Comprehensive Report on Time-Driven Activity Based Costing System

VerifiedAdded on 2020/05/28

|12

|2994

|116

Report

AI Summary

This report provides a comprehensive analysis of the Time-Driven Activity Based Costing (TDABC) system. It begins with an executive summary highlighting the advantages of TDABC over traditional ABC, especially for complex organizations with numerous activities and cost objects. The report then introduces the client, a hotel entrepreneur, and their need to manage costs effectively. It details the features of TDABC, contrasting it with the ABC system, and illustrates the differences with examples. The report explains how to calculate the figures used in TDABC and outlines the phases involved in its implementation, including calculating departmental costs, practical capacity, and identifying activities. The analysis emphasizes the time equation as a core element of TDABC and concludes by positioning TDABC as a more suitable and efficient cost model for modern business environments. References are included for further study. This report is available on Desklib, a platform offering AI-powered study tools for students.

Report on Time-Driven ABC System 0

[Draw your reader in with an engaging

abstract. It is typically a short summary of

the document. When you’re ready to add

your content, just click here and start

typing.]

Report on Time-Driven Activity Based Costing

System

[Document subtitle]

Abasus Solution

[Draw your reader in with an engaging

abstract. It is typically a short summary of

the document. When you’re ready to add

your content, just click here and start

typing.]

Report on Time-Driven Activity Based Costing

System

[Document subtitle]

Abasus Solution

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Report on Time-Driven ABC System 1

Table of Contents

Contents

Executive Summary...................................................................................................................2

Introduction and Description of Client......................................................................................2

Time-Driven Activity Based Management and it’s features......................................................3

Difference between ABC System and TDABC.........................................................................4

Illustration showing contrast between Activity Based Costing System and Time-driven

Activity Based Costing...........................................................................................................5

How the figure of 2,12,160 has been calculated?...................................................................6

Other features of TDABC......................................................................................................7

Phases in Time-driven Activity based costing.......................................................................7

Conclusion................................................................................................................................10

References:...............................................................................................................................10

Table of Contents

Contents

Executive Summary...................................................................................................................2

Introduction and Description of Client......................................................................................2

Time-Driven Activity Based Management and it’s features......................................................3

Difference between ABC System and TDABC.........................................................................4

Illustration showing contrast between Activity Based Costing System and Time-driven

Activity Based Costing...........................................................................................................5

How the figure of 2,12,160 has been calculated?...................................................................6

Other features of TDABC......................................................................................................7

Phases in Time-driven Activity based costing.......................................................................7

Conclusion................................................................................................................................10

References:...............................................................................................................................10

Report on Time-Driven ABC System 2

Executive Summary

Leaving small organisations, Time and cost is a major barrier in ABC enabled organisations

when the company has nearly 100 activities and 5 Lac cost objects. Consequently, Data and

storage of around 2 billion items would be required if ABC is implemented. Taking other

example in consideration, Hendee Enterprises, fabricator of awnings (worth $ 12 million)

took four days to calculate cost for its 39 departments, 140 activities, 9,000 orders and 44,000

line items.

TDABC has the ability to handle complex issues. Further it relies on informal managerial

estimates not considering complex employee surveys that are subjective. Adding further, it is

relatively flexible enough to accommodate the complexity of operations. Moreover, TDABC

can be installed very fast and can be updated with response to changes in processes & orders.

It pinpoints unutilised resource capacity also.

Introduction and Description of Client

The world is changing and change itself is changing. With the passage of time, the Universe

of Business and Management is witnessing tectonic shift in Business Environment and

Business Practices. For Instance, the concept of ABC was popular in 1990’s. In the present

era, without underestimating the utility of ABC System, the concept of ABC system of

costing has been replaced by better alternative practice – Time-Driven Activity based costing

(TDABC). TDABC looks fool-proof and fined –tuned with the need of an hour. However, in

real life it has lost some relevance with the change in facts and circumstances and changing

size of business organisations

The discussion on the Time-Driven Activity based costing (TDABC) will be explained with

the help of example of Cases Study. The client of Management Consultancy firm is an

entrepreneur who owns and manages Hotel. His Hotel provides various services: Food

Executive Summary

Leaving small organisations, Time and cost is a major barrier in ABC enabled organisations

when the company has nearly 100 activities and 5 Lac cost objects. Consequently, Data and

storage of around 2 billion items would be required if ABC is implemented. Taking other

example in consideration, Hendee Enterprises, fabricator of awnings (worth $ 12 million)

took four days to calculate cost for its 39 departments, 140 activities, 9,000 orders and 44,000

line items.

TDABC has the ability to handle complex issues. Further it relies on informal managerial

estimates not considering complex employee surveys that are subjective. Adding further, it is

relatively flexible enough to accommodate the complexity of operations. Moreover, TDABC

can be installed very fast and can be updated with response to changes in processes & orders.

It pinpoints unutilised resource capacity also.

Introduction and Description of Client

The world is changing and change itself is changing. With the passage of time, the Universe

of Business and Management is witnessing tectonic shift in Business Environment and

Business Practices. For Instance, the concept of ABC was popular in 1990’s. In the present

era, without underestimating the utility of ABC System, the concept of ABC system of

costing has been replaced by better alternative practice – Time-Driven Activity based costing

(TDABC). TDABC looks fool-proof and fined –tuned with the need of an hour. However, in

real life it has lost some relevance with the change in facts and circumstances and changing

size of business organisations

The discussion on the Time-Driven Activity based costing (TDABC) will be explained with

the help of example of Cases Study. The client of Management Consultancy firm is an

entrepreneur who owns and manages Hotel. His Hotel provides various services: Food

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Report on Time-Driven ABC System 3

Services, Room Services, reception of guests, Dance floor, Event management and other

related services. He has already implemented Activity Based Costing. Now he has expanded

his operation by infusing $ 100 million dollars. However, he has cost escalation issue.

