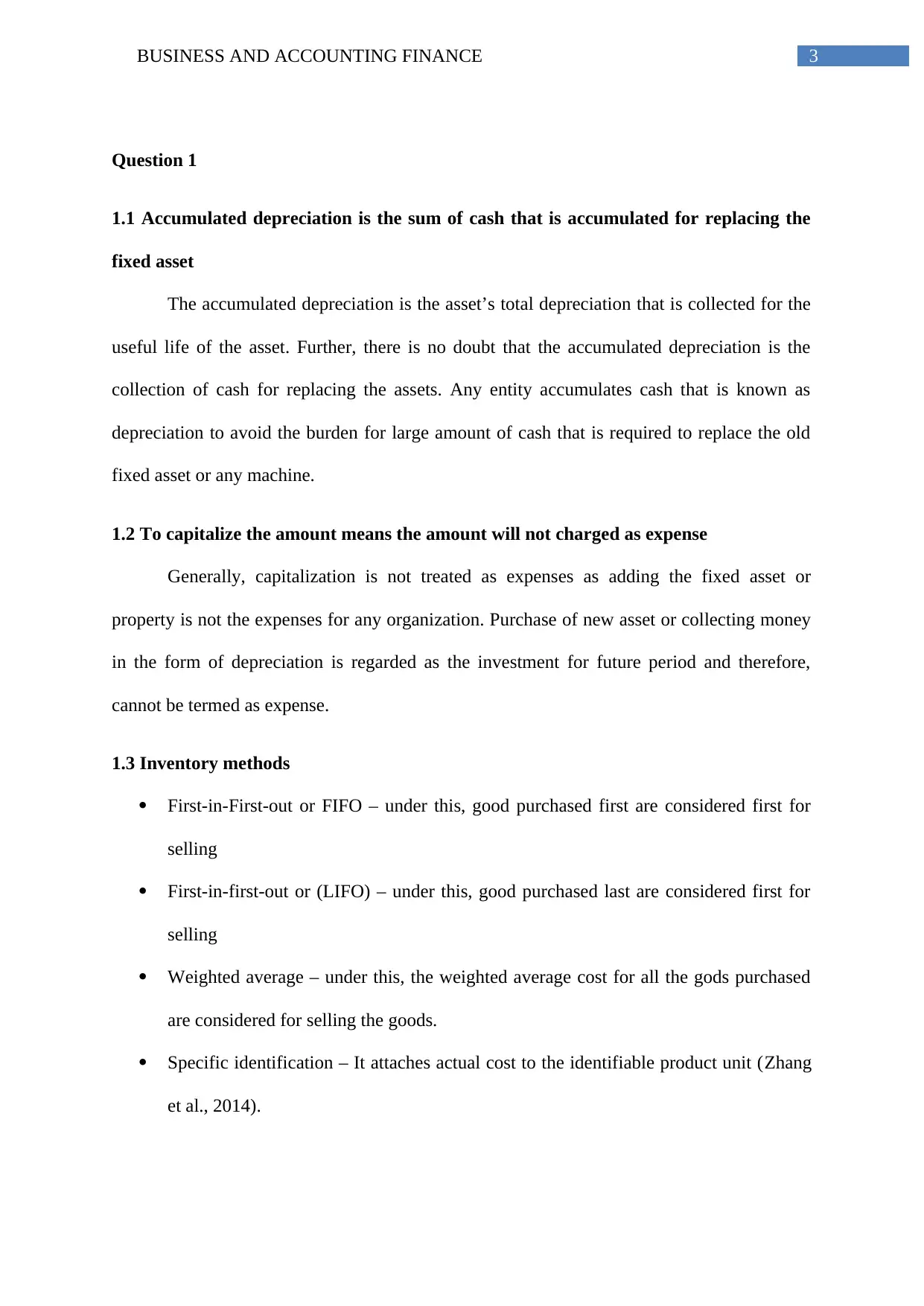

Question 1

1.1 Accumulated depreciation is the sum of cash that is accumulated for replacing the

fixed asset

The accumulated depreciation is the asset’s total depreciation that is collected for the

useful life of the asset. Further, there is no doubt that the accumulated depreciation is the

collection of cash for replacing the assets. Any entity accumulates cash that is known as

depreciation to avoid the burden for large amount of cash that is required to replace the old

fixed asset or any machine.

1.2 To capitalize the amount means the amount will not charged as expense

Generally, capitalization is not treated as expenses as adding the fixed asset or

property is not the expenses for any organization. Purchase of new asset or collecting money

in the form of depreciation is regarded as the investment for future period and therefore,

cannot be termed as expense.

1.3 Inventory methods

First-in-First-out or FIFO – under this, good purchased first are considered first for

selling

First-in-first-out or (LIFO) – under this, good purchased last are considered first for

selling

Weighted average – under this, the weighted average cost for all the gods purchased

are considered for selling the goods.

Specific identification – It attaches actual cost to the identifiable product unit (Zhang

et al., 2014).

Question 1

1.1 Accumulated depreciation is the sum of cash that is accumulated for replacing the

fixed asset

The accumulated depreciation is the asset’s total depreciation that is collected for the

useful life of the asset. Further, there is no doubt that the accumulated depreciation is the

collection of cash for replacing the assets. Any entity accumulates cash that is known as

depreciation to avoid the burden for large amount of cash that is required to replace the old

fixed asset or any machine.

1.2 To capitalize the amount means the amount will not charged as expense

Generally, capitalization is not treated as expenses as adding the fixed asset or

property is not the expenses for any organization. Purchase of new asset or collecting money

in the form of depreciation is regarded as the investment for future period and therefore,

cannot be termed as expense.

1.3 Inventory methods

First-in-First-out or FIFO – under this, good purchased first are considered first for

selling

First-in-first-out or (LIFO) – under this, good purchased last are considered first for

selling

Weighted average – under this, the weighted average cost for all the gods purchased

are considered for selling the goods.

Specific identification – It attaches actual cost to the identifiable product unit (Zhang

et al., 2014).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4BUSINESS AND ACCOUNTING FINANCE

