Financial Analysis and Strategies for City Brasserie Ltd: Finance

VerifiedAdded on 2020/01/15

|17

|5303

|159

Report

AI Summary

This report provides a comprehensive financial analysis of City Brasserie Ltd, focusing on the financial aspects of opening a new restaurant. It explores various sources of funding like debt, equity, and retained earnings, recommending equity financing as the most suitable option. The report delves into income generation strategies, including cookery classes, merchandising, and event catering. It evaluates cost elements such as materials, consumables, labor, and overheads, and discusses methods for increasing gross profit. Business methods like stocktaking and cash security are also assessed. The report covers the structure and source of a trial balance, evaluates business accounts, and explains the purpose of financial budgets and variance analysis. Financial ratios are computed, and recommendations are made for improving financial management. The report also categorizes costs, calculates contribution margin, and suggests strategies for earning desired profits. The report concludes with a summary of findings and recommendations to enhance the financial performance of City Brasserie Ltd.

Finance in

hospitality

hospitality

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Introduction......................................................................................................................................3

TASK 1 ...........................................................................................................................................3

a) Sources of funding available for opening new restaurant .......................................................3

b) Sources of income generation .................................................................................................5

Task 2...............................................................................................................................................5

A: Evaluation of cost and gross profit.........................................................................................5

B: Evaluation of business methods..............................................................................................6

Task 3...............................................................................................................................................7

A: Source and structure of trial balance.......................................................................................7

B: Evaluation of business accounts..............................................................................................8

C: Purpose of financial budgets and the process suitable for the budgetary control...................9

D: Variance analysis of budgeted and actual figures...................................................................9

Task 4.............................................................................................................................................10

A: Computation of financial ratios............................................................................................10

B: Recommendation for City Brasserie Ltd for making improvement in their financial

management strategies...............................................................................................................12

Task 5.............................................................................................................................................12

A: Categorization of cost using examples from City Brasserie Ltd..........................................12

B: Calculation of contribution and relationship between cost, profit and volume....................13

C: Recommendation of tickets to be sold in order to earn desired profit..................................14

Conclusion.....................................................................................................................................14

References......................................................................................................................................16

2

Introduction......................................................................................................................................3

TASK 1 ...........................................................................................................................................3

a) Sources of funding available for opening new restaurant .......................................................3

b) Sources of income generation .................................................................................................5

Task 2...............................................................................................................................................5

A: Evaluation of cost and gross profit.........................................................................................5

B: Evaluation of business methods..............................................................................................6

Task 3...............................................................................................................................................7

A: Source and structure of trial balance.......................................................................................7

B: Evaluation of business accounts..............................................................................................8

C: Purpose of financial budgets and the process suitable for the budgetary control...................9

D: Variance analysis of budgeted and actual figures...................................................................9

Task 4.............................................................................................................................................10

A: Computation of financial ratios............................................................................................10

B: Recommendation for City Brasserie Ltd for making improvement in their financial

management strategies...............................................................................................................12

Task 5.............................................................................................................................................12

A: Categorization of cost using examples from City Brasserie Ltd..........................................12

B: Calculation of contribution and relationship between cost, profit and volume....................13

C: Recommendation of tickets to be sold in order to earn desired profit..................................14

Conclusion.....................................................................................................................................14

References......................................................................................................................................16

2

INDEX OF TABLES

Table 1: Format of trial balance .....................................................................................................8

Table 2: Variance analysis of budgeted and actual figures of City Brasserie Ltd.........................10

Table 3: Computation of financial ratios of City Brasserie Ltd.....................................................11

3

Table 1: Format of trial balance .....................................................................................................8

Table 2: Variance analysis of budgeted and actual figures of City Brasserie Ltd.........................10

Table 3: Computation of financial ratios of City Brasserie Ltd.....................................................11

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Finance is regarded as one of the most significant resource of the business without which it

is not possible for company to operate efficiently in the market. Further, hospitality sector

delivers large number of services to its target market due to which its financial requirement is

high. Companies operating in this sector have to consider different sources through which their

financial needs can be satisfied in appropriate manner. Apart from this, different business

accounts are prepared so as to know overall performance of firm such as balance sheet, income

statement etc. (Shim and Siegel, 2008). The present report being prepared is based on City

Brasserie Ltd where at present business is planning to open new restaurant in London. Therefore,

it is required to identify the appropriate source of finance for business. Various tasks have been

covered in the study which involves sources of income generation, elements of cost, source and

structure of trial balance, usefulness of balance sheet, income statement etc.

TASK 1

a) Sources of funding available for opening new restaurant

Different sources of finance are available with city Brasserie Ltd which business can

consider for satisfying its overall need. At present business is planning to open a new restaurant

near the strand in central London. Therefore, to accomplish this overall aim it is required for

business to adopt appropriate source of finance (Hussey and Ong, 2005). Opening up of new

restaurant in the market of UK requires high investment and due to this basic reason company

has to select source which is cheap and in turn large amount of funds can be easily obtained by

business. Following are the sources of finance which are as follows: Debt financing: It is regarded as the act of raising business finance by borrowing money.