Further, he recently attended seminar on Time-Driven Activity-Based Costing. He wants an

analysis on whether he should replace Activity Based Costing System (ABC) by Time-

Driven Activity based costing (TDABC) or continue with ABC system. His objective is to

know the various costs exactly, control cost and expenditure and consequently increase profit

margin.

Description of Time-Driven Activity Based Management and it’s features

Before 1985, Costing Systems were not advanced and were not prevalent among various

Industries. However, in 1987, Cooper and Kaplan devised the concept of Activity Based

Costing System (The Economist, 2018). Within few years, it became the buzzword of

Corporates as it solved the cost escalation issues of thousands of companies. However, with

the passage of time and advancement in Information and Communication Technology, the

businesses became complex and difficult to manage (Miller, 2018).

Now ABC system has lost relevance in managing large Organisations as with the passage of

time activities of business have become complex. Moreover, ABC system is difficult to

implement. Adding further it is difficult to maintain (Onlinemasters.ohio.edu,

2018).Secondly, ABC system became less effective as this method was not capable of taking

into consideration the complexity of operations of enterprises, was expensive to install and

took long time in implementation. Moreover, when employees are assessed on how much

time they have spent on various activities, they report partial metrics as they do not disclose

idle or unused time (Simplestudies.com, 2018).

Services, Room Services, reception of guests, Dance floor, Event management and other

related services. He has already implemented Activity Based Costing. Now he has expanded

his operation by infusing $ 100 million dollars. However, he has cost escalation issue.

Further, he recently attended seminar on Time-Driven Activity-Based Costing. He wants an

analysis on whether he should replace Activity Based Costing System (ABC) by Time-

Driven Activity based costing (TDABC) or continue with ABC system. His objective is to

know the various costs exactly, control cost and expenditure and consequently increase profit

margin.

Description of Time-Driven Activity Based Management and it’s features

Before 1985, Costing Systems were not advanced and were not prevalent among various

Industries. However, in 1987, Cooper and Kaplan devised the concept of Activity Based

Costing System (The Economist, 2018). Within few years, it became the buzzword of

Corporates as it solved the cost escalation issues of thousands of companies. However, with

the passage of time and advancement in Information and Communication Technology, the

businesses became complex and difficult to manage (Miller, 2018).

Now ABC system has lost relevance in managing large Organisations as with the passage of

time activities of business have become complex. Moreover, ABC system is difficult to

implement. Adding further it is difficult to maintain (Onlinemasters.ohio.edu,

2018).Secondly, ABC system became less effective as this method was not capable of taking

into consideration the complexity of operations of enterprises, was expensive to install and

took long time in implementation. Moreover, when employees are assessed on how much

time they have spent on various activities, they report partial metrics as they do not disclose

idle or unused time (Simplestudies.com, 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Report on Time-Driven ABC System 4

So, in ABC System, full capacity is assumed that provides biased results and biased

interpretation (Oklu, R., Haas, D., Kaplan, R., Brinegar, K., Bassoff, N., Harvey, H., Brink, J.

and Prabhakar, A., 2018). This leads to assessing of cost-driver rates that are too high and

wrong. However, TDABC considers realistic figures by deducting idle time of chats and

other informal activities. In TDABC, management assesses resource demand as per each

transaction, customer or product rather than assigning resource cost to the activities in the

first step and then to customers or products. Moreover in TDABC only two parameters are

considered: Cost per time unit of supplying capacity of resources and unit times of

consumption of resources by customers, services or producers (Kaplan and Anderson, 2006).

The fact that ABC System has disadvantages doesn’t mean it has no utility (Barndt, Oehlers

and Soltis, 2018).ABC method has solved dilemma of hundreds of companies (Campanale,

Cinquini and Tenucci, 2018).Consequently Time-Driven Activity Based Costing (TDABC)

was devised by RS Kaplan and Steven R.Anderson in the year 2004 and soon became popular

and replaced traditional ABC.TDABC takes into consideration duration cost drivers (hours or

minutes) in place of Transaction cost drivers (number of Bills processed). Only two

yardsticks are required in TDABC: cost per time unit for supplying resources and the unit

times of usage of resource capacity by products, customers and services (Tibor, L., Schultz,

S., Menaker, R., Weber, B., Ness, J., Smith, P. and Young, P., 2018).The ABC system has

assisted many organisations by improving processes on Shop floor, low cost designs of

products and other benefits (Bahnub, 2010).

Difference between ABC System and TDABC

In ABC system, Decision making takes place at product level while in TDABC decisions

takes place at both product level and process level (Wiese, 2009).In ABC System, the focus is

on financial measures whereas in TDABC focus is on non financial measures(Kaplan and

Cooper, 1998).

