Management Accounting Report: Analysis of R.L. Maynard's Finances

VerifiedAdded on 2020/01/23

|16

|5023

|132

Report

AI Summary

This report provides a detailed analysis of management accounting practices within the R.L. Maynard Company, a UK-based restaurant with less than 50 employees and an annual turnover under £500,000. It explores various management accounting systems utilized, including cost accounting, inventory management, job costing, and price optimizing systems. The report further examines different methods of management accounting reporting, such as job cost reports, inventory management reports, operating budget reports, accounts receivable aging reports, and performance reports. Additionally, it delves into the calculation of costs through various methods, including fixed, variable, and semi-variable costs. The report also discusses the advantages and disadvantages of different planning tools used in budgetary control and concludes by examining the application of management accounting systems in addressing financial problems within the company. The report provides a comprehensive overview of the financial and accounting strategies employed by the restaurant to aid in managerial decision-making and improve stakeholder value.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and different types of management accounting systems...............1

P2 Different methods used for management accounting reporting.............................................3

TASK 2............................................................................................................................................5

P3 Calculation of cost through different methods.......................................................................5

TASK 3............................................................................................................................................8

P4 Advantages and disadvantages of different planning tools used in Budgetary control.........8

P5 Management accounting systems in solving financial problems.........................................10

CONCLUSION.............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and different types of management accounting systems...............1

P2 Different methods used for management accounting reporting.............................................3

TASK 2............................................................................................................................................5

P3 Calculation of cost through different methods.......................................................................5

TASK 3............................................................................................................................................8

P4 Advantages and disadvantages of different planning tools used in Budgetary control.........8

P5 Management accounting systems in solving financial problems.........................................10

CONCLUSION.............................................................................................................................12

REFERENCES..............................................................................................................................13

Illustration Index

Illustration 1: Calculation of cost through absorption costing.........................................................6

Illustration 2: Calculation of cost through marginal costing...........................................................6

Illustration 1: Calculation of cost through absorption costing.........................................................6

Illustration 2: Calculation of cost through marginal costing...........................................................6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

The management accounting is a process in which different techniques are used for

making use of various resources of the company so that managers can be aided in the function of

taking significant decisions and increase the value of customers and shareholders. The said

accounting is a technique in which through effective processes, the decisions related to financial

and non financial matters are considered. The present report is based on management accounting

in which the major focus is laid on different vital aspects of the said discipline. In business

organisation, the use of management accounting is inevitable and useful (Elbashir, Collier and

Sutton, 2011). The present report has discussed the entire management accounting on R.L.

Maynard company which is a well known restaurant in UK. The mentioned restaurant has less

than 50 employees and the annual turnover is also not more than £500,000. In the present report,

the discussion will be made on various accounting systems and that are followed by mentioned

enterprise. Besides this, it has a discussion over various methods that are used for management

accounting. In addition to this, the report will have a discussion over different costing techniques

that are used by the firm. Besides this the final section will be focussing on use of accounting

system in solving the financial problems.

TASK 1

P1 Management accounting and different types of management accounting systems

Management accounting system is a significant tool which can be referred as the

information system that generates useful information asked by the managers for managing the

resources and creating value for various stakeholders (Garrison and et.al., 2010). Further, the

accounting system act on ad hoc terms so that decision related to short and long durations can be

made. Thus, it prepares a wider information system within the firm. The R.L. Maynard company

use this system so that different crucial information can be accessed regularly as and when

required by the concerned persons. The said accounting system includes different types of

information like cost of producing goods and services, details regarding planning and control

functions and performance measurements. The major accounting systems that are used by

mentioned enterprise are as follows:

Cost accounting system: The cost accounting system takes into consideration different

estimates regarding the cost incurred on production of goods and services (Ward, 2012).

1

The management accounting is a process in which different techniques are used for

making use of various resources of the company so that managers can be aided in the function of

taking significant decisions and increase the value of customers and shareholders. The said

accounting is a technique in which through effective processes, the decisions related to financial

and non financial matters are considered. The present report is based on management accounting

in which the major focus is laid on different vital aspects of the said discipline. In business

organisation, the use of management accounting is inevitable and useful (Elbashir, Collier and

Sutton, 2011). The present report has discussed the entire management accounting on R.L.

Maynard company which is a well known restaurant in UK. The mentioned restaurant has less

than 50 employees and the annual turnover is also not more than £500,000. In the present report,

the discussion will be made on various accounting systems and that are followed by mentioned

enterprise. Besides this, it has a discussion over various methods that are used for management

accounting. In addition to this, the report will have a discussion over different costing techniques

that are used by the firm. Besides this the final section will be focussing on use of accounting

system in solving the financial problems.

