Financial Resource Management: Analysis of J Sainsbury PLC Finance

VerifiedAdded on 2020/02/17

|22

|6889

|342

Report

AI Summary

This report provides a comprehensive analysis of financial resource management, focusing on J Sainsbury PLC. It explores various sources of finance, including equity shares, debentures, and retained earnings, evaluating their implications and costs. The report delves into the importance of financial planning, the information required for decision-making, and the impact of finance on financial statements. It includes a discussion on cash budgeting, unit cost calculation, and investment appraisal techniques to assess project viability. Furthermore, the report examines main financial statements and the interpretation of financial statements using internal and external ratios. The conclusion summarizes the key findings and insights gained from the analysis of financial resource management practices within the context of the case study company.

Managing Financial

Resources

Resources

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................4

1.1 Sources of finance available to a businesses.........................................................................4

1.2 Implication of different sources of finance..........................................................................5

1.3 Evaluation of different sources of finance............................................................................5

2.1 Cost of different sources of finance......................................................................................6

2.2 Importance of Financial Planning.........................................................................................6

2.3 Information which are needed for making decisions............................................................7

2.4 Impact of finance on the financial statements.......................................................................7

3.1 Cash budget for the business entity.......................................................................................8

3.2 Calculation of Unit Cost........................................................................................................9

3.3 Assess the viability of a project using investment appraisal techniques.............................10

TASK 2..........................................................................................................................................12

4.1 Main financial statement.....................................................................................................12

4.2 Compare the appropriate formats of financial statement in the different type of business.12

4.3 Interpretation of financial statements using appropriate ratios by using internal and

external ratios............................................................................................................................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................4

1.1 Sources of finance available to a businesses.........................................................................4

1.2 Implication of different sources of finance..........................................................................5

1.3 Evaluation of different sources of finance............................................................................5

2.1 Cost of different sources of finance......................................................................................6

2.2 Importance of Financial Planning.........................................................................................6

2.3 Information which are needed for making decisions............................................................7

2.4 Impact of finance on the financial statements.......................................................................7

3.1 Cash budget for the business entity.......................................................................................8

3.2 Calculation of Unit Cost........................................................................................................9

3.3 Assess the viability of a project using investment appraisal techniques.............................10

TASK 2..........................................................................................................................................12

4.1 Main financial statement.....................................................................................................12

4.2 Compare the appropriate formats of financial statement in the different type of business.12

4.3 Interpretation of financial statements using appropriate ratios by using internal and

external ratios............................................................................................................................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

Financial management includes the planning, organising, controlling as well as

monitoring the different resources so that they can attain the goals and objectives. The

employees of the business entity have to make the statements which are related to finance so that

they can improve the performance as well as viability of the organisation (Arthur, Cheng and

Czernkowski, 2010). It assist in providing the appreciation of costing along with the budgeting

techniques and they have their own role on the control system of business enterprise. They have

to develop the methods so that they can evaluate the capital investment proposals. The present

report is based on J Sainsbury PLC which is a second largest chain of supermarket in UK with

having a share of 16.9%. J Sainsbury PLC having three divisions which includes supermarket,

Bank and Argos . In the below mentioned report, discussion based on the different sources of

finance and also the cost should be analysed of the different sources of finance (Managing Your

Resources, 2017).

TASK 1

1.1 Sources of finance available to a businesses

Different sources of finance include the J Sainsbury plc which is following:

1. Equity share:- Equity share is also known as ordinary share. It is the owner of the

company is is also issue for cash. Ordinary share have right to take decision in a

company. In this share the risk is maximum with the business (Bennouna, Meredith and

Marchant, 2010). And also have voting rights to the holders. Equity shares are the

included the dividend after paying to the preference share and the dividend depend on the

profit of the company. And the dividend rate is not fixed in equity capital.

2. Debenture:- Debenture is a long term security and fixed rate of interest. It is also known

as bond which is issued by the company. Debenture is a type of loan but it is not issued

by the bank. Debenture have first right to take interest in fixed rate in the availability of

the profit. Debenture is debt which is used by companies to borrow money at a fixed rate

of interest that can help in raise of money regarding the company (Bodie, 2013).

3. Retained earning:- It is a reinvestment process that is recorded in the equity share capital.

It is non payable but also reinvest in the company. In this process the net income added in

the retained earning and subtracting the net losses and opening retained earning and also

Financial management includes the planning, organising, controlling as well as

monitoring the different resources so that they can attain the goals and objectives. The

employees of the business entity have to make the statements which are related to finance so that

they can improve the performance as well as viability of the organisation (Arthur, Cheng and

Czernkowski, 2010). It assist in providing the appreciation of costing along with the budgeting

techniques and they have their own role on the control system of business enterprise. They have

to develop the methods so that they can evaluate the capital investment proposals. The present

report is based on J Sainsbury PLC which is a second largest chain of supermarket in UK with

having a share of 16.9%. J Sainsbury PLC having three divisions which includes supermarket,

Bank and Argos . In the below mentioned report, discussion based on the different sources of

finance and also the cost should be analysed of the different sources of finance (Managing Your

Resources, 2017).

TASK 1

1.1 Sources of finance available to a businesses

Different sources of finance include the J Sainsbury plc which is following:

1. Equity share:- Equity share is also known as ordinary share. It is the owner of the

company is is also issue for cash. Ordinary share have right to take decision in a

company. In this share the risk is maximum with the business (Bennouna, Meredith and

Marchant, 2010). And also have voting rights to the holders. Equity shares are the

included the dividend after paying to the preference share and the dividend depend on the

profit of the company. And the dividend rate is not fixed in equity capital.

2. Debenture:- Debenture is a long term security and fixed rate of interest. It is also known

as bond which is issued by the company. Debenture is a type of loan but it is not issued

by the bank. Debenture have first right to take interest in fixed rate in the availability of

the profit. Debenture is debt which is used by companies to borrow money at a fixed rate

of interest that can help in raise of money regarding the company (Bodie, 2013).

3. Retained earning:- It is a reinvestment process that is recorded in the equity share capital.

It is non payable but also reinvest in the company. In this process the net income added in

the retained earning and subtracting the net losses and opening retained earning and also

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

subtracting dividend paid by the share holders. It is profit generated by the company that

is not give the customers as well as suppliers(stakeholders). It can reduce the company y

losses (Bradbury, 2011).

1.2 Implication of different sources of finance

1. Equity share:- Equity share is a ordinary share to take decision regarding the J Sainbury

plc company that is helps in investment process and also take the right decision about the

invest the money to earn the higher profit in the company but it is more risky to the

company in the issue of share (Carballo-Penela and Doménech, 2010). Either availability

of the profit or loss the equity share to have the right after paying the preference share

capital to give the dividend at no fixed rate. In the implication process the equity share

holders have to higher return and higher risk.

