Financial Ratio Analysis and Asset Valuation: Harvey Norman Report

VerifiedAdded on 2023/01/17

|9

|1986

|50

Report

AI Summary

This report provides a comprehensive financial analysis of Harvey Norman Holdings Limited. It begins with an overview of the company and the industry in which it operates, detailing its business model and market position within the computer, electronics, furniture, and bedding goods sector. The core of the report focuses on evaluating Harvey Norman's financial performance through ratio analysis, calculating and interpreting key ratios such as the current ratio, debt ratio, and interest earned ratio over a five-year period (2015-2019) to assess its liquidity, solvency, and profitability. The analysis includes graphical representations of the ratios to illustrate trends and identify areas of strength and weakness. Furthermore, the report includes a valuation of Harvey Norman's assets, examining the methods used for revaluation of property, plant, and equipment, as well as the treatment of intangible assets. The report concludes with a summary of the findings and insights into the company's financial health and performance.

REPORT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

EXECUTIVE SUMMARY.............................................................................................................3

MAIN BODY...................................................................................................................................3

1. About the company and the industry in which this operates..................................................3

2. Evaluation of financial performance of above company on the basis of ratio analysis..........3

3. Valuation of above company's assets. ....................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

EXECUTIVE SUMMARY.............................................................................................................3

MAIN BODY...................................................................................................................................3

1. About the company and the industry in which this operates..................................................3

2. Evaluation of financial performance of above company on the basis of ratio analysis..........3

3. Valuation of above company's assets. ....................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

EXECUTIVE SUMMARY

The project report summarise about the analysis of financial performance of Harvey

Norman Holdings limited. Under the report, different types of ratios are calculated and

interpreted in order to assess efficiency of above company. The ratios which are computed are

current ratio, debt and interest earned ratio. In the end part of report, valuation of financial assets

of above company is done in an effective manner.

MAIN BODY

1. About the company and the industry in which this operates.

Overview of company – The Harvey Norman Holdings limited is a holding company for other

entities and operates in a 3rd party agreement. Basically, the it is based on international business

of furniture, bedding and many electronic products. This company has its headquarter in New

south Wales, Australia. It was founded by Gerry Harvey and Ian Norman in year 1982. As

accordance of financial year 2016, their net income was of $349 million and overall revenue was

of $5.3 billion in Australia (About over view of company, 2019.). This indicates that company is

performing very well in the context of generating revenues.

Industry in which the company operates – The company operates in the industry of computer,

electronic, furniture and bedding goods. They have large number of product portfolio in order to

provide needed products by their customers. There are about 194 Australian franchised

companies and 86 overseas companies.

2. Evaluation of financial performance of above company on the basis of ratio analysis.

Ratio analysis- It can be defined as type of technique that is used for making proper financial

analysis of companies. Under this method, vital range of ratios are calculated and interpreted. In

the context of above Harvey Norman Holdings limited company below mentioned ratios are

interpreted for assessing their overall performance :

Current ratio = It is a type of ratio which is calculated in order to assess the liquidity

position of companies (Dehnavi, Aghdam, Pradhan & Varzandeh, 2015). This ratio

shows the relation between current assets and current liabilities. The ideal ratio is of 2:1.

Herein, below formula of computing current ratio is mentioned in such manner:

The project report summarise about the analysis of financial performance of Harvey

Norman Holdings limited. Under the report, different types of ratios are calculated and

interpreted in order to assess efficiency of above company. The ratios which are computed are

current ratio, debt and interest earned ratio. In the end part of report, valuation of financial assets

of above company is done in an effective manner.

MAIN BODY

1. About the company and the industry in which this operates.

Overview of company – The Harvey Norman Holdings limited is a holding company for other

entities and operates in a 3rd party agreement. Basically, the it is based on international business

of furniture, bedding and many electronic products. This company has its headquarter in New

south Wales, Australia. It was founded by Gerry Harvey and Ian Norman in year 1982. As

accordance of financial year 2016, their net income was of $349 million and overall revenue was

of $5.3 billion in Australia (About over view of company, 2019.). This indicates that company is

performing very well in the context of generating revenues.

Industry in which the company operates – The company operates in the industry of computer,

electronic, furniture and bedding goods. They have large number of product portfolio in order to

provide needed products by their customers. There are about 194 Australian franchised

companies and 86 overseas companies.

