Business Finance Report: Module MOD003319, Semester 2, 2019/20

VerifiedAdded on 2023/01/11

|13

|3489

|64

Report

AI Summary

This report delves into key aspects of business finance, beginning with an exploration of the differences between profit and cash flow, alongside an explanation of relevant accounting terms. It examines the impact of working capital on cash flow and analyzes the financial results of Mediterranean Delights Ltd, including a cash flow statement. The report then provides recommendations for managing financial results. Part 2 focuses on budgeting, outlining the purpose of preparing a budget and comparing traditional and alternative budgeting approaches, with a specific focus on Second Sight PLC. The report concludes with an analysis of the best budgeting approach for the company, offering insights into effective financial management.

BUSINESS

FINANCE

FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

EXECUTIVE SUMMARY.........................................................................................................................3

PART 1.......................................................................................................................................................3

(a) Profit and cash flow and their difference............................................................................................3

(b) Meaning of accounting terms.............................................................................................................4

(c) Changes in working capital affect cash flow......................................................................................5

2. Manage financial results......................................................................................................................5

3. Analysis and recommendations...........................................................................................................7

PART 2.......................................................................................................................................................8

EXECUTIVE SUMMARY.........................................................................................................................8

1. Purpose of preparing budget................................................................................................................8

2. Application of traditional and alternative budgeting approach for planning cost of second sight plc

...............................................................................................................................................................11

3. Analysis of best approach..................................................................................................................11

CONCLUSION.............................................................................................................................................12

REFERENCES..............................................................................................................................................13

EXECUTIVE SUMMARY.........................................................................................................................3

PART 1.......................................................................................................................................................3

(a) Profit and cash flow and their difference............................................................................................3

(b) Meaning of accounting terms.............................................................................................................4

(c) Changes in working capital affect cash flow......................................................................................5

2. Manage financial results......................................................................................................................5

3. Analysis and recommendations...........................................................................................................7

PART 2.......................................................................................................................................................8

EXECUTIVE SUMMARY.........................................................................................................................8

1. Purpose of preparing budget................................................................................................................8

2. Application of traditional and alternative budgeting approach for planning cost of second sight plc

...............................................................................................................................................................11

3. Analysis of best approach..................................................................................................................11

CONCLUSION.............................................................................................................................................12

REFERENCES..............................................................................................................................................13

EXECUTIVE SUMMARY

Business finance relates to the money management practice for the business. This is

important in managing a business. An organization's effectiveness depends on how well its

executives handle cash-making streams. This report is based on Mediterranean Delights Ltd. data

gathering. Within this concept of benefit and cash flow the impact of working capital on cash-

flow tasks and ways is explained which allows managers to produce successful cash-flow tasks

with the support of successful working capital management.

PART 1

(a) Profit and cash flow and their difference

Profit- The term benefit defines company sector entities as a net price of tax benefit aeries across

their operations. Either financial or non-financial, it is a part of any company organization. It

demonstrates the company's progress and good operating position (Burns and Dewhurst, 2016).

Cash flow- It describes a net quantity of gash generated by flow activities and outflow. Cash

flow announcement is used by business associations to analyze the activities supporting

production money from financing, investment and operations. This allows management to make

its fund strategy choices. Some believe that the cash flow and dividends are similar, although

there is definitely be a disparity below.

Difference between profit and cash flow:

Particular Profit Cash flow

Meaning Positive differences in revenue

and production and running

costs.

Money interest that flows in or

out of a specific time.

Time No time for calculating profits

will be set. Companies can

calculate their profits on a

monthly or regular basis.

No time for calculating profits

will be set. Companies can

calculate their profits on a

monthly or regular basis.

Business finance relates to the money management practice for the business. This is

important in managing a business. An organization's effectiveness depends on how well its

executives handle cash-making streams. This report is based on Mediterranean Delights Ltd. data

gathering. Within this concept of benefit and cash flow the impact of working capital on cash-

flow tasks and ways is explained which allows managers to produce successful cash-flow tasks

with the support of successful working capital management.

PART 1

(a) Profit and cash flow and their difference

Profit- The term benefit defines company sector entities as a net price of tax benefit aeries across

their operations. Either financial or non-financial, it is a part of any company organization. It

demonstrates the company's progress and good operating position (Burns and Dewhurst, 2016).

Cash flow- It describes a net quantity of gash generated by flow activities and outflow. Cash

flow announcement is used by business associations to analyze the activities supporting

production money from financing, investment and operations. This allows management to make

its fund strategy choices. Some believe that the cash flow and dividends are similar, although

there is definitely be a disparity below.

Difference between profit and cash flow:

Particular Profit Cash flow

Meaning Positive differences in revenue

and production and running

costs.

Money interest that flows in or

out of a specific time.

Time No time for calculating profits

will be set. Companies can

calculate their profits on a

monthly or regular basis.

No time for calculating profits

will be set. Companies can

calculate their profits on a

monthly or regular basis.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Calculation Profits can also be calculated

using different forms in

financial accounting or.