Examples of various inventory methods

Data

Date Particulars Units Cost P.U Total cost

Oct-01 Opening inventory 50 $ 50.00 $ 2,500.00

Oct-03 Purchase 25 $ 40.00 $ 1,000.00

Oct-12 Purchase 50 $ 30.00 $ 1,500.00

Oct-18 Purchase 75 $ 25.00 $ 1,875.00 $ 6,875.00

Oct-31 Inventory on hand 150

FIFO method – cost of ending inventory

75 units @ 25 $ 1,875.00

50 units @ 30 $ 1,500.00

25 units @ 40 $ 1,000.00

Cost of 150 units $ 3,375.00

FIFO method – cost of ending inventory

50 units @ 50 $ 2,500.00

25 units @ 40 $ 1,000.00

50 units @ 30 $ 1,500.00

Cost of 150 units $ 3,500.00

Weighted average method – cost of ending inventory

Total cost of units available for sale $ 6,875.00

Total units available for sale 261

Average cost per unit $ 26.34

Cost of ending inventory $ 3,951.15

Specific identification method – cost of 75 units of ending inventory

Cost of ending inventory will be = 75 units * $ 25 = $ 1,875

The above cost is selected as it is easy to identify the specific lot for sales

Examples of various inventory methods

Data

Date Particulars Units Cost P.U Total cost

Oct-01 Opening inventory 50 $ 50.00 $ 2,500.00

Oct-03 Purchase 25 $ 40.00 $ 1,000.00

Oct-12 Purchase 50 $ 30.00 $ 1,500.00

Oct-18 Purchase 75 $ 25.00 $ 1,875.00 $ 6,875.00

Oct-31 Inventory on hand 150