2. Evaluation of financial performance of above company on the basis of ratio analysis.

Ratio analysis- It can be defined as type of technique that is used for making proper financial

analysis of companies. Under this method, vital range of ratios are calculated and interpreted. In

the context of above Harvey Norman Holdings limited company below mentioned ratios are

interpreted for assessing their overall performance :

Current ratio = It is a type of ratio which is calculated in order to assess the liquidity

position of companies (Dehnavi, Aghdam, Pradhan & Varzandeh, 2015). This ratio

shows the relation between current assets and current liabilities. The ideal ratio is of 2:1.

Herein, below formula of computing current ratio is mentioned in such manner:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

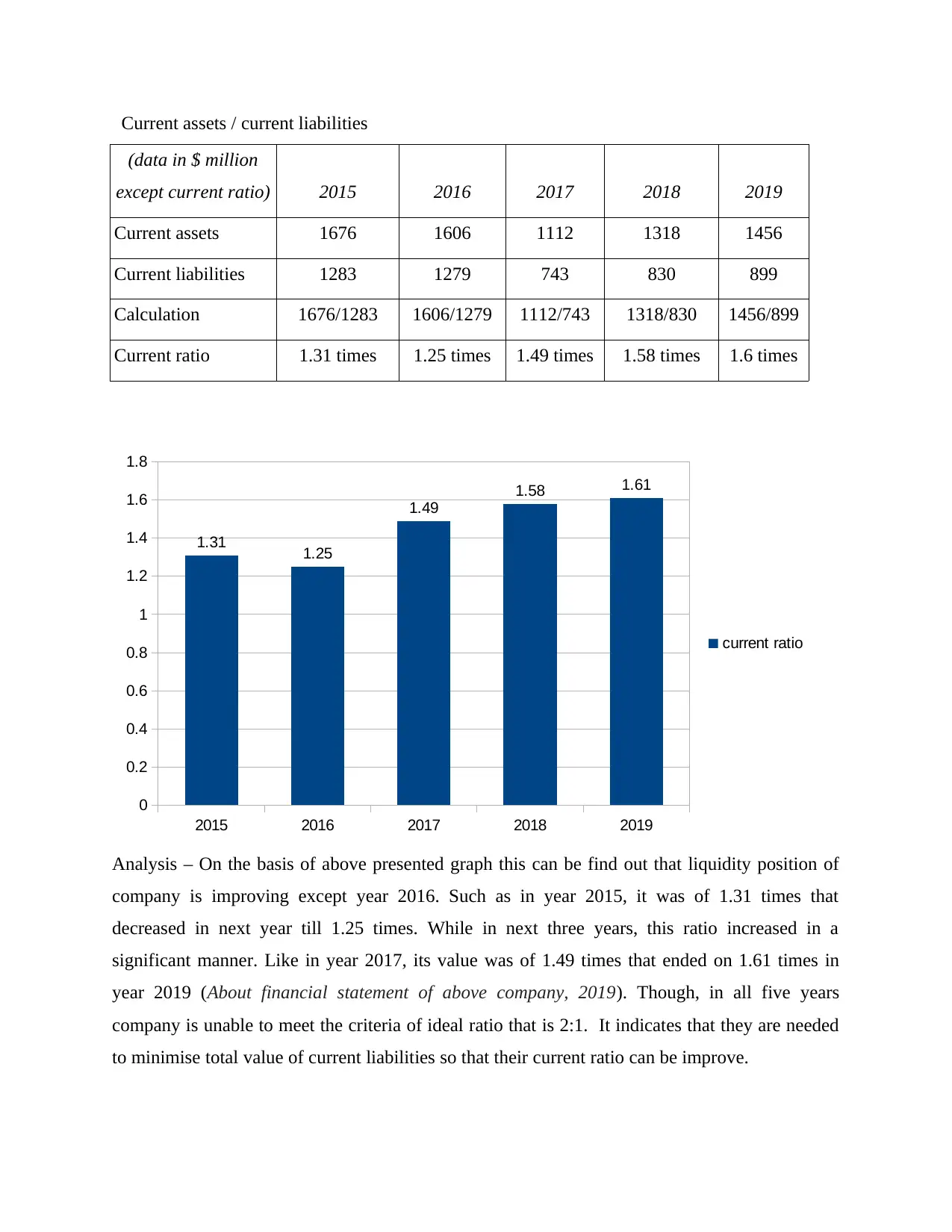

Current assets / current liabilities

(data in $ million

except current ratio) 2015 2016 2017 2018 2019

Current assets 1676 1606 1112 1318 1456

Current liabilities 1283 1279 743 830 899

Calculation 1676/1283 1606/1279 1112/743 1318/830 1456/899

Current ratio 1.31 times 1.25 times 1.49 times 1.58 times 1.6 times

2015 2016 2017 2018 2019

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

1.31 1.25

1.49

1.58 1.61

current ratio

Analysis – On the basis of above presented graph this can be find out that liquidity position of