2. Debenture:- Debenture is a log term finance for the J Sainbury plc company. The

debenture includes the fixed rate of interest to pay for the company in the instalments.

The debenture relates in debt financing that is includes the benefits of tax. Debenture can

help for the company that is include the rate of interest in a availability of the profit. In

the debenture the profit is not share in the debenture holder the can charge only fixed rate

of interest.

3. Retained earning:- Retained earning is a important financial sources of internal uses for

working capital. In can be increase the value of the share holder regarding the boost up

the firm in a financial term (Collier and et. al., 2010). In the retained earning the cost of

financing that shows the no cost of the company regarding the general process of the

company. In the retained earning the important advantage is cheaper source of finance

which is not involved the coast as well as obligation to pay anything in the company. And

the disadvantage of thr retained earning that is improper utilization of fund.

1.3 Evaluation of different sources of finance

There are different sources of finance which helps in making appropriate and relevant

decision for doing the investments. In the equity share is a best way to get money in the business

to helps in cash flow. In the investing decision the fundamental analysis is also based on the

companies balance sheet that can helps in show the cash flow of the company ans also provide

the income statement. Foe the appropriate decision the saving is the most important factor of

putting the money in the company (Collins, Hribar and Tian, 2014). In the terms of finance by

is not give the customers as well as suppliers(stakeholders). It can reduce the company y

losses (Bradbury, 2011).

1.2 Implication of different sources of finance

1. Equity share:- Equity share is a ordinary share to take decision regarding the J Sainbury

plc company that is helps in investment process and also take the right decision about the

invest the money to earn the higher profit in the company but it is more risky to the

company in the issue of share (Carballo-Penela and Doménech, 2010). Either availability

of the profit or loss the equity share to have the right after paying the preference share

capital to give the dividend at no fixed rate. In the implication process the equity share

holders have to higher return and higher risk.

2. Debenture:- Debenture is a log term finance for the J Sainbury plc company. The

debenture includes the fixed rate of interest to pay for the company in the instalments.

The debenture relates in debt financing that is includes the benefits of tax. Debenture can

help for the company that is include the rate of interest in a availability of the profit. In

the debenture the profit is not share in the debenture holder the can charge only fixed rate

of interest.

3. Retained earning:- Retained earning is a important financial sources of internal uses for

working capital. In can be increase the value of the share holder regarding the boost up

the firm in a financial term (Collier and et. al., 2010). In the retained earning the cost of

financing that shows the no cost of the company regarding the general process of the

company. In the retained earning the important advantage is cheaper source of finance

which is not involved the coast as well as obligation to pay anything in the company. And

the disadvantage of thr retained earning that is improper utilization of fund.

1.3 Evaluation of different sources of finance

There are different sources of finance which helps in making appropriate and relevant

decision for doing the investments. In the equity share is a best way to get money in the business

to helps in cash flow. In the investing decision the fundamental analysis is also based on the

companies balance sheet that can helps in show the cash flow of the company ans also provide

the income statement. Foe the appropriate decision the saving is the most important factor of

putting the money in the company (Collins, Hribar and Tian, 2014). In the terms of finance by

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

using as well as issuing share company can raise their finance. In the sources of finance the risk

is always there so the company can evaluated the risk in a investment process in the company

they can define the higher investment as well as higher risk. When investment is low the risk is

automatically low ans the investment is hight the risk is also high. In a business to take a loan to

achieve the more finance by the bank. Before provide the loan bank must to know about the

business as well as business opportunities and also involve the risk regarding the loan (Cui and

Ryan, 2011).

2.1 Cost of different sources of finance

There are several sources of finance by which J Sainsbury PLC get the amount to do

more investments. They can earn money by issuing equity shares, preference shares, debentures

etc. Along with this it helps in making the correct and appropriate decisions. Different sources of

finance are:

Equity shares: For those person who are having the equity shares of the business entity they

have to pay dividend cost in which price of the shares is given to the equity shareholders and the

cost which are related to equity shares they are included in the working capital (Drivelos and

Georgiou, 2012). Cost of equity shares can be measured by price ratio method, earning yield

method etc.

Debentures: These are also issued by J Sainsbury PLC to earn money as these also helps in

making the appropriate decisions regarding investments. In this interest cost can be charged. It is

the second bond holders and they are paid at a fixed or specified time. Along with this they are

charged on the face value of debentures. There is a formula to calculate the cost of debentures

that is:

Kd = I/Po

Retained earnings: It is also a part of the company which provide the sources to do more finance

as well as investment. In this cost which is calculated that is opportunity cost. Moreover, it is

different from the other sources which includes the debt or equity (Gervais, 2010). Cost of

retained eraning can be measured or calculated by the formula that is:

Kr = Ke(1-t)(1-b)

2.2 Importance of Financial Planning

Financial planning is necessary for J Sainsbry PLC as it assist in determining the

financial goals whether it is short term or long term. Along with this the employees have to

is always there so the company can evaluated the risk in a investment process in the company

they can define the higher investment as well as higher risk. When investment is low the risk is

automatically low ans the investment is hight the risk is also high. In a business to take a loan to

achieve the more finance by the bank. Before provide the loan bank must to know about the

business as well as business opportunities and also involve the risk regarding the loan (Cui and

Ryan, 2011).

2.1 Cost of different sources of finance

There are several sources of finance by which J Sainsbury PLC get the amount to do

more investments. They can earn money by issuing equity shares, preference shares, debentures

etc. Along with this it helps in making the correct and appropriate decisions. Different sources of

finance are:

Equity shares: For those person who are having the equity shares of the business entity they

have to pay dividend cost in which price of the shares is given to the equity shareholders and the

cost which are related to equity shares they are included in the working capital (Drivelos and

Georgiou, 2012). Cost of equity shares can be measured by price ratio method, earning yield

method etc.

Debentures: These are also issued by J Sainsbury PLC to earn money as these also helps in

making the appropriate decisions regarding investments. In this interest cost can be charged. It is

the second bond holders and they are paid at a fixed or specified time. Along with this they are

charged on the face value of debentures. There is a formula to calculate the cost of debentures

that is:

Kd = I/Po

Retained earnings: It is also a part of the company which provide the sources to do more finance

as well as investment. In this cost which is calculated that is opportunity cost. Moreover, it is

different from the other sources which includes the debt or equity (Gervais, 2010). Cost of

retained eraning can be measured or calculated by the formula that is:

Kr = Ke(1-t)(1-b)

2.2 Importance of Financial Planning

Financial planning is necessary for J Sainsbry PLC as it assist in determining the

financial goals whether it is short term or long term. Along with this the employees have to

create a balanced plan so that they can meet the targets. It assist in making the relevant decision.