FIFO method – cost of ending inventory

75 units @ 25 $ 1,875.00

50 units @ 30 $ 1,500.00

25 units @ 40 $ 1,000.00

Cost of 150 units $ 3,375.00

FIFO method – cost of ending inventory

50 units @ 50 $ 2,500.00

25 units @ 40 $ 1,000.00

50 units @ 30 $ 1,500.00

Cost of 150 units $ 3,500.00

Weighted average method – cost of ending inventory

Total cost of units available for sale $ 6,875.00

Total units available for sale 261

Average cost per unit $ 26.34

Cost of ending inventory $ 3,951.15

Specific identification method – cost of 75 units of ending inventory

Cost of ending inventory will be = 75 units * $ 25 = $ 1,875

The above cost is selected as it is easy to identify the specific lot for sales

5BUSINESS AND ACCOUNTING FINANCE

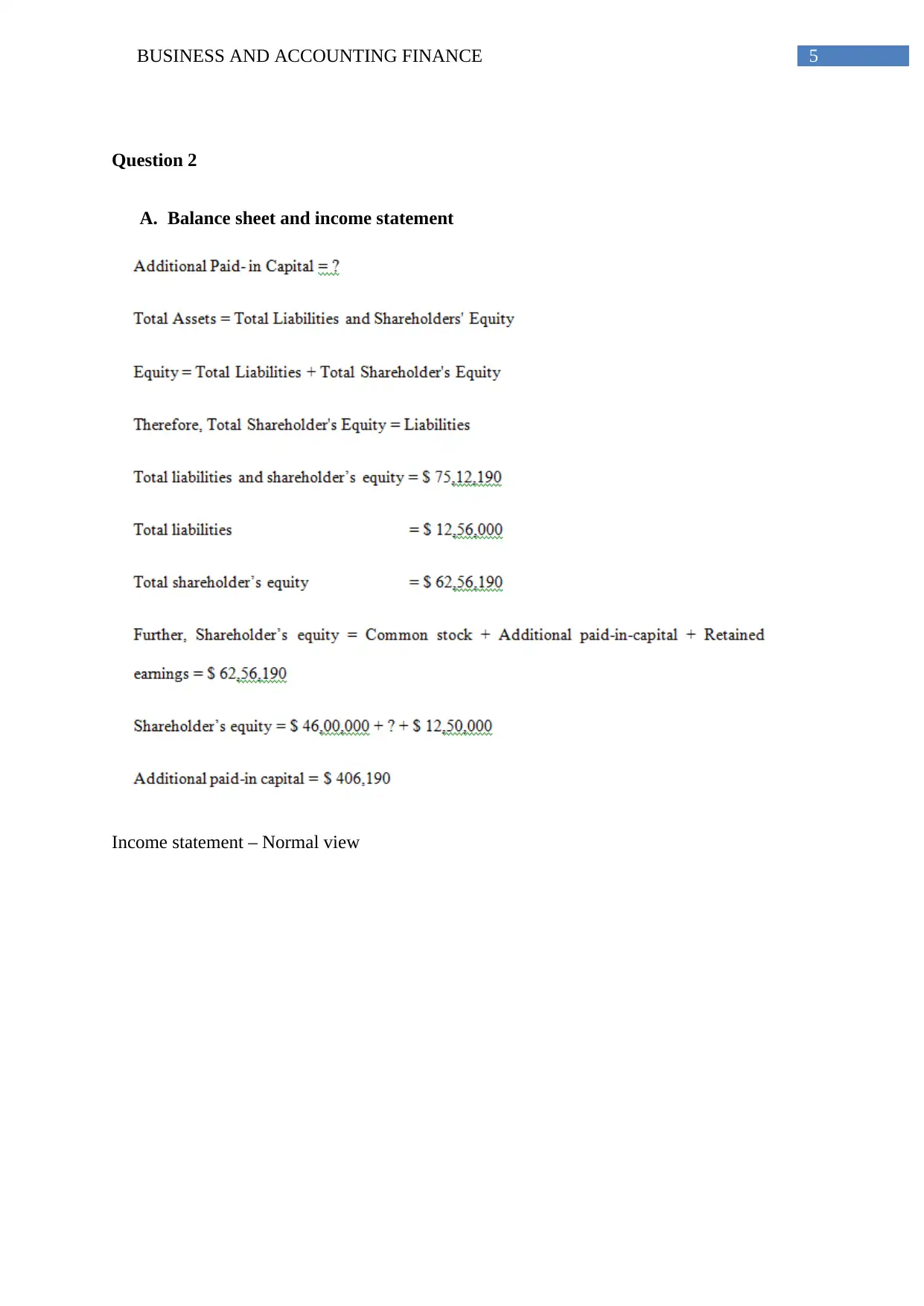

Question 2

A. Balance sheet and income statement

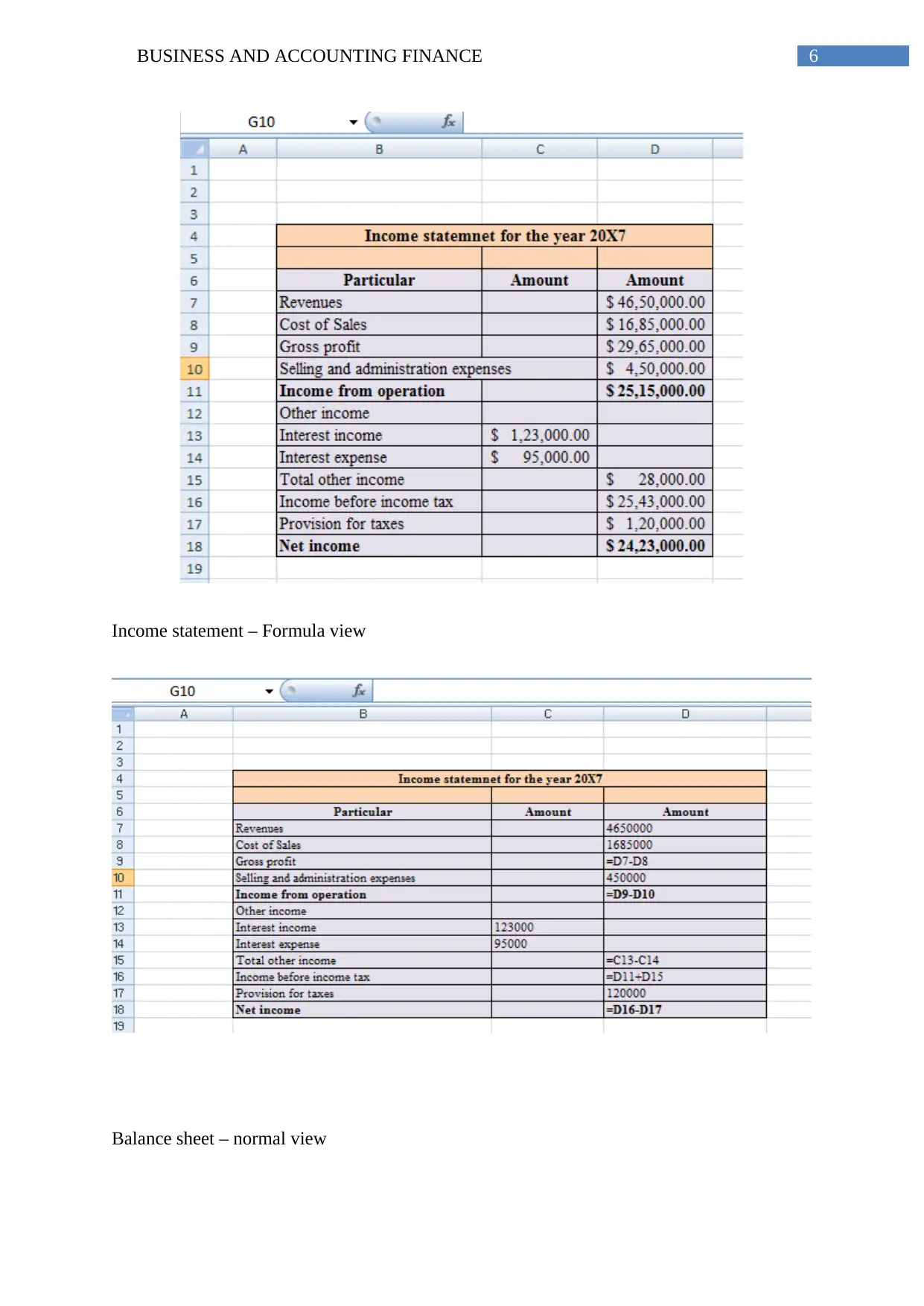

Income statement – Normal view

Question 2

A. Balance sheet and income statement

Income statement – Normal view

6BUSINESS AND ACCOUNTING FINANCE

Income statement – Formula view

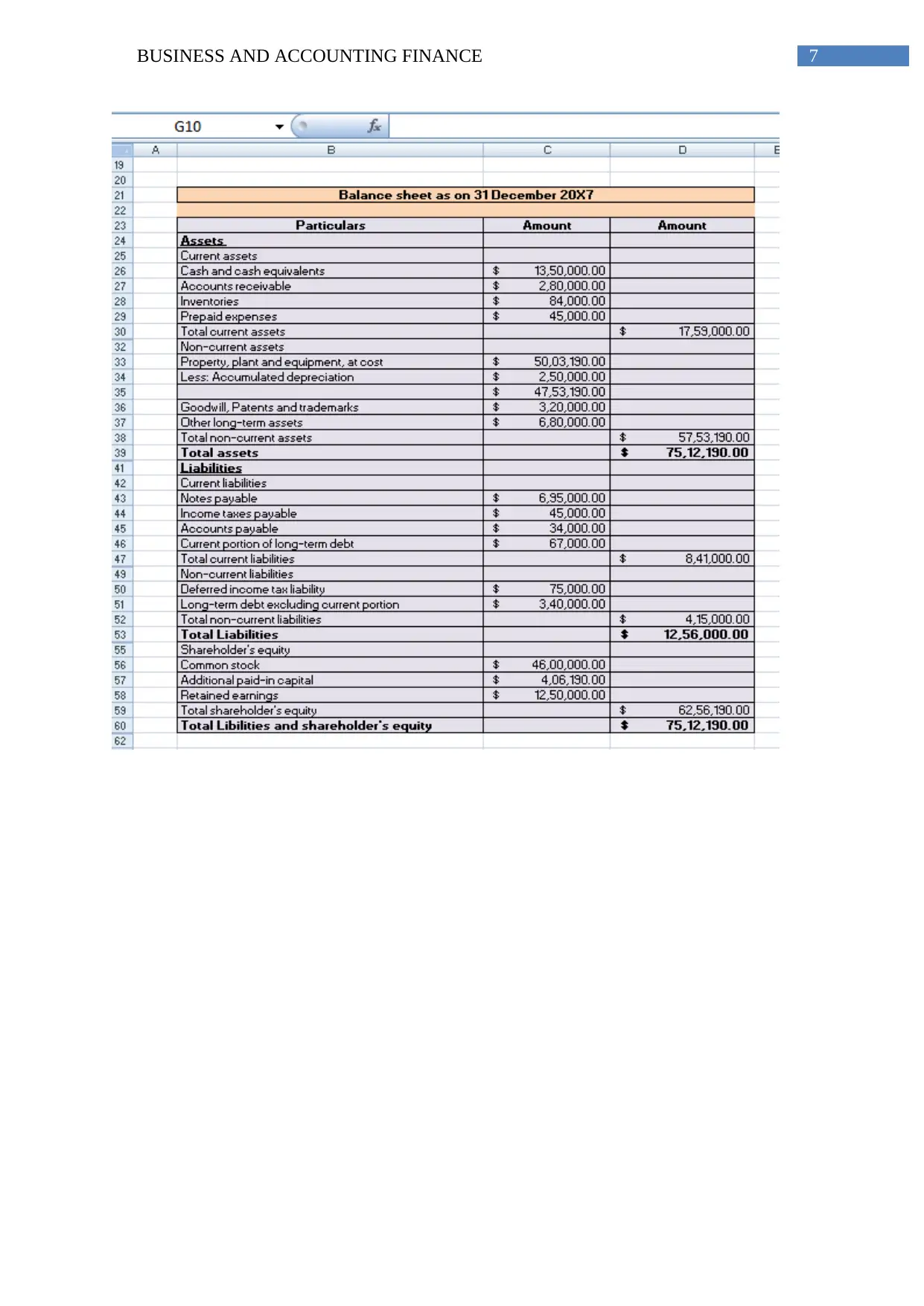

Balance sheet – normal view

Income statement – Formula view

Balance sheet – normal view

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7BUSINESS AND ACCOUNTING FINANCE