company is improving except year 2016. Such as in year 2015, it was of 1.31 times that

decreased in next year till 1.25 times. While in next three years, this ratio increased in a

significant manner. Like in year 2017, its value was of 1.49 times that ended on 1.61 times in

year 2019 (About financial statement of above company, 2019). Though, in all five years

company is unable to meet the criteria of ideal ratio that is 2:1. It indicates that they are needed

to minimise total value of current liabilities so that their current ratio can be improve.

(data in $ million

except current ratio) 2015 2016 2017 2018 2019

Current assets 1676 1606 1112 1318 1456

Current liabilities 1283 1279 743 830 899

Calculation 1676/1283 1606/1279 1112/743 1318/830 1456/899

Current ratio 1.31 times 1.25 times 1.49 times 1.58 times 1.6 times

2015 2016 2017 2018 2019

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

1.31 1.25

1.49

1.58 1.61

current ratio

Analysis – On the basis of above presented graph this can be find out that liquidity position of

company is improving except year 2016. Such as in year 2015, it was of 1.31 times that

decreased in next year till 1.25 times. While in next three years, this ratio increased in a

significant manner. Like in year 2017, its value was of 1.49 times that ended on 1.61 times in

year 2019 (About financial statement of above company, 2019). Though, in all five years

company is unable to meet the criteria of ideal ratio that is 2:1. It indicates that they are needed

to minimise total value of current liabilities so that their current ratio can be improve.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