So, in ABC System, full capacity is assumed that provides biased results and biased

interpretation (Oklu, R., Haas, D., Kaplan, R., Brinegar, K., Bassoff, N., Harvey, H., Brink, J.

and Prabhakar, A., 2018). This leads to assessing of cost-driver rates that are too high and

wrong. However, TDABC considers realistic figures by deducting idle time of chats and

other informal activities. In TDABC, management assesses resource demand as per each

transaction, customer or product rather than assigning resource cost to the activities in the

first step and then to customers or products. Moreover in TDABC only two parameters are

considered: Cost per time unit of supplying capacity of resources and unit times of

consumption of resources by customers, services or producers (Kaplan and Anderson, 2006).

The fact that ABC System has disadvantages doesn’t mean it has no utility (Barndt, Oehlers

and Soltis, 2018).ABC method has solved dilemma of hundreds of companies (Campanale,

Cinquini and Tenucci, 2018).Consequently Time-Driven Activity Based Costing (TDABC)

was devised by RS Kaplan and Steven R.Anderson in the year 2004 and soon became popular

and replaced traditional ABC.TDABC takes into consideration duration cost drivers (hours or

minutes) in place of Transaction cost drivers (number of Bills processed). Only two

yardsticks are required in TDABC: cost per time unit for supplying resources and the unit

times of usage of resource capacity by products, customers and services (Tibor, L., Schultz,

S., Menaker, R., Weber, B., Ness, J., Smith, P. and Young, P., 2018).The ABC system has

assisted many organisations by improving processes on Shop floor, low cost designs of

products and other benefits (Bahnub, 2010).

Difference between ABC System and TDABC

In ABC system, Decision making takes place at product level while in TDABC decisions

takes place at both product level and process level (Wiese, 2009).In ABC System, the focus is

on financial measures whereas in TDABC focus is on non financial measures(Kaplan and

Cooper, 1998).

Report on Time-Driven ABC System 5

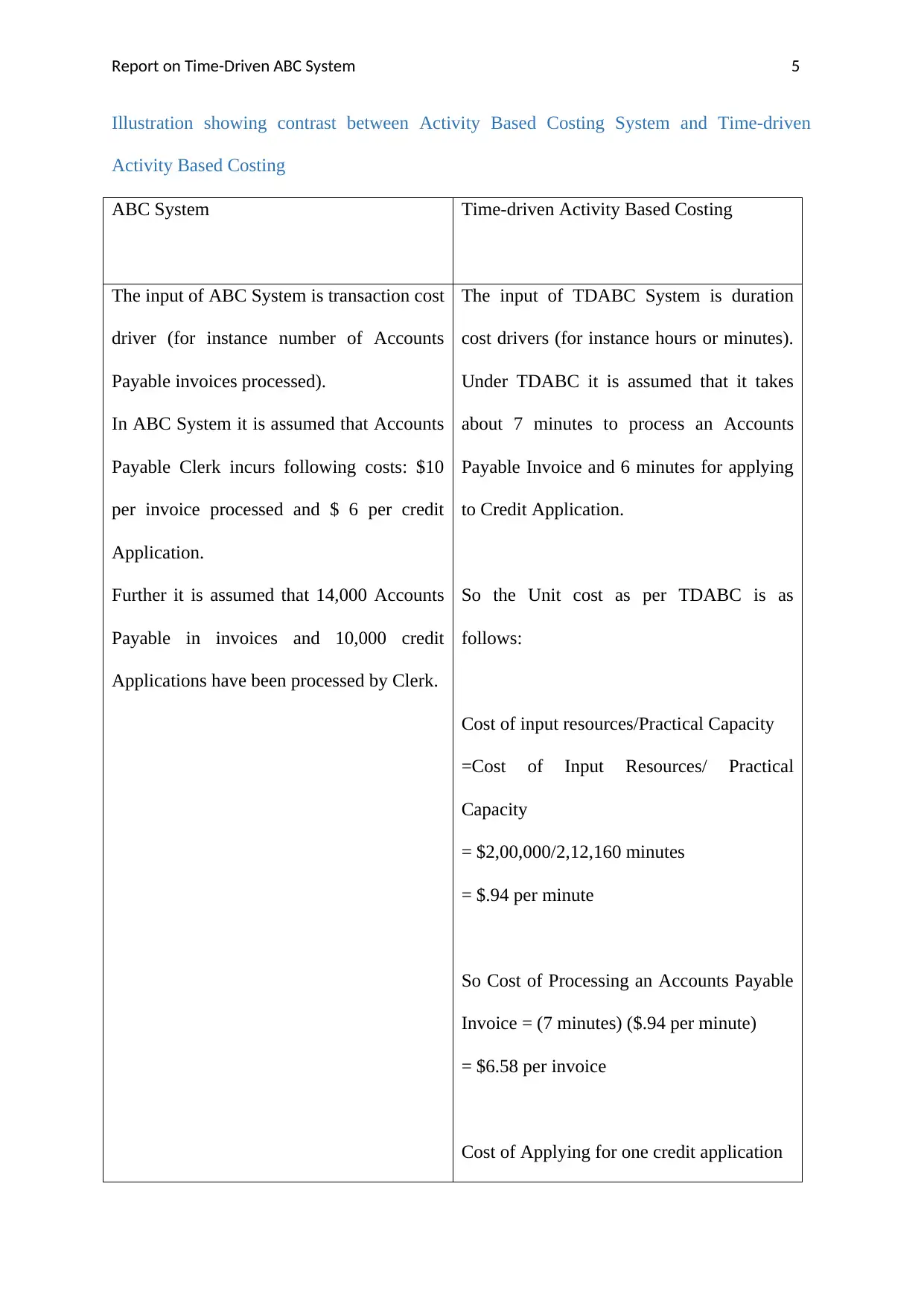

Illustration showing contrast between Activity Based Costing System and Time-driven

Activity Based Costing

ABC System Time-driven Activity Based Costing

The input of ABC System is transaction cost

driver (for instance number of Accounts

Payable invoices processed).

