C31RM-Regression Analysis and Weak Form Efficiency Tests.

VerifiedAdded on 2023/04/07

|19

|3577

|114

Report

AI Summary

This report conducts regression analysis using Ordinary Least Squares (OLS) to examine the relationship between CEO compensation and various factors like return on assets, firm size, CEO tenure, and demographic variables. It further performs tests for weak form efficiency, analyzing stock price data to determine if historical prices can predict future movements. The analysis includes descriptive statistics, correlation matrices, and regression outputs, with a discussion of the findings in relation to existing literature. The report concludes with an assessment of the model's limitations and suggestions for future research.

Running head: Research Methods

Research Methods

Name of the Student

Course Id:

Course Name:

Research Methods

Name of the Student

Course Id:

Course Name:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

Research Methods

Table of Contents

Introduction................................................................................................................................2

Part I: Regression analysis.........................................................................................................2

Regression analysis....................................................................................................................2

Step 3: Empirical Discussions....................................................................................................4

1) Report resulting......................................................................................................................4

2) Description of the results.......................................................................................................6

3. Discussion of findings relating with relevant literature.......................................................11

4. Optional Opportunity for Individual Initiative.....................................................................11

Part II: Tests for Weak Form Efficiency..................................................................................12

Step 2: Tests of Weak Form Efficiency...................................................................................13

Reference list............................................................................................................................16

Research Methods

Table of Contents

Introduction................................................................................................................................2

Part I: Regression analysis.........................................................................................................2

Regression analysis....................................................................................................................2

Step 3: Empirical Discussions....................................................................................................4

1) Report resulting......................................................................................................................4

2) Description of the results.......................................................................................................6

3. Discussion of findings relating with relevant literature.......................................................11

4. Optional Opportunity for Individual Initiative.....................................................................11

Part II: Tests for Weak Form Efficiency..................................................................................12

Step 2: Tests of Weak Form Efficiency...................................................................................13

Reference list............................................................................................................................16

2

Research Methods

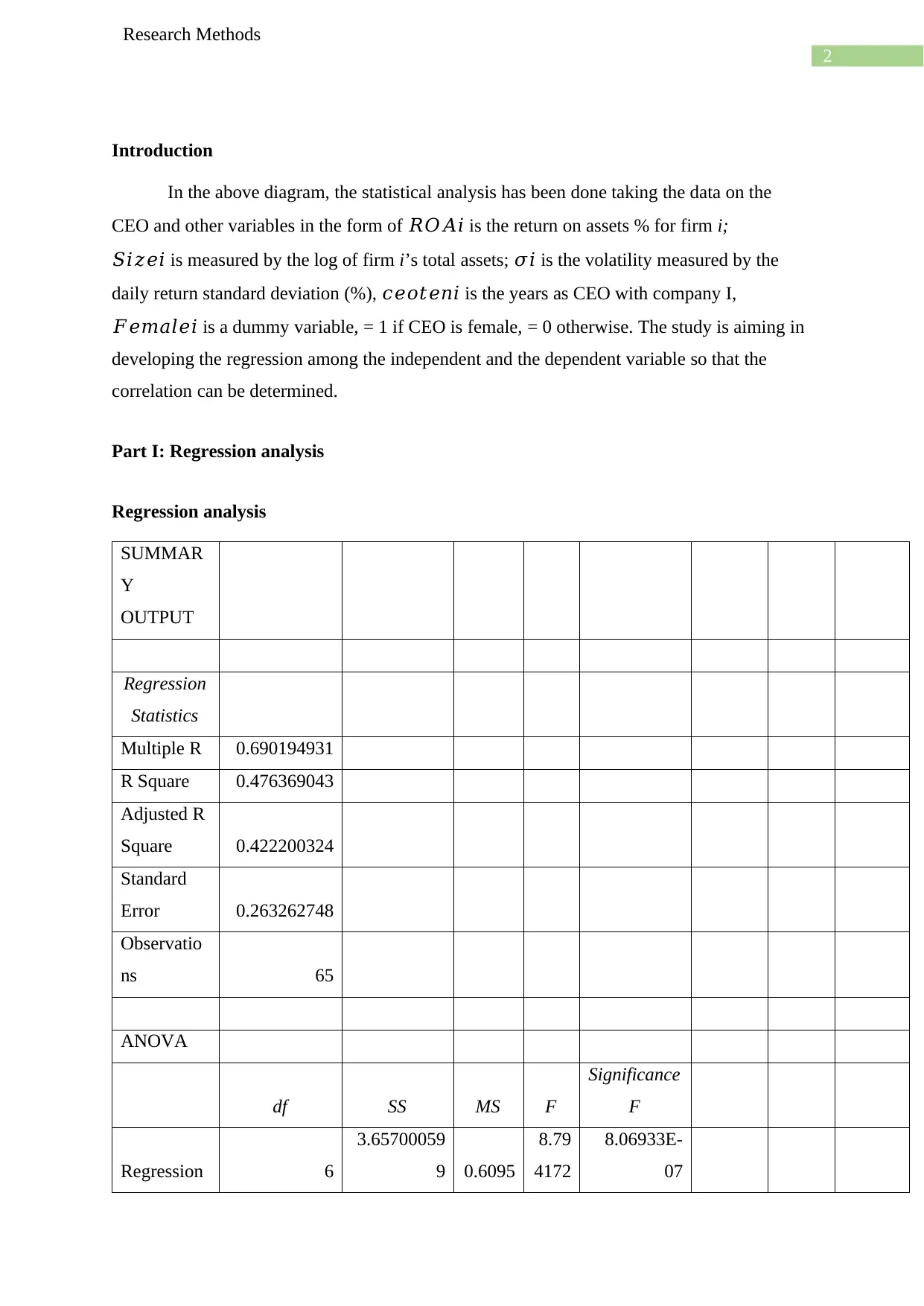

Introduction

In the above diagram, the statistical analysis has been done taking the data on the

CEO and other variables in the form of 𝑅𝑂𝐴𝑖 is the return on assets % for firm i;

𝑆𝑖𝑧𝑒𝑖 is measured by the log of firm i’s total assets; 𝜎𝑖 is the volatility measured by the

daily return standard deviation (%), 𝑐𝑒𝑜𝑡𝑒𝑛𝑖 is the years as CEO with company I,

𝐹𝑒𝑚𝑎𝑙𝑒𝑖 is a dummy variable, = 1 if CEO is female, = 0 otherwise. The study is aiming in

developing the regression among the independent and the dependent variable so that the

correlation can be determined.

Part I: Regression analysis

Regression analysis

SUMMAR

Y

OUTPUT

Regression

Statistics

Multiple R 0.690194931

R Square 0.476369043

Adjusted R

Square 0.422200324

Standard

Error 0.263262748

Observatio

ns 65

ANOVA

df SS MS F

Significance

F

Regression 6

3.65700059

9 0.6095

8.79

4172

8.06933E-

07

Research Methods

Introduction

In the above diagram, the statistical analysis has been done taking the data on the

CEO and other variables in the form of 𝑅𝑂𝐴𝑖 is the return on assets % for firm i;

𝑆𝑖𝑧𝑒𝑖 is measured by the log of firm i’s total assets; 𝜎𝑖 is the volatility measured by the

daily return standard deviation (%), 𝑐𝑒𝑜𝑡𝑒𝑛𝑖 is the years as CEO with company I,

𝐹𝑒𝑚𝑎𝑙𝑒𝑖 is a dummy variable, = 1 if CEO is female, = 0 otherwise. The study is aiming in

developing the regression among the independent and the dependent variable so that the

correlation can be determined.