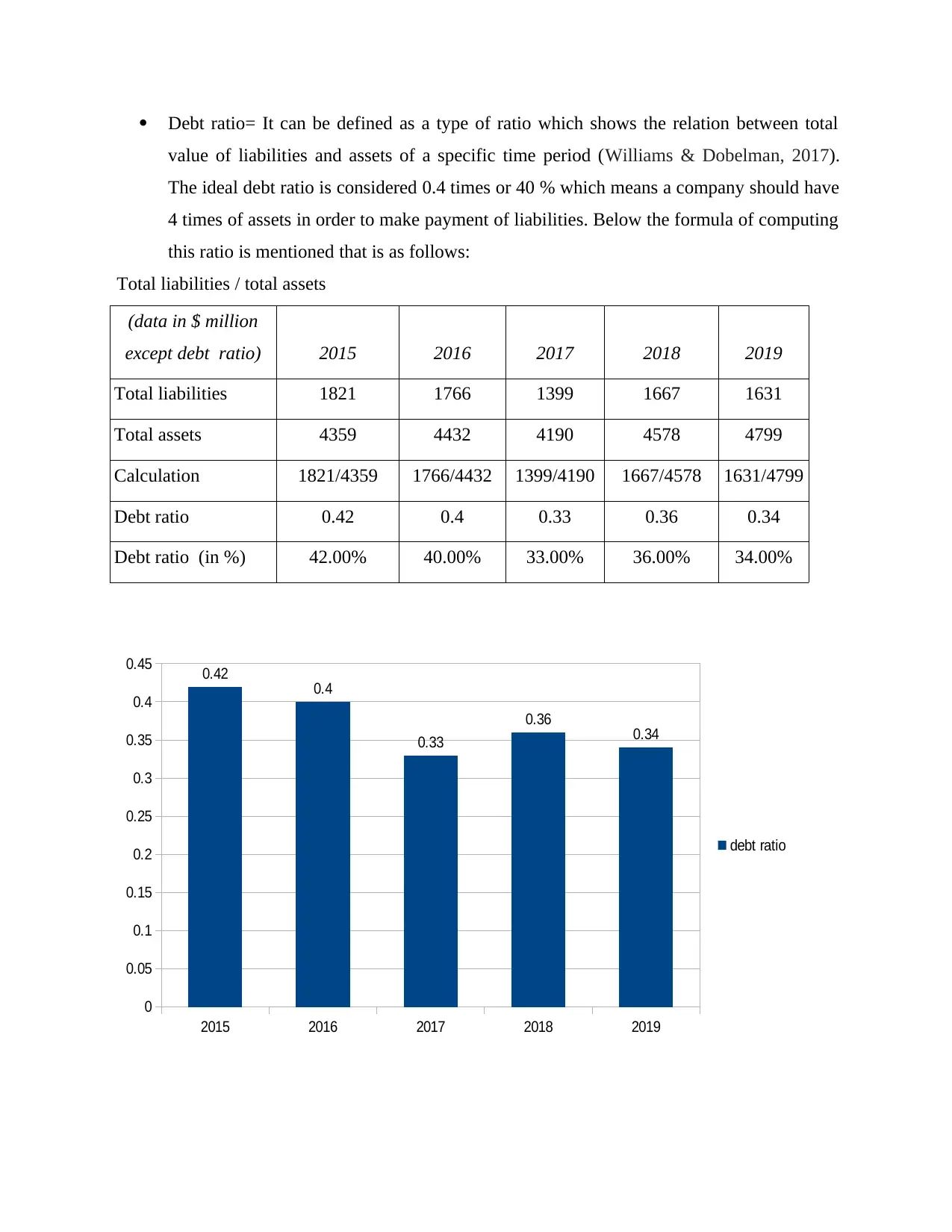

Debt ratio= It can be defined as a type of ratio which shows the relation between total

value of liabilities and assets of a specific time period (Williams & Dobelman, 2017).

The ideal debt ratio is considered 0.4 times or 40 % which means a company should have

4 times of assets in order to make payment of liabilities. Below the formula of computing

this ratio is mentioned that is as follows:

Total liabilities / total assets

(data in $ million

except debt ratio) 2015 2016 2017 2018 2019

Total liabilities 1821 1766 1399 1667 1631

Total assets 4359 4432 4190 4578 4799

Calculation 1821/4359 1766/4432 1399/4190 1667/4578 1631/4799

Debt ratio 0.42 0.4 0.33 0.36 0.34

Debt ratio (in %) 42.00% 40.00% 33.00% 36.00% 34.00%

2015 2016 2017 2018 2019

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

0.45 0.42 0.4

0.33

0.36 0.34

debt ratio

value of liabilities and assets of a specific time period (Williams & Dobelman, 2017).

The ideal debt ratio is considered 0.4 times or 40 % which means a company should have

4 times of assets in order to make payment of liabilities. Below the formula of computing

this ratio is mentioned that is as follows:

Total liabilities / total assets

(data in $ million

except debt ratio) 2015 2016 2017 2018 2019

Total liabilities 1821 1766 1399 1667 1631

Total assets 4359 4432 4190 4578 4799

Calculation 1821/4359 1766/4432 1399/4190 1667/4578 1631/4799

Debt ratio 0.42 0.4 0.33 0.36 0.34

Debt ratio (in %) 42.00% 40.00% 33.00% 36.00% 34.00%

2015 2016 2017 2018 2019

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

0.45 0.42 0.4

0.33

0.36 0.34

debt ratio

Analysis – On the basis of above presented graph, this can be find out that performance of above

in the aspect of debt ratio is excellent except year 2015. If the debt ratio is 40% or lower then

40% then this is considered a better condition for companies. In the aspect of above Harvey

Norman Holdings limited company, it can be find out that their debt ratio was of 40%, 33%, 36%

and 34% for year 2016, 2017, 2018 and 2019 respectively. Though, in the starting year 2015 it

was more then 40% but in upcoming years company performed well.