Along with this financial planning is important as it helps in managing the income and by that

they can make the tax payment, expenditure and savings (Healy and Palepu, 2012). Financial

planning increases the cash flow on the basis of that they can monitor the spending patterns and

expenses. When financial planning increases the cash flow then it also increases the capital. So,

that higher authorities of J Sainsbury PLC can make the correct decisions for making the

investments. When the business entity make the proper financial plan and for that they have to

consider the personal circumstances, objectives and risk tolerance. It provides the guidance to

choose the right type of investments so that they can fit into the needs, personality along with the

goals. Further, financial planning aid in making the changes so that they can not face any

problem in making the correct decision for investment on the basis of high liquidity (Hodge,

Hopkins and Wood, 2010). They have to establish a relationship so that they can make a advice

on the basis of finance. They have to meet and assess the current financial circumstances. Along

with this they have to develop the comprehensive plan so that they can attain the goals and

objectives.

2.3 Information which are needed for making decisions

They have to make the appropriate decisions in the terms of financial planning in which

employees of J Sainsbury PLC. While doing the financial planning some information which is to

be used by the employees that is size of J Siansbury PLC. When the size of the organisation is

huge then they require the large amount of money. Management of the projects is also essential

so that they can invest the money in the different projects in which they are having the definite

life as well as objectives (Kirkham, 2012). They have to manage the cost of capital as well as

opportunity cost so that they can attain the good result and on the basis of that they can improve

the performance in the market place. Leaders, managers and management of a cited company

are the final decision makers. They collect appropriate amount of information form external and

internal environment and then lead in taking effective decisions. Hence they can use either one of

the style of decision making through which they can attain all of their goals and objectives in an

effective manner:

1. Command: According to the scenario they take effective decision without consulting

their teams. This form of style is also consider as the autocratic style of leader because

Along with this financial planning is important as it helps in managing the income and by that

they can make the tax payment, expenditure and savings (Healy and Palepu, 2012). Financial

planning increases the cash flow on the basis of that they can monitor the spending patterns and

expenses. When financial planning increases the cash flow then it also increases the capital. So,

that higher authorities of J Sainsbury PLC can make the correct decisions for making the

investments. When the business entity make the proper financial plan and for that they have to

consider the personal circumstances, objectives and risk tolerance. It provides the guidance to

choose the right type of investments so that they can fit into the needs, personality along with the

goals. Further, financial planning aid in making the changes so that they can not face any

problem in making the correct decision for investment on the basis of high liquidity (Hodge,

Hopkins and Wood, 2010). They have to establish a relationship so that they can make a advice

on the basis of finance. They have to meet and assess the current financial circumstances. Along

with this they have to develop the comprehensive plan so that they can attain the goals and

objectives.

2.3 Information which are needed for making decisions

They have to make the appropriate decisions in the terms of financial planning in which

employees of J Sainsbury PLC. While doing the financial planning some information which is to

be used by the employees that is size of J Siansbury PLC. When the size of the organisation is

huge then they require the large amount of money. Management of the projects is also essential

so that they can invest the money in the different projects in which they are having the definite

life as well as objectives (Kirkham, 2012). They have to manage the cost of capital as well as

opportunity cost so that they can attain the good result and on the basis of that they can improve

the performance in the market place. Leaders, managers and management of a cited company

are the final decision makers. They collect appropriate amount of information form external and

internal environment and then lead in taking effective decisions. Hence they can use either one of

the style of decision making through which they can attain all of their goals and objectives in an

effective manner:

1. Command: According to the scenario they take effective decision without consulting

their teams. This form of style is also consider as the autocratic style of leader because

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

there is not even a single information and judgement is based on subordinates. Such style

is only use at the time of financial decision or at the time of crises.

2. Collaborative: This is a sound form of decision making. In this form decision are taken as

a whole. Leaders get their team and take decision on their basis. The final call is

ultimately call by the leader itself but decision are take on the basis of whole team.

There are different decision makers in the company who can make the correct decisions

for the betterment and also to collect the actual information. Managers is the person who help the

firm in making correct decision so that they require the budgets as well as other internal records.

Leaders are also helps in making the correct decision and provide the information to their

subordinates. Another one is shareholders who help in making the correct and appropriate

decisions in investing in the company so that they can increase their assets. Along with this they

require the different financial statements to make better decisions.

2.4 Impact of finance on the financial statements

Financial system is a process of interchange of funds between the lenders, investors as

well as borrowers. It is at national and global level to used the money in the financial system. It

is used by the organisation that involve the three basic financial statements:

Balance sheet: In this statement the company involve their assets, liabilities, share capital to

explain the financial situation in a systemic manner (Kumbirai and Webb, 2010). It is basically

show the true image of the company. All the assets as well as liabilities are takeover by the firm

at the time of using the finance. If any change in the firm takes place which affect the balance

sheet.

Income statement: It is also known as profit and loss statement that is show the income and

expenditure as well as profit of the company in this statement the information related to the

operation. This record is set up keeping in mind the end goal to earn the benefits that have been

made and for that every individuals income that are earned and all expenses that have been

caused in any period will be recorded in it. As all these will be made as far as fund so one might

say that with the adjustment in these sums the money related statement will be modified.

Statement of retained earning: it is can be calculated by the profit of the specific time and it is

divided by the dividend which is given to the shareholders and retained earnings. Along with this

they are out into balance sheet so that the accumulate under owners equity (Minnis and

Sutherland, 2017).

is only use at the time of financial decision or at the time of crises.

2. Collaborative: This is a sound form of decision making. In this form decision are taken as

a whole. Leaders get their team and take decision on their basis. The final call is

ultimately call by the leader itself but decision are take on the basis of whole team.

There are different decision makers in the company who can make the correct decisions

for the betterment and also to collect the actual information. Managers is the person who help the

firm in making correct decision so that they require the budgets as well as other internal records.

Leaders are also helps in making the correct decision and provide the information to their

subordinates. Another one is shareholders who help in making the correct and appropriate

decisions in investing in the company so that they can increase their assets. Along with this they

require the different financial statements to make better decisions.