TASK 1

P1 Management accounting and different types of management accounting systems

Management accounting system is a significant tool which can be referred as the

information system that generates useful information asked by the managers for managing the

resources and creating value for various stakeholders (Garrison and et.al., 2010). Further, the

accounting system act on ad hoc terms so that decision related to short and long durations can be

made. Thus, it prepares a wider information system within the firm. The R.L. Maynard company

use this system so that different crucial information can be accessed regularly as and when

required by the concerned persons. The said accounting system includes different types of

information like cost of producing goods and services, details regarding planning and control

functions and performance measurements. The major accounting systems that are used by

mentioned enterprise are as follows:

Cost accounting system: The cost accounting system takes into consideration different

estimates regarding the cost incurred on production of goods and services (Ward, 2012).

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Besides this, it also considers the prices which of each unit working within the company

department wise. By referring the cost accounting reports, the management gets

information on cost data which is useful in controlling the operations of business in

present as well as in future. This accounting system is usually used by manufacturing

industries, retailers and service providers on wider basis. The major benefit of utilising

this system by mentioned hotel is the help provided in determination of costs due to

which the organisation can easily take decisions of marketing. Further, it becomes more

simple for the firm to determine selling prices and attain competitive advantages. Thus,

they easily analyse their profitability earned from their performance (Baldvinsdottir,

Mitchell and Nørreklit, 2010).

Inventory management system: The inventory can be termed as all those resources which

are utilised by the enterprise in various forms of raw material, work in progress and end

products as well. The inventory management system is necessary to be monitored so that

the company can have the knowledge regarding level of stock within the organisation.

Besides this, it will also help in placing order on time for the products which are getting

finished from the stock. Thus, the enterprise can have various benefits by protecting

themselves from various types of uncertainties like scarcity of raw material or finished

goods, changes in demand patterns etc. Besides this, it will also help in getting

advantages of economies of scale in all the operations of business.

Job costing system: The Job costing system is used by the companies for allocating the

cost for either individual or batches of products. This costing system is usually used when

manufactured goods and services are completely different from each other (Lukka and

Modell, 2010). The stated business firm utilise the job costing system as it deals in

various types of products and services that are different from each other in adequate

manner. The job costing system is best suitable in those business where entire work is

based on customers' demands and the orders are also of less duration. Thus, it aids in

planning and also in the function of cost controlling. The R.L. Maynard company has its

more utility as it depends to give services on the demands of customers and their needs.

Price optimising systems: This is an effective management accounting system that aids

the business organisations in determining the price sensitivity and its impact on

customers. The mentioned entity can use this system so as to attain information about

2

department wise. By referring the cost accounting reports, the management gets

information on cost data which is useful in controlling the operations of business in

present as well as in future. This accounting system is usually used by manufacturing

industries, retailers and service providers on wider basis. The major benefit of utilising

this system by mentioned hotel is the help provided in determination of costs due to

which the organisation can easily take decisions of marketing. Further, it becomes more

simple for the firm to determine selling prices and attain competitive advantages. Thus,

they easily analyse their profitability earned from their performance (Baldvinsdottir,

Mitchell and Nørreklit, 2010).

Inventory management system: The inventory can be termed as all those resources which

are utilised by the enterprise in various forms of raw material, work in progress and end

products as well. The inventory management system is necessary to be monitored so that

the company can have the knowledge regarding level of stock within the organisation.

Besides this, it will also help in placing order on time for the products which are getting

finished from the stock. Thus, the enterprise can have various benefits by protecting

themselves from various types of uncertainties like scarcity of raw material or finished

goods, changes in demand patterns etc. Besides this, it will also help in getting

advantages of economies of scale in all the operations of business.

Job costing system: The Job costing system is used by the companies for allocating the

cost for either individual or batches of products. This costing system is usually used when

manufactured goods and services are completely different from each other (Lukka and

Modell, 2010). The stated business firm utilise the job costing system as it deals in

various types of products and services that are different from each other in adequate

manner. The job costing system is best suitable in those business where entire work is

based on customers' demands and the orders are also of less duration. Thus, it aids in

planning and also in the function of cost controlling. The R.L. Maynard company has its

more utility as it depends to give services on the demands of customers and their needs.

Price optimising systems: This is an effective management accounting system that aids

the business organisations in determining the price sensitivity and its impact on

customers. The mentioned entity can use this system so as to attain information about

2

their consumers in relation to changes in price and its effect on them. Thus, they set a

level to be attained for gaining the profits. For setting the level of price, cited enterprise

has an option to tailor its cost on the basis of different segments of the customers

(Lazonick, 2012). Thus, it will be easier to anticipate about their possible reaction on

changes made in price. This method is best suitable if the firm is intending to make larger

profits without losing its customers. They will have a good method to fix the rates at an

optimum level. They will be able to develop a better understanding in relation to price

changes and its sensitivity on the customers. In addition to this, the enterprise will be able

to retain existing customers with all possibilities of making new ones as well.