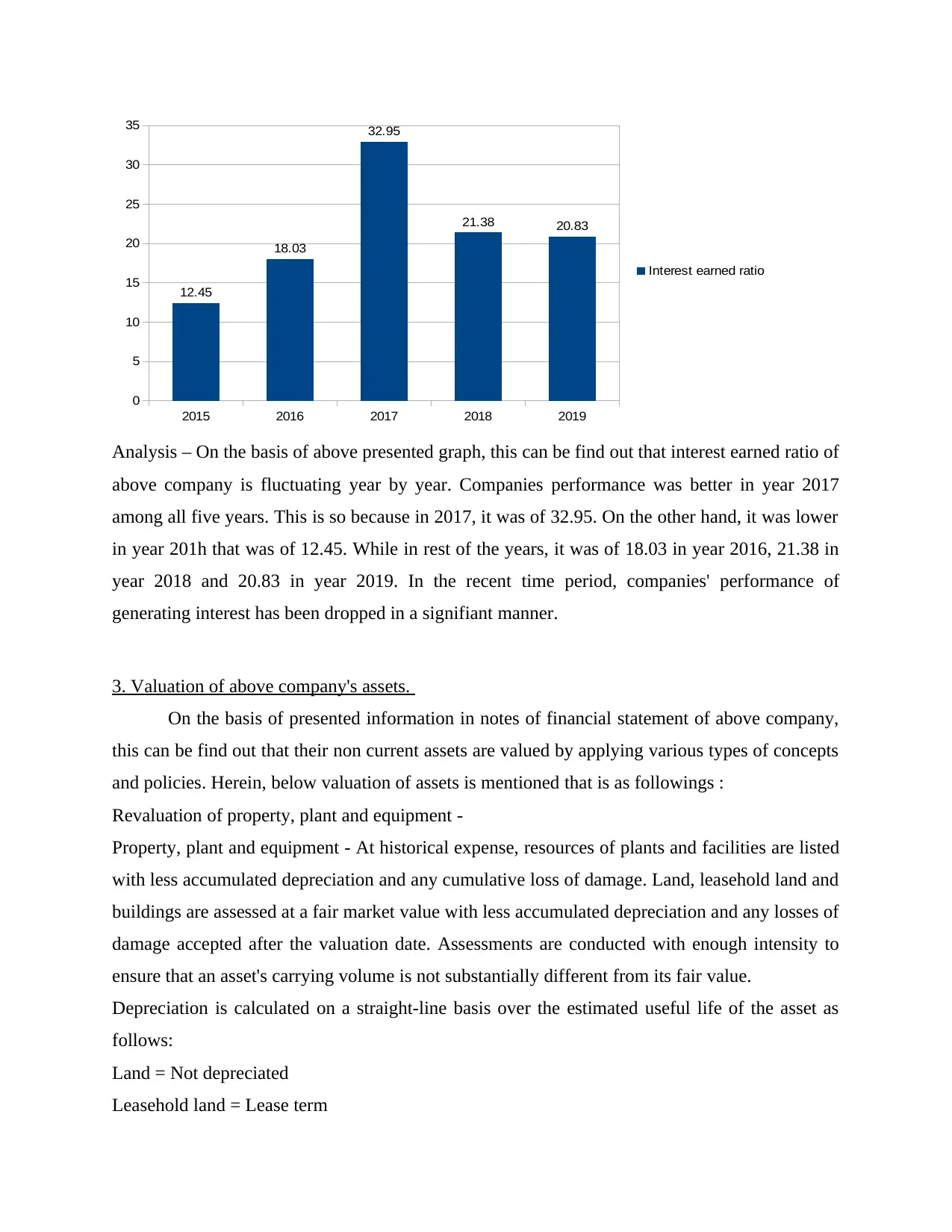

Interest earned ratio = This is a type of ratio which assess company's efficiency in the

context of honouring of debt payments (Burt, 2013). Its formula is mentioned below such

as:

Income before interest and tax / interest expenses

(data in $ million

except interest

earned ratio ratio) 2015 2016 2017 2018 2019

Income before

interest and tax 411 523 659 556 604

Interest expenses 33 29 20 26 29

Calculation 411/33 523/29 659/20 556/26 604/29

Interest earned ratio 12.45 18.03 32.95 21.38 20.83

in the aspect of debt ratio is excellent except year 2015. If the debt ratio is 40% or lower then

40% then this is considered a better condition for companies. In the aspect of above Harvey

Norman Holdings limited company, it can be find out that their debt ratio was of 40%, 33%, 36%

and 34% for year 2016, 2017, 2018 and 2019 respectively. Though, in the starting year 2015 it

was more then 40% but in upcoming years company performed well.

Interest earned ratio = This is a type of ratio which assess company's efficiency in the

context of honouring of debt payments (Burt, 2013). Its formula is mentioned below such

as:

Income before interest and tax / interest expenses

(data in $ million

except interest

earned ratio ratio) 2015 2016 2017 2018 2019

Income before

interest and tax 411 523 659 556 604

Interest expenses 33 29 20 26 29

Calculation 411/33 523/29 659/20 556/26 604/29

Interest earned ratio 12.45 18.03 32.95 21.38 20.83

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2015 2016 2017 2018 2019

0

5

10

15

20

25

30

35

12.45

18.03

32.95

21.38 20.83

Interest earned ratio

Analysis – On the basis of above presented graph, this can be find out that interest earned ratio of

above company is fluctuating year by year. Companies performance was better in year 2017

among all five years. This is so because in 2017, it was of 32.95. On the other hand, it was lower

in year 201h that was of 12.45. While in rest of the years, it was of 18.03 in year 2016, 21.38 in

year 2018 and 20.83 in year 2019. In the recent time period, companies' performance of

generating interest has been dropped in a signifiant manner.