Part I: Regression analysis

Regression analysis

SUMMAR

Y

OUTPUT

Regression

Statistics

Multiple R 0.690194931

R Square 0.476369043

Adjusted R

Square 0.422200324

Standard

Error 0.263262748

Observatio

ns 65

ANOVA

df SS MS F

Significance

F

Regression 6

3.65700059

9 0.6095

8.79

4172

8.06933E-

07

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Research Methods

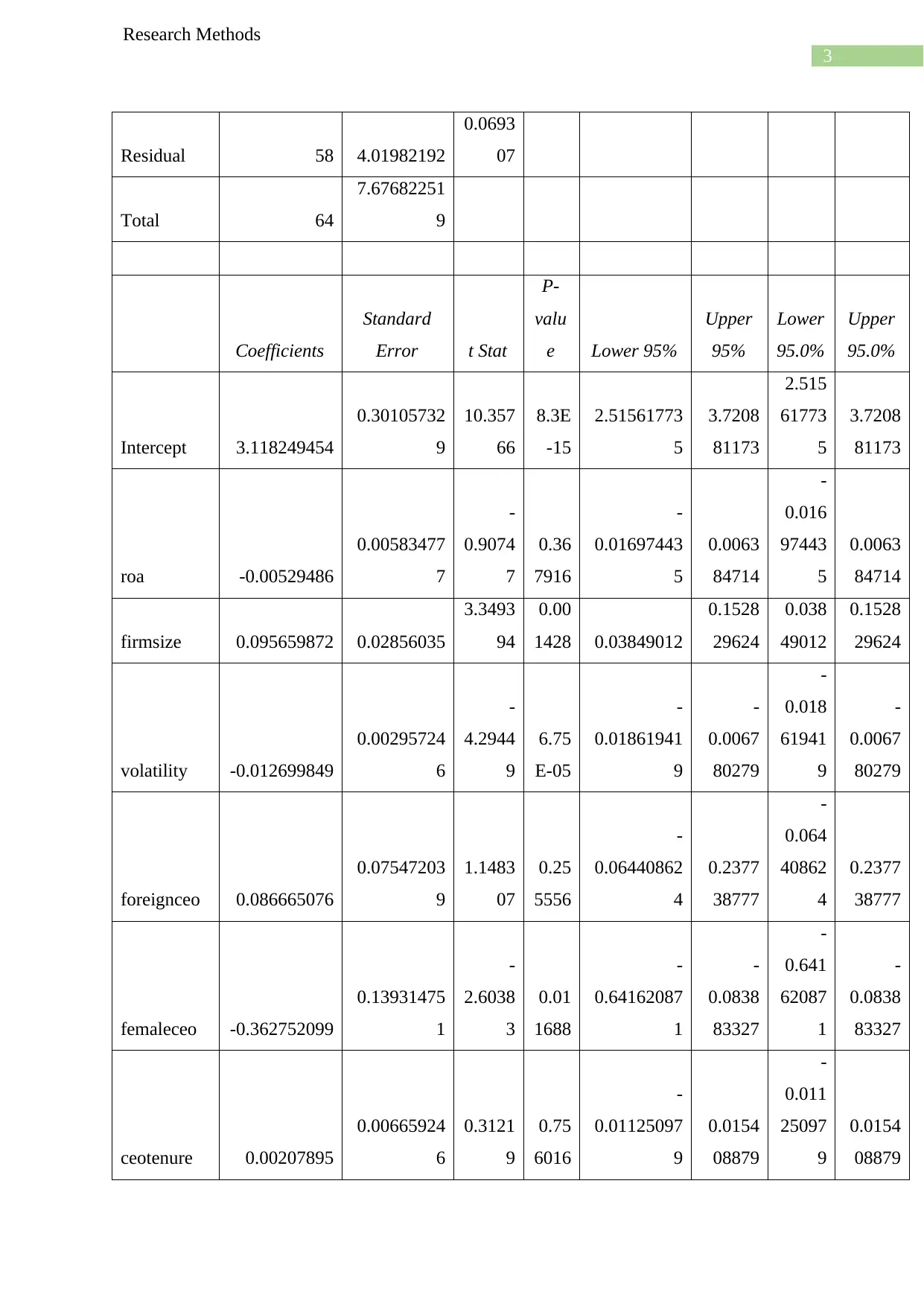

Residual 58 4.01982192

0.0693

07

Total 64

7.67682251

9

Coefficients

Standard

Error t Stat

P-

valu

e Lower 95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept 3.118249454

0.30105732

9

10.357

66

8.3E

-15

2.51561773

5

3.7208

81173

2.515

61773

5

3.7208

81173

roa -0.00529486

0.00583477

7

-

0.9074

7

0.36

7916

-

0.01697443

5

0.0063

84714

-

0.016

97443

5

0.0063

84714

firmsize 0.095659872 0.02856035

3.3493

94

0.00

1428 0.03849012

0.1528

29624

0.038

49012

0.1528

29624

volatility -0.012699849

0.00295724

6

-

4.2944

9

6.75

E-05

-

0.01861941

9

-

0.0067

80279

-

0.018

61941

9

-

0.0067

80279

foreignceo 0.086665076

0.07547203

9

1.1483

07

0.25

5556

-

0.06440862

4

0.2377

38777

-

0.064

40862

4

0.2377

38777

femaleceo -0.362752099

0.13931475

1

-

2.6038

3

0.01

1688

-

0.64162087

1

-

0.0838

83327

-

0.641

62087

1

-

0.0838

83327

ceotenure 0.00207895

0.00665924

6

0.3121

9

0.75

6016

-

0.01125097

9

0.0154

08879

-

0.011

25097

9

0.0154

08879

Research Methods

Residual 58 4.01982192

0.0693

07

Total 64

7.67682251

9

Coefficients

Standard

Error t Stat

P-

valu

e Lower 95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept 3.118249454

0.30105732

9

10.357

66

8.3E

-15

2.51561773

5

3.7208

81173

2.515

61773

5

3.7208

81173

roa -0.00529486

0.00583477

7

-

0.9074

7

0.36

7916

-

0.01697443

5

0.0063

84714

-

0.016

97443

5

0.0063

84714

firmsize 0.095659872 0.02856035

3.3493

94

0.00

1428 0.03849012

0.1528

29624

0.038

49012

0.1528

29624

volatility -0.012699849

0.00295724

6

-

4.2944

9

6.75

E-05

-

0.01861941

9

-

0.0067

80279

-

0.018

61941

9

-

0.0067

80279

foreignceo 0.086665076

0.07547203

9

1.1483

07

0.25

5556

-

0.06440862

4

0.2377

38777

-

0.064

40862

4

0.2377

38777

femaleceo -0.362752099

0.13931475

1

-

2.6038

3

0.01

1688

-

0.64162087

1

-

0.0838

83327

-