P2 Different methods used for management accounting reporting

The management accounting reports are the special purpose reports that help the

management in providing vital decisions which have a major impact on the business. The said

reporting system collects the information from various areas of financial and non financial

aspects so that the decision making can be done in effective manner. Several types of

management accounting reports that are of major use for organisation are as follows:

Job cost report: The Job cost report gives the information to the company about costs

incurred in a specific project. As per the estimates made by the company, job cost reports

aid in evaluating profitability from the projects. Further, the company becomes able in

identifying the areas that are helping in generating more profits and revenues in business

(Vieira and Teixeira, 2010). Thus, the mentioned organisation can use this system in

pointing out the areas of higher earning which helps in diverting the focus from the

aspects which are proving to be of waste in time and cost. Apart from this, the stated

report assist in assessing different costs at the time of work in progress because of which

the deviations and any incorrect process can be eliminated and corrected.

Inventory management reports: The business enterprises which have more deals in

physical inventories have a special importance of inventory management reports. This

accounting report helps in ascertaining the level of stock currently organisation has along

with the information of level of stock that must be refilled. This report includes additional

information regarding wastages, labour costs and per unit overheads as well. The top

level managers and concerned authorities compare the report with assembly lines so that

areas requiring improvements can be identified and those departments which are

3

level to be attained for gaining the profits. For setting the level of price, cited enterprise

has an option to tailor its cost on the basis of different segments of the customers

(Lazonick, 2012). Thus, it will be easier to anticipate about their possible reaction on

changes made in price. This method is best suitable if the firm is intending to make larger

profits without losing its customers. They will have a good method to fix the rates at an

optimum level. They will be able to develop a better understanding in relation to price

changes and its sensitivity on the customers. In addition to this, the enterprise will be able

to retain existing customers with all possibilities of making new ones as well.

P2 Different methods used for management accounting reporting

The management accounting reports are the special purpose reports that help the

management in providing vital decisions which have a major impact on the business. The said

reporting system collects the information from various areas of financial and non financial

aspects so that the decision making can be done in effective manner. Several types of

management accounting reports that are of major use for organisation are as follows:

Job cost report: The Job cost report gives the information to the company about costs

incurred in a specific project. As per the estimates made by the company, job cost reports

aid in evaluating profitability from the projects. Further, the company becomes able in

identifying the areas that are helping in generating more profits and revenues in business

(Vieira and Teixeira, 2010). Thus, the mentioned organisation can use this system in

pointing out the areas of higher earning which helps in diverting the focus from the

aspects which are proving to be of waste in time and cost. Apart from this, the stated

report assist in assessing different costs at the time of work in progress because of which

the deviations and any incorrect process can be eliminated and corrected.

Inventory management reports: The business enterprises which have more deals in

physical inventories have a special importance of inventory management reports. This

accounting report helps in ascertaining the level of stock currently organisation has along

with the information of level of stock that must be refilled. This report includes additional

information regarding wastages, labour costs and per unit overheads as well. The top

level managers and concerned authorities compare the report with assembly lines so that

areas requiring improvements can be identified and those departments which are

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

performing in outstanding way can be rewarded (Hood, 2013). Thus, the cited entity can

use this report for determining inventory level and also assess the performance of

department.

Operating budget report: The operating budget reports aid business firms in measuring

the performance level of different departments so that the cost of operating can be

monitored effectively. For this purpose, the budgets are prepared by the enterprise in

beginning so that the activities requiring different expenses and investments can be

determined in advance. On this basis, the organization can make an anticipation related to

risks that can be faced by company in situations of uncertainties. In addition to this, the

management can keep control on its various activities because of which the investments

can be made in more productive areas avoiding the investments on different unproductive

projects. Besides this, the budget reports also act as a standard report that helps in setting

a fixed level according to which the business should be managed. Thus keeping a control

over various activities and possibilities of getting diversions can be minimised. This

report can also be used by quoted firm in providing incentives to the staff by analysing

their performances (Guthrie, Olson and Humphrey, 2010).

Accounts receivable aging report: This report is a critical tool that helps in management

of different cash flows of business along with the record of different credit purchase

made by customers. The mentioned report keeps a proper record of each customer and

their balances as well so that the company can have the information regarding due

amounts from them. The aging reports make a classification of report on the basis of time

durations in which various columns are made. For instance, 30 days late, 60 days late etc.

this report helps in identifying the issues because of which the collection procedure of

entity becomes faulty. If the left out balances are more from customers' side, it signifies

that the organisation should tighten their credit policy. This report also allows the firm in

overlooking over the debts from earlier periods.

Performance reports: The performance reports are made to have information on the

performance of different products and services which are existing in the market (Eckerd,

2015). This report contains information on profitability analysis which is based on

different segments and also product lines. Thus, the firm has easier access on exploitation

of different advantages. Besides this, through this report, enterprise take corrective

4

use this report for determining inventory level and also assess the performance of

department.