Economic year revenue

calculated by income and loss

readiness comment.

Cash flow statements are

compiled by administrators to

explain the net cash flow

activity. Cash flow reports are

graded by the manager.

Purpose Set up competitiveness within

the competitive environment.

Financial achievement

acknowledges practices to

generate money.

(b) Meaning of accounting terms

Working capital- It determines the estimated cumulative worth of a company's liquid assets.

Working capital can be a key term used every day for an organization’s company. Manager uses

working capital to fulfill the main requirements of these companies. Gross working capital

means an increase in power and networking capital may be the gaps between a company's

current assets and liabilities. In this term, efficiency and short term financial health can be

achieved (Tomkin, 2016).

Receivable-The term applies to the actual demand for the products and services they purchase for

their buyers from the businesses. This considered companies to be current assets. The debtor-

claim ratio is used by management to determine the degree of success of their customers to

compensate their sum of liability.

Inventory- In accounting the inventories are net value of waste and other equipment and tools

needed by an organization to generate goods and services with its own customers. There are

different forms of inventories such as raw material, finished goods and work in progress goods.

Payables-This term defines the value of economic funding owned by companies of their own

creditors in order to successfully conduct their small business. It generated responsibilities for a

corporation. This term is used by managers to identify a net series of short-term company

obligations (Maxwell, 2017).

using different forms in

financial accounting or.

Economic year revenue

calculated by income and loss

readiness comment.

Cash flow statements are

compiled by administrators to

explain the net cash flow

activity. Cash flow reports are

graded by the manager.

Purpose Set up competitiveness within

the competitive environment.

Financial achievement

acknowledges practices to

generate money.

(b) Meaning of accounting terms

Working capital- It determines the estimated cumulative worth of a company's liquid assets.

Working capital can be a key term used every day for an organization’s company. Manager uses

working capital to fulfill the main requirements of these companies. Gross working capital

means an increase in power and networking capital may be the gaps between a company's

current assets and liabilities. In this term, efficiency and short term financial health can be

achieved (Tomkin, 2016).

Receivable-The term applies to the actual demand for the products and services they purchase for

their buyers from the businesses. This considered companies to be current assets. The debtor-

claim ratio is used by management to determine the degree of success of their customers to

compensate their sum of liability.

Inventory- In accounting the inventories are net value of waste and other equipment and tools

needed by an organization to generate goods and services with its own customers. There are

different forms of inventories such as raw material, finished goods and work in progress goods.

Payables-This term defines the value of economic funding owned by companies of their own

creditors in order to successfully conduct their small business. It generated responsibilities for a

corporation. This term is used by managers to identify a net series of short-term company