8BUSINESS AND ACCOUNTING FINANCE

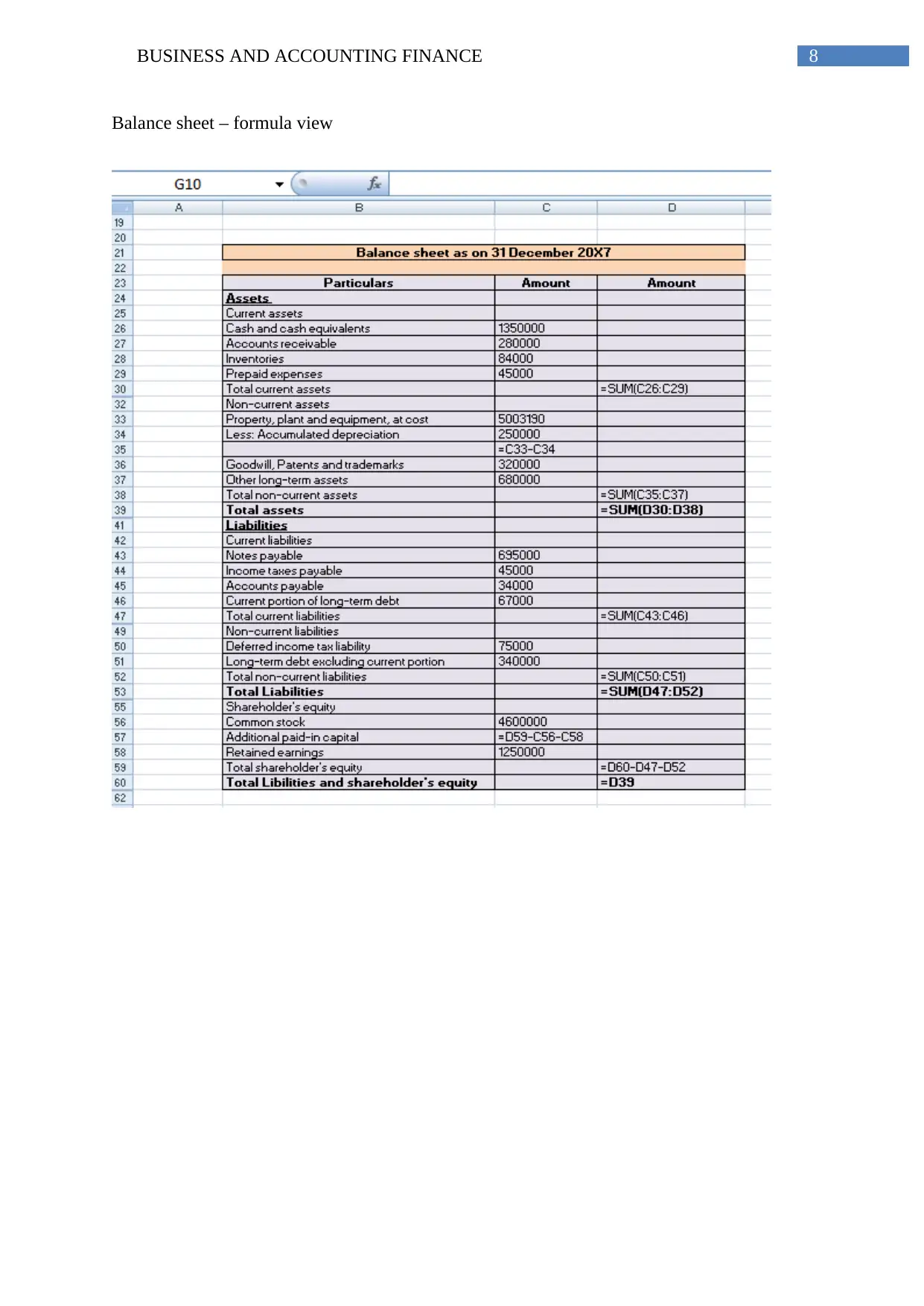

Balance sheet – formula view

Balance sheet – formula view

9BUSINESS AND ACCOUNTING FINANCE

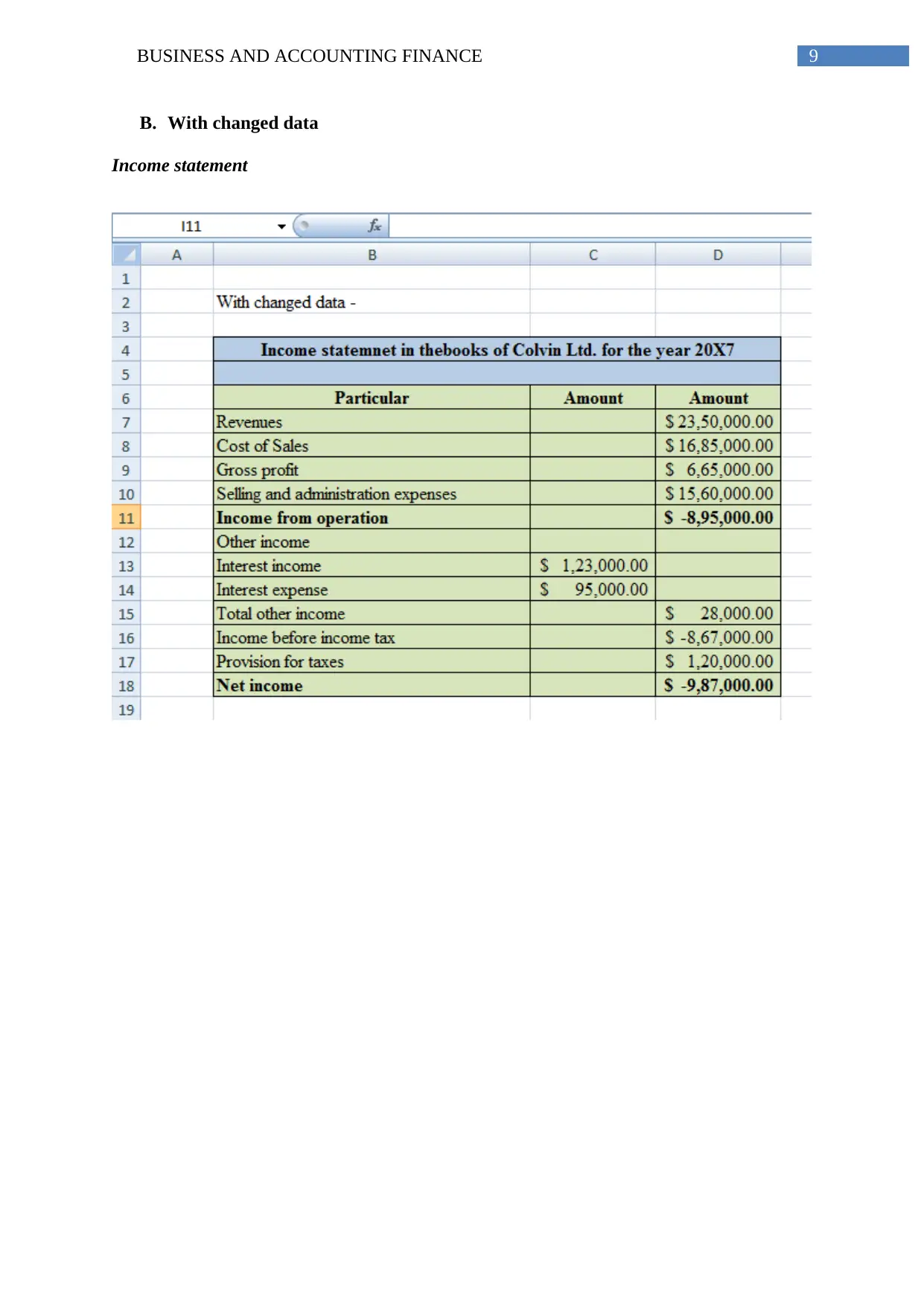

B. With changed data

Income statement

B. With changed data

Income statement

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10BUSINESS AND ACCOUNTING FINANCE