Business can consider this source by taking loan from the financial institutions present in

the market. Further, it can enhance liquidity position of the business where expansion can

also take place easily. Main advantage of using debt financing as a source is that it leads

to effective utilization of resources of firm as business has to pay some amount in the

form of interest due to which it becomes necessary to fully utilize the resources. Tax

advantage is also one of the main benefits of considering this source where business can

obtain tax advantage as interest is deductible for income tax purpose. Simple loan

4

Finance is regarded as one of the most significant resource of the business without which it

is not possible for company to operate efficiently in the market. Further, hospitality sector

delivers large number of services to its target market due to which its financial requirement is

high. Companies operating in this sector have to consider different sources through which their

financial needs can be satisfied in appropriate manner. Apart from this, different business

accounts are prepared so as to know overall performance of firm such as balance sheet, income

statement etc. (Shim and Siegel, 2008). The present report being prepared is based on City

Brasserie Ltd where at present business is planning to open new restaurant in London. Therefore,

it is required to identify the appropriate source of finance for business. Various tasks have been

covered in the study which involves sources of income generation, elements of cost, source and

structure of trial balance, usefulness of balance sheet, income statement etc.

TASK 1

a) Sources of funding available for opening new restaurant

Different sources of finance are available with city Brasserie Ltd which business can

consider for satisfying its overall need. At present business is planning to open a new restaurant

near the strand in central London. Therefore, to accomplish this overall aim it is required for

business to adopt appropriate source of finance (Hussey and Ong, 2005). Opening up of new

restaurant in the market of UK requires high investment and due to this basic reason company

has to select source which is cheap and in turn large amount of funds can be easily obtained by

business. Following are the sources of finance which are as follows: Debt financing: It is regarded as the act of raising business finance by borrowing money.

Business can consider this source by taking loan from the financial institutions present in

the market. Further, it can enhance liquidity position of the business where expansion can

also take place easily. Main advantage of using debt financing as a source is that it leads

to effective utilization of resources of firm as business has to pay some amount in the

form of interest due to which it becomes necessary to fully utilize the resources. Tax

advantage is also one of the main benefits of considering this source where business can

obtain tax advantage as interest is deductible for income tax purpose. Simple loan

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

repayment is also one of the advantages of this source where lenders are only entitled to

loan repayment and interest on loan (Keller, 2013). Further, future impact forecasting is

also one of the main advantage of this source where principal repayment along with

interest are based on fixed percentage and it is possible to forecast. On the other hand this

source has some disadvantage which are regular payments of installment is required and

this leads to rise in expenditure level of the company. Further, many times it is possible

that financial institutions may impose penalty for late payment and this may have adverse

impact on city Brasserie Ltd. Apart from this failure to make payment on loan can have

negative impact on credit rating of the organization. Therefore, in this way these are some

of the main disadvantage of this source which company has to consider. Equity: For obtaining large amount of funds it is possible for city Brasserie Ltd to issue

equity shares in the market. Further, through this source funds can be obtained from

investors who may purchase shares of company (Cox and Fardon, 2005). Main advantage

of this source is that business does not have to keep cost of debt financing, right business

angels bring valuable skills, investors are attracted to provide follow up funding etc. On

the other hand some disadvantage of this source is that equity financing is demanding,

costly and time consuming.

Retained earnings: It is also regarded as one of the most effective source of finance

where business can utilize its savings for satisfying its expansion needs. Further, main

advantage of this source is that large amount of funds can be obtained easily and it is not

required to bear any cost (Keller, 2013). On the other hand it reduces overall savings of

firm which is major drawback.

Out of all these three sources most appropriate one for city Brasserie Ltd is equity

financing where organization can easily issue equity shares in the market and amount for

expansion can be obtained easily. Main reason behind not recommending debt financing is that

business has already taken loan from bank of large amount and this source will not be

appropriate for firm as interest cost will rise. Further, retained earnings as a source cannot be

considered by business as large amount is required for investment.

5

loan repayment and interest on loan (Keller, 2013). Further, future impact forecasting is

also one of the main advantage of this source where principal repayment along with

interest are based on fixed percentage and it is possible to forecast. On the other hand this

source has some disadvantage which are regular payments of installment is required and

this leads to rise in expenditure level of the company. Further, many times it is possible

that financial institutions may impose penalty for late payment and this may have adverse

impact on city Brasserie Ltd. Apart from this failure to make payment on loan can have

negative impact on credit rating of the organization. Therefore, in this way these are some

of the main disadvantage of this source which company has to consider. Equity: For obtaining large amount of funds it is possible for city Brasserie Ltd to issue

equity shares in the market. Further, through this source funds can be obtained from

investors who may purchase shares of company (Cox and Fardon, 2005). Main advantage

of this source is that business does not have to keep cost of debt financing, right business

angels bring valuable skills, investors are attracted to provide follow up funding etc. On

the other hand some disadvantage of this source is that equity financing is demanding,

costly and time consuming.

Retained earnings: It is also regarded as one of the most effective source of finance

where business can utilize its savings for satisfying its expansion needs. Further, main

advantage of this source is that large amount of funds can be obtained easily and it is not

required to bear any cost (Keller, 2013). On the other hand it reduces overall savings of

firm which is major drawback.

Out of all these three sources most appropriate one for city Brasserie Ltd is equity

financing where organization can easily issue equity shares in the market and amount for

expansion can be obtained easily. Main reason behind not recommending debt financing is that

business has already taken loan from bank of large amount and this source will not be

appropriate for firm as interest cost will rise. Further, retained earnings as a source cannot be

considered by business as large amount is required for investment.