Operating budget report: The operating budget reports aid business firms in measuring

the performance level of different departments so that the cost of operating can be

monitored effectively. For this purpose, the budgets are prepared by the enterprise in

beginning so that the activities requiring different expenses and investments can be

determined in advance. On this basis, the organization can make an anticipation related to

risks that can be faced by company in situations of uncertainties. In addition to this, the

management can keep control on its various activities because of which the investments

can be made in more productive areas avoiding the investments on different unproductive

projects. Besides this, the budget reports also act as a standard report that helps in setting

a fixed level according to which the business should be managed. Thus keeping a control

over various activities and possibilities of getting diversions can be minimised. This

report can also be used by quoted firm in providing incentives to the staff by analysing

their performances (Guthrie, Olson and Humphrey, 2010).

Accounts receivable aging report: This report is a critical tool that helps in management

of different cash flows of business along with the record of different credit purchase

made by customers. The mentioned report keeps a proper record of each customer and

their balances as well so that the company can have the information regarding due

amounts from them. The aging reports make a classification of report on the basis of time

durations in which various columns are made. For instance, 30 days late, 60 days late etc.

this report helps in identifying the issues because of which the collection procedure of

entity becomes faulty. If the left out balances are more from customers' side, it signifies

that the organisation should tighten their credit policy. This report also allows the firm in

overlooking over the debts from earlier periods.

Performance reports: The performance reports are made to have information on the

performance of different products and services which are existing in the market (Eckerd,

2015). This report contains information on profitability analysis which is based on

different segments and also product lines. Thus, the firm has easier access on exploitation

of different advantages. Besides this, through this report, enterprise take corrective

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

measures which can help in bringing efficiency by making a control on the cost of

operations. Apart from this, it also helps in monitoring over expenses so that it can be

checked that spent money has been used in proper areas of business.

TASK 2

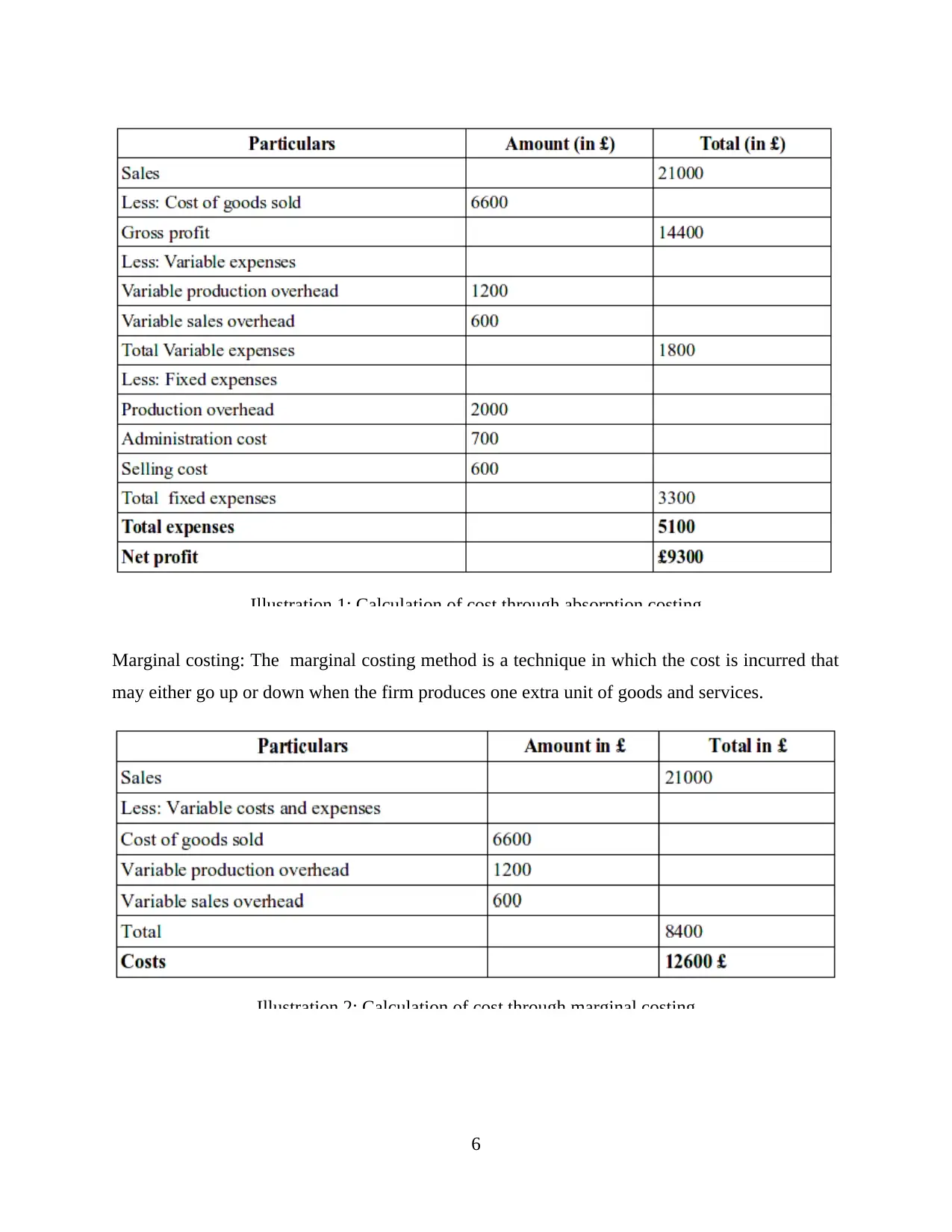

P3 Calculation of cost through different methods

The cost is referred as that amount which is used for purchasing or attaining something.