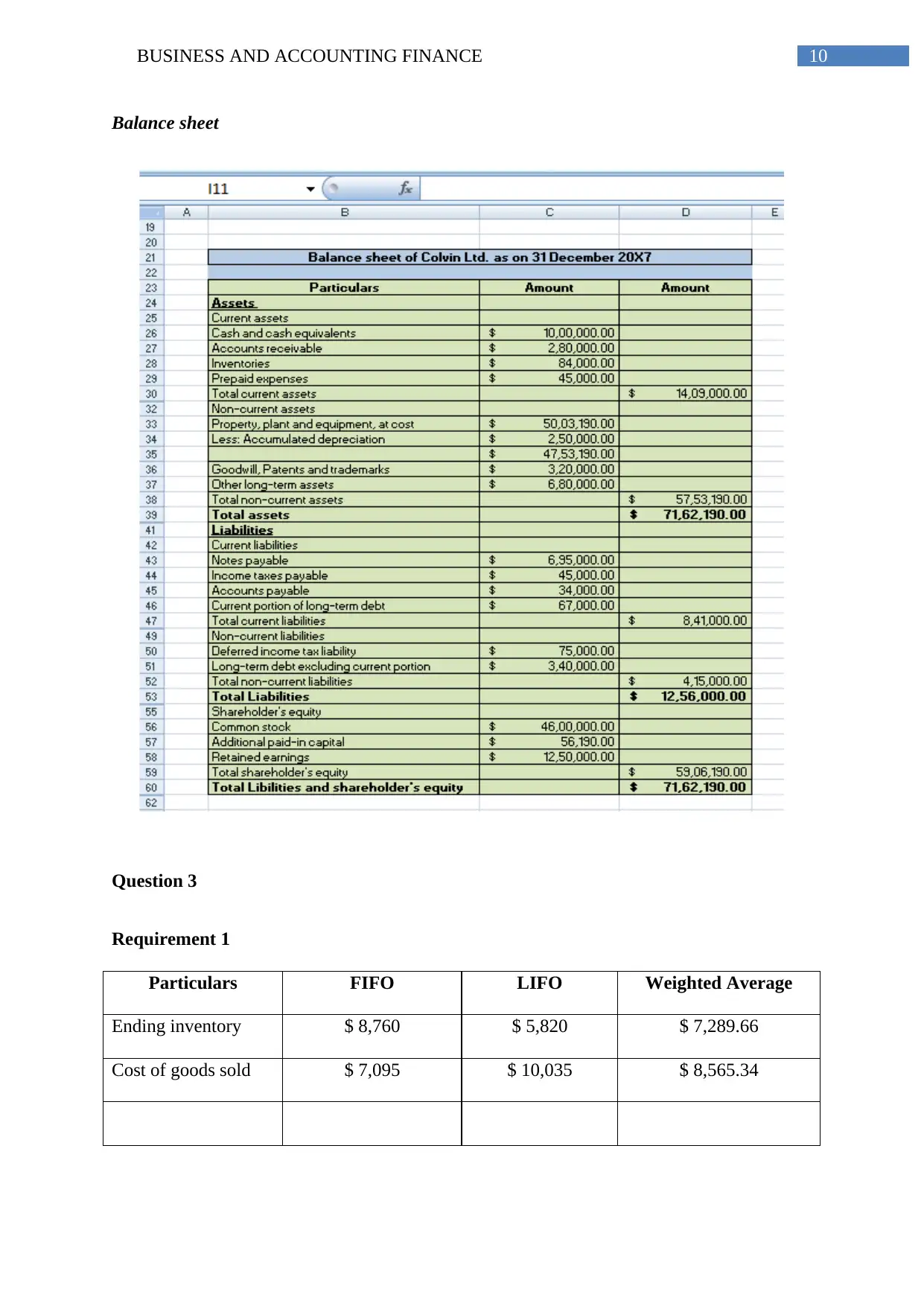

Balance sheet

Question 3

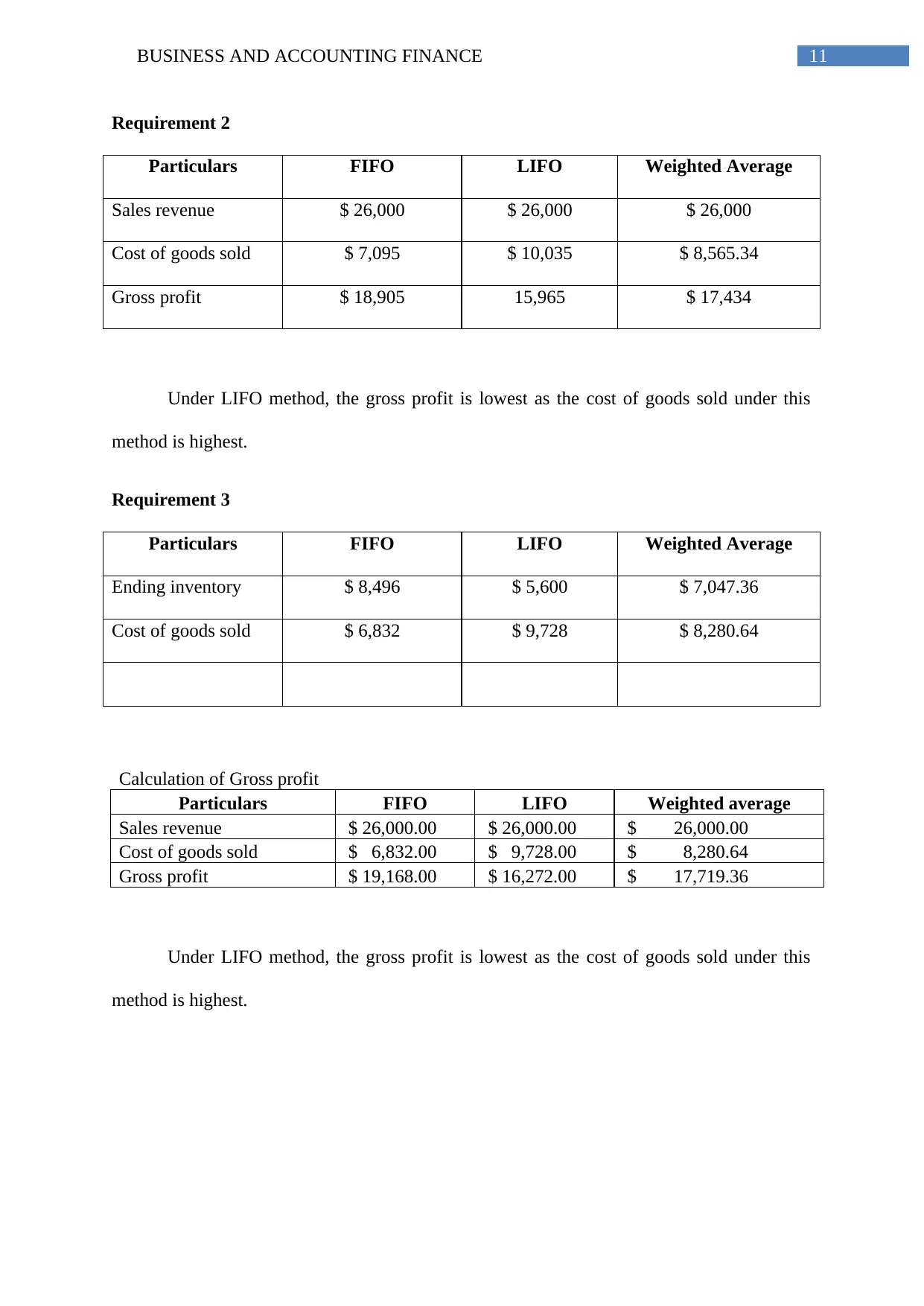

Requirement 1

Particulars FIFO LIFO Weighted Average

Ending inventory $ 8,760 $ 5,820 $ 7,289.66

Cost of goods sold $ 7,095 $ 10,035 $ 8,565.34

Balance sheet

Question 3

Requirement 1

Particulars FIFO LIFO Weighted Average

Ending inventory $ 8,760 $ 5,820 $ 7,289.66

Cost of goods sold $ 7,095 $ 10,035 $ 8,565.34

11BUSINESS AND ACCOUNTING FINANCE

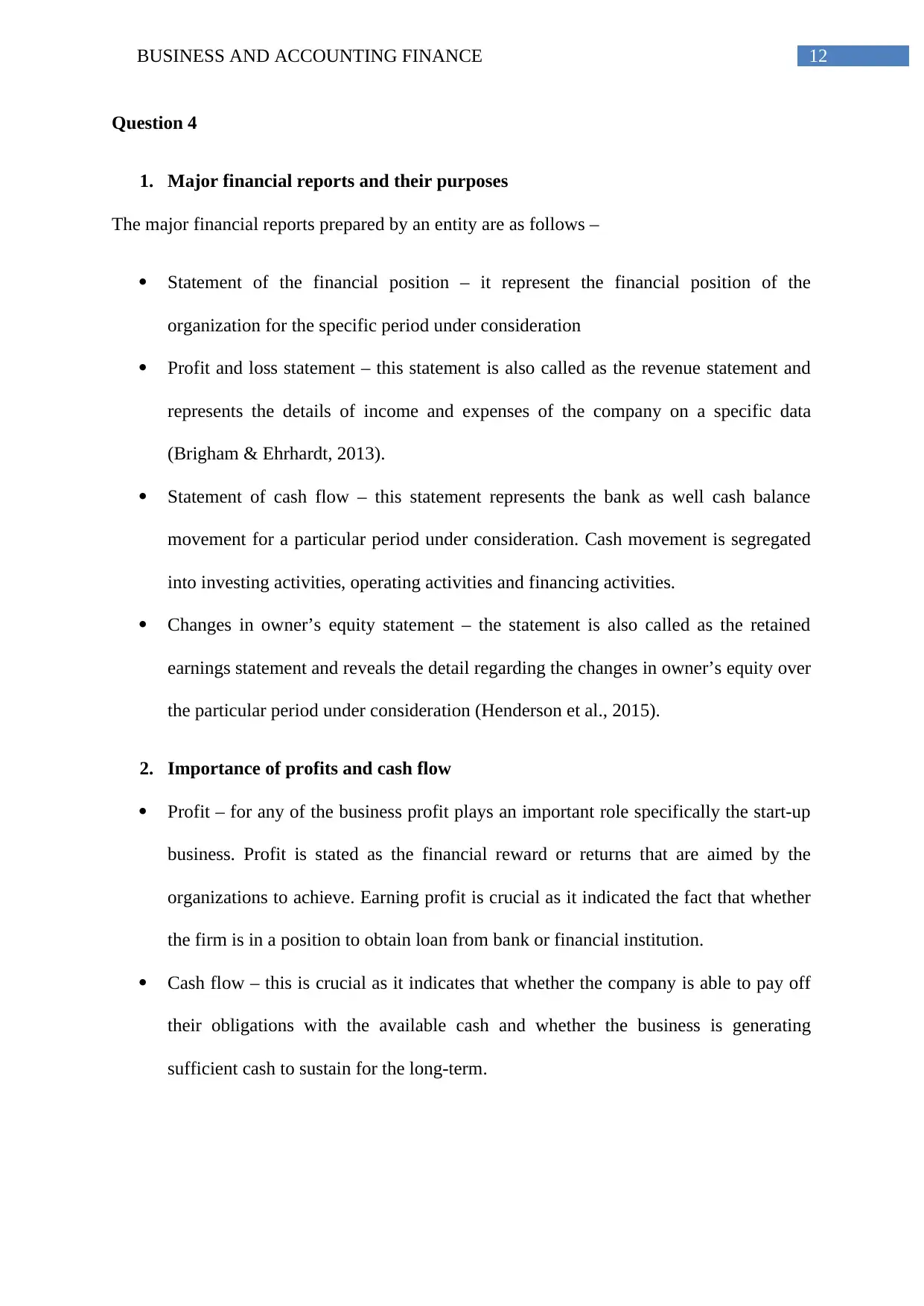

Requirement 2

Particulars FIFO LIFO Weighted Average

Sales revenue $ 26,000 $ 26,000 $ 26,000

Cost of goods sold $ 7,095 $ 10,035 $ 8,565.34

Gross profit $ 18,905 15,965 $ 17,434

Under LIFO method, the gross profit is lowest as the cost of goods sold under this

method is highest.

Requirement 3

Particulars FIFO LIFO Weighted Average

Ending inventory $ 8,496 $ 5,600 $ 7,047.36

Cost of goods sold $ 6,832 $ 9,728 $ 8,280.64

Calculation of Gross profit

Particulars FIFO LIFO Weighted average

Sales revenue $ 26,000.00 $ 26,000.00 $ 26,000.00

Cost of goods sold $ 6,832.00 $ 9,728.00 $ 8,280.64

Gross profit $ 19,168.00 $ 16,272.00 $ 17,719.36

Under LIFO method, the gross profit is lowest as the cost of goods sold under this

method is highest.

Requirement 2

Particulars FIFO LIFO Weighted Average

Sales revenue $ 26,000 $ 26,000 $ 26,000

Cost of goods sold $ 7,095 $ 10,035 $ 8,565.34

Gross profit $ 18,905 15,965 $ 17,434

Under LIFO method, the gross profit is lowest as the cost of goods sold under this

method is highest.

Requirement 3

Particulars FIFO LIFO Weighted Average

Ending inventory $ 8,496 $ 5,600 $ 7,047.36

Cost of goods sold $ 6,832 $ 9,728 $ 8,280.64

Calculation of Gross profit

Particulars FIFO LIFO Weighted average

Sales revenue $ 26,000.00 $ 26,000.00 $ 26,000.00

Cost of goods sold $ 6,832.00 $ 9,728.00 $ 8,280.64

Gross profit $ 19,168.00 $ 16,272.00 $ 17,719.36

Under LIFO method, the gross profit is lowest as the cost of goods sold under this

method is highest.