2.4 Impact of finance on the financial statements

Financial system is a process of interchange of funds between the lenders, investors as

well as borrowers. It is at national and global level to used the money in the financial system. It

is used by the organisation that involve the three basic financial statements:

Balance sheet: In this statement the company involve their assets, liabilities, share capital to

explain the financial situation in a systemic manner (Kumbirai and Webb, 2010). It is basically

show the true image of the company. All the assets as well as liabilities are takeover by the firm

at the time of using the finance. If any change in the firm takes place which affect the balance

sheet.

Income statement: It is also known as profit and loss statement that is show the income and

expenditure as well as profit of the company in this statement the information related to the

operation. This record is set up keeping in mind the end goal to earn the benefits that have been

made and for that every individuals income that are earned and all expenses that have been

caused in any period will be recorded in it. As all these will be made as far as fund so one might

say that with the adjustment in these sums the money related statement will be modified.

Statement of retained earning: it is can be calculated by the profit of the specific time and it is

divided by the dividend which is given to the shareholders and retained earnings. Along with this

they are out into balance sheet so that the accumulate under owners equity (Minnis and

Sutherland, 2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

For any working concern finance is consider as the life line of any organisation. Without

any financial related activity a statement will not lead to prepare. Hence finance made a positive

and negative impact because if the financial statement have good monetary values then it leads in

increase more and more investors for that firm. Also if the reports showing positive and

appropriate information which is related with all organisation long term and short term

investment then it lead in satisfy their investors more and more.

For example, if company purchase the raw material then it will affect the income statement.

Along with this if wages and rent is due then this affect the profit and loss statement. Likewise, if

Bank loan would increase liability in balance sheet and interest on the same would increase

expenses in income statement, Equity capital would increase overall capital and cash in balance.

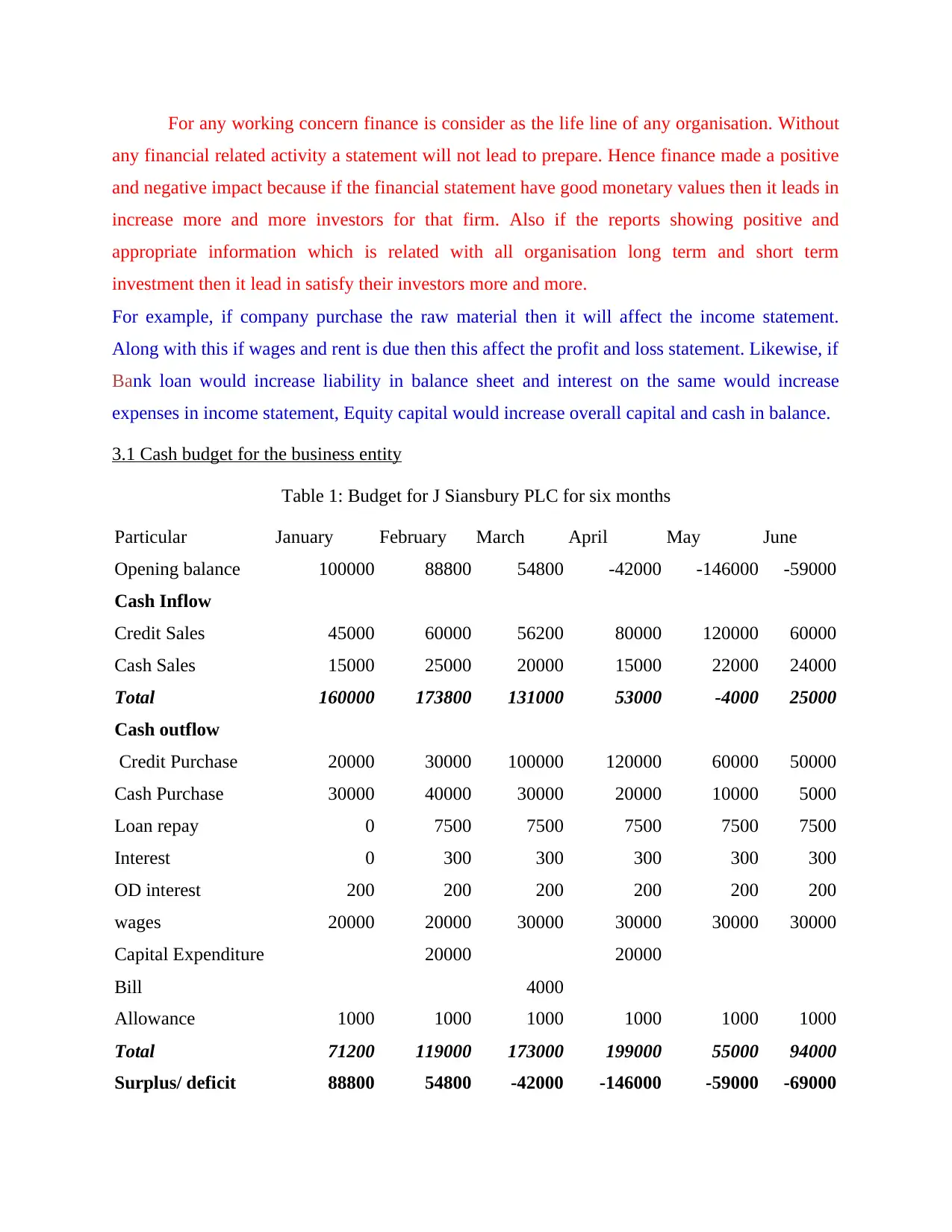

3.1 Cash budget for the business entity

Table 1: Budget for J Siansbury PLC for six months

Particular January February March April May June

Opening balance 100000 88800 54800 -42000 -146000 -59000

Cash Inflow

Credit Sales 45000 60000 56200 80000 120000 60000

Cash Sales 15000 25000 20000 15000 22000 24000

Total 160000 173800 131000 53000 -4000 25000

Cash outflow

Credit Purchase 20000 30000 100000 120000 60000 50000

Cash Purchase 30000 40000 30000 20000 10000 5000

Loan repay 0 7500 7500 7500 7500 7500

Interest 0 300 300 300 300 300

OD interest 200 200 200 200 200 200

wages 20000 20000 30000 30000 30000 30000

Capital Expenditure 20000 20000

Bill 4000

Allowance 1000 1000 1000 1000 1000 1000

Total 71200 119000 173000 199000 55000 94000

Surplus/ deficit 88800 54800 -42000 -146000 -59000 -69000

any financial related activity a statement will not lead to prepare. Hence finance made a positive

and negative impact because if the financial statement have good monetary values then it leads in

increase more and more investors for that firm. Also if the reports showing positive and

appropriate information which is related with all organisation long term and short term

investment then it lead in satisfy their investors more and more.

For example, if company purchase the raw material then it will affect the income statement.