obligations (Maxwell, 2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

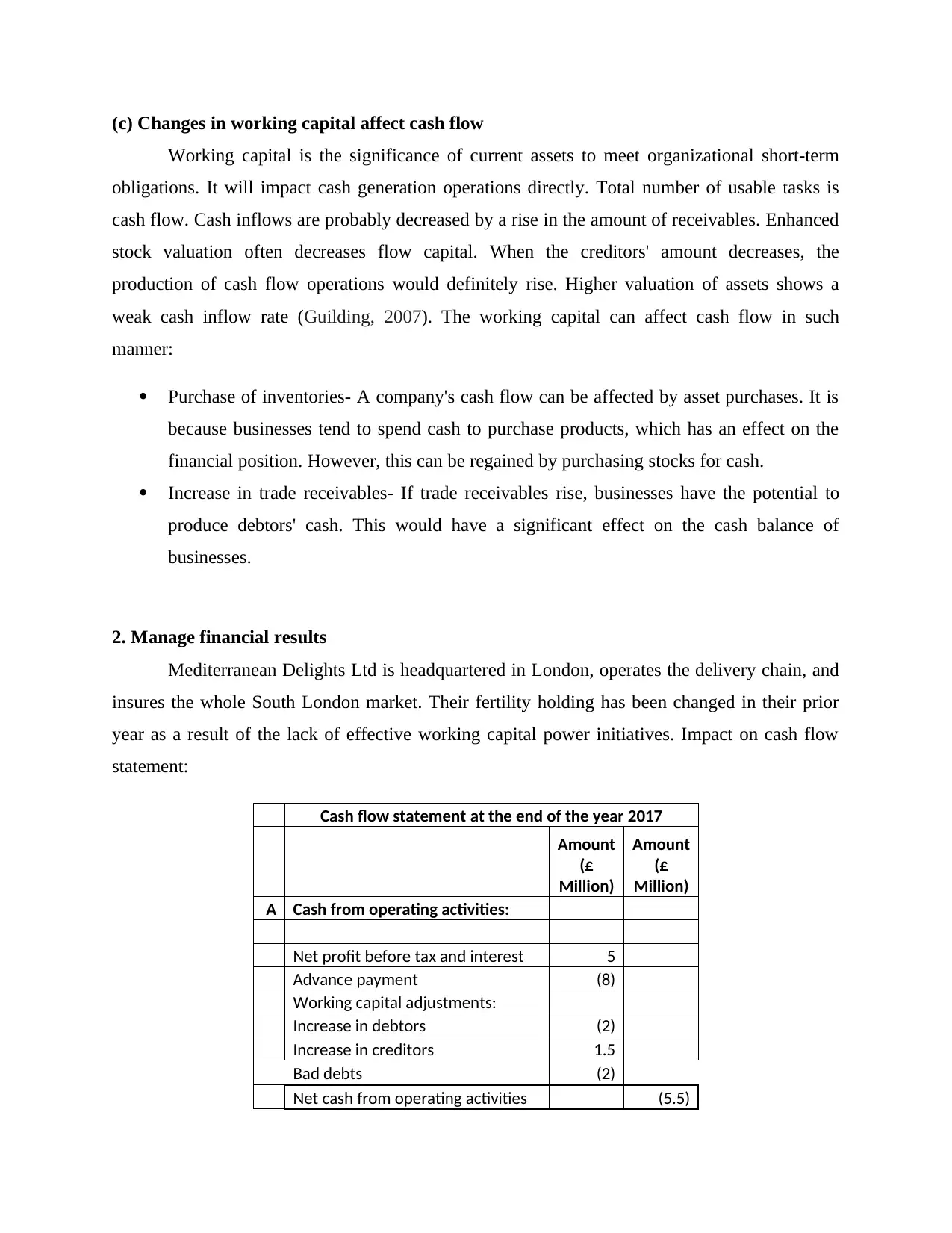

(c) Changes in working capital affect cash flow

Working capital is the significance of current assets to meet organizational short-term

obligations. It will impact cash generation operations directly. Total number of usable tasks is

cash flow. Cash inflows are probably decreased by a rise in the amount of receivables. Enhanced

stock valuation often decreases flow capital. When the creditors' amount decreases, the

production of cash flow operations would definitely rise. Higher valuation of assets shows a

weak cash inflow rate (Guilding, 2007). The working capital can affect cash flow in such

manner:

Purchase of inventories- A company's cash flow can be affected by asset purchases. It is

because businesses tend to spend cash to purchase products, which has an effect on the

financial position. However, this can be regained by purchasing stocks for cash.

Increase in trade receivables- If trade receivables rise, businesses have the potential to

produce debtors' cash. This would have a significant effect on the cash balance of

businesses.

2. Manage financial results

Mediterranean Delights Ltd is headquartered in London, operates the delivery chain, and

insures the whole South London market. Their fertility holding has been changed in their prior

year as a result of the lack of effective working capital power initiatives. Impact on cash flow

statement:

Cash flow statement at the end of the year 2017

Amount

(£

Million)

Amount

(£

Million)

A Cash from operating activities:

Net profit before tax and interest 5

Advance payment (8)

Working capital adjustments:

Increase in debtors (2)

Increase in creditors 1.5

Bad debts (2)

Net cash from operating activities (5.5)

Working capital is the significance of current assets to meet organizational short-term

obligations. It will impact cash generation operations directly. Total number of usable tasks is

cash flow. Cash inflows are probably decreased by a rise in the amount of receivables. Enhanced

stock valuation often decreases flow capital. When the creditors' amount decreases, the

production of cash flow operations would definitely rise. Higher valuation of assets shows a

weak cash inflow rate (Guilding, 2007). The working capital can affect cash flow in such

manner:

Purchase of inventories- A company's cash flow can be affected by asset purchases. It is

because businesses tend to spend cash to purchase products, which has an effect on the

financial position. However, this can be regained by purchasing stocks for cash.

Increase in trade receivables- If trade receivables rise, businesses have the potential to

produce debtors' cash. This would have a significant effect on the cash balance of

businesses.

2. Manage financial results

Mediterranean Delights Ltd is headquartered in London, operates the delivery chain, and

insures the whole South London market. Their fertility holding has been changed in their prior

year as a result of the lack of effective working capital power initiatives. Impact on cash flow

statement:

Cash flow statement at the end of the year 2017

Amount

(£

Million)

Amount

(£

Million)

A Cash from operating activities:

Net profit before tax and interest 5

Advance payment (8)

Working capital adjustments:

Increase in debtors (2)

Increase in creditors 1.5

Bad debts (2)

Net cash from operating activities (5.5)