3. Valuation of above company's assets.

On the basis of presented information in notes of financial statement of above company,

this can be find out that their non current assets are valued by applying various types of concepts

and policies. Herein, below valuation of assets is mentioned that is as followings :

Revaluation of property, plant and equipment -

Property, plant and equipment - At historical expense, resources of plants and facilities are listed

with less accumulated depreciation and any cumulative loss of damage. Land, leasehold land and

buildings are assessed at a fair market value with less accumulated depreciation and any losses of

damage accepted after the valuation date. Assessments are conducted with enough intensity to

ensure that an asset's carrying volume is not substantially different from its fair value.

Depreciation is calculated on a straight-line basis over the estimated useful life of the asset as

follows:

Land = Not depreciated

Leasehold land = Lease term

0

5

10

15

20

25

30

35

12.45

18.03

32.95

21.38 20.83

Interest earned ratio

Analysis – On the basis of above presented graph, this can be find out that interest earned ratio of

above company is fluctuating year by year. Companies performance was better in year 2017

among all five years. This is so because in 2017, it was of 32.95. On the other hand, it was lower

in year 201h that was of 12.45. While in rest of the years, it was of 18.03 in year 2016, 21.38 in

year 2018 and 20.83 in year 2019. In the recent time period, companies' performance of

generating interest has been dropped in a signifiant manner.

3. Valuation of above company's assets.

On the basis of presented information in notes of financial statement of above company,

this can be find out that their non current assets are valued by applying various types of concepts

and policies. Herein, below valuation of assets is mentioned that is as followings :

Revaluation of property, plant and equipment -

Property, plant and equipment - At historical expense, resources of plants and facilities are listed

with less accumulated depreciation and any cumulative loss of damage. Land, leasehold land and

buildings are assessed at a fair market value with less accumulated depreciation and any losses of

damage accepted after the valuation date. Assessments are conducted with enough intensity to

ensure that an asset's carrying volume is not substantially different from its fair value.

Depreciation is calculated on a straight-line basis over the estimated useful life of the asset as

follows:

Land = Not depreciated

Leasehold land = Lease term

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Buildings under construction = No depreciation is computed

Buildings = 20 years to 40 years

Owned plant and equipments = 3 years to 20 years

Plant and equipment under finance lease = 1 year to 5 years

The residual values of the assets, helpful lives and practices of amortization are evaluated and

adapted at the end of each fiscal year, if necessary.

Intangible assets - Intangible assets are evaluated for deficiency where there is a cognitive

function measure, either separately or at the level of the unit producing cash (Vaze, 2013).

Useful lives are also checked periodically and changes are made on a prospect basis, where

appropriate. Gains or losses resulting from the de-cognition of an intangible asset are calculated

as the difference between the net sale revenues and the carrying value of the intangible asset and

are recorded in the statement of profits when the intangible asset is recognised.

Construction investment on an individual project is regarded as an intangible asset. When the

combined company will demonstrate:

The practical viability of finishing the intangible asset so that it can be used or sold.

Their intention to achieve and their ability to use or sell the asset

The asset is held at value less any accumulated amortization and cumulative depreciation losses

following initial identification of the construction expenditure as an investment (April Márquez‐

Grant & Richards,2012). Once production is complete, the amortization of the resource begins

and the asset is ready for use. During the expected future gain period, it is amortized. The asset

will be checked periodically for damage during the development period.

CONCLUSION

On the basis of above project report, it has been concluded financial analysis is essential

for companies in order to become aware about actual position. The report concludes about

overview of Harvey Norman Holdings limited company and its monetary performance. In the

terms of analysed different ratios, it can be concluded that their overall performance is better. As

well as further part of report concludes regards to valuation of non current assets of chosen

company.

Buildings = 20 years to 40 years

Owned plant and equipments = 3 years to 20 years

Plant and equipment under finance lease = 1 year to 5 years

The residual values of the assets, helpful lives and practices of amortization are evaluated and

adapted at the end of each fiscal year, if necessary.