In ABC System it is assumed that Accounts

Payable Clerk incurs following costs: $10

per invoice processed and $ 6 per credit

Application.

Further it is assumed that 14,000 Accounts

Payable in invoices and 10,000 credit

Applications have been processed by Clerk.

The input of TDABC System is duration

cost drivers (for instance hours or minutes).

Under TDABC it is assumed that it takes

about 7 minutes to process an Accounts

Payable Invoice and 6 minutes for applying

to Credit Application.

So the Unit cost as per TDABC is as

follows:

Cost of input resources/Practical Capacity

=Cost of Input Resources/ Practical

Capacity

= $2,00,000/2,12,160 minutes

= $.94 per minute

So Cost of Processing an Accounts Payable

Invoice = (7 minutes) ($.94 per minute)

= $6.58 per invoice

Cost of Applying for one credit application

Illustration showing contrast between Activity Based Costing System and Time-driven

Activity Based Costing

ABC System Time-driven Activity Based Costing

The input of ABC System is transaction cost

driver (for instance number of Accounts

Payable invoices processed).

In ABC System it is assumed that Accounts

Payable Clerk incurs following costs: $10

per invoice processed and $ 6 per credit

Application.

Further it is assumed that 14,000 Accounts

Payable in invoices and 10,000 credit

Applications have been processed by Clerk.

The input of TDABC System is duration

cost drivers (for instance hours or minutes).

Under TDABC it is assumed that it takes

about 7 minutes to process an Accounts

Payable Invoice and 6 minutes for applying

to Credit Application.

So the Unit cost as per TDABC is as

follows:

Cost of input resources/Practical Capacity

=Cost of Input Resources/ Practical

Capacity

= $2,00,000/2,12,160 minutes

= $.94 per minute

So Cost of Processing an Accounts Payable

Invoice = (7 minutes) ($.94 per minute)

= $6.58 per invoice

Cost of Applying for one credit application

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Report on Time-Driven ABC System 6

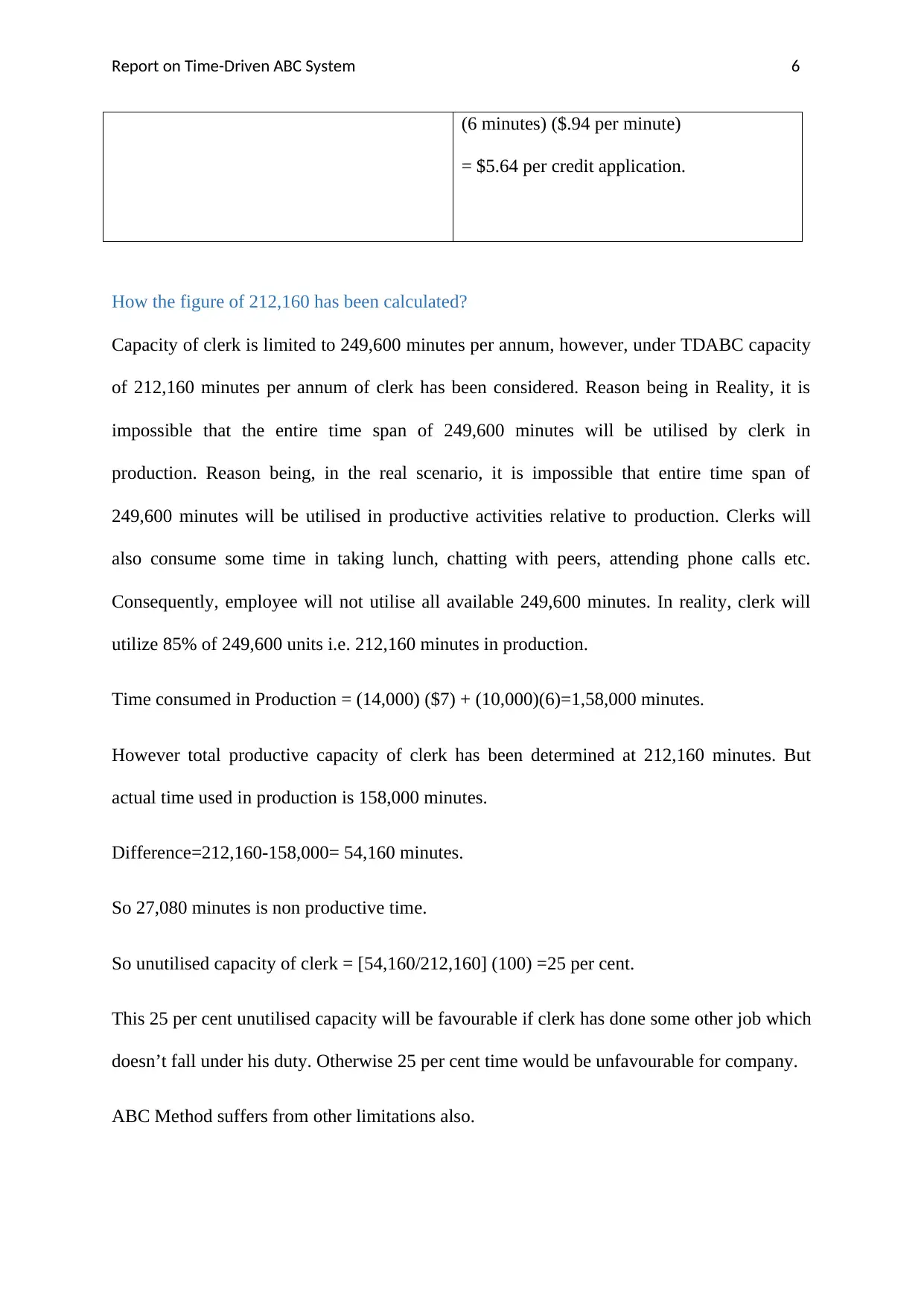

(6 minutes) ($.94 per minute)

= $5.64 per credit application.