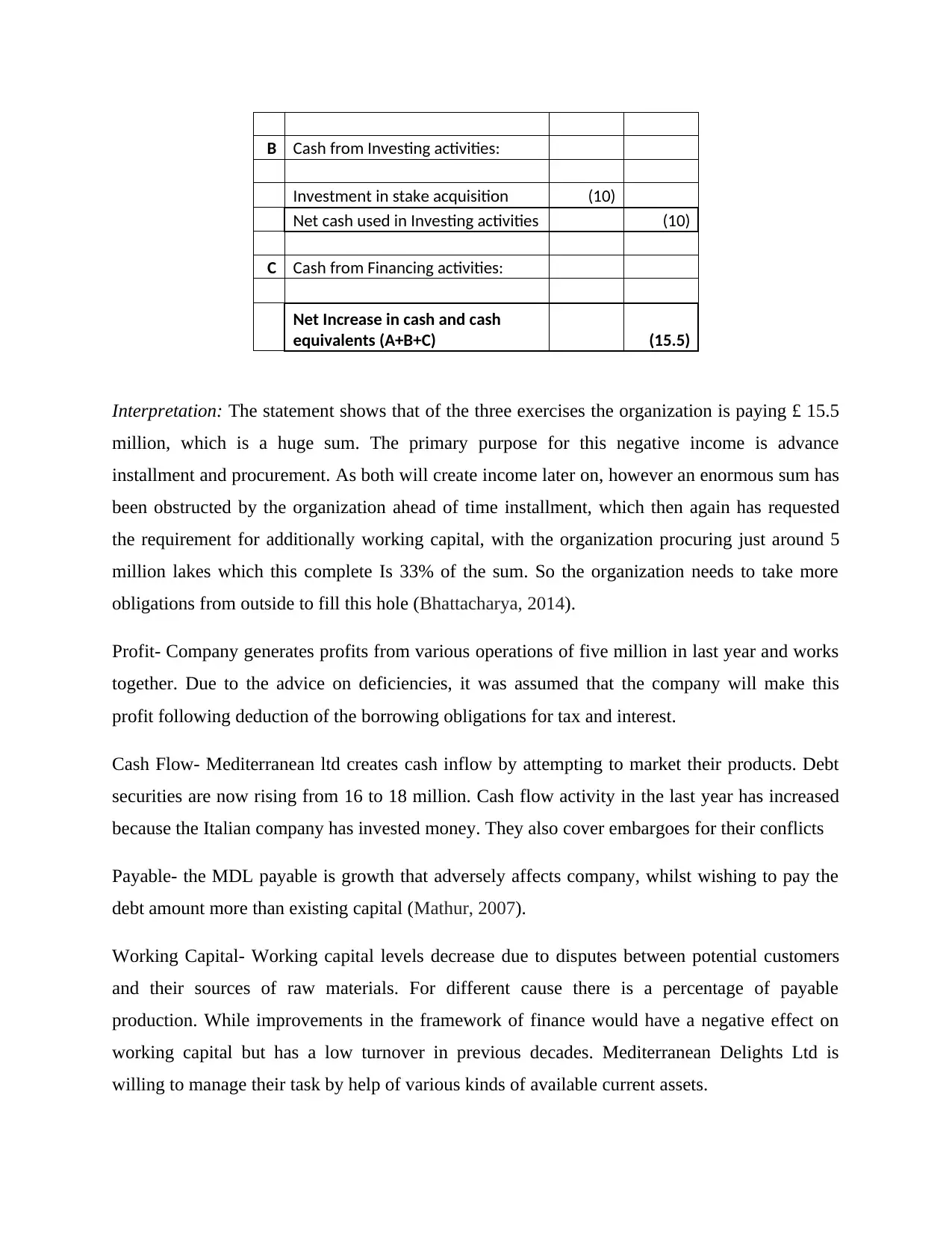

B Cash from Investing activities:

Investment in stake acquisition (10)

Net cash used in Investing activities (10)

C Cash from Financing activities:

Net Increase in cash and cash

equivalents (A+B+C) (15.5)

Interpretation: The statement shows that of the three exercises the organization is paying £ 15.5

million, which is a huge sum. The primary purpose for this negative income is advance

installment and procurement. As both will create income later on, however an enormous sum has

been obstructed by the organization ahead of time installment, which then again has requested

the requirement for additionally working capital, with the organization procuring just around 5

million lakes which this complete Is 33% of the sum. So the organization needs to take more

obligations from outside to fill this hole (Bhattacharya, 2014).

Profit- Company generates profits from various operations of five million in last year and works

together. Due to the advice on deficiencies, it was assumed that the company will make this

profit following deduction of the borrowing obligations for tax and interest.

Cash Flow- Mediterranean ltd creates cash inflow by attempting to market their products. Debt

securities are now rising from 16 to 18 million. Cash flow activity in the last year has increased

because the Italian company has invested money. They also cover embargoes for their conflicts

Payable- the MDL payable is growth that adversely affects company, whilst wishing to pay the

debt amount more than existing capital (Mathur, 2007).

Working Capital- Working capital levels decrease due to disputes between potential customers

and their sources of raw materials. For different cause there is a percentage of payable

production. While improvements in the framework of finance would have a negative effect on

working capital but has a low turnover in previous decades. Mediterranean Delights Ltd is

willing to manage their task by help of various kinds of available current assets.

Investment in stake acquisition (10)

Net cash used in Investing activities (10)

C Cash from Financing activities:

Net Increase in cash and cash

equivalents (A+B+C) (15.5)

Interpretation: The statement shows that of the three exercises the organization is paying £ 15.5

million, which is a huge sum. The primary purpose for this negative income is advance

installment and procurement. As both will create income later on, however an enormous sum has

been obstructed by the organization ahead of time installment, which then again has requested

the requirement for additionally working capital, with the organization procuring just around 5

million lakes which this complete Is 33% of the sum. So the organization needs to take more

obligations from outside to fill this hole (Bhattacharya, 2014).