0.641

62087

1

-

0.0838

83327

ceotenure 0.00207895

0.00665924

6

0.3121

9

0.75

6016

-

0.01125097

9

0.0154

08879

-

0.011

25097

9

0.0154

08879

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

Research Methods

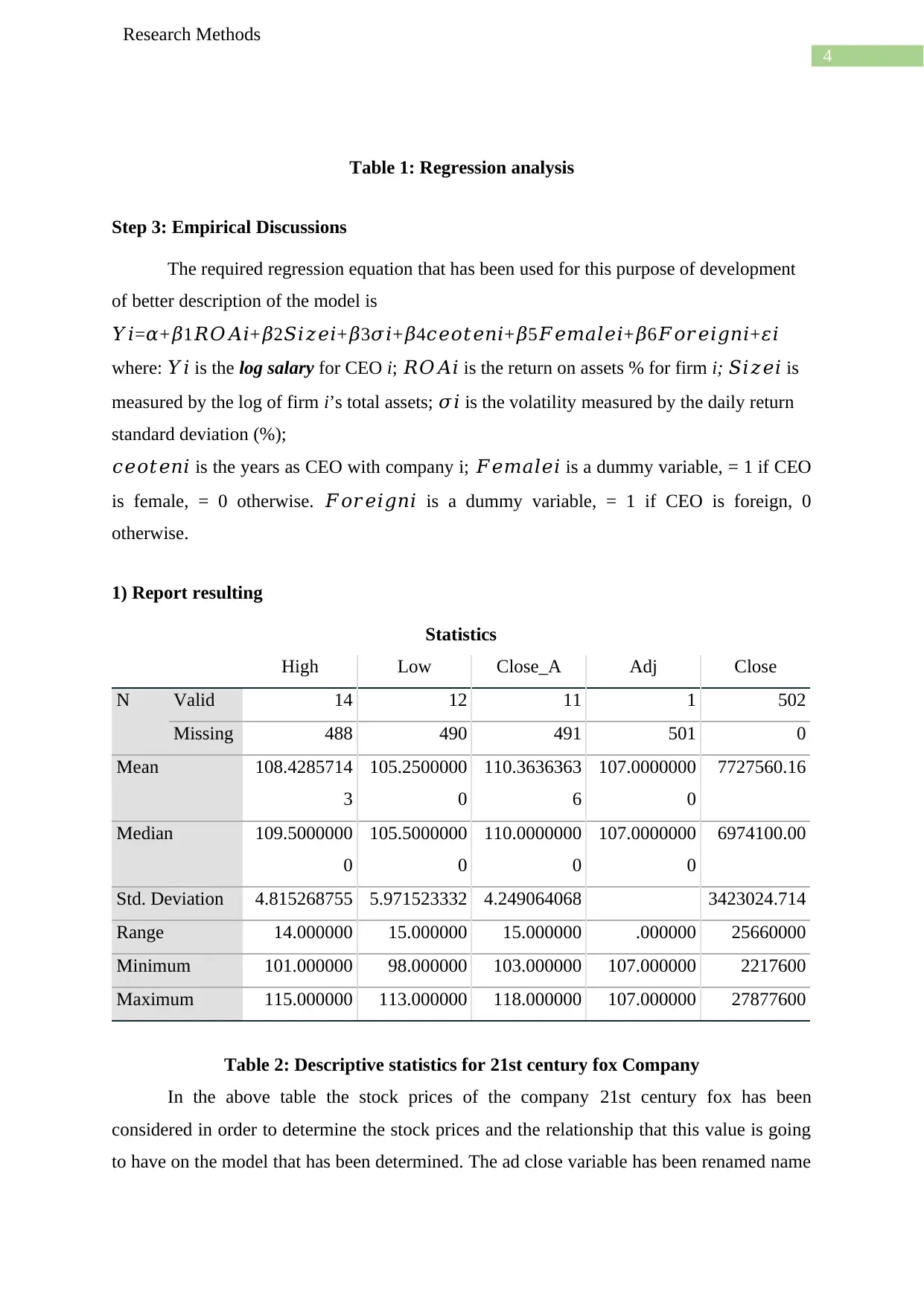

Table 1: Regression analysis

Step 3: Empirical Discussions

The required regression equation that has been used for this purpose of development

of better description of the model is

𝑌𝑖=𝛼+𝛽1𝑅𝑂𝐴𝑖+𝛽2𝑆𝑖𝑧𝑒𝑖+𝛽3𝜎𝑖+𝛽4𝑐𝑒𝑜𝑡𝑒𝑛𝑖+𝛽5𝐹𝑒𝑚𝑎𝑙𝑒𝑖+𝛽6𝐹𝑜𝑟𝑒𝑖𝑔𝑛𝑖+𝜀𝑖

where: 𝑌𝑖 is the log salary for CEO i; 𝑅𝑂𝐴𝑖 is the return on assets % for firm i; 𝑆𝑖𝑧𝑒𝑖 is

measured by the log of firm i’s total assets; 𝜎𝑖 is the volatility measured by the daily return

standard deviation (%);

𝑐𝑒𝑜𝑡𝑒𝑛𝑖 is the years as CEO with company i; 𝐹𝑒𝑚𝑎𝑙𝑒𝑖 is a dummy variable, = 1 if CEO

is female, = 0 otherwise. 𝐹𝑜𝑟𝑒𝑖𝑔𝑛𝑖 is a dummy variable, = 1 if CEO is foreign, 0

otherwise.

1) Report resulting

Statistics

High Low Close_A Adj Close

N Valid 14 12 11 1 502

Missing 488 490 491 501 0

Mean 108.4285714

3

105.2500000

0

110.3636363

6

107.0000000

0

7727560.16

Median 109.5000000

0

105.5000000

0

110.0000000

0

107.0000000

0

6974100.00

Std. Deviation 4.815268755 5.971523332 4.249064068 3423024.714

Range 14.000000 15.000000 15.000000 .000000 25660000

Minimum 101.000000 98.000000 103.000000 107.000000 2217600

Maximum 115.000000 113.000000 118.000000 107.000000 27877600

Table 2: Descriptive statistics for 21st century fox Company

In the above table the stock prices of the company 21st century fox has been

considered in order to determine the stock prices and the relationship that this value is going

to have on the model that has been determined. The ad close variable has been renamed name

Research Methods

Table 1: Regression analysis

Step 3: Empirical Discussions

The required regression equation that has been used for this purpose of development

of better description of the model is

𝑌𝑖=𝛼+𝛽1𝑅𝑂𝐴𝑖+𝛽2𝑆𝑖𝑧𝑒𝑖+𝛽3𝜎𝑖+𝛽4𝑐𝑒𝑜𝑡𝑒𝑛𝑖+𝛽5𝐹𝑒𝑚𝑎𝑙𝑒𝑖+𝛽6𝐹𝑜𝑟𝑒𝑖𝑔𝑛𝑖+𝜀𝑖

where: 𝑌𝑖 is the log salary for CEO i; 𝑅𝑂𝐴𝑖 is the return on assets % for firm i; 𝑆𝑖𝑧𝑒𝑖 is

measured by the log of firm i’s total assets; 𝜎𝑖 is the volatility measured by the daily return

standard deviation (%);

𝑐𝑒𝑜𝑡𝑒𝑛𝑖 is the years as CEO with company i; 𝐹𝑒𝑚𝑎𝑙𝑒𝑖 is a dummy variable, = 1 if CEO

is female, = 0 otherwise. 𝐹𝑜𝑟𝑒𝑖𝑔𝑛𝑖 is a dummy variable, = 1 if CEO is foreign, 0

otherwise.