How the figure of 212,160 has been calculated?

Capacity of clerk is limited to 249,600 minutes per annum, however, under TDABC capacity

of 212,160 minutes per annum of clerk has been considered. Reason being in Reality, it is

impossible that the entire time span of 249,600 minutes will be utilised by clerk in

production. Reason being, in the real scenario, it is impossible that entire time span of

249,600 minutes will be utilised in productive activities relative to production. Clerks will

also consume some time in taking lunch, chatting with peers, attending phone calls etc.

Consequently, employee will not utilise all available 249,600 minutes. In reality, clerk will

utilize 85% of 249,600 units i.e. 212,160 minutes in production.

Time consumed in Production = (14,000) ($7) + (10,000)(6)=1,58,000 minutes.

However total productive capacity of clerk has been determined at 212,160 minutes. But

actual time used in production is 158,000 minutes.

Difference=212,160-158,000= 54,160 minutes.

So 27,080 minutes is non productive time.

So unutilised capacity of clerk = [54,160/212,160] (100) =25 per cent.

This 25 per cent unutilised capacity will be favourable if clerk has done some other job which

doesn’t fall under his duty. Otherwise 25 per cent time would be unfavourable for company.

ABC Method suffers from other limitations also.

(6 minutes) ($.94 per minute)

= $5.64 per credit application.

How the figure of 212,160 has been calculated?

Capacity of clerk is limited to 249,600 minutes per annum, however, under TDABC capacity

of 212,160 minutes per annum of clerk has been considered. Reason being in Reality, it is

impossible that the entire time span of 249,600 minutes will be utilised by clerk in

production. Reason being, in the real scenario, it is impossible that entire time span of

249,600 minutes will be utilised in productive activities relative to production. Clerks will

also consume some time in taking lunch, chatting with peers, attending phone calls etc.

Consequently, employee will not utilise all available 249,600 minutes. In reality, clerk will

utilize 85% of 249,600 units i.e. 212,160 minutes in production.

Time consumed in Production = (14,000) ($7) + (10,000)(6)=1,58,000 minutes.

However total productive capacity of clerk has been determined at 212,160 minutes. But

actual time used in production is 158,000 minutes.

Difference=212,160-158,000= 54,160 minutes.

So 27,080 minutes is non productive time.

So unutilised capacity of clerk = [54,160/212,160] (100) =25 per cent.

This 25 per cent unutilised capacity will be favourable if clerk has done some other job which

doesn’t fall under his duty. Otherwise 25 per cent time would be unfavourable for company.

ABC Method suffers from other limitations also.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Report on Time-Driven ABC System 7