Profit- Company generates profits from various operations of five million in last year and works

together. Due to the advice on deficiencies, it was assumed that the company will make this

profit following deduction of the borrowing obligations for tax and interest.

Cash Flow- Mediterranean ltd creates cash inflow by attempting to market their products. Debt

securities are now rising from 16 to 18 million. Cash flow activity in the last year has increased

because the Italian company has invested money. They also cover embargoes for their conflicts

Payable- the MDL payable is growth that adversely affects company, whilst wishing to pay the

debt amount more than existing capital (Mathur, 2007).

Working Capital- Working capital levels decrease due to disputes between potential customers

and their sources of raw materials. For different cause there is a percentage of payable

production. While improvements in the framework of finance would have a negative effect on

working capital but has a low turnover in previous decades. Mediterranean Delights Ltd is

willing to manage their task by help of various kinds of available current assets.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3. Analysis and recommendations

This is essential for business entities for manage their cash flows and in order to improve

cash flow of company, there are different kinds of course of action which are as follows:

Delay or postpone the investment program- Companies may spend large amounts of cash for

investment ventures, contributing to reduced cash flows. By preventing investments, companies

can increase cash flows. Such as above company can apply this to enhance their cash flows.

Identify and sell any unwanted assets-That is also a method of improving company cash flow.

The selling of certain properties that are not in service can be possible. This allows businesses to

earn higher cash, resulting in increased cash flow (Michalski, 2014).

Minimize the expenditure on legal fees and settle the litigation as soon as possible- It will be

easier for businesses, if companies cut legal fees, to get higher cash value in their accounts.

Resolve the on-going disputes and improve relationships-Despite ongoing controversies,

businesses continue to spend cash and thus face a problem of weak cash flow. If businesses settle

their conflicts, so investing cash in their accounts will be simpler.

PART 2

EXECUTIVE SUMMARY

Budget is a statistical statement where managers are expected to predict potential

financial gains from their small business through industry associations. It is used to develop

decision-making techniques. Additionally, the manager uses strategy regardless of the success

method. This research examines the basic dependence on decision-making funds and investigates

This is essential for business entities for manage their cash flows and in order to improve

cash flow of company, there are different kinds of course of action which are as follows:

Delay or postpone the investment program- Companies may spend large amounts of cash for

investment ventures, contributing to reduced cash flows. By preventing investments, companies

can increase cash flows. Such as above company can apply this to enhance their cash flows.

Identify and sell any unwanted assets-That is also a method of improving company cash flow.

The selling of certain properties that are not in service can be possible. This allows businesses to

earn higher cash, resulting in increased cash flow (Michalski, 2014).

Minimize the expenditure on legal fees and settle the litigation as soon as possible- It will be

easier for businesses, if companies cut legal fees, to get higher cash value in their accounts.

Resolve the on-going disputes and improve relationships-Despite ongoing controversies,

businesses continue to spend cash and thus face a problem of weak cash flow. If businesses settle

their conflicts, so investing cash in their accounts will be simpler.

PART 2

EXECUTIVE SUMMARY

Budget is a statistical statement where managers are expected to predict potential

financial gains from their small business through industry associations. It is used to develop

decision-making techniques. Additionally, the manager uses strategy regardless of the success

method. This research examines the basic dependence on decision-making funds and investigates

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

critically the effect on a company's performance of different communication strategies.

Conventional and new budgeting approaches for company administration systems are also

analyzed.

1. Purpose of preparing budget

A budget is a qualitative strategy established by the company with tax implications for a

specified period usually spanning 1 year. Often businesses plan their yearly budget with the

profit for each year. Herein, below purpose of budget is mentioned below in such manner:

Tool for decision-making- The key goal behind preparing funds is to expand own decision-

making mechanism to a financial system. They are the route steps that may or must not be

prepared by help of budgets. With the support of the funding advisor, the sales and costs of the

approved operations are estimated and company activities are handled depending on funding

(Wildavsky, 2017).

Forecast of Revenue & cost- Budgeting is a significant field of business strategy. Business and

different companies’ owners estimate benefit and loss whether a business is going to produce a

profit or not. The primary goal in marketing is to establish a strategic strategy to publicly

disclose the activity of the product. This helps to develop schedules, activities and schedules.

Monitoring of the efficiency of the organization and funding finance to monitor actual company

results to be quantified against activity forecasts. Then monitor the activities of businesses and

follow the financing to make projections that help vision plc to expand their SMEs.

So these are the purpose of budget for companies.

(a) Traditional budgeting approach

Traditional budgeting is only a way of preparing financing according to the budgets of

the previous year. When the traditional preparation method is used, the planning takes priority in

the last year. In other words, Traditional budgeting for a specific time period under evaluation is

the method used to plan the spending plan of the Firm, when the preparatory budget is regarded

as the basis for preparing that spending plan of the current year that is the budget of the current

financial year, by making any changes with last year's spending plan (Bouma, Jeucken and

Klinkers, 2017).