1) Report resulting

Statistics

High Low Close_A Adj Close

N Valid 14 12 11 1 502

Missing 488 490 491 501 0

Mean 108.4285714

3

105.2500000

0

110.3636363

6

107.0000000

0

7727560.16

Median 109.5000000

0

105.5000000

0

110.0000000

0

107.0000000

0

6974100.00

Std. Deviation 4.815268755 5.971523332 4.249064068 3423024.714

Range 14.000000 15.000000 15.000000 .000000 25660000

Minimum 101.000000 98.000000 103.000000 107.000000 2217600

Maximum 115.000000 113.000000 118.000000 107.000000 27877600

Table 2: Descriptive statistics for 21st century fox Company

In the above table the stock prices of the company 21st century fox has been

considered in order to determine the stock prices and the relationship that this value is going

to have on the model that has been determined. The ad close variable has been renamed name

5

Research Methods

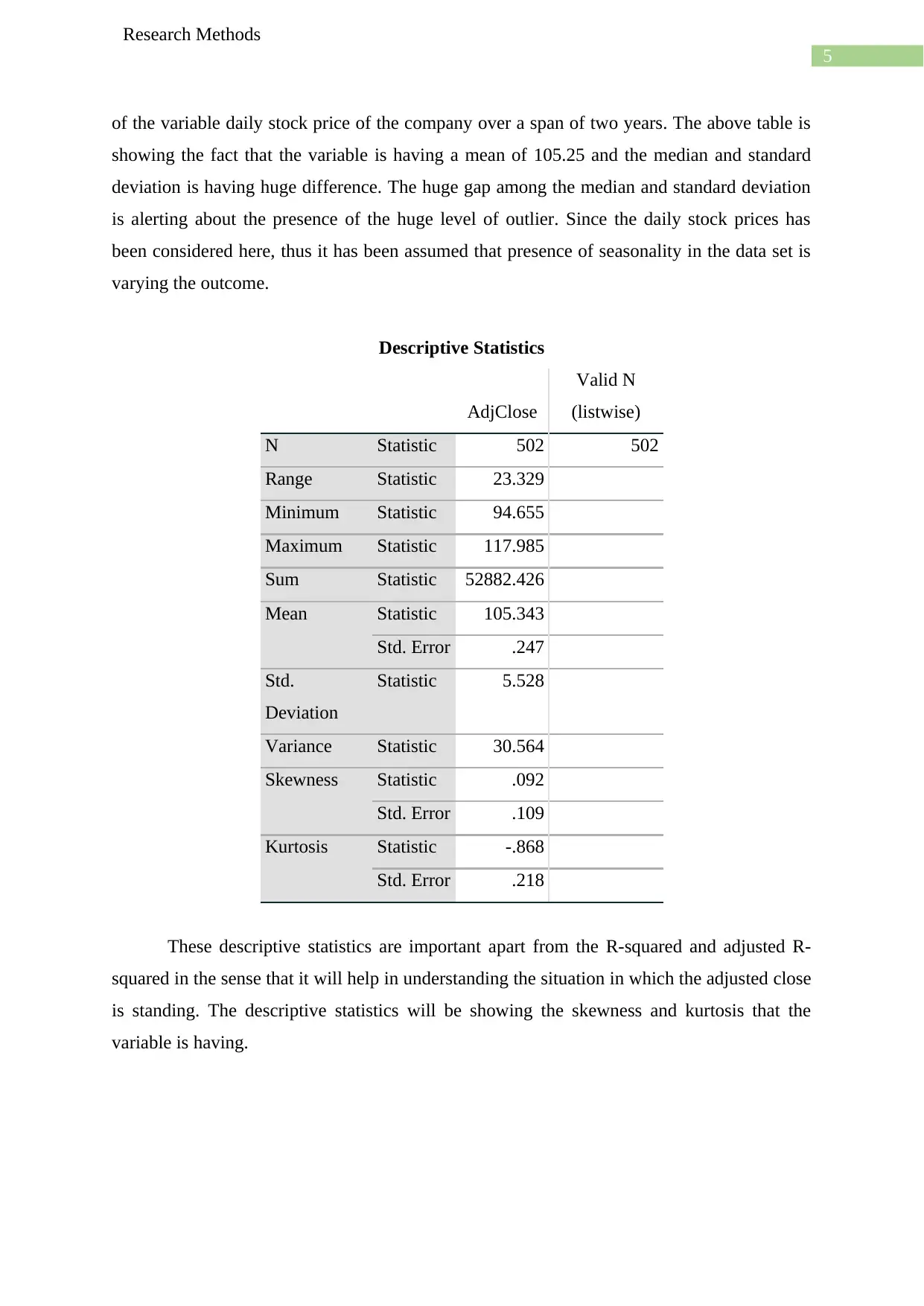

of the variable daily stock price of the company over a span of two years. The above table is

showing the fact that the variable is having a mean of 105.25 and the median and standard

deviation is having huge difference. The huge gap among the median and standard deviation

is alerting about the presence of the huge level of outlier. Since the daily stock prices has

been considered here, thus it has been assumed that presence of seasonality in the data set is

varying the outcome.

Descriptive Statistics

AdjClose

Valid N

(listwise)

N Statistic 502 502

Range Statistic 23.329

Minimum Statistic 94.655

Maximum Statistic 117.985

Sum Statistic 52882.426

Mean Statistic 105.343

Std. Error .247

Std.

Deviation

Statistic 5.528

Variance Statistic 30.564

Skewness Statistic .092

Std. Error .109

Kurtosis Statistic -.868

Std. Error .218

These descriptive statistics are important apart from the R-squared and adjusted R-

squared in the sense that it will help in understanding the situation in which the adjusted close

is standing. The descriptive statistics will be showing the skewness and kurtosis that the

variable is having.

Research Methods

of the variable daily stock price of the company over a span of two years. The above table is

showing the fact that the variable is having a mean of 105.25 and the median and standard

deviation is having huge difference. The huge gap among the median and standard deviation

is alerting about the presence of the huge level of outlier. Since the daily stock prices has

been considered here, thus it has been assumed that presence of seasonality in the data set is

varying the outcome.

Descriptive Statistics

AdjClose

Valid N

(listwise)

N Statistic 502 502

Range Statistic 23.329

Minimum Statistic 94.655

Maximum Statistic 117.985

Sum Statistic 52882.426

Mean Statistic 105.343

Std. Error .247

Std.

Deviation

Statistic 5.528

Variance Statistic 30.564

Skewness Statistic .092

Std. Error .109

Kurtosis Statistic -.868

Std. Error .218

These descriptive statistics are important apart from the R-squared and adjusted R-

squared in the sense that it will help in understanding the situation in which the adjusted close

is standing. The descriptive statistics will be showing the skewness and kurtosis that the