12BUSINESS AND ACCOUNTING FINANCE

Question 4

1. Major financial reports and their purposes

The major financial reports prepared by an entity are as follows –

Statement of the financial position – it represent the financial position of the

organization for the specific period under consideration

Profit and loss statement – this statement is also called as the revenue statement and

represents the details of income and expenses of the company on a specific data

(Brigham & Ehrhardt, 2013).

Statement of cash flow – this statement represents the bank as well cash balance

movement for a particular period under consideration. Cash movement is segregated

into investing activities, operating activities and financing activities.

Changes in owner’s equity statement – the statement is also called as the retained

earnings statement and reveals the detail regarding the changes in owner’s equity over

the particular period under consideration (Henderson et al., 2015).

2. Importance of profits and cash flow

Profit – for any of the business profit plays an important role specifically the start-up

business. Profit is stated as the financial reward or returns that are aimed by the

organizations to achieve. Earning profit is crucial as it indicated the fact that whether

the firm is in a position to obtain loan from bank or financial institution.

Cash flow – this is crucial as it indicates that whether the company is able to pay off

their obligations with the available cash and whether the business is generating

sufficient cash to sustain for the long-term.

Question 4

1. Major financial reports and their purposes

The major financial reports prepared by an entity are as follows –

Statement of the financial position – it represent the financial position of the

organization for the specific period under consideration

Profit and loss statement – this statement is also called as the revenue statement and

represents the details of income and expenses of the company on a specific data

(Brigham & Ehrhardt, 2013).