Conventional and new budgeting approaches for company administration systems are also

analyzed.

1. Purpose of preparing budget

A budget is a qualitative strategy established by the company with tax implications for a

specified period usually spanning 1 year. Often businesses plan their yearly budget with the

profit for each year. Herein, below purpose of budget is mentioned below in such manner:

Tool for decision-making- The key goal behind preparing funds is to expand own decision-

making mechanism to a financial system. They are the route steps that may or must not be

prepared by help of budgets. With the support of the funding advisor, the sales and costs of the

approved operations are estimated and company activities are handled depending on funding

(Wildavsky, 2017).

Forecast of Revenue & cost- Budgeting is a significant field of business strategy. Business and

different companies’ owners estimate benefit and loss whether a business is going to produce a

profit or not. The primary goal in marketing is to establish a strategic strategy to publicly

disclose the activity of the product. This helps to develop schedules, activities and schedules.

Monitoring of the efficiency of the organization and funding finance to monitor actual company

results to be quantified against activity forecasts. Then monitor the activities of businesses and

follow the financing to make projections that help vision plc to expand their SMEs.

So these are the purpose of budget for companies.

(a) Traditional budgeting approach

Traditional budgeting is only a way of preparing financing according to the budgets of

the previous year. When the traditional preparation method is used, the planning takes priority in

the last year. In other words, Traditional budgeting for a specific time period under evaluation is

the method used to plan the spending plan of the Firm, when the preparatory budget is regarded

as the basis for preparing that spending plan of the current year that is the budget of the current

financial year, by making any changes with last year's spending plan (Bouma, Jeucken and

Klinkers, 2017).