variable is having.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

Research Methods

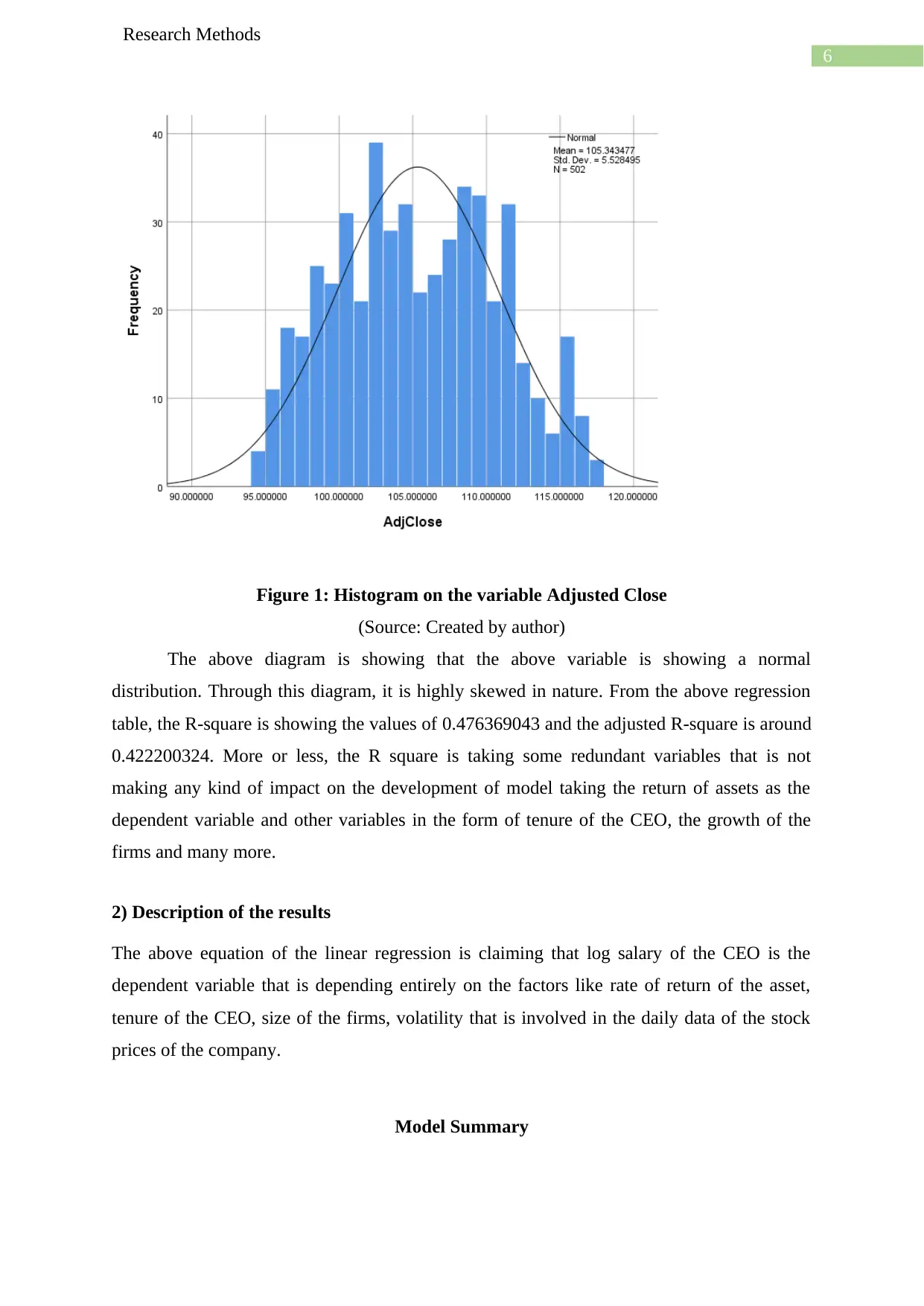

Figure 1: Histogram on the variable Adjusted Close

(Source: Created by author)

The above diagram is showing that the above variable is showing a normal

distribution. Through this diagram, it is highly skewed in nature. From the above regression

table, the R-square is showing the values of 0.476369043 and the adjusted R-square is around

0.422200324. More or less, the R square is taking some redundant variables that is not

making any kind of impact on the development of model taking the return of assets as the

dependent variable and other variables in the form of tenure of the CEO, the growth of the

firms and many more.

2) Description of the results

The above equation of the linear regression is claiming that log salary of the CEO is the

dependent variable that is depending entirely on the factors like rate of return of the asset,

tenure of the CEO, size of the firms, volatility that is involved in the daily data of the stock

prices of the company.

Model Summary

Research Methods

Figure 1: Histogram on the variable Adjusted Close

(Source: Created by author)

The above diagram is showing that the above variable is showing a normal

distribution. Through this diagram, it is highly skewed in nature. From the above regression

table, the R-square is showing the values of 0.476369043 and the adjusted R-square is around

0.422200324. More or less, the R square is taking some redundant variables that is not

making any kind of impact on the development of model taking the return of assets as the

dependent variable and other variables in the form of tenure of the CEO, the growth of the

firms and many more.

2) Description of the results

The above equation of the linear regression is claiming that log salary of the CEO is the

dependent variable that is depending entirely on the factors like rate of return of the asset,

tenure of the CEO, size of the firms, volatility that is involved in the daily data of the stock

prices of the company.

Model Summary

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

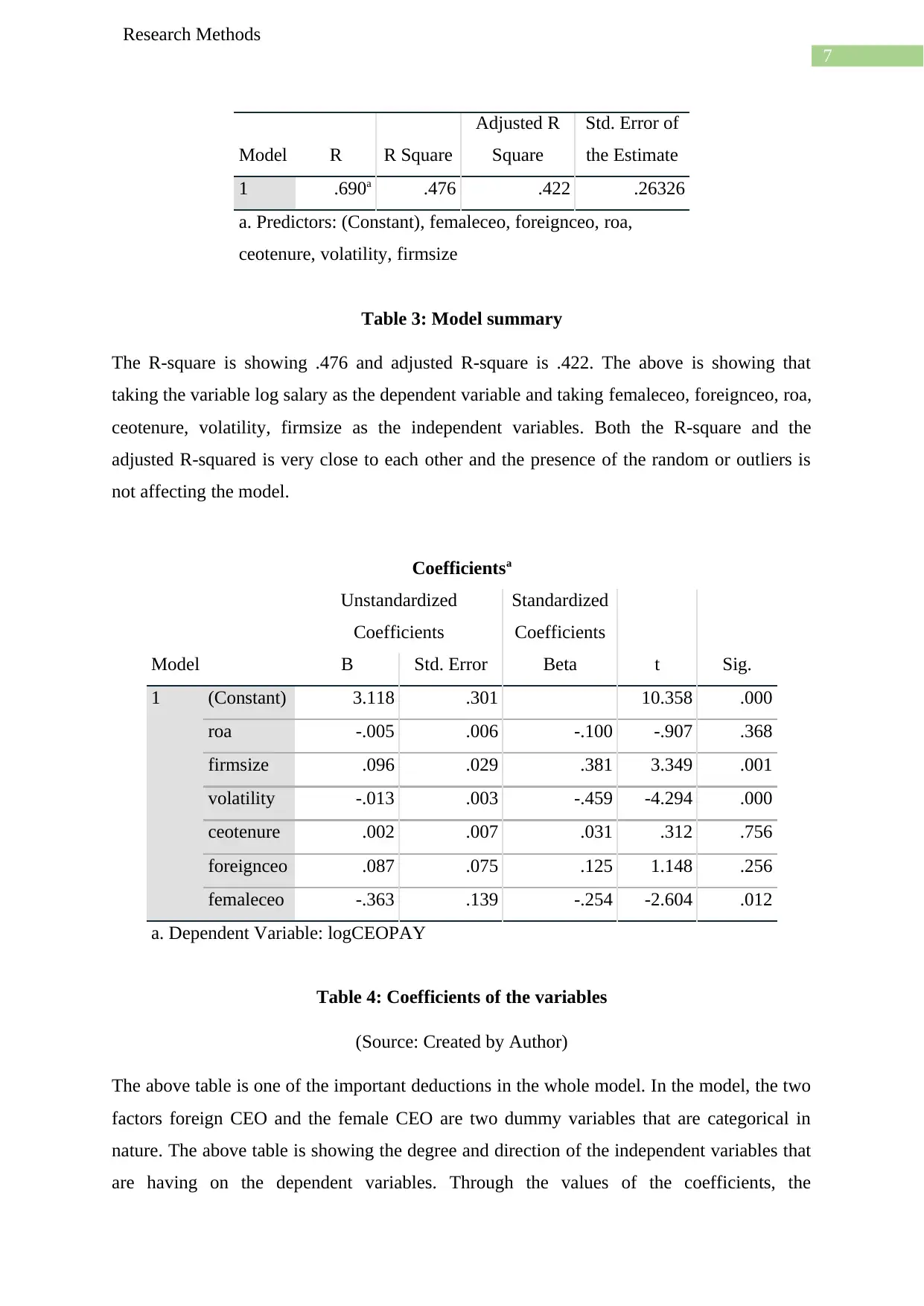

Research Methods

Model R R Square

Adjusted R

Square

Std. Error of

the Estimate

1 .690a .476 .422 .26326

a. Predictors: (Constant), femaleceo, foreignceo, roa,

ceotenure, volatility, firmsize

Table 3: Model summary

The R-square is showing .476 and adjusted R-square is .422. The above is showing that

taking the variable log salary as the dependent variable and taking femaleceo, foreignceo, roa,

ceotenure, volatility, firmsize as the independent variables. Both the R-square and the

adjusted R-squared is very close to each other and the presence of the random or outliers is

not affecting the model.