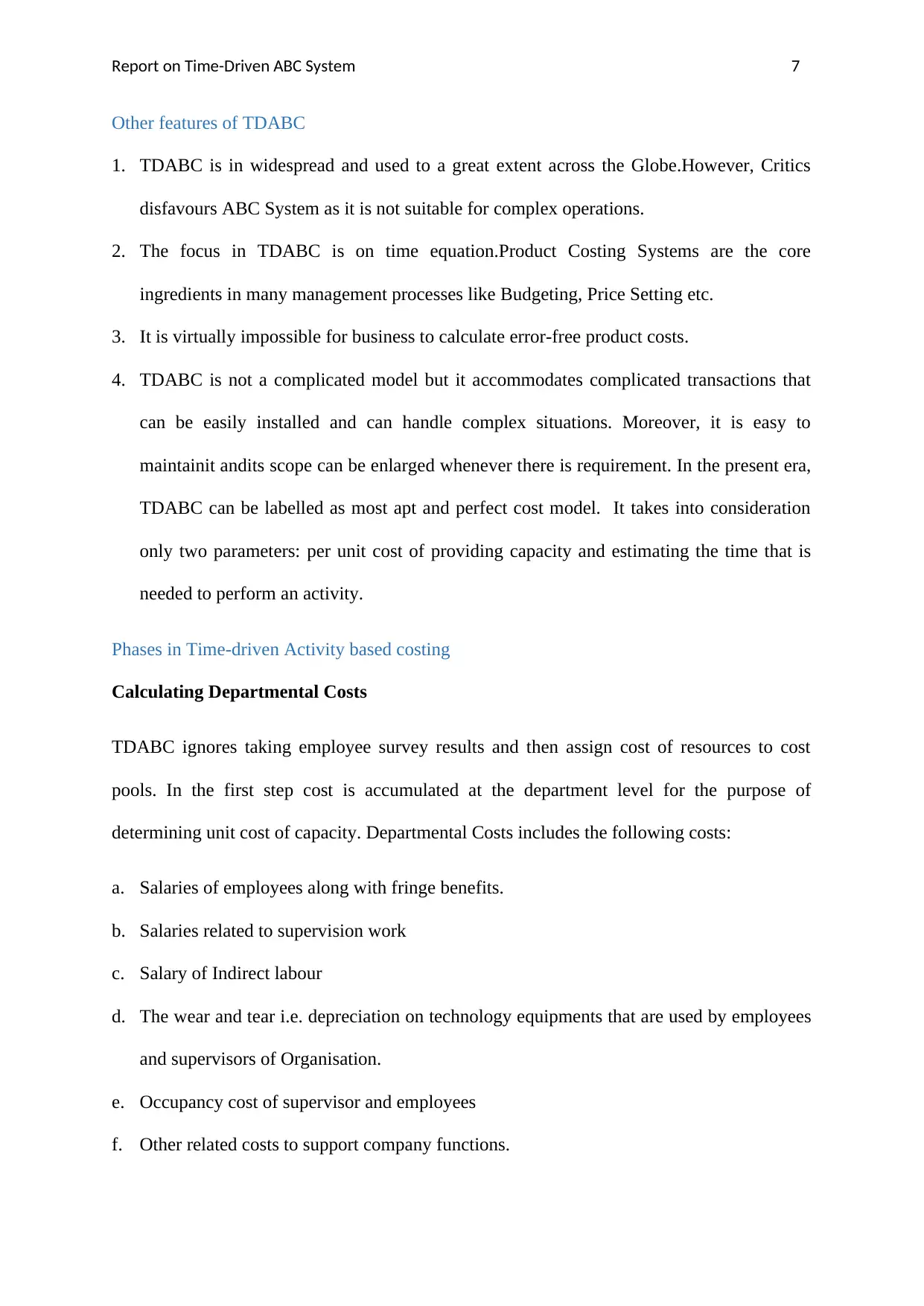

Other features of TDABC

1. TDABC is in widespread and used to a great extent across the Globe.However, Critics

disfavours ABC System as it is not suitable for complex operations.

2. The focus in TDABC is on time equation.Product Costing Systems are the core

ingredients in many management processes like Budgeting, Price Setting etc.

3. It is virtually impossible for business to calculate error-free product costs.

4. TDABC is not a complicated model but it accommodates complicated transactions that

can be easily installed and can handle complex situations. Moreover, it is easy to

maintainit andits scope can be enlarged whenever there is requirement. In the present era,

TDABC can be labelled as most apt and perfect cost model. It takes into consideration

only two parameters: per unit cost of providing capacity and estimating the time that is

needed to perform an activity.

Phases in Time-driven Activity based costing

Calculating Departmental Costs

TDABC ignores taking employee survey results and then assign cost of resources to cost

pools. In the first step cost is accumulated at the department level for the purpose of

determining unit cost of capacity. Departmental Costs includes the following costs:

a. Salaries of employees along with fringe benefits.

b. Salaries related to supervision work

c. Salary of Indirect labour

d. The wear and tear i.e. depreciation on technology equipments that are used by employees

and supervisors of Organisation.

e. Occupancy cost of supervisor and employees

f. Other related costs to support company functions.

Other features of TDABC

1. TDABC is in widespread and used to a great extent across the Globe.However, Critics

disfavours ABC System as it is not suitable for complex operations.

2. The focus in TDABC is on time equation.Product Costing Systems are the core

ingredients in many management processes like Budgeting, Price Setting etc.

3. It is virtually impossible for business to calculate error-free product costs.

4. TDABC is not a complicated model but it accommodates complicated transactions that

can be easily installed and can handle complex situations. Moreover, it is easy to

maintainit andits scope can be enlarged whenever there is requirement. In the present era,

TDABC can be labelled as most apt and perfect cost model. It takes into consideration

only two parameters: per unit cost of providing capacity and estimating the time that is

needed to perform an activity.

Phases in Time-driven Activity based costing

Calculating Departmental Costs

TDABC ignores taking employee survey results and then assign cost of resources to cost

pools. In the first step cost is accumulated at the department level for the purpose of

determining unit cost of capacity. Departmental Costs includes the following costs:

a. Salaries of employees along with fringe benefits.

b. Salaries related to supervision work

c. Salary of Indirect labour

d. The wear and tear i.e. depreciation on technology equipments that are used by employees

and supervisors of Organisation.

e. Occupancy cost of supervisor and employees

f. Other related costs to support company functions.

Report on Time-Driven ABC System 8

What should be done or emphasised?

a. Sustaining expenses of organisation should be considered. The above-mentioned costs are

difficult to trace to operating units.

b. TDABC analysis should be extended to shared services.

Calculating Practical Capacity

TDABC utilises time to drive cost. Capacity is measured in time (seconds, minutes or hours)

that employees have to use for executing activities related to work (Haron, 2010). Total

Capacity is measured in machine hours available multiplied by number of employees. But the

time allotted is not the total time utilised in performing activities. Employees will use some

time in chatting with peers and other informal activities(Kaplan and Anderson, 2007).So

Machine hours should be reduced after considering informal activities to reach the figure of

Practical Capacity.

Identification of Activities

The next step is the identification of activities that are performed in each department. The

activity dictionary of ABC system is helpful in identifying the processes. Flow charts and

narratives can also be prepared. With the adoption of TDABC employee survey have been

replaced by estimates of the time or capacity that is required to perform an activity and

present it in terms of equation. The equations includes base time that is required to process a

transaction along with time required for variation in the activities that would be

witnessed.Commonly, Equations are formed by starting with principal factor of transaction

and then adding variables. It is better to start with the most costly processes. After defining

processes, the important variables or drivers that consume time are identified. In the first step,

it is easier to use driver data that has been previously collected instead of developing and

expanding data collection facilities. The format of time equation is as follows:

What should be done or emphasised?

a. Sustaining expenses of organisation should be considered. The above-mentioned costs are

difficult to trace to operating units.

b. TDABC analysis should be extended to shared services.