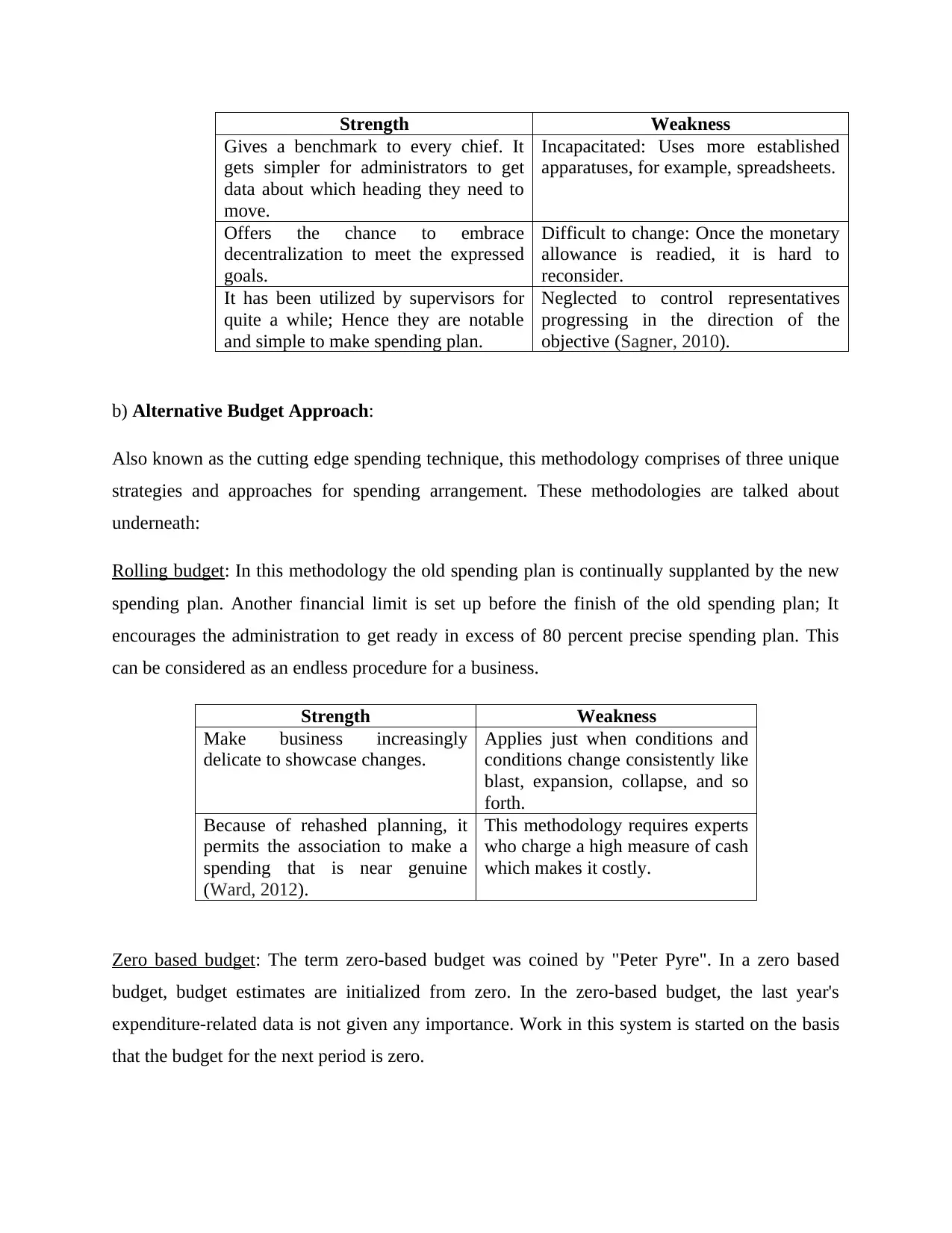

Strength Weakness

Gives a benchmark to every chief. It

gets simpler for administrators to get

data about which heading they need to

move.

Incapacitated: Uses more established

apparatuses, for example, spreadsheets.

Offers the chance to embrace

decentralization to meet the expressed

goals.

Difficult to change: Once the monetary

allowance is readied, it is hard to

reconsider.

It has been utilized by supervisors for

quite a while; Hence they are notable

and simple to make spending plan.

Neglected to control representatives

progressing in the direction of the

objective (Sagner, 2010).

b) Alternative Budget Approach:

Also known as the cutting edge spending technique, this methodology comprises of three unique

strategies and approaches for spending arrangement. These methodologies are talked about

underneath:

Rolling budget: In this methodology the old spending plan is continually supplanted by the new

spending plan. Another financial limit is set up before the finish of the old spending plan; It

encourages the administration to get ready in excess of 80 percent precise spending plan. This

can be considered as an endless procedure for a business.

Strength Weakness

Make business increasingly

delicate to showcase changes.

Applies just when conditions and

conditions change consistently like

blast, expansion, collapse, and so

forth.

Because of rehashed planning, it

permits the association to make a

spending that is near genuine

(Ward, 2012).

This methodology requires experts

who charge a high measure of cash

which makes it costly.

Zero based budget: The term zero-based budget was coined by "Peter Pyre". In a zero based

budget, budget estimates are initialized from zero. In the zero-based budget, the last year's

expenditure-related data is not given any importance. Work in this system is started on the basis

that the budget for the next period is zero.

Gives a benchmark to every chief. It

gets simpler for administrators to get

data about which heading they need to

move.

Incapacitated: Uses more established

apparatuses, for example, spreadsheets.

Offers the chance to embrace

decentralization to meet the expressed

goals.

Difficult to change: Once the monetary

allowance is readied, it is hard to

reconsider.

It has been utilized by supervisors for

quite a while; Hence they are notable

and simple to make spending plan.

Neglected to control representatives

progressing in the direction of the

objective (Sagner, 2010).

b) Alternative Budget Approach:

Also known as the cutting edge spending technique, this methodology comprises of three unique

strategies and approaches for spending arrangement. These methodologies are talked about

underneath:

Rolling budget: In this methodology the old spending plan is continually supplanted by the new

spending plan. Another financial limit is set up before the finish of the old spending plan; It

encourages the administration to get ready in excess of 80 percent precise spending plan. This

can be considered as an endless procedure for a business.

Strength Weakness

Make business increasingly

delicate to showcase changes.

Applies just when conditions and

conditions change consistently like

blast, expansion, collapse, and so

forth.

Because of rehashed planning, it

permits the association to make a

spending that is near genuine

(Ward, 2012).

This methodology requires experts

who charge a high measure of cash

which makes it costly.

Zero based budget: The term zero-based budget was coined by "Peter Pyre". In a zero based

budget, budget estimates are initialized from zero. In the zero-based budget, the last year's

expenditure-related data is not given any importance. Work in this system is started on the basis

that the budget for the next period is zero.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It is the responsibility of every manager to explain why it is necessary to spend money in a

project or plan and what kind of loss will happen if this project or plan is not started. That is, no

new money is released until the work or project is justified. That is, there is a provision in this

process that every manager has been given the burden of giving proof that he should explain why

he should spend the money (Scapens, 1991).

Activity based budget: An activity-based budget - ABB 'activity-based budgeting is a method of

budgeting in which the costs of costs are recorded in each functional area of an organization and

their relationships are defined and analyzed. Activity-based budgeting of inflation or business

development Instead, activity-based budgeting is efficient in business operations based on these

tasks. Seek work and development budget (Scapens, 1991).

The activity-based budgeting process can be simplified into a three-step process first, relevant

activities are identified. These cost drivers are the items responsible for revenue or expenditure.

Second, the number of units related to each activity is determined as the baseline for calculation.

Finally, the cost of the activity is determined per unit and multiplied against the activity level.

2. Application of traditional and alternative budgeting approach for planning

cost of second sight plc

As both approaches have their advantages and limitations for the company. Application of

various methods:

I. Traditional approach: The organization needs to take a base year for the present year's financial

limit. Followed to £ 250 million income a year ago, it intends to open a branch where 800

representatives will work. Work is less expensive in India, so at any rate 500 representatives

should build its expense for the worker by 25% from the past one. As indicated by this view the

organization should expand its income by 20%.