Coefficientsa

Model

Unstandardized

Coefficients

Standardized

Coefficients

t Sig.B Std. Error Beta

1 (Constant) 3.118 .301 10.358 .000

roa -.005 .006 -.100 -.907 .368

firmsize .096 .029 .381 3.349 .001

volatility -.013 .003 -.459 -4.294 .000

ceotenure .002 .007 .031 .312 .756

foreignceo .087 .075 .125 1.148 .256

femaleceo -.363 .139 -.254 -2.604 .012

a. Dependent Variable: logCEOPAY

Table 4: Coefficients of the variables

(Source: Created by Author)

The above table is one of the important deductions in the whole model. In the model, the two

factors foreign CEO and the female CEO are two dummy variables that are categorical in

nature. The above table is showing the degree and direction of the independent variables that

are having on the dependent variables. Through the values of the coefficients, the

Research Methods

Model R R Square

Adjusted R

Square

Std. Error of

the Estimate

1 .690a .476 .422 .26326

a. Predictors: (Constant), femaleceo, foreignceo, roa,

ceotenure, volatility, firmsize

Table 3: Model summary

The R-square is showing .476 and adjusted R-square is .422. The above is showing that

taking the variable log salary as the dependent variable and taking femaleceo, foreignceo, roa,

ceotenure, volatility, firmsize as the independent variables. Both the R-square and the

adjusted R-squared is very close to each other and the presence of the random or outliers is

not affecting the model.

Coefficientsa

Model

Unstandardized

Coefficients

Standardized

Coefficients

t Sig.B Std. Error Beta

1 (Constant) 3.118 .301 10.358 .000

roa -.005 .006 -.100 -.907 .368

firmsize .096 .029 .381 3.349 .001

volatility -.013 .003 -.459 -4.294 .000

ceotenure .002 .007 .031 .312 .756

foreignceo .087 .075 .125 1.148 .256

femaleceo -.363 .139 -.254 -2.604 .012

a. Dependent Variable: logCEOPAY

Table 4: Coefficients of the variables

(Source: Created by Author)

The above table is one of the important deductions in the whole model. In the model, the two

factors foreign CEO and the female CEO are two dummy variables that are categorical in

nature. The above table is showing the degree and direction of the independent variables that

are having on the dependent variables. Through the values of the coefficients, the

8

Research Methods

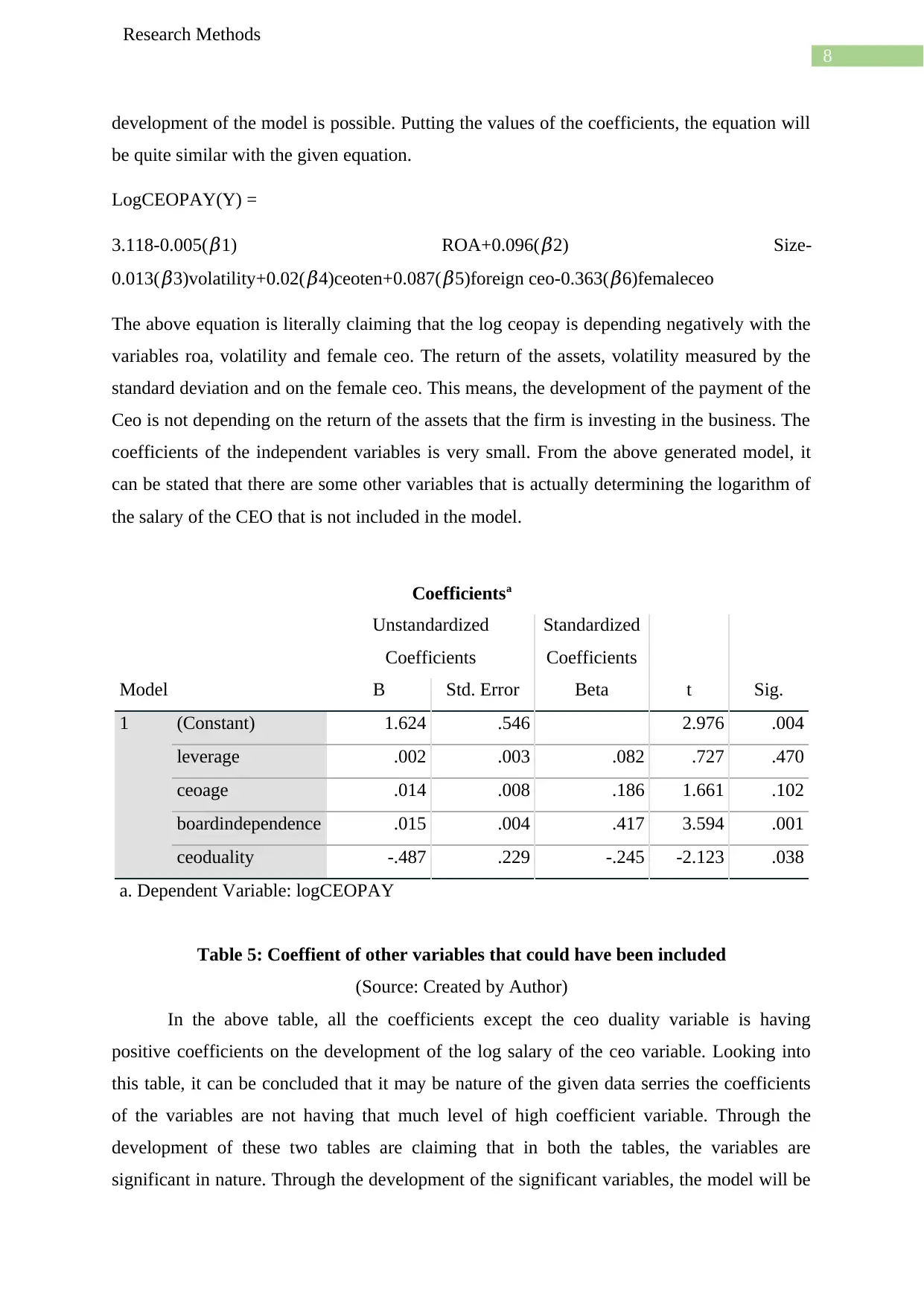

development of the model is possible. Putting the values of the coefficients, the equation will

be quite similar with the given equation.