Calculating Practical Capacity

TDABC utilises time to drive cost. Capacity is measured in time (seconds, minutes or hours)

that employees have to use for executing activities related to work (Haron, 2010). Total

Capacity is measured in machine hours available multiplied by number of employees. But the

time allotted is not the total time utilised in performing activities. Employees will use some

time in chatting with peers and other informal activities(Kaplan and Anderson, 2007).So

Machine hours should be reduced after considering informal activities to reach the figure of

Practical Capacity.

Identification of Activities

The next step is the identification of activities that are performed in each department. The

activity dictionary of ABC system is helpful in identifying the processes. Flow charts and

narratives can also be prepared. With the adoption of TDABC employee survey have been

replaced by estimates of the time or capacity that is required to perform an activity and

present it in terms of equation. The equations includes base time that is required to process a

transaction along with time required for variation in the activities that would be

witnessed.Commonly, Equations are formed by starting with principal factor of transaction

and then adding variables. It is better to start with the most costly processes. After defining

processes, the important variables or drivers that consume time are identified. In the first step,

it is easier to use driver data that has been previously collected instead of developing and

expanding data collection facilities. The format of time equation is as follows:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Report on Time-Driven ABC System 9

Depending on the resource availability, transaction base times along with time required to

accomplish each variable can be determined. Industrial engineering data of time and motion

studies provides valuable information. The two approaches for data gathering and observation

are employee survey and observation of the transactions being processed and then taking into

consideration average time. TDBAC takes into consideration less data in comparison to ABC

System. However, TDABC requires transaction data on customers, products, orders and other

cost objects. Companies that have installed Enterprise Resource Planning already process rich

data. Rest of the organisations have to invest in the necessary technology. It is better to start

with test drive: pilot study or small-scale implementation. The advantage of TDABC is that

time equations can be updated for improvements.

Conclusion

So Time-Driven Activity based costing is suitable for the client who is the entrepreneur,

manages the hotel and is currently planning to expand operations by infusing funds.

Company is also facing cost escalation issue. Further, Time-based Activity Based Costing in

the above-mentioned hotel has lost relevance since the hotel considered will operate on large

scale. ABC is very difficult to utilise in case of large organisations. Last but not the least, It is

better to implement TDABC since company is facing complexity in operations due to

expansion.

Depending on the resource availability, transaction base times along with time required to

accomplish each variable can be determined. Industrial engineering data of time and motion

studies provides valuable information. The two approaches for data gathering and observation

are employee survey and observation of the transactions being processed and then taking into

consideration average time. TDBAC takes into consideration less data in comparison to ABC

System. However, TDABC requires transaction data on customers, products, orders and other

cost objects. Companies that have installed Enterprise Resource Planning already process rich

data. Rest of the organisations have to invest in the necessary technology. It is better to start

with test drive: pilot study or small-scale implementation. The advantage of TDABC is that

time equations can be updated for improvements.

Conclusion

So Time-Driven Activity based costing is suitable for the client who is the entrepreneur,

manages the hotel and is currently planning to expand operations by infusing funds.

Company is also facing cost escalation issue. Further, Time-based Activity Based Costing in

the above-mentioned hotel has lost relevance since the hotel considered will operate on large

scale. ABC is very difficult to utilise in case of large organisations. Last but not the least, It is

better to implement TDABC since company is facing complexity in operations due to

expansion.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Report on Time-Driven ABC System 10

References:

Bahnub, B. (2010). Activity-Based Management for Financial Institutions: Driving Bottom-

Line Results. Indianapolis: Wiley.

Barndt, R., Oehlers, P. and Soltis, G. (2018). Time-Driven Activity Based Costing: A

Powerful Cost Model. [online] Tscpa.org. Available at: https://www.tscpa.org/docs/default-

source/default-document-library/activitybasedcostmodel_marapril2015.pdf?sfvrsn=2

[Accessed 4 Jan. 2018].

Campanale, C., Cinquini, L. and Tenucci, A. (2018). Time-driven activity-based costing to

improve transparency and decision making in healthcare | A case study | Qualitative

Research in Accounting & Management | Vol 11, No 2. [online] Emeraldinsight.com.

Available at: http://www.emeraldinsight.com/doi/abs/10.1108/QRAM-04-2014-0036

[Accessed 4 Jan. 2018].

Haron, A. (2010). Application of Time-driven Activity Based Costing (TDABC) for Small-

medium Enterprise (SME) Company. Johor: UniversitiTeknologi Malaysia.

Kaplan, R. and Anderson, S. (2006). Time-Driven Activity-Based Costing. [online] HBS

Working Knowledge. Available at: https://hbswk.hbs.edu/item/time-driven-activity-based-

costing [Accessed 4 Jan. 2018].

Kaplan, R. and Anderson, S. (2007). Time-Driven Activity-Based Costing: A Simpler and

More Powerful Path to Higher Profits. Massachusetts: Harvard Business Press.

References:

Bahnub, B. (2010). Activity-Based Management for Financial Institutions: Driving Bottom-

Line Results. Indianapolis: Wiley.