II. Rolling Budget: The organization needs to make a financial limit for the following a half year

before the finish of this present month. The company's present obligation is around £ 50 million

and the promoted share is £ 300 million.

III. Zero Based Budget: Second Sigh Plc prepared for joint endeavor in India which is another

and diverse area for the organization. It can begin all expenses at level zero. First it needs to

project or plan and what kind of loss will happen if this project or plan is not started. That is, no

new money is released until the work or project is justified. That is, there is a provision in this

process that every manager has been given the burden of giving proof that he should explain why

he should spend the money (Scapens, 1991).

Activity based budget: An activity-based budget - ABB 'activity-based budgeting is a method of

budgeting in which the costs of costs are recorded in each functional area of an organization and

their relationships are defined and analyzed. Activity-based budgeting of inflation or business

development Instead, activity-based budgeting is efficient in business operations based on these

tasks. Seek work and development budget (Scapens, 1991).

The activity-based budgeting process can be simplified into a three-step process first, relevant

activities are identified. These cost drivers are the items responsible for revenue or expenditure.

Second, the number of units related to each activity is determined as the baseline for calculation.

Finally, the cost of the activity is determined per unit and multiplied against the activity level.

2. Application of traditional and alternative budgeting approach for planning

cost of second sight plc

As both approaches have their advantages and limitations for the company. Application of

various methods:

I. Traditional approach: The organization needs to take a base year for the present year's financial

limit. Followed to £ 250 million income a year ago, it intends to open a branch where 800

representatives will work. Work is less expensive in India, so at any rate 500 representatives

should build its expense for the worker by 25% from the past one. As indicated by this view the

organization should expand its income by 20%.

II. Rolling Budget: The organization needs to make a financial limit for the following a half year

before the finish of this present month. The company's present obligation is around £ 50 million

and the promoted share is £ 300 million.

III. Zero Based Budget: Second Sigh Plc prepared for joint endeavor in India which is another

and diverse area for the organization. It can begin all expenses at level zero. First it needs to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

comprehend the conditions like work rate, accessibility of assets in India; Whether it needs to

import assets or is accessible in the host nation (Porter and Norton, 2012).

IV. Activity Based Budget: The organization's primary business is eyeglasses and shades that

supply it to different organizations. In this manner it should concentrate more on tasks and

transportation, lessening different expenses and overhead.

3. Analysis of best approach

In light of the investigates led above, it is unequivocally suggested that the organization ought to

receive a zero-based spending approach as Second Sigh plc is going to begin another business in

another condition where the expense is totally not quite the same as beginning it without any

preparation need to.

Why not the customary methodology?

In any case, the customary methodology is appropriate just for the development of business,

however just in the present conditions and market. It has no key job for the new market. In this

manner it may not have any significant bearing in another joint endeavor venture with an Indian

organization (Bendell and Doyle2017).

Why not roll and action based spending plan?

Rolling spending plan is additionally appropriate for existing business, it can assist the

organization with avoiding surprising circumstances, yet it cannot support the business, when it

intends to open in new conditions (Haeger, 2017).

While movement based planning is just useful when action based costing is known.

However, in this present circumstance where everything begins without any preparation,

it isn't useful (Drury, 2013).

import assets or is accessible in the host nation (Porter and Norton, 2012).

IV. Activity Based Budget: The organization's primary business is eyeglasses and shades that

supply it to different organizations. In this manner it should concentrate more on tasks and

transportation, lessening different expenses and overhead.

3. Analysis of best approach

In light of the investigates led above, it is unequivocally suggested that the organization ought to

receive a zero-based spending approach as Second Sigh plc is going to begin another business in

another condition where the expense is totally not quite the same as beginning it without any

preparation need to.

Why not the customary methodology?

In any case, the customary methodology is appropriate just for the development of business,

however just in the present conditions and market. It has no key job for the new market. In this

manner it may not have any significant bearing in another joint endeavor venture with an Indian

organization (Bendell and Doyle2017).

Why not roll and action based spending plan?

Rolling spending plan is additionally appropriate for existing business, it can assist the

organization with avoiding surprising circumstances, yet it cannot support the business, when it

intends to open in new conditions (Haeger, 2017).

While movement based planning is just useful when action based costing is known.

However, in this present circumstance where everything begins without any preparation,

it isn't useful (Drury, 2013).

CONCLUSION

Hence, on the bases of above analyses, it can be concluded that; Budget is the account of

estimated revenue and expenditure of any government. The most important element of public

administration is the financial system. Money is required for all the work done by the

government. Where will this money come from and where will this money be spent. All these

things should be well thought out and well organized. This system is known as budget.

Hence, on the bases of above analyses, it can be concluded that; Budget is the account of

estimated revenue and expenditure of any government. The most important element of public

administration is the financial system. Money is required for all the work done by the

government. Where will this money come from and where will this money be spent. All these

things should be well thought out and well organized. This system is known as budget.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.