Along with this if wages and rent is due then this affect the profit and loss statement. Likewise, if

Bank loan would increase liability in balance sheet and interest on the same would increase

expenses in income statement, Equity capital would increase overall capital and cash in balance.

3.1 Cash budget for the business entity

Table 1: Budget for J Siansbury PLC for six months

Particular January February March April May June

Opening balance 100000 88800 54800 -42000 -146000 -59000

Cash Inflow

Credit Sales 45000 60000 56200 80000 120000 60000

Cash Sales 15000 25000 20000 15000 22000 24000

Total 160000 173800 131000 53000 -4000 25000

Cash outflow

Credit Purchase 20000 30000 100000 120000 60000 50000

Cash Purchase 30000 40000 30000 20000 10000 5000

Loan repay 0 7500 7500 7500 7500 7500

Interest 0 300 300 300 300 300

OD interest 200 200 200 200 200 200

wages 20000 20000 30000 30000 30000 30000

Capital Expenditure 20000 20000

Bill 4000

Allowance 1000 1000 1000 1000 1000 1000

Total 71200 119000 173000 199000 55000 94000

Surplus/ deficit 88800 54800 -42000 -146000 -59000 -69000

The cash budget helps in identifying the position of cash whether it is inflow and outflow

for J Sainsbury PLC for the upcoming budget of six months which prepared above. Along with

this it presents the income as well as expenses of the business entity. From the above cash

budget, it can be analysed that J Sainsbury PLC is going to improve or earn surplus in the

starting months but after two months the company is facing the deficit. The major areas of the

business expenses are interest paid against the bank loan as well as overdraft. Along with this, in

addition wages as well as capital expenditure is the another form of expense as it helps in

controlling its expenses (Müller, 2011). Moreover, it helps in improving the position of cash and

they are suggested to use the cash management techniques.

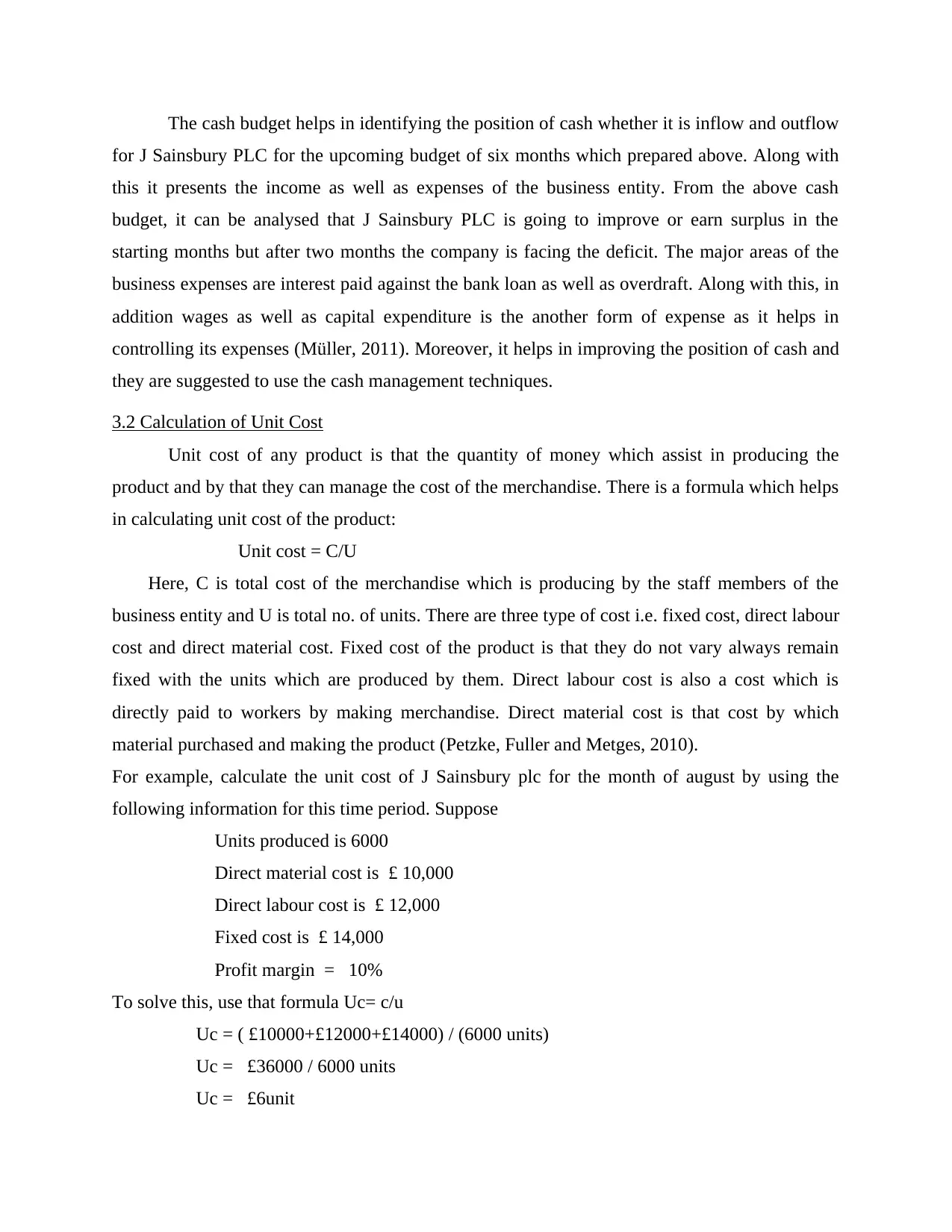

3.2 Calculation of Unit Cost

Unit cost of any product is that the quantity of money which assist in producing the

product and by that they can manage the cost of the merchandise. There is a formula which helps

in calculating unit cost of the product:

Unit cost = C/U

Here, C is total cost of the merchandise which is producing by the staff members of the

business entity and U is total no. of units. There are three type of cost i.e. fixed cost, direct labour

cost and direct material cost. Fixed cost of the product is that they do not vary always remain

fixed with the units which are produced by them. Direct labour cost is also a cost which is

directly paid to workers by making merchandise. Direct material cost is that cost by which

material purchased and making the product (Petzke, Fuller and Metges, 2010).