LogCEOPAY(Y) =

3.118-0.005(𝛽1) ROA+0.096(𝛽2) Size-

0.013(𝛽3)volatility+0.02(𝛽4)ceoten+0.087(𝛽5)foreign ceo-0.363(𝛽6)femaleceo

The above equation is literally claiming that the log ceopay is depending negatively with the

variables roa, volatility and female ceo. The return of the assets, volatility measured by the

standard deviation and on the female ceo. This means, the development of the payment of the

Ceo is not depending on the return of the assets that the firm is investing in the business. The

coefficients of the independent variables is very small. From the above generated model, it

can be stated that there are some other variables that is actually determining the logarithm of

the salary of the CEO that is not included in the model.

Coefficientsa

Model

Unstandardized

Coefficients

Standardized

Coefficients

t Sig.B Std. Error Beta

1 (Constant) 1.624 .546 2.976 .004

leverage .002 .003 .082 .727 .470

ceoage .014 .008 .186 1.661 .102

boardindependence .015 .004 .417 3.594 .001

ceoduality -.487 .229 -.245 -2.123 .038

a. Dependent Variable: logCEOPAY

Table 5: Coeffient of other variables that could have been included

(Source: Created by Author)

In the above table, all the coefficients except the ceo duality variable is having

positive coefficients on the development of the log salary of the ceo variable. Looking into

this table, it can be concluded that it may be nature of the given data serries the coefficients

of the variables are not having that much level of high coefficient variable. Through the

development of these two tables are claiming that in both the tables, the variables are

significant in nature. Through the development of the significant variables, the model will be

Research Methods

development of the model is possible. Putting the values of the coefficients, the equation will

be quite similar with the given equation.

LogCEOPAY(Y) =

3.118-0.005(𝛽1) ROA+0.096(𝛽2) Size-

0.013(𝛽3)volatility+0.02(𝛽4)ceoten+0.087(𝛽5)foreign ceo-0.363(𝛽6)femaleceo

The above equation is literally claiming that the log ceopay is depending negatively with the

variables roa, volatility and female ceo. The return of the assets, volatility measured by the

standard deviation and on the female ceo. This means, the development of the payment of the

Ceo is not depending on the return of the assets that the firm is investing in the business. The

coefficients of the independent variables is very small. From the above generated model, it

can be stated that there are some other variables that is actually determining the logarithm of

the salary of the CEO that is not included in the model.

Coefficientsa

Model

Unstandardized

Coefficients

Standardized

Coefficients

t Sig.B Std. Error Beta

1 (Constant) 1.624 .546 2.976 .004

leverage .002 .003 .082 .727 .470

ceoage .014 .008 .186 1.661 .102

boardindependence .015 .004 .417 3.594 .001

ceoduality -.487 .229 -.245 -2.123 .038

a. Dependent Variable: logCEOPAY

Table 5: Coeffient of other variables that could have been included

(Source: Created by Author)

In the above table, all the coefficients except the ceo duality variable is having

positive coefficients on the development of the log salary of the ceo variable. Looking into

this table, it can be concluded that it may be nature of the given data serries the coefficients

of the variables are not having that much level of high coefficient variable. Through the

development of these two tables are claiming that in both the tables, the variables are

significant in nature. Through the development of the significant variables, the model will be

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

Research Methods

able to ignite the development of the business that will help in prediction of the variables.

Through the development of better benefits that the most of the companies will be able to

predict the future consequences that will not only improve the development of the model.

The model though is not depicting the dependence among the variables, as the R-squared

values and the adjusted R-squared values is not going past 0.5-1. The value of both R-squared

and adjusted R-squared are well below the standard measure of the correlation coefficient. On

the other hand, the development of these two variables are not helping in the development of

the better and effective modelling. Through the development of the resource utilisation, it is

possible for the development of an unbiased model that will not only increase the

development of the model and will be helping in the effective predictions.

In most of the regression, it is assumed that all the variables will be highly significant in

nature and the variables will be giving highly

Research Methods

able to ignite the development of the business that will help in prediction of the variables.

Through the development of better benefits that the most of the companies will be able to

predict the future consequences that will not only improve the development of the model.

The model though is not depicting the dependence among the variables, as the R-squared

values and the adjusted R-squared values is not going past 0.5-1. The value of both R-squared

and adjusted R-squared are well below the standard measure of the correlation coefficient. On

the other hand, the development of these two variables are not helping in the development of

the better and effective modelling. Through the development of the resource utilisation, it is

possible for the development of an unbiased model that will not only increase the

development of the model and will be helping in the effective predictions.

In most of the regression, it is assumed that all the variables will be highly significant in

nature and the variables will be giving highly

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

Research Methods

Correlations

logCEOPA

Y roa firmsize volatility foreignceo femaleceo

logCEOPA

Y

Pearson Correlation 1 -.057 .493** -.396** .310* -.249*

Sig. (2-tailed) .651 .000 .001 .012 .045

N 65 65 65 65 65 65

roa Pearson Correlation -.057 1 -.300* -.364** .069 .070

Sig. (2-tailed) .651 .015 .003 .587 .580

N 65 65 65 65 65 65

firmsize Pearson Correlation .493** -.300* 1 -.003 .412** -.112

Sig. (2-tailed) .000 .015 .980 .001 .374

N 65 65 65 65 65 65

volatility Pearson Correlation -.396** -.364** -.003 1 -.082 -.120

Sig. (2-tailed) .001 .003 .980 .518 .343

N 65 65 65 65 65 65

foreignceo Pearson Correlation .310* .069 .412** -.082 1 .028

Sig. (2-tailed) .012 .587 .001 .518 .826

N 65 65 65 65 65 65

femaleceo Pearson Correlation -.249* .070 -.112 -.120 .028 1

Sig. (2-tailed) .045 .580 .374 .343 .826

N 65 65 65 65 65 65

**. Correlation is significant at the 0.01 level (2-tailed).

*. Correlation is significant at the 0.05 level (2-tailed).