Statement of cash flow – this statement represents the bank as well cash balance

movement for a particular period under consideration. Cash movement is segregated

into investing activities, operating activities and financing activities.

Changes in owner’s equity statement – the statement is also called as the retained

earnings statement and reveals the detail regarding the changes in owner’s equity over

the particular period under consideration (Henderson et al., 2015).

2. Importance of profits and cash flow

Profit – for any of the business profit plays an important role specifically the start-up

business. Profit is stated as the financial reward or returns that are aimed by the

organizations to achieve. Earning profit is crucial as it indicated the fact that whether

the firm is in a position to obtain loan from bank or financial institution.

Cash flow – this is crucial as it indicates that whether the company is able to pay off

their obligations with the available cash and whether the business is generating

sufficient cash to sustain for the long-term.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13BUSINESS AND ACCOUNTING FINANCE

3. Ethical issues of ABC case study

ABC Learning owner was in the view that the financial statements are not of much

importance and therefore, ignored the horrible disorder of the accounts.

The owner of the company forgot the fact that is is not the manager and his concept

regarding he is the most suitable person to operate the business led the business on the

concept of “too fast – too much – too expensive” which in turn led the company

towards unethical approach of earning profit at any cost

Corporate governance practice of the company was of poor quality

Question 5

Comparisons made with the ratios

Three kinds of comparisons generally performed with the ratios are –

Inter-firm comparisons – this comparison involve the comparisons among different

firms of the same industry. Therefore, it indicates performance of the firm as

compared to the competitor (Grinblatt & Titman, 2016).

Trend analysis – it involves the ratio comparison of an entity over the specific time

period and the past ratios are compared with present ratios for the same entity. It

reveals the performance of the firm with regard to constancy, deterioration and

improvement

Comparing with industry average or standards average – under this, the ratios of an

entity is compared with the industry average or the standard average of that ratio.

3. Ethical issues of ABC case study

ABC Learning owner was in the view that the financial statements are not of much

importance and therefore, ignored the horrible disorder of the accounts.

The owner of the company forgot the fact that is is not the manager and his concept

regarding he is the most suitable person to operate the business led the business on the

concept of “too fast – too much – too expensive” which in turn led the company

towards unethical approach of earning profit at any cost

Corporate governance practice of the company was of poor quality

Question 5

Comparisons made with the ratios

Three kinds of comparisons generally performed with the ratios are –

Inter-firm comparisons – this comparison involve the comparisons among different

firms of the same industry. Therefore, it indicates performance of the firm as

compared to the competitor (Grinblatt & Titman, 2016).

Trend analysis – it involves the ratio comparison of an entity over the specific time

period and the past ratios are compared with present ratios for the same entity. It

reveals the performance of the firm with regard to constancy, deterioration and

improvement

Comparing with industry average or standards average – under this, the ratios of an

entity is compared with the industry average or the standard average of that ratio.