For example, calculate the unit cost of J Sainsbury plc for the month of august by using the

following information for this time period. Suppose

Units produced is 6000

Direct material cost is £ 10,000

Direct labour cost is £ 12,000

Fixed cost is £ 14,000

Profit margin = 10%

To solve this, use that formula Uc= c/u

Uc = ( £10000+£12000+£14000) / (6000 units)

Uc = £36000 / 6000 units

Uc = £6unit

for J Sainsbury PLC for the upcoming budget of six months which prepared above. Along with

this it presents the income as well as expenses of the business entity. From the above cash

budget, it can be analysed that J Sainsbury PLC is going to improve or earn surplus in the

starting months but after two months the company is facing the deficit. The major areas of the

business expenses are interest paid against the bank loan as well as overdraft. Along with this, in

addition wages as well as capital expenditure is the another form of expense as it helps in

controlling its expenses (Müller, 2011). Moreover, it helps in improving the position of cash and

they are suggested to use the cash management techniques.

3.2 Calculation of Unit Cost

Unit cost of any product is that the quantity of money which assist in producing the

product and by that they can manage the cost of the merchandise. There is a formula which helps

in calculating unit cost of the product:

Unit cost = C/U

Here, C is total cost of the merchandise which is producing by the staff members of the

business entity and U is total no. of units. There are three type of cost i.e. fixed cost, direct labour

cost and direct material cost. Fixed cost of the product is that they do not vary always remain

fixed with the units which are produced by them. Direct labour cost is also a cost which is

directly paid to workers by making merchandise. Direct material cost is that cost by which

material purchased and making the product (Petzke, Fuller and Metges, 2010).

For example, calculate the unit cost of J Sainsbury plc for the month of august by using the

following information for this time period. Suppose

Units produced is 6000

Direct material cost is £ 10,000

Direct labour cost is £ 12,000

Fixed cost is £ 14,000

Profit margin = 10%

To solve this, use that formula Uc= c/u

Uc = ( £10000+£12000+£14000) / (6000 units)

Uc = £36000 / 6000 units

Uc = £6unit

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

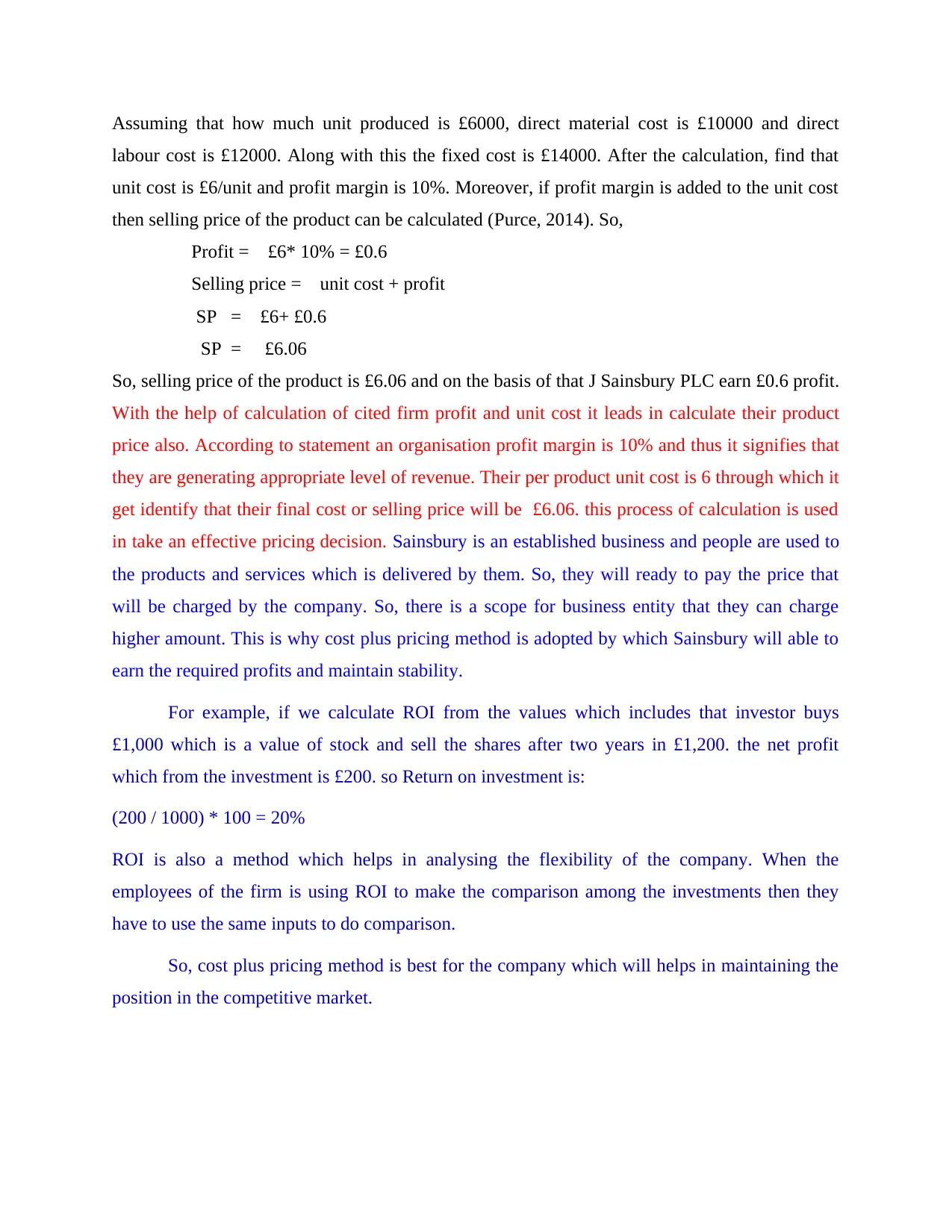

Assuming that how much unit produced is £6000, direct material cost is £10000 and direct

labour cost is £12000. Along with this the fixed cost is £14000. After the calculation, find that

unit cost is £6/unit and profit margin is 10%. Moreover, if profit margin is added to the unit cost

then selling price of the product can be calculated (Purce, 2014). So,

Profit = £6* 10% = £0.6

Selling price = unit cost + profit

SP = £6+ £0.6

SP = £6.06

So, selling price of the product is £6.06 and on the basis of that J Sainsbury PLC earn £0.6 profit.

With the help of calculation of cited firm profit and unit cost it leads in calculate their product

price also. According to statement an organisation profit margin is 10% and thus it signifies that

they are generating appropriate level of revenue. Their per product unit cost is 6 through which it

get identify that their final cost or selling price will be £6.06. this process of calculation is used

in take an effective pricing decision. Sainsbury is an established business and people are used to

the products and services which is delivered by them. So, they will ready to pay the price that

will be charged by the company. So, there is a scope for business entity that they can charge

higher amount. This is why cost plus pricing method is adopted by which Sainsbury will able to

earn the required profits and maintain stability.