Intangible assets - Intangible assets are evaluated for deficiency where there is a cognitive

function measure, either separately or at the level of the unit producing cash (Vaze, 2013).

Useful lives are also checked periodically and changes are made on a prospect basis, where

appropriate. Gains or losses resulting from the de-cognition of an intangible asset are calculated

as the difference between the net sale revenues and the carrying value of the intangible asset and

are recorded in the statement of profits when the intangible asset is recognised.

Construction investment on an individual project is regarded as an intangible asset. When the

combined company will demonstrate:

The practical viability of finishing the intangible asset so that it can be used or sold.

Their intention to achieve and their ability to use or sell the asset

The asset is held at value less any accumulated amortization and cumulative depreciation losses

following initial identification of the construction expenditure as an investment (April Márquez‐

Grant & Richards,2012). Once production is complete, the amortization of the resource begins

and the asset is ready for use. During the expected future gain period, it is amortized. The asset

will be checked periodically for damage during the development period.

CONCLUSION

On the basis of above project report, it has been concluded financial analysis is essential

for companies in order to become aware about actual position. The report concludes about

overview of Harvey Norman Holdings limited company and its monetary performance. In the

terms of analysed different ratios, it can be concluded that their overall performance is better. As

well as further part of report concludes regards to valuation of non current assets of chosen

company.

REFERENCES

Books and journals:

Dehnavi, A., Aghdam, I. N., Pradhan, B., & Varzandeh, M. H. M. (2015). A new hybrid model

using step-wise weight assessment ratio analysis (SWARA) technique and adaptive

neuro-fuzzy inference system (ANFIS) for regional landslide hazard assessment in

Iran. Catena. 135. 122-148.

Williams, E. E., & Dobelman, J. A. (2017). Financial statement analysis. World Scientific Book

Chapters. 109-169.

Burt, N. M. (2013). Stable isotope ratio analysis of breastfeeding and weaning practices of

children from medieval Fishergate House York, UK. American Journal of Physical

Anthropology. 152(3). 407-416.

Vaze, R. (2013, April). Competitive ratio analysis of online algorithms to minimize packet

transmission time in energy harvesting communication system. In 2013 Proceedings

IEEE INFOCOM. (pp. 115-1123). IEEE.

Nehlich, O., Fuller, B. T., Márquez‐Grant, N., & Richards, M. P. (2012). Investigation of

diachronic dietary patterns on the islands of Ibiza and Formentera, Spain: evidence from

sulfur stable isotope ratio analysis. American Journal of Physical Anthropology. 149(1).

115-124.

Online:

About financial statement of above company, 2019. [online] available

through:<http://financials.morningstar.com/balance-sheet/bs.html?

t=HVN®ion=aus&culture=en-US>

About over view of company, 2019. [online] available

through:<http://www.harveynormanholdings.com.au/company>

Books and journals:

Dehnavi, A., Aghdam, I. N., Pradhan, B., & Varzandeh, M. H. M. (2015). A new hybrid model

using step-wise weight assessment ratio analysis (SWARA) technique and adaptive

neuro-fuzzy inference system (ANFIS) for regional landslide hazard assessment in

Iran. Catena. 135. 122-148.

Williams, E. E., & Dobelman, J. A. (2017). Financial statement analysis. World Scientific Book

Chapters. 109-169.

Burt, N. M. (2013). Stable isotope ratio analysis of breastfeeding and weaning practices of

children from medieval Fishergate House York, UK. American Journal of Physical

Anthropology. 152(3). 407-416.

Vaze, R. (2013, April). Competitive ratio analysis of online algorithms to minimize packet

transmission time in energy harvesting communication system. In 2013 Proceedings

IEEE INFOCOM. (pp. 115-1123). IEEE.

Nehlich, O., Fuller, B. T., Márquez‐Grant, N., & Richards, M. P. (2012). Investigation of

diachronic dietary patterns on the islands of Ibiza and Formentera, Spain: evidence from

sulfur stable isotope ratio analysis. American Journal of Physical Anthropology. 149(1).

115-124.

Online:

About financial statement of above company, 2019. [online] available

through:<http://financials.morningstar.com/balance-sheet/bs.html?

t=HVN®ion=aus&culture=en-US>

About over view of company, 2019. [online] available

through:<http://www.harveynormanholdings.com.au/company>

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.