14BUSINESS AND ACCOUNTING FINANCE

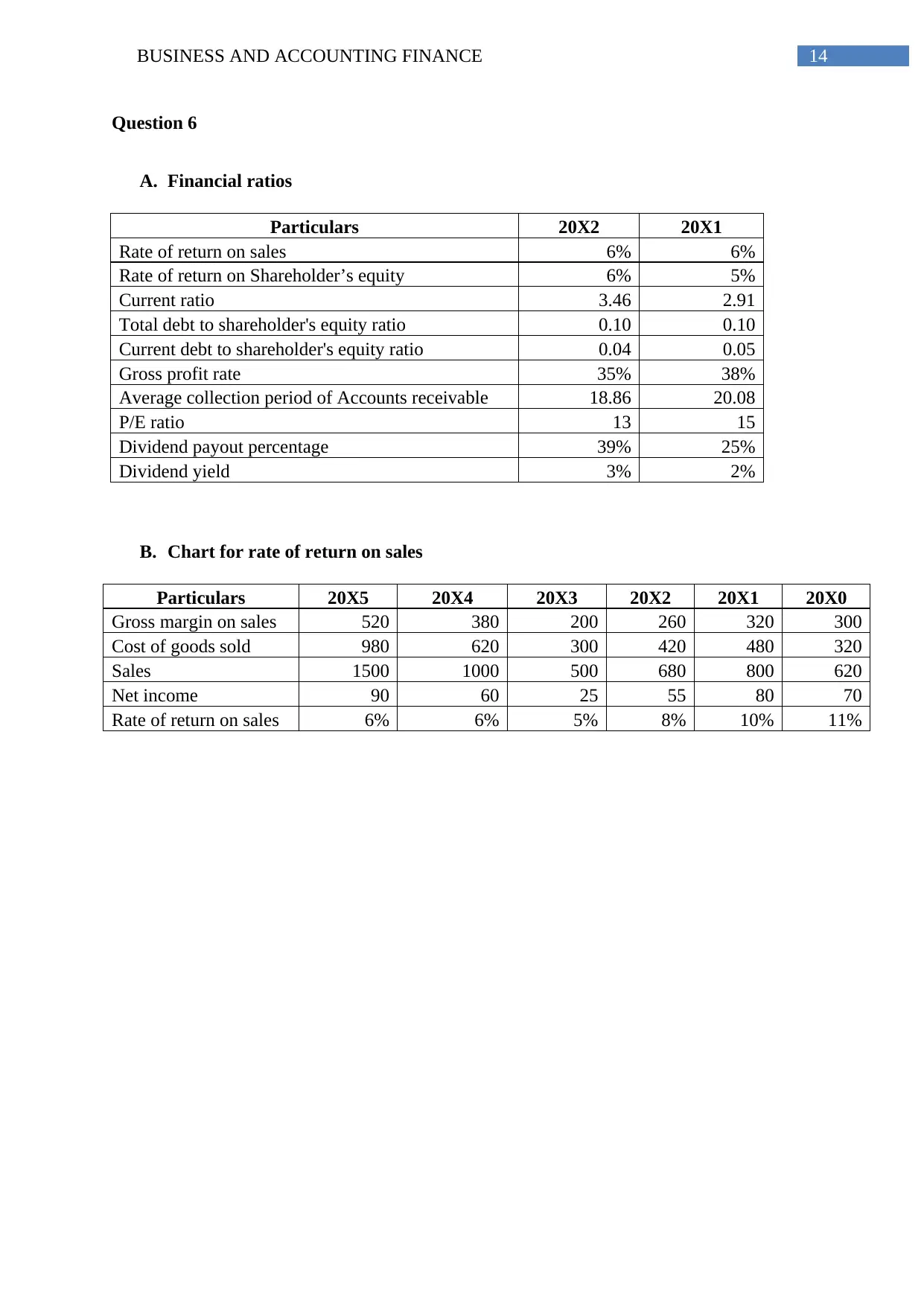

Question 6

A. Financial ratios

Particulars 20X2 20X1

Rate of return on sales 6% 6%

Rate of return on Shareholder’s equity 6% 5%

Current ratio 3.46 2.91

Total debt to shareholder's equity ratio 0.10 0.10

Current debt to shareholder's equity ratio 0.04 0.05

Gross profit rate 35% 38%

Average collection period of Accounts receivable 18.86 20.08

P/E ratio 13 15

Dividend payout percentage 39% 25%

Dividend yield 3% 2%

B. Chart for rate of return on sales

Particulars 20X5 20X4 20X3 20X2 20X1 20X0

Gross margin on sales 520 380 200 260 320 300

Cost of goods sold 980 620 300 420 480 320

Sales 1500 1000 500 680 800 620

Net income 90 60 25 55 80 70

Rate of return on sales 6% 6% 5% 8% 10% 11%

Question 6

A. Financial ratios

Particulars 20X2 20X1

Rate of return on sales 6% 6%

Rate of return on Shareholder’s equity 6% 5%

Current ratio 3.46 2.91

Total debt to shareholder's equity ratio 0.10 0.10

Current debt to shareholder's equity ratio 0.04 0.05

Gross profit rate 35% 38%

Average collection period of Accounts receivable 18.86 20.08

P/E ratio 13 15

Dividend payout percentage 39% 25%

Dividend yield 3% 2%

B. Chart for rate of return on sales

Particulars 20X5 20X4 20X3 20X2 20X1 20X0

Gross margin on sales 520 380 200 260 320 300

Cost of goods sold 980 620 300 420 480 320

Sales 1500 1000 500 680 800 620

Net income 90 60 25 55 80 70

Rate of return on sales 6% 6% 5% 8% 10% 11%

15BUSINESS AND ACCOUNTING FINANCE

Line chart

Rate of return on sales

0%

2%

4%

6%

8%

10%

12%

6%6%

5%

8%

10%

11%

20X5

20X4

20X3

20X2

20X1

20X0

3D column chart

Rate of return on sales

0%

2%

4%

6%

8%

10%

12%

6% 6%

5%

8%

10%

11%

20X5

20X4

20X3

20X2

20X1

20X0

Line chart

Rate of return on sales

0%

2%

4%

6%

8%

10%

12%

6%6%

5%

8%

10%

11%

20X5

20X4

20X3

20X2

20X1

20X0

3D column chart

Rate of return on sales

0%

2%

4%

6%

8%

10%

12%

6% 6%

5%

8%

10%

11%

20X5

20X4

20X3

20X2

20X1

20X0

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16BUSINESS AND ACCOUNTING FINANCE

C. Report on calculation and chart

Calculation – calculation for A for ratio has been done by using various formulas for the

given particular ratios. For the calculation, amount given in the spreadsheet are taken into

consideration. Ratios have been calculated for the year 20X2 as well as 20X1. Details of the

formulas used are mention in the excel sheet on the right hand side of each ratio.

Chart – for preparation of chart on rate of return on sales, amounts for 20X0, 20X1 and 20X2

has been taken from the figures provided. However, for the year 20X3, 20X4 and 20X5 own

made-up data has been considered. The return forecast has been shown through the line graph

and 3D column chart that is selected from the chart tools from the Excel sheet.

Question 7

Business report for decision making aspect

Digital dashboard

Introduction – the digital dashboard is the electronic interface that is used to visualize and

aggregate the data from various sources like web service, locally hosted files and database.

Dashboards assist in monitoring the business performance through display of actionable data,

historical trend and information on real-time basis (Whyte, 2013).

Discussion – each person involved in the business, irrespective of their responsibilities, want

to know the performance of the company. Digital dashboards assist in visualizations of data

to provide the answers of various questions like how many customers are there waiting for

the reply from sales representatives and how the campaign of the company is performing on

the social media. However, the final product requires time for designing (Sjöbergh & Tanaka,

2014). An efficient dashboard is constructed on strong foundation for good data. Further, the

efficient dashboard accumulates data into actionable, meaningful and concise visualizations.

C. Report on calculation and chart

Calculation – calculation for A for ratio has been done by using various formulas for the

given particular ratios. For the calculation, amount given in the spreadsheet are taken into

consideration. Ratios have been calculated for the year 20X2 as well as 20X1. Details of the

formulas used are mention in the excel sheet on the right hand side of each ratio.

Chart – for preparation of chart on rate of return on sales, amounts for 20X0, 20X1 and 20X2

has been taken from the figures provided. However, for the year 20X3, 20X4 and 20X5 own

made-up data has been considered. The return forecast has been shown through the line graph

and 3D column chart that is selected from the chart tools from the Excel sheet.

Question 7

Business report for decision making aspect

Digital dashboard

Introduction – the digital dashboard is the electronic interface that is used to visualize and

aggregate the data from various sources like web service, locally hosted files and database.

Dashboards assist in monitoring the business performance through display of actionable data,

historical trend and information on real-time basis (Whyte, 2013).

Discussion – each person involved in the business, irrespective of their responsibilities, want

to know the performance of the company. Digital dashboards assist in visualizations of data

to provide the answers of various questions like how many customers are there waiting for

the reply from sales representatives and how the campaign of the company is performing on

the social media. However, the final product requires time for designing (Sjöbergh & Tanaka,

2014). An efficient dashboard is constructed on strong foundation for good data. Further, the

efficient dashboard accumulates data into actionable, meaningful and concise visualizations.

17BUSINESS AND ACCOUNTING FINANCE

Conclusion – it is concluded from the above discussion that irrespective of various

departments, the dashboard assists in answering various questions required in business

scenario. Further, the visualizations can take various forms. The users shall identify which

one is appropriate for which business.

Accounting and impression management

Introduction – this is the impression management with regard to the accounting

communication. The impression management seeks to construct the organization’s

impression with the objective of appealing to the audiences evolving the stakeholders,

shareholders, media and general public (Yang & Liu, 2017).

Discussion – if the impression management is successful, then it will undermine the

financial reporting quality along with the misallocation of capital. The impression

management is identified with regard to four aspects. They are – critical, psychological,

economic and socio-logical. Using assumptions that are alternatively rational like

irrationality, bounded rationality, rationality notion and substantive rationality as the social

Conclusion – it is concluded from the above discussion that irrespective of various

departments, the dashboard assists in answering various questions required in business

scenario. Further, the visualizations can take various forms. The users shall identify which

one is appropriate for which business.

Accounting and impression management

Introduction – this is the impression management with regard to the accounting

communication. The impression management seeks to construct the organization’s

impression with the objective of appealing to the audiences evolving the stakeholders,

shareholders, media and general public (Yang & Liu, 2017).

Discussion – if the impression management is successful, then it will undermine the

financial reporting quality along with the misallocation of capital. The impression

management is identified with regard to four aspects. They are – critical, psychological,

economic and socio-logical. Using assumptions that are alternatively rational like

irrationality, bounded rationality, rationality notion and substantive rationality as the social

18BUSINESS AND ACCOUNTING FINANCE

contract, the impression management are segregated as accounting rhetoric, symbolic

management and self-service bias (Brennan & Merkl-Davies, 2013).

Conclusion – from the above discussion, it is concluded that the concept of impression

management is much complex and rich phenomenon as compared to predominant perspective

based on economy. The concept establishes a relationship among the organizational

audiences and managers and focuses on the real reason, real behaviour and real people.

contract, the impression management are segregated as accounting rhetoric, symbolic

management and self-service bias (Brennan & Merkl-Davies, 2013).

Conclusion – from the above discussion, it is concluded that the concept of impression

management is much complex and rich phenomenon as compared to predominant perspective

based on economy. The concept establishes a relationship among the organizational

audiences and managers and focuses on the real reason, real behaviour and real people.

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.