Barndt, R., Oehlers, P. and Soltis, G. (2018). Time-Driven Activity Based Costing: A

Powerful Cost Model. [online] Tscpa.org. Available at: https://www.tscpa.org/docs/default-

source/default-document-library/activitybasedcostmodel_marapril2015.pdf?sfvrsn=2

[Accessed 4 Jan. 2018].

Campanale, C., Cinquini, L. and Tenucci, A. (2018). Time-driven activity-based costing to

improve transparency and decision making in healthcare | A case study | Qualitative

Research in Accounting & Management | Vol 11, No 2. [online] Emeraldinsight.com.

Available at: http://www.emeraldinsight.com/doi/abs/10.1108/QRAM-04-2014-0036

[Accessed 4 Jan. 2018].

Haron, A. (2010). Application of Time-driven Activity Based Costing (TDABC) for Small-

medium Enterprise (SME) Company. Johor: UniversitiTeknologi Malaysia.

Kaplan, R. and Anderson, S. (2006). Time-Driven Activity-Based Costing. [online] HBS

Working Knowledge. Available at: https://hbswk.hbs.edu/item/time-driven-activity-based-

costing [Accessed 4 Jan. 2018].

Kaplan, R. and Anderson, S. (2007). Time-Driven Activity-Based Costing: A Simpler and

More Powerful Path to Higher Profits. Massachusetts: Harvard Business Press.

Report on Time-Driven ABC System 11

Kaplan, R. and Cooper, R. (1998). Cost & Effect: Using Integrated Cost Systems to Drive

Profitability and Performance. Massachusetts: Harvard Business Press.

Miller, T. (2018). The ABCs of Activity-Based Costing for Logistics. [online] Material

Handling and Logistics (MHL News). Available at: http://www.mhlnews.com/transportation-

distribution/abcs-activity-based-costing-logistics [Accessed 4 Jan. 2018].

Oklu, R., Haas, D., Kaplan, R., Brinegar, K., Bassoff, N., Harvey, H., Brink, J. and

Prabhakar, A. (2018). Time-Driven Activity-Based Costing in IR. [online]Journal of Vascular

and Interventional Radiology. Available at: http://www.jvir.org/article/S1051-

0443(15)00660-0/abstract [Accessed 4 Jan. 2018].

Onlinemasters.ohio.edu. (2018). Using Activity-Based Costing (ABC) to Increase

Profitability | Ohio University. [online] Available at: https://onlinemasters.ohio.edu/using-

activity-based-costing-abc-to-increase-profitability/ [Accessed 4 Jan. 2018].

Simplestudies.com. (2018). A different approach to activity-based costing (ABC) -

Accounting guide | Simplestudies.com. [online] Available at:

http://simplestudies.com/different_approach_to_activity_based_costing_abc.html/page/2

[Accessed 4 Jan. 2018].

The Economist. (2018). Activity-based costing. [online] Available at:

http://www.economist.com/node/13933812 [Accessed 4 Jan. 2018].

Tibor, L., Schultz, S., Menaker, R., Weber, B., Ness, J., Smith, P. and Young, P. (2018).

Improving Efficiency Using Time-Driven Activity-Based Costing Methodology. [online]

Journal of the American College of Radiology. Available at:

http://www.jacr.org/article/S1546-1440(16)31323-0/abstract [Accessed 4 Jan. 2018].

Wiese, N. (2009). Activity-Based-Costing (ABC). Munich: GRIN Verlag.

Kaplan, R. and Cooper, R. (1998). Cost & Effect: Using Integrated Cost Systems to Drive

Profitability and Performance. Massachusetts: Harvard Business Press.

Miller, T. (2018). The ABCs of Activity-Based Costing for Logistics. [online] Material

Handling and Logistics (MHL News). Available at: http://www.mhlnews.com/transportation-

distribution/abcs-activity-based-costing-logistics [Accessed 4 Jan. 2018].

Oklu, R., Haas, D., Kaplan, R., Brinegar, K., Bassoff, N., Harvey, H., Brink, J. and

Prabhakar, A. (2018). Time-Driven Activity-Based Costing in IR. [online]Journal of Vascular

and Interventional Radiology. Available at: http://www.jvir.org/article/S1051-

0443(15)00660-0/abstract [Accessed 4 Jan. 2018].

Onlinemasters.ohio.edu. (2018). Using Activity-Based Costing (ABC) to Increase

Profitability | Ohio University. [online] Available at: https://onlinemasters.ohio.edu/using-

activity-based-costing-abc-to-increase-profitability/ [Accessed 4 Jan. 2018].

Simplestudies.com. (2018). A different approach to activity-based costing (ABC) -

Accounting guide | Simplestudies.com. [online] Available at:

http://simplestudies.com/different_approach_to_activity_based_costing_abc.html/page/2

[Accessed 4 Jan. 2018].

The Economist. (2018). Activity-based costing. [online] Available at:

http://www.economist.com/node/13933812 [Accessed 4 Jan. 2018].

Tibor, L., Schultz, S., Menaker, R., Weber, B., Ness, J., Smith, P. and Young, P. (2018).

Improving Efficiency Using Time-Driven Activity-Based Costing Methodology. [online]

Journal of the American College of Radiology. Available at:

http://www.jacr.org/article/S1546-1440(16)31323-0/abstract [Accessed 4 Jan. 2018].

Wiese, N. (2009). Activity-Based-Costing (ABC). Munich: GRIN Verlag.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.