For example, if we calculate ROI from the values which includes that investor buys

£1,000 which is a value of stock and sell the shares after two years in £1,200. the net profit

which from the investment is £200. so Return on investment is:

(200 / 1000) * 100 = 20%

ROI is also a method which helps in analysing the flexibility of the company. When the

employees of the firm is using ROI to make the comparison among the investments then they

have to use the same inputs to do comparison.

So, cost plus pricing method is best for the company which will helps in maintaining the

position in the competitive market.

labour cost is £12000. Along with this the fixed cost is £14000. After the calculation, find that

unit cost is £6/unit and profit margin is 10%. Moreover, if profit margin is added to the unit cost

then selling price of the product can be calculated (Purce, 2014). So,

Profit = £6* 10% = £0.6

Selling price = unit cost + profit

SP = £6+ £0.6

SP = £6.06

So, selling price of the product is £6.06 and on the basis of that J Sainsbury PLC earn £0.6 profit.

With the help of calculation of cited firm profit and unit cost it leads in calculate their product

price also. According to statement an organisation profit margin is 10% and thus it signifies that

they are generating appropriate level of revenue. Their per product unit cost is 6 through which it

get identify that their final cost or selling price will be £6.06. this process of calculation is used

in take an effective pricing decision. Sainsbury is an established business and people are used to

the products and services which is delivered by them. So, they will ready to pay the price that

will be charged by the company. So, there is a scope for business entity that they can charge

higher amount. This is why cost plus pricing method is adopted by which Sainsbury will able to

earn the required profits and maintain stability.

For example, if we calculate ROI from the values which includes that investor buys

£1,000 which is a value of stock and sell the shares after two years in £1,200. the net profit

which from the investment is £200. so Return on investment is:

(200 / 1000) * 100 = 20%

ROI is also a method which helps in analysing the flexibility of the company. When the

employees of the firm is using ROI to make the comparison among the investments then they

have to use the same inputs to do comparison.

So, cost plus pricing method is best for the company which will helps in maintaining the

position in the competitive market.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

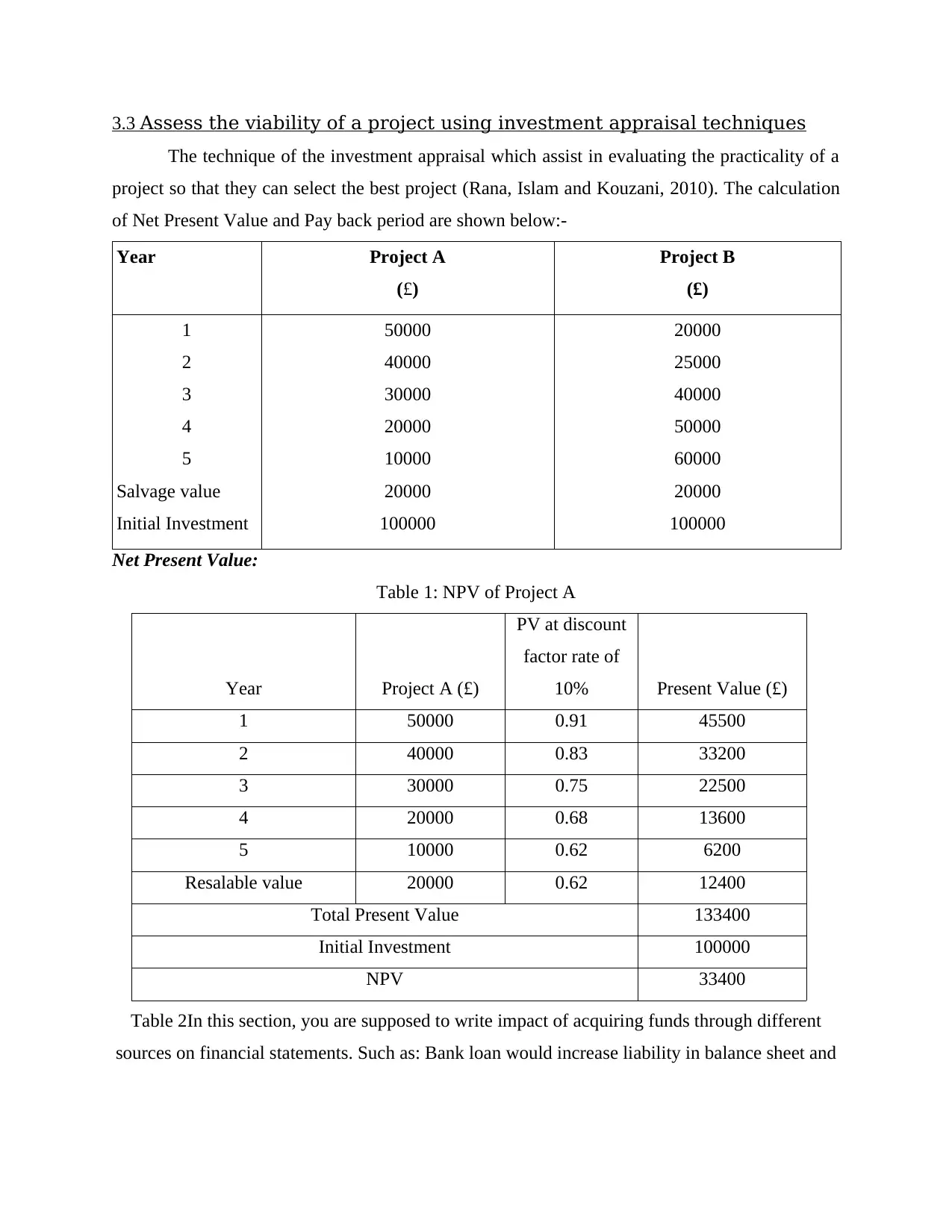

3.3 Assess the viability of a project using investment appraisal techniques

The technique of the investment appraisal which assist in evaluating the practicality of a

project so that they can select the best project (Rana, Islam and Kouzani, 2010). The calculation

of Net Present Value and Pay back period are shown below:-

Year Project A

(£)

Project B

(£)

1

2

3

4

5

Salvage value

Initial Investment

50000

40000

30000

20000

10000

20000

100000

20000

25000

40000

50000

60000

20000

100000

Net Present Value:

Table 1: NPV of Project A

Year Project A (£)

PV at discount

factor rate of

10% Present Value (£)

1 50000 0.91 45500

2 40000 0.83 33200

3 30000 0.75 22500

4 20000 0.68 13600

5 10000 0.62 6200

Resalable value 20000 0.62 12400

Total Present Value 133400

Initial Investment 100000

NPV 33400

Table 2In this section, you are supposed to write impact of acquiring funds through different

sources on financial statements. Such as: Bank loan would increase liability in balance sheet and