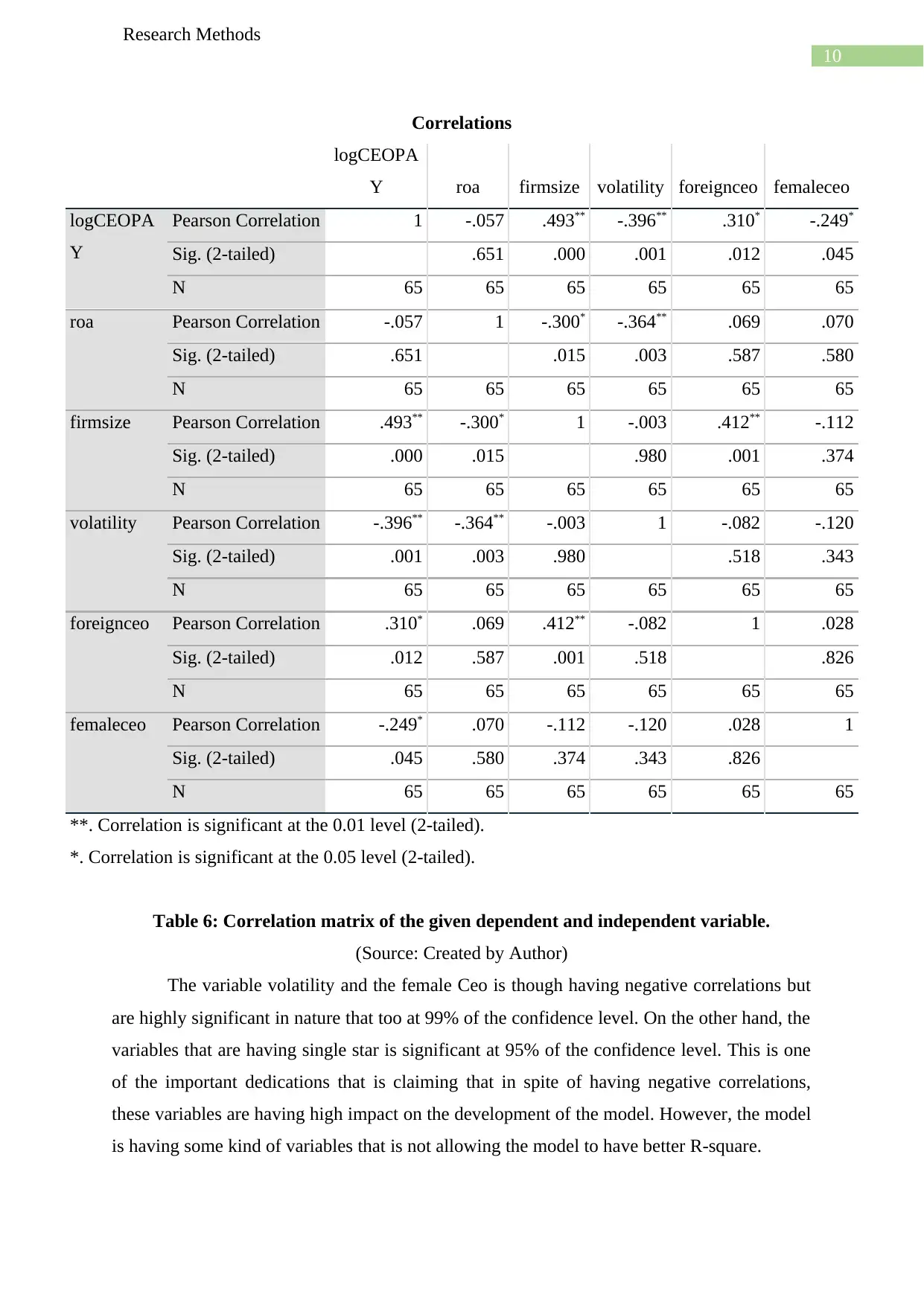

Table 6: Correlation matrix of the given dependent and independent variable.

(Source: Created by Author)

The variable volatility and the female Ceo is though having negative correlations but

are highly significant in nature that too at 99% of the confidence level. On the other hand, the

variables that are having single star is significant at 95% of the confidence level. This is one

of the important dedications that is claiming that in spite of having negative correlations,

these variables are having high impact on the development of the model. However, the model

is having some kind of variables that is not allowing the model to have better R-square.

Research Methods

Correlations

logCEOPA

Y roa firmsize volatility foreignceo femaleceo

logCEOPA

Y

Pearson Correlation 1 -.057 .493** -.396** .310* -.249*

Sig. (2-tailed) .651 .000 .001 .012 .045

N 65 65 65 65 65 65

roa Pearson Correlation -.057 1 -.300* -.364** .069 .070

Sig. (2-tailed) .651 .015 .003 .587 .580

N 65 65 65 65 65 65

firmsize Pearson Correlation .493** -.300* 1 -.003 .412** -.112

Sig. (2-tailed) .000 .015 .980 .001 .374

N 65 65 65 65 65 65

volatility Pearson Correlation -.396** -.364** -.003 1 -.082 -.120

Sig. (2-tailed) .001 .003 .980 .518 .343

N 65 65 65 65 65 65

foreignceo Pearson Correlation .310* .069 .412** -.082 1 .028

Sig. (2-tailed) .012 .587 .001 .518 .826

N 65 65 65 65 65 65

femaleceo Pearson Correlation -.249* .070 -.112 -.120 .028 1

Sig. (2-tailed) .045 .580 .374 .343 .826

N 65 65 65 65 65 65

**. Correlation is significant at the 0.01 level (2-tailed).

*. Correlation is significant at the 0.05 level (2-tailed).

Table 6: Correlation matrix of the given dependent and independent variable.

(Source: Created by Author)

The variable volatility and the female Ceo is though having negative correlations but

are highly significant in nature that too at 99% of the confidence level. On the other hand, the

variables that are having single star is significant at 95% of the confidence level. This is one

of the important dedications that is claiming that in spite of having negative correlations,

these variables are having high impact on the development of the model. However, the model

is having some kind of variables that is not allowing the model to have better R-square.

11

Research Methods

3. Discussion of findings relating with relevant literature

Carroll (2017) opined that in order to determine the development of the model, it is

important to consider the variable at first that are going to have significant impact on the

mode. It has been opined that making the regression model effective in nature will definitely

bring in effective innovations. Through the development of better regression model, it is

important to indulge better techniques of sample collection that will increase the probability

of having better R-squared and adjusted R-squared. Through the development of this

regression analysis, it will be possible for the statistical analysis to introduce better model

development.

According to Chatterjee and Hadi (2015), the development of the regression analysis

will take on the development of variables that will not only lie within the significant values

but will also increase the development of the authenticity of the model. The regression

analysis will not only induce the development of the eternal strength and will highlight the

dependence of the independent variables on the dependent variable. On the other hand, it is

important to integrate variables in the model having the identification that will increase the

model verification. Through the identification of the variables it is important to increase the

resource of the modelling of data.

As opined by Darlington and Hayes (2016), in order to find the regression analysis

and linear model is helpful for the development of correlation coefficient is important in the

sense that through the development of the correlation coefficient it is important for the

statisticians to indulge the development of the business by predicting the variable.

4. Optional Opportunity for Individual Initiative

In order to discuss about the CEO compensations, it is important to include some of

the important variables in the sense that through the development of better model, it is

important to introduce the benefits that the most of the CEO will be taking as part of the

individual initiative that will help in the development of the return through the development

of the business. In order to increase the model development of ceo salary, it is important to

undertake certain variables that will not only increase the development of the model but will

also indulge the development of ceo salary. Through the development of better innovation

technologies. Through the development of the model, it is important for the involvement of

Research Methods

3. Discussion of findings relating with relevant literature

Carroll (2017) opined that in order to determine the development of the model, it is

important to consider the variable at first that are going to have significant impact on the

mode. It has been opined that making the regression model effective in nature will definitely

bring in effective innovations. Through the development of better regression model, it is

important to indulge better techniques of sample collection that will increase the probability

of having better R-squared and adjusted R-squared. Through the development of this

regression analysis, it will be possible for the statistical analysis to introduce better model

development.

According to Chatterjee and Hadi (2015), the development of the regression analysis

will take on the development of variables that will not only lie within the significant values

but will also increase the development of the authenticity of the model. The regression

analysis will not only induce the development of the eternal strength and will highlight the

dependence of the independent variables on the dependent variable. On the other hand, it is

important to integrate variables in the model having the identification that will increase the

model verification. Through the identification of the variables it is important to increase the

resource of the modelling of data.

As opined by Darlington and Hayes (2016), in order to find the regression analysis

and linear model is helpful for the development of correlation coefficient is important in the

sense that through the development of the correlation coefficient it is important for the

statisticians to indulge the development of the business by predicting the variable.

4. Optional Opportunity for Individual Initiative

In order to discuss about the CEO compensations, it is important to include some of

the important variables in the sense that through the development of better model, it is

important to introduce the benefits that the most of the CEO will be taking as part of the

individual initiative that will help in the development of the return through the development

of the business. In order to increase the model development of ceo salary, it is important to

undertake certain variables that will not only increase the development of the model but will

also indulge the development of ceo salary. Through the development of better innovation

technologies. Through the development of the model, it is important for the involvement of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.