For a business organisation, it can be termed as the sum which is spent over creation of products

and services. The costs can be of various types in the accounting which makes up a significant

part of price in the management accounting system. The major types of costs that are utilised in

the business are:

Fixed cost: The fixed costs are those which remains static and does not show any change in its

level according to the changed in production level (Kaplan and Atkinson, 2015). Thus, it remains

unaffected regardless of changes in output level, for instance rent of building.

Variable cost: The variable costs are opposite to the fixed costs as it does not remain same and

use to change as per the alterations coming in the level of output. For instance, cost of raw

materials that use to fluctuate as per the level of production.

Semi-variable costs: The semi variable costs are the mixture of both fixed and variable costs. For

instance, the telephone bills in which the charges of line rental are fixed while the charges of

additional calls are variable charges.

The Income statements in a business are prepared for knowing the financial soundness of

the company. These statements can be prepared through two types of ways to calculate costs and

determine the gross profits. There are two types of methods through which costing can be

determined by the firm:

Absorption costing: The absorption costing method is a techniques through which costs can be

calculated with the help of including all types of expenses (Smith, 2014). Thus, it depicts a

process in which all types of costs are allocated to a particular cost centre.

5

operations. Apart from this, it also helps in monitoring over expenses so that it can be

checked that spent money has been used in proper areas of business.

TASK 2

P3 Calculation of cost through different methods

The cost is referred as that amount which is used for purchasing or attaining something.

For a business organisation, it can be termed as the sum which is spent over creation of products

and services. The costs can be of various types in the accounting which makes up a significant

part of price in the management accounting system. The major types of costs that are utilised in

the business are:

Fixed cost: The fixed costs are those which remains static and does not show any change in its

level according to the changed in production level (Kaplan and Atkinson, 2015). Thus, it remains

unaffected regardless of changes in output level, for instance rent of building.

Variable cost: The variable costs are opposite to the fixed costs as it does not remain same and

use to change as per the alterations coming in the level of output. For instance, cost of raw

materials that use to fluctuate as per the level of production.

Semi-variable costs: The semi variable costs are the mixture of both fixed and variable costs. For

instance, the telephone bills in which the charges of line rental are fixed while the charges of

additional calls are variable charges.

The Income statements in a business are prepared for knowing the financial soundness of

the company. These statements can be prepared through two types of ways to calculate costs and

determine the gross profits. There are two types of methods through which costing can be

determined by the firm:

Absorption costing: The absorption costing method is a techniques through which costs can be

calculated with the help of including all types of expenses (Smith, 2014). Thus, it depicts a

process in which all types of costs are allocated to a particular cost centre.

5

Illustration 1: Calculation of cost through absorption costing

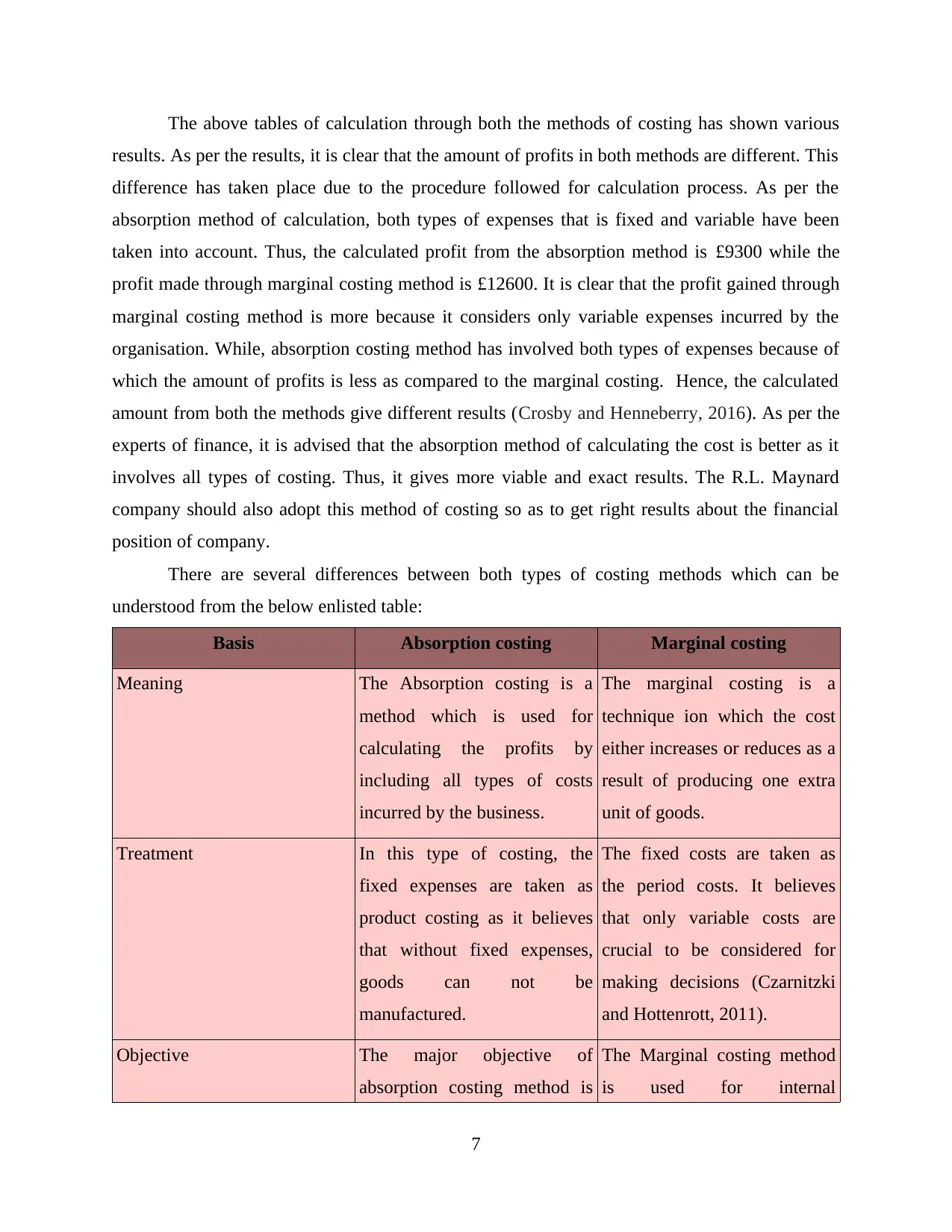

Marginal costing: The marginal costing method is a technique in which the cost is incurred that

may either go up or down when the firm produces one extra unit of goods and services.

Illustration 2: Calculation of cost through marginal costing

6

Marginal costing: The marginal costing method is a technique in which the cost is incurred that

may either go up or down when the firm produces one extra unit of goods and services.

Illustration 2: Calculation of cost through marginal costing

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The above tables of calculation through both the methods of costing has shown various

results. As per the results, it is clear that the amount of profits in both methods are different. This

difference has taken place due to the procedure followed for calculation process. As per the

absorption method of calculation, both types of expenses that is fixed and variable have been

taken into account. Thus, the calculated profit from the absorption method is £9300 while the

profit made through marginal costing method is £12600. It is clear that the profit gained through

marginal costing method is more because it considers only variable expenses incurred by the

organisation. While, absorption costing method has involved both types of expenses because of

which the amount of profits is less as compared to the marginal costing. Hence, the calculated

amount from both the methods give different results (Crosby and Henneberry, 2016). As per the

experts of finance, it is advised that the absorption method of calculating the cost is better as it

involves all types of costing. Thus, it gives more viable and exact results. The R.L. Maynard

company should also adopt this method of costing so as to get right results about the financial

position of company.

There are several differences between both types of costing methods which can be

understood from the below enlisted table:

Basis Absorption costing Marginal costing

Meaning The Absorption costing is a

method which is used for

calculating the profits by

including all types of costs

incurred by the business.

The marginal costing is a

technique ion which the cost

either increases or reduces as a

result of producing one extra

unit of goods.

Treatment In this type of costing, the

fixed expenses are taken as

product costing as it believes

that without fixed expenses,

goods can not be

manufactured.

The fixed costs are taken as

the period costs. It believes

that only variable costs are

crucial to be considered for

making decisions (Czarnitzki

and Hottenrott, 2011).

Objective The major objective of

absorption costing method is

The Marginal costing method

is used for internal

7

results. As per the results, it is clear that the amount of profits in both methods are different. This

difference has taken place due to the procedure followed for calculation process. As per the

absorption method of calculation, both types of expenses that is fixed and variable have been

taken into account. Thus, the calculated profit from the absorption method is £9300 while the

profit made through marginal costing method is £12600. It is clear that the profit gained through

marginal costing method is more because it considers only variable expenses incurred by the

organisation. While, absorption costing method has involved both types of expenses because of

which the amount of profits is less as compared to the marginal costing. Hence, the calculated

amount from both the methods give different results (Crosby and Henneberry, 2016). As per the

experts of finance, it is advised that the absorption method of calculating the cost is better as it

involves all types of costing. Thus, it gives more viable and exact results. The R.L. Maynard

company should also adopt this method of costing so as to get right results about the financial

position of company.

There are several differences between both types of costing methods which can be

understood from the below enlisted table:

Basis Absorption costing Marginal costing

Meaning The Absorption costing is a

method which is used for

calculating the profits by

including all types of costs

incurred by the business.

The marginal costing is a

technique ion which the cost

either increases or reduces as a

result of producing one extra

unit of goods.

Treatment In this type of costing, the

fixed expenses are taken as

product costing as it believes

that without fixed expenses,

goods can not be

manufactured.

The fixed costs are taken as

the period costs. It believes

that only variable costs are

crucial to be considered for

making decisions (Czarnitzki

and Hottenrott, 2011).

Objective The major objective of

absorption costing method is

The Marginal costing method

is used for internal

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

to give report for external

management. Thus, it aids in

effective management of

overall company (Elbashir,

Collier and Sutton, 2011).

management so that decision

making can become easier.

Presentation In the absorption costing

method, the presentation is

based on traditional manner.

In this method of costing, the

presentation is done by

highlighting the contribution

of each factor.

TASK 3

P4 Advantages and disadvantages of different planning tools used in Budgetary control

The planning tools for the company are those which can help it in getting growth and

development in an effective manner. The planning tools that are used by organisations are

Budgets and various types included in it. Besides this, there are some pricing strategies as well

which also act as a planning tool for the business entities.

Budgeting and budgetary control: The budgeting is a tool which are prepared by the managers

in advance. This tool is a written statement in which managers use to develop a formalised plans

for making a plan based on future activities. Besides this, it acts as a planning and controlling

tool as it sets a standard procedure which has to be followed (Garrison and et.al., 2010). The

managers use this standard to compare the performances. The actual performance is compared

with the standard ones so as to check the real position. Any type of error or deviation is checked

and corrective actions are taken. In addition to this, it also helps in establishing a coordination

between various activities. There are different types of budgets that can be used by the R.L.

Maynard company for effective planning. Besides the above stated tools there are some other

techniques which can be utilised for gaining better efficiency and managing activities in a better

way.

There are several benefits of the budgeting which can be demonstrated in below mentioned way:

Through Budgeting managers are forced to make plans and also clearly define various

aims and objectives of business (Ward, 2012).

8

management. Thus, it aids in

effective management of

overall company (Elbashir,

Collier and Sutton, 2011).

management so that decision

making can become easier.

Presentation In the absorption costing

method, the presentation is

based on traditional manner.

In this method of costing, the

presentation is done by

highlighting the contribution

of each factor.

TASK 3

P4 Advantages and disadvantages of different planning tools used in Budgetary control

The planning tools for the company are those which can help it in getting growth and

development in an effective manner. The planning tools that are used by organisations are

Budgets and various types included in it. Besides this, there are some pricing strategies as well

which also act as a planning tool for the business entities.

Budgeting and budgetary control: The budgeting is a tool which are prepared by the managers

in advance. This tool is a written statement in which managers use to develop a formalised plans

for making a plan based on future activities. Besides this, it acts as a planning and controlling

tool as it sets a standard procedure which has to be followed (Garrison and et.al., 2010). The

managers use this standard to compare the performances. The actual performance is compared

with the standard ones so as to check the real position. Any type of error or deviation is checked

and corrective actions are taken. In addition to this, it also helps in establishing a coordination

between various activities. There are different types of budgets that can be used by the R.L.

Maynard company for effective planning. Besides the above stated tools there are some other

techniques which can be utilised for gaining better efficiency and managing activities in a better

way.

There are several benefits of the budgeting which can be demonstrated in below mentioned way:

Through Budgeting managers are forced to make plans and also clearly define various

aims and objectives of business (Ward, 2012).

8

It provides a foundation for control process so that the actual performance can be

compared with the standard ones.

It helps in establishing an effective coordination in all the activities so that a right level of

communication and information sharing is set up. Besides all this, it also acts as a motivational tool which helps in motivating the staff for

performing in a better way.

Drawbacks

The budgets are usually less flexible because of which the changes that have to be made

as per the changing circumstances are generally difficult (Baldvinsdottir, Mitchell and

Nørreklit, 2010).

It is not sure that by preparing budgets, the company will get success and effective results

as expected. Sometimes, due to tight budgets, many productive and attractive investments have to be

avoided because of restrictions made on investments that have to be done according to

budget.

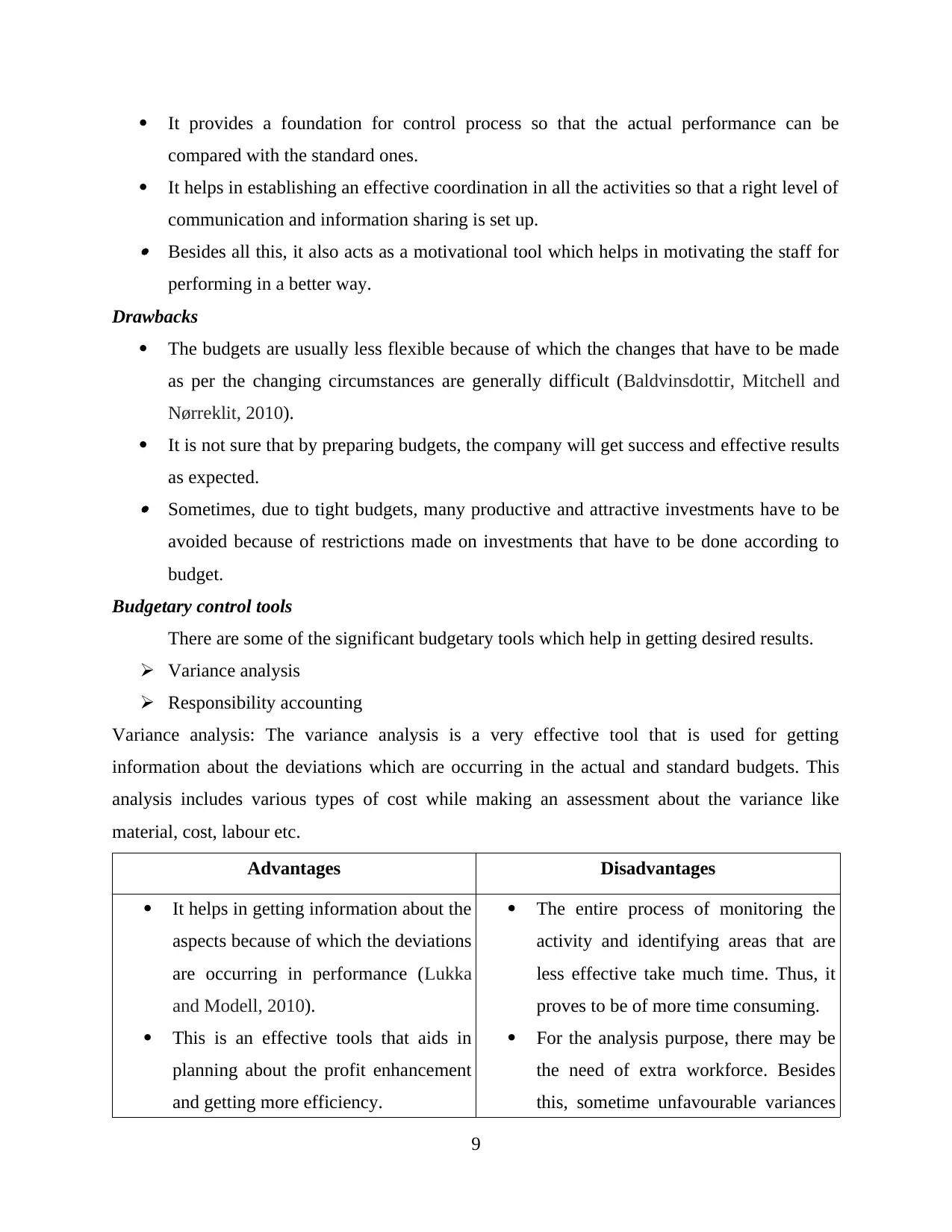

Budgetary control tools

There are some of the significant budgetary tools which help in getting desired results.

Variance analysis

Responsibility accounting

Variance analysis: The variance analysis is a very effective tool that is used for getting

information about the deviations which are occurring in the actual and standard budgets. This

analysis includes various types of cost while making an assessment about the variance like

material, cost, labour etc.

Advantages Disadvantages

It helps in getting information about the

aspects because of which the deviations

are occurring in performance (Lukka

and Modell, 2010).

This is an effective tools that aids in

planning about the profit enhancement

and getting more efficiency.

The entire process of monitoring the

activity and identifying areas that are

less effective take much time. Thus, it

proves to be of more time consuming.

For the analysis purpose, there may be

the need of extra workforce. Besides

this, sometime unfavourable variances

9

compared with the standard ones.

It helps in establishing an effective coordination in all the activities so that a right level of

communication and information sharing is set up. Besides all this, it also acts as a motivational tool which helps in motivating the staff for

performing in a better way.

Drawbacks

The budgets are usually less flexible because of which the changes that have to be made

as per the changing circumstances are generally difficult (Baldvinsdottir, Mitchell and

Nørreklit, 2010).

It is not sure that by preparing budgets, the company will get success and effective results

as expected. Sometimes, due to tight budgets, many productive and attractive investments have to be

avoided because of restrictions made on investments that have to be done according to

budget.

Budgetary control tools

There are some of the significant budgetary tools which help in getting desired results.

Variance analysis

Responsibility accounting

Variance analysis: The variance analysis is a very effective tool that is used for getting

information about the deviations which are occurring in the actual and standard budgets. This

analysis includes various types of cost while making an assessment about the variance like

material, cost, labour etc.

Advantages Disadvantages

It helps in getting information about the

aspects because of which the deviations

are occurring in performance (Lukka

and Modell, 2010).

This is an effective tools that aids in

planning about the profit enhancement

and getting more efficiency.

The entire process of monitoring the

activity and identifying areas that are

less effective take much time. Thus, it

proves to be of more time consuming.

For the analysis purpose, there may be

the need of extra workforce. Besides

this, sometime unfavourable variances

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.