5

b) Sources of income generation

Different sources of income are present which City Brasserie Ltd which business can

consider for enhancing its overall profitability level. Such sources are: Cookery classes: Chefs working in City Brasserie Ltd can organize cookery classes and

can charged fess from individual for the same. This will be appropriate source of income

for company and people can learn about preparing different dishes etc. This services can

be provided by the ideal labour of the restaurant in the morning time in which there are

fewer customers in restaurant (Portz and Lere, 2010). In this manner, they will be able to

make optimum utilization of available resources. Merchandising with cookbooks and kitchen items: For City Brasserie Ltd it is possible

to introduce cookbooks and kitchen items. Further, same can be offered to local public so

that they can know about the ways through which different dishes can be prepared.

Therefore, this will also be appropriate source of income. City Brasserie Ltd is reputed

French restaurant with good market image. On the basis of their goodwill they can sell

their cooking recipes to the customers (Ojha, Gianiodis and Manuj, 2013). For this

activity, they do not required to incur heavy expenses but they can earn good profits from

this source.

Events catering: Company can take catering order of different events such as party,

marriage etc and income can be earned by charging fees from the same. For this source,

they can introduce different themes for their customers in order to make their experience

more memorable. They can also provide their services to the commercial entities by

getting associated with them.

TASK 2

A: Evaluation of cost and gross profit

Elements of costs including labour, consumables and overheads

Elements of cost can be defined as the expenditure occurred by business entity for the

manufacturing process of the cost centres (Curzon and Wingler, 2013). In the context to the City

Brasserie Ltd, description of cost components is as follows:

6

Different sources of income are present which City Brasserie Ltd which business can

consider for enhancing its overall profitability level. Such sources are: Cookery classes: Chefs working in City Brasserie Ltd can organize cookery classes and

can charged fess from individual for the same. This will be appropriate source of income

for company and people can learn about preparing different dishes etc. This services can

be provided by the ideal labour of the restaurant in the morning time in which there are

fewer customers in restaurant (Portz and Lere, 2010). In this manner, they will be able to

make optimum utilization of available resources. Merchandising with cookbooks and kitchen items: For City Brasserie Ltd it is possible

to introduce cookbooks and kitchen items. Further, same can be offered to local public so

that they can know about the ways through which different dishes can be prepared.

Therefore, this will also be appropriate source of income. City Brasserie Ltd is reputed

French restaurant with good market image. On the basis of their goodwill they can sell

their cooking recipes to the customers (Ojha, Gianiodis and Manuj, 2013). For this

activity, they do not required to incur heavy expenses but they can earn good profits from

this source.

Events catering: Company can take catering order of different events such as party,

marriage etc and income can be earned by charging fees from the same. For this source,

they can introduce different themes for their customers in order to make their experience

more memorable. They can also provide their services to the commercial entities by

getting associated with them.

TASK 2

A: Evaluation of cost and gross profit

Elements of costs including labour, consumables and overheads

Elements of cost can be defined as the expenditure occurred by business entity for the

manufacturing process of the cost centres (Curzon and Wingler, 2013). In the context to the City

Brasserie Ltd, description of cost components is as follows:

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Materials: Materials cost are involved when finished goods are ready to sell to the

consumers. Materials can be of raw materials and finished materials. Example of material

in City Brasserie Ltd crockery, knives, silverware etc. Consumables: Consumables can be termed as the goods which are consumed by the

consumers (Elearn, 2013). It can be used for consumption either to spent or wasted.

These includes napkins, cutlery, food and beverages items. Labor: Labor is consists of human resources who was charged for the work in the

industry. For example: management and all the staff members.

Overhead Costs: It is the type of expenses which does not include labour, materials and

other expenses. It is also known as indirect cost. It includes electricity costs, telephone

bills, rent, taxes etc.

Increase in gross profit percentages by changing selling prices

For the increase in the gross profit percentage, one should consider their market price

point which should be fair, every expenses of the business and menu item cost. One can increase

their profit by changing selling price of their cost or product. Gross profit can be obtained from

cost of goods minus revenue (Keller, 2013). The difference between cost of goods sold and

revenues is known as gross profit. This aspect shows that increase in selling price will make

increase in gross profits.

B: Evaluation of business methods

Stock taking for control and management

for City Brasserie Ltd

Stock taking can be defined as procedure for the recording amount of stock held by

business. It is an effective method for the management of inventory in the business. This method

provides accurate information regarding recording of inventory by which management can make

decisions regarding order quantity and duration. In addition to this, company will be able to

minimize their storage and carrying cost.

Stock taking also assists in reduction of abnormal cost by making proper inventory

management. Further, by making use of this method the movement of stores items can be

watched more closely by the store auditor (Gitman, 2013). With this approach, chances of

obsolescence buying will be reduced. In addition to this final accounts can be quickly prepared.

7

consumers. Materials can be of raw materials and finished materials. Example of material

in City Brasserie Ltd crockery, knives, silverware etc. Consumables: Consumables can be termed as the goods which are consumed by the

consumers (Elearn, 2013). It can be used for consumption either to spent or wasted.

These includes napkins, cutlery, food and beverages items. Labor: Labor is consists of human resources who was charged for the work in the

industry. For example: management and all the staff members.

Overhead Costs: It is the type of expenses which does not include labour, materials and

other expenses. It is also known as indirect cost. It includes electricity costs, telephone

bills, rent, taxes etc.

Increase in gross profit percentages by changing selling prices

For the increase in the gross profit percentage, one should consider their market price

point which should be fair, every expenses of the business and menu item cost. One can increase

their profit by changing selling price of their cost or product. Gross profit can be obtained from

cost of goods minus revenue (Keller, 2013). The difference between cost of goods sold and

revenues is known as gross profit. This aspect shows that increase in selling price will make

increase in gross profits.

B: Evaluation of business methods

Stock taking for control and management

for City Brasserie Ltd

Stock taking can be defined as procedure for the recording amount of stock held by

business. It is an effective method for the management of inventory in the business. This method

provides accurate information regarding recording of inventory by which management can make

decisions regarding order quantity and duration. In addition to this, company will be able to

minimize their storage and carrying cost.

Stock taking also assists in reduction of abnormal cost by making proper inventory

management. Further, by making use of this method the movement of stores items can be

watched more closely by the store auditor (Gitman, 2013). With this approach, chances of

obsolescence buying will be reduced. In addition to this final accounts can be quickly prepared.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

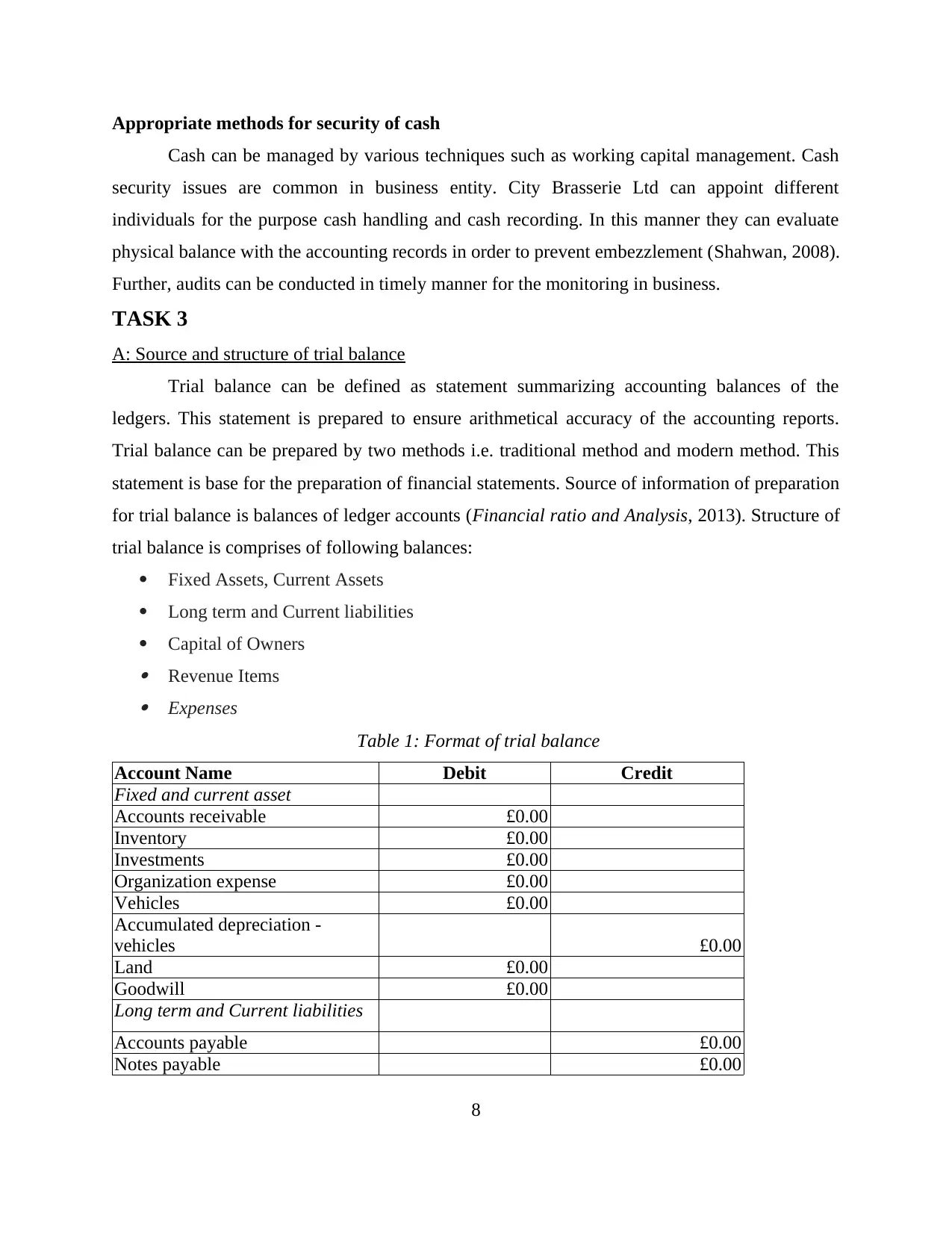

Appropriate methods for security of cash

Cash can be managed by various techniques such as working capital management. Cash

security issues are common in business entity. City Brasserie Ltd can appoint different

individuals for the purpose cash handling and cash recording. In this manner they can evaluate

physical balance with the accounting records in order to prevent embezzlement (Shahwan, 2008).

Further, audits can be conducted in timely manner for the monitoring in business.

TASK 3

A: Source and structure of trial balance

Trial balance can be defined as statement summarizing accounting balances of the

ledgers. This statement is prepared to ensure arithmetical accuracy of the accounting reports.

Trial balance can be prepared by two methods i.e. traditional method and modern method. This

statement is base for the preparation of financial statements. Source of information of preparation

for trial balance is balances of ledger accounts (Financial ratio and Analysis, 2013). Structure of

trial balance is comprises of following balances:

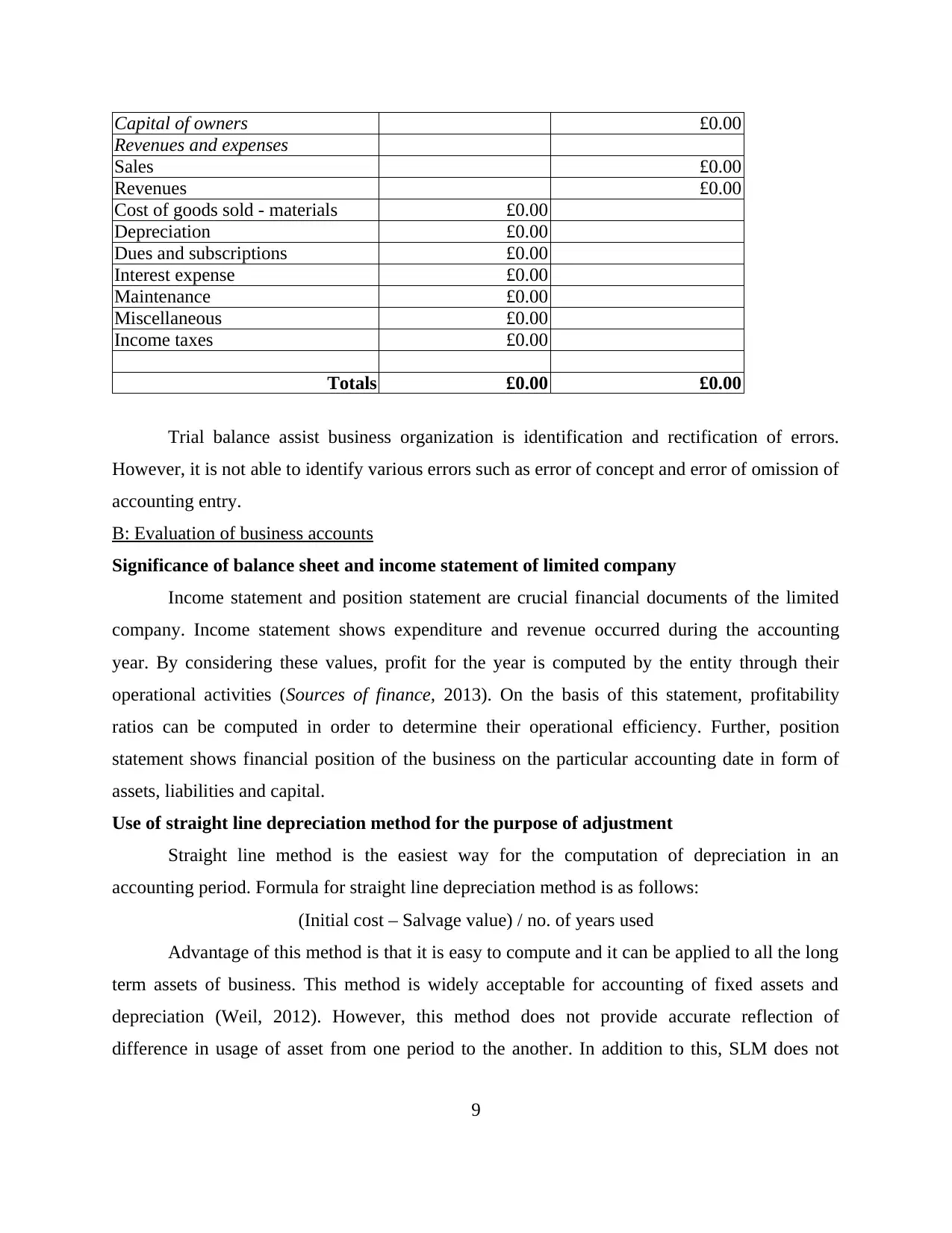

Fixed Assets, Current Assets

Long term and Current liabilities

Capital of Owners Revenue Items Expenses

Table 1: Format of trial balance

Account Name Debit Credit

Fixed and current asset

Accounts receivable £0.00

Inventory £0.00

Investments £0.00

Organization expense £0.00

Vehicles £0.00

Accumulated depreciation -

vehicles £0.00

Land £0.00

Goodwill £0.00

Long term and Current liabilities

Accounts payable £0.00

Notes payable £0.00

8

Cash can be managed by various techniques such as working capital management. Cash

security issues are common in business entity. City Brasserie Ltd can appoint different

individuals for the purpose cash handling and cash recording. In this manner they can evaluate

physical balance with the accounting records in order to prevent embezzlement (Shahwan, 2008).

Further, audits can be conducted in timely manner for the monitoring in business.

TASK 3

A: Source and structure of trial balance

Trial balance can be defined as statement summarizing accounting balances of the

ledgers. This statement is prepared to ensure arithmetical accuracy of the accounting reports.

Trial balance can be prepared by two methods i.e. traditional method and modern method. This

statement is base for the preparation of financial statements. Source of information of preparation

for trial balance is balances of ledger accounts (Financial ratio and Analysis, 2013). Structure of

trial balance is comprises of following balances:

Fixed Assets, Current Assets

Long term and Current liabilities

Capital of Owners Revenue Items Expenses

Table 1: Format of trial balance

Account Name Debit Credit

Fixed and current asset

Accounts receivable £0.00

Inventory £0.00

Investments £0.00

Organization expense £0.00

Vehicles £0.00

Accumulated depreciation -

vehicles £0.00

Land £0.00

Goodwill £0.00

Long term and Current liabilities

Accounts payable £0.00

Notes payable £0.00

8

Capital of owners £0.00

Revenues and expenses

Sales £0.00

Revenues £0.00

Cost of goods sold - materials £0.00

Depreciation £0.00

Dues and subscriptions £0.00

Interest expense £0.00

Maintenance £0.00

Miscellaneous £0.00

Income taxes £0.00

Totals £0.00 £0.00

Trial balance assist business organization is identification and rectification of errors.

However, it is not able to identify various errors such as error of concept and error of omission of

accounting entry.

B: Evaluation of business accounts

Significance of balance sheet and income statement of limited company

Income statement and position statement are crucial financial documents of the limited

company. Income statement shows expenditure and revenue occurred during the accounting

year. By considering these values, profit for the year is computed by the entity through their

operational activities (Sources of finance, 2013). On the basis of this statement, profitability

ratios can be computed in order to determine their operational efficiency. Further, position

statement shows financial position of the business on the particular accounting date in form of

assets, liabilities and capital.

Use of straight line depreciation method for the purpose of adjustment

Straight line method is the easiest way for the computation of depreciation in an

accounting period. Formula for straight line depreciation method is as follows:

(Initial cost – Salvage value) / no. of years used

Advantage of this method is that it is easy to compute and it can be applied to all the long

term assets of business. This method is widely acceptable for accounting of fixed assets and

depreciation (Weil, 2012). However, this method does not provide accurate reflection of

difference in usage of asset from one period to the another. In addition to this, SLM does not

9

Revenues and expenses

Sales £0.00

Revenues £0.00

Cost of goods sold - materials £0.00

Depreciation £0.00

Dues and subscriptions £0.00

Interest expense £0.00

Maintenance £0.00

Miscellaneous £0.00

Income taxes £0.00

Totals £0.00 £0.00

Trial balance assist business organization is identification and rectification of errors.

However, it is not able to identify various errors such as error of concept and error of omission of

accounting entry.

B: Evaluation of business accounts

Significance of balance sheet and income statement of limited company

Income statement and position statement are crucial financial documents of the limited

company. Income statement shows expenditure and revenue occurred during the accounting

year. By considering these values, profit for the year is computed by the entity through their

operational activities (Sources of finance, 2013). On the basis of this statement, profitability

ratios can be computed in order to determine their operational efficiency. Further, position

statement shows financial position of the business on the particular accounting date in form of

assets, liabilities and capital.

Use of straight line depreciation method for the purpose of adjustment

Straight line method is the easiest way for the computation of depreciation in an

accounting period. Formula for straight line depreciation method is as follows:

(Initial cost – Salvage value) / no. of years used

Advantage of this method is that it is easy to compute and it can be applied to all the long

term assets of business. This method is widely acceptable for accounting of fixed assets and

depreciation (Weil, 2012). However, this method does not provide accurate reflection of

difference in usage of asset from one period to the another. In addition to this, SLM does not

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

necessarily match cost with the revenues in various types of long term assets. This method is not

appropriate for the assets with rapid developing technology.

Importance of account notes

Account notes are significant for user as it provides descriptive information of the

financial figures used in financial statements of the limited company (Hussey and Ong, 2005).

These notes provide complete understanding of specific terms and financial conditions of the

company.

C: Purpose of financial budgets and the process suitable for the budgetary control

Purpose of financial budgets

Budgets are prepared by business organizations in order to forecast future activities. On

the basis of this forecasting, resources are allocated by the management in order to make its

effective utilization. Financial budgets also assist in management of inflow and outflow of cash

to maintain proper liquidity and solvency in business. In addition to this, it also mitigates future

risk by taking pro-active steps in business.

Process for budgetary control

Budgetary control can be defined as technique for the comparison of actual results with

the budgeted results (Winand and et. al, 2012). On the basis of this comparison variances are

computed in order to make viable modification by the business. Planning by the management of

City Brasserie Ltd cannot get successful if it is not supported by efficient and effective system of

control. Process of budgetary control is inclusive of preparation of several budgets, comparison

of actual results with the budgeted figures and revision of budgets in order to make valuable

changes in operational activities. System of budgetary control is not rigid because company is

required to modify it with the changing circumstances.

D: Variance analysis of budgeted and actual figures

(i) Indicative for occurrence of favourable and adverse variance

Table 2: Variance analysis of budgeted and actual figures of City Brasserie Ltd

Particulars Budgeted Figures Actual Figures Variance

Adverse or

favourable

Sales £70,000.00 £65,000.00 -£5,000.00 Adverse

Cost of Goods Sold £15,000.00 £13,500.00 £1,500.00 Favourable

10

appropriate for the assets with rapid developing technology.

Importance of account notes

Account notes are significant for user as it provides descriptive information of the

financial figures used in financial statements of the limited company (Hussey and Ong, 2005).

These notes provide complete understanding of specific terms and financial conditions of the

company.

C: Purpose of financial budgets and the process suitable for the budgetary control

Purpose of financial budgets

Budgets are prepared by business organizations in order to forecast future activities. On

the basis of this forecasting, resources are allocated by the management in order to make its

effective utilization. Financial budgets also assist in management of inflow and outflow of cash

to maintain proper liquidity and solvency in business. In addition to this, it also mitigates future

risk by taking pro-active steps in business.

Process for budgetary control

Budgetary control can be defined as technique for the comparison of actual results with

the budgeted results (Winand and et. al, 2012). On the basis of this comparison variances are

computed in order to make viable modification by the business. Planning by the management of

City Brasserie Ltd cannot get successful if it is not supported by efficient and effective system of

control. Process of budgetary control is inclusive of preparation of several budgets, comparison

of actual results with the budgeted figures and revision of budgets in order to make valuable

changes in operational activities. System of budgetary control is not rigid because company is

required to modify it with the changing circumstances.

D: Variance analysis of budgeted and actual figures

(i) Indicative for occurrence of favourable and adverse variance

Table 2: Variance analysis of budgeted and actual figures of City Brasserie Ltd

Particulars Budgeted Figures Actual Figures Variance

Adverse or

favourable

Sales £70,000.00 £65,000.00 -£5,000.00 Adverse

Cost of Goods Sold £15,000.00 £13,500.00 £1,500.00 Favourable

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Gross Profit £55,000.00 £51,500.00 £3,500.00 Favourable

Labour Costs £15,000.00 £19,000.00 -£4,000.00 Adverse

Direct Expense Costs £7,000.00 £6,500.00 £500.00 Favourable

Overhead Costs £8,000.00 £8,500.00 -£500.00 Adverse

Net Profit £25,000.00 £17,500.00 -£7,500.00 Adverse

(ii) Justified suggestions for appropriate future management

action

In accordance with the variance analysis, management of City Brasserie Ltd is

recommended to make appropriate forecast by considering changing market trend and values. In

addition to this, company is recommended to render service as per demand in the market. In this

manner, company will be able to make optimum utilization of available resources in order to

enhance their profitability (Arnold, 2005). Company is also required to enhance their efficiency

to make reduction in their expenses and abnormal wastage of the available resources. For this

aspect, they can install new plant and machinery in the business. With this approach they will be

able to enhance their production capacity to attain cost advantages. Further, in order to determine

demand in the market they are required to conduct market survey.

TASK 4

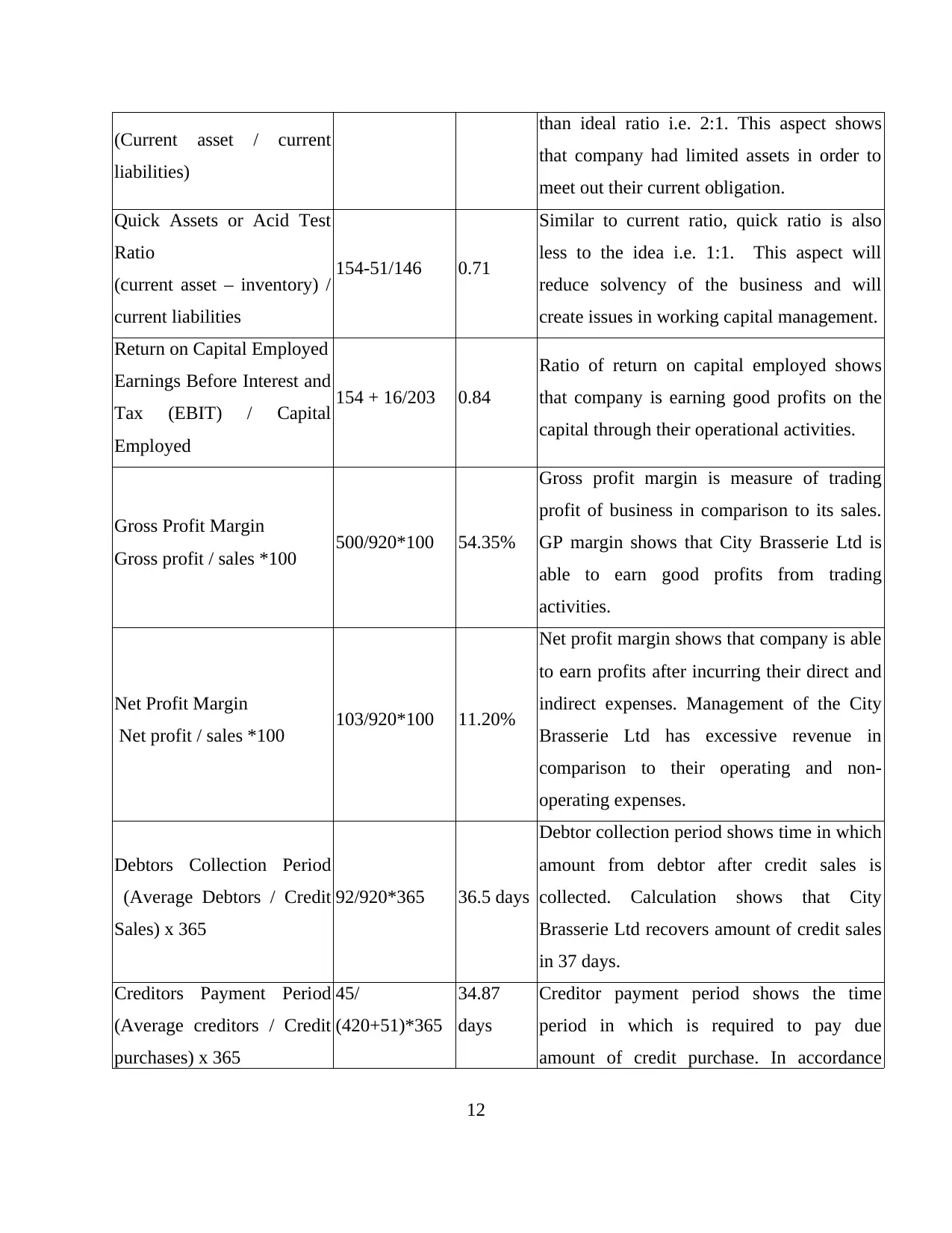

A: Computation of financial ratios

Financial ratios are computed to analyse financial position of business by considering

profit and loss account and balance sheet. Ratio is a numerical expression which shows

relationship between two variables (Vice, 2013). Computation of financial ratios of City

Brasserie Ltd is as follows:

Table 3: Computation of financial ratios of City Brasserie Ltd

Ratio and Formula Calculation Answer Interpretation

Current ratio 154/146 1.05 Current ratio of City Brasserie Ltd is less

11

Labour Costs £15,000.00 £19,000.00 -£4,000.00 Adverse

Direct Expense Costs £7,000.00 £6,500.00 £500.00 Favourable

Overhead Costs £8,000.00 £8,500.00 -£500.00 Adverse

Net Profit £25,000.00 £17,500.00 -£7,500.00 Adverse

(ii) Justified suggestions for appropriate future management

action

In accordance with the variance analysis, management of City Brasserie Ltd is

recommended to make appropriate forecast by considering changing market trend and values. In

addition to this, company is recommended to render service as per demand in the market. In this

manner, company will be able to make optimum utilization of available resources in order to

enhance their profitability (Arnold, 2005). Company is also required to enhance their efficiency

to make reduction in their expenses and abnormal wastage of the available resources. For this

aspect, they can install new plant and machinery in the business. With this approach they will be

able to enhance their production capacity to attain cost advantages. Further, in order to determine

demand in the market they are required to conduct market survey.

TASK 4

A: Computation of financial ratios

Financial ratios are computed to analyse financial position of business by considering

profit and loss account and balance sheet. Ratio is a numerical expression which shows

relationship between two variables (Vice, 2013). Computation of financial ratios of City

Brasserie Ltd is as follows:

Table 3: Computation of financial ratios of City Brasserie Ltd

Ratio and Formula Calculation Answer Interpretation

Current ratio 154/146 1.05 Current ratio of City Brasserie Ltd is less

11

(Current asset / current

liabilities)

than ideal ratio i.e. 2:1. This aspect shows

that company had limited assets in order to

meet out their current obligation.

Quick Assets or Acid Test

Ratio

(current asset – inventory) /

current liabilities

154-51/146 0.71

Similar to current ratio, quick ratio is also

less to the idea i.e. 1:1. This aspect will

reduce solvency of the business and will

create issues in working capital management.

Return on Capital Employed

Earnings Before Interest and

Tax (EBIT) / Capital

Employed

154 + 16/203 0.84

Ratio of return on capital employed shows

that company is earning good profits on the

capital through their operational activities.

Gross Profit Margin

Gross profit / sales *100 500/920*100 54.35%

Gross profit margin is measure of trading

profit of business in comparison to its sales.

GP margin shows that City Brasserie Ltd is

able to earn good profits from trading

activities.

Net Profit Margin

Net profit / sales *100 103/920*100 11.20%

Net profit margin shows that company is able

to earn profits after incurring their direct and

indirect expenses. Management of the City

Brasserie Ltd has excessive revenue in

comparison to their operating and non-

operating expenses.

Debtors Collection Period

(Average Debtors / Credit

Sales) x 365

92/920*365 36.5 days

Debtor collection period shows time in which

amount from debtor after credit sales is

collected. Calculation shows that City

Brasserie Ltd recovers amount of credit sales

in 37 days.

Creditors Payment Period

(Average creditors / Credit

purchases) x 365

45/

(420+51)*365

34.87

days

Creditor payment period shows the time

period in which is required to pay due

amount of credit purchase. In accordance

12

liabilities)

than ideal ratio i.e. 2:1. This aspect shows

that company had limited assets in order to

meet out their current obligation.

Quick Assets or Acid Test

Ratio

(current asset – inventory) /

current liabilities

154-51/146 0.71

Similar to current ratio, quick ratio is also

less to the idea i.e. 1:1. This aspect will

reduce solvency of the business and will

create issues in working capital management.

Return on Capital Employed

Earnings Before Interest and

Tax (EBIT) / Capital

Employed

154 + 16/203 0.84

Ratio of return on capital employed shows

that company is earning good profits on the

capital through their operational activities.

Gross Profit Margin

Gross profit / sales *100 500/920*100 54.35%

Gross profit margin is measure of trading

profit of business in comparison to its sales.

GP margin shows that City Brasserie Ltd is

able to earn good profits from trading

activities.

Net Profit Margin

Net profit / sales *100 103/920*100 11.20%

Net profit margin shows that company is able

to earn profits after incurring their direct and

indirect expenses. Management of the City

Brasserie Ltd has excessive revenue in

comparison to their operating and non-

operating expenses.

Debtors Collection Period

(Average Debtors / Credit

Sales) x 365

92/920*365 36.5 days

Debtor collection period shows time in which

amount from debtor after credit sales is

collected. Calculation shows that City

Brasserie Ltd recovers amount of credit sales

in 37 days.

Creditors Payment Period

(Average creditors / Credit

purchases) x 365

45/

(420+51)*365

34.87

days

Creditor payment period shows the time

period in which is required to pay due

amount of credit purchase. In accordance

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.