The technique of the investment appraisal which assist in evaluating the practicality of a

project so that they can select the best project (Rana, Islam and Kouzani, 2010). The calculation

of Net Present Value and Pay back period are shown below:-

Year Project A

(£)

Project B

(£)

1

2

3

4

5

Salvage value

Initial Investment

50000

40000

30000

20000

10000

20000

100000

20000

25000

40000

50000

60000

20000

100000

Net Present Value:

Table 1: NPV of Project A

Year Project A (£)

PV at discount

factor rate of

10% Present Value (£)

1 50000 0.91 45500

2 40000 0.83 33200

3 30000 0.75 22500

4 20000 0.68 13600

5 10000 0.62 6200

Resalable value 20000 0.62 12400

Total Present Value 133400

Initial Investment 100000

NPV 33400

Table 2In this section, you are supposed to write impact of acquiring funds through different

sources on financial statements. Such as: Bank loan would increase liability in balance sheet and

interest on the same would increase expenses in income statement; Equity capital would increase

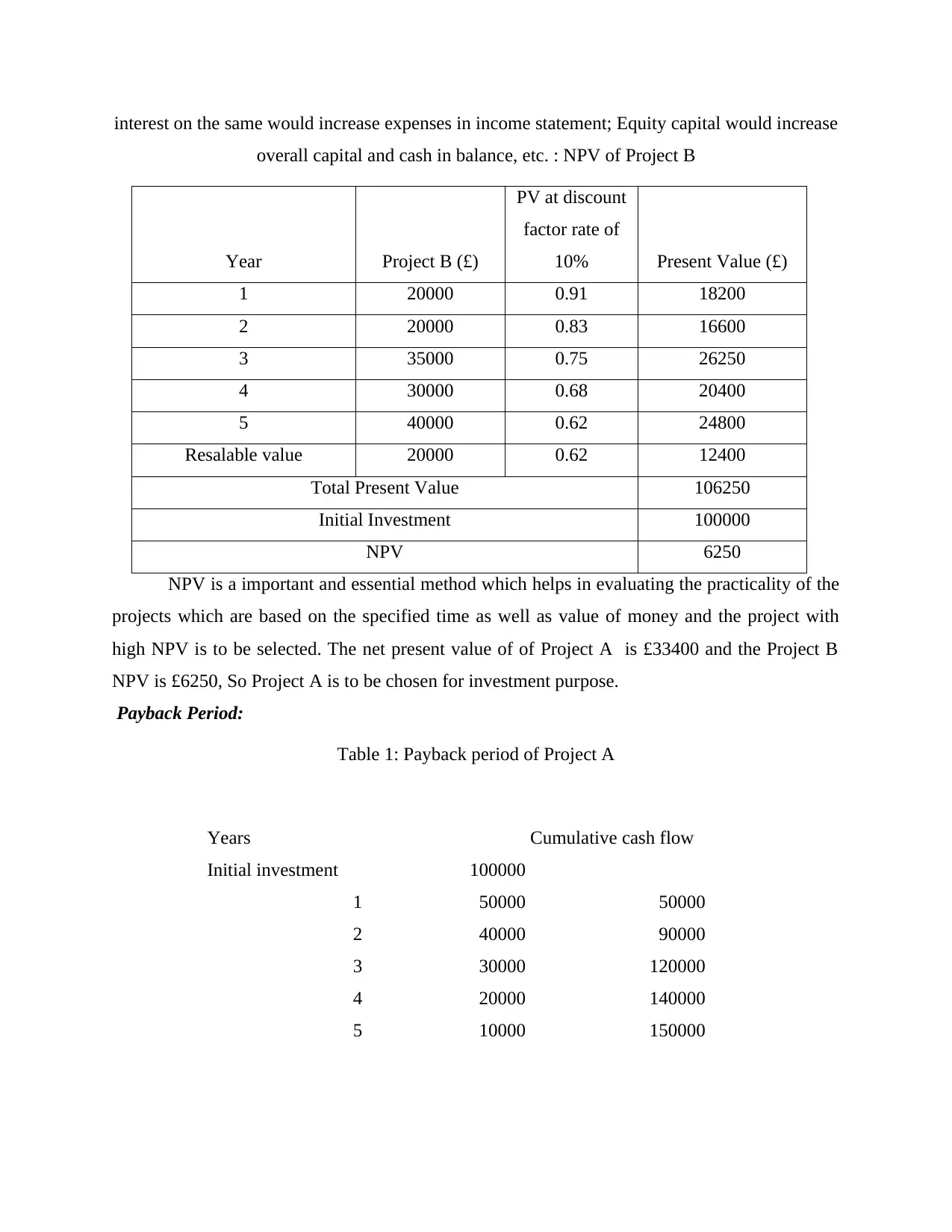

overall capital and cash in balance, etc. : NPV of Project B

Year Project B (£)

PV at discount

factor rate of

10% Present Value (£)

1 20000 0.91 18200

2 20000 0.83 16600

3 35000 0.75 26250

4 30000 0.68 20400

5 40000 0.62 24800

Resalable value 20000 0.62 12400

Total Present Value 106250

Initial Investment 100000

NPV 6250

NPV is a important and essential method which helps in evaluating the practicality of the

projects which are based on the specified time as well as value of money and the project with

high NPV is to be selected. The net present value of of Project A is £33400 and the Project B

NPV is £6250, So Project A is to be chosen for investment purpose.

Payback Period:

Table 1: Payback period of Project A

Years Cumulative cash flow

Initial investment 100000

1 50000 50000

2 40000 90000

3 30000 120000

4 20000 140000

5 10000 150000

overall capital and cash in balance, etc. : NPV of Project B

Year Project B (£)

PV at discount

factor rate of

10% Present Value (£)

1 20000 0.91 18200

2 20000 0.83 16600

3 35000 0.75 26250

4 30000 0.68 20400

5 40000 0.62 24800

Resalable value 20000 0.62 12400

Total Present Value 106250

Initial Investment 100000

NPV 6250

NPV is a important and essential method which helps in evaluating the practicality of the

projects which are based on the specified time as well as value of money and the project with

high NPV is to be selected. The net present value of of Project A is £33400 and the Project B

NPV is £6250, So Project A is to be chosen for investment purpose.

Payback Period:

Table 1: Payback period of Project A

Years Cumulative cash flow

Initial investment 100000

1 50000 50000

2 40000 90000

3 30000 120000

4 20000 140000

5 